FAQs on Purpose and Effect test for RPTs

-Team Vinod Kothari and Company | corplaw@vinodkothari.com

Loading…

Loading…

For further reading on the topic –

-Team Vinod Kothari and Company | corplaw@vinodkothari.com

Loading…

For further reading on the topic –

For understanding the intricacies, laying systems and implementing

| Register here: https://forms.gle/uX6cFio1UVjxCcsW8 |

Loading…

Read our related resources

– Vinita Nair, Senior Partner | vinita@vinodkothari.com

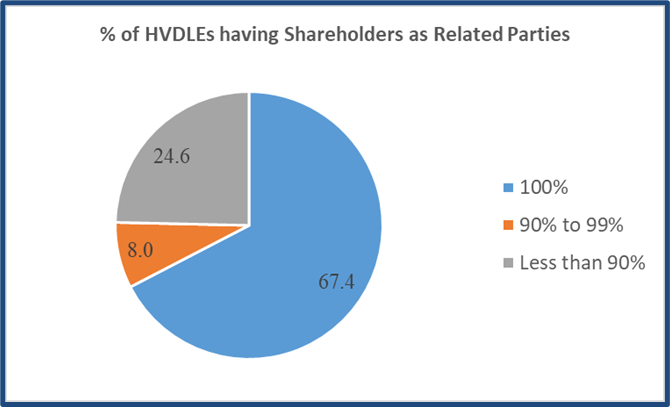

SEBI continues to tighten the regulatory regime for debt listed entities as it aims to promote corporate bond market. After equating debt listed entities with outstanding value of listed non-convertible debt securities of Rs. 500 crore and above with equity listed entities for the purpose of corporate governance norms, SEBI proposes a stricter approval regime for Related Party Transactions (‘RPTs’) under Reg. 23 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘LODR’) vide Consultation paper on review of Corporate Governance norms for a High Value Debt Listed Entity (‘HVDLE’)[1]. This has been rolled out just before the corporate governance provisions become applicable on a mandatory basis effective from April 1, 2023. The composition of 138 HVDLEs, in terms of shareholding pattern, as on March 31, 2022 was as under:

– Lovish Jain, Executive | lovish@vinodkothari.com

Some days ago, Mr. Vinod Kothari had commented on a LinkedIn post :

“Do we realise how many places does a lender (NBFC, Bank) register information about a loan? There are 4 credit information companies (such as CIBIL) where the credit data, including performance history, is uploaded. If the exposure is Rs 5 crores or above, in the aggregate over the banking system, information goes on CRILC too.

RBI has recently written to NBFCs reminding them of the obligation to register details with NeSL, an information utility under IBC, irrespective of whether the provisions of Code apply (for example in case of individuals), or whether the lender in question is at all contemplating resorting to IBC as a remedy (for example, consumer loans).

If the loan is a secured loan, the details need to be filed with CERSAI. If the secured loan borrower is a company, details need to be filed with RoC too. If the security interest is on immovable property, one needs to file particulars with land registry. If the security interest is on motor vehicles, the hypothecation is registered with Vahan portal too.

Read more →– Prapti Kanakia, Manager | prapti@vinodkothari.com

Loading…

ICAI and ICSI issue social audit standards

– Sharon Pinto & Kaushal Shah (corplaw@vinodkothari.com)

As we understand, the concept of Social Stock Exchanges (‘SSEs’) have been brought under the regulatory purview of Securities and Exchange Board of India (‘SEBI’) for listing and raising of capital by Social Enterprises, the details of which can be read in our article Social stock exchanges: philanthropy on the bourses as well as our other resources linked with the concept of SSEs and social sectors.

Social Enterprises are defined under regulation 292A (h) of the SEBI (ICDR) Regulations, 2018 (‘ICDR Regulations’) and are expected to be engaged in the specified activities provided therein. With the objective to assess the impact created by such social activities by the Social Enterprises, Self Regulatory Organisations (‘SRO’s) recognised under ICAI, ICSI and such other bodies as may be prescribed by SEBI have been considered to be eligible to act as platforms to register Social Auditors. ICAI has approved the formation of an SRO named ‘Institute of Social Auditors of India’ while ‘ICSI Institute of Social Auditors’ is the recognsied SRO under ICSI. Such auditors are also required to undergo a certification program conducted by National Institute of Securities Market (‘NISM’).

ICAI has recently sought interest for the initial empanelment of Social Auditors.[1] The eligibility criteria for empanelment as a Social Audit firm requires having a track record of minimum three years of conducting social impact assessment. Further, average annual grants or expenditure of social enterprise of the last 3 financial years should be atleast Rs. 50 lakhs and the firm should have suitable human resources in the field of social development having experience of usage of relevant methodology of social audit. The disqualifications includes any individual or any of the partner/director of an entity being convicted for an offence of moral turpitude or declared as an undischarged insolvent/bankrupt or has been debarred by SEBI.

To put it in simple terms, Social Auditors are required to conduct Social Audit of the activities carried on by Social Enterprises. To aid the Social Auditors in carrying out the Social Audit, both the SROs being ICAI and ICSI have rolled out the Social Audit Standards (‘SAS’) to assist and guide their empanelled auditors for the purpose of carrying out the audit in accordance with the SAS Framework. Looking at the imminence of SSEs to come into reality with SEBI granting in-principle approval to both BSE and NSE in December, 2022, SROs have rolled out SAS for the quick reference and guidance for their registered auditors.

In this write-up, we have covered the key takeaways from the SAS and its relevance, applicability as well as mapping with the global principles on social audit.

Read more →– Burhanuddin Kholiya | corplaw@vinodkothari.com

Loading…

Read our more detailed discussion on the said topic here

– Payal Agarwal, Assistant Manager (payal@vinodkothari.com)

2022 has been a relatively stable year when it comes to Companies Act, save changes in the forms and filing procedures with increasing online processes, there has been significant traction on the part of SEBI. While Structured Digital Database (SDD) remained the buzzword for the listed entities with the stock exchanges requiring them to submit quarterly compliance certificates, the stress for proper controls on insider trading remained the focal point. For social enterprises, a landmark development was the introduction of the concept of Social Stock Exchanges, which seems to be shortly getting into operational mode.

We have tried to briefly cover the major developments in corporate laws during the year 2022. You may also refer to our brief discussion of the same in this youtube video. For updates relevant to the financial sector including the overseas investment norms, refer 2022 in retrospect: Regulatory activity in the financial sector. You may also refer to our quick round-up of regulatory developments in IBC in the year 2022.

Read more →