Securitisation, Transfer and Distribution of Credit Risk- for Banks and NBFCs.

We are pleased to announce the launch of our e-book — Securitisation, Transfer and Distribution of Credit Risk- for Banks and NBFCs.

This book, spanning over 900+ pages, provides a comprehensive analysis of the evolving regulatory and transactional landscape relating to credit risk transfer in India, with detailed commentary on:

• RBI regulations on securitisation

• Transfer of Loan Exposures or so-called direct assignments

• Co-lending arrangements

• Loan syndication arrangements

• SEBI regulations governing the issue and listing of securitised debt instruments

Designed specifically for banks, NBFCs, market participants, legal professionals and compliance teams, the publication offers practical insights into the regulatory framework governing structured finance and credit distribution transactions.

The Commentary is based on RBI’s November, 2025 version of consolidated Directions.

The book was launched during the 14th Securitisation Summit, and the e-book is available exclusively through the Premium Section of our website.

Kindly note that access to the book will be for a period of one year from the date of purchase of the book.

Read an excerpt from the book here.

Click here to purchase now directly, or

Table of Contents

About the book ……………………………………………………………………………………………………………………………. 1

Preface to Second Edition …………………………………………………………………………………………………………… 22

Chapter 1: Understanding the Basics of Securitisation & Structured Finance ……………………………………. 24

Chapter 2: Securitisation in India: Tracing the developments in the market ………………………………………. 51

Chapter 3: Asset Classes and Structures in India ……………………………………………………………………………. 67

Chapter 4: Law of assignment and true sale of receivables ……………………………………………………………… 83

Chapter 5: Commentary on the Directions on Securitisation of Standard Assets ………………………………. 107

Chapter 6: Listing Regulations On Securitised Debt Instruments & Security Receipts ……………………… 458

Chapter 7: Commentary on the Directions on Transfer of Loan Exposures ……………………………………… 659

Chapter 8: Co-lending Arrangements …………………………………………………………………………………………. 844

Chapter 9: Loan syndication, Consortium Lending, Participation Certificates and Balance Transfers …. 917

Chapter 10: Taxation aspects of Securitisation, Transfer of Loan Exposures and Co-lending ……………. 939

ABOUT THE CONTRIBUTORS ……………………………………………………………………………………………… 960

Indian Securitisation in FY26: Securitised Paper Volumes grow, with originator and asset diversity

– Vinod Kothari & Chirag Agarwal | finserv@vinodkothari.com

Volumes of securitisation (which, of course, have always included bilateral assignments or so-called DA transactions) fell by 6% in FY 26, if the origination volume by Reliance group entities in the first half were to be excluded. However, the market has shown more originator diversity, with an increasing share of smaller issuers, including those tasting the market for the first time.

The dip in volumes is because of the larger issuers who were prominently absent or subdued – Shriram Finance as the largest issuer having raised on-balance sheet liquidity, and banking companies. However, the share of gold loans went up sharply, largely due to the sharp increase in gold prices and gold lending, Microfinance companies went more for securitisation, rather than direct assignment transactions.

For anyone studying the Indian securitisation market, it is important to note the following:

- Reported volumes in India include direct assignments, which, in international parlance, are not “securitisation” (pure bilateral loan sales). However, in India, traditionally, DA has been a close and quick proxy for securitisation, and hence, mostly included. In FY 26, the split of DA/PTC volumes shows PTC transactions having gained in proportion. One rating agency1 reports an increase of PTC volume percentage from 54% to 60%; another one2 shows the increase from 48% to 52%.

- Indian transactions mostly show LAP transactions as a part of MBS, whereas what the world reports as RMBS is quite small in India. Last year, there was a prominent transaction by LIC Housing Finance, through the NHB-promoted RDCL. There was no RDCL issuance this year. It seems that RMBS volume was either too small to be reportable, or was completely absent.

- Microfinance sector has been under some stress in the recent past; however, MFIs have increasingly resorted to PTC issuances, with small deal sizes. Some deal sizes are even below 100 crores. This is indicating greater diversity of issuers, and of course, yields and ratings.

- The market also seems to be showing larger acceptance for lower rated securities i.e., BBB+.

Overall, in a stressful global scenario, securitisation has stood firm. Non financial sector entities have shown increasing willingness to tap the market. Of course, SEBI regulations have to be more enabling.

Below, we give a detailed overview of the securitisation market, including a discussion on the asset classes.

NBFCs vs Banks

Securitisation volumes have been largely driven by NBFCs, which recorded a 30% year-on-year increase in value. In contrast, originations by banks have declined significantly.

Recent Securitisation Structures in India – A Mix of Tradition and Innovation

Among asset classes, vehicle loans (including commercial vehicles and two-wheelers) accounted for 50% of securitisation volumes (vs 47% in the corresponding period last fiscal). Mortgage-backed loans accounted for about 28% of securitisation volume (vs 37% in the last FY).

Vehicle loan-backed securitisations dominated the market, both in terms of number of deals and total value, reaffirming the sector’s strong position. This is consistent with the growth trend in vehicle loan originations during FY 25.

In addition to vehicle loans, originators also securitised receivables from a diverse set of underlying asset classes during Q4, including:

- Microfinance Loans

- Secured Business Loans

- Unsecured Business Loans

- Home Loans

- Unsecured Personal Loans

- Gold Loans

The continued diversification in underlying asset classes highlights the evolving maturity of India’s securitisation market and growing investor appetite across segments. The break-up of securitisation volumes across various asset classes have been presented below:

Securitisation of Vehicle Loans

The issuance volume for vehicle loan securitisation during FY26 was approximately ₹1.26 lakh crores. Most of the transactions were structured as single-tranche issuances. However, a few exceptions featured more layered structures comprising senior and equity tranches, or senior, mezzanine, and equity tranches.

In terms of credit ratings, the tranches were rated between A- and AAA. Notably, the senior tranches in the majority of transactions received high investment-grade ratings, typically falling within the AA+ to AAA range. This indicates strong investor confidence and reflects the underlying credit quality of the asset pools, supported by adequate credit enhancement mechanisms.

Further, replenishing structures were also observed commonly during FY26. These variations indicate growing sophistication in transaction structuring within the vehicle loan securitisation space, aimed at catering to different investor preferences, improving credit protection, and aligning with originator risk appetite. As the market matures, further innovation in structuring and risk mitigation features can be expected.

In terms of credit enhancements, most vehicle loan securitisation transactions during the last quarter of FY26 featured: cash collateral (CC) and overcollateralisation (OC), with the Excess Interest Spread (EIS) serving as the first layer of loss absorption.

Securitisation of Microfinance Loans

During FY26, the MFI sector has seen a revival after a period of stress during FY 25 and FY 24. This has been due to better credit underwriting of lenders, improving performance trends and granular pool characteristics. Further, after a period of stress, the lenders relied on time-tested borrowers rather than exploring new markets leading to higher average ticket size of loans. This has led to a growth in the volumes of securitisation of microfinance loans during FY26. The PTC issuance volume of microfinance institutions increased to 14% of total PTC issuance in FY26 from 6% of total PTC issuances in FY25. Most of the transactions were structured as a single tranche securitisation.

Further, most microfinance loan securitisation transactions during the quarter featured credit enhancement through two primary mechanisms: CC and overcollateralisation OC, with the EIS serving as the first layer of loss absorption.

Securitisation of pool of loans backed by Home Loans & LAP

The volume of mortgage backed securitisation has been low both in terms of number as well as in terms of amount of issuance. As compared to FY25, the total MBS issuances dropped to 28% of total issuance from 37%. The transactions featured a common waterfall matrix and had received an overall rating of AAA.

In terms of credit enhancement, CC and OC has been provided as a credit enhancement with the EIS serving as the first layer of loss absorption.

Securitisation of Gold Loans

Gold loan securitisation volumes in H2FY26 stood at approximately ₹18,500 crore, significantly higher than the ₹5,000 crore recorded for the whole of FY25.

The jump in gold lending securitisation may be due to increase in gold prices and resultant increase in the value of the collateral. As a result of this valuation spike, average ticket sizes have increased, indicating that as gold valuations rise, consumers are leveraging higher-value loans to meet their financing needs. Another reason for the increased origination may be removal of LTV restriction in case of income generating gold loans.

Securitisation of Unsecured Loans

As per rating rationales published by Care the securitisation volumes of unsecured loans (both personal and business) increased during FY26. Investors in unsecured loan transactions, are preferring the PTC route, due to the support provided by external enhancement. CC and OC have also been provided as a credit enhancement with the EIS serving as the first layer of loss absorption.

- Secure with Securitisation: Global Volumes Expected to Rise in 2025

- India securitisation volumes 2024: Has co-lending taken the sheen?

- Indian securitisation enters a new phase: Banks originate with a bang

- Securitisation: Indian market grows amidst global volume contraction

- Crisil report on securitisation volumes: https://www.crisilratings.com/en/home/newsroom/press-releases/2026/04/securitisation-deal-value-peaks-to-rs-2-55-lakh-crore-in-fiscal-2026.html ↩︎

- Care report on securitisation volumes

https://www.careratings.com/uploads/newsfiles/1775801608_FY26%20Retail%20Securitisation%20at%20Rs%202.53%20Trillion%20First%20Dip%20PostPandemic.pdf ↩︎

Banking group NBFCs: Need to map businesses to avoid overlaps with the parent banks

– Vinod Kothari | finserv@vinodkothari.com

The new dispensation implemented from 5th December 2025 implies that lending business, obviously carried in the parent bank, needs to be allocated between the bank and the group entities so as to avoid overlaps. The bank will have to take its business allocation plan, at a group level, to its board, by 31st March 2026.

The RBI’s present move has certain global precedents. Singapore passed an anti-commingling rule applicable to banking groups way back in 2004, but has subsequently relaxed the rule by a provision referred to as section 23G of the Banking Regulations. However, the approach is not uniformly shared across jurisdictions.

We are of the view that as the decision works both at the bank as well as the NBFC/HFC level, the same has to be taken to the boards of the respective NBFCs/HFCs too.

Businesses which currently overlap include the following:

- Loans against properties

- Housing finance

- Loans against shares

- Trade finance

- Personal loans

- Digital lending

- Small business loans

- Gold loans

- Loans against vehicles – passenger and commercial, or loans against construction equipment

In our view, banks will have serious concerns in meeting their priority sector lending targets, unless they decide to keep priority sector lending business in the bank’s books. Priority sector lending is quite often much less profitable, and the NBFCs in the group are able to create such loans at much higher rates of return due to their delivery strengths or customer franchise. As to how the banks will be able to originate such loans departmentally, will remain a big question.

There are other implications of the above restrictions too:

- If a bank is engaged, for example, in MSME lending, but auto loans are done at the group entity, the bank cannot be a co-lender with its group entity, nor can it acquire auto loans originated by its group entity.

- Extending the same argument, if the banking group is carrying auto loan activity in its group NBFC, it cannot buy auto loans either by way of a direct assignment or co-lending, originated by other banks or other independent NBFCs. The reason for this is obvious – if the bank has decided to carry auto lending activity in its group entity, it should stay away from that exposure, even if originated by other entities.

- The decision to keep particular loan products with group entities – can it be stretched to the extent that bank will not have indirect exposure in such products, for example, by way of giving a loan to its group entity for on-lending for a product which the bank does not undertake departmentally? One of the reasons that may have prompted the Mohanty Group report in 2020 to segregate products between the bank and its group entities was contagion risk. If contagion is at the core of the present restriction, then that risk is still there even if the bank lends to a group entity for on-lending for a product. However, in our view, the present restriction is primarily aimed at avoiding regulatory arbitrages, and cannot be expected to require a completely independent financing of the loan products that a subsidiary finances, and not the bank.

- Therefore, in our view, a bank may not only on-lend to its group entities (of course, on the basis of an arm’s length lending approach), but it may also buy the asset-backed securities arising from such loan portfolios as sit with its group entities.

Factors to decide loan product allocation

In case of several non-lending products such as securities trading, demat services, etc., the approach may be easier. However, lending services constitute the bulk of any bank’s financial business, and group NBFCs and HFCs are also evidently engaged in lending. Hence, there may be a delicate decisioning by each of the boards on who does what. Note that this choice is not spasmodic – it is a strategic decision that will bind the entities for several years.

The factors based on which banks will have to decide on their business allocation may include:

- Delivery mechanisms – Mostly, branch and team strengths are sitting in group entities. Therefore, the loan products that entail last mile customer outreach, geographical access, etc are naturally housed in entities which possess those abilities.

- Technology strength: Some of the products are based on fintech or similar technology strength, which may be sitting with respective entities.

- Recovery mechanisms – Group entities are typically more nimble than banks. Hence, while banks may keep loans on their books, but they may engage group entities for recovery purposes.

- Priority sector requirements-: This will be a very important factor in deciding business allocation. Banks are mandated to invest 40% of their ANBC in qualifying priority sector loans – not NBFCs. Hence, for such loans as qualify as priority sector, the option may be to house the portfolios with the bank, or to invest in pass through certificates.

Securitised notes: whether investment in group entities?

Talking about pass through certificates, there is a complicated question as to whether the investment limits imposed by the 5th Dec. 2025 amendment on aggregate investments in group entities will include investment in pass through certificates arising out of pools originated by group entities. In our view, the answer is in the negative, as the investment is not originator, but in the asset pools. However, if the bank makes investment in the equity tranche or credit enhancing unrated tranches, the view may be different.

Conclusion

Banks are heading shortly in the last quarter of a year which is laden with strong headwinds. In this scenario, facing business allocation decisions, rather than business expansion or risk management, may be more challenging than it may seem to the regulators.

Other resources:

- Banks’ exposure to AIFs: Group-wide limits introduced

- Bank group NBFCs fall in Upper Layer without RBI identification

- Group-level regulation: RBI brings major regulatory restrictions on banks and group entities

- New NBFC Regulations: A ready reckoner guide

- New Commercial Bank Regulations: A ready reckoner guide

A matter of scale in securitisation

Qasim Saif, Vice President and Yuvraj Kundargi, Executive | finserv@vinodkothari.com

Background

The previous financial year witnessed Indian banks entering the securitisation market as originators, marking a positive step towards large-volume transactions. Their participation also raised expectations that non-lending institutions could increasingly come in as investors in such instruments.

Midway through this year, the Reliance group announced a landmark transaction, raising funds through securitisation of loan receivables of its group entities. These loans are proposed to be repaid from the receivables from usage of digital telecommunication infrastructure by Reliance group companies.

Issuances were made by three trusts: Radhakrishna Securitisation Trust, Shivshakti Securitisation Trust, and Siddhivinayak Securitisation Trust with maturities of approximately three, four and five years respectively, and carrying an average coupon of 7.75%.

This transaction represents the largest securitisation issuance in India to date. It is marked by a unique structure where the transaction is not supported by credit enhancements from the originator. Instead, the obligors’ rating, supported by a guarantee from Reliance Industries Ltd., enabled the securities to achieve a AAA rating.

This article discusses the structure of the transaction, its elements, and the flow of funds.

Read more: A matter of scale in securitisationUnderstanding the Structure

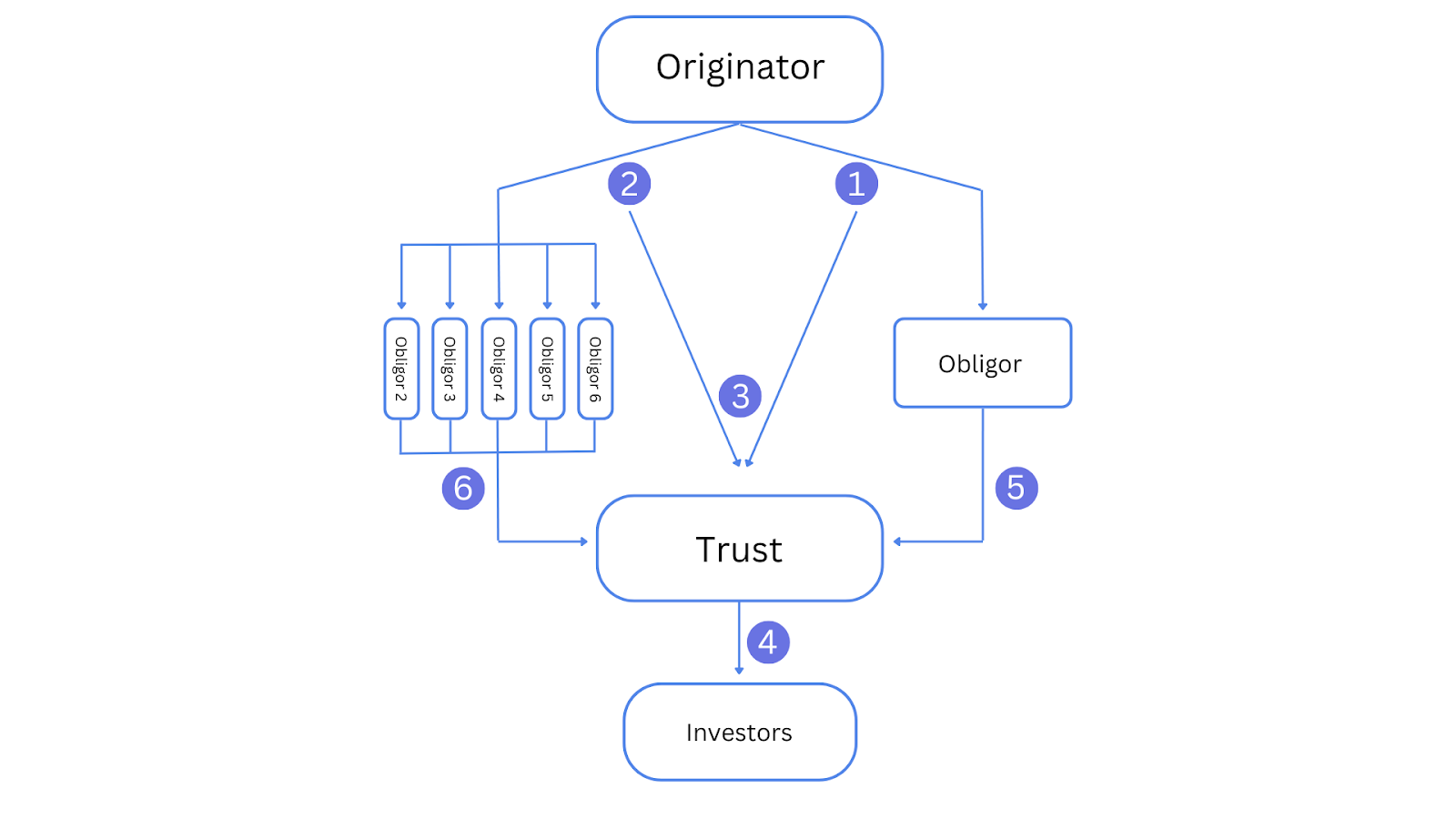

1. Loan by Originator

The originators, Sikka Ports & Terminals Limited (SPTL) and Jamnagar Utilities & Power Private Limited (JUPL), provided a long-tenure loan to the obligor, Digital Fibre Infrastructure Trust (DFIT).

However, the maturity of the loan’s principal extends far beyond the tenure of the pass-through certificates (PTCs) issued under the securitisation structure. Out of a total sanction amount of ₹33131 crore, ₹25000 crore was lent out by the originators for a period of 30 years. An additional loan amounting to ₹8131 crore was also extended, but is not being securitised in this transaction.

2. Put Option with Originator

Parallely, the originator entered into a put option agreement with five Reliance group entities, namely, Reliance Industries Holding Pvt. Ltd., Srichakra Commercials LLP, Karuna Commercials LLP, Devarshi Commercials LLP, and Tattvam Enterprises LLP. The put option gave the originator the right to sell the loan receivables to these entities. Since the maturity of the underlying loan is significantly longer than the tenure of PTCs, the trustee would exercise the put option with the group entities and proceeds from sale of the loan receivables would be used for principal repayment.

Section 19A of the SDI Regulations, which specifies the conditions governing securitisation, mandates that no obligor shall have more than 25% in the asset pool at the time of securitisation. This serves to reduce credit concentration by specifying a minimum number of obligors. Entering into an option agreement with five separate entities fulfills these diversification requirements, ensuring compliance with the SDI regulations.

3. Assignment of Receivables to the Securitisation Trust

The originator assigned the loan receivables, along with the receivables under the put option agreement, to the securitisation trusts. Three trusts were involved in this deal: Siddhivinayak, Shivshakti, and Radhakrishna. SPTL assigned its loans to the first two trusts, while JUPL assigned its loan to Radhakrishna. Reliance Industries Holding Pvt. Ltd., one of the option counterparties, is not a part of the structure of the first trust; Siddhivinayak only has four option counterparties.

(all values in ₹ crore)

| Structure of the deal | |||

| Trusts | Siddhivinayak | Shivshakti | Radhakrishna |

| Value of Receivables | 6780.34 | 6943.36 | 4461.71 |

| Assignor of Receivables | STPL | JUPL | JUPL |

| Value of PTCs | 8000.00 | 8000.00 | 5000.00 |

| Value of Options | 1615.93 | 1339.92 | 870.24 |

| Number of Option Counterparties | 4 | 5 | 5 |

| Principal Repayment from Options | 6463.72 | 6699.62 | 4351.22 |

| Principal Repayment from DFIT | 1536.28 | 1300.38 | 648.78 |

| Yield on PTCs | 7.80% | 7.73% | 7.66% |

| Tenure of PTCs in years | 5 | 4 | 3 |

4. Issuance of Securitised Notes

The trusts issued securitised notes to investors, backed by loan receivables. These notes, or pass-through certificates (PTCs), have varying tenures of five, four, and three years respectively. They also have different yields, as the table above highlights. The notes were rated by two independent agencies, Crisil and Care Edge, and all three issuances were given a AAA rating.

5. Investor Participation

Roughly three-fourths of the issuance has been subscribed by the country’s leading asset managers, including Aditya Birla Sun Life AMC, HDFC AMC, ICICI Prudential AMC, Nippon Life India AMC, and SBI Funds Management Ltd.

6. Servicing of Securitised Notes

- Interest payments: Serviced from the interest on the underlying loan by DFIT .

- Principal repayments: Since the maturity of the underlying loan is significantly longer than the PTCs, the trustee would exercise the put option with the group entities. The proceeds from the sale of the loan under this option were then used to repay the principal to the securitised noteholders.

Read our other articles:

Listed and Restricted? Additional Compliances and Prohibitions for listing of SDIs by RBI regulated Originators

– Payal Agarwal & Dayita Kanodia (finserv@vinodkothari.com)

Securitisation Transactions in India are primarily governed by:

- The RBI Securitisation of Standard Assets Directions, 2021 (in case the originator is regulated by RBI)

- SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, which become applicable if the securitisation notes are listed.

Consequently, an RBI regulated originator will be required to adhere to both the SSA Directions as well as the SDI Framework in case it intends to go for listing of the securisation notes.

Here, we have discussed the additional prohinitions and compliance requirements for RBI regulated originators which becomes applicable in case of listing of securitisation notes.

| Additional Prohibitions under the SEBI SDI Framework for RBI Regulated Originators | |||

| Para Ref | Relevant Regulatory Provision | Our Comments | |

| Single Asset Securitisation not permitted | 19A(a) | “No obligor shall have more than twenty-five percent in asset pool at the time of issuance.” | An RBI regulated originator will not be able to undertake single asset securitisation if it intends to list the securitisation notes, though the same is permitted under the RBI regulations (proviso to para 5(s) of the SSA Directions). Comments: Single asset securitisation is not a very common practice, but this is explicitly permitted under RBI regulations |

| All assets to be homogenous | 19A(b) | “Assets comprising the securitisation pool shall be homogeneous.” | The RBI SSA Directions only require the assets to be homogeneous in case of simple, transparent, and comparable securitisation transactions (STC Transactions). STC transactions are currently not very common, and in any case, is an investor classification, not that of issuer.For non-STC cases, there is no such requirement. Therefore, originators will be required to ensure that the assets comprising the pool are homogeneous in case they intend to go for listing of the securitisation notes. Comment: Homogeneity may be subjective |

| SPV can only be constituted in the form of a trust | 9(1) | “The special purpose distinct entity shall be constituted in the form of a trust the constitutional document whereof entitles the trustees to issue securitised debt instruments.” | The RBI SSA Directions (para 5(w)) allow SPVs to be constituted in the form of a company, trust or other entity. Comment: Not a very big pain, as SPVs in India are almost always in the trust form. |

| Originator and Trustee not be under the same group or control. | 10(3) | “No special purpose distinct entity shall acquire any debt or receivables from any originator which is part of the same group or which is under the same control as the trustee.” | This requirement, although essential to maintain independence, is not a part of the RBI SSA Directions. Accordingly, the same will be required to be ensured. |

| Additional Compliances applicable to RBI regulated Originators under the SEBI SDI Framework | |||

| Para Ref | Relevant Regulatory Provision | Our Comments | |

| Registration of Trustees under the Securities and Exchange Board of India(Debenture Trustees) Regulations, 1993 | 4(b) | “(1) On and from the commencement of these regulations, no person shall make a public offer of securitised debt instruments or seek listing for such securitised debt instruments unless –XX(b)all its trustees are registered with the Board under 26[the Securities and Exchange Board of India(Debenture Trustees) Regulations, 1993];XX” | Accordingly, the trustees will be required to comply with the SEBI Debenture Trustee regulations. Comment: This is a useful provision, and mostly, the SPV trustees are registered debenture trustees. Hence, it is a useful regulatory requirement. |

| Contents of the Instrument of Trust | Schedule IV | Schedule IV of the SEBI SDI Framework prescribes the minimum contents of the instrument of trust. | The contents prescribed under the SDI Framework are more detailed as compared to the RBI SSA Directions, which only indicate the contents of the trust deed. Comment: Useful regulation, serving the purpose of proper disclosures. Notably, disclosures are the domain of the securities regulator. |

| Quarterly reports to the trustee about the performance of the underlying pool and auditor certificate | 10A(1) and (2) | “(1) The originator shall provide the periodic reports to the trustee regarding the performance of the underlying asset pool, at least on a quarterly basis. (2) The originator shall provide a certificate from its auditor (s) regarding the disclosures of underlying asset pool assigned to the securitization trust, as made by the originator, on quarterly basis.” | The RBI SSA Directions (para 114 and 115) require semi-annual disclosures to be made. Further, there is no requirement to provide an auditor’s certificate under the RBI Directions. Comment: Useful regulation, serving the purpose of investor information. These disclosures are typically part of the securities regulators’ domain. |

| Minimum Ticket Size for subsequent transfers | 30A(2)(i) | “The minimum ticket size for subsequent transfers of a securitised debt instrument shall be as follows:(i)for originators which are not regulated by the Reserve Bank of India, the minimum ticket size shall be rupees one crore.” | In case of public offer of SDIs, the minimum ticket size is Rs. 1 Crore even for subsequent transfers of SDIs. This requirement is more stringent as compared to the RBI SSA Directions (para 28), which only requires the minimum ticket size of Rs. 1 Crore to be seen at the time of issuance. Comments: The requirement has only been introduced for the public offer of SDIs. Public issue of SDIs is howe,ver not a common practice currently. Accordingly, this may not seem to be a major concern for RBI regulated originators. |

| Other miscellaneous provisions – offer period, allotment period, dematerialisation | 29, 31(1) | Offer Period: No public offer of securitised debt instruments shall remain open for less than two working days and more than ten working days. Allotment Period:The securitised debt instruments shall be allotted to the investors within five days of closure of the offer. Further, the securitises will need to be issued mandatorily in demat form. | Comments: These requirements are applicable only in case of public offers. |

| Facility to avail electronic bidding platform | Master Circular dated May 16, 2025 | On issue and listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper and on Review of provisions pertaining to Electronic Book Provider (EBP) platform to increase its efficacy and utility | The facility of using EBP has been extended to SDIs too. Comment: This is an optional facility, and as of now, very limited issuers have made use of this. |

| LODR Requirements – Chapter III | |||

| Disclosure by KMPs, directors, etc | Reg 5 | 5. The listed entity shall ensure that key managerial personnel, directors, promoters or any other person dealing with the listed entity, complies with responsibilities or obligations, if any, assigned to them under these regulations 51[:]52[Provided that the key managerial personnel, directors, promoter, promoter group or any other person dealing with the listed entity shall disclose to the listed entity all information that is relevant and necessary for the listed entity to ensure compliance with the applicable laws.] | This requires the concerned officers of the Listed Entity (in this case, the SPV] to make requisite disclosures for the purpose of complying with the law. Comment: Does not seem to be practically relevant, as Originators’ KMPs mostly do not have interest in the SPV. However, where needed, it is a useful disclosure. |

| Compliance officer to be appointed. | Reg 6, Chap III | 6. (1) A listed entity shall appoint a qualified company secretary as the compliance officer Other provisions of the regulation | An issuer of SDIs is required to appoint a Compliance Officer. Comments: The requirement may be complied with at SPV level. |

| Share Transfer Agent | Reg 7 | (1)The listed entity shall appoint a share transfer agent or manage the share transfer facility in-house:Other requirements of the regulation | The requirement to appoint a share transfer agent is typically part of the securities regulators’ domain. Comment: Mostly not relevant as the securities are offered in demat form. |

| Information to intermediaries | Reg 8 | The listed entity, wherever applicable, shall co-operate with and submit correct and adequate information to the intermediaries registered with the Board such as credit rating agencies, registrar to an issue and share transfer agents, debenture trustees etc, within timelines and procedures specified under the Act, regulations and circulars issued there under:Provided that requirements of this regulation shall not be applicable to the units issued by mutual funds listed on a recognised stock exchange(s) for which the provisions of the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996 shall be applicable. | Requirement to share information with the information agencies. Comment: In case of listed SDIs, this is a part of the information eco system. |

| Policy for preservation of documents | Reg 9 | The listed entity shall have a policy for preservation of documents, etc. | Useful for preservation of documents. |

| Filing of reports, statements and other documents | Reg 10 | (1) The listed entity shall file the reports, statements, documents, filings and any other information with the recognised stock exchange(s) on the electronic platform as specified by the Board or the recognised stock exchange(s).Other provisions of the regulation | This is a general filing requirement for filing of information on the stock exchanges. |

| Scheme of arrangement to not violate, affect or override the provisions of securities law | Reg 11 | The listed entity shall ensure that any scheme of arrangement /amalgamation /merger /reconstruction /reduction of capital etc. to be presented to any Court or Tribunal does not in any way violate, override or limit the provisions of securities laws or requirements of the stock exchange(s):. | Mostly not relevant for SDIs |

| Use of electronic mode of payments | Reg 12 | The listed entity shall use any of the electronic mode of payment facility approved by the Reserve Bank of India, in the manner specified in Schedule I, for the payment of the following:(a) dividends;(b) interest;(c) redemption or repayment amounts: | Provides for mode of payments to investors. Not a cumbersome requirement as it refers to RBI-permitted payment systems to be used. |

| SCORES | Reg 13 | (1) 61[The listed entity shall redress investor grievances promptly but not later than twenty-one calendar days from the date of receipt of the grievance and in such manner as may be specified by the Board.]Other provisions of the Regulation | This relates to use of the SCORES mechanism for settling investor issues |

| Payment of Fees and charges | Reg 14 | The listed entity shall pay all such fees or charges, as applicable, to the recognised stock exchange(s), in the manner specified by the Board or the recognised stock exchange(s). | This mandates payment of listing fees. Usual provision for all listed securities |

| LODR Regulations – Chapter VIII | |||

| The entire Chapter is dedicated to listed SDI issuance. | Reg 81 | Applicability(1) The provisions of this chapter shall apply to Special Purpose Distinct Entity issuing securitised debt instruments and trustees of Special Purpose Distinct Entity shall ensure compliance with each of the provisions of these regulations.(2) The expressions “asset pool”, “clean up call option”, “credit enhancement”, “debt or receivables”, “investor”, “liquidity provider”, “obligor”, “originator”, “regulated activity”, “scheme”, “securitization”, “securitized debt instrument”, “servicer”, “special purpose distinct entity”, “sponsor” and “trustee” shall have the same meaning as assigned to them under [Securities and Exchange Board of India (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008]555; | Specifies applicability of the Chapter and refers to meaning of relevant expressions |

| Intimation and filings with stock exchange(s) | Reg 82 | (1) The listed entity shall intimate the Stock exchange, of its intention to issue new securitized debt instruments either through a public issue or on private placement basis (if it proposes to list such privately placed debt securities on the Stock exchange) prior to issuing such securities.(2) The listed entity shall intimate to the stock exchange(s), at least two working days in advance, excluding the date of the intimation and date of the meeting, regarding the meeting of its board of trustees, at which the recommendation or declaration of issue of securitized debt instruments or any other matter affecting the rights or interests of holders of securitized debt instruments is proposed to be considered.(3) The listed entity shall submit such statements, reports or information including financial information pertaining to Schemes to stock exchange within seven days from the end of the month/ actual payment date, either by itself or through the servicer, on a monthly basis in the format as specified by the Board from time to time:Provided that where periodicity of the receivables is not monthly, reporting shall be made for the relevant periods.(4) The listed entity shall provide the stock exchange, either by itself or through the servicer, loan level information, without disclosing particulars of individual borrowers, in manner specified by stock exchange. | This regulation is equivalent of reg 29 in case of listed equities, and provides for prior intimation to investors for certain critical actions on the part of issuers. |

| Disclosure of information having bearing on performance/operation of listed entity and/or price sensitive information | 83 read with Part D of Schedule III | (1) The listed entity shall promptly inform the stock exchange(s) of all information having bearing on the on performance/operation of the listed entity and price sensitive information.(2) Without prejudice to the generality of sub-regulation(1), the listed entity shall make the disclosures specified in Part D of Schedule III.Explanation.- The expression ‘promptly inform’, shall imply that the stock exchange must be informed must as soon as practically possible and without any delay and that the information shall be given first to the stock exchange(s) before providing the same to any third party. | This regulation is to ensure the regular flow of information from issuers to investors, to maintain information symmetry. This is typical for all listed securities – for example, Reg 30 in case of listed equities, and reg 51 in case of listed non convertible debt securities. |

| Credit Rating to be periodically reviewed and any revision to be notified | Reg 84 | (1) Every rating obtained by the listed entity with respect to securitised debt instruments shall be periodically reviewed, preferably once a year, by a credit rating agency registered by the Board.(2) Any revision in rating(s) shall be disseminated by the stock exchange(s). | This Regulation requires a mandatory annual review of credit ratings on the SDIs by a SEBI-registered CRA, and intimation of any revision to the stock exchanges. |

| Information to Investors | Reg 85 | (1) The listed entity shall provide either by itself or through the servicer, loan level information without disclosing particulars of individual borrower to its investors.(2) The listed entity shall provide information regarding revision in rating as a result of credit rating done periodically in terms of regulation 84 above to its investors.(3) The information at sub-regulation (1) and (2) may be sent to investors in electronic form/fax if so consented by the investors.(4) The listed entity shall display the email address of the grievance redressal division and other relevant details prominently on its website and in the various materials / pamphlets/ advertisement campaigns initiated by it for creating investor awareness. | This clause requires certain pool level information; useful information for the poolComment: As in case of other jurisdictions, the disclosure requirements are typically laid by the securities regulations |

| Terms of Securitized Debt Instruments | Reg 86 | (1) The listed entity shall ensure that no material modification shall be made to the structure of the securitized debt instruments in terms of coupon, conversion, redemption, or otherwise without prior approval of the recognised stock exchange(s) where the securitized debt instruments are listed and the listed entity shall make an application to the recognised stock exchange(s) only after the approval by Trustees.(2) The listed entity shall ensure timely interest/ redemption payment.(3) The listed entity shall ensure that where credit enhancement has been provided for, it shall make credit enhancement available for listed securitized debt instruments at all times.(4) The listed entity shall not forfeit unclaimed interest and principal and such unclaimed interest and principal shall be, after a period of seven years, transferred to the Investor Protection and Education Fund established under the Securities and Exchange Board of India (Investor Protection and Education Fund) Regulations, 2009.(5) Unless the terms of issue provide otherwise, the listed entity shall not select any of its listed securitized debt instruments for redemption otherwise than on pro rata basis or by lot and shall promptly submit to the recognised stock exchange(s) the details thereof.(6) The listed entity shall remain listed till the maturity or redemption of securitised debt instruments or till the same are delisted as per the procedure laid down by the BoardProvided that the provisions of this sub-regulation shall not restrict the right of the recognised stock exchange(s) to delist, suspend or remove the securities at any time and for any reason which the recognised stock exchange(s) considers proper in accordance with the applicable legal provisions. | This requires prior approval of the stock exchange to be obtained for making any material modification to the structure of SDIs. It also requires the originator to ensure timely payments of interest and for the credit enhancement to be available at all times. |

| Record Date | Reg 87 | (1) The listed entity shall fix a record date for payment of interest and payment of redemption or repayment amount or for such other purposes as specified by the recognised stock exchange(s).(2) The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to the recognised stock exchange(s) of the record date or of as many days as the Stock Exchange may agree to or require specifying the purpose of the record date. | This is for fixation of record date for payouts; useful for investor decisions for entry or exit. |

| Disclosure of Information having bearing on performance/ operation of listed entity and/ or price sensitive information | Part D of Schedule III | Several disclosure requirements for significant events and developments | See comments under reg 83 |

Other Resources: Buy our book on Securitised Debt Instruments here.

More Than Enough: Overcollateralisation as credit enhancement in Securitisations

Vinod Kothari, Dayita Kanodia and Archisman Bhattacharjee | finserv@vinodkothari.com

Overcollateralisation (OC) is a widely employed credit enhancement technique in securitisation transactions, serving as a layer of protection for investors. In essence, it refers to a situation where the value of the underlying asset pool exceeds the amount of the liabilities, that is, the securities issued.

A simple illustration of OC is as follows:

Read more →From Rooftops to Ratings: India’s Green Securitisation Debut

– Payal Agarwal, Partner | finserv@vinodkothari.com

Probably the first in India, green securitisation has finally found an entry with the recent issuance of pass-through certificates backed by residential rooftop solar loan receivables in India. The loans were originated by a ‘green-only’ NBFC focussed on climate-positive lending. The present issuance is in the form of green collateral securitisation – since the securitised receivables qualify as ‘green’. Further, given the activities of the originator, it seems that the same may qualify to be a green capital securitisation, with the freed capital of the originator being utilised towards creation of green assets.

Notably, as per a recent publication of Climate Policy Initiative, the Global Landscape of Climate Finance 2025, India has been ranked as the leading country in the South Asia region in terms of mobilisation of climate finance (as per the data for 2023). Green securitisation may act as a catalyst to the growth of green finance in India. See a whitepaper on the same here.

A broader concept in the context of climate finance is sustainable securitisation, our whitepaper on the same can be accessed here. The recent guidelines of SEBI also permits the issuance and listing of sustainable securitised debt instruments, based on the recommendations of the Working Group constituted for the review of SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, chaired by Mr. Vinod Kothari. An article on the concept of sustainable SDIs may be accessed here.

Our various resources on sustainability finance is available at – https://vinodkothari.com/resources-on-sustainability-finance/

Our various resources on securitisation is available at – https://vinodkothari.com/2025/01/securitisation-resource-centre/

LISTING REGULATIONS ON SECURITISED DEBT INSTRUMENTS AND SECURITY RECEIPTS

We are pleased to unveil “Listing Regulations on Securitised Debt Instruments and Security Receipts”, an in-depth commentary on the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations. The book offers practitioners, market participants, and legal professionals a comprehensive understanding of the evolving regulatory landscape for listed securitised products in India.

Incorporating key regulatory updates, including SEBI’s Master Circulars and Exchange-level compliance requirements, this book not only deciphers the law but also contextualises it within the broader evolution of the securitisation market. With a focus on both regulatory interpretation and market practice, it serves as a valuable resource for anyone engaging with the growing ecosystem of securitised instruments in India.

Loading…

Loading…

In order to access the e-book, register your interest here.