Exclusivity Club: Light-touch regulations for AIFs with accredited investors

– SEBI notifies light-touch regulations for AIFs in which only Accredited Investors are investors and flexibilities for Large Value Funds (LVFs)

– Payal Agarwal, Partner | corplaw@vinodkothari.com

This version: 20th November, 2025

Since its introduction in 2021, the concept of Accredited Investors (AIs) has been through some changes. A Consultation Paper was published on 17th June, 2025 to provide for certain flexibilities in the accreditation framework. Another Consultation Paper dated 8th August 2025 (‘AI CP’) proposed to bring light-touch regulations for AIF schemes seeking investments from only AIs, including extension of various exemptions to such schemes, that are currently available to Large Value Funds (LVFs).

Further, vide another Consultation Paper (‘LVF CP’), some relaxations were also proposed to be extended to Large Value Funds (LVFs) for AIs. Note that the LVFs are available only for AIs, and hence, the Amendment Regulations define the AIs-only schemes to include LVF.

The SEBI (Alternative Investment Funds) (Third Amendment) Regulations, 2025 has been notified on 18th November, 2025, thus introducing the concept of AI-only schemes in the regulatory framework. Note that, vide the 2nd Amendment Regulations, the angel funds have also been exclusively restricted to Accredited Investors only. See an article on the Angel Funds 2.0: Navigating the New Regulatory Landscape.

Accredited Investors – who are they?

An AI is considered as an investor having professional expertise and experience of making riskier investments. Reg 2(1)(ab) of AIF Regulations defines an accredited investor as any person who is granted a certificate of accreditation by an accreditation agency, and specifies eligibility criteria. The eligibility criteria is as follows:

Further, certain categories of investors are deemed to be AIs, that is, certificate of accreditation is not required, such as, Central and State Governments, developmental agencies set up under the aegis of the Central Government or the State Governments, sovereign wealth funds and multilateral agencies, funds set up by the Government, Category I foreign portfolio investors, qualified institutional buyers, etc.

‘Accreditation’ as a measure of risk sophistication

AIFs are investment vehicles pooling funds of sophisticated investors, and not for soliciting money from retail investors. The measure of sophistication, as specified in the AIF Regulations currently, is in the form of the ‘minimum commitment threshold’. Reg 10(c) of the Regulations require a minimum investment of Rs. 1 crore, except in case of investors who are employees or directors of the AIF or of the Manager.

There are certain shortcomings of considering the minimum commitment threshold as the metric of risk sophistication of an investor, such as:

- May not necessarily lead to an actual draw-down, thus exposing to the risk of onboarding investors with inflated commitments. As per the data available on SEBI’s website, out of the total commitment of Rs. 13 lac crores for the quarter ended 31st March 2024, only about Rs. 5 lac crores worth of funds were actually drawn down. Similarly, for the quarter ended 31st March 2025, the value of commitment vis-a-vis funds raised

- Does not consider the investor’s financial health (income, net worth etc), hence, a potential risk of the investor putting majority of its wealth in AIFs, a riskier investment class.

The concept of AIs, as proposed in February 2021, was to introduce a class of investors who have an understanding of various financial products and the risks and returns associated with them and therefore, are able to take informed decisions regarding their investments. Accreditation of investors is a way of ensuring that investors are capable of assessing risk responsibly.

The June 2025 CP indicated that it is being examined to move AIFs gradually in an exclusively for AIs approach, starting with investments in angel funds and in framework for co-investing in unlisted securities of investee companies of AIFs. Accordingly, the present CP has proposed a gradual and consultative transition from ‘minimum commitment threshold’ to ‘accreditation status’ as a metric of risk sophistication of an investor.

Flexibility for AIs-only schemes vis-a-vis other AIFs

The accreditation status is to be ensured at the time of onboarding of investors only. Therefore, if an investor subsequently loses the status of AI in interim, the same shall still be considered as an AI for the AI only scheme, once on-boarded. The following relaxations have been extended to AIs-only schemes, in order to provide for a light-touch regulatory framework, from investor protection viewpoint, considering that the AIs have the necessary knowledge and means to understand the features including risks involved in such investment products:

| Topic | Regulatory requirement for other AIFs | Our Comments |

| Differential rights of investors [reg 20(22)] | Shall be pari-passu, differential rights may be offered to select investors, without affecting the interest of other investors of the scheme in compliance with SEBI Circular dated 13th Dec, 2024 r/w Implementation Standards | This facilitates differential rights to different classes of investors within a scheme. |

| Extension of tenure of close-ended funds [reg 13(5)] | up to two years subject to approval of two-thirds of the unit holders by value of their investment in AIF | This facilitates a longer tenure extension to an existing close-ended scheme, if suited to investors. However, it is further clarified that the maximum extension permissible to such AI only schemes, inclusive of any tenure extension prior to such conversion, shall be 5 years. |

| Certification criteria for key investment team of Manager [reg 4(g)(i)] | Atleast one key personnel with relevant NISM certification | The investors, being accredited, the reliance on key investment team of the Manager is comparatively low. |

Further, in case of AIs-only Funds, the responsibilities of Trustee as specified in Reg 20 r/w the Fourth Schedule shall be fulfilled by the Manager itself. This is based on the premise that, the investors, being accredited, the reliance on Trustee for investor protection is comparatively low.

Large Value Funds: a sub-category of AIs only scheme

The concept of LVF was also introduced in 2021, along with the concept of AIs. An LVF, in fact, is an AIs only fund, with a minimum investment threshold. Reg 2(1)(pa) of the AIF Regulations defines LVF as:

“large value fund for accredited investors” means an Alternative Investment Fund or scheme of an Alternative Investment Fund in which each investor (other than the Manager, Sponsor, employees or directors of the Alternative Investment Fund or employees or directors of the Manager) is an accredited investor and invests not less than seventy crore rupees.

Since an LVF is included within the meaning of an AIs-only scheme, all exemptions as available to an AIs only scheme, are naturally available with an LVF, although the converse is not true.

Additional Exemptions available to LVFs (other than as available to AIs only scheme)

In addition to the relaxations extended to an AIs only scheme, there are additional exemptions available to an LVF. These are:

| Regulatory reference | Topic | Exemption for LVF |

| Reg 12(2) | Filing of placement memorandum through merchant banker | Not applicable |

| Reg 12(3) | Comments of SEBI on PPM through merchant banker | Not applicable, only filing with SEBI required |

| Reg 15(1)(c) | Investment concentration for Cat I and Cat II AIFs – cannot invest more than 25% of investable funds in an investee company, directly or through units of other AIFs | May invest upto 50% of investable funds in an investee company, directly or through units of other AIFs |

| Reg 15(1)(d) | Investment concentration for Cat III AIFs – cannot invest more than 10% of investable funds in an investee company, directly or through units of other AIFs | May invest upto 25% of investable funds in an investee company, directly or through units of other AIFs |

Reduction in minimum investment size for LVFs

The minimum investment threshold for investors in LVF has been reduced from Rs. 70 crores to Rs. 25 crores, based on the recommendations of SEBI’s Alternative Investment Policy Advisory Committee (AIPAC). The rationale is to lower entry barriers to facilitate improved fund raising, without compromising on the level of investor sophistication. The reduction of investment thresholds would also facilitate investments by regulated entities having a strict exposure limit, such as insurance companies.

Exemptions from requiring specific waivers for certain provisions

The extant regulations permitted that the responsibilities of the Investment Committee may be waived by the investors (other than the Manager, Sponsor, and employees/ directors of Manager and AIF), if they have a commitment of at least Rs. 70 crores (USD 10 billion or other equivalent currency), by providing an undertaking to such effect, in the format as provided under Annexure 11 of the AIF Master Circular, including a confirmation that they have the independent ability and mechanism to carry out due diligence of the investments.

The requirement of specific waiver has been omitted for LVFs considering that AIs are already required to provide an undertaking for the purpose of availing benefits of ‘accreditation’. The undertaking, as per the format given in Annexure 8 of the AIF Master Circular states the following:

(i) The prospective investor ‘consents’ to avail benefits under the AI framework.

(ii) The prospective investor has the necessary knowledge and means to understand the features of the investment Product/service eligible for AIs, including the risks associated with the investment.

(iii) The prospective investor is aware that investments by AIs may not be subject to the same regulatory oversight as applicable to investment by other investors.

(iv) The prospective investor has the ability to bear the financial risks associated with the investment.

Similarly, LVFs have been exempt from following the standard PPM template without the requirement of obtaining specific waiver from investors.

Migration of existing eligible AIFs

One of the proposals of the LVF CP is to permit eligible AIFs, not formed as an LVF, to convert themselves into an LVF and avail the benefits available to LVF schemes. The conversion shall be subject to obtaining positive consent from all the investors. Following the same, the modalities for such migration has been specified by SEBI vide circular dated 8th December, 2025.

Pursuant to such migration, the AIF manager shall ensure that:

- Name of the converted scheme contains ‘AI only fund’ or ‘LVF’ as the case may be

- Such conversion and change in name to be reported to SEBI within 15 days through dedicated email ID

- Such change in name to be reported to depositories within 15 days of conversion

Limit on maximum number of investors

Reg 10(f) puts a cap on the maximum number of investors in a scheme. Pursuant to the Amendment Regulations, the cap of 1000 investors shall not include the AIs.

In practice, the number of investors in an AIF is much lower than 1000, and hence, the amendment may not have much of a practical relevance.

Conclusion

The amendments are a step towards providing a lighter regulatory regime for AIFs, meant for sophisticated investors, capable of making well-informed decisions. The move is expected to witness more schemes focussed on AIs only, and thus, bring an AIs only regime for AIFs. In order to differentiate an AIs only scheme or an LVF from other AIF schemes, it is mandatory for the newly launched schemes henceforth to have the words ‘AI only fund’ or ‘LVF’ as the case maybe.

Our resources on the topic-

- Understanding the Governance & Compliance Framework for AIFs

- Round-Tripping Reined: RBI Rolls Out Relaxed Rules for Investments in AIF

- Regulatory landscape for AIFs: what’s new?

- FAQs on Specific Due Diligence of investors & investments of AIFs

- Angel Funds 2.0: Navigating the New Regulatory Landscape.

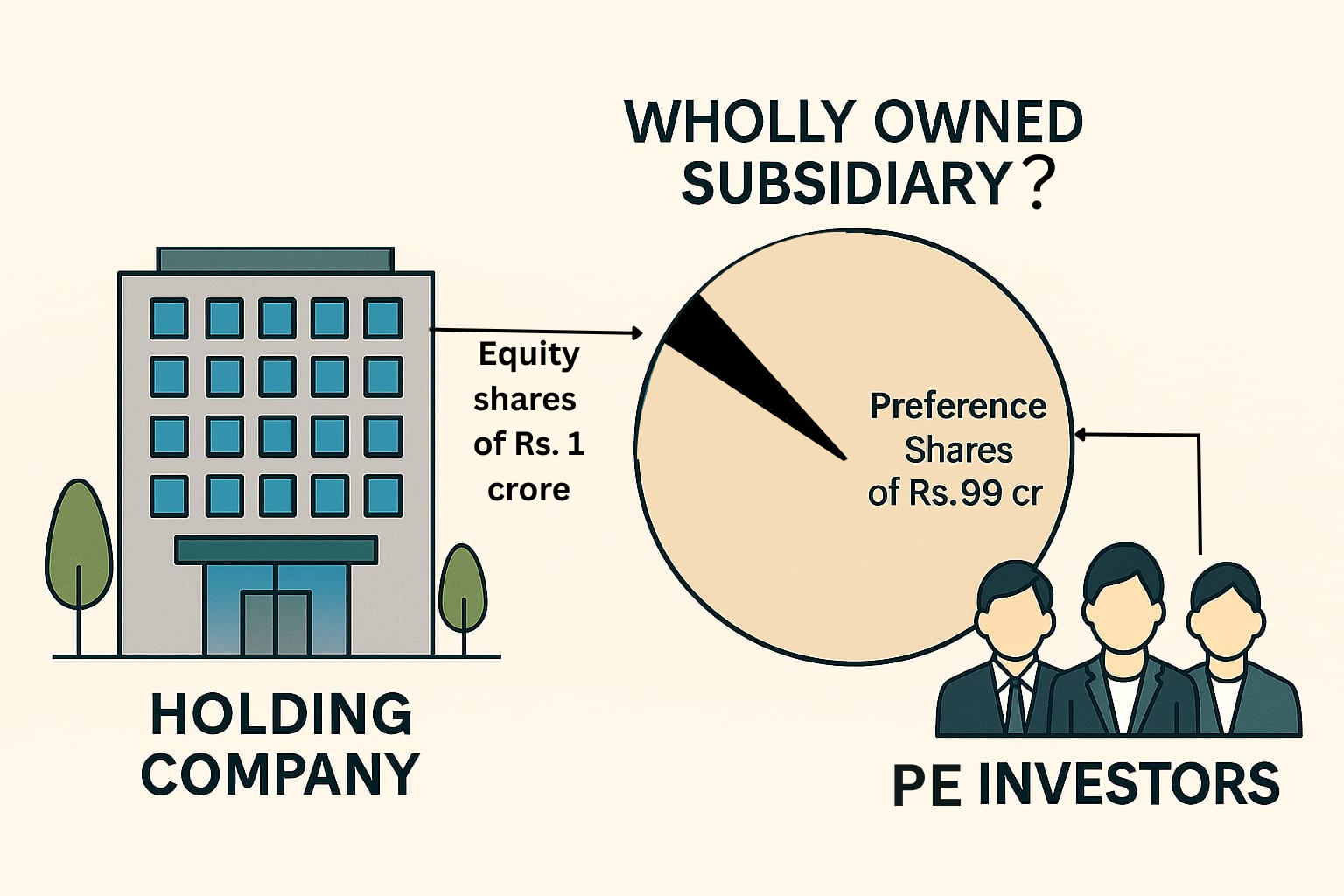

Wholly controlled, but not wholly owned

– Payal Agarwal, Partner and Saloni Khant, Executive | corplaw@vinodkothari.com

Do preference shares matter for wholly-owned subsidiary status?

Preference shares are a much preferred means of raising funds from third party investors by Indian startups. The reasons for such popularity may be accorded to the priority of payment over the equity shares, thus providing a layer of protection, flexibility in exit as compared to the permanent equity capital, ease of structuring and various other factors. Very often, this may lead to the total preference share capital holding a higher proportion as against the equity share capital of the company.

This brings a very interesting question to the fore – whether a company having preference share capital held by third parties, may still be considered to be a “Wholly Owned Subsidiary” (WOS), if such company has a sole equity shareholder, as its holding company. The question becomes particularly relevant in view of the exemptions provided to a company/ its group with respect to the WOS.

Compliance haven provided to a WOS

The Indian laws provide a myriad of relaxations in statutory requirements – a compliance haven to wholly owned subsidiaries.

Some of these have been tabulated below:

| Sr. No | Law | Section / Rule/ Regulation | Exemption |

| 1. | CA, 2013 | Section 185 | The prohibitions/ restrictions u/s 185 does not apply with respect to the loans given by the holding company to its WOS or security or guarantee provided in respect of loans to its WOS. |

| 2. | CA, 2013 | Section 186 | The limits on loan, guarantee, security, investments etc by holding company is not applicable in case of WOS. |

| 3. | CA, 2013 | Section 177(4)(iv) and 188 | Transactions between a holding company and its WOS are exempt from the approval of the Audit Committee, except in some cases. Further, RPTs specified under section 188 are exempt from shareholders’ approval. Our article on RPTs with WOS may be accessed here. |

| 4. | SEBI Listing Regulations, 2015 | Regulation 23 | Exemption from AC and shareholders’ approval for RPTs with a WOS or between two WOS of the listed holding company. |

| 5. | CA, 2013 | Section 149(4), 177 and 178 read with Rule 4 of the Companies (Appointment and Qualification of Directors) Rules, 2014 and Rule 6 of Companies (Meetings of Board and its Powers) Rules, 2014 | The following requirements do not apply: Appointment of independent directors Constitution of Audit Committee Constitution of Nomination and Remuneration Committee |

| 6. | CA, 2013 | Section 2(87) r/w Rule 2(1) of the Companies (Restriction on Number of Layers) Rules, 2017 | A layer consisting entirely of 1 or more WOS is not considered as a layer for the prohibition on having only 2 layers of subsidiaries. Our article on the restrictions w.r.t. layers of subsidiaries may be read here. |

| 7. | CA, 2013 | Section 29 read with Rule 9A(11) of the Companies (Prospectus and Allotment of Securities) Rules, 2017 | A public company that is a WOS is exempt from the requirement of mandatory dematerialisation of securities. Read our article on mandatory dematerialisation of shares here. |

| 8. | CA, 2013 | Section 233 | Fast track Merger is permitted between a holding company and its WOS. See our article on the procedure of fast track merger here. |

| 9. | SEBI Listing Regulations, 2015 | Regulation 37 | The requirement of obtaining a No-Objection Letter from the Stock exchange is dispensed for a scheme of arrangement between a listed holding company and its WOS. |

| 10. | SEBI Listing Regulations, 2015 | Regulation 37A | The requirement of shareholders’ approval for sale, lease or disposal of an undertaking, outside a scheme of arrangement, is exempt if made to the WOS. |

| 11. | The Indian Stamp Act, 1899 | Articles 23 and 62 of Schedule I, Circular issued in 1937 | Stamp duty on mergers is remitted if the merger is between a parent company and subsidiary company (parent company holding beneficial ownership of at least 90% of its share capital) or2 subsidiary companies (Common parent company is holding the beneficial ownership of at least 90% of the share capital of both the companies). Our article on the same may be accessed here |

The exemptions follow primarily an enterprise level approach, as against, entity level – thus, considering the WOS as nothing but an extended arm of the holding company. The Listing Regulations further uses the expression: whose accounts are consolidated with such listed entity, thus, signifying the relevance of ‘control’ while availing exemptions w.r.t. a WOS.

Thus, the position and rights of the preference shareholders need to be analysed in reference to whether the same provides any sort of ‘ownership’ or ‘control’ to such shareholders.

Preference shareholder as a member of the company

Section 2(55) of the CA, 2013 defines the term ‘member’ in the following manner:

(i) the subscriber to the memorandum of the company who shall be deemed to have agreed to become member of the company, and on its registration, shall be entered as member in its register of members;

(ii) every other person who agrees in writing to become a member of the company and whose name is entered in the register of members of the company;

(iii) every person holding shares of the company and whose name is entered as a beneficial owner in the records of a depository;

The definition covers every person whose name is entered in the register of members, as well as every person holding ‘shares’ in the company having their name recorded with the depository. The term ‘shares’ covers both equity and preference shares [Section 2(84) read with Section 43]. Further, in terms of section 88, the details of preference shareholders shall also be entered in the register of members. Thus, it is beyond doubt that the preference shareholders, too, are members of the company.

Preference shares: equivalent to ‘debt’ or considered as ‘capital’

In accounting parlance, preference shares are more likely to be classified as ‘debt’ than ‘equity’, depending on the terms of redemption or conversion. However, legally, the position of preference shareholder is not considered equivalent to a ‘creditor’, as has been a matter of jurisprudence in various cases.

The Hon’ble Bombay High Court held the following in the case of Aditya Prakash Entertainment Pvt. Ltd vs Magikwand Media Pvt. Ltd :

“The shareholders of redeemable preference shares of the company do not become creditors of the company in case their shares are not redeemed by the company at the appropriate time. They continue to be shareholders, no doubt subject to certain preferential rights mentioned in Section 85 of the Companies Act, 1956.”

The Bombay High Court cited references to Hindustan Gas and Industries Ltd. v. Commissioner of Income-tax, West Bengal-II, as also “Company Law” by Robert R. Pennington, 2nd edn. and noted from the said judgment that:

“ . . . we cannot persuade ourselves to accept the contentions of the assessee and hold that when a company issues redeemable preference shares it is in fact obtaining a loan as it could by issuing debentures. There is a fundamental difference between the capital made available to a company by issue of a share and money obtained by a company under a loan or a debenture. Respective incidences and consequences of issuing a share and borrowing money on loan or on a debenture are different and distinctive. A debenture-holder as a creditor has a right to sue the company, whereas a shareholder has no such right. Apart from that the scheme of the Companies Act and in particular the forms and contents of its balance-sheets are extremely rigid and, in our view, by reason of the specific compartments in such accounts it is not possible to convert an item of capital into an item of loan as has been suggested on behalf of the assesse.”

In the context of assigning a vote to the preference shareholders in a meeting of creditors, the Hon’ble Bombay High Court held the following in the case of State Bank Of India vs Alstom Power Boilers Ltd :

“A preference share is not a debt instrument. Preference share amount is a capital and not a debt. Thus, in the meeting of the creditors, it would not be possible to assign a value to the vote of a holder of preference share. If we were to hold that the preference shareholders who are not paid dividend for more than two years are also entitled to attend the meeting of the creditors under Section 391 of the Act and to vote thereat, then it would be impossible to determine what would be the value to their votes vis-a-vis the value of votes of creditors. It would be wrong to contend that preference shareholders have a right to vote but, valuation of their vote is unascertainable. We are therefore of the view that preference shareholders are not entitled to attend and vote at the meeting of the creditors convened under Section 391 of the Act even though dividend on the preference shares have remained unpaid for more than 2 years.

In Globe United Engineering & Foundry Co. Ltd, the Hon’ble Delhi High Court, while dealing with the question pertaining to the rights of the preference shareholders over arrears of dividend, observed the following:

“(15) The outside investor may be induced to subscribe for preference rather than ordinary shares by reason of the bargain offered; such investor has usually little knowledge of the company’s business, has no wish to participate in the company’s management and is keen only on his promised return. It may also happen that if the companies want to raise new capital when their existing shares are worth less than the nominal value the only direct way of raising new capital. apart from borrowings and debentures, will be to issue new class of shares with preferential rights over the existing ones. The preference shares are really part of the company share capital: they are not loans.”

The question of whether a failed redemption of preference shares constitute a contractual debt, has been a matter of jurisprudence, primarily in the context of maintainability of an application under IBC. See an article on the same here. The Hon’ble NCLAT, in a very recent judgement in the matter of EPC Constructions India Limited v. M/S Matix Fertiliser and Chemicals Limited, pertaining to the maintainability of an application by the preference shareholders under section 7 of IBC, held the following:

“…the Appellant who is holder CRPS is holder of shares which is in the nature of equity in capital, which is part of preferential share capital as defined in Section 43. Preferential shares being part of the preferential share capital of the Company shall not transfer any debt so as to initiate any Section 7 proceeding. Further, the Company having not earned any profit nor any dividend having been declared, no redemption was permissible by the statutory provision, hence, no debt was due on basis of which Section 7 application could be filed by the Appellant. There is also no material that any proceeds of a fresh issue of shares made for the Company Appeal (AT) (Insolvency) No. 1424 of 2023 purpose of such redemption was available. We, thus, fully endorse the finding of the Adjudicating Authority that there did not exist any default.”

Rights of the Preference Shareholders

Based on the various rulings discussed above, it is amply clear that preference shareholders are not creditors of the company, rather, shareholders. However, these are not equity shares, and cannot be treated at par with the equity shareholders. Murray A Pickering, in a scholarly analysis [The Problem of the Preference Share, Vol. 26 (1963) Modem Law Review], regards three principles as basically established and quotes from three decisions :

(1) The rights inter se of preference and ordinary shareholders must depend on the terms of the instrument which contains the bargain that they have made with the company and each other (a question of construction, vide Lord Simonds in Scottish Insurance Corporation, Limited v. Wilsons & Clyde Coal Company Limited, 1949 A.C. 462);

(2) where the articles set out the rights attached to a class of shares to participate in profits while the company is a going concern or to share in the property of the company in liquidation; prima facie, the rights so set out are in each case exhaustive (vide Wynn Parry, J. in re The Isle of Thenet Electricity Supply Co. Ltd., (1950) Ch. 161) and

(3) In the absence of specific provisions the rights of all shareholders are deemed to be the same (vide Lord Macnaghten in Birch v. Cooper and others, (1889) 14 A.C. 525)- case not referred (page 500 of Pickcring’s Article).

Thus, the rights of preference shareholders are based on the terms of the instrument and the Articles of the company. In the absence of any specific provisions, the rights of all shareholders are deemed to be the same.

Under the Companies Act, 2013, the rights of the preference shareholders are briefly contained in section 43 and section 47. Further, where a right is available to equity shareholders only, the same is stated expressly under the relevant provision. For instance, section 62 of the Act explicitly recognises only equity shareholders to be eligible for participating in a rights issue.

- Economic rights of preference shareholders

Certain rights are available to preference shareholders, by definition. This includes preferential rights with respect to:

- Payment of dividend, either as a fixed amount or a fixed rate

- Repayment of capital, at the time of winding up or otherwise

Depending on the terms of issue, this may further include the participating rights with respect to surplus dividend or capital repayment.

- Voting rights of preference shareholders

Section 47(2) of CA, 2013 limits the preference shareholders’ right to vote in a company on the following resolutions only in the same proportion as the paid-up capital in respect of the preference shares bears to the paid-up capital in respect of the equity capital:

- Resolutions which directly affect the rights attached to their preference shares.

- Resolution for winding up of the company.

- Resolution for the repayment or reduction of its equity or preference share capital.

However, pursuant to the second proviso to the said section, the preference shareholders acquire a right to vote on all the resolutions of the company where the dividend in respect of that particular class of preference shares has not been paid for a period of 2 years or more. Thus, the preference shareholders are not completely devoid of voting rights, they too have the right to vote on some matters or in specified conditions.

Preference shareholders, thus, may be compared with a sleeping monster. As long as the dividend is paid, the monster remains sleeping. But if the company defaults in the payment of their dividend for a period of 2 years, the monster awakens and is entitled to equal voting rights in the company as the equity shareholders. Once the default is made good by the company, that is to say, dividend is paid to the preference shareholders, whether the additional voting rights of such preference shareholders are revoked and they assume their erstwhile status or the voting rights assume permanence is not clearly laid down under the current provisions of CA, 2013. The question has been discussed in our article titled Voting Rights on Preference Shares: An Unclear Provision?. Companies putting off the payment of dividend on preference shares risk waking up the monster who might never go back to sleep again.

Further, pursuant to MCA notification no. GSR 464 (E) dated 5th June, 2015, certain exemptions were given to private companies. The notification, amongst others, provides exemption from the applicability of section 43 and section 47 to a private company where memorandum or articles of association of the private company so provides.

Hence, flexibility is provided to a private company to structure its share capital, including the voting rights therein, in the manner as may be required by such company, by providing for the same in the MoA or AoA of the company.

Thus, the voting rights on preference shares are not only in accordance with section 47 of the Act, but are also dependent on the terms of issue. In fact, companies which have issued compulsorily convertible preference shares (CCPS) often determine their total voting power on ‘as if converted’ basis.

- Rights as a member of the company

In addition to the rights specific to preference shares, other rights that are available to any member of a company are also available to a preference shareholder. These rights inter alia include:

- Right to receive annual reports and financial statements of the company [section 136]

- Right to receive notice and attend general meetings of the company [section 101]

- Right to inspect the registers and records of the company [section 94]

- Right to give special notice for removing directors [section 115]

- Right to give consent to or object to any proposed variation of shareholders’ rights [section 48]

- Right to apply to the Tribunal for relief in case of oppression & mismanagement [section 244]

Meaning of ‘subsidiary’: based on shares or voting rights?

Wholly owned subsidiary is basically a ‘subsidiary’ that is ‘wholly owned’ by a shareholder. The term ‘Wholly Owned Subsidiary’ has not been defined under the CA, 2013 or the SEBI Listing Regulations, 2015. However, reference may be drawn from the definition of ‘subsidiary company’ as defined in section 2(87) of the CA, 2013. The definition reads as:

‘A company in which the holding company controls the composition of the Board of Directors or exercises or controls more than one-half of the total voting power either at its own or together with one or more of its subsidiary companies.’

Note that a subsidiary is defined with reference to ‘voting powers’ and not ‘shareholding’. Therefore, the non-voting share capital of a company is not required to be considered in the determination of a company as a ‘subsidiary’.

The shift from ‘total share capital’ to ‘total voting power’ was based on the recommendations of the Company Law Committee, which considered the alignment of the meaning of subsidiary with consolidation principles in accounting. The CLC deliberated as follows:

During the deliberations, it was noted that by virtue of the present definition, a company in which the preference share capital was greater than its equity share capital, could become a subsidiary of an entity that holds the preference shares, even though it might not have control, or any voting rights in such a company. Further, inclusion of the preference share capital in the total share capital could create confusion about ownership of the company. Further, such companies could be shown as subsidiaries, but would not be considered for consolidation purposes, as per the applicable Accounting Standards.

Thus, preference shareholding would generally not be considered for the purpose of determining a holding-subsidiary relationship, unless such preference shares carry voting rights. Further, in view of the rationale provided by the CLC, it is clear that the voting rights need to be in the nature of ‘decision-making’ rights, and not merely affirmative or protective rights.

Wholly-owned subsidiary: is control the only factor?

While the determination of a subsidiary is based on voting powers, can it be said that it is only the equity shareholders that ‘own’ a company? In other words, whether the preference shareholders do not have any ‘ownership’ rights over the company?

In the context of incorporating a WoS outside India, the erstwhile Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2000, further amended in 2004defined the term Wholly Owned Subsidiary as “A foreign entity formed, registered or incorporated in accordance with the laws and regulations of the host country, whose entire capital is held by the Indian party.” In the absence of any specific exclusions from the meaning of ‘capital’, the same would cover both equity and preference share capital.

Though this definition is no longer in force, the same hints on the intent of the regulator in considering the entire share capital holding as a criteria for considering a company as WoS.

WOS in the Global Context

That the determination of ‘subsidiary’ is a control-based approach, whereas a WoS is based on the entire shareholding and not merely voting rights is very clearly laid down in section 1159 of the Companies Act, 2006 of the United Kingdom. The section defines both ‘subsidiary’ and ‘wholly owned subsidiary’, in the following manner:

| Subsidiary | Wholly owned subsidiary |

| A company is a “subsidiary” of another company, its “holding company”, if that other company— (a)holds a majority of the voting rights in it, or (b)is a member of it and has the right to appoint or remove a majority of its board of directors, or (c)is a member of it and controls alone, pursuant to an agreement with other members, a majority of the voting rights in it, or if it is a subsidiary of a company that is itself a subsidiary of that other company. | A company is a “wholly-owned subsidiary” of another company if it has no members except that other and that other’s wholly-owned subsidiaries or persons acting on behalf of that other or its wholly-owned subsidiaries. |

Thus, while a ‘subsidiary’ is based on majority voting rights or such other rights that leads to ‘control’, the test of ‘wholly owned subsidiary’ is dependent on the sole membership, and is not restricted to just voting rights.

The Companies Act, 2006 of Singapore also defines subsidiary and wholly owned subsidiary in a similar fashion:

| Subsidiary | Wholly owned Subsidiary |

| 5.—(1) For the purposes of this Act, a corporation shall, subject to subsection (3), be deemed to be a subsidiary of another corporation, if — that other corporation — (i) controls the composition of the board of directors of the first-mentioned corporation; (ii) controls more than half of the voting power of the first-mentioned corporation; or (iii) holds more than half of the issued share capital of the first-mentioned corporation (excluding any part thereof which consists of preference shares and treasury shares); or the first-mentioned corporation is a subsidiary of any corporation which is that other corporation’s subsidiary. | 5B. For the purposes of this Act, a corporation is a wholly owned subsidiary of another corporation if none of the members of the first-mentioned corporation is a person other than — that other corporation;a nominee of that other corporation;a subsidiary of that other corporation being a subsidiary none of the members of which is a person other than that other corporation or a nominee of that other corporation; ora nominee of such subsidiary. |

Thus, while preference shares are explicitly excluded from the definition of ‘subsidiary’, no similar approach is followed in defining a wholly owned subsidiary.

15 U.S. Code § 80a-2 defines the term WoS in reference to ‘voting securities’. Thus, WoS is defined as: “a company 95 per centum or more of the outstanding voting securities of which are owned by such person, or by a company which, within the meaning of this paragraph, is a Wholly Owned Subsidiary of such person”. ‘Voting securities’, as defined in the said Code means “any security presently entitling the owner or holder thereof to vote for the election of directors of a company”. This may also include the preference shares, given the 12 U.S. Code § 51b entitles preference shareholders to such voting rights as may be provided for in the Articles of Association of the company.

Conclusion

Preference shareholders, though having certain rights distinct from equity shareholders, are still members of the company. Voting rights may be assigned to them either as a part of the terms of issue or upon non-payment of dividend. These preference shares may either be redeemable or convertible, and in case of the latter, becomes a part of equity share capital upon conversion. Wholly owned subsidiary should indicate complete ownership, in the form of 100% shareholding, and hence, even non-voting shares should be considered for the purpose of identification of an entity as such.

Where the preference shares are held by a person other than the holding company, the company should not be entitled to the benefits of being a wholly owned subsidiary.

12 hours Certificate Course on Nuts and Bolts of Related Party Transactions

Listed and Restricted? Additional Compliances and Prohibitions for listing of SDIs by RBI regulated Originators

– Payal Agarwal & Dayita Kanodia (finserv@vinodkothari.com)

Securitisation Transactions in India are primarily governed by:

- The RBI Securitisation of Standard Assets Directions, 2021 (in case the originator is regulated by RBI)

- SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, which become applicable if the securitisation notes are listed.

Consequently, an RBI regulated originator will be required to adhere to both the SSA Directions as well as the SDI Framework in case it intends to go for listing of the securisation notes.

Here, we have discussed the additional prohinitions and compliance requirements for RBI regulated originators which becomes applicable in case of listing of securitisation notes.

| Additional Prohibitions under the SEBI SDI Framework for RBI Regulated Originators | |||

| Para Ref | Relevant Regulatory Provision | Our Comments | |

| Single Asset Securitisation not permitted | 19A(a) | “No obligor shall have more than twenty-five percent in asset pool at the time of issuance.” | An RBI regulated originator will not be able to undertake single asset securitisation if it intends to list the securitisation notes, though the same is permitted under the RBI regulations (proviso to para 5(s) of the SSA Directions). Comments: Single asset securitisation is not a very common practice, but this is explicitly permitted under RBI regulations |

| All assets to be homogenous | 19A(b) | “Assets comprising the securitisation pool shall be homogeneous.” | The RBI SSA Directions only require the assets to be homogeneous in case of simple, transparent, and comparable securitisation transactions (STC Transactions). STC transactions are currently not very common, and in any case, is an investor classification, not that of issuer.For non-STC cases, there is no such requirement. Therefore, originators will be required to ensure that the assets comprising the pool are homogeneous in case they intend to go for listing of the securitisation notes. Comment: Homogeneity may be subjective |

| SPV can only be constituted in the form of a trust | 9(1) | “The special purpose distinct entity shall be constituted in the form of a trust the constitutional document whereof entitles the trustees to issue securitised debt instruments.” | The RBI SSA Directions (para 5(w)) allow SPVs to be constituted in the form of a company, trust or other entity. Comment: Not a very big pain, as SPVs in India are almost always in the trust form. |

| Originator and Trustee not be under the same group or control. | 10(3) | “No special purpose distinct entity shall acquire any debt or receivables from any originator which is part of the same group or which is under the same control as the trustee.” | This requirement, although essential to maintain independence, is not a part of the RBI SSA Directions. Accordingly, the same will be required to be ensured. |

| Additional Compliances applicable to RBI regulated Originators under the SEBI SDI Framework | |||

| Para Ref | Relevant Regulatory Provision | Our Comments | |

| Registration of Trustees under the Securities and Exchange Board of India(Debenture Trustees) Regulations, 1993 | 4(b) | “(1) On and from the commencement of these regulations, no person shall make a public offer of securitised debt instruments or seek listing for such securitised debt instruments unless –XX(b)all its trustees are registered with the Board under 26[the Securities and Exchange Board of India(Debenture Trustees) Regulations, 1993];XX” | Accordingly, the trustees will be required to comply with the SEBI Debenture Trustee regulations. Comment: This is a useful provision, and mostly, the SPV trustees are registered debenture trustees. Hence, it is a useful regulatory requirement. |

| Contents of the Instrument of Trust | Schedule IV | Schedule IV of the SEBI SDI Framework prescribes the minimum contents of the instrument of trust. | The contents prescribed under the SDI Framework are more detailed as compared to the RBI SSA Directions, which only indicate the contents of the trust deed. Comment: Useful regulation, serving the purpose of proper disclosures. Notably, disclosures are the domain of the securities regulator. |

| Quarterly reports to the trustee about the performance of the underlying pool and auditor certificate | 10A(1) and (2) | “(1) The originator shall provide the periodic reports to the trustee regarding the performance of the underlying asset pool, at least on a quarterly basis. (2) The originator shall provide a certificate from its auditor (s) regarding the disclosures of underlying asset pool assigned to the securitization trust, as made by the originator, on quarterly basis.” | The RBI SSA Directions (para 114 and 115) require semi-annual disclosures to be made. Further, there is no requirement to provide an auditor’s certificate under the RBI Directions. Comment: Useful regulation, serving the purpose of investor information. These disclosures are typically part of the securities regulators’ domain. |

| Minimum Ticket Size for subsequent transfers | 30A(2)(i) | “The minimum ticket size for subsequent transfers of a securitised debt instrument shall be as follows:(i)for originators which are not regulated by the Reserve Bank of India, the minimum ticket size shall be rupees one crore.” | In case of public offer of SDIs, the minimum ticket size is Rs. 1 Crore even for subsequent transfers of SDIs. This requirement is more stringent as compared to the RBI SSA Directions (para 28), which only requires the minimum ticket size of Rs. 1 Crore to be seen at the time of issuance. Comments: The requirement has only been introduced for the public offer of SDIs. Public issue of SDIs is howe,ver not a common practice currently. Accordingly, this may not seem to be a major concern for RBI regulated originators. |

| Other miscellaneous provisions – offer period, allotment period, dematerialisation | 29, 31(1) | Offer Period: No public offer of securitised debt instruments shall remain open for less than two working days and more than ten working days. Allotment Period:The securitised debt instruments shall be allotted to the investors within five days of closure of the offer. Further, the securitises will need to be issued mandatorily in demat form. | Comments: These requirements are applicable only in case of public offers. |

| Facility to avail electronic bidding platform | Master Circular dated May 16, 2025 | On issue and listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper and on Review of provisions pertaining to Electronic Book Provider (EBP) platform to increase its efficacy and utility | The facility of using EBP has been extended to SDIs too. Comment: This is an optional facility, and as of now, very limited issuers have made use of this. |

| LODR Requirements – Chapter III | |||

| Disclosure by KMPs, directors, etc | Reg 5 | 5. The listed entity shall ensure that key managerial personnel, directors, promoters or any other person dealing with the listed entity, complies with responsibilities or obligations, if any, assigned to them under these regulations 51[:]52[Provided that the key managerial personnel, directors, promoter, promoter group or any other person dealing with the listed entity shall disclose to the listed entity all information that is relevant and necessary for the listed entity to ensure compliance with the applicable laws.] | This requires the concerned officers of the Listed Entity (in this case, the SPV] to make requisite disclosures for the purpose of complying with the law. Comment: Does not seem to be practically relevant, as Originators’ KMPs mostly do not have interest in the SPV. However, where needed, it is a useful disclosure. |

| Compliance officer to be appointed. | Reg 6, Chap III | 6. (1) A listed entity shall appoint a qualified company secretary as the compliance officer Other provisions of the regulation | An issuer of SDIs is required to appoint a Compliance Officer. Comments: The requirement may be complied with at SPV level. |

| Share Transfer Agent | Reg 7 | (1)The listed entity shall appoint a share transfer agent or manage the share transfer facility in-house:Other requirements of the regulation | The requirement to appoint a share transfer agent is typically part of the securities regulators’ domain. Comment: Mostly not relevant as the securities are offered in demat form. |

| Information to intermediaries | Reg 8 | The listed entity, wherever applicable, shall co-operate with and submit correct and adequate information to the intermediaries registered with the Board such as credit rating agencies, registrar to an issue and share transfer agents, debenture trustees etc, within timelines and procedures specified under the Act, regulations and circulars issued there under:Provided that requirements of this regulation shall not be applicable to the units issued by mutual funds listed on a recognised stock exchange(s) for which the provisions of the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996 shall be applicable. | Requirement to share information with the information agencies. Comment: In case of listed SDIs, this is a part of the information eco system. |

| Policy for preservation of documents | Reg 9 | The listed entity shall have a policy for preservation of documents, etc. | Useful for preservation of documents. |

| Filing of reports, statements and other documents | Reg 10 | (1) The listed entity shall file the reports, statements, documents, filings and any other information with the recognised stock exchange(s) on the electronic platform as specified by the Board or the recognised stock exchange(s).Other provisions of the regulation | This is a general filing requirement for filing of information on the stock exchanges. |

| Scheme of arrangement to not violate, affect or override the provisions of securities law | Reg 11 | The listed entity shall ensure that any scheme of arrangement /amalgamation /merger /reconstruction /reduction of capital etc. to be presented to any Court or Tribunal does not in any way violate, override or limit the provisions of securities laws or requirements of the stock exchange(s):. | Mostly not relevant for SDIs |

| Use of electronic mode of payments | Reg 12 | The listed entity shall use any of the electronic mode of payment facility approved by the Reserve Bank of India, in the manner specified in Schedule I, for the payment of the following:(a) dividends;(b) interest;(c) redemption or repayment amounts: | Provides for mode of payments to investors. Not a cumbersome requirement as it refers to RBI-permitted payment systems to be used. |

| SCORES | Reg 13 | (1) 61[The listed entity shall redress investor grievances promptly but not later than twenty-one calendar days from the date of receipt of the grievance and in such manner as may be specified by the Board.]Other provisions of the Regulation | This relates to use of the SCORES mechanism for settling investor issues |

| Payment of Fees and charges | Reg 14 | The listed entity shall pay all such fees or charges, as applicable, to the recognised stock exchange(s), in the manner specified by the Board or the recognised stock exchange(s). | This mandates payment of listing fees. Usual provision for all listed securities |

| LODR Regulations – Chapter VIII | |||

| The entire Chapter is dedicated to listed SDI issuance. | Reg 81 | Applicability(1) The provisions of this chapter shall apply to Special Purpose Distinct Entity issuing securitised debt instruments and trustees of Special Purpose Distinct Entity shall ensure compliance with each of the provisions of these regulations.(2) The expressions “asset pool”, “clean up call option”, “credit enhancement”, “debt or receivables”, “investor”, “liquidity provider”, “obligor”, “originator”, “regulated activity”, “scheme”, “securitization”, “securitized debt instrument”, “servicer”, “special purpose distinct entity”, “sponsor” and “trustee” shall have the same meaning as assigned to them under [Securities and Exchange Board of India (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008]555; | Specifies applicability of the Chapter and refers to meaning of relevant expressions |

| Intimation and filings with stock exchange(s) | Reg 82 | (1) The listed entity shall intimate the Stock exchange, of its intention to issue new securitized debt instruments either through a public issue or on private placement basis (if it proposes to list such privately placed debt securities on the Stock exchange) prior to issuing such securities.(2) The listed entity shall intimate to the stock exchange(s), at least two working days in advance, excluding the date of the intimation and date of the meeting, regarding the meeting of its board of trustees, at which the recommendation or declaration of issue of securitized debt instruments or any other matter affecting the rights or interests of holders of securitized debt instruments is proposed to be considered.(3) The listed entity shall submit such statements, reports or information including financial information pertaining to Schemes to stock exchange within seven days from the end of the month/ actual payment date, either by itself or through the servicer, on a monthly basis in the format as specified by the Board from time to time:Provided that where periodicity of the receivables is not monthly, reporting shall be made for the relevant periods.(4) The listed entity shall provide the stock exchange, either by itself or through the servicer, loan level information, without disclosing particulars of individual borrowers, in manner specified by stock exchange. | This regulation is equivalent of reg 29 in case of listed equities, and provides for prior intimation to investors for certain critical actions on the part of issuers. |

| Disclosure of information having bearing on performance/operation of listed entity and/or price sensitive information | 83 read with Part D of Schedule III | (1) The listed entity shall promptly inform the stock exchange(s) of all information having bearing on the on performance/operation of the listed entity and price sensitive information.(2) Without prejudice to the generality of sub-regulation(1), the listed entity shall make the disclosures specified in Part D of Schedule III.Explanation.- The expression ‘promptly inform’, shall imply that the stock exchange must be informed must as soon as practically possible and without any delay and that the information shall be given first to the stock exchange(s) before providing the same to any third party. | This regulation is to ensure the regular flow of information from issuers to investors, to maintain information symmetry. This is typical for all listed securities – for example, Reg 30 in case of listed equities, and reg 51 in case of listed non convertible debt securities. |

| Credit Rating to be periodically reviewed and any revision to be notified | Reg 84 | (1) Every rating obtained by the listed entity with respect to securitised debt instruments shall be periodically reviewed, preferably once a year, by a credit rating agency registered by the Board.(2) Any revision in rating(s) shall be disseminated by the stock exchange(s). | This Regulation requires a mandatory annual review of credit ratings on the SDIs by a SEBI-registered CRA, and intimation of any revision to the stock exchanges. |

| Information to Investors | Reg 85 | (1) The listed entity shall provide either by itself or through the servicer, loan level information without disclosing particulars of individual borrower to its investors.(2) The listed entity shall provide information regarding revision in rating as a result of credit rating done periodically in terms of regulation 84 above to its investors.(3) The information at sub-regulation (1) and (2) may be sent to investors in electronic form/fax if so consented by the investors.(4) The listed entity shall display the email address of the grievance redressal division and other relevant details prominently on its website and in the various materials / pamphlets/ advertisement campaigns initiated by it for creating investor awareness. | This clause requires certain pool level information; useful information for the poolComment: As in case of other jurisdictions, the disclosure requirements are typically laid by the securities regulations |

| Terms of Securitized Debt Instruments | Reg 86 | (1) The listed entity shall ensure that no material modification shall be made to the structure of the securitized debt instruments in terms of coupon, conversion, redemption, or otherwise without prior approval of the recognised stock exchange(s) where the securitized debt instruments are listed and the listed entity shall make an application to the recognised stock exchange(s) only after the approval by Trustees.(2) The listed entity shall ensure timely interest/ redemption payment.(3) The listed entity shall ensure that where credit enhancement has been provided for, it shall make credit enhancement available for listed securitized debt instruments at all times.(4) The listed entity shall not forfeit unclaimed interest and principal and such unclaimed interest and principal shall be, after a period of seven years, transferred to the Investor Protection and Education Fund established under the Securities and Exchange Board of India (Investor Protection and Education Fund) Regulations, 2009.(5) Unless the terms of issue provide otherwise, the listed entity shall not select any of its listed securitized debt instruments for redemption otherwise than on pro rata basis or by lot and shall promptly submit to the recognised stock exchange(s) the details thereof.(6) The listed entity shall remain listed till the maturity or redemption of securitised debt instruments or till the same are delisted as per the procedure laid down by the BoardProvided that the provisions of this sub-regulation shall not restrict the right of the recognised stock exchange(s) to delist, suspend or remove the securities at any time and for any reason which the recognised stock exchange(s) considers proper in accordance with the applicable legal provisions. | This requires prior approval of the stock exchange to be obtained for making any material modification to the structure of SDIs. It also requires the originator to ensure timely payments of interest and for the credit enhancement to be available at all times. |

| Record Date | Reg 87 | (1) The listed entity shall fix a record date for payment of interest and payment of redemption or repayment amount or for such other purposes as specified by the recognised stock exchange(s).(2) The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to the recognised stock exchange(s) of the record date or of as many days as the Stock Exchange may agree to or require specifying the purpose of the record date. | This is for fixation of record date for payouts; useful for investor decisions for entry or exit. |

| Disclosure of Information having bearing on performance/ operation of listed entity and/ or price sensitive information | Part D of Schedule III | Several disclosure requirements for significant events and developments | See comments under reg 83 |

Other Resources: Buy our book on Securitised Debt Instruments here.

Repetitive Overhaul: RPT regime to get softer

– Team Corplaw | corplaw@vinodkothari.com

SEBI rolls out Consultation Paper: Materiality threshold for RPTs to be scale-based, Industry Standard to get softer, de minimis exemptions

Since 2021, the RPT framework for listed entities has been witnessing repetitive changes, and the current year 2025 has seen SEBI on a regulatory fast track in relation to RPTs. Be it the launch of RPT Analysis Portal, offering unprecedented visibility into RPT governance data, or the Industry Standards Note (‘ISN’), requiring seemingly a pile of information w.r.t RPTs, both in the month of February, 2025. Originally scheduled to be effective from FY 25, the applicability of ISN was later pushed on to July 1, 2025, and while on the verge of becoming effective, on June 26, 2025, SEBI notified Revised RPT Industry Standards, prescribing tiered but somewhat simplified disclosure formats effective September 1, 2025.

Even before the ISN could become effective, a 32-pager consultation paper proposing further amendments to RPT provisions has been rolled out by SEBI on August 4, 2025.

Based on the “Ease of Doing Business” theme, the Consultation Paper proposes amendments in the RPT framework, based on recommendations from the Advisory Committee on Listing Obligations and Disclosures (ACLOD). The proposals aim to address practical challenges faced by listed entities while maintaining robust governance standards.

Below we present the proposed amendments and our analysis of the same.

1. Materiality Thresholds: From One-Size-Fits-All to several sizes for short-and-tall

Proposal in CP

A scale-based threshold mechanism is proposed through a new Schedule XII to LODR Regulations, such that the RPT materiality threshold increases with the increase in the turnover of the company, though at a reduced rate, thus leading to an appropriate number of RPTs being categorized as material, thereby reducing the compliance burden of listed entities. The maximum upper ceiling of materiality has been kept at Rs. 5,000 crores, as against the existing absolute threshold of Rs. 1000 crores.

Proposed materiality thresholds:

| Annual Consolidated Turnover of listed entity (in Crores) | Proposed threshold (as a % of consolidated turnover) | Maximum upper ceiling (in Crores) |

| < Rs.20,000 | 10% | 2,000 |

| 20,001 – 40,000 | 2,000 Crs + 5% above Rs. 20,000 Crs | 3,000 |

| > 40,000 | 3,000 Crs + 2.5% above Rs. 40,000 Crs | 5,000 (as proposed) |

Back-testing the proposal scale on RPTs undertaken by top 100 NSE companies show a 60% reduction in material RPT approvals for FY 2023-24 and 2024-25 with total no. of such resolutions reducing from 235 and 293, to around 95 to 119. The 60% reduction may itself be seen as a bold admission that the present framework is causing too many proposals to go for shareholder approval.

Historical Benchmark

The absolute threshold of Rs. 1000 crores, for determination of RPTs as material was brought pursuant to an amendment in November 2021, following the recommendations of the Working Group on RPTs. The proposal of WG was based on the data between the years 2015 to 2019, which showed that only around 70 to 91 resolutions were placed for material RPT approvals by the top 500 listed entities.

Our Analysis and Comments

- Turnover as a single metric is not a measure of materiality: Scale-based tests align materiality with turnover, introducing proportionality, but the question remains whether turnover itself is at all an appropriate yardstick to measure materiality.

Turnover is an inadequate metric for determining the materiality of RPTs. Materiality should reflect the likely financial impact of a transaction, which may have little or no correlation with turnover. For instance, transactions involving investments, asset acquisitions or disposals, or borrowings pertain to the balance sheet rather than the revenue-generating side of operations. Even if an item pertains to revenues, there are businesses where gross profits ratios are low, and therefore, turnover will be high. Globally, jurisdictions like the UK adopt a more nuanced, consonance-based approach [Refer Annex 1 of UKLR 7] using different parameters viz. gross assets test, consideration test, and the gross capital test for different transaction types to ensure relevance and proportionality. Section 188 of the Companies Act, 2013 also adopts a similar multi-metric approach, applying turnover and net worth, depending on the nature of the transaction.

It is also critical to recognise the wide disparity in asset-turnover ratio across industries. A trading company might turn its assets over 20 times annually, while a manufacturing entity with a 90-day working capital cycle may show a turnover approximately four times its assets. On the other hand, entities in the financial sector, such as NBFCs and banks, generate turnover largely through interest income, which is barely 6 to 10 percent of the asset base. Therefore, applying a turnover-based threshold to such entities results in thresholds being disproportionately low when compared to the actual scale of transactions, thereby distorting the materiality assessment.

Given these sectoral variations and the diversity of transaction types, a flat turnover-based threshold oversimplifies the assessment and may result in both overregulation and underreporting. A more calibrated, transaction-specific materiality framework, drawing on consonance-based criteria as seen in Regulation 30 of the LODR Regulations, would offer a more balanced and effective approach. SEBI may consider moving towards such a harmonised model to ensure that materiality thresholds meaningfully reflect the substance of transactions, rather than relying on a single yardstick.

- Regulatory Lag: It took SEBI almost 4 years, i.e., from 2021 to 2025, to conclude that the threshold of ₹1,000 crores is too small, and that it requires an upward revision, which is now proposed to be increased to ₹5,000 crores. In the context of India’s rapidly growing economy, where turnover figures are expected to rise steadily, even this upwardly revised absolute threshold may soon lose relevance. Frequent threshold shifts risk “chasing” market realities rather than anticipating them. SEBI’s decision to cap at ₹5,000 crore reflects caution but may quickly become outdated.

2. Significant RPTs of Subsidiaries: Plugging Gaps with Dual Thresholds

Existing provisions vis-a-vis Proposal in CP

Pursuant to the amendments in 2021, RPTs exceeding a threshold of 10% of the standalone turnover of the subsidiary are considered as Significant RPTs, thus, requiring approval of the Audit Committee of the listed entity. The CP proposes the following modifications with respect to the thresholds of Significant RPTs of Subsidiaries:

- ‘Material’ is always ‘Significant’: There may be instances where a transaction by a subsidiary may trigger the materiality threshold for shareholder approval, based on the consolidated turnover of the listed entity, but still fall below the 10% threshold of the subsidiary’s own standalone turnover. As a result, such a transaction would escape the scrutiny of the listed entity’s audit committee. This inconsistency highlights a regulatory gap and reinforces the need to revisit and revise the threshold criteria to ensure comprehensive oversight in a way that aligns with evolving group structures and scale of operations. RPTs of subsidiary would require listed holding company’s audit committee approval if they breach the lower of following limits:

- 10% of the standalone turnover of the subsidiary or

- Material RPT thresholds as applicable to listed holding company

- Exemption for small value RPTs: The threshold for Significant RPTs is subject to an exemption for small value RPTs based on the absolute value of Rs. 1 crore. Thus, where a transaction between a subsidiary and a related party (of the listed entity/ subsidiary), on an aggregate, does not exceed Rs. 1 crore, the same is not required to be placed for approval of the Audit Committee of the listed entity, even if the aforesaid limits are breached.

- Net Worth Alternative: For newly incorporated subsidiaries which are <1 year old, consequently not having audited financial statements for a period of at least one year, the threshold for Significant RPTs to be determined as below:

- 10% of standalone net worth of the subsidiary (or share capital + securities premium, if negative net worth),

- as on a date not more than 3 months prior to seeking AC’s approval

- certified by a practising CA

Our Analysis and Comments

● De-minimis exemption for significant RPTs of subsidiaries

The exemption for RPTs up to Rs. 1 crore in absolute terms might provide some relief for the holding entities, particularly, entities having various small subsidiaries, which, on a standalone basis, may not be material for the listed entity at all – however, the RPTs being significant at the subsidiary’s level still required approval of the parent’s audit committee. However, still the exemption threshold may be further enhanced to a higher limit, as a de minimis exemption of Rs. 1 crore entails the subsidiary having a turnover of mere Rs. 10 crores, which, from the perspective of a listed entity is a not a very practically beneficial scenario.

For newly incorporated companies not having a financial track record, linking the significant RPT threshold with net worth brings additional compliance burden in the form of certification requirements from PCA. Net worth alternative introduces valuation and certification burdens for newly incorporated entities, in which case It may be considerable to extend a blanket first year exemption of upto Rs. 5 crore, to balance ease of doing business for newly incorporated subsidiaries, the very decision of which would be stemming from the management of the parent listed entity. In fact, insisting on the net worth certificate itself seems unnecessary, as the net worth is mostly based on paid up capital, which does not warrant certification.

● Need for easing inclusion of RPs of subsidiaries as RPs of listed entity

First of all, a statement of fact. The number of related parties of listed entities went for a significant explosion in November, 2021, where the definition of RP of a listed entity included RPs of subsidiaries. For any diversified group, there are typically several subsidiaries, each of them with their own independent boards.

While the proposals pertain to significant RPTs of subsidiaries, the most crucial component of the RPT framework lies in identification of RPs, which, under the current framework, covers RPs of subsidiaries as well. These RPs may be, many a times, companies in which the directors of the subsidiaries are holding mere directorships, often, an independent directorship. There is absolutely no scope of conflict of interests in dealing with companies where a person is interested, solely on account of his directorship where there is no direct or indirect shareholding or ownership interest. Such a situation has an explicit carve out under the Ind AS 24 as well, where an entity does not become a RP by the mere reason of having a common director or KMP [Para 11(a) of Ind AS 24]. While the Companies Act treats a company as an RP based on common directorship (in case of a private company), however, the extension of such definition to RPs of subsidiaries is pursuant to the provisions of SEBI LODR and hence, appropriate exclusions may be specified for under LODR.

3. Tiered Disclosures: Balancing Transparency and Burden

Existing provisions vis-a-vis Proposal in CP

The Industry Standards Note on RPTs, effective from 1st September, 2025 provides an exemption from disclosures as per ISN for RPTs aggregating to Rs. 1 crore in a FY. The proposal seeks to provide further relief from the ISN, by introducing a new slab for small-value RPTs aggregating to lower of:

- 1% of annual consolidated turnover of the listed entity as per the last audited financial statements, or

- Rs. 10 crore

In such cases, the disclosures are proposed to be given in the Annexure-2 of the Consultation Paper. The disclosure as per the Annexure is in line with the minimum information as is currently required to be placed by the listed entity before its Audit Committee in terms of SEBI Circular dated 22nd November, 2021 (currently subsumed in LODR Master Circular dated November 11, 2024). In the event of the same becoming effective, disclosures would be required in the following manner as per LODR:

| Value of transaction | Disclosure Requirements | Applicability of ISN |

| < Rs. 1 crore | Reg 23(3) of SEBI LODR | NA – exempt as per ISN |

| > Rs 1 crore, but less than 1% of consolidated turnover of listed entity or Rs. 10 crores, whichever is lower (‘Moderate Value RPTs’) | Annexure-2 of CP (Paragraph 4 under Part A of Section III-B of SEBI Master Circular dated November 11, 2024) | Proposed to be exempt from ISN |

| Other than Moderate Value RPTs but less than Material RPTs (specified transactions) | Part A and B of ISN | Yes |

| Material RPTs (specified transactions are material) | Part A, B and C of ISN | Yes |

| Other than Moderate Value RPTs but less than Material RPTs (other than specified transactions) | Part A of ISN | Yes |

Our Analysis and Comments

The proposal would result in creation of multiple reference points with respect to disclosure requirements. As per the existing regulatory requirements, the disclosure requirements before the Audit Committee comes from the following sources:

- Rule 6A of Companies (Meetings of Board and its Powers) Rules, 2014 – for listed entities incorporated as a company

- Reg 23(3)(c) of SEBI LODR – for omnibus approvals

- SEBI Circular dated 26th June, 2025 read with Industry Standards Note on RPTs – effective from 1st September 2025, for all RPTs other than exempted RPTs (aggregate value of upto Rs. 1 crore)

The proposal leads to an additional classification of RPTs into moderate value RPTs where limited disclosures in terms of the draft Circular will be applicable. While the introduction of differentiated disclosure thresholds aims to rationalise compliance, care must be taken to ensure that the disclosure framework does not become overly template-driven. RPTs, by nature, require contextual judgment, and a uniform disclosure format may not always capture the nuances of each case. It is therefore important that the regulatory design continues to place trust in the informed discretion of the Audit Committee, allowing it the flexibility to seek additional information where necessary, beyond the prescribed formats.

4. Clarification w.r.t. validity of shareholders’ Omnibus Approval

Existing provisions vis-a-vis Proposal in CP

The existing provisions [Para (C)11 of Section III-B of LODR Master Circular] permit the validity of the omnibus approval by shareholders for material RPTs as:

- From AGM to AGM – in case approval is obtained in an AGM

- One year – in case approval is obtained in any other general meeting/ postal ballot

A clarification is proposed to be incorporated that the AGM to AGM approval will be valid for a period of not more than 15 months, in alignment with the maximum timeline for calling AGM as per section 96 of the Companies Act.

Further, the provisions, currently a part of the LODR Master Circular, are proposed to be embedded as a part of Reg 23(4) of LODR.

5. Exemptions & Definitions: Pruning Redundancies

Problem Statement

Proviso (e) to Regulation 2(1)(zc) of the SEBI LODR Regulations exempts transactions involving retail purchases by employees from being classified as Related Party Transactions (RPTs), even though employees are not technically classified as related parties. Conversely, it includes transactions involving the relatives of directors and Key Managerial Personnel (KMPs) within its ambit. Additionally, Regulation 23(5)(b) provides an exemption from audit committee and shareholder approvals for transactions between a holding company and its wholly owned subsidiary. However, the term “holding company” used in this context has remained undefined, leaving ambiguity as to whether it refers only to a listed holding company or includes unlisted ones as well.

Proposal in CP

The Consultation Paper proposes two key clarifications:

- The exemption related to retail transactions should be expressly limited to related parties (i.e., directors, KMPs, or their relatives) to grant the appropriate exemption.

- The exemption for transactions with wholly owned subsidiaries should apply only where the holding company is also a listed entity, thereby excluding unlisted holding structures from this relaxation

Our Analysis and Comments

Under the existing framework, retail purchases made on the same terms as applicable to all employees are exempt when undertaken by employees, but not when made by relatives of directors or KMPs. This has led to an inconsistent treatment, where similarly situated individuals receive different regulatory treatment solely on the basis of their relationship with the company. The proposed language attempts to streamline this by including such relatives within the exemption, but it introduces its own drafting concern.

- The phrasing – “retail purchases from any listed entity or its subsidiary by its directors or its

employeeskey managerial personnel(s) or their relatives, without establishing a business relationship and at the terms which are uniformly applicable/offered to allemployees anddirectors and key managerial personnel(s)” – creates a potential loophole. As worded, the exemption could be interpreted to cover purchases made on favourable terms offered to directors or KMPs themselves, rather than being benchmarked against terms applicable to employees at large. The intended spirit of the provision seems to be to exempt only those transactions where the terms are genuinely uniform and non-preferential. A more appropriate construction would make it clear that the exemption is intended to apply only where such transactions mirror employee-level retail transactions, not privileged arrangements for senior management. - Regarding the exemption under Regulation 23(5)(b) for transactions between a holding company and its wholly owned subsidiary, this clarification seeks to align the treatment under Regulations 23(5)(b) and 23(5)(c). While this provides helpful interpretational guidance, incorporating the word “listed” directly into the text of the Regulation itself could offer greater precision and eliminate the need for retrospective explanations. Since unlisted holding companies are not subject to LODR, they are unlikely to have interpreted the exemption as applicable in the first place. As such, a simple prospective clarification might serve the purpose more effectively.

Conclusion

SEBI’s August 2025 proposals are largely aimed at relaxation, though in some cases, the ability to think beyond the existing track of the law seems missing. With the new leadership at SEBI meant to rationalise regulations, it was quite an appropriate occasion to do so. However, at many places, the August 2025 proposals are simply making tinkering changes in 2021 amendments and fine-tuning the June 2025 ISN. In sum, SEBI’s iterative approach to RPT governance demonstrates commendable responsiveness but calls for a holistic RPT policy road-map, harmonizing LODR regulations, circulars, and guidelines. Only a forward-looking, principles-based framework, will deliver the twin objectives of ease of doing business and investor protection in the long run.

Read More:

FAQs on Standards for minimum information to be disclosed for RPT approval

Tailored to Fit Practically: Disclosure for RPTs under Revised Industry Standards

Round-Tripping Reined: RBI Rolls Out Relaxed Rules for Investments in AIFs

-Sikha Bansal, Senior Associate & Harshita Malik, Executive | finserv@vinodkothari.com

Background

The RBI’s regulatory approach to investments by Regulated Entities (REs) in Alternate Investment Funds (AIFs) has undergone a remarkable transformation over the past two years. Initially, the RBI responded to the risks of “evergreening”, where banks and NBFCs could mask bad loans by routing fresh funds to existing debtor companies via AIF structures, by issuing stringent circulars in December 20231 and March 20242 (collectively known as ‘Previous Circulars’). The December 2023 circular imposed a blanket ban on RE investments in AIFs that had downstream exposures to debtor companies, while the March 2024 clarification excluded pure equity investments (not hybrid ones) from this restriction. This stance aimed to strengthen asset quality but quickly highlighted significant operational and market challenges for institutional investors and the AIF ecosystem. Many leading banks took significant provisioning losses, as the Circulars required lenders to dispose off the AIF investments; clearly, there was no such secondary market.

In response to the feedback from the financial sector, as well as evolving oversight by other regulators like SEBI, the RBI undertook a comprehensive review of its framework and issued Draft Directions- Investment by Regulated Entities in Alternate Investment Funds (‘Draft Directions’) on May 19, 20253. The Draft Directions have now been finalised as Reserve Bank of India (Investment in AIF) Directions, 2025 (‘Final Directions’) on 29th May, 2025. The Final Directions shift away from outright prohibitions and instead introduce a carefully balanced regime of prudential limits, targeted provisioning requirements, and enhanced governance standards.

Comparison at a Glance

A compressed comparison between Previous Circulars and Final Directions is as follows –

| Particulars | Previous Circulars | Final Directions | Intent/Implication |

|---|---|---|---|