Can CICs invest in AIFs? A Regulatory Paradox

-Anshika Agarwal (finserv@vinodkothari.com)

Core Investment Companies (CIC) and Alternative Investment Funds (AIF) are two very common modes to channelise investments in the Indian market. Both are regulated by different regulators; while CICs are regulated by the RBI, AIFs are regulated by the SEBI. Under their respective regulatory frameworks, both are technically permitted to invest in one another. However, this permissibility introduces an intriguing paradox, especially for a CIC, which is allowed to invest in group companies. It points out that this approach effectively creates two investment pools—one directly under the CICs and another through the AIFs. This dual-pool structure complicates what could otherwise be a straightforward process, introducing unnecessary layers of complexity, thus deviating from the primary purpose of CICs to hold and manage investments efficiently within group companies.

The following article examines the implications of Paragraph 26(a)1 of the Master Direction – Core Investment Companies (Reserve Bank) Directions, 2016 (“CIC Master Directions”), but before delving into the specifics, it may be worthwhile to discuss in brief the concepts of AIF and CIC.

What are AIFs (Alternative Investment Funds)?

AIFs have gained prominence as a pivotal part of the financial ecosystem, providing investors with access to diverse and innovative investment opportunities. The key features of an AIF are as follows:

- An AIF is a privately pooled investment vehicle, therefore, it cannot raise money from public at large through a public issue of units;

- The investors could be Indian or foreign – there is no bar on the nature of the investor who can invest.

- The investments made by the fund should be in accordance with the investment policy.

- There are three categories of AIFs, depending on the kind of investments they make, and each category is regulated differently:

- Category 1 which invests in start up or early stage ventures or social ventures or SMEs or infrastructure or other sectors or areas which the government or regulators consider as socially or economically desirable and shall include venture capital funds, SME Funds, social venture funds, infrastructure funds and such other Alternative Investment Funds as may be specified.

- Category 2 which does not fall in Category I and III and which does not undertake leverage or borrowing other than to meet day to day operational requirements and as permitted in these regulations. It includes private equity funds or debt funds for which no specific incentives or concessions are given by the government or any other regulator shall be included.

- Category 3 which employs diverse or complex trading strategies and may employ leverage including through investment in listed or unlisted derivatives.

What are Core Investment Companies (CICs)?

CICs are a specialized subset of Non-Banking Financial Companies (NBFCs) established with the primary purpose of holding and managing investments in group companies. CICs do not engage in traditional financial intermediation but play a vital role in maintaining financial stability within the ‘group companies’. CICs are governed under the CIC Master Directions to ensure that their activities align with regulatory standards.

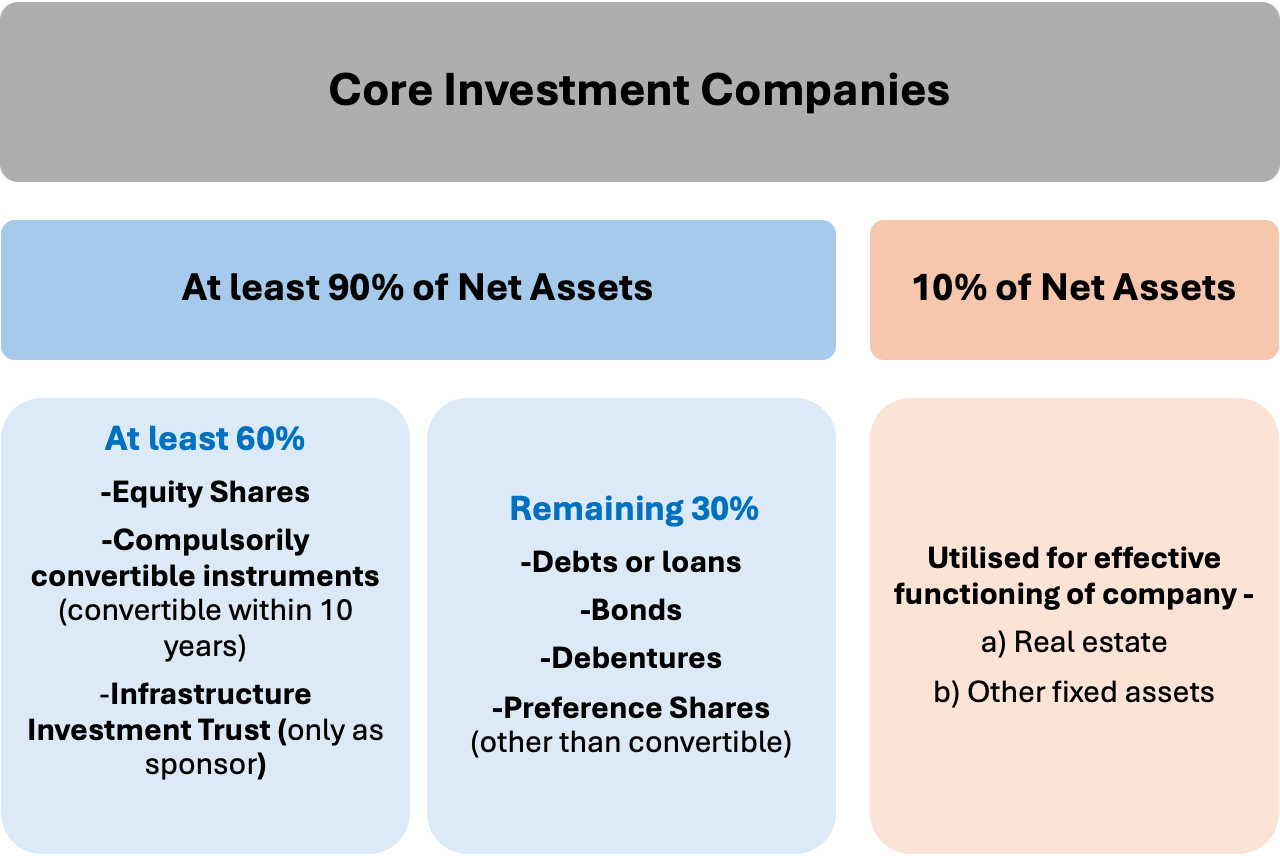

Below given graph explains the regulatory permissibility of the kind of investments a CIC can make:

In addition with the aforesaid, it may further be noted that CICs are permitted to carry out the following financial activities only:

- investment in-

- bank deposits,

- money market instruments, including money market mutual funds that make investments in debt/money market instruments with a maturity of up to 1 year.

- government securities, and

- bonds or debentures issued by group companies,

- granting of loans to group companies and

- issuing guarantees on behalf of group companies.

It may be noted that the RBI’s FAQs on Core Investment Companies, particularly Question 92 has clarified about the 10% of Net Asset –

“What items are included in the 10% of Net assets which CIC/CIC’s-ND-SI can hold outside the group?

Ans: These would include real estate or other fixed assets which are required for effective functioning of a company, but should not include other financial investments/loans in non group companies.”

Who are included in Group Companies?

The term “group companies” is defined under Para 3(1)(v) of the CIC Master Directions. It refers to an arrangement involving two or more entities that are related to each other through any of the following relationships:

| Subsidiary – Parent (as defined under AS 21), Joint Venture (as defined under AS 27), Associate (as defined under AS 23), Promoter-Promotee (as per the SEBI [Acquisition of Shares and Takeover] Regulations, 1997 for listed companies), Related Party (as defined under AS 18), Entities sharing a Common Brand Name, or Entities with an investment in equity shares of 20% or more |

The Issue with Paragraph 26(a): The paradox

Para 26A of the CIC Master Directions deals with Investments in AIFs. The language of the provisions suggest that CICs are permitted to invest in AIFs. However, this provision introduces a significant legal contradiction that undermines the regulatory framework governing CICs. According to the Doctrine of Colorable Legislation, a legal principle ensuring legislative consistency, what cannot be achieved directly cannot be permitted indirectly. By allowing CICs to invest in AIFs, Para 26(a) effectively circumvents the explicit restriction on investments outside group companies. This indirect allowance is inconsistent with the foundational objectives of the CIC Master Directions and creates substantial legal and operational confusion.

Can there be an AIF which in turn invests in the group only?

Under the SEBI (Alternative Investment Funds) Regulations, 2012, the primary objective of an Alternative Investment Fund (AIF) is to pool funds from investors and allocate them across diverse investment opportunities. However, structuring an AIF to invest predominantly or exclusively in entities within the same group raises concerns regarding compliance with SEBI’s regulatory framework, particularly its diversification. SEBI imposes strict investment concentration limits, as outlined in one of its Circular3.

For Category I and II AIFs, no more than 25% of their investable funds can be allocated to a single investee company, while Category III AIFs are restricted to 10%. These regulations inherently prevent AIFs from focusing solely on group entities unless the investment structure strictly adheres to these limits. For CICs intending to invest in AIFs, these restrictions pose significant limitations if the goal is to channel funds primarily into group companies.

Can AIFs be a Group Entity in a CIC’s Group Structure?

Technically, the answer is affirmative—AIFs can be part of a group entity within a group if it satisfies any of the conditions mentioned in the definition. However, if CICs invest in AIFs within the same group structure, it fails to resolve the underlying issue. AIFs often invest outside the group companies, exposing CICs indirectly to entities external to the group. This contradicts the core purpose of CICs, which is to focus investments within their own group companies. Such a structure not only undermines the original intent of CICs but also raises compliance concerns. The RBI adopts a pass-through approach in these cases and is likely to view such practices as non-compliant.

Conclusion

The regulatory paradox of allowing CICs to invest in AIFs under Para 26(a) of the CICs Master Direction raises important questions about the practicality and purpose of this provision. At its core, CICs are meant to simplify and streamline the management of investments within their group companies. However, the inclusion of AIFs creates an unnecessary layer of complexity, dividing investments into dual investment pools and making it harder to track, manage, and maintain transparency.

This arrangement doesn’t just complicate operations, it also moves CICs away from their original purpose. By routing investments through AIFs, CICs are exposed to entities outside their group, which can lead to compliance risks, regulatory confusion, and inefficiencies. Even from a taxation perspective, the setup offers no real benefits, adding financial burdens without meaningful gains. Paragraph 26(a) of the CICs Master Direction has been taken from the SBR Master Direction, which is applicable to NBFCs. However, including it in the CICs Master Direction, which provided regulation specifically for CICs NBFC does not appear to serve any purpose. Even if it were to be amended, its relevance of stating the same for CICs NBFC would still remain questionable.

- Reserve Bank of India, Master Direction – Core Investment Companies (Reserve Bank) Directions, 2016. Available at:https://www.lawrbit.com/wp-content/uploads/2021/05/Master-Direction-Core-Investment-Companies-Reserve-Bank-Directions-2016.pdf (Accessed: 19 January 2025). ↩︎

- FAQs on Core Investment Companies, available at: https://www.rbi.org.in/commonman/english/scripts/FAQs.aspx?Id=836 (Accessed: 19 January 2025). ↩︎

- SEBI (Alternative Investment Funds) Regulations, 2012 available at: https://www.sebi.gov.in/legal/regulations/apr-2017/sebi-alternative-investment-funds-regulations-2012-last-amended-on-march-6-2017-_34694.html ↩︎

Leave a Reply

Want to join the discussion?Feel free to contribute!