Posts

Presentation on Controls over RPTs.

Read more on RPTs here.

Downstream investment to be treated at par with FDIs

Introduction

The Master Direction on Foreign Investment in India, recently updated on January 20, 2025, goes beyond a mere consolidation of the recent amendments in the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (‘NDI Rules’), providing clarifications in several areas of legislative silence. One of the key areas of clarification include the rules around downstream investments.

In this note, we have discussed downstream investment through stock deals and other significant clarifications provided in the Master Direction.

Background

Rule 6(a) of the NDI Rules deals with the investment by a person resident outside India (‘PROI’) in the equity instruments of an Indian company. The said rule refers to Schedule I, which, amongst others, specifies the modes of payment of consideration. Prior to the FEM (Non-Debt Instruments) (Fourth Amendment), Rules, 2024 dated August 16, 2024 (“Fourth Amendment Rules”), the Schedule contained an enabling provision for Indian companies to issue its equity instruments to PROI by way of swap of equity instruments. Since the term “equity instruments”, as defined under Rule 2(k) of Principal NDI Rules, means equity shares, convertible debentures, preference shares and share warrants issued by an Indian company, the provision permitting share swaps was read narrowly to refer to swap of shares of an Indian company against that of another Indian company only.

However, pursuant to the Fourth Amendment Rules, the Schedule was further amended to expressly provide for the swap of equity capital, as defined under rule 2(1)(e) of Foreign Exchange Management (Overseas Investment) Rules, 2022. The same is defined as “equity shares or perpetual capital or instruments that are irredeemable or contribution to non-debt capital of a foreign entity in the nature of fully and compulsorily convertible instruments.”

Downstream investment, on the other hand, is governed by the provisions of Rule 23 of the NDI Rules. While the said rule specified certain requirements to be complied with in the context of downstream investment, including the sources through which funds can be brought in for the purpose of such investments, the rule neither explicitly provided for the share swaps as a permitted mode of payment, nor contained any reference to Schedule I of the NDI Rules. As a result there was uncertainty among industry stakeholders on permissibility of share swaps as a form of consideration in case of downstream investment.

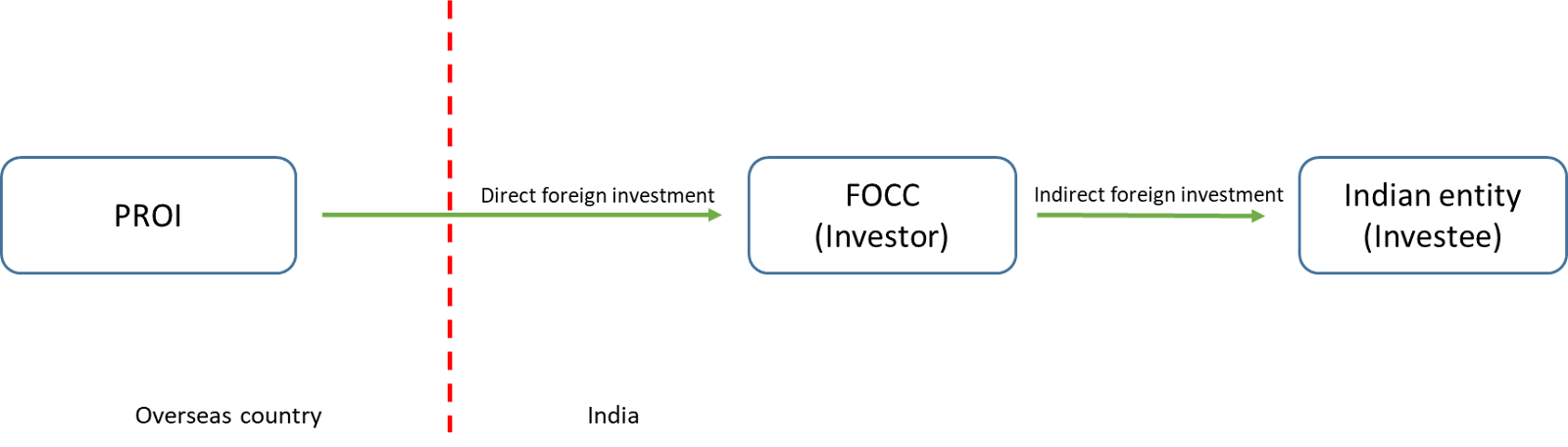

Meaning of Downstream Investment

The explanation to Rule 23 (also contained in Para 9.1.13 of the Master Direction) states that:

Downstream Investment is an investment made by an Indian entity which has received foreign investment or an Investment Vehicle in the equity instruments or the capital, as the case may be, of another Indian entity.

In other words, when an Indian entity owned or controlled by PROI [commonly referred to as a Foreign Owned and Controlled Entity (FOCC)] makes investments in the equity instruments/ capital of an Indian entity, such an investment will be considered as downstream investment for the PROI. Such arrangements enable PROI to hold investment in other Indian entities indirectly, thus, considered as an indirect foreign investment. As a result, the restrictions, prohibitions and limitations as applicable to direct foreign investments will be applicable at the time of downstream investment as well. For better understanding, refer to the figure below:

Guiding principle on downstream investment: what cannot be done directly, shall not be done indirectly

The recent updates in the Master Directions provide for the guiding principles of downstream investments, thereby clarifying that all permissions and prohibitions vis-à-vis direct foreign investment under the NDI Rules will be applicable to indirect foreign investment (i.e. downstream investment) as well.

Para 9 of the Recent Master Direction reads as below:

“The guiding principle of the downstream investment guidelines is that “what cannot be done directly, shall not be done indirectly”. Accordingly, downstream investments which are treated as indirect foreign investment are subject to the entry routes, sectoral caps or the investment limits, as the case may be, pricing guidelines, and the attendant conditionalities for such investment as laid down in the NDI Rules.”

Giving reference to above guiding principles, the Master Directions explicitly refers to the permissibility of the arrangements which are available for direct investment such as investment by way of swap of equity instruments/equity capital, payment arrangements/mechanism as per Rule 9(6) of the Rules etc, for the purpose of downstream investment as well.

Implication of above clarification

The above clarification has paved a way for Foreign Owned or Controlled entities (FOCC) to make further investments in Indian entities by way of swapping equity capital of foreign companies held by it in addition to other sources as already available. This arrangement of swapping of securities is known as a stock deal.

Previously, for making downstream investment, an FOCC was allowed to raise fresh funds from abroad by way of issue of securities including non-convertible debentures or by utilising internal accruals such as profits after tax. For more clarity refer to the table below:

| Sources of making investment by FOCC in another Indian entity | Position prior to the clarification | After clarification |

|---|---|---|

| Internal accruals (i.e., profits transferred to reserve account after payment of taxes) | Allowed | Allowed |

| Fresh funds from abroad including issue of NCD | Allowed | Allowed |

| Swap of equity instruments/ capital | No express provision | Allowed |

| Using funds borrowed in the domestic markets | Not allowed | Not allowed |

Other conditions w.r.t downstream investment in light of the guiding principle

As per the guiding principle on downstream investments as discussed above, an Indian entity which has received indirect foreign investment is subject to permissions and prohibitions as applicable to direct foreign investment under NDI Rules. Further, the onus of ensuring such compliances are on the FOCC making such investments, and not on the Indian investee entity receiving such indirect FDI.

- Investment from land border sharing countries

In order to curb opportunistic takeovers/ acquisitions of Indian companies due to COVID-19 pandemic, the Government of India restricted investment from countries sharing land borders with India or where the beneficial owner of an investment into India is situated in or is a citizen of any such country, by way of issue of Press Note-3. As a result, any foreign direct investment from such countries would be permitted with prior approval of the Government of India in permissible sectors.

This will be applicable in case of investment by FOCC as well, where such FOCC, in turn, has received investment from such countries as discussed above.

- Deferred payment arrangements

Similarly, the facility of making deferred payment of up to 25% in case of transfer of equity instruments between PROI and Person Resident in India (PRI) will also be applicable in case of downstream investment. This is, subject to the compliance with the conditions as laid down in Rule 9(6) of the NDI Rules.

The Master Directions further state that a transaction intended to be undertaken using above arrangement(s) shall require the share purchase/transfer agreement to contain the respective clause and related conditions for such arrangement.

- Subsequent classification as downstream investment

Where an Indian entity (i.e., investor) at the time of making further investment in another Indian entity (i.e., investee) was not an FOCC at the time of investment, but subsequently becomes an FOCC, then such investment in another Indian entity would need to be reclassified as downstream investment from the date when investor entity becomes FOCC. Consequently, such downstream investment shall be in compliance with the applicable entry route and sectoral cap compliances and shall be required to be reported by the investor entity within 30 days from the date of such reclassification in form DI.

- Valuation requirement

As per para 8.4 of the Recent Master Direction, in case of swap of equity instruments, irrespective of the amount, valuation will have to be made by a Merchant Banker registered with SEBI or an Investment Banker outside India registered with the appropriate regulatory authority in the host country.

- Downstream Investment by NRI/OCI on non-repat. basis to be treated as domestic investment

The investments made by NRIs/OCIs on non-repatriation basis is treated as deemed domestic investment. Accordingly, an investment made by an Indian entity which is owned and controlled by a Non-Resident Indian or an Overseas Citizen of India including a company, a trust and a partnership firm incorporated outside India and owned and controlled by a Non-Resident Indian or an Overseas Citizen of India, on a non-repatriation basis in compliance with Schedule IV of these rules, shall not be considered for calculation of indirect foreign investment.

To know more about foreign investment, check out our YouTube repository on:

- Overview of Foreign Direct Investment

- Understanding the Downstream Investment

- Overview of Overseas Investment Rules

Reduction of capital – an alternate to buyback and minority exit?

– Payal Agarwal, Partner | corplaw@vinodkothari.com

Updated on March 26, 2026

Buyback was considered as one of the most effective means of scaling down of capital by a company and distribution of accumulated profits, until the tax law changes pursuant to the Finance Act, 2024 effective 1st October, 2024. With buybacks becoming ineffective, one may want to look at reduction of capital u/s 66 of the Companies Act, 2013 (‘Act’) as an alternate route for scaling down capital. In fact, the section has been worded in a manner that seems to suggest that the capital reduction procedure u/s 66 can serve various objectives, as also highlighted in various rulings of NCLT and NCLAT, including the Supreme Court.

Manner of capital reduction u/s 66

Section 66 of the Act reads as:

- Subject to confirmation by the Tribunal on an application by the company, a company limited by shares or limited by guarantee and having a share capital may, by a special resolution, reduce the share capital in any manner and in, particular, may—

XXX

Thus, the opening sub-section of the section seems to suggest that the share capital may be reduced in any manner, as the company may approve by a special resolution, upon confirmation by the NCLT.

However, the section is further followed by clauses specifying the manner in which the capital reduction may be effected.

(a) extinguish or reduce the liability on any of its shares in respect of the share capital not paid-up; or

(b) either with or without extinguishing or reducing liability on any of its shares,—

(i) cancel any paid-up share capital which is lost or is unrepresented by available assets; or

(ii) pay off any paid-up share capital which is in excess of the wants of the company,

alter its memorandum by reducing the amount of its share capital and of its shares accordingly:

(a) Extinguishment of uncalled capital

Clause (a) deals with extinguishment of uncalled capital. Hence, if a company has issued shares at a face value of say, Rs. 10 each, of which Rs. 8 per share has been paid-up, the company may reduce the share capital, by extinguishing the liability towards the uncalled and unpaid capital of Rs. 2 per share.

This results in a reduction in the face value of the share capital, although, no reduction in the voting rights or shareholding percentage of the shareholders, if effected proportionately for all the shareholders.

(b) (i) Cancellation of deteriorated capital

Clause (b)(i) deals with the capital that gets deteriorated on account of the deterioration in the value of the assets. This assists in reflecting the true value of the company by cancelling such value of the capital that is not represented by assets of equivalent value.

For instance, the face value of each share of the company is Rs. 100, represented by assets worth Rs. 80, for each share. In this case, the company may write-off its share capital to the extent of Rs. 20 per share.

(b) (ii) Payment of the excess paid-up capital available with the company

Clause (b)(ii) deals with the payment of capital that is in excess of the requirement of the company. This is similar to Clause (a), except that in case of the former, the capital was unpaid, and hence, there is no cash outflow in the hands of the company. In case of the latter, that is, under Clause (b)(ii), the capital having already been paid by the shareholders, the cancellation of the same requires payment on the part of the company to the shareholders.

Sources of payment for capital reduction

Where capital reduction is on account of the loss in the value of assets, the same would technically, not result in any payment from the company to its shareholders. In other cases, however, there is a cash outflow on the part of the company, and hence, it becomes relevant to understand the sources from which such payment can be made.

Capital reduction essentially means a reduction in the capital of the company, being excess than required, and hence, remaining unutilised. Further, in terms of Section 52 of the Act, the application of securities premium, except for the purpose as specified in sub-section (2) or (3) thereof, as applicable, constitutes a reduction in share capital.

Capital reduction as a means of profit distribution?

A part of the consideration may also be payable from the accumulated profits of the company, thereby, also leading to distribution of profits through capital reduction. However, the same is considered as deemed dividends, for income tax purposes, attracting tax implications, as discussed in later paragraphs below.

Capital reduction for consideration other than cash

The consideration payable on account of capital reduction need not necessarily be paid in cash, the same may also be paid through other means, that is, by distributing property owned by the company. In re Aavishkaar Venture Management Services Private Limited, the NCLT Mumbai affirmed the permissibility of capital reduction for consideration other than cash, against an observation of the Regional Director, Western Region, having reference to other judicial precedents.

Capital reduction by creation of liability in any other form

An extended and striking version of capital reduction for consideration other than cash is the creation of resultant liability in the hands of the shareholders against capital reduction. In Ulundurpet Expressways Private Limited, the NCLT Mumbai rejected the scheme of capital reduction, proposing capital reduction through creation of resultant loan to be repaid to the shareholders over a period of time. It was stated that:

“…the scheme of section 66(1)(b)(ii) of the Companies Act, 2013 only enables a company to pay off excess capital to its shareholders, which is considered in excess of wants of the company. The facts of the case clearly shows that such reduced share capital can not be said to be in excess of wants of the company on the date of passing of special resolution. Accordingly, such reduction is not permissible under the terms of Section 66(1)(b)(ii) of the Companies Act, 2013.”

The matter was put to appeal before NCLAT, that reversed NCLT’s order, thereby allowing such a scheme of capital reduction. The appellant had referred to two similar cases where the consideration was to be discharged over a period of time and was kept outstanding as a loan between the Company and its shareholders, and such a scheme had been approved by the NCLT Mumbai. NCLAT referred to various rulings in the context of capital reduction, and concluded that the same is permissible under section 66 allowing capital reduction “in any manner”, being a domestic issue. In Indian National Press (Indore) Ltd (1989) 66 Comp Cas 387 (MP), the High Court held:

“The need for reducing capital may arise in various ways, for example, trading losses, heavy capital expenses, and assets of reduced or doubtful value. As a result, the original capital may either have become lost or a company may find that it has more resources than it can profitably employ. In either case, the need may arise to adjust the relation between capital and assets. The company has the right to determine the extent, the mode and incidence of the reduction of its capital. But the court, before it proceeds to confirm the reduction of capital, must see that the interests of the minority and that of the creditors are adequately protected and there is no unfairness to it, even though it is a domestic matter of the company. The power of confirming or refusing to confirm the special resolution of a company to reduce its capital is conferred on the court in order to enable it to protect the interest of person who dissented or even of persons who did not appear, except on the argument and hearing of the petitioner.”

Other cases where the capital reduction has been effected through creation of liability to be discharged over a period of time include Tamil Nadu Newsprint & Papers Ltd (CP No. 17 of 1995) wherein redeemable non-convertible debentures were issued in consideration for reduction of capital, Dewas Bhopal Corridor Private Limited (CP No. 252 of 2022) and Godhra Expressways Private Limited (CP No. 254 of 2022) etc. NCLAT also cited various judgements stating capital reduction as a matter of domestic concern, discussed in the paragraph below.

Proportionate rule or selective reduction?

A question that has been raised time and again in the context of capital reduction is, whether the same needs to be effected in a proportionate manner for all the shareholders, or whether it can also be structured in a manner so as to selectively reduce/ extinguish the rights of some shareholders, thereby, reducing their overall holding in the company, including a complete buy-out of the minority shareholders.

Ruling disallowing minority buy-out through capital reduction

A recent ruling by NCLT Kolkata (pronounced on 19th September, 2024) in the matter of Philip India Ltd answers the aforesaid question of selective reduction in negative. The judgement considers the two clauses u/s 66(1) to conclude that Section 66 cannot be invoked for buying out the minority stake, and that the petition is liable to be dismissed since “…share capital reduction is only incidental to the main objective of buy back of shares…”

| Relevant clause of section 66 | Application to the case |

| Sec 66(1)(a) | Not applicable as the capital reduction is not sought for extinguishing or reducing the share capital that has not been paid-up |

| Sec 66(1)(b)(i) | Not applicable since nothing has been pleaded to show that the the reduction in share capital is for cancellation of paid-up capital, which is lost or unrepresented by available assets |

| Sec 66(1)(b)(ii) | Not applicable since it is not pleaded that they wanted to pay off capital which is in excess of the wants of the Company. In fact, there are borrowings/ liabilities in the balance sheet of the petitioner |

The matter has been appealed for and currently pending before the NCLAT.

Rulings allowing minority buy-out through capital reduction

While NCLT Kolkata disallowed selective capital reduction, there is a plethora of rulings – both under the existing 2013 Act and the erstwhile 1956 Act, as well as English rulings allowing selective capital reduction, where the same is not unfair or inequitable.

In British and American Trustee and Finance Corporation v. Couper, (1894) AC 399, the House of Lords of England held that:

“…if there is nothing unfair or inequitable in the transaction, I cannot see that there is any objection to allowing a company limited by shares to extinguish some of its shares without dealing in the same manner with all other shares of the same class. There may be no inequality in the treatment of a class of shareholders, although they are not all paid in the same coin, or in coin of the same denomination.”

The principle was reiterated in Poole v. National Bank of China, 1907 AC 229 and Westbern Sugar Refineries Ltd., (1951) 1 All. E.R. 881 (HL) etc.

“…the general rule is that the prescribed majority of the shareholders is entitled to decide whether there should be a reduction of capital, and, if so, in what manner and to what extent it should be carried into effect”

The principle has been followed and restated in various rulings of the Indian courts from time to time.

In Reckitt Berickiser (India) Ltd (2005) 122 DLT 612, the Delhi High Court approved the scheme of capital reduction resulting in paying off the minority public shareholders based on the aforesaid judicial dicta, while also laying down the principles for capital reduction in the following manner:

(i) The question of reduction of share capital is treated as matter of domestic concern, i.e. it is the decision of the majority which prevails.

(ii) If majority by special resolution decides to reduce share capital of the company, it has also right to decide as to how this reduction should be carried into effect.

(iii) While reducing the share capital company can decide to extinguish some of its shares without dealing in the same manner as with all other shares of the same class. Consequently, it is purely a domestic matter and is to be decided as to whether each member shall have his share proportionately reduced, or whether some members shall retain their shares unreduced, the shares of others being extinguished totally, receiving a just equivalent.

(iv) The company limited by shares is permitted to reduce its share capital in any manner, meaning thereby a selective reduction is permissible within the framework of law (see Re. Denver Hotel Co., 1893 (1) Chancery Division 495).

(v) When the matter comes to the Court, before confirming the proposed reduction the Court has to be satisfied that (i) there is no unfair or inequitable transaction and (ii) all the creditors entitled to object to the reduction have either consented or been paid or secured.”

The aforesaid has been referred to in various judgements such as in RS Livemedia Pvt Ltd, and Bombay Gas Company Ltd, thereby answering the question of permissibility of selective capital reduction in affirmative.

On the question of whether the special resolution which proposes to wipe out a class of shareholders (through capital reduction) after paying them just compensation can be termed as unfair and inequitable, the Bombay High Court, in Sandvik Asia Ltd. vs. Bharat Kumar Padamsi (2009) SCC Online Bom. 541 has answered in negative, having reliance on the judgment of the House of Lords in the case of British and American Trustee and Finance Corpn (supra). The Bombay High Court also referred to the judgment of the SC in Ramesh B. Desai v/s. Bipin Vadilal Mehta, (2006) 5 SCC 638 for the same.

“As the Supreme Court has recognised that the judgment of the House of Lords in the case of British & American Trustee and Finance Corporation Ltd. is a leading judgment on the subject, we are justified in considering ourselves bound by the law laid down in that judgment. As we find that there is similarity in the facts in which the observations were made in the judgment in the case of British & American Trustee and Finance Corporation, we will be well advised to follow the law laid down in that case.”

While the elimination of minority shareholders through payment of compensation has generally been upheld as permissible, courts have consistently underscored that such exit must be accompanied by fair and equitable compensation. Surprisingly, in Pannalal Bhansali v. Bharti Telecom Limited & Ors., the SC ruled to the contrary. A proposal of selective reduction was allegedly vitiated by several shortcoming such as the valuer having potential conflict of interest, valuation discounted in an unusual manner, procedural defects and precedents of higher valuation was opposed by the minority shareholders. However, the SC set aside these allegations holding that obtaining valuation report is not even a mandatory requirement u/s 66 of the Act. It was held by the SC that :

“32. Reduction of share capital can be achieved by a special resolution and confirmation by the Tribunal, without a report of valuation from an approved/registered valuer and hence, it does not fall within the ambit of a relevant material;….”

Further, in Brillio Technologies Pvt Ltd. vs ROC & RD, referring to various judgements including the ones cited above, the NCLAT held that:

“…Section 66 of the Companies Act, 2013 makes provision for reduction of share capital simpliciter without it being part of any scheme of compromise and arrangement. The option of buyback of shares as provided in Section 68 of the Act, is less beneficial for the shareholders who have requested the exit opportunity.”

The aforesaid ruling does not only permit selective reduction of capital, it expressly puts capital reduction u/s 66 as an alternative to buyback of shares u/s 68 where the former is more beneficial to the shareholders than the latter. The ruling has also been referred to by NCLT Mumbai in Reliance Retail Ltd.

Tax implications on capital reduction

Capital reduction qualify as “transfer” u/s 2(47) of IT Act

In order to qualify for taxability as capital gains, or claiming set-off of capital losses pursuant to a capital reduction, it is necessary that the transaction falls within the meaning of “transfer” u/s 2(47) of the IT Act. The term “transfer” has been defined in the following manner:

“transfer”, in relation to a capital asset, includes,—

(i) the sale, exchange or relinquishment of the asset ; or

(ii) the extinguishment of any rights therein ; or

XXX

The question of whether reduction of capital amounts to ‘transfer’ has been a matter of discussion before courts, including the Supreme Court in several instances. The Supreme Court has, recently (pronounced on 2nd January, 2025), in the matter of PCIT v. Jupiter Capital Pvt Ltd 2025 INSC 38 considered the matter at length and answered in affirmative. In the facts of the case, while the number of shares held by the shareholder assessee had reduced on account of capital reduction, the shareholding pattern remained the same, due to which the Assessing Officer concluded that there is no “extinguishment of rights”, thereby the capital reduction cannot amount as ‘transfer’ u/s 2(47) and no capital losses can be booked by the assessee on the same.

The Supreme Court, having regard to its judgement in previous matters concerning the question of whether capital reduction amounts to transfer, dismissed the petition filed by Revenue, thereby, allowing the assessee to claim capital loss.

Reference was made of the decision of Supreme Court in Kartikeya V. Sarabhai v. Commissioner of Income Tax, (1997) 7 SCC 524, where, on account of capital reduction, the face value of shares were reduced although the number of shares remained the same. The SC, having regard to its another decision in Anarkali Sarabhai v. Commissioner of Income-Tax, Gujarat 138 I.T.R. 437 (pertaining to redemption of preference shares) held that:

“Section 2(47) which is an inclusive definition, inter alia, provides that relinquishment of an asset or extinguishment of any right therein amounts to a transfer of a capital asset. While, it is no doubt true that the appellant continuous of a share capital but it is not possible to accept the contention that there has been no extinguishment of any part of his right as a share holder qua the company. It is not necessary that for a capital asset. Sale is only one of the modes of transfer envisaged by Section 2(47) of the Act. Relinquishment of the asset or the extinguishment of any right in it, which may not amount to sale, can also be considered as a transfer and any profit or gain which arises from the transfer of a capital asset is liable to be taxed under section 45 of the Act.”

The views expressed in Kartikeya V. Sarabhai (supra) was reiterated in the matter of CIT v. G. Narasimhan, 1999 (1) SCC 510.

In Anarkali Sarabhai (supra), it was held that both reduction of share capital and redemption of shares involve the purchase of its own shares by the company and hence will be included within the meaning of transfer under Section 2(47) of the Income Tax Act, 1961. Relevant excerpts are reproduced below:

The view taken by the Bombay High Court accords with the view taken by the Gujarat High Court in the judgment under appeal. In the judgment under appeal, it was pointed out that the genesis of reduction or redemption of capital both involved a return of capital by the company. The reduction of share capital or redemption of shares is an exception to the rule contained in Section 77(1) that no company limited by shares shall have the power to buy its own shares. When it redeems its preference shares, what in effect and substance it does is to purchase preference shares. Reliance was placed on the passage from Buckley on the Companies Acts, 14th Edn., Vol. I, at p. 181: “Every return of capital, whether to all shareholders or to one, is pro tanto a purchase of the shareholder’s rights. It is illegal as a reduction of capital, unless it be made under the statutory authority, but in the latter case is perfectly valid.”

In Commissioner of Income Tax v. Vania Silk Mills (P.) Ltd, (1977) 107 ITR 300 (Guj) the expression “extinguishment of any right therein” has been interpreted in a wider fashion.

14. The word “extinguishment” is the kingpin of this expression. It is a word of ordinary usage having the widest import. Usually it connotes the end of a thing, precluding the existence of future life therein (see Black’s Law Dictionary, fourth edition, page 696). It has been variously defined as meaning a complete wiping out, destruction, annihilation, termination, cancellation or extinction and it is ordinarily used in relation to right, title, interest, charge, debt, power, contract, or estate (see Corpus Juris Secundum, volume 35, page 294). In Rawson’s Pocket Law Lexicon, the meaning assigned to it is : “the destruction or cessation of a right either by satisfaction or by the acquisition of one which is greater”. In Ramanlal Gulabchand Shah v. State of Gujarat AIR 1969 SC 168 at page 175, the word “extinguishment”, which is employed in conjunction with the expression “of any such rights” in Article 31A of the Constitution, was interpreted as meaning ” complete termination of the rights “.

15. The word “extinguishment” is here used in a similar context, namely, in combination with the expression “of any rights therein”. This expression again has a wide ambit and coverage. The word “therein” refers to “capital asset” mentioned earlier in the definition. So far as the expression “any rights” is concerned, it was observed by this court in Commissioner of Income-tax v. R.M. Amin [1971] 82 ITR 194 at page 201, while interpreting this very provision :

” ……the word ‘ any ‘ is a word which ordinarily excludes limitation or qualification and it should be given as wide a construction as possible, unless, of course, there is any indication in the subject-matter or context to limit or qualify the ordinary wide construction of that word……There being no contrary intention in the subject-matter, or context, the words ‘any rights’ must include all rights……”

16. It was there pointed out that where the capital asset consists of incorporeal property, such as a chose-in-action, the bundle of rights which constitutes such incorporeal property would be comprehended within the meaning of the words “any rights”. It would thus appear that the expression. “any rights therein ” is wide enough to take in all kinds of rights–qualitative and quantitative–in the capital asset.

In view of the judgements cited above, the SC held that:

“…the reduction in share capital of the subsidiary company and subsequent proportionate reduction in the shareholding of the assessee would be squarely covered within the ambit of the expression “sale, exchange or relinquishment of the asset” used in Section 2(47) the Income Tax Act, 1961.”

Distribution of accumulated profits taxable as “dividend”

Reduction of capital results in extinguishment of some rights on the part of the shareholders, and hence, can be construed as “transfer” within the meaning of sec 2(47) of IT Act, resulting in the tax implications u/s 54 (capital gains or loss, as the case may be).

However, as stated above, some part of the consideration may be paid out of the accumulated profits of the company. To that extent, the consideration received by the shareholders is taxable as dividend u/s 2(22)(d) of the IT Act. The section reads as below:

(22) dividend includes –

XXX

(d) any distribution to its shareholders by a company on the reduction of its capital, to the extent to which the company possesses accumulated profits which arose after the end of the previous year ending next before the 1st day of April, 1933, whether such accumulated profits have been capitalised or not;

Thus, to the extent the consideration for capital reduction is paid from the accumulated profits of the company, the same would be taxable as dividend in the hands of the shareholders. In Commissioner of Income-Tax v. Urmila Remesh, 230 ITR 422, the Supreme Court clarified that:

Section 2(22) of the Act has used the expression `accumulated profits’ Whether capitalised or not”. This expression tends to show that under Section 2(22) it is only the distribution of the accumulated profits which are deemed to be dividends in the hands of the share-holders. By using the expression “whether capitalised or not” the legislative intent clearly is that the profits which are deemed to be dividend would be those which were capable of being accumulated and which would also be capable of being capitalised. The amounts should, in other words, be in the nature of profits which the company could have distributed to its share-holders. This would clearly exclude return of part of a capital to the company, as the same cannot be regarded as profit capable of being capitalised, the return being of capital itself.

This was further reiterated in the matter of G. Narasimhan (supra).

Whether the new buyback taxation rule applies on capital reduction?

In various rulings, capital reduction has been employed as a means to buy back the shares of the minority investors. Therefore, a question arises on whether the new taxation rule on buyback (refer our article here) would apply to capital reduction as well.

Here, reference may be made to the language of Section 2(22)(f) of the IT Act, that reads as:

(f) any payment by a company on purchase of its own shares from a shareholder in accordance with the provisions of section 68 of the Companies Act, 2013 (18 of 2013)

The provision, thus, clearly refers to buyback u/s 68 of the Act, whereas, capital reduction is effected u/s 66 of the Act. On the other hand, distribution of profits on capital reduction is explicitly covered u/s 2(22)(d) of the IT Act. Hence, there is no reason one should take a view that the new rules on taxation of buyback also extends to capital reduction.

Illustration showing tax implications upon capital reduction

The below table contains a few illustrations with respect to the tax implications upon reduction of capital.

| Sl. No. | Particulars | Part consideration from accumulated profits & Capital gains | Capital loss on account of capital reduction | No consideration paid on capital reduction |

| Amount (Rs.) | Amount (Rs.) | Amount (Rs.) | ||

| A. | Consideration received on capital reduction | 1,00,000 | 10,000 | – |

| B. | Amount paid out of accumulated profits | 30,000 | – | – |

| C. | Amount taxable as deemed dividends u/s 2(22)(d) [(B)] | 30,000 | – | – |

| D. | Cost of acquisition of shares | 20,000 | 20,000 | 20,000 |

| E. | Amount taxable as capital gains/ (loss) [(A) – (C) – (D)] | 50,000 | (10,000) | (20,000) |

Conclusion

The aforesaid discussion reveals how capital reduction has been given the widest possible meaning by the courts and tribunals, in the interpretation of the expression “in any manner”. Capital reduction can be used in scaling down the capital in any manner, so long as the same is (i) not unfair or inequitable to the shareholders and creditors, and (ii) duly approved by the shareholders through a special resolution. Though the process requires an approval of NCLT, the role of the Tribunal is supervisory in nature, since the matter is one of “a domestic affair”.

Our other resources on the subject:

[1] Read a detailed article on the same at Bye Bye to Share Buybacks

FAQs on Business Responsibility and Sustainability Report (BRSR)

Team Corplaw | corplaw@vinodkothari.com

Closure and Scaling Down of Business

Refer our related resources:

Affixing Vicarious Liability on Directors: See a Breakthrough

Introduction:

It is well established that a company, being an artificial legal entity, conducts its day-to-day operations through a collective body of individuals known as the Board of Directors. This body bears direct responsibility for the company’s functioning and decision-making. Consequently, in instances of default, both the company and its directors are often held accountable. Under Section 2(60) of the Companies Act, 2013 (hereinafter referred to as “the Act”), directors can be designated as “officers who are in default,” thereby making them personally liable in specific situations.

Despite its artificial nature, a company is recognized as a separate legal entity under the law. Therefore, for any offence committed by a company, it is primarily the company itself that is liable to face legal consequences. However, this fundamental principle is sometimes overlooked, and directors are held accountable for the corporation’s adverse actions. This stems from the perception that directors act as the “mind” of the company and control its operations.

Recently, the Supreme Court of India, in Sanjay Dutt & ORS. v. State of Haryana & ANR (Criminal Appeal No. 11 of 2025), reaffirmed the distinction between the company’s liability and that of its directors. This decision underscores the importance of adhering to the principle of separate legal personality, ensuring that directors are not unfairly held liable unless their personal involvement or negligence in the offence is established.

Brief facts of the Case:

The case under discussion revolves around a complaint lodged under the Punjab Land Preservation Act, 1900 (PLPA) against three directors of a company, alleging environmental damage caused by uprooting trees using machinery in a notified area. The appellants (directors of Tata Realty and related entities) sought to quash the complaint, asserting that the alleged actions were conducted by the company and not attributable to them personally. The complaint, however, excluded the company as a party and focused on the directors’ liability under Section 4 read with Section 19 of the PLPA.

Key observations by the Supreme Court:

- Primary Liability of the Company: The Court emphasized that the company itself, as the licensee and beneficiary of the land, was primarily liable for any violations. Excluding the company from the complaint undermined the case’s premise.

- Vicarious Liability Not Automatic: The Court reiterated that directors cannot be automatically held vicariously liable unless the statute explicitly provides for such liability or there is evidence of their personal involvement in the offence.

- Lack of Specific Allegations: The complaint failed to attribute specific actions or responsibilities to the directors. It merely assumed liability based on their official positions, which is insufficient for criminal prosecution.

- Legal Fiction Requires Explicit Provision: Vicarious liability in criminal matters requires clear statutory backing. The PLPA contains no provisions imposing vicarious liability on directors for offences committed by the company.

Understanding the Concept of Vicarious Liability:

The concept of vicarious liability allows courts to hold one person accountable for the actions of another. This principle is rooted in the idea that a person may bear responsibility for the acts carried out by someone under their authority or on their behalf. In the corporate context, this doctrine extends to holding companies liable for the actions of their employees, agents, or representatives.

Initially developed within the framework of tort law, the doctrine of vicarious liability later found application in criminal law, particularly in cases involving offences of absolute liability. This marked a departure from the once-prevailing notion that corporations, as artificial entities, could not commit crimes. Modern legal interpretations now recognize that a corporation may be held criminally liable if its human agents, acting within the scope of their employment, engage in unlawful conduct.

Doctrine of Attribution:

Currently, a company does not have the immunity to safeguard itself under the blanket of laxity of mens rea, an important component for the constitution of a criminal intent. It was established that corporations are liable for criminal and civil wrongdoings if the offences were committed through the corporation’s ‘directing mind and will’. This attribution of liability to the corporations is known as the ‘Doctrine of Attribution’

‘Doctrine of Attribution’ says that in the event of an act or omission leading to violation of criminal law, the mens rea i.e. intention of committing the act is attributed to those who are the ‘directing mind and will’ of the corporations. It can be said that Doctrine of Attribution is a subset of Principle of Vicarious Liability wherein a corporation can be held responsible even in case of a criminal liability.

The landmark judgment in H.L. Bolton (Engineering) Co. Ltd. v. T.J. Graham & Sons Ltd., (1957 1 QB 159) provided a foundational understanding of corporate liability. The court compared a corporation with a human body, with its directors and managers representing the “mind and will” of the organization. These individuals dictate the company’s actions and decisions, and their state of mind is legally treated as that of the corporation itself. Employees or agents, by contrast, are viewed as the “hands” that execute tasks but do not represent the company’s intent or direction.

This conceptual framework underscores that while corporations are artificial entities, they can be held criminally liable when those who embody their directing mind commit offences. The recognition of corporate criminal liability has since evolved, balancing the need for accountability with the distinction between the roles of employees and the decision-makers within an organization.

You can read more about the corporate criminal liability here.

Analyzing the Sanjay Dutt Judgment:

- Liability must be expressly mentioned

In the present case, the Court underscored the principle that vicarious liability cannot be imposed on directors or office-bearers of a company unless explicitly provided by statute. This was reiterated in Sunil Bharti Mittal v. Central Bureau of Investigation, (AIR 2015 SC 923) where it was held that individual liability for an offence must be clearly established through direct evidence of involvement or by a specific statutory provision. Without such statutory backing, directors cannot be presumed vicariously liable for a company’s actions.

The Court further emphasized that statutes must clearly define the scope of liability and the persons to whom it applies. This clarity is essential to prevent ambiguity and ensure that only those genuinely responsible for the offence are held accountable.

- Personal involvement of Directors :

The Court reaffirmed that corporate liability does not inherently extend to directors unless supported by statutory provisions or evidence of personal involvement. In Pharmaceuticals Ltd. v. Neeta Bhalla and Anr. (AIR 2005 SC 3512), it was held that directors are not automatically vicariously liable for offences committed by the company. Only those who were directly in charge of and responsible for the conduct of the company’s business at the time of the offence may be held liable.

The judgment further emphasized that liability must stem from personal involvement or actions beyond routine corporate duties. Routine oversight or general authorization does not suffice to establish criminal liability unless it can be shown that the director personally engaged in, or negligently facilitated, the unlawful act.

- ‘In charge of’ and ‘responsible to’

In K.K. Ahuja vs V.K. Vora & Anr. (2009 10 SCC 48), the Supreme Court analysed the two terms often used in vicarious liability provisions, i.e., ‘in charge of’ and ‘responsible to’. It was held that the ‘in-charge’ principle presents a factual test and the ‘responsible to’ principle presents a legal test.

A person ‘responsible to’ the company might not be ‘in charge’ of the operations of the company and so in order to be vicariously liable for the act, both the principles must satisfy. It stated as, “Section 141 (of the Negotiable Instrument Act, 1881), uses the words “was in charge of, and was responsible to the company for the conduct of the business of the company”. There may be many directors and secretaries who are not in charge of the business of the company at all.”

- The Complainant’s Burden of Proof:

Under Section 104 of the Bharatiya Sakshya Adhiniyam, 2023, the burden of proof lies on the complainant. It is the complainant’s responsibility to make specific allegations that directly link a director’s conduct to the offence in question. This principle was reiterated in Maksud Saiyed v. State of Gujarat (AIR 2007 SC 332), where the Court held that vague or generalized accusations against directors are insufficient.

A valid complaint must include:

- Clear and specific allegations detailing the director’s role in the offence.

- Evidence linking the director’s actions to the company’s criminal liability.

- Statutory provisions or legal grounds for attributing vicarious liability.

Referring to Susela Padmavathy Amma and M/s Bharti Airtel Limited (Special Leave Petition (Criminal) No.12390-12391 of 2022), wherein it was reaffirmed by the Supreme Court that even when statutes explicitly provide for vicarious liability, merely holding the position of a director does not automatically render an individual liable for the company’s offences.

To establish a director’s liability, the Court emphasized the need for specific and detailed allegations that clearly demonstrate the director’s involvement in the offence. It must be shown how and in what manner the director was responsible for the company’s actions.

The Court further clarified that there is no universal rule assigning responsibility for a company’s day-to-day operations to every director. Vicarious liability can only be attributed to a director if it is proven that they were directly in charge of and responsible for the day-to-day affairs of the company at the time the offence occurred.

- MCA Directive to RD and ROCs: Circular Dated March 2, 2020:

It’s noteworthy that, even MCA, vide its General Circular no. 1/2020 dated 2nd March, 2020, directed Regional Directors and Registrar of Companies that at the time of serving notices relating to non-compliances, necessary documents may be sought so as to ascertain the involvement of the concerned officers of the company.

- Duties of Directors under the Companies Act, 2013

Section 166 of the Act lists down duties of directors of a company. To summarise, directors must adhere to the company’s articles, act in good faith for members’ benefit, exercise due care and independent judgment, avoid conflicts of interest, undue gain. However, of note, it does not mention that a director shall be responsible for all the affairs of a company.

In addition to the above case, the following related judgements are also noteworthy:

- Pooja Ravinder Devidasani vs. State of Maharashtra and another, (2014) 16 SCC 1: In this case, the Court asserted that, only those persons who were in-charge of and responsible for the conduct of the business of the Company at the time of commission of an offence will be liable for criminal action.

- S.M.S. Pharmaceuticals Ltd. vs Neeta Bhalla and another, (2005) 8 SCC 89: the Court considered the definition of the word “director” as defined in Section 2(13) of the Companies Act, 1956. It held that “…There is nothing which suggests that simply by being a director in a company, one is supposed to discharge particular functions on behalf of a company. It happens that a person may be a director in a company but he may not know anything about the day-to-day functioning of the company…”.

- SEBI vs. Gaurav Varshney, (2016) 14 SCC 430: The Court held that even a person without any official title or designation such as “director” in a company may still be liable, if they fulfill the main requirement of being in charge of and responsible for the conduct of business at the relevant time. Liability is contingent upon the role one plays in the affairs of a company, rather than their formal designation or status.

- Maharashtra State Electricity Distribution Company Limited and Anr., v. Datar Switchgear Limited and Ors., (10 SCC 479): The Supreme court held that wherever by a legal fiction the principle of vicarious liability is attracted and a person who is otherwise not personally involved in the commission of an offence is made liable for the same, it has to be specifically provided in the statute concerned and it is necessary for the the complainant to specifically aver the role of each of the accused in the complaint.

Vicarious liability must be explicitly provided for in the statute and supported by clear evidence of personal involvement and criminal intent. Also, it is necessary for the complainants to make specific averments in the complaints.

Conclusion:

The above judgments reinforces the principle that corporate and individual liabilities are distinct. Vicarious liability of directors is not presumed and can only be imposed with statutory backing or compelling evidence of personal involvement. By placing the burden of proof on the complainant, the judiciary ensures fairness and prevents misuse of the legal system to harass directors without substantive evidence. This balanced approach safeguards both corporate governance and individual accountability.

You can read more about this subject here.

Disclosures in Financial Statements: Role of CS

SEBI’s Implementation Circular for several LODR Amendments

Read our other resources:

- Presentation on LODR 3rd Amendment Regulations, 2024

- The Load of LODR: Listing regulations become more prescriptive

- Webinar: Online workshop on SEBI LODR 3rd Amendment Regulations 2024

- Youtube video: Position of Compliance Officer: Analysing ‘one level below the board’

- Perched at the Peak: Compliance Officer as CXO