Downstream investment to be treated at par with FDIs

Introduction

The Master Direction on Foreign Investment in India, recently updated on January 20, 2025, goes beyond a mere consolidation of the recent amendments in the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (‘NDI Rules’), providing clarifications in several areas of legislative silence. One of the key areas of clarification include the rules around downstream investments.

In this note, we have discussed downstream investment through stock deals and other significant clarifications provided in the Master Direction.

Background

Rule 6(a) of the NDI Rules deals with the investment by a person resident outside India (‘PROI’) in the equity instruments of an Indian company. The said rule refers to Schedule I, which, amongst others, specifies the modes of payment of consideration. Prior to the FEM (Non-Debt Instruments) (Fourth Amendment), Rules, 2024 dated August 16, 2024 (“Fourth Amendment Rules”), the Schedule contained an enabling provision for Indian companies to issue its equity instruments to PROI by way of swap of equity instruments. Since the term “equity instruments”, as defined under Rule 2(k) of Principal NDI Rules, means equity shares, convertible debentures, preference shares and share warrants issued by an Indian company, the provision permitting share swaps was read narrowly to refer to swap of shares of an Indian company against that of another Indian company only.

However, pursuant to the Fourth Amendment Rules, the Schedule was further amended to expressly provide for the swap of equity capital, as defined under rule 2(1)(e) of Foreign Exchange Management (Overseas Investment) Rules, 2022. The same is defined as “equity shares or perpetual capital or instruments that are irredeemable or contribution to non-debt capital of a foreign entity in the nature of fully and compulsorily convertible instruments.”

Downstream investment, on the other hand, is governed by the provisions of Rule 23 of the NDI Rules. While the said rule specified certain requirements to be complied with in the context of downstream investment, including the sources through which funds can be brought in for the purpose of such investments, the rule neither explicitly provided for the share swaps as a permitted mode of payment, nor contained any reference to Schedule I of the NDI Rules. As a result there was uncertainty among industry stakeholders on permissibility of share swaps as a form of consideration in case of downstream investment.

Meaning of Downstream Investment

The explanation to Rule 23 (also contained in Para 9.1.13 of the Master Direction) states that:

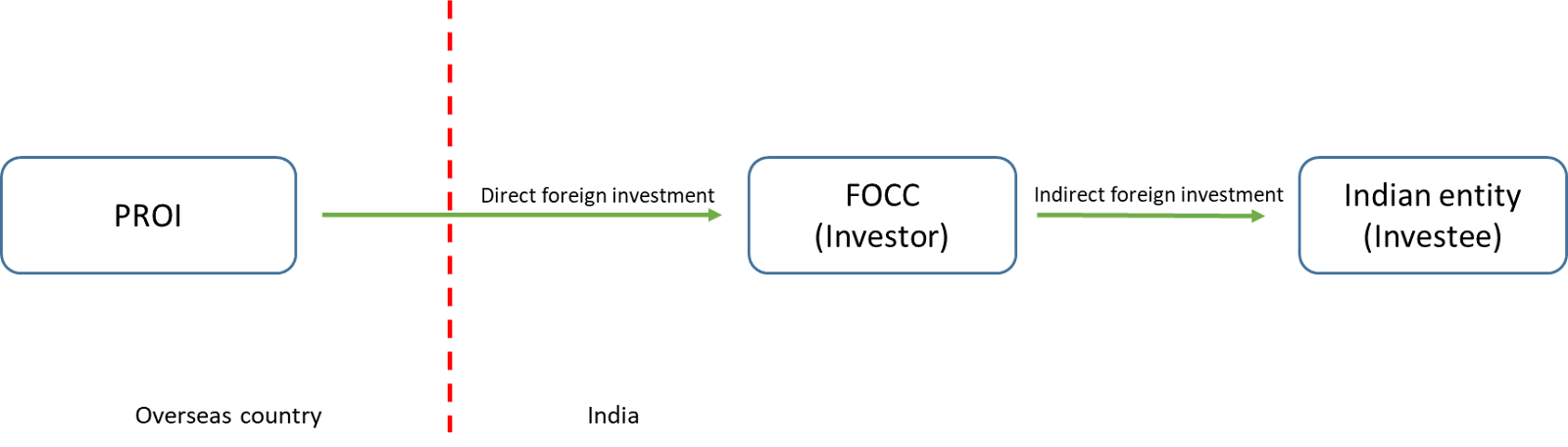

Downstream Investment is an investment made by an Indian entity which has received foreign investment or an Investment Vehicle in the equity instruments or the capital, as the case may be, of another Indian entity.

In other words, when an Indian entity owned or controlled by PROI [commonly referred to as a Foreign Owned and Controlled Entity (FOCC)] makes investments in the equity instruments/ capital of an Indian entity, such an investment will be considered as downstream investment for the PROI. Such arrangements enable PROI to hold investment in other Indian entities indirectly, thus, considered as an indirect foreign investment. As a result, the restrictions, prohibitions and limitations as applicable to direct foreign investments will be applicable at the time of downstream investment as well. For better understanding, refer to the figure below:

Guiding principle on downstream investment: what cannot be done directly, shall not be done indirectly

The recent updates in the Master Directions provide for the guiding principles of downstream investments, thereby clarifying that all permissions and prohibitions vis-à-vis direct foreign investment under the NDI Rules will be applicable to indirect foreign investment (i.e. downstream investment) as well.

Para 9 of the Recent Master Direction reads as below:

“The guiding principle of the downstream investment guidelines is that “what cannot be done directly, shall not be done indirectly”. Accordingly, downstream investments which are treated as indirect foreign investment are subject to the entry routes, sectoral caps or the investment limits, as the case may be, pricing guidelines, and the attendant conditionalities for such investment as laid down in the NDI Rules.”

Giving reference to above guiding principles, the Master Directions explicitly refers to the permissibility of the arrangements which are available for direct investment such as investment by way of swap of equity instruments/equity capital, payment arrangements/mechanism as per Rule 9(6) of the Rules etc, for the purpose of downstream investment as well.

Implication of above clarification

The above clarification has paved a way for Foreign Owned or Controlled entities (FOCC) to make further investments in Indian entities by way of swapping equity capital of foreign companies held by it in addition to other sources as already available. This arrangement of swapping of securities is known as a stock deal.

Previously, for making downstream investment, an FOCC was allowed to raise fresh funds from abroad by way of issue of securities including non-convertible debentures or by utilising internal accruals such as profits after tax. For more clarity refer to the table below:

| Sources of making investment by FOCC in another Indian entity | Position prior to the clarification | After clarification |

|---|---|---|

| Internal accruals (i.e., profits transferred to reserve account after payment of taxes) | Allowed | Allowed |

| Fresh funds from abroad including issue of NCD | Allowed | Allowed |

| Swap of equity instruments/ capital | No express provision | Allowed |

| Using funds borrowed in the domestic markets | Not allowed | Not allowed |

Other conditions w.r.t downstream investment in light of the guiding principle

As per the guiding principle on downstream investments as discussed above, an Indian entity which has received indirect foreign investment is subject to permissions and prohibitions as applicable to direct foreign investment under NDI Rules. Further, the onus of ensuring such compliances are on the FOCC making such investments, and not on the Indian investee entity receiving such indirect FDI.

- Investment from land border sharing countries

In order to curb opportunistic takeovers/ acquisitions of Indian companies due to COVID-19 pandemic, the Government of India restricted investment from countries sharing land borders with India or where the beneficial owner of an investment into India is situated in or is a citizen of any such country, by way of issue of Press Note-3. As a result, any foreign direct investment from such countries would be permitted with prior approval of the Government of India in permissible sectors.

This will be applicable in case of investment by FOCC as well, where such FOCC, in turn, has received investment from such countries as discussed above.

- Deferred payment arrangements

Similarly, the facility of making deferred payment of up to 25% in case of transfer of equity instruments between PROI and Person Resident in India (PRI) will also be applicable in case of downstream investment. This is, subject to the compliance with the conditions as laid down in Rule 9(6) of the NDI Rules.

The Master Directions further state that a transaction intended to be undertaken using above arrangement(s) shall require the share purchase/transfer agreement to contain the respective clause and related conditions for such arrangement.

- Subsequent classification as downstream investment

Where an Indian entity (i.e., investor) at the time of making further investment in another Indian entity (i.e., investee) was not an FOCC at the time of investment, but subsequently becomes an FOCC, then such investment in another Indian entity would need to be reclassified as downstream investment from the date when investor entity becomes FOCC. Consequently, such downstream investment shall be in compliance with the applicable entry route and sectoral cap compliances and shall be required to be reported by the investor entity within 30 days from the date of such reclassification in form DI.

- Valuation requirement

As per para 8.4 of the Recent Master Direction, in case of swap of equity instruments, irrespective of the amount, valuation will have to be made by a Merchant Banker registered with SEBI or an Investment Banker outside India registered with the appropriate regulatory authority in the host country.

- Downstream Investment by NRI/OCI on non-repat. basis to be treated as domestic investment

The investments made by NRIs/OCIs on non-repatriation basis is treated as deemed domestic investment. Accordingly, an investment made by an Indian entity which is owned and controlled by a Non-Resident Indian or an Overseas Citizen of India including a company, a trust and a partnership firm incorporated outside India and owned and controlled by a Non-Resident Indian or an Overseas Citizen of India, on a non-repatriation basis in compliance with Schedule IV of these rules, shall not be considered for calculation of indirect foreign investment.

To know more about foreign investment, check out our YouTube repository on:

- Overview of Foreign Direct Investment

- Understanding the Downstream Investment

- Overview of Overseas Investment Rules

Could you please clarify, In connection with the downstream investments. An investment made by an FOCC or it’s Wholly Owned Subsidiary by way of subscribing to the IPOs or by way of purchasing the equity shares through the stock exchanges will trigger the requirement of making the DI filings? There are a lot of FOCC’s which as part of treasury activities carrying out such investments.

Under Rule 23(2), the existing carve-out is restricted only to banking companies and does not extend to any other category of entities. Accordingly, where a Foreign Owned and Controlled Company (FOCC) makes an investment in the equity instruments of another Indian company, full compliance with Rule 23 is required, including filing of Form DI. This requirement applies irrespective of the mode of acquisition whether the shares are acquired by way of subscription to an IPO or through secondary market purchases on stock exchanges, as both constitute investments in equity instruments under the said Rule.