ECBs become Easy: RBI liberalises norms for external commercial borrowings

– Vinita Nair, Joint Managing Partner and Heta Mehta, Senior Executive | corplaw@vinodkothari.com

Updated as on 19th February, 2026

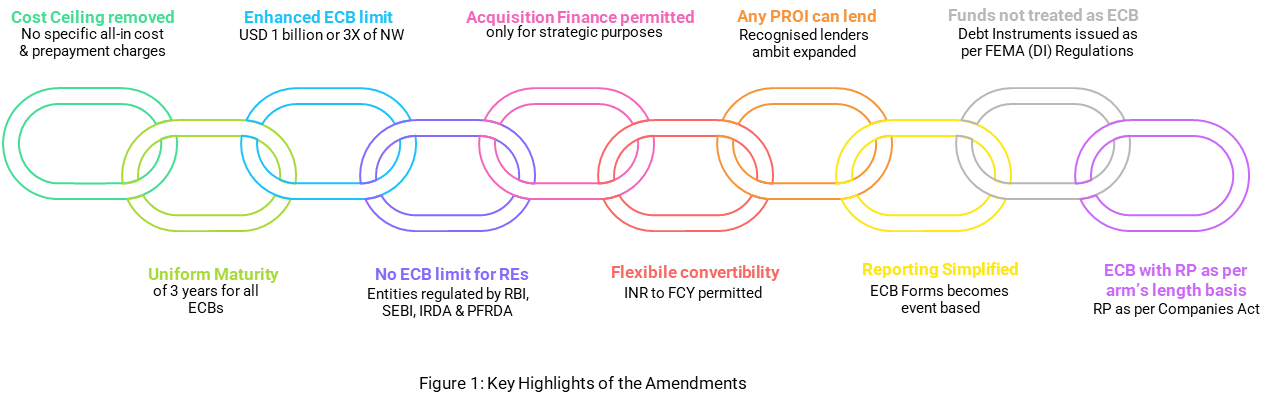

Permits acquisition finance, enhances limits to 3x of net worth, removes cost ceilings, all PROIs become eligible lenders and many more.

RBI significantly relaxed the framework for External Commercial Borrowings (ECBs) effective February 16, 2026, permitting entities to borrow from any person resident outside India (PROI), enhancing the ECB limit from USD 750 mn to higher of USD 1 bn / 300% of net worth, relaxing it for financial sector regulated entities, removing the absolute restrictions on all-in cost, penal interest on all ECBs etc. Necessary amendments have been notified in FEMA (Borrowing and Lending) Regulations, 2018 pursuant to which the RBI Master Directions on ECB also stands modified. ECB norms are now governed by Schedule 1 of these regulations. These measures are expected to further strengthen cross-border fundraising avenues for Indian corporates.

As per RBI data, ECB inflows rose sharply from approximately USD 8 billion in FY 2022–23 to USD 26.5 billion in FY 2023–24, and further to over USD 61 billion in FY 2024–25. In FY 2025–26, around USD 27.6 billion has been mobilised up to December, indicating continued access to offshore funds, though at a moderate pace compared to the previous year’s peak. The present amendment will provide further impetus to entities to avail ECBs.

Gist of amendment

No ceiling on all-in cost, prepayment charges: [Para 7 – Sch 1]

- No fixed ceiling, all costs, including prepayment charge/ penal interest, will be market driven.

- Cap for Trade Credits applicable to ECBs with an MAMP of less than 3 years:

- FCY-denominated ECB: Benchmark Rate + 3%

- INR-denominated ECB: Benchmark Rate + 2.5%

- For fixed rate loans: the ceiling is applicable for the floating rate + spread of the corresponding swap.

- Earlier ceiling for All in cost – FCY ECB – Benchmark rate + 5%; INR ECB – Benchmark rate + 4.5% p.a. Prepayment charge/ penal interest – upto 2 % over and above the contracted rate of interest.

Minimum maturity standardized [Para 6 – Sch 1]:

- Single minimum average maturity period of 3 years for all ECBs. Earlier maturity buckets of 3, 5, 7 and 10 years based on end use, stands consolidated.

- Manufacturing entities may raise ECB with MAMP of 1-3 years for outstanding ECBs up to USD 150 mn (earlier USD 50 mn per FY).

- MAMP not applicable in case of:

- Conversion of ECB to Non-debt Instrument (NDI) as per FEMA NDI Rules;

- Repayment using proceeds from issuance of NDI (on repat basis) as per FEMA NDI Rules received after ECB drawdown;

- Refinance of ECB (MAMP requirement applicable on the original borrowing);

- Waiver of debt by the lender;

- Repayment of ECB for undertaking corporate actions.

- MAMP Computation: Provided in Annex I of the Regulations.

ECB threshold enhanced to 1 USD billion [Para 5 – Sch 1]:

- Threshold: An eligible borrower may raise ECB up to the higher of:

- Outstanding ECBs of USD 1 billion; or

- 3X the net worth – external + domestic debt.

- Earlier limit – USD 750 mn per financial year.

- This “higher of” construct enhances borrowing headroom by aligning ECB capacity with the borrower’s financial strength while retaining an absolute monetary ceiling.

- Limit not applicable to RBI, SEBI, IRDA, PFRDA regulated borrower entities.

- Given that these entities are already governed by sector-specific capital, leverage and liquidity norms prescribed by the Financial Sector Regulators, a separate uniform ECB cap is not considered necessary.

- Proposed ECB will not include ECB for refinancing.

End-use restrictions simplified: [Reg. 3A]

- Acquisition finance permitted only for strategic purpose: ECB proceeds can now be utilised for merger, demerger, amalgamation, arrangement, or acquisition of control as per CA, 2013, SAST Reg, SARFAESI Act or IBC if it is availed for strategic purposes, driven by the core objective of creating long-term value through potential synergies, rather than for short-term gains.

- Acquisition finance has been permitted here as well, creating a level playing field for both domestic as well as foreign banks. Open ups a huge competitive situation for lenders from all over the world to compete to fund an acquisition. Recently, RBI opened up avenues for Banks, refer our detailed article here.

- Transacting in listed/unlisted securities is not permitted.

- Negative list aligned with FDI prohibited sectors under NDI Rules: ECB Proceeds cannot be utilised for chit funds, nidhi company, trading in TDRs, real estate business & construction of farm houses, plantation and agriculture & animal husbandry (other than expressly permitted under NDI Rules).

- Scope of real estate business aligned with NDI Rules. Additionally, excludes purchase, sale and lease (not amounting to transfer) of land or immovable property for commercial or residential properties for own use of the borrower;

- Repayment of a domestic INR loan, if availed for end use restricted under Reg. 3A or classified as NPA.

- Notably, the restricted sectors have now been aligned with sectors prohibited for FDI under NDI Rules, ensuring regulatory consistency across India’s external borrowing and foreign investment regimes.

- Onlending for any of the restricted purposes.

Recognised lender’s ambit expanded [Para 2 – Sch 1] :

- Any PROI (including individuals) can be a lender.

- Separate borrowing conditions in case of foreign equity holders removed.

- Financial institution or a branch set up in IFSC.

- A branch outside India of an entity whose lending business is RBI regulated. Earlier foreign branches / subsidiaries of Indian banks were permitted as recognised lenders only for FCY ECB availed by manufacturing entities.

- Repayment of ECBs sourced from NRO will go to NRO account only.

Eligible borrower’s eligibility relaxed [Para 1- Sch 1]:

- Any entity can avail ECB if permitted under applicable laws.

- incorporated, established or registered under a Central or State Act;

- Eligible borrowers undergoing restructuring or CIRP will be permitted only if expressly provided under the approved restructuring or resolution plan.

- Entities against whom any investigation, adjudication or appeal by a law enforcement agency is pending can also raise ECB, subject to disclosure in Form ECB 1.

Forms of ECB simplified [Para 4 – Sch 1]:

- ECB may be raised in any form of commercial borrowing arrangement that involves payment of agreed interest and repayment of principal. Includes FCCBs and FCEBs

- Earlier a specific list was provided comprising of loans including bank loans; floating/ fixed rate notes/ bonds/ debentures (other than CCDs); Trade credits beyond 3 years; FCCBs; FCEBs and Financial Lease. Preference shares (other than CCPS) could be raised only as INR denominated ECB.

- excludes

- Investments as per FEMA (Debt Instrument) Regulations, 2019

- Earlier too the ECB framework was not applicable in respect of investments in NCDs made by FPIs.

- Trade credit with original maturity upto 3 years

- Export advance received as per FEMA Export Regulations

- Convertible notes issued by start-ups under FEMA NDI Rules and

- Investments by FVCI as per FEMA NDI Rules.

- Investments as per FEMA (Debt Instrument) Regulations, 2019

Currency of borrowing made flexible [Para 3 – Sch 1]:

- ECB can be raised in any currency (FCY or INR)

- Option to change from one FCY to another FCY, FCY to INR or INR to FCY

- Earlier conversion from INR to FCY was not permitted.

Reporting requirements [Para 16 – Sch 1]:

- Form ECB 1 – for providing details of ECB and obtaining LRN

- Revised Form ECB 1 – separate form introduced for reporting any change in previously reported ECB parameters.

- To be filed within 7 calendar days after month end in which change was effected.

- Earlier this was reported in Form ECB within 7 days from the changes effected.

- Form ECB 2 – for reporting receipt of ECB proceeds and debt servicing.

- within 7 calendar days from the end of the month in which the ECB received or debt servicing was undertaken.

- Earlier to be submitted every month within 7 calendar days.

- Master Directions on Reporting under FEMA modified

- ‘Form ECB 1’ as per the format in Annex I to formecb@rbi.org.in

- ‘Revised Form ECB 1’ as per the format in Annex I to revisedformecb@rbi.org.in ‘Form ECB 2’ as per the format in Annex II to ecb2return@rbi.org.in

Arm’s length requirement [Para 9 – Sch 1]:

- ECBs from related parties to be on an arms length basis. Related party shall have the same meaning as assigned to it under Companies Act, 2013.

Receipt of ECB Proceeds [ Para 10 – Sch 1]

- For FCY expenditure: ECB proceeds can now be parked in an FCY account held in India or outside India (as per FEM (Foreign Currency Accounts by a Person Resident in India) Regulation, 2015).

- Earlier, such ECB proceeds could only be parked outside India.

- For INR expenditure: ECB proceeds to be credited to an INR account in India by end of the succeeding month from date of receipt.

- Earlier, immediate repatriation to Rupee accounts was required.

Impact on existing ECBs:

- LRN obtained prior to February 16, 2026 – Compliance to be done with erstwhile norms. Reporting will be required to be done as per amended norms.

Definitions [Reg. 2]:

- New definitions added for added clarity – net-worth, arm’s length basis, control, cost of borrowing, financial sector regulator, FCCBs, FCEBs, infrastructure sector, etc.

Read more:

The security clause read as co terminus to the loan tenure ?