Posts

SEBI approves cartload of amendments

– Team Corplaw | corplaw@vinodkothari.com

SEBI in its Board meeting dated December 18, 2024, has approved amendments pertaining to BRSR, HVDLEs, DTs, SMEs, Intermediaries, etc. This article gives a brief overview of the approved amendments.

Ease of Doing Business for BRSR

- Scope of BRSR Core for Value Chain Partners shrunk

- Value chain partners now consist of individuals comprising 2% or more of the listed entity’s purchases and sales (by value) instead of 75% of listed entity’s purchases/sales (by value).

- Further, the listed entity may limit disclosure of value chain to cover 75% of its purchases and sales (by value), respectively.

- Deferred applicability of ESG disclosures for the value chain partners & its limited assurance by one financial year

- Applicability of ESG disclosures for the value chain deferred from FY 24-25 to FY 25-26.

- Applicability of limited assurance deferred from FY 25-26 to FY 26-27.

- Voluntary disclosure of ESG disclosures for the value chain partners & its limited assurance instead of comply-or-explain

- Top 250 listed entities by market cap can now comply with the ESG disclosures for the value chain partners & its limited assurance on a voluntary basis in place of comply-or-explain.

- Term ‘Assurance’ replaced with ‘assessment or assurance’ to prevent unwarranted association with a particular profession (specifically audit profession).

- Assessment defined as third-party assessment undertaken as per standards to be developed by the Industry Standards Forum (ISF) in consultation with SEBI.

- Reporting of previous year numbers voluntary in case of first year of reporting of ESG disclosures for value chain.

- Addition of disclosure pertaining to green credits as a leadership indicator under Principle 6 – Businesses should respect and make efforts to protect and restore the environment of BRSR

Immediate actionables for Listed entities:

- Entity to re-assess its value chain partners as per the revised definition.

- Entity forming part of top 250 listed entities by market cap to undertake third party assessment of its BRSR Core disclosure for FY 24-25 as per the standards to be developed by ISF.

- To disclose about the green credits procured/generated by the entity during FY 24-25.

Debenture Trustee (‘DT’) Regulations:

- Introduction of provisions relating to ‘Rights of DTs exercisable to aid in the performance of their duties, obligations, roles and responsibilities’, which broadly indicates (as proposed in the CP):

- Calling information/ documents from issuer w.r.t. the issuance;

- Calling documents from various intermediaries;

- Calling of and utilization of Recovery Expense Fund, with consent of holders.

- Corresponding obligations on the issuers to submit necessary information/documents to DTs.

VKCo comments: In addition to the corresponding obligations on the issuer, CP also proposed to mandate Depositories and Stock exchanges to provide requisite information to DTs, which is yet to be approved. The right to call information from issuers and market participants including corresponding obligations on them will enable DTs to perform their functions efficiently.

- Introduction of standardized format of the Debenture Trust Deed (‘DTD’)

- To be issued by Industry Standards Forum with SEBI consultation;

- In case of deviation from the format of DTD, disclosure is to be made for investor review. (CP proposed to disclose deviation as insertion of a key summary sheet of deviation in GID/KID)

VKCo comments: While the introduction of model DTD is appreciated, the draft model DTD proposed in the CP was not aligned with the general market practices followed by the DTs as well as the applicable laws such as SEBI Listing Regulations, NCS Regulations, Indian Trust Act, etc.

- Activity-based Regulation for DTs:

- DTs are to undertake only such activities regulated by other financial sector regulators/ authorities (as SEBI specifies);

- Hive off non-regulated activities to a separate entity – within 2 years;

- Sharing of resources between DT and hived-off entity is allowed, subject to segregation of legal liabilities;

- Hived-off entity can use DT’s brand/logo – only for a period of 2 years (CP suggested 1 year); Both DT and hived-off entity to abide by SEBI’s code of conduct during such period.

- Refer to our discussion on CP in SEBI unveils new reforms for Debenture Trustees

Applicability of CG norms on HVDLEs

Under this segment of changes discussed by SEBI, most of the proposals are in alignment with the Consultation Paper dated 31st October, 2024, except for few changes in relation with PSUs coming together with public enterprises under Public Private Partnership.

- Threshold for being identified as HVDLE increased from 500 Crores to 1,000 Crores to align with the criteria of Large Corporates

VKCo Comments: The proposal to enhance the extant threshold is encouraging in terms of governing the maximum value of outstanding debt while at the same time achieving the same without bearing the burden of compliance by an increased number of purely debt listed entities. Subsequently, effective implementation of such a proposal aligns it with the identification criteria of Large Corporates.

- Introduction of a separate chapter for entities having only debt listed, and sunset clause for applicability of CG norms

VKCO Comments: While this proposal is noteworthy, however, instead of rolling out a new chapter, there could have been certain modifications in the existing regulations by way of a proviso to align with the needs of an HVDLE. Further, one also needs to wait to see the fine print -of the provisions once the same is issued.

VKCo Comments: The proposal is welcome since it clearly sets the HVDLEs free from the barrier of once an HVDLE so always an HVDLE. This proposal sets a clear nexus between the compliance and the size of the debt outstanding, for the protection of which in the very first place, the compliance triggered.

- Optional constitution of RMC, NRC, and SRC and delegation of their functions to the AC and Board respectively.

VKCo Comments: Given the close construct of debt listed entities, it is often observed that the constitution of such committees becomes more of a hardship than in smoothing compliance and discussing specific matters. Accordingly, it looks appropriate to redirect the functions of NRC and RMC to the Audit Committee and that of the SRC to the Board.

- HVDLEs to be included in the counting of maximum no. of directorships, memberships and chairmanships of committees. However, this shall exclude directorships arising out of ex-officio position by virtue of statute or applicable contractual framework in case of PSUs and entities set up under the Public Private Partnership (PPP) mode respectively, in the count. The said exclusion was not in the CP.

VKCo Comments: The rationale completely aligns with the proposal made and seems to be justified. Further, as far as the exclusion is concerned, this seems more from excluding those members who are part of the board not on the basis of their appointment but their current tenure being served in a particular position in the company.

- RPT Approval by way of NOC from DT (who obtains it from holders), before going for shareholders’ approval [w.e.f. 1st April, 2025]

VKCo Comments – While the CP suggested two ways of seeking approval for material RPTs of an HVDLE. The Board has only considered the alternative mode of first seeking NOC of DT and thereafter approaching the shareholders. Further, as discussed in our related write up on the CP, there does not seem to be any incentive to first approach the DT and thereafter the DT to approach the NCD holders. Instead the approval of the NCD holders can be taken up directly by the HVDLE.

- Submission of BRSR on a voluntary basis

VKCo Comments: The inclusion of a voluntary provision in the legislation with respect to a comprehensive report like BRSR is not likely to be submitted given the huge details under the BRSR. However, an opportunity to submit BRSR can be a game changer for an HVDLE from the perspective of being able to raise funds based on its reporting standards in this regard.

One of the changes discussed by the Board is relaxation to HVDLEs set up under the PPP mode from composition requirements of directors. While this was not a part of the CP, however, even if we have to understand that change proposed, this looks like relaxing the composition requirement of the Board of Directors.

CHANGES NOT APPROVED:

- Compulsory filing of CG compliance report in XBRL format

VKCo Comments: This proposal was with an objective to align and standardize the filing of quarterly CG compliance report for bringing parity as in the case of equity listed entities

- Exemption to entities not being a Company

VKCo Comments: While SEBI refers to the introduction of similar exclusion for equity listed entities, however, it has also mentioned the subsequent amendment wherein the same was omitted. The proposal not being notified is in alignment with the position of equity listed entities, however, the same would have been a welcome change since it would have helped such entities to give preference to their principal statutes and not an ancillary one like LODR.

Our detailed write up on the CP can be accessed here.

Amendments in the definition of UPSI – making the law more prescriptive

- Inclusion of 17 items in definition of UPSI: The illustrative list of USPI in reg. 2 (1) (n) of the PIT Regulations has been expanded to include 17 items from the list of material events laid out in Part A of Schedule III of the Listing Regulations [Originally proposed in the CP – 13 items]

- Threshold limits under reg. 30 made applicable: materiality thresholds specified in reg. 30 (4) (i) (c) of the Listing Regulations have been made applicable for identification of events as UPSI

- As per the current practice, any event that is likely to materially affect the price of the securities can be identified as UPSI

- Extended timelines for making entries in SDD: for an event of UPSI that emanates outside the company, entries can be made in the SDD within 2 days of occurrence. Further closure of the trading window will not be mandatory in such cases.

- This has been introduced as a part of EODB

- As per the current practice entries in the SDD have to be made promptly

Refer to our discussion on CP in: Laundry List: SEBI’s proposal to elongate list of deemed UPSIs

Perched at the Peak: Compliance Officer as CXO

– Do LODR changes force all companies to change their org structures?

– Vinita Nair, Senior Partner (corplaw@vinodkothari.com)

This version: 3rd April, 2025 (Updated as per SEBI Circular dated 1st April, 2025)

With the enforcement of recent amendments in LODR Regulations effective December 12, 2024 a qualified company secretary appointed as a Compliance Officer (‘CO’) is required to be an officer, who is in whole-time employment of the listed entity, not more than one level below the board of directors, designated as a Key Managerial Personnel (‘KMP’) and form part of senior management.

Listed entities now face the question of whether this entails a re-look at the organisation structure, hierarchy, profile of the CO? Whether the board of directors needs to be sensitised of this requirement and the impact, if any?

Watch our YouTube video on the same here.

Scope of “compliance”

The Basel paper of 2005 gives clarity on what is compliance, and the ambit of compliance function. First of all, the scope of the word “compliance” is not limited to laws and regulations only. “Compliance laws, rules and standards have various sources, including primary legislation, rules and standards issued by legislators and supervisors, market conventions, codes of practice promoted by industry associations, and internal codes of conduct applicable to the staff members of the bank. For the reasons mentioned above, these are likely to go beyond what is legally binding and embrace broader standards of integrity and ethical conduct.”

The compliance function is a cornerstone of an entity’s governance, internal control, and risk management framework. It includes the systems, procedures, and organisational infrastructure required to ensure:

- Compliance with all statutory and regulatory requirements;

- Maintenance of high standards of market conduct;

- Implementation of effective systems for managing conflicts of interest;

- Fair treatment of customers;

- Delivery of suitable and high-quality customer service;

- Compliance with the various codes of conducts (including the voluntary ones) and their own internal rules, policies and procedures.

Appointment of Compliance Officers (‘COs’)

Appointment of COs is required under different statutes. In case of listed entities, for the purpose of ensuring compliance with securities law, appointment of CO is specified in the initial listing regulations viz. SEBI ICDR[1], SEBI ILNCS[2] Regulations and the responsibility of CO for continuous listing requirement is included in the common obligations under LODR. In case of LODR the person is required to be a qualified Company Secretary (‘CS’) and in case of ILNCS, the CS of the issuer is required to be the CO. Similarly, the requirement under the Listing Agreement[3] was to appoint the CS of the issuer as the CO.

SEBI PIT Regulations (applicable to a listed entity as well as an intermediary/ fiduciary) requires appointment of a senior officer, who is financially literate and is capable of appreciating requirements for legal and regulatory compliance under PIT regulations as the CO, who reports to the board of directors and ensures compliance of policies, procedures, UPSI preservation, implementation of codes etc, under the overall supervisions of the board of directors.

Additionally, Banks, NBFCs, Insurance companies, SEBI registered intermediaries, etc all are required to appoint CO as per laws specifically applicable to the company operating in that particular sector.

Whether one person can serve as CO for each of the above requirements? This is surely feasible, unless there is an express bar. For e.g., in case of banking regs/ NBFCs regs, there is a bar on dual hatting – that is, the CO as per those laws should not be dealing with any other line function.

Position of CO under LODR post amendment

It may be contended that the role of a CS is a mix of compliance and ministerial functions. He/ she may be tasked with several other functions as well – depending on the organization. The provision of the LODR Regs is obviously not concerned with either other functions performed by the CO, nor with other compliance roles.

The intent of the provision, as we read it, is that the compliance function pertaining to LODR Regs is directly discharged by the CO under the supervision of the board of directors. The board has the supervisory responsibility, and the CO has the executive responsibility. The provision is intended to attach significance to the organisation-wide role of compliance function.

As observed from the report of the Expert Committee, recommendations were made for strengthening the position of the CO. The challenge faced by the CO, despite forming part of ‘senior management’, was inability to advise the management to act in accordance with the law and being in a position to get influenced by other people in senior management due to the reporting structure. Therefore, the suggestion was for appropriate positioning to get adequate power, commensurate with the responsibilities cast upon the CO, to be able to advise the management on points of law and ensure effective discharge of statutory duties and responsibilities.

In the light of above, the regulations now clarify the position of the CO by having them one level below the board of directors. Here the intent of the regulator, in our reading, did not seem to define the organisational structure, but to clear the path for the CO for effective discharge of its responsibilities. In our view, the amendment results in fixing the responsibility of the CO and that the CO, now, cannot shirk its responsibility or cannot take the pretext of being a junior person, having no power or access, having a reporting line limited to someone in senior management. It now provides the CO with straight access to the board of directors, when it comes to ensuring compliance with LODR requirements. To the extent of the compliance function the CO will now be directly accountable to the board.

The way we read this requirement is that it certainly attaches significance to the compliance function, and therefore, may result in repositioning of compliance officers in the organization hierarchy. But is the law concerned with organisation hierarchy, designations, scales, ranks, etc? In our view, the objective of the law is attained by a functional reporting line to the board. This is also evident from SEBI’s analysis of the suggestions/ comments received,[4] that the objective is to empower COs to perform their duties and discharge their responsibilities effectively. Some companies do have the practice of having a CO report to the Managing Director / CEO. However, it is for the listed entity to decide the reporting structure of its KMPs and senior management while ensuring compliance with the regulatory requirements.

However, SEBI has issued a Circular dated April 1, 2025, where SEBI states: “it is clarified that the term ‘level’ used in regulation 6(1) refers to the position of the Compliance Officer in the organization structure of the listed entity. Therefore, ‘one level below the board of directors’ means one level below the Managing Director or Whole-time Director (s) who are part of the Board of Directors of the listed entity.” After issuing this Circular, SEBI staff has also issued two Informal Guidance letters, being for DCB Bank Ltd and Pakka Ltd.

Hence, SEBI seems to be clearly opining that SEBI is intending the organisational hierarchy of the entities to also be adjusted to reflect the CO’s position at one level below the board.

Reporting structure of CO post amendment

Organizational hierarchy is a matter of many things. Regular reporting structure for the various functions that a position has: lines of authority and responsibility, scales and other benefits related to the scale, promotion policies, regular administrative roles such as approval of claims, benefits, etc

The CO stands empowered to manage the compliance function independently and without fear, and to that extent the CO needs to report to the board. However, boards meet infrequently. The company may or may not have an MD/ WTD – it may be working with a CEO/president reporting to the board. It is quite possible in an organisation to have one or more WTDs who report to the MD. There are several officers who report to the MD but their level in the organisation is not the same as those of other seniors placed at one level below the board. In such cases, whether the CO reporting to an MD is a sufficient compliance? SEBI’s IG, specifically in the matter of DCB Bank Ltd , seems to answer in the negative. Therefore, SEBI suggests the organisational levels also to align to the expected reporting lines. Therefore, the amendment, seen in the SEBI’s circular of 1st April, is concerned with both reporting lines as well as organisational hierarchy of the CO. Irrespective of the SEBI Board agenda dated 30th September, 2024 stating that organisational structure is an internal matter for companies, “…it is for the listed entity to decide the reporting structure of its KMPs and senior management while ensuring compliance with the regulatory requirements”, it seems that the regulator has done so in the 1st April 2025 circular. Although, in general, the organisational hierarchy usually corresponds to and is commensurate with functional hierarchy; however, the law has sought to interfere with the organisational structure.

CS as CO under LODR

Does the amendment necessitate a relook on whether the CS can continue as CO? The answer to this also seems negative, as law only prescribes who can be the CO. SEBI has also clarified that the CO and CS may be different persons. While law admits having different persons occupying the position, practically, it seems less feasible in view of the overlap and interconnectedness in the functions discharged by a CS in terms of Companies Act, 2013 and by a CO under LODR.

Actionable for listed entities

The amendment is certainly required to be sensitised to the board of directors. However, do the regulations expect companies across the country to revisit their organisational structures? SEBI has expressed its views in the 1st April, 2025 circular. Therefore, listed entities need to evaluate if the functional level and organisational level of the CO is in line with the regulatory requirements and expectations. If no, listed entities may want to revisit the same.

Power brings onus

Everyone may also readily understand that SEBI’s intent in empowering the CO is not just to confer a new power, but to be able to hold the CO answerable for any compliance gaps. Therefore, if it is a new cap that the CO is donning, the cap is made of flowers and nettles both.

[1] Reg 23 (8) ICDR – The issuer shall appoint a compliance officer who shall be responsible for monitoring the compliance of the securities laws and for redressal of investors’ grievances.

[2] Reg 27 (4) of ILNCS – The lead manager(s) shall ensure that the draft offer document clearly specifies the names and contact particulars including the postal and email address and telephone number of the compliance officer who shall be a Company Secretary of the issuer.

[3] The requirement was notified on May 18, 1999 pursuant to the recommendations of the Accounting Standards Committee constituted by SEBI under the Chairmanship of Shri Y. H. Malegam to the effect that Compliance officer to be appointed by Listed companies in Compliance with Circular No. SMD/POLICY/CIR-06/98 dated February, 12, 1988 (every company shall appoint a Senior Officer as Compliance Officer) shall be the Company Secretary of the Company.

[4] Agenda of SEBI BM dated September 30, 2024 [Clause (iii) (a) of Para 28.3.2].

Other Resources on LODR:

SEBI proposals to ease overheated SME IPO market

SEBI proposes amendments in ICDR and LODR Regulations owing to recent concerns around SME listing

– Sakshi Patil, Executive and Sourish Kundu, Executive| corplaw@vinodkothari.com

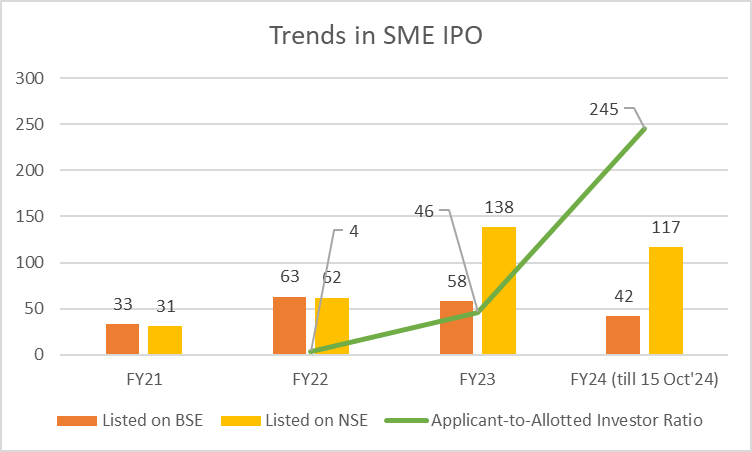

SME IPOs are constantly increasing at an evergrowing rate, with 31 companies listed on SME in FY 21-22 to a total of 138 companies listed in FY 23-24, and 117 companies already listed on SME as of the current FY (till 15th October, 2024) on NSE alone. Not only the number of SME IPOs, the investor participation in such IPOs has also increased substantially, with the applicant to allotted investor ratio from 4X in FY 22 to 46X in FY23 and 245X in FY24. A data on the SME listings during the current and previous FY suggests that, while majority of listed SMEs have booked listing gains, approx 20-30% of such entities have subsequently witnessed a price drop (39 out of 224 companies listed on NSE, 26 out of 91 companies listed on BSE1).

The recent surge in SME IPOs over the last few years, including substantial investor participation in such IPOs, coupled with the recent regulatory concerns w.r.t. diversion of issue proceeds, funding to shell companies, misinflation of revenues etc. has required a re-look into the existing regulatory universe under which SMEs are listed and operate post listing. In August 2024, an advisory was also issued by SEBI regarding investment in the securities of entities listed on SMEs. NSE rolled out stricter eligibility criteria effective September 1, 2024. Greater emphasis on positive cashflow pre listing (w.e.f. Sept 1), capping of 90% over issue price during special pre-open session for SME IPO (w.e.f. July 4) signal the emphasis for investor protection. Following the same, a Consultation Paper has been issued by SEBI, proposing amendments to the provisions of ICDR and LODR Regulations, with a view to strengthen the pre and post-listing requirements for SMEs. Key proposals include restricting the access of SME Exchange to informed investors, and ensuring such IPOs serve the original purpose of making finance available to SMEs for their business growth, and not for funding the promoters’ requirements.

A brief of the 27 proposals, as against the existing requirements and our comments are presented below:

| Particulars | Existing requirement | Proposal under CP | Rationale and Our Comments |

|---|---|---|---|

| Stricter eligibility conditions for SME IPO | |||

| Ineligibility conditions for IPO (Proposal 8) | Currently based on PromotersDirectors Selling shareholders in some cases. | To be extended to promoter group as well. | SME companies are closely held by promoter and promoter groups. Hence, any action against the promoter group may also have a significant bearing on the issuer. |

| Additional eligibility requirements for SME IPO(Proposal 9A & 9B) | Firm/ LLP converted into company can apply for IPO without any cooling period – track record requirements are considered on a combined basis. | Co. which has been converted from LLP or partnership firm, shall be in existence for at least 2 yrs, with restated financial statements post conversion drawn in accordance with Schedule III of CA, 2013.Cooling off of 2 years in case of change of promoter, or introduction of new promoter acquiring 50% or more shareholding prior to filing of DRHP. | Helps in bringing a clearer picture of financial position post conversion. Cooling period in case of change in promoter is to bring steadiness in IPO.Track record should be based on the effective management of new promoter(s) and not past promoter(s). |

| Operating profits (EBIDTA)(Proposal 11) | Positive. | Rs. 3 cr for at least 2 out of 3 immediately preceding FYs. | To ensure financial viability of the company. Our Comments: NSE additionally mandates positive Free cash flow to Equity (FCFE) for at least 2 out of 3 financial years preceding the application. |

| Conversion of Pre-IPO outstanding convertible securities before IPO(Proposal 20) | Conversion not mandatory | Conversion mandatory | In line with the requirement for Main Board IPO. Provides clarity to investors on the company’s capital structure before they invest. |

| Structure of IPO and allotment | |||

| Minimum issue size(Proposal 10) | Not specified | Rs. 10 cr | To ensure companies with significant growth potential access the market.Loans and alternative funding sources typically cater to smaller amounts.Is aligned with BSE’s and NSE’s requirement for Main Board listing. |

| Offer for sale(Proposal 4A & 4B) | No restriction | Dual limits proposedOFS restricted upto 20% of issue size and for selling shareholders, OFS shall not exceed 20% of pre-issue shareholding on a fully diluted basis. | To prevent use of SME listing for dilution of promoter stake. |

| Face value(Proposal 12) | Not Specified | Rs. 10/- per share for existing issued capital and proposed new shares to be issued. | To enable better comparison amongst various issuers. |

| Minimum application size (Proposal 1) | Rs. 1 lakh | Rs. 2 lakh with existing minimum allocation of 35% (book-build issue)/ 50% (fixed price issue) to RIIs, ORRs. 4 lakh (resulting in deletion of RII category for minimum allocation requirements). | Limit participation of retail investors (bidding for upto Rs. 2 lakhs) to protect interest of smaller retail investors;Attract investors with risk taking appetite; Enhance the overall credibility of the SME segment. |

| Minimum no. of allottees (Proposal 3) | 50 | 200 | To ensure sizeable no. of investors Provide liquidity |

| Allotment methodology for Non – institutional investors (NII) category (Proposal 2) | Proportional allotment for NIIs | Draw of lots for minimum bid lot to NIIs divided into 2 categories: ⅓ rd of allocation for application size upto 10L⅔ rd of allocation for application size exceeding 10L | Align allocation methodology with Main Board IPO; Proportional allotment may encourage over-leveraging, over statement of interest and thus at times encourage mispricing. |

| Objects of issue & utilisation of proceeds | |||

| Raising funds for General corporate purpose (GCP) and unidentified acquisition (Proposal 7A & 7B) | GCP < – 25% of issue sizeGCP + unidentified acquisition < – should not exceed 35% of issue size | GCP restricted to lower of 10% of issue size or Rs. 10 cr;Prohibition on raising funds for unidentified acquisition | To reduce the risk of misuse of issue proceeds |

| Repayment of loan of promoter/ promoter group as an object of issue(Proposal 14) | No express prohibition. | Not allowed | To ensure that funds raised through IPO are used for business growth, not for repayment of promoters’ liabilities |

| Funding for working capital (Proposal 15) | No specific requirement | Mandatory statutory auditor certificate on a half-yearly basis for use of working capital funds raised exceeding Rs. 5 Crore, with disclosure of the same in financial statements. | Ensures that working capital funds are appropriately used Our Comments: The requirement of statutory auditor’s certificate is proposed to be made mandatory for all SME IPOs where a monitoring agency is not required to be appointed (see below). A specific mandate for working capital monitoring may not serve any additional purpose. |

| Monitoring of issue proceeds (Proposal 5A, 5B & 5C) | Monitoring agency mandatory if issue size >100 cr | Monitoring agency mandatory if: Issue size >20 cr ORObject of issue includes:funding subsidiary, repay loans/ borrowing of the subsidiary investment in JV/ subsidiaryacquisition In other cases, utilization certificate from statutory auditor on half-yearly basisPlace before AC and board Submit to stock exchange | Reduce risk of misuse or diversionBring more transparency for investors and accountability for issuer Our Comments: Presently, Reg 32(5) of LODR requires statutory auditors to certify the statement w.r.t. Utilisation of funds on an annual basis. The proposal will additionally require the same to be done on a half-yearly basis, in cases where a monitoring agency is not required to be appointed. |

| Disclosure of sources in case of requirement of having firm arrangement of finance for a project(Proposal 16) | No such requirement | Sanction letter to be disclosed in draft offer document and offer document where partial funding is by bank/NBFCs. | Additional diligence and disclosure for investors w.r.t. project appraisal by financial institutions. |

| Exit opportunity for dissenting shareholders in case of change in objects(Proposal 23) | No specific provision | Post-listing exit opportunity for dissenting shareholders in case of changes in the objects or terms, in line with Main Board provisions | Protects the interests of dissenting shareholders, ensuring they have an exit option in case of significant changes post-listing. |

| Promoter contribution and lock-in requirements | |||

| Lock-in of promoter holding(Proposal 6A & 6B) | Minimum Promoter Contribution (MPC) – 3 yrs Excess holding – 1 yr | MPC – 5 yrsExcess – Lock in on 50% to be released after 1 yr and;For remaining 50% to be released after 2 yrs. | To ensure that entire holding is not diluted post the lock in periodTo ensure promoter continues to have skin in game till company is on SME Exchange |

| Securities ineligible for MPC(Proposal 24) | No clarification w.r.t. adjustment of price for corporate action | Price per share for determining MPC eligibility should be adjusted for corporate actions (e.g., bonus, stock split) | Clarifies the pricing mechanism and ensures fairness in determining MPC eligibility, preventing manipulation through corporate actions. |

| Other additional disclosures | |||

| Disclosure of senior level management(Proposal 17) | KMP and SMP details are required to be disclosed in offer document | Disclosure of senior-level employees (e.g., head of sales, plant head, etc.), with their experiencesAdditional disclosure on ESIC/EPF detailsSite visit by merchant banker to form part of DD report and included in material inspection documents in offer document. | Better disclosure w.r.t. Employee strength of the company |

| Merchant banker fees(Proposal 18) | No requirement to disclose issue related fees | Merchant banker fees, by any name, to be disclosed in RHP | Increased transparency – presently such costs exceeds 30-40% of issue size, defeating the primary purpose of fundraising |

| Public comments on DRHP (Proposal 19) | No requirement. | At least 21 days’ for public comments; Disclose on website of SEs and lead managers;Public announcement in 3 newspapers – English, Hindi and regional. | Allows the public to provide feedback during draft offer document stage instead of opening of offer |

| Due diligence certificate by merchant banker(Proposal 21) | Required at the time of submission of offer document to SEs. | Mandatory submission to SE at the time of filing draft offer document. | Ensures that the due diligence process is completed and certified before the public sees the draft offer document. |

| Migration to Main Board | |||

| Migration from SME to Main Board(Proposal 13) | Post-issue face value of capital > Rs. 25 crores pursuant to fresh issue. | Where listed SME is not eligible to migrate, fund raising to be still permitted beyond Rs. 25 crores, subject to compliance with corporate governance norms and disclosure requirements under LODR. | Ensures that company can remain listed on SME platform having post issue face value more than 25cr with light touch of regulations applicable to them related to LODR |

| Corporate Governance Requirements | |||

| Related Party Transactions(Proposal 25) | Exempt from Reg 23 pursuant to Reg 15(2)(b). Compliance as per Companies Act applicable: Meaning of RP [as per section 2(76)]Approval of AC (for all RPTs)Approval of Board (for specified transactions if not in ordinary course or arm’s length)Approval of shareholders (for material RPTs requiring board approval as above) | Reg 23 to be made applicable to SME listed entities.De minimis exemption continues for smaller listed entities [Reg 15(2)(a)]Material RPTs based on turnover thresholds (10% of annual consolidated turnover)Absolute limits of Rs. 1000 crores not applicable. | Enhanced requirements to mitigate risk of circular transactions and abusive RPTs |

| Quarterly corporate governance report [Reg 27](Proposal 26) | Not applicable | Quarterly disclosure w.r.t. composition and meetings of the board and its committees to the stock exchange(s) | Harmonize disclosure requirements for SME and Main Board entitiesEnhancing transparency on functioning of board and committee Our comments: The CP mentions about disclosure of board and committees, however, it is not clear as to whether the other disclosures as are applicable to Main Board entities under the corporate governance report, is also proposed to be extended to SMEs |

| Periodic filings to stock exchanges(Proposal 27) | Half yearly filing of:: Shareholding pattern [Reg 31], Statement of deviation(s) or variation(s) [Reg 32],Financial Results [Reg 33] | To be made on a quarterly basis, at par with Main Board listed entities. | Reflects the financial health and fund utilization by companies; Aligned with requirements applicable to the Main Board. |

Our related resources:

- NSE tightens eligibility criteria for SME listing on NSE Emerge

- BSE and NSE SME Exchange Platforms: Big Opportunities for Small Companies and growing India

- The basics of bringing an IPO

- Based on market data as on 15th October, 2024. Taken from SEBI CP

↩︎

SDD non-compliance to entail stringent action from exchanges

Lavanya Tandon, Executive | corplaw@vinodkothari.com

Our related resources on the topic-

DPs to furnish periodic & continual disclosures for units of its own mutual fund to AMC

Shaivi Bhamaria, Associate & Sakshi Patil, Executive | corplaw@vinodkothari.com

Loading…

Loading…

Refer to our related resources below:

FAQs on Specific Due Diligence of investors & investments of AIFs

Team Vinod Kothari & Company | corplaw@vinodkothari.com

Refer to our related resources below:

- Trust, but verify: AIFs cannot be used as regulatory arbitrage (updated as on October 9, 2024)

- AIFs ail SEBI: Cannot be used for regulatory breach

- Cat I & II AIFs can borrow to meet temporary shortfall in investment drawdown

- RBI bars lenders’ investments in AIFs investing in their borrowers

- Some relief in RBI stance on lenders’ round tripping investments in AIFs

SEBI rationalises offer document contents and certain timelines for NCD public issuance

– Palak Jaiswani, Manager & Garima Chugh, Executive | corplaw@vinodkothari.com

Loading…

Read More:

- Disclosure requirements w.r.t. debt securities | Amendments in LODR & NCS Regulations

- SEBI proposes to ease compliance for issuers of non-convertible securities (NCS) | Consultation Paper

- Introducing common offer document disclosures for Private Placement and Public Issue

- EoDB measures for debt-listed entities: Consultation Paper on Listing Regulations