Expected to bleed: ECL framework to cause ₹60,000 Cr. hole to Bank Profits

Dayita Kanodia and Chirag Agarwal | finserv@vinodkothari.com

The proposed ECL framework marks a major regulatory shift for India’s banking sector; it is long overdue, and therefore, there is no case that the RBI should have deferred it further. However, it comes coupled with regulatory floors for provisions, which would cause a major increase in provisioning requirements over the present requirements. Our assessment, on a very conservative basis, is that the first hit to Bank P/Ls will be at least Rs 60000 crores in the aggregate.

RBI came up with a draft framework on ECL pursuant to the Statement on Developmental and Regulatory Policies, wherein it indicated its intention to replace the extant framework based on incurred loss with an ECL approach. The highlights can be accessed here.

A major impact that the draft directions will have on the Banking sector is the need to maintain increased provisioning pursuant to a shift from an incurred loss framework to the ECL framework. Under the existing framework, banks make provisions only after a loss has been incurred, i.e., when loans actually turn non-performing. The proposed ECL model, however, requires banks to anticipate potential credit losses and set aside provisions for such anticipated losses.

Banks presently classify an asset as SMA1 when it hits 30 DPD, and SMA2 when it turns 60. Both these, however, are standard assets, which currently call for 0.4% provision. Under ECL norms, both these will be treated as Stage 2 assets, which calls for a lifetime probability of loss, with a regulatory floor of 5%. Thus, the differential provision here becomes 4.6%.

Once an asset turns NPA, the present regulatory requirement is a 15% provision; the ECL framework puts these assets under Stage 3, where the regulatory minimum provision, depending on the collateral and ageing, may range from 25% to 100%. Our Table below gives more granular comparison.

| Type of asset | Asset classification | Existing requirement | Proposed requirement | Difference |

| Farm Credit, Loan to Small and Micro Enterprises | SMA 0 | 0.25% | 0.25% | – |

| SMA 1 | 0.25% | 5% | 4.75% | |

| SMA 2 | 0.25% | 5% | 4.75% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Commercial real estate loans | SMA 0 | 1% | Construction Phase -1.25% Operational Phase – 1% | Construction Phase -0.25% Operational Phase – Nil |

| SMA 1 | 1% | Construction Phase -1.8125% Operational Phase – 1.5625% | Construction Phase -0.8125% Operational Phase – 0.5625% | |

| SMA 2 | 1% | Construction Phase -1.8125% Operational Phase – 1.5625% | Construction Phase -0.8125% Operational Phase – 0.5625% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Secured retail loans, Corporate Loan, Loan to Medium Enterprises | SMA 0 | 0.4% | 0.4% | – |

| SMA 1 | 0.4% | 5% | 4.6% | |

| SMA 2 | 0.4% | 5% | 4.6% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Home Loans | SMA 0 | 0.25% | 0.40% | 0.15% |

| SMA 1 | 0.25% | 1.5% | 1.25% | |

| SMA 2 | 0.25% | 1.5% | 1.25% | |

| NPA | 15% | 10%-100% based on Vintage | (-)5% – 85% based on Vintage | |

| LAP | SMA 0 | 0.4% | 0.4% | – |

| SMA 1 | 0.4% | 1.5% | 1.1% | |

| SMA 2 | 0.4% | 1.5% | 1.1% | |

| NPA | 15% | 10%-100% based on Vintage | (-)5% – 85% based on Vintage | |

| Unsecured Retail loan | SMA 0 | 0.4% | 1% | 0.6% |

| SMA 1 | 0.4% | 5% | 4.6% | |

| SMA 2 | 0.4% | 5% | 4.6% | |

| NPA | 25% | 25%-100% based on Vintage | 0%-75% based on Vintage |

The actual impact of such additional provisioning will be a hit of more than 3% to the profit of banks1. Based on the RBI Financial Stability Report of FY 24-252, the current level of SMA and NPA is estimated to be ₹3,78,000 crores (2%) and ₹4,28,000 crores (2.3%), respectively.

Accordingly, an additional provision of approximately₹ 18,000 crores (4.6% of SMA volume) and ₹ 42,000 crores (10% of NPA volume) will be required for SMA and NPA respectively, leading to a total impact of at least ₹60,000 crores. This estimate has been arrived at by considering the % of NPAs and SMA-1 & SMA-2 portfolios of banks. The actual impact may be higher, as lot of loans may be unsecured, and may have ageing exceeding 1 year, in which case the differential provision may be higher.

It may be noted that while the draft directions allow Banks to add back the excess ECL provisioning to the CET 1 capital, it does not neutralize the immediate profitability impact, as the additional provisions would still flow through the profit and loss account.

How do we expect banks to smoothen this hit that may affect the FY 27-28 P/L statements? We hold the view that it will be prudent for banks, who have system capabilities, to estimate their ECL differential, and create an additional provision in FY 25-26, or do technical write-offs.

Other Resources

- Expected credit losses on loans: Guide for NBFCs

- Impact of restructuring on ECL computation

- Tattva Session 3 – RBI Provisions and Expected Credit Loss (ECL): Understanding their Interplay

- The total Net profit of SCBs is ₹ 23.50 Lakh Crore for FY 24. (https://ddnews.gov.in/en/indian-scbs-post-record-net-profit-of-%E2%82%B923-50-lakh-crore-in-fy24-reduce-npas/ )

↩︎ - Based on our rough estimate of the data available here: https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=1300 ↩︎

AIF Regulatory framework evolves from light-touch to right-hold

Simrat Singh | Finserv@vinodkothari.com

When AIF Regulations were formally introduced in 2012, the regulatory approach was deliberately light. The framework targeted sophisticated investors, allowing flexibility with limited oversight. Over the years, however, AIFs have become significant participants in capital markets. Market practices over the decade exposed regulatory loopholes and arbitrages. For example, some investors who did not individually qualify as QIBs accessed preferential benefits indirectly through AIF structures and investors who were restricted to invest in certain companies started investing through AIF making AIF an investment facade. There were concerns regarding circumvention of FEMA norms as well1. In the credit space, regulated entities such as banks and NBFCs started channeling funds through AIFs to refinance their stressed borrowers, raising concerns around loan evergreening2. These developments prompted regulatory response. RBI first issued two circulars, one in 2023 and the other in 2024. Finally, in 2025 formal directions governing investments by regulated entities in AIFs were also issued3. These Directions introduced exposure caps and provisioning requirements.4

While the RBI addressed prudential risks arising from regulated entities’ participation in AIFs, SEBI focused on investor protection, governance within the AIF ecosystem and curbing the regulatory arbitrages. First it mandated on-going due diligence by AIF Managers5. It then mandated specific due diligence6 of investors and investments of AIF to prevent indirect access to regulatory benefits. Fiduciary duties of sponsors and investment managers and reporting obligations were progressively codified through circulars. Managers were expected to maintain transparency vis-a-vis their investment decisions, maintain written policies including ones to deal with conflict of interest with unitholders and submit accurate information to the Trustee. What were once broad, principle-based expectations have evolved into detailed, enforceable rules. Regulatory tightening has been matched by a more assertive enforcement approach. SEBI’s recent settlement order7 against an AIF underscores its increasing scrutiny of governance lapses, mismanagement of conflicts and inaccurate reporting. This clearly signals that any compliance gaps will no longer be overlooked and are likely to attract regulatory action. In a separate adjudication order, SEBI imposed penalties on both the Trustee and the Manager for the delayed winding-up of the scheme, underscoring that accountability within an AIF structure extends to all key parties and is not limited to the Manager alone.

However, SEBI’s approach has not been solely restrictive. Alongside regulatory tightening, it has also sought to preserve commercial flexibility and respond to market needs. Examples include the introduction of the co-investment framework8 for AIFs, framework for offering differential rights to select investors and a revamp for angel funds9.

Together, these measures are reshaping the regulatory landscape for AIFs and their managers. Investors can no longer rely on AIF structures to indirectly obtain regulatory advantages otherwise unavailable to them. As AIFs have grown in scale and importance, what is emerging is a more transparent, prudentially sound and closely supervised regulatory regime designed to align investor protection and commercial flexibility.

- See SEBI’s Consultation paper on proposal to enhance trust in the AIF ecosystem ↩︎

- See our write-up on AIFs being used for regulatory arbitrages here. ↩︎

- RBI (Investment In AIF) Directions, 2025 ↩︎

- See our detailed analysis of the Directions here. ↩︎

- See our write-up on ongoing due diligence for AIFs here ↩︎

- See our FAQs on specific due diligence of investors and investments of AIFs here. ↩︎

- See the complete order here ↩︎

- See our write-up on co-investments here. ↩︎

- See our write-up on changes w.r.t Angel Funds here ↩︎

The Law of Prepaid Payment Instruments (PPIs): A Guide For New Market Entrants

ECL Framework for Banks: Key Highlights

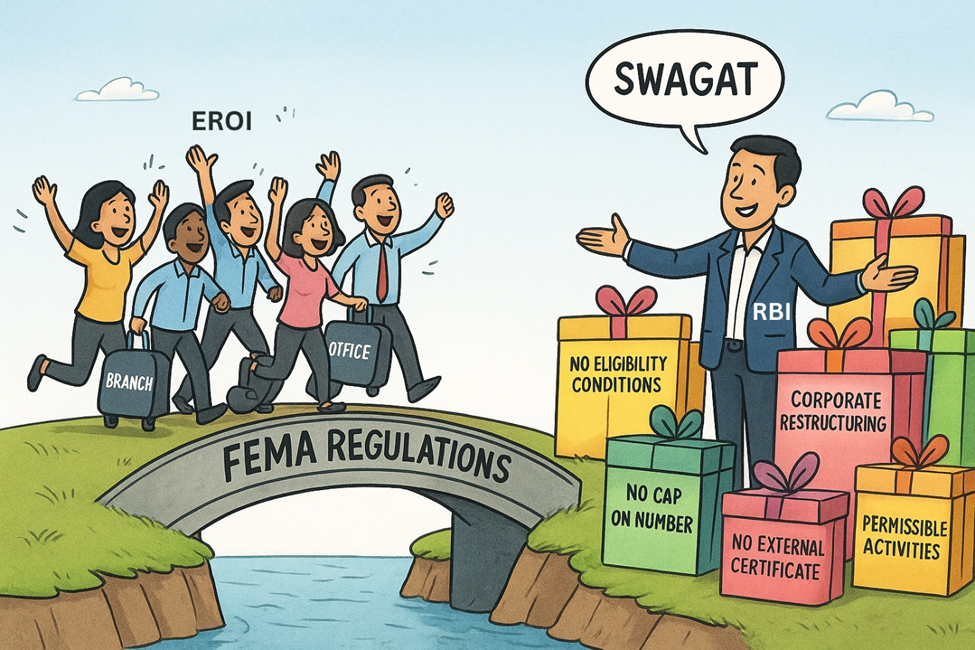

SWAGAT to foreign branches or offices in India: RBI proposes draft regulations on such establishments

– Team Corplaw | Corplaw@vinodkothari.com

As a part of its efforts to rationalise the regulations for establishment of a place of business in India by overseas entities[1], RBI has issued Draft Foreign Exchange Management (Establishment in India of a branch or office) Regulations, 2025. The proposals primarily aim to enable delegation of more powers to AD banks and reduction of compliance burden, thereby further enhancing the ease of doing business in India.

As against the extant Foreign Exchange Management (Establishment in India of a branch office or a liaison office or a project office or any other place of business) Regulations, 2016, as updated in Master Direction – Establishment of Branch Office (BO)/ Liaison Office (LO)/ Project Office (PO) or any other place of business in India by foreign entities, the classification of foreign establishments have been limited to (a) branch and (b) office.

Read more →Revised Form IEPF-5 paves way for simplified claim process

Lavanya Tandon, Senior Executive & Anushka Ganguly, Executive | corplaw@vinodkothari.com

Demystifying Structured Debt Securities: Beyond Plain Vanilla Bonds

Palak Jaiswani, Manager | corplaw@vinodkothari.com

Debentures, one of the most common means for raising debt funding, where investors lend money to the issuer in return for periodic interest and repayment of principal at maturity. While the basic feature of any debenture is a fixed coupon rate and a defined tenure (commonly referred to as plain vanilla instruments), sometimes these instruments may be topped up with enhanced features such as additional credit support, market-linked returns, convertibility option, etc., thus referred to as structured debt securities.

Structured debt securities: motivation for issuers

Apart from the economic favouring such structural modifications, a primary motivation for the issuer in issuing such structured instruments might be the regulatory advantages that these securities offer. For instance,

- Chapter VIII of SEBI NCS Master Circular provides an extra limit of 5 ISINs for structured debt securities & market-linked securities, thus more room for the issuers to issue debt securities, compared to the restriction of a maximum of 9 ISINs for plain vanilla debt.

- In addition, as per NSE Guidelines on Electronic Book Provider (EBP) mechanism, market-linked debentures are not required to be routed through EBP, allowing issuers to place such instruments almost like an over-the-counter trade. This allows issuers to structure the debt securities on a tailored basis and offer them directly to specific investors.

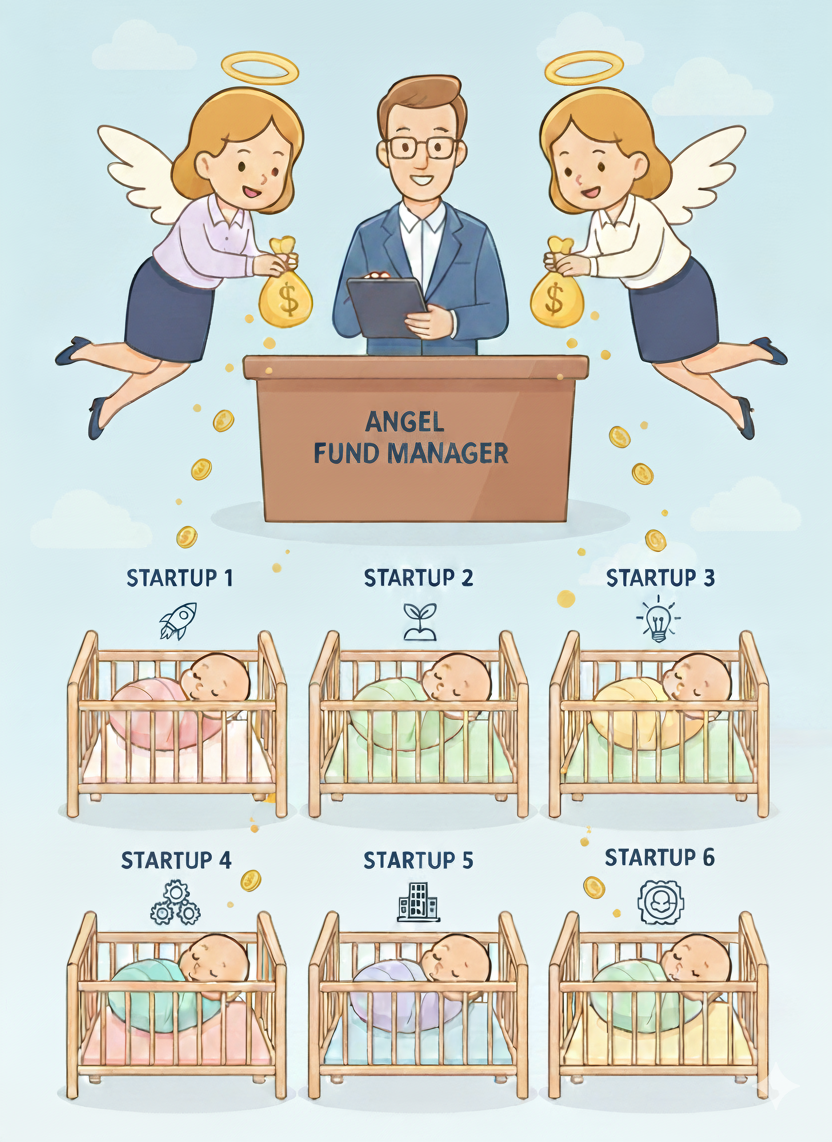

Angel Funds 2.0: Navigating the New Regulatory Landscape

Payal Agarwal, Partner & Jayesh Rudra, Executive | corplaw@vinodkothari.com

The 2025 Amendments to the AIF Regulations has brought substantive changes to the regulatory landscape for angel funds, moving the same as a category of Cat I Funds, as against a sub-category of Venture Capital Funds. However, regulatory oversight strictens, with the access exclusively limited to accredited investors only. In view of the redundancy of a “scheme” in the context of angel funds (see below), the same has been omitted and replaced with each investment based participation of investors.

Angel Funds, a unique type of start-up friendly investment vehicle, was formally recognised by SEBI in the year 2013 with the introduction of Chapter III-A to the SEBI (Alternative Investment Funds) Regulations, 2012. As on 31st March 2025, there are 103 registered Angel Funds with a total commitment of Rs. 10,138 crores. The regulatory landscape for angel funds has been substantially revamped with the notification of SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2025, dated 8th September, 2025. The Amendment Regulations are further supplemented with a Circular dated September 10, 2025 prescribing the specific conditions and modalities pertaining to the provisions applicable to Angel Funds.

The amendments are based on the Consultation Paper dated 13th November, 2024, released post the Union Budget announcement of abolishment of angel tax (see a brief presentation here), for operational clarity and strengthening the governance and disclosure requirements for angel funds.

Uniqueness of structure

The uniqueness of Angel Funds lie in its structure. Unlike a typical AIF, in the case of Angel Funds, the investors provide specific consent to each investment opportunity. As such, there is no proportionality between the contribution of the investors in a scheme of AIF vis-a-vis the indirect contribution made in an investee company by such AIF scheme. As such, as against the usual “scheme” structure, an Angel Fund follows an “investment” structure.

Applicability

The Amendment Regulations are effective from the date of publication of the same in the Official Gazette, viz., 8th September 2025. The Circular was issued on 10th September, 2025. Further, in order to facilitate transition of the existing Angel Funds, additional timeline has been provided for compliance in some cases.

Exclusive to AIs: eligibility to act as an angel investor

Pursuant to the amendments, it is only an Accredited Investor who is eligible to be onboarded as an angel investor in an angel fund. The difference between the eligibility conditions are tabulated below:

| Particulars | Angel Investors (Erstwhile Framework) | Accredited Investors (Amended Framework) |

| Categories of investors | Individual/Body corporate/AIF/ VCF | IndividualHUF Family trust Sole proprietorship Body corporate Trust other than family trust Partnership firm Government, Govt development agencies, QIBs, FPIs, Sovereign Wealth Funds etc – exempt from accreditation requirement |

| Eligibility criteria | In case of individual, Net tangible assets > Rs. 2 crs (excluding principal residence) andHas experience of Early stage investment or Serial entrepreneur or SMP with at least 10 years’ experience | In case of 1 to 4, either of the following: Annual income > Rs. 2 crs or Net worth > Rs. 7.5 crs out of which at least Rs. 3.75 crs is in the form of financial assets.Annual Income ≥ Rs. 1 cr + Net Worth ≥ Rs. 5 crs, out of which at least Rs. 2.5 crs is in the form of financial assets.In case of 7, each partner to separately meet aforesaid criteria |

| In case of body corporate, networth > Rs. 10 crs | In case of body corporate, networth > Rs. 50 crs | |

| Trust other than family trust, networth > Rs. 50 crs | ||

| Independent accreditation | Not applicable | Applicable |

Not only the eligibility conditions are stringent in case of AIs as compared to erstwhile concept of angel investors, but the mandatory “accreditation” criteria would be a primary factor that may lead to elimination of many investors who were earlier eligible for acting as an angel investor.

Transition period

For angel funds registered on or before 10th September 2025 (the date of issue of Circular), a timeline of 1 year, that is, upto 8th September 2026 has been specified, for transition into the new framework. During this period, offers can be made to upto 200 non-AIs.

No new contribution can be accepted from non-AIs post 8th September, 2026, though the investors continue to hold their existing investments already made in the angel fund.

Regulatory regime for Angel Funds: old v/s new

| Topic | Old Framework | New Framework | Rationale |

|---|---|---|---|

| STRUCTURE OF THE FUND | |||

| Category of AIF [Reg 19A(1)] | Sub-category of VCF under Cat -I | Sub-category of Cat – I | In view of the unique features of Angel Funds as compared to VCFs. See differences below |

| Schemes under Fund [Reg 19E] | Allowed | Not allowed | Since there is practically no distinction between a “scheme” and an “investment” in the context of an angel fund, hence, the concept of scheme is not relevant for an angel fund. |

| Filing of placement memorandum with SEBI [Reg 19D(4)] | Not applicable | PPM to be filed along with application for registration through merchant banker for comments of SEBI | Previously, term sheets for each Schemes were filed with SEBI for “informational” purposes. The requirement has been substituted with filing of PPM at the time of registration itself. |

| Filing of the term sheet for schemes with SEBI [Reg 19E] | Mandatory, 10 days from launch of scheme | Not applicable | Term sheet is filed for material information of each Scheme, not relevant since scheme structure is omitted for angel funds |

| Minimum continuing interest of Sponsor/ Manager [Reg 19G] | 2.5% of corpus or Rs. 50 lacs, whichever is lower | 0.5% of investment amount or Rs. 50,000, in each investee, whichever is higher | To ensure that manager/sponsor has interest in every investment |

| INVESTMENT IN ANGEL FUND | |||

| Eligibility of investor [Reg 19D(1)] | Angel Investor based on certain eligibility conditions specified therein (see later in this article) | Accredited Investor KMP of Angel Fund/ Manager | To ensure proper verification of the risk appetite and informed decision making capabilities of the investor, since investment in start-ups are highly risky. To enhance skin in the game |

| Minimum corpus [Reg 19D(2)] | Rs. 5 crore | NA | NA since each investment is based on prior consent of investor, the concept of a common corpus is irrelevant |

| Minimum investment per investor [Reg 19D(3)] | Rs. 25 Lakhs | NA | No minimum limit since only AIs are allowed to invest |

| Minimum number of investors [Reg 19D(6)] | Not specified | At least 5 AIs prior to disclosing first close | To ensure sufficient investor interest prior to starting to make investments, in the absence of any minimum corpus requirement. |

| Maximum number of investors | 200 in a scheme [Reg 19E(2) – omitted] | No limit | Since only AIs are eligible who are independently verified, sufficient guardrails exist. No cap on number of investors facilitate scaling up of the industry and enhance capital flow to start-ups. Further, ICDR Regulations have been amended to include AIs within the meaning of QIBs for the purpose of investment in angel funds, accordingly, the limit of 200 as per section 42 of the Companies Act, 2013 shall also not apply in case the AIF is formed as a company. |

| INVESTMENT BY ANGEL FUNDS | |||

| Prohibition from investment in certain investees [Reg 19F(6)] | Companies with family connection with any of the angel investors. | No investments from such investors who are related party to an investee | See below. |

| Follow-on investment in existing investee [proviso to Reg 19F(1)] | Not permitted once the investee ceases to be start-up | Allowed subject to the condition that the Fund’s post-issue shareholding percentage does not exceed pre-issue shareholding percentage | To protect and preserve the value of the existing investments of Angel Funds in an investee. Investment cap is to ensure that while pre-emptive rights can be exercised by angel funds, does not result in dilution of the regulatory intent behind angel funds |

| Minimum investment in an investee [Reg 19F(1)] | Rs. 25 Lakhs | Rs. 10 Lakhs | The increase in range is to reflect the growth of angel ecosystem, providing more flexibility to the Angel Funds |

| Maximum investment in an investee [Reg 19F(1)] | Rs. 10 crores | Rs. 25 crores (including upon follow-on investment) | |

| Lock-in on investments [Reg 19F(3)] | 1 year | 6 months – if sold to a third party subject to AoA of investee. 1 year – in other cases, including buyback, sale to promoters of investee/ associates of promoters | To maintain stability of investments while providing flexibility of favourable exit to the angel fund |

| Minimum number of AIF investors in each investee [Reg 19F(5)] | No such limit | 2 investors | Also serves as a check against misuse of angel fund structure for facilitating investments from single investor |

| COMPLIANCES APPLICABLE TO ANGEL FUNDS | |||

| Exception from application of certain provisions of the Regs [19B (2)] | Reg 10(a), (b), (c), (d), (f) – Conditions w.r.t. Investment in AIFReg 12 – Filing of Scheme Reg 14 – Listing of unitsReg 15(1)(a), (c), (e) – Conditions w.r.t. Investment by AIFReg 16(1)(b) – OmittedReg 16(2) – Additional conditions applicable to VCFsReg 20(21) – Rights of investors pro rata to their contribution | Following additional exceptions: Reg 15(da) – AIFs making investments through multiple layers of AIFsReg 16(1)(a) – Types of investeeReg 17 – Conditions for Cat II investments Reg 18 – Conditions for Cat III investments | The exceptions are majorly in alignment with the non-Scheme structure of the Angel Funds |

| Annual audit of compliance with terms of PPM | Not applicable | Mandatory, if total investment (at cost) exceeds Rs. 100 crs | Exemption to continue for smaller Angel Funds, larger Angel Funds be subject to audit of PPM |

| Reporting in relation to performance benchmarking | Not applicable | Applicable from FY 25-26 | To improve transparency |

Related Party v/s Family Connection

Angel Funds are not permitted to accept contributions from such investors, who are related parties to the investee company in which the investment is to be made. Here, the definition of “related party” is to be taken from Reg 2(1)(zb) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015. The definition, in turn, refers to Companies Act and applicable accounting standards as well.

Various questions arise:

- Who prepares the list of related parties as per LODR definition? Is it the prospective investee that is responsible?

- Can the investment manager and investor be absolved of their responsibilities of verification of whether or not the investor is a related party to the investee?

- What if the investor becomes a related party of the investee entity, subsequent to making such investments?

The change from the term “family connection” to “related party” seems to simplify the identification for the prospective investee company, since such companies would have already identified related parties in terms of section 2(76) of CA, 2013 and applicable accounting standards. The only additional categories for such investees would be:

- Promoters and members of promoter group, and

- Shareholders holding 10% or more equity shares in the company on a beneficial interest basis.

Concluding Remarks

The amended regulatory framework makes it stringent for angel funds to raise funds from angel investors, restricting the access to accredited investors only. With the limited number of investors “accredited” registered in India (649 as on May 2025), early stage start-ups might face obstacles in startup funding. While SEBI has proposed ease of accreditation requirements, the same has not been made effective yet. As on 30th June 2025, data shows that the number of VCFs are much higher than the number of angel funds, and with the amended requirements, it might so happen that the investors would prefer VCFs over angel funds, as a means of investing in start-ups.

See our other resources on AIF:

- CIV-ilizing Co-investments: SEBI’s new framework for Co-investments under AIF Regulations

- FAQs on specific due diligence of investors & investments of AIFs

- RBI bars lenders’ investments in AIFs investing in their borrowers

- Capital subject to ‘caps’: RBI relaxes norms for investment by REs in AIFs, subject to threshold limits

- Can CICs invest in AIFs? A Regulatory Paradox

- Trust, but verify: AIFs cannot be used as regulatory arbitrage