Disaster, Distress and Resolution: Decoding RBI’s NBFC Relief Framework

-Jeel Ranavat, Assistant Manager (jeel@vinodkothari.com)

Overview

A natural calamity does not just damage property or disrupt livelihoods — it can instantly push otherwise disciplined borrowers into financial stress. Loan repayments become difficult not because borrowers are unwilling to pay, but because businesses halt, incomes disappear, and economic activity comes to a standstill. Recognising this reality, the RBI has introduced a comprehensive new framework on relief measures in areas affected by natural calamities (Natural Calamities Directions) for lenders that fundamentally changes how borrower distress arising from calamities is to be handled.

RBI has moved towards a more structured and time-bound relief mechanism — one that focuses not only on faster restructuring and borrower protection, but also on ensuring prudential discipline for lenders. From proactive resolution and protection against sudden NPA downgrades to stricter timelines, additional provisioning norms, and disaster-sensitive credit assessment.

Key Highlights of the Framework

Not Every Loan Gets Relief, Here’s Who Qualifies

As per para 122 F of the Natural Calamities Directions, borrowers whose accounts are classified as “Standard” with no default exceeding 30 days (that is to say, classified as SMA-0) as on the date of the calamity’s occurrence (as opposed to erstwhile framework where loan restructuring, is generally available only where assessed crop loss equals or exceeds 33%) are eligible for restructuring under the Natural Calamities Directions.

The calamity resolution framework will apply only to direct borrower exposure and not to loans where the NBFC has given credit facilities/refinance support to another lending entity.

By this amendment RBI has formally defined “date of invocation” and “natural calamity,”.

‘date of invocation’ shall mean the date on which the borrower and the NBFC agree to proceed with a resolution plan under Chapter VI-A of these Directions through a documented arrangement, other than in case of deemed invocation as specified in paragraph 122J of these Directions.

‘natural calamity’ shall mean an event recognized under the National Disaster Response Fund (NDRF) / State Disaster Response Fund (SDRF).

RBI puts borrower relief on the clock

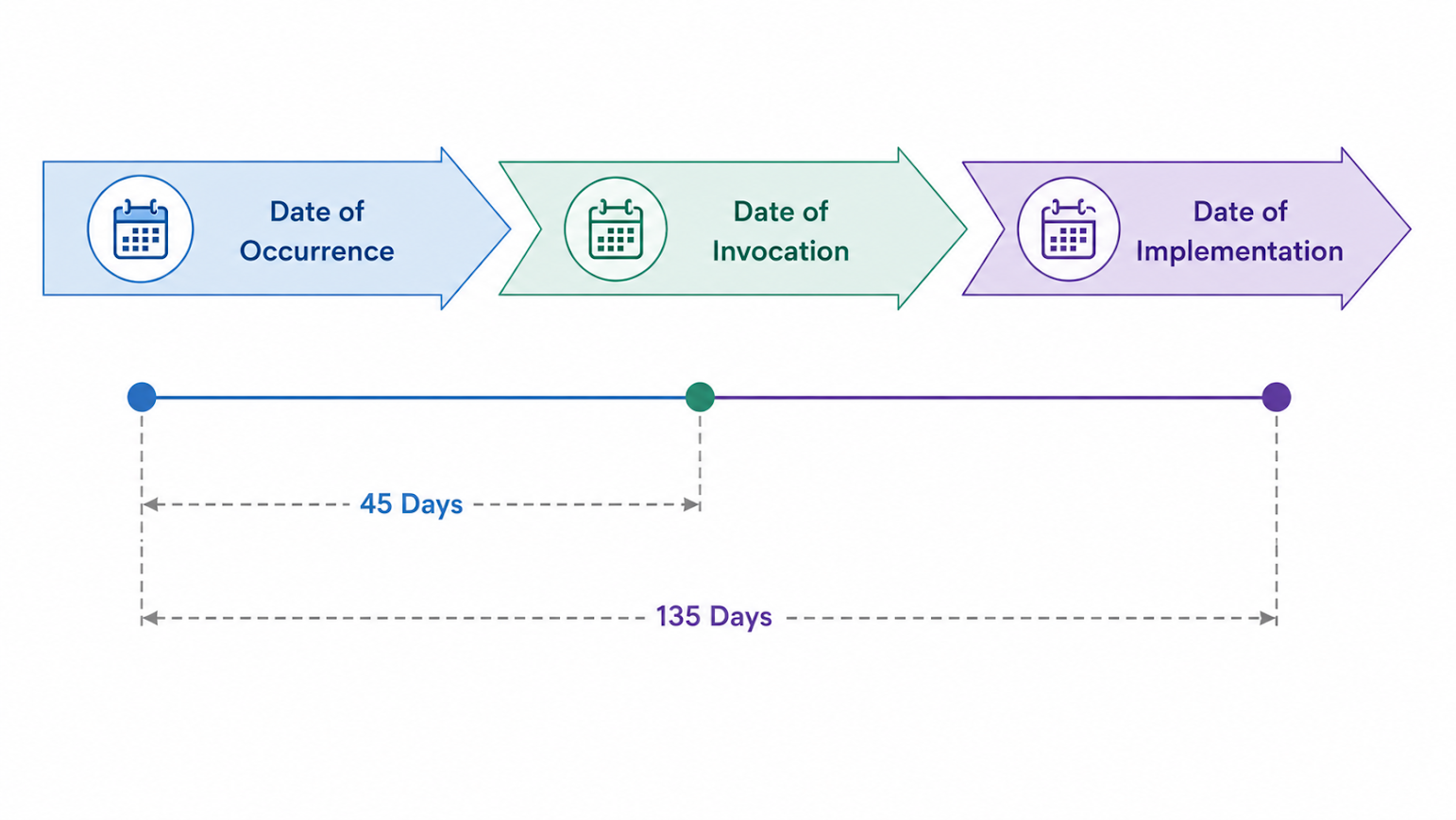

By prescribing clear timelines of invocation within 45 days and implementation within 135 days from the date of calamity declaration, the RBI seeks to ensure that borrower relief is delivered promptly rather than getting trapped in prolonged procedural delays.

‘Date of occurence’ shall mean the date on which the calamity arised, however in case no specific date of occurrence is ascertainable in respect of a calamity, the date of declaration of such calamity by the Central / State Governments shall be treated as the date of occurrence.

The “date of occurrence” is the date on which the natural calamity takes place, while the “date of invocation” is the date on which, after the calamity, the borrower and the NBFC formally agree to proceed with a resolution plan. Thus, the former relates to the occurrence of the calamity, whereas the latter marks the commencement of the resolution process.

“Date of implementation” means the implementation of the relief measures(rescheduling of payments etc.) for the impacted borrowers.

The prescribed timelines given above means that once the calamity occurs the formal arrangement between the lender and the borrower shall be done within a maximum of 45 days from the date of occurrence of calamity and the relief measures shall be implemented within 135 days from date of declaration.

Suo Motu Restructuring

As an exception to the above lenders can suo moto initiate restructuring and implement resolution plans without waiting for a formal borrower request. Such action is treated as a “deemed invocation,” while borrowers retain the right to opt out within 135 days from the calamity declaration. In suo motu cases, in our view the restructuring would generally follow a lender devising a common restructuring plan based on product-wise and borrower-wise classification

Hence accordingly, the regulation also clarifies that need of a formal arrangement between the borrower and the lender will not be required in case where the lenders voluntarily restructures the loan.

It is further emphasized that even where suo motu cognizance is taken by the lender, the 45-day invocation timeline still applies. Hence, in our view the lender should not wait until the last day to communicate with the borrower. Such communication should be shared at the earliest opportunity, so as to afford the borrower adequate time to consider, and if necessary, reject the invocation, and to engage in meaningful discussions with the lender regarding a separate restructuring arrangement all within the stipulated 45-day period from the date of occurrence of the natural calamity.

Clear Rules, Faster Relief

NBFCs are now expected to clearly define who qualifies for relief, what forms of assistance may be granted, and the objective parameters on which such decisions will be based. Equally important, the amendment requires the creation of a delegation structure ensuring that restructuring approvals and additional finance are not delayed due to procedural bottlenecks.

In this regard, the lenders must have in place a policy for grant of relief, which should lay down the following:

- Objective principles for the terms of relief to be granted to various borrower / loan categories. (For eg. the nature of relief shall vary based on the loan category and borrower profile, similar relief measures shall be extended to similarly placed borrowers etc).

- Determination of borrower eligibility

- Potential relief measures, such as restructuring, sanction of additional finance etc.

- Timelines for implementation of relief measures

- Verifiable parameters for making such determination(For eg. Inclusion of the borrower’s location in a Government-notified calamity-affected area, Damage to productive assets, inventory, crops, or property etc.)

- Delegation matrix for deciding and implementing relief measures (if any)

Suo Motu Restructuring

The framework marks a shift from a reactive to a proactive approach by allowing lenders to suo motu initiate restructuring and implement resolution plans without waiting for a formal borrower request. Such action is treated as a “deemed invocation,” while borrowers retain the right to opt out within 135 days from the calamity declaration.

Relief Measures

The lenders may by rescheduling repayments, converting accrued interest into a separate credit facility,granting additional finance, waiver or reduction of fees, granting moratorium, alteration of repayment terms etc (increasing the loan tenure etc). based on the borrower’s future viability and repayment capacity.

Ensuring Continuous Credit Support During Disasters

NBFCs may grant restructuring and fresh finance without waiting for insurance claim settlements, while later adjusting insurance proceeds against restructured loans.

Government interest subvention and repayment incentives must be extended to all eligible borrowers, and existing State/Central relief measures must be factored in.

For agricultural borrowers affected by calamities, alternative certificates from revenue or community authorities may be accepted where original land records are lost.

Asset Classification

The framework provides protection against deterioration of borrower asset classification due to calamity-related stress. If a resolution plan is implemented in accordance with Chapter VI-A, borrower accounts that were already classified as “Standard” can continue to retain that status.

Further, even if an account slipped into NPA after the occurrence of the calamity but before implementation of the resolution plan, it may be upgraded back to “Standard” upon successful implementation of the resolution plan as the account has defaulted due to temporary disruption caused by natural calamity and not by borrowers weak credit profile.

Additional Provisioning Requirement for Restructured Accounts

An additional 5% provisioning over and above what is required under the law has to be maintained on restructured accounts as an additional financial buffer against the risk associated with restructured accounts;however total provisioning cannot exceed 100% of the outstanding exposure.

However, if the borrower starts repaying properly after restructuring, specifically repays at least 20% of the loan without the account turning into NPA again, the NBFC is allowed to reverse this extra provision.

Prudential Treatment of Interest Income

RBI allows normal income recognition for standard restructured accounts, but becomes more cautious where repeated restructuring indicates higher repayment uncertainty, meaning for accounts restructured only once under the framework the NBFCs can continue to recognize income on accrual basis but in case of repeated restructuring interest shall be recognized on cash basis only.

Waiver of Fees & Charges During Calamities

A discretionary relief can be provided by the lenders in areas officially declared as calamity-hit, by providing relief to borrowers by waiving or reducing certain fees and charges for up to one year.

Calamity Risk Now Part of Credit Appraisal

Credit assessments carried out by the NBFCs should suitably factor potential calamity risks especially for borrowers in vulnerable regions. It seeks to strengthen portfolio resilience and reduce future defaults arising from disaster-related disruptions.

Credit assessment for a geographically distributed business is multidimensional. It evaluates the risk at any location where a disruption could impair the borrowers repayment capacity or asset quality. Hence, when the calamity risk of a borrower is being factored in the credit assessments, the same should not be limited to the place of residence/registered office and the risks of the places/region from where it conducts its economic activity or the region or place on which the prospective borrower’s economic activity is dependent, should also be factored in the credit assessment process..

For instance the borrower runs an e-commerce business, where their stocks are stored in a different place than their registered office. A natural calamity affecting the place where the borrower’s stock is stored may affect their economic activity. Hence, calamity risk assessment of the region on which the borrower’s economic activity is dependent on also becomes important.

Since lenders assess all factors relevant to a borrower’s repayment capacity, including income sources and business operations, during credit origination, the same holistic approach should be followed while evaluating eligibility for calamity-related relief measures.

The RBI’s revamped NBFC relief framework essentially replaces firefighting with fire preparedness. Instead of scrambling to craft one-off solutions each time disaster strikes, lenders now operate within a pre-built playbook—clear triggers, defined timelines, and predictable rules. For borrowers, this means faster access to restructuring without the stigma of default classification. For lenders, it means absorbing shock without balance sheet chaos. The real shift is philosophical, treating natural calamities not as exceptions that break the system, but as foreseeable events the system is designed to handle

Read our other articles

Leave a Reply

Want to join the discussion?Feel free to contribute!