MoF permits foreign individuals to buy/ sell listed equity

– Vinita Nair and Saloni Khant | corplaw@vinodkothari.com

With the backdrop of the outflow of billions of foreign funds and the RBI’s multipronged approach to draw foreign funds (Read our article: RBI attempts to woo fleeing foreign investors), RBI notified the FEM (Non-debt Instruments) (Third Amendment) Rules, 2026 effective from June 12, 2026. All foreign individuals who are persons resident outside India PROIs are now permitted to purchase and sell equity instruments[1] of a listed Indian company subject to an individual limit of 10% and aggregate limit of 24%. Corresponding amendments made in FEM (Mode of Payment and Reporting of Non-Debt Instruments) (Amendment) Regulations, 2026 effective from June 13, 2026, which provides the manner of mode of payment and remittance of sale proceeds etc.

Eligibility and permissible limits for investing in equity instruments of listed companies

- Who can invest?

- All individual PROI. Earlier it was limited to NRI and OCIs.

- What are the revised investment limits?

| Investment Limits | Erstwhile limits (only for NRI and OCI) as other PROI not permitted to invest | Revised limits for all individual PROI (including NRI and OCI) |

| Individually | 5% | 10% |

| Aggregate | 10% (Could be increased to 24% by passing a special resolution) | 24% (No need to pass a special resolution for increasing the limits ) |

- For private sector banks, the limits for NRIs are stricter and remain the same. This may be a gap or a deliberate move to remain aligned with the limit of investments beyond 5% requiring the approval of the RBI under the RBI (Commercial Banks – Acquisition and Holding of Shares or Voting Rights) Directions, 2025. The limits are on both repatriation and non-repatriation basis. For other sectors, investment on non-repatriation basis is permitted without any limits and treated akin to domestic investment.

- Individual limit – 5 percent of the total paid up capital

- Aggregate limit – 10 percent of the total paid up capital both

- NRI holdings shall be allowed up to 24 percent of the total paid up capital both on repatriation and non-repatriation basis subject to passing of a special resolution.

- Limit applicable to individuals registered as Cat II FPIs

- The individual limit stated above is a combined limit for investment made under different schedules.

- Consequence of breach of individual limit of 10%:

- Divestment required within 5 trading days of settlement of trade crossing threshold. In case of non divestment, investment is considered to be FDI.

- Investor to intimate investee company and depositories through AD Cat-1 Bank within 7 trading days of such settlement date.

- Sale beyond the prescribed period will be treated as contravention of NDI Rules.

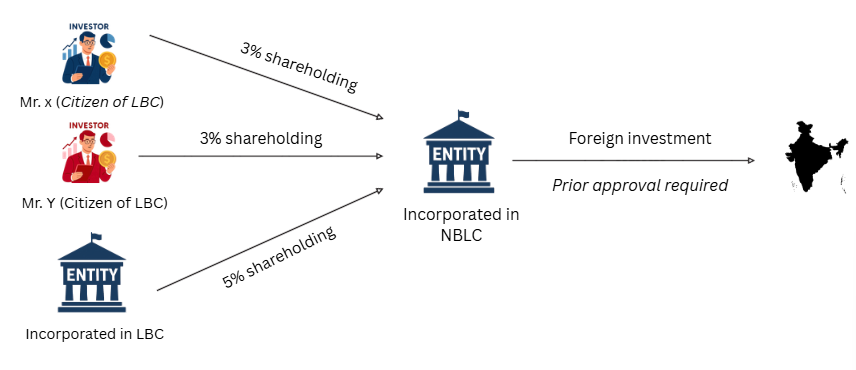

- When is government approval required?

- Acquisition of control of an Indian investee entity by a citizen/ entity of a country sharing land border with India (LBC investor).

- Control means the right to appoint the majority of the directors / control the management or policy decisions.

- Acquisition of ownership of an Indian investee entity by an LBC investor.

- Ownership means beneficial holding of more than 50% of the equity instrument of such company.

- Acquisition of beneficial ownership by a citizen of an LBC.

- Beneficial ownership primarily refers to more than 10% entitlement of shares/ capital/ profits of the investor company. (Rule 9(3)(b) of the PML (Maintenance of Records) Rules 2005.

- This is in alignment with the amendment in NDI Rules w.e.f. May 2, 2026. Read our article: Open but Guarded Gates: Relaxations for Border-Country Investments.

- Acquisition of control of an Indian investee entity by a citizen/ entity of a country sharing land border with India (LBC investor).

Transfer of Investments in Listed Equity/ Units

- Who can transfer to whom?

- All individual PROIs can transfer by sale/ gift to any PROI or may sell on stock exchange.

- When is government approval required?

- In case of sale or gift to another PROI, prior Government approval is required to be obtained for any transfer in case the company is engaged in a sector which requires Government approval.

- Same 3 scenarios as above, involving LBC investor.

Mode of payment for investment

- Consideration may be paid by inward remittance from abroad through banking channels or out of funds held in any repatriable deposit account maintained in accordance with the FEMA (Deposit) Regulations,2016 – for e.g. NRE, FCNR (B) or SNRR a/c.

- A repatriable rupee account maintained in accordance with the FEMA (Deposit) Regulations,2016, required to be designated by an individual PROI to be used exclusively for investments permitted under Schedule III.

Remittance of sale proceeds

- The sale proceeds (net of taxes) of equity instruments may be remitted outside India or may be credited to the designated rupee account of the person concerned.

Reporting requirements

- To be done by AD Category-1 Bank to RBI in Form LEC (Individual Foreign Investor – IFI) for purchase/ sale of listed equity instruments by individual PROIs including NRIs, OCIs. The designated link office of the AD bank shall furnish to RBI, a report on a daily basis, for their entire bank.

[1] Equity instruments comprises equity shares, convertible debentures, preference shares and share warrants issued by an Indian company [Rule 2(k) of FEM (NDI) Rules]

Refer to our other resources: