When AIF Regulations were formally introduced in 2012, the regulatory approach was deliberately light. The framework targeted sophisticated investors, allowing flexibility with limited oversight. Over the years, however, AIFs have become significant participants in capital markets. Market practices over the decade exposed regulatory loopholes and arbitrages. For example, some investors who did not individually qualify as QIBs accessed preferential benefits indirectly through AIF structures and investors who were restricted to invest in certain companies started investing through AIF making AIF an investment facade. There were concerns regarding circumvention of FEMA norms as well1. In the credit space, regulated entities such as banks and NBFCs started channeling funds through AIFs to refinance their stressed borrowers, raising concerns around loan evergreening2. These developments prompted regulatory response. RBI first issued two circulars, one in 2023 and the other in 2024. Finally, in 2025 formal directions governing investments by regulated entities in AIFs were also issued3. These Directions introduced exposure caps and provisioning requirements.4

While the RBI addressed prudential risks arising from regulated entities’ participation in AIFs, SEBI focused on investor protection, governance within the AIF ecosystem and curbing the regulatory arbitrages. First it mandated on-going due diligence by AIF Managers5. It then mandated specific due diligence6 of investors and investments of AIF to prevent indirect access to regulatory benefits. Fiduciary duties of sponsors and investment managers and reporting obligations were progressively codified through circulars. Managers were expected to maintain transparency vis-a-vis their investment decisions, maintain written policies including ones to deal with conflict of interest with unitholders and submit accurate information to the Trustee. What were once broad, principle-based expectations have evolved into detailed, enforceable rules. Regulatory tightening has been matched by a more assertive enforcement approach. SEBI’s recent settlement order7 against an AIF underscores its increasing scrutiny of governance lapses, mismanagement of conflicts and inaccurate reporting. This clearly signals that any compliance gaps will no longer be overlooked and are likely to attract regulatory action. In a separate adjudication order, SEBI imposed penalties on both the Trustee and the Manager for the delayed winding-up of the scheme, underscoring that accountability within an AIF structure extends to all key parties and is not limited to the Manager alone.

However, SEBI’s approach has not been solely restrictive. Alongside regulatory tightening, it has also sought to preserve commercial flexibility and respond to market needs. Examples include the introduction of the co-investment framework8 for AIFs, framework for offering differential rights to select investors and a revamp for angel funds9.

Together, these measures are reshaping the regulatory landscape for AIFs and their managers. Investors can no longer rely on AIF structures to indirectly obtain regulatory advantages otherwise unavailable to them. As AIFs have grown in scale and importance, what is emerging is a more transparent, prudentially sound and closely supervised regulatory regime designed to align investor protection and commercial flexibility.

See SEBI’s Consultation paper on proposal to enhance trust in the AIF ecosystem ↩︎

See our write-up on AIFs being used for regulatory arbitrages here. ↩︎

See our write-up on changes w.r.t Angel Funds here↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-09 10:45:482025-10-10 10:19:44AIF Regulatory framework evolves from light-touch to right-hold

Within an AIF structure, funds are committed by the investors and the AIF in turn, through its Investment Manager, makes investments in investee entities in line with the fund’s strategy. Situations may arise where an investee company of the AIF may require additional capital, that the Investment Manager may not be willing to provide out of the fund’s corpus possibly due to multiple reasons such as over-exposure, non-alignment with funding strategy, capital constraints etc.

In such cases, the Manager may encourage investors to commit further funds directly into the investee. This gives rise to what is known as ‘co-investment’ –an investment by limited partners (LPs or investors) in a specific investee alongside, but distinct from, the flagship fund. Globally, these are also called ‘Sidecar’ funds or ‘parallel’ funds.1

Benefits of co-investments

Investors benefit from co-investments primarily in terms of cost efficiency, in the following ways:

No or lower management fees and a reduced rate of carried interest.2

Reducing/ removing operational and administrative expenses such as in due diligence process & deal sourcing

Where management and incentive fees are directly charged on co-investments, they are usually capped and lower than when investing directly into the PE Fund.3

Not only are headline rates4 typically lower, but management fees are often charged on invested rather than committed capital, reducing fee drag and mitigating the J-Curve.5

For Managers co-investment offers the following advantages:

Provide access to expanded capital;

Enables it to pursue larger transactions without over extending the main fund

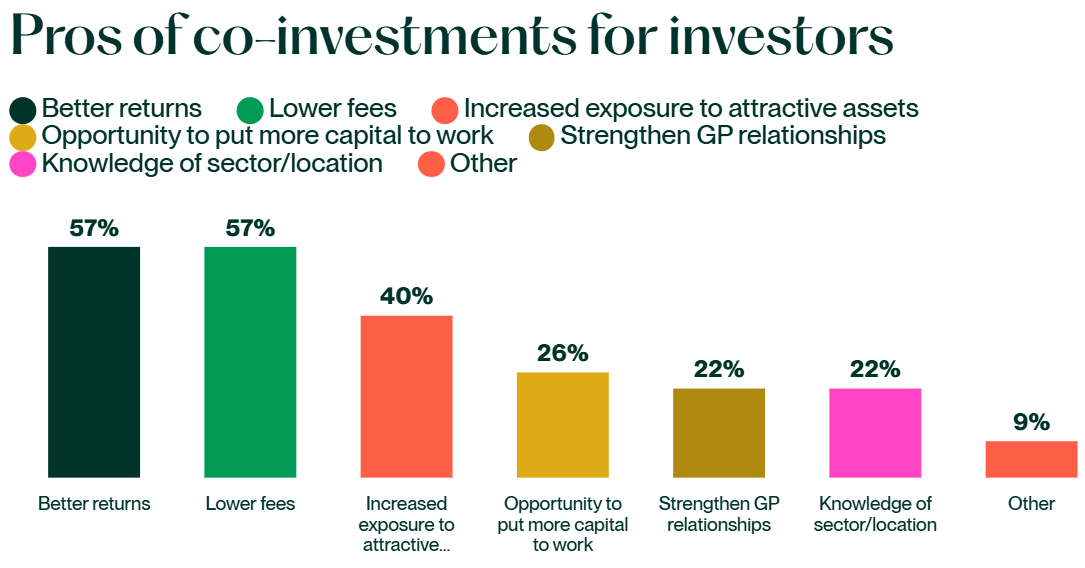

A Preqin study6 found that 80% of LPs reported better performance from equity co-investments than traditional fund structures.

Fig 2: Investor’s perceived benefits of co-investment

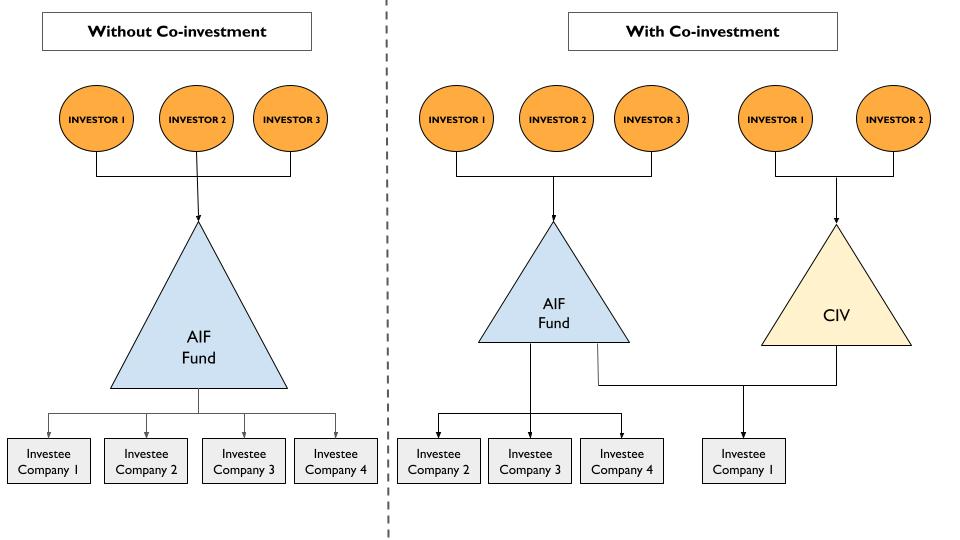

Co-investments by AIF investors in the investees of AIF were primarily offered in accordance with the SEBI (Portfolio Managers) Regulations, 2020 (“PM Regulations”). In 2021, PM Regulations were amended to regulate AIF Managers offering co-investments by acting as a portfolio manager of the investors (see need for regulating the co-investment structure below). The AIF Regulations, in turn, required the investment manager to be registered under PM Regulations, for providing co-investment related services.

Keeping in view the rising demand for co-investments, SEBI, based on a recent Consultation Paper issued on 9th May 2025, has amended the AIF Regulations, vide notification dated 9th September, 2025 and issued a circular in September 2025 introducing a dedicated framework for co-investments within the AIF regime itself. Note that the recently introduced framework is in addition to and does not completely replace the co-investment framework through PM as provided in the PM Regulations.

The newly introduced framework refers to co-investments as an affiliate scheme within the main scheme of the fund, in the form of a Co-investment Vehicle Scheme (CIV) and does not require a separate registration by the Investment Manager in the form of Portfolio Manager under PM Regulations.

Interestingly, in May 2025, IFSCA also issued a Circular specifying operational aspects for co-investments by venture capital funds and restricted schemes operating in the IFSC. In this article, we discuss the new framework vis-a-vis the existing PMS route.

Need for regulating co-investments

Conflicts of interest

Especially around the timing of exit. Main fund vs. co-investors may have different preferences.

Voting rights alignment

Misalignment can fragment decision-making.

Risk concentration for investors

Exposure to a single company rather than a diversified portfolio.

Disclosure and transparency obligations for managers

Other fund investors need clarity on why the deal was structured as a co-investment.

Questions may arise on whether the main fund had sufficient capacity to invest.

Risk of concerns about preferential treatment of select investors.

Operational issues:

Warehousing: main fund may initially acquire the investment until co-investment vehicle is ready; requires proper compensation to the fund for interim costs.

Expense allocation: management costs must be fairly shared between the fund and the co-investment vehicle.

Co-investment through PMS Route – the existing framework

Under the PMS Route, the AIF Manager intending to offer co-investment opportunities to its investors shall first register itself as a ‘Co-investment Portfolio Manager’ (see reg. 2(1)(fa) of PM Regulations) post which it can invest the funds of investors subject to the following conditions:

100% of AUM shall be invested in unlisted securities [see reg. 24(4B)];

Only a manager of a Cat I & II AIF is allowed to offer co-investment;

The terms of co-investment in an investee company by a co-investor, shall not be more favourable than the terms of investment of the AIF [see proviso to reg. 22(2)]:

Terms relating to exit of co-investors shall be identical to that of exit of AIF [see proviso to reg. 22(2)];

Early termination/withdrawal of funds by co-investor shall not be allowed. [see reg. 24(2)(a)]

The AIF Manager, registered as a Co-investment Portfolio Manager, is subject to all the compliances as required under the PM Regulations, read with the circulars issued thereunder, except the following:

The minimum investment limit of Rs. 50 Lac per investor in case of PMS will not apply [see reg. 23(2)];

Min. net worth criteria of Rs. 5 Crore shall not apply to such a PM [see reg. 11(e)];

Appointment of a custodian is not required. (see reg. 26)

Roles and responsibilities of the compliance officer can be discharged by the principal officer of the Manager. [see reg. 34(1)]

Particulars

Discretionary

Non-discretionary

Co-investment

No. of clients

1,92,548

6,733

609

AUM (Rs. Crores)

33,05,958

3,18,685

4,674

Table 1: No. of co-investment clients and their total AUM as on 31.07.2025.

As per Table 1, it is evident that co-investment under the PMS Regulations has not taken off yet. One of the major reasons is the additional registration & compliance burden associated with this route.

Co-investment through CIV : the recently approved framework

“Co-investment” means investment made by a Manager or Sponsor or investor of a Category I or II Alternative Investment Fund in unlisted securities of investee companies where such a Category I or Category II Alternative Investment Fund makes investment;”

The framework is restricted to “unlisted securities” only, for the following reasons:

There is a greater information symmetry in case of unlisted securities;

In case of investment in listed securities, it is difficult to establish whether an investor’s decision to invest is driven by the fund manager’s advice or based on the investor’s own independent assessment;

Co-investments are typically undertaken in unlisted entities.

Reg 2(1)(fa) defines co-investment scheme as:

“Co-investment scheme” means a scheme of a Category I or Category II Alternative Investment Fund, which facilitates co-investment to investors of a particular scheme of an Alternative Investment Fund, in unlisted securities of an investee company where the scheme of the Alternative Investment Fund is making investment or has invested;”

The conditions for co-investment through the AIF route is prescribed through the newly inserted Reg 17A to the AIF Regulations read with the Circular dated September 09, 2025. Additionally, the Circular also refers to the implementation standards, if any, formulated by SFA with regard to offering of the co-investment schemes by the AIFs. Since the CIV operates as an affiliate AIF, in order to make it operationally feasible, a CIV has been granted the following exemptions under the AIF Regulations [See reg. 17A(10) of AIF Regulations]:

No minimum corpus of ₹20 Cr.

No continuing sponsor/manager interest (2.5%/₹5 Cr).

Exempt from Placement Memorandum contents, filing modalities, tenure requirement.

Exempt from 25% single-investee company concentration limit

Investment via PMS vs Investment via CIV of an AIF

Post the AIF Amendment, investors have a choice for investing either through the PMS Route or through the CIV route under AIF Regulations. A comparison between the 2 routes is listed below:

Aspects

Investing through CIV

Investing through PMS

Regulatory framework

SEBI (Alternative Investment Funds) Regulations, 2012

SEBI (Portfolio Managers) Regulations, 2020

Limit on investment by each investor

Upto 3 times of investment made by such investor in the investee company through AIF.

Directly in the securities of the investee company.

Co-terminus exit

Timing of exit of CIV = Timing of exit of AIF Scheme from such investee company.

Co-terminus exit

Eligibility of investor

Only Accredited Investors

Any investor

No regulatory bypass

CIV cannot: – Give indirect exposure to such investees where direct exposure is not permitted to the investors; – Create situations needing additional disclosures; – Channel funds where investors are otherwise restricted.

Considered as direct investment by the investor.

Ineligibility of investors

Defaulting, excused, or excluded investors of AIF cannot participate in CIV.

No such exclusion. This seems like a regulatory loophole.

Operational burden

CIV aggregates co-investors’ exposure; hence, only the Scheme appears on the capital table; Unified voting and simplification of compliance requirements for investees as well

Multiple co-investors appear directly on the investee company’s cap table. Closing times may be different, and operationally difficult for investors and investees to exercise voting rights and ensure compliances at each investor’s level.

Scope for co-investment

Managers can extend co-investment services to investors of any AIF managed by them (Sponsor may be same or different)

A Co-investment Portfolio Manager can serve only his own AIF’s investors, and others only if managed by him with the same sponsor

Ring-fencing of funds and investments

Separate bank & demat accounts for each CIV

Bank & demat account of investor

Leverage restrictions

CIV cannot undertake any leverage.

The PM cannot undertake leverage and invest.

Taxation

Tax pass through granted to Cat I & II AIFs make the investors directly liable to tax except on business income of the AIF

Capital gain and DDT payable by investor directly

Filing a shelf PM

Managers are required to file a separate Shelf PM for each CIV Scheme.

No such requirement

Conclusion

Much of the future trajectory of co-investments in India will depend on how both investors and managers weigh the relative merits of the PMS and CIV routes. While the PMS framework comes with higher compliance costs and additional registration requirements, the absence of a maximum cap on investments by the co-investors may still serve as a motivational factor for continued usage of the same. By contrast, the CIV framework seeks to simplify execution and preserve alignment with the parent AIF, although the 3 times’ cap on the co-investor’s share may be a hindrance for investors, thus making the CIV structure less attractive. Recently RBI had also issued Directions for regulated entities investing in AIFs with a view to curb evergreening and excessing investing in AIF structures (see our article on the same). The AIF Manager shall be cognizant of these restrictions in order to ensure there is no bypass through CIV.

Large institutional investors, sovereign funds and pension funds are likely to be the early adopters of CIV structures, given their scale, accredited investor status, and preference for alignment with fund managers. High-net-worth individuals (HNIs) and family offices, on the other hand, may still prefer the PMS route owing to its flexibility and direct exposure. Over time, the regulatory tweaking of these frameworks, if any and the appetite of investors for concentrated exposure will determine how the Indian co-investment landscape unfolds.

In private equity, the headline rate (e.g., 2% management fee, 20% carry) is what’s stated in the PPM, but the effective rate investors actually pay is usually lower. This depends on factors like fees on committed vs. invested capital, negotiated discounts or preferential terms, and lifecycle adjustments such as fee step-downs post-investment period. ↩︎

The J Curve represents the tendency of private equity funds to post negative returns in the initial years and then post increasing returns in later years when the investments mature. The negative returns at the onset of investments may result from investment costs, management fees, an investment portfolio that is yet to mature, and underperforming portfolios that are written off in their early days: Corporate Finance Institute↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-18 14:36:572025-09-18 17:12:59CIV-ilizing Co-investments: SEBI’s new framework for Co-investments under AIF Regulations

Since its introduction in 2021, the concept of Accredited Investors (AIs) has been through some changes. A Consultation Paper was published on 17th June, 2025 to provide for certain flexibilities in the accreditation framework. Another Consultation Paper dated 8th August 2025(‘AI CP’) proposed to bring light-touch regulations for AIF schemes seeking investments from only AIs, including extension of various exemptions to such schemes, that are currently available to Large Value Funds (LVFs).

Further, vide another Consultation Paper(‘LVF CP’), some relaxations were also proposed to be extended to Large Value Funds (LVFs) for AIs. Note that the LVFs are available only for AIs, and hence, the Amendment Regulations define the AIs-only schemes to include LVF.

The SEBI (Alternative Investment Funds) (Third Amendment) Regulations, 2025 has been notified on 18th November, 2025, thus introducing the concept of AI-only schemes in the regulatory framework. Note that, vide the 2nd Amendment Regulations, the angel funds have also been exclusively restricted to Accredited Investors only. See an article on the Angel Funds 2.0: Navigating the New Regulatory Landscape.

Accredited Investors – who are they?

An AI is considered as an investor having professional expertise and experience of making riskier investments. Reg 2(1)(ab) of AIF Regulations defines an accredited investor as any person who is granted a certificate of accreditation by an accreditation agency, and specifies eligibility criteria. The eligibility criteria is as follows:

Further, certain categories of investors are deemed to be AIs, that is, certificate of accreditation is not required, such as, Central and State Governments, developmental agencies set up under the aegis of the Central Government or the State Governments, sovereign wealth funds and multilateral agencies, funds set up by the Government, Category I foreign portfolio investors, qualified institutional buyers, etc.

‘Accreditation’ as a measure of risk sophistication

AIFs are investment vehicles pooling funds of sophisticated investors, and not for soliciting money from retail investors. The measure of sophistication, as specified in the AIF Regulations currently, is in the form of the ‘minimum commitment threshold’. Reg 10(c) of the Regulations require a minimum investment of Rs. 1 crore, except in case of investors who are employees or directors of the AIF or of the Manager.

There are certain shortcomings of considering the minimum commitment threshold as the metric of risk sophistication of an investor, such as:

May not necessarily lead to an actual draw-down, thus exposing to the risk of onboarding investors with inflated commitments. As per the data available on SEBI’s website, out of the total commitment of Rs. 13 lac crores for the quarter ended 31st March 2024, only about Rs. 5 lac crores worth of funds were actually drawn down. Similarly, for the quarter ended 31st March 2025, the value of commitment vis-a-vis funds raised

Does not consider the investor’s financial health (income, net worth etc), hence, a potential risk of the investor putting majority of its wealth in AIFs, a riskier investment class.

The concept of AIs, as proposed in February 2021, was to introduce a class of investors who have an understanding of various financial products and the risks and returns associated with them and therefore, are able to take informed decisions regarding their investments. Accreditation of investors is a way of ensuring that investors are capable of assessing risk responsibly.

The June 2025 CP indicated that it is being examined to move AIFs gradually in an exclusively for AIs approach, starting with investments in angel funds and in framework for co-investing in unlisted securities of investee companies of AIFs. Accordingly, the present CP has proposed a gradual and consultative transition from ‘minimum commitment threshold’ to ‘accreditation status’ as a metric of risk sophistication of an investor.

Flexibility for AIs-only schemes vis-a-vis other AIFs

The accreditation status is to be ensured at the time of onboarding of investors only. Therefore, if an investor subsequently loses the status of AI in interim, the same shall still be considered as an AI for the AI only scheme, once on-boarded. The following relaxations have been extended to AIs-only schemes, in order to provide for a light-touch regulatory framework, from investor protection viewpoint, considering that the AIs have the necessary knowledge and means to understand the features including risks involved in such investment products:

This facilitates differential rights to different classes of investors within a scheme.

Extension of tenure of close-ended funds [reg 13(5)]

up to two years subject to approval of two-thirds of the unit holders by value of their investment in AIF

This facilitates a longer tenure extension to an existing close-ended scheme, if suited to investors.

However, it is further clarified that the maximum extension permissible to such AI only schemes, inclusive of any tenure extension prior to such conversion, shall be 5 years.

Certification criteria for key investment team of Manager [reg 4(g)(i)]

Atleast one key personnel with relevant NISM certification

The investors, being accredited, the reliance on key investment team of the Manager is comparatively low.

Further, in case of AIs-only Funds, the responsibilities of Trustee as specified in Reg 20 r/w the Fourth Schedule shall be fulfilled by the Manager itself. This is based on the premise that, the investors, being accredited, the reliance on Trustee for investor protection is comparatively low.

Large Value Funds: a sub-category of AIs only scheme

The concept of LVF was also introduced in 2021, along with the concept of AIs. An LVF, in fact, is an AIs only fund, with a minimum investment threshold. Reg 2(1)(pa) of the AIF Regulations defines LVF as:

“large value fund for accredited investors” means an Alternative Investment Fund or scheme of an Alternative Investment Fund in which each investor (other than the Manager, Sponsor, employees or directors of the Alternative Investment Fund or employees or directors of the Manager) is an accredited investor and invests not less than seventy crore rupees.

Since an LVF is included within the meaning of an AIs-only scheme, all exemptions as available to an AIs only scheme, are naturally available with an LVF, although the converse is not true.

Additional Exemptions available to LVFs (other than as available to AIs only scheme)

In addition to the relaxations extended to an AIs only scheme, there are additional exemptions available to an LVF. These are:

Regulatory reference

Topic

Exemption for LVF

Reg 12(2)

Filing of placement memorandum through merchant banker

Not applicable

Reg 12(3)

Comments of SEBI on PPM through merchant banker

Not applicable, only filing with SEBI required

Reg 15(1)(c)

Investment concentration for Cat I and Cat II AIFs – cannot invest more than 25% of investable funds in an investee company, directly or through units of other AIFs

May invest upto 50% of investable funds in an investee company, directly or through units of other AIFs

Reg 15(1)(d)

Investment concentration for Cat III AIFs – cannot invest more than 10% of investable funds in an investee company, directly or through units of other AIFs

May invest upto 25% of investable funds in an investee company, directly or through units of other AIFs

Reduction in minimum investment size for LVFs

The minimum investment threshold for investors in LVF has been reduced from Rs. 70 crores to Rs. 25 crores, based on the recommendations of SEBI’s Alternative Investment Policy Advisory Committee (AIPAC). The rationale is to lower entry barriers to facilitate improved fund raising, without compromising on the level of investor sophistication. The reduction of investment thresholds would also facilitate investments by regulated entities having a strict exposure limit, such as insurance companies.

Exemptions from requiring specific waivers for certain provisions

The extant regulations permitted that the responsibilities of the Investment Committee may be waived by the investors (other than the Manager, Sponsor, and employees/ directors of Manager and AIF), if they have a commitment of at least Rs. 70 crores (USD 10 billion or other equivalent currency), by providing an undertaking to such effect, in the format as provided under Annexure 11 of the AIF Master Circular, including a confirmation that they have the independent ability and mechanism to carry out due diligence of the investments.

The requirement of specific waiver has been omitted for LVFs considering that AIs are already required to provide an undertaking for the purpose of availing benefits of ‘accreditation’. The undertaking, as per the format given in Annexure 8 of the AIF Master Circular states the following:

(i) The prospective investor ‘consents’ to avail benefits under the AI framework.

(ii) The prospective investor has the necessary knowledge and means to understand the features of the investment Product/service eligible for AIs, including the risks associated with the investment.

(iii) The prospective investor is aware that investments by AIs may not be subject to the same regulatory oversight as applicable to investment by other investors.

(iv) The prospective investor has the ability to bear the financial risks associated with the investment.

Similarly, LVFs have been exempt from following the standard PPM template without the requirement of obtaining specific waiver from investors.

Migration of existing eligible AIFs

One of the proposals of the LVF CP is to permit eligible AIFs, not formed as an LVF, to convert themselves into an LVF and avail the benefits available to LVF schemes. The conversion shall be subject to obtaining positive consent from all the investors. Following the same, the modalities for such migration has been specified by SEBI vide circular dated 8th December, 2025.

Pursuant to such migration, the AIF manager shall ensure that:

Name of the converted scheme contains ‘AI only fund’ or ‘LVF’ as the case may be

Such conversion and change in name to be reported to SEBI within 15 days through dedicated email ID

Such change in name to be reported to depositories within 15 days of conversion

Limit on maximum number of investors

Reg 10(f) puts a cap on the maximum number of investors in a scheme. Pursuant to the Amendment Regulations, the cap of 1000 investors shall not include the AIs.

In practice, the number of investors in an AIF is much lower than 1000, and hence, the amendment may not have much of a practical relevance.

Conclusion

The amendments are a step towards providing a lighter regulatory regime for AIFs, meant for sophisticated investors, capable of making well-informed decisions. The move is expected to witness more schemes focussed on AIs only, and thus, bring an AIs only regime for AIFs. In order to differentiate an AIs only scheme or an LVF from other AIF schemes, it is mandatory for the newly launched schemes henceforth to have the words ‘AI only fund’ or ‘LVF’ as the case maybe.

The RBI’s regulatory approach to investments by Regulated Entities (REs) in Alternate Investment Funds (AIFs) has undergone a remarkable transformation over the past two years. Initially, the RBI responded to the risks of “evergreening”, where banks and NBFCs could mask bad loans by routing fresh funds to existing debtor companies via AIF structures, by issuing stringent circulars in December 20231 and March 20242 (collectively known as ‘Previous Circulars’). The December 2023 circular imposed a blanket ban on RE investments in AIFs that had downstream exposures to debtor companies, while the March 2024 clarification excluded pure equity investments (not hybrid ones) from this restriction. This stance aimed to strengthen asset quality but quickly highlighted significant operational and market challenges for institutional investors and the AIF ecosystem. Many leading banks took significant provisioning losses, as the Circulars required lenders to dispose off the AIF investments; clearly, there was no such secondary market.

In response to the feedback from the financial sector, as well as evolving oversight by other regulators like SEBI, the RBI undertook a comprehensive review of its framework and issued Draft Directions- Investment by Regulated Entities in Alternate Investment Funds (‘Draft Directions’) on May 19, 20253. The Draft Directions have now been finalised as Reserve Bank of India (Investment in AIF) Directions, 2025 (‘Final Directions’) on 29th May, 2025. The Final Directions shift away from outright prohibitions and instead introduce a carefully balanced regime of prudential limits, targeted provisioning requirements, and enhanced governance standards.

Comparison at a Glance

A compressed comparison between Previous Circulars and Final Directions is as follows –

Particulars

Previous Circulars

Final Directions

Intent/Implication

Blanket Ban

Blanket ban on RE investments in AIFs lending to debtor companies (except equity)

No outright ban; investments allowed with limits, provisioning, and other prudential controls

Move from a complete prohibition to a limit-based regime. Max. Exposures as defined (see below) taken as prudential limits

Definition of debtor company

Only equity shares excluded for the purpose of reckoning “investment” exposure of RE in the debtor company

Therefore, if RE has made investments in convertible equity, it will be considered as an investment exposure in the counterparty – thereby, the directions become inapplicable in all such cases.

Individual Investment Limit in any AIF scheme

Not applicable (ban in place)

Max 10% of AIF corpus by a single RE, subject to a max. of 5% in case of an AIF, which has downstream investments in a debtor company of RE.

Controls individual exposure risk. Lower threshold in cases where AIF has downstream investments.

Collective Investment Limit by all REs in any AIF scheme

Would require monitoring at the scheme level itself.

Downstream investments by AIF in the nature of equity or convertible equity

Equity shares were excluded, but hybrid instruments were not.

All equity instruments

Exclusions from downstream investments widened to include convertible equity as well. Therefore, if the scheme has invested in any equity instruments of the debtor company, the Circular does not hit the RE.

Provisioning

100% provisioning to the extent of investment by the RE in the AIF scheme which is further invested by the AIF in the debtor company, and not on the entire investment of the RE in the AIF scheme or 30-day liquidation, if breach

If >5% in AIF with exposure to debtor, 100% provision on look-through exposure, capped at RE’s direct exposure5 (see illustrations below)

No impact vis-a-vis Previous Circulars. For provisioning requirements, see illustrations later.

Subordinated Units/Capital

Equal Tier I/II deduction for subordinated units with a priority distribution model

Entire investment deducted proportionately from Tier 1 and Tier 2 capital proportionately

Adjustments from Tier I and II, now to be done proportionately, instead of equally.

Investment Policy

Not emphasized

Mandatory board-approved6 investment policy for AIF investments

One of the actionables on the part of REs – their investment policies should now have suitable provisions around investments in AIFs keeping in view provisions of these Directions

Exemptions

No specific exemption. However, Investments by REs in AIFs through intermediaries such as fund of funds or mutual funds were excluded from the scope of circulars.

Prior RBI-approved investments exempt; Government notified AIFs may be exempt

Provides operational flexibility and recognizes pre-approved or strategic investments.No specific mention of investments through MFs/FoFs – however, given the nature of these funds, we are of the view that such exclusion would continue.

Transition/Legacy Treatment

Not applicable

Legacy investments may choose to follow old or new rules

See discussion later.

Key Takeaways:

Detailed analysis on certain aspects of the Final Directions is as follows:

Prudential Limits

Under the Previous Circulars, any downstream exposure by an AIF to a regulated entity’s debtor company, regardless of size, triggered a blanket prohibition on RE investments. The Final Directions replace this blanket ban with prudential limits:

10% Individual Limit: No single RE can invest more than 10% of any AIF scheme’s corpus.

20% Collective Limit: All REs combined cannot exceed 20% of any AIF scheme’s corpus; and

5% Specific Limit: Special provisioning requirements apply when an RE’s investment exceeds 5% of an AIF’s corpus, which has made downstream investments in a debtor company.

Therefore, if an AIF has existing investments in a debtor company (which has loan/investment exposures from an RE), the RE cannot invest more than 5% in the scheme. But what happens in a scenario where RE already has a 10% exposure in an AIF and the AIF does a downstream investment (in forms other than equity instruments) in a debtor company? Practically speaking, AIF cannot ask every time it invests in a company whether a particular RE has exposure to that company or not. In such a case, as a consequence of such downstream investment, RE may either have to liquidate its investments, or make provisioning in accordance with the Final Directions. Hence, in practice, given the complexities involved, it appears that REs will have to conservatively keep AIF stakes at or below 5% to avoid the consequences as above.

Now, consider a scenario – where the investee AIF invests in a company (which is not a debtor company of RE), which in turn, invests in the debtor company. Will the restrictions still apply? In our view, it is a well-established principle that substance prevails over form. If a clear nexus could be established between two transactions – first being investment by AIF in the intermediate company, and second being routing of funds from intermediate company to debtor company, it would clearly tantamount to circumventing the provisions. Hence, the provisioning norms would still kick-in.

Provisioning Requirements

Coming to the provisioning part, the Final Directions require REs to make 100 per cent provision to the extent of its proportionate investment in the debtor company through the AIF Scheme, subject to a maximum of its direct loan and/ or investment exposure to the debtor company, if the REs exposure to an AIF exceeds 5% and that AIF has exposure to its debtor company. The requirement is quite obvious – RE cannot be required to create provisioning in its books more than the exposure on the debtor company as it stands in the RE’s books.

The provisioning requirements can be understood with the help of the following illustrations:

Scenario

Illustration

Extent of provisioning required

Existing investment of RE in AIF Scheme (direct loan and/or investment exposure exists as on date or in the past 12 months)

For example, an RE has a loan exposure of 10 cr on a debtor company and the RE makes an investment of 60 cr in an AIF (which has a corpus of 800 cr), the RE’s share in the corpus of the AIF turns out to be 7.5%. The AIF further invested 200 cr in the debtor company of the RE.

The proportionate share of the RE in the investment of AIF in the debtor company comes out to be 15 cr (7.5% of 200 cr). However, the RE’s loan exposure is 10 crores only. Therefore, provisioning is required to the extent of Rs. 10 crores.

Existing investment of RE in AIF Scheme (direct loan and/or investment exposure does not exist as on date or in the past 12 months)

Facts being same as above, in such a scenario, the provisioning requirement shall be minimum of the following two:-15 cr(full provisioning of the proportionate exposure); or-0 (full provisioning subject to the REs direct loan exposure in the debtor company)

Therefore, if direct exposure=0, then the minimum=0 and hence no requirement to create provision.

Some possible measures which REs can adopt to ensure compliance are as follows:

Maintain an up-to-date, board-approved AIF investment policy aligned with both RBI and SEBI rules;

Implement robust internal systems for real-time tracking of all AIF investments and debtor exposures (including the 12-month history);

Require regular, detailed portfolio disclosures from AIF managers;

appropriate monitoring and automated alerts for nearing the 5%/10%/20% thresholds; and

Establish suitable escalation procedures for potential breaches or ambiguities.

Further, it shall be noted that the intent is NOT to bar REs from ever investing more than 5% in AIFs. The cap is soft, provisioning is only required if there is a debtor company overlap. But the practical effect is, unless AIFs develop robust real-time reporting/disclosure and REs set up systems to track (and predict) debtor overlap, 5% becomes a limit for specifically the large-scale REs for practical purposes.

Investment Policy

The Final Directions call for framing and implementing an investment policy (amending if already exists) which shall have suitable provisions governing its investments in an AIF Scheme, compliant with extant law and regulations. Para 5 of the Final Directions does not mandate board approval of that policy, however, Para 29 of the RBI’s Master Directions on Scale Based Regulations stipulates that any investment policy must be formally approved by the Board. In light of this broader governance requirement, it is our view that an RE’s AIF investment policy should similarly receive Board approval. Below is a tentative list of key elements to be included in the investment policy:

Limits: 10% individual, 20% collective, with 5% threshold alerts;

Provision for real-time 12-month debtor-exposure monitoring and pre-investment checks;

Clear provisioning methodology: 100% look-through at >5%, capped by direct exposure; proportional Tier-1/Tier-2 deduction for subordinated units; and

Approval procedures for making/continuing with AIF investments; decision-making process

Applicability of the provisions of these Directions on investments made pursuant to commitments existing on or before the effective date of these Directions.

Subordinated Units Treatment

Under the Final Directions, investments by REs in the subordinated units7 of any AIF scheme must now be fully deducted from their capital funds, proportionately from Tier I and Tier II as against equal deduction under the Previous Circulars. While the March 2024 Circular clarified that reference to investment in subordinated units of AIF Scheme includes all forms of subordinated exposures, including investment in the nature of sponsor units; the same has not been clarified under the Final Directions. However, the scope remains the same in our view.

What happens to positions that already exist when the Final Directions arrive?

As regards effective date, Final Directions shall come into effect from January 1, 2026 or any such earlier date as may be decided as per their internal policy by the REs.

Although, under the Final Directions, the Previous Circulars are formally repealed, the Final Directions has prescribed the following transition mechanism:

Time of making Investments by RE in AIF

Permissible treatment under Final Directions

New commitments (post-effective date)

Must comply with the new directions; no grandfathering or mixed approaches allowed

Existing Investments

Where past commitments fully honoured: Continue under old circulars

Partially drawn commitments: One-time choice between old and new regimes

Closing Remarks

The RBI’s evolution from blanket prohibitions to calibrated risk-based oversight in AIF investments represents a mature regulatory approach that balances systemic stability with market development, and provides for enhanced governance standards while maintaining robust safeguards against evergreening and regulatory arbitrage.

Of course, there would be certain unavoidable side-effects, e.g. significant operational and compliance burdens on REs, requiring sophisticated real-time monitoring systems, comprehensive debtor exposure tracking, board-approved investment policies, and enhanced coordination with AIF managers. Hence, there can be some challenges to practical implementation. Further, the success of this recalibrated regime will largely depend on the operational readiness of both REs and AIFs to develop transparent monitoring systems and proactive compliance frameworks.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-07-31 17:45:492025-08-05 11:10:55Round-Tripping Reined: RBI Rolls Out Relaxed Rules for Investments in AIFs