Strengthening India’s Corporate Bond Market: A Look at NITI Aayog’s Recommendations

Simrat Singh | finserv@vinodkothari.com

India’s aspiration to become a US $30 Trillion economy by 2047 rests on its ability to mobilise long-term, stable and affordable capital. Debt capital can be an attractive source for this. While banks have historically been the backbone of credit intermediation in India, a bank-dominated financial system may be inadequate to meet the financing needs of a developing country like India which includes long-gestation exposures to infrastructure, climate transition, manufacturing and other emerging sectors. Recognising this constraint, NITI Aayog’s report on Deepening the Corporate Bond Market in India (‘Report’) lays out reforms to develop corporate bonds as another major tool for mobilising long-term low-cost capital.

In this note we highlight some of the reforms being advocated in the Report.

Key Thrust Areas of Reforms:

Regulatory Efficiency

A central theme of the Report is the need to reduce regulatory friction arising from fragmented and overlapping oversight by SEBI, RBI and the MCA for corporate bonds. Inconsistent treatment of similar bonds, procedural complexity, overlapping disclosures and different approval timelines are identified as major constraints, particularly for public issuances and lower-rated issuers. A specific concern highlighted is issuer-based regulation: bonds issued by banks and NBFCs are regulated by the RBI, while similar bonds issued by non-financial corporates fall under SEBI and MCA oversight. This results in different disclosure standards and compliance processes for similar bonds

To combat this, first, the Report calls for stronger inter-regulatory coordination and recommends measures such as mutual recognition of disclosures, a joint regulatory help desk/single point of contact as well as joint circulars detailing the jurisdictions of each regulator – essentially a centralised coordination mechanism involving SEBI, RBI, MCA and the Ministry of Finance.

Second, the Report emphasises the need to rationalise disclosure norms for public bond issuances, which are significantly more onerous than those applicable to private placements. This asymmetry has led to an overwhelming reliance on private placements, which account for nearly 98% of corporate bond issuances in India (p. 25). Drawing on global practices, the Report recommends a differentiated disclosure regime for well-compliant issuers (p. 66). Specific reforms include extending the validity of offer documents from one year to two or three years, removing ISIN-wise issuance constraints, simplifying PAS-2 and Information Memorandum filings through digital automation on the MCA portal, and introducing a “Well-Known Seasoned Issuer” framework to enable fast-track access to public bond markets for reputed issuers.

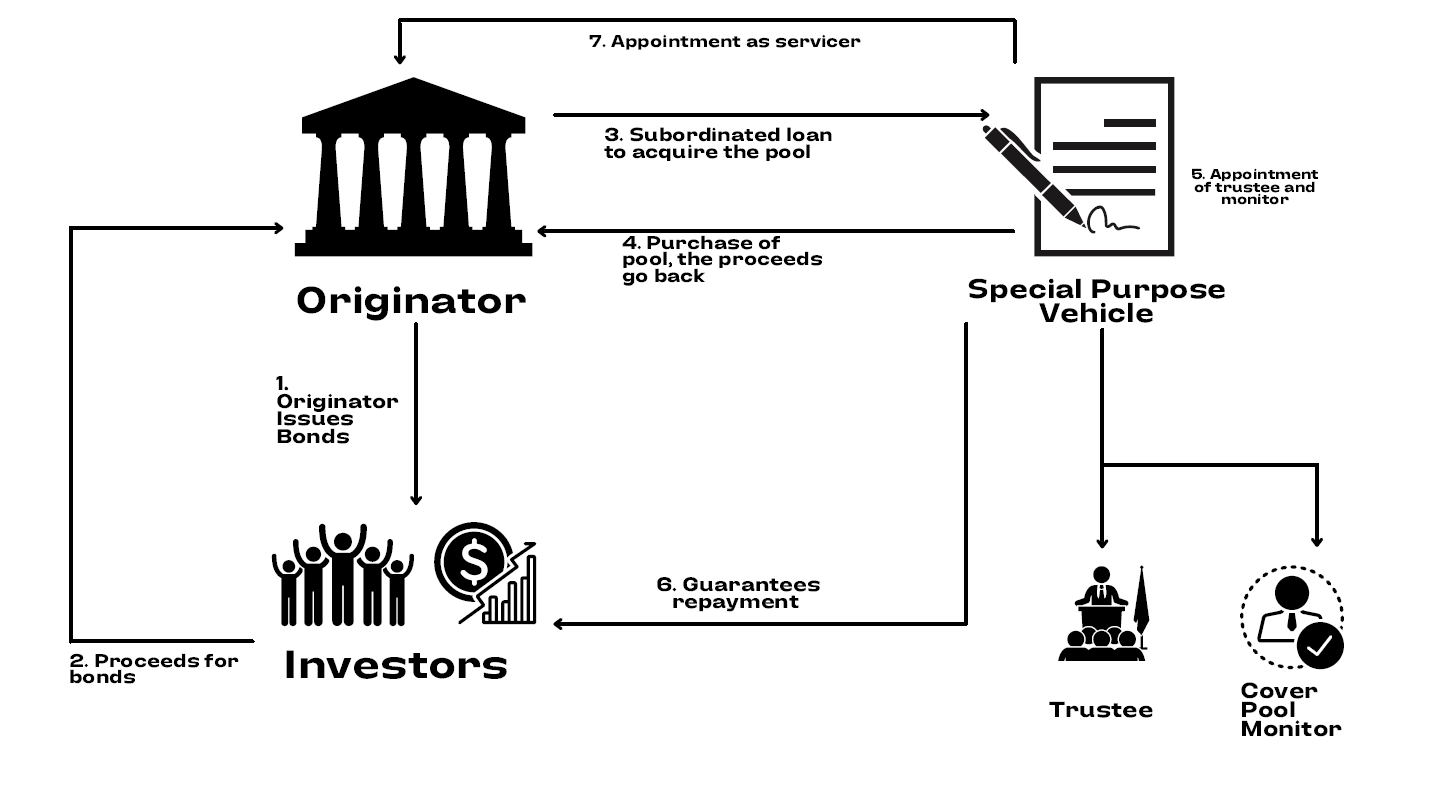

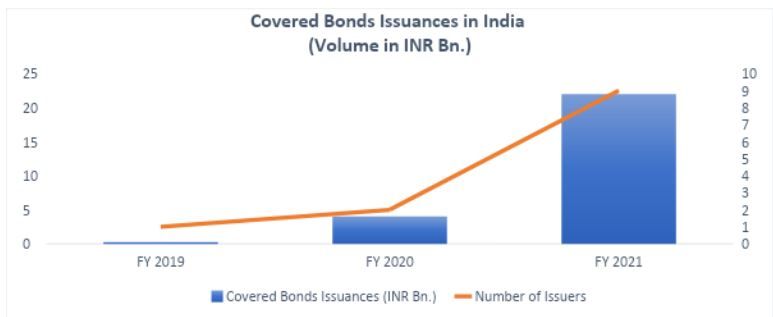

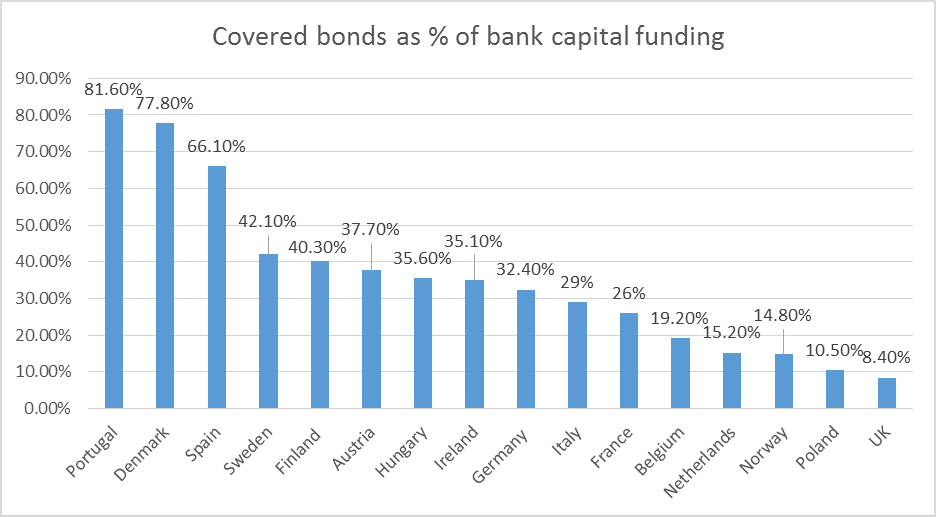

Third, the Report stresses the need for regulatory clarity for hybrid instruments, including covered bonds1, securitised debt and infrastructure-linked securities. Many instruments used globally to fund long-term assets do not fit neatly within India’s regulator-specific silos. Jurisdictional ambiguity (which regulator oversees which instrument?) and the absence of standardised regulatory treatment have impeded market development. The Report recommends clearly defined frameworks to facilitate market clarity. In this context, it also highlights tax distortions; for instance, SDIs2 currently attract significantly higher TDS than corporate bonds. The Report states that SDIs are taxed at a higher rate than corporate bonds which prevents securitisation of bonds. However, effective 1.04.2025, SDI TDS rates are aligned with bond rate; both at 10% (See section 194LBC of Tax Act).

Market Infrastructure and Liquidity

Bonds are heterogeneous instruments, varying by type of issuer, tenor, covenants and structure. Unlike equities, electronic order matching alone cannot ensure immediacy of execution or continuous liquidity in the secondary market, particularly in lower-rated or infrequently traded bonds. Despite progress through electronic platforms such as RFQ for secondary trading and EBP for primary issuance, trading volumes remain shallow and concentrated in highly rated bonds.

The Report recommends expanding electronic trading, enhancing post-trade reporting (to improve price discovery) and increasing the proportion of trades settled on a Delivery-versus-Payment (DVP) basis3. Absence of a robust market-making ecosystem is seen as a major constraint on secondary-market liquidity (pp. 22, 36, 106). Limited risk appetite and balance-sheet constraints deter intermediaries from providing continuous two-way quotes, especially in lower-rated and longer-tenor bonds.

To address this, the Report recommends enabling market-making through regulatory incentives and improved access to repo markets. In particular, the creation of a standing repo facility by RBI for high rated corporate bonds would allow market makers4 to monetise inventories efficiently and support continuous liquidity provision. While corporate bonds are included in the RBI’s list of repo-eligible instruments, their treatment differs materially from Government securities (G-Secs). Repos in G-Secs are exempt from CRR and SLR computation which means Banks can access funds through G-Sec repos without providing SLR and CRR on those funds. In contrast, cash raised through repos backed by corporate bonds is treated as a liability for CRR and SLR purposes, hence banks have to provide CRR and SLR on the resulting liquidity. Also, unlike G-Secs, which are centrally cleared and settled through CCIL, corporate bond repos lack a single, standardised clearing and settlement mechanism; they are cleared through F-TRAC and stock exchanges. The result is that the volume of corporate bond repo is negligible (exact data on corporate bond repo could not be sourced).

The Report also flags structural weaknesses in the credit rating ecosystem, including rating inflation, conflicts of interest under the issuer-pays model, and excessive regulatory reliance on ratings (p. 71). Strengthening governance standards is the key recommendation for credit ratings. To improve credit rating access for smaller issuers, the Report suggests exploring alternative credit assessment models, including technology-driven frameworks using GST-returns and other turnover based data and digital transaction histories.

Further, the Report recommends strengthening the existing framework requiring large corporates to raise a portion of incremental borrowings through debt securities (LCB Framework)5. Proposed enhancements include increasing the minimum market borrowing requirement and progressively extending the framework to smaller corporates with lower thresholds.

Drawing on the IMF’s FSAP 2025, the Report also recommends allowing high-quality corporate bonds to be used as collateral in RBI’s repo operations. International experience from the ECB, Bank of Japan, and Reserve Bank of Australia suggests that such measures can enhance secondary-market liquidity and broaden the investor base, subject to appropriate safeguards.

Equally important is the creation of a government-backed, centralised corporate bond data repository. Fragmented data across regulators and exchanges currently hampers price discovery and covenant monitoring. A unified, real-time repository is recommended to improve transparency for issuers, investors, and regulators.

Innovation in Instruments and Market design

The Report makes it clear that regulatory reforms alone are insufficient; product and market innovation are essential to expand depth and distribute risk. India’s bond market remains narrow not only due to investor risk aversion but also due to the limited availability of instruments aligned with diverse risk–return preferences and long-gestation financing needs. Green bonds, sustainability-linked bonds6, and transition bonds are identified as important instruments for financing climate action and infrastructure. However, the absence of a standardised green taxonomy and concerns around greenwashing have constrained growth. The Report, therefore, recommends establishing clear definitions, disclosure standards and verification frameworks to ensure credibility and scale ESG-oriented bond markets.

The Report proposes institutionalising a dedicated class of Corporate Bond Dealers (CBDs), modelled on the U.S. primary dealer system. Eligible banks, NBFCs and other financial institutions would be required to provide continuous two-way quotes, supported by incentives such as capital relief on bond inventories and access to RBI refinance and repo facilities. Enhanced market surveillance, real-time trade reporting, price dissemination and inventory disclosures are also recommended.

Investor and Issuer Participation

Broadening the investor base is identified as another critical reform pillar. Long-term institutional investors such as insurance companies, pension funds and provident funds are natural holders of long-duration bonds, yet regulatory investment norms constrain exposure only to higher-rated securities. The Report recommends a calibrated relaxation of these norms.

For retail investors, the Report proposes lowering minimum investment thresholds (from existing ₹ 10,000), increasing retail quotas in public bond issuances, particularly for tax-free and ESG-linked bonds7, and simplifying TDS provisions to address tax inefficiencies in secondary market trades. OBPPs have been acknowledged to contribute to secondary market liquidity, however, the volumes are low. Further, there is no mention of concerns w.r.t downselling through OBPPs which was recently highlighted by SEBI8

On the issuer side, India’s corporate bond market remains heavily concentrated among AAA and AA-rated entities. To address this imbalance, the Report advocates scaling up credit enhancement mechanisms such as PCEs and support from development finance institutions. It also highlights the need to promote longer-tenor issuances, especially for infrastructure and climate-linked projects, where asset lives significantly exceed typical corporate bond maturities. In this context, it is noteworthy that NITI Aayog has cited our resource, “Partial Credit Enhancement: A Catalyst for Boosting Infrastructure Bond Issuances?”, in the Report while discussing the role of partial credit enhancement mechanisms in deepening the corporate bond market (pp. 75 and 99). Further, regulatory subsidies for first-time or low-volume issuers and pooled issuance platforms to facilitate market access for smaller issuers is also recommended (pp. 65, 75).

The Report recognizes that CDS are underdeveloped. Currently, CDS can be purchased only by investors who already own the underlying bond, which prevents trading in the CDS market. Further, only single-name CDS are permitted, which means a separate CDS contract is required for each issuer, unlike global markets such as the U.S., where index CDS allows one CDS to cover a basket of bonds. Lastly, there is a limit on FPI investors providing CDS which is 5% of the outstanding corporate bond market. These restrictions have resulted in limited CDS protection. The Report also recommends bigger NBFCs to act as CDS market makers

Conclusion

NITI Aayog’s recommendations envisage a corporate bond market that evolves from a supplementary funding channel into a core pillar of India’s financial system. If implemented in a coordinated manner, these reforms could expand the market to ₹100–120 trillion by 2030, improve financial stability, and channel long-term capital into productive investment. The real challenge, however, lies in execution, particularly in achieving sustained regulatory coordination and market-making capacity. Addressing these constraints will be critical if corporate bonds are to play a meaningful role in financing India’s long-term growth and infrastructure ambitions under the vision of Viksit Bharat by 2047.

See our other resources on bonds

- Bond Credit Enhancement Framework: Competitive, rational, reasonable

- Demystifying Structured Debt Securities: Beyond Plain Vanilla Bonds

- Bond market needs a friend, not parent

- SEBI Securitisation Regulations: Track Record, Risk retention and Investment size among several new requirements

- Mandatory listing for further bond issues

- NHB’s PCE Scheme for HFCs

- Corporate Bonds and Debentures

- Covered bonds are secured debt instruments backed by a segregated pool of high-quality assets, offering investors dual recourse to both the issuer and the underlying assets. May refer to our resource on covered bonds. ↩︎

- May refer to our book Listing Regulations on Securitised Debt Instruments and Security Receipts ↩︎

- DVP is a settlement mechanism in which the transfer of securities and funds occurs simultaneously, eliminating counterparty and settlement risk

↩︎ - May refer to our resource ‘Bond issuers set to become Market Maker to enhance liquidity’ ↩︎

- May refer to our resource ‘Mandatory bond issuance by Large Corporates: FAQs on revised framework’ ↩︎

- May refer to our resources ‘Sustainability or ESG Bonds’ and ‘From Rooftops to Ratings: India’s Green Securitisation Debut’ ↩︎

- May refer to our resource ESG Debt Securities: Framework for Issuance and Listing in India ↩︎

- May refer to our resource “Downstreamed through intermediaries: Deemed public issue concerns for privately placed debt” ↩︎