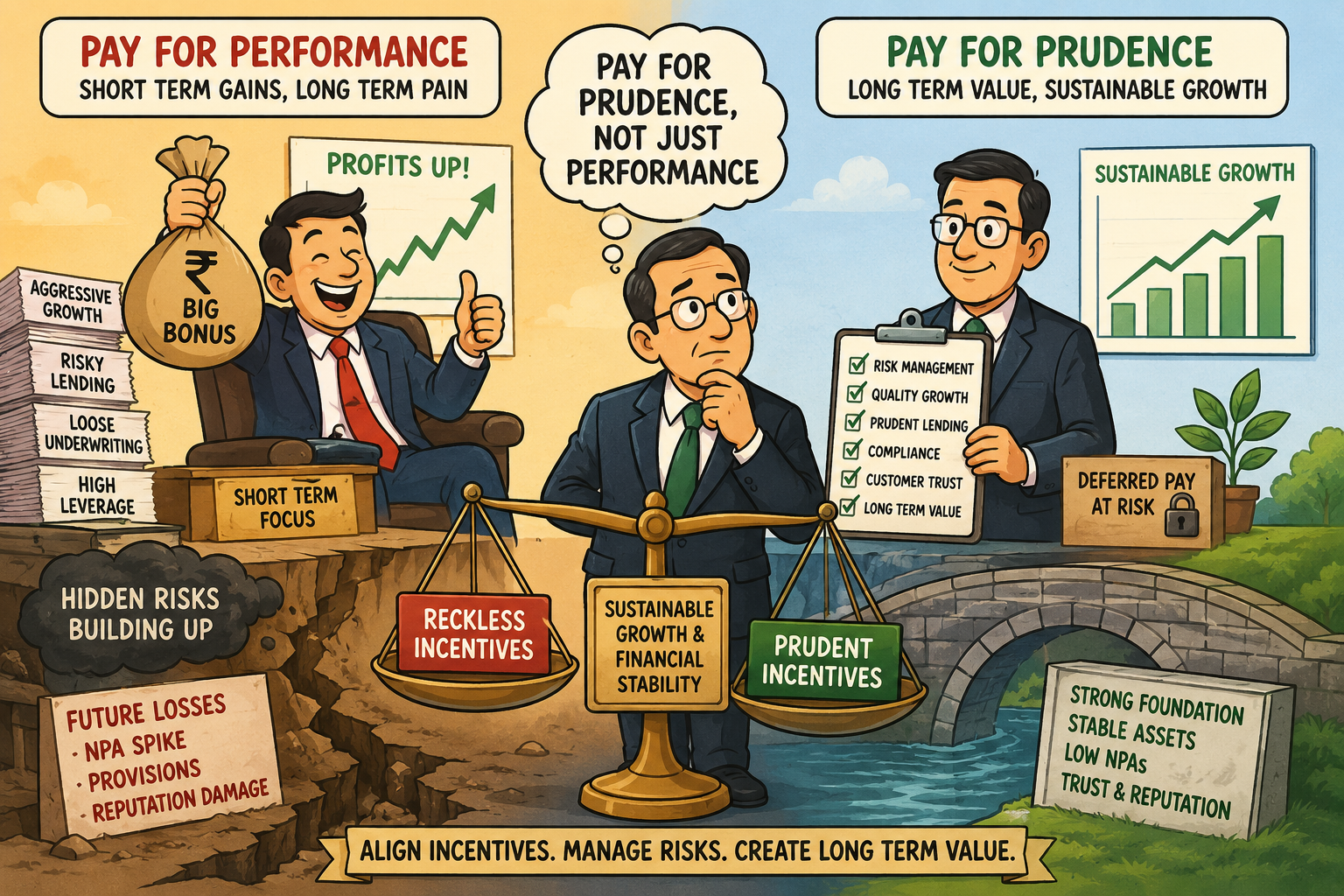

Pay for Performance Or Pay for Prudence?

Understanding Compensation Framework for NBFCs

- Pranjal Dave & Kushal Agrawal | finserv@vinodkothari.com

On 9 March 2026, the Reserve Bank of India imposed a monetary penalty of ₹2.70 lakh on a financial institution for violations regarding the payment of the entire variable remuneration to certain KMPs upfront, without deferring any portion, in breach of applicable compensation guidelines. While the quantum of the penalty is insignificant relative to the Company’s scale of operations, it reflects the RBI’s clear regulatory emphasis on ensuring that NBFC compensation practices are aligned with prescribed regulatory requirements.

Compensation structures in financial institutions, like any other institution, have traditionally been designed to reward performance. Higher profits, stronger business growth, and increased market share have often translated into higher incentives and bonuses for senior management. However, the manner in which institutions reward their key personnel can significantly influence the risks they choose to take. Where the remuneration is excessively linked to short-term profitability, it may encourage risk-taking without adequate regard to long-term consequences, particularly where the underlying risks may materialise only several years later.

The Lessons of History: From Performance to Prudence

The 2008 Global Financial Crisis (GFC) illustrated the above mechanism. Mortgage originators earned fee income upfront on loan disbursements while credit risk was securitised and passed to counterparties; traders at large investment banks received annual cash bonuses tied to mark-to-market gains while systemic risks accumulated on balance sheets. When those risks materialised, bonus recipients were under no obligation to return payments.

Mr Raghuram Rajan (2006), writing before the GFC , identified competitive pressures pushing financial sector executives toward risk strategies concealed within opaque compensation structures, specifically, strategies that generate near-certain short-term income while accumulating rare but catastrophic risks.

In a landmark 2011 study, Fahlenbrach and Stulz revealed a shocking paradox – banks where CEOs owned the most stock actually suffered the worst losses during the crash. Because their personal wealth was tied to share prices, these executives took massive, highly concentrated gambles to boost short-term returns. The conclusion of their research was clear that how an executive is paid is just as critical as how much they are paid.

The international response to these concerns was reflected in the Financial Stability Board’s Principles for Sound Compensation Practices and the accompanying implementation standards, which advocated alignment of remuneration with long-term risk outcomes. This was followed by further guidance from the Basel Committee on Banking Supervision on the assessment and risk-adjustment of remuneration practices.

Why only financial institutions? Rather, every Company is covered

Section 178(4)(c) of the Companies Act, 2013, requires the Nomination and Remuneration Committee (NRC) of every prescribed class of company to formulate the criteria for, and recommend to the Board, a policy relating to the remuneration of directors, KMPs, and other employees. While RBI has prescribed a more structured framework for banks and NBFCs, the underlying principles are equally relevant to non-financial entities and are consistent with the remuneration governance framework envisaged under Section 178 of the Companies Act, 2013. In any company, compensation is often linked to performance metrics such as profits, revenue growth, operational targets, or share price performance. Where such performance is subsequently found to have been achieved through misconduct, inaccurate reporting, regulatory breaches, or unsustainable business practices, malus and clawback mechanisms enable the company to reduce or recover variable remuneration.

Where an industrial company’s CEO makes poor strategic decisions, the primary losers are shareholders. Where an NBFC’s senior management makes poor credit or investment decisions, the losses spread to depositors (in deposit-taking NBFCs), borrowers facing credit contraction, financial system counterparties, and, at sufficient scale, the broader economy.

Consider a hypothetical Middle Layer NBFC. In FY2023, its loan book grew by 35%, driven by aggressive commercial lending and disbursements. Net interest margin expands, provisions are low, and PAT rises sharply. The board approves variable pay of ₹8 crore for the MD and ₹3-5 crore for the senior credit team, paid immediately in April 2023.

By FY2025, borrower stress in the commercial segment becomes apparent. NPA recognition in the FY2023-24 begins. Provisions of ₹400-600 crore are required across two financial years, erasing the PAT that justified the FY2023 bonuses. The credit decisions that drove FY2023 profitability and the bonuses are the same decisions that drove FY2025 impairment.

Under a properly designed deferral and clawback framework, a material portion of the FY2023 variable pay would remain unvested in FY2024 and FY2025. As NPA ratios deteriorate beyond prescribed thresholds, malus provisions would cancel unvested amounts. If fraud or deliberate misreporting in origination is subsequently found, clawback provisions would enable recovery of amounts already paid. In the absence of such provisions, the incentive structure is undisturbed: gains are privatised, losses are socialised.

Building Blocks of Sound Compensation Governance

A simple principle: individuals who generate profits should also bear the consequences of the risks taken to generate those profits.

A. Variable Pay

Variable pay is the performance-linked component of remuneration. Two dimensions are critical: the quantum that is the share of variable pay relative to fixed pay must be material enough to serve as a genuine incentive without dominating compensation to the point of creating perverse incentives to maximise near-term metrics. Secondly, the variable pay must be assessed against risk-adjusted, institution-wide outcomes, not merely individual disbursement volumes, gross fees, or absolute PAT. Variable pay must be capable of being reduced to zero in poor performance periods.

B. Deferral of Compensation

Deferral withholds a portion of variable pay for payment at a future date, subject to the absence of adverse risk outcomes during the deferral window. The purpose is to ensure that remuneration remains exposed to the consequences of decisions throughout the period over which those decisions actually materialise. The deferral period must be calibrated to the risk horizon.

C. Share-Linked Instruments

Awarding a portion of variable pay in share-linked instruments like stock options, ESOPs, phantom stock, stock appreciation rights aligns executive incentives with the long-term market value of the institution. An executive holding significant unvested equity is personally exposed to the consequences of decisions that may impair the institution’s stock price years after they are taken.

D. Malus

The term “malus” originates from the Latin word meaning bad or adverse, reflecting a mechanism that reduces or cancels remuneration before it vests. It is the primary ex-post adjustment tool during the deferral period.

The malus period must cover, at minimum, the entire deferral period, otherwise the deferral itself is meaningless. For malus to operate as a genuine deterrent, the policy must specify quantitative triggers rather than purely discretionary language.

E. Clawback

“Clawback” literally denotes the act of taking back something previously given, and refers to the recovery of remuneration that has already vested or been paid. It operates after the deferral period and is therefore more operationally complex. It requires enforceable contractual provisions in individual employment agreements (a policy reference alone is insufficient), may face legal challenges in certain jurisdictions, and demands investigation processes before invocation.

Malus and clawback are complementary, not substitutes. Malus stops deferred pay from flowing out during the risk-materialisation window; clawback reverses compensation already received where subsequent investigation reveals misconduct or misreporting that was not apparent at the time of payment.

Global Compensation Frameworks: Numbers, Not Principles

All major jurisdictions that have addressed financial institution compensation have converged on prescriptive parameters such as minimum deferral percentages, defined deferral periods, mandatory clawback windows, and MRT identification beyond the C-suite.

European Union: Capital Requirements Directive V (Art. 94)

Variable remuneration for MRTs is capped at 100% of fixed remuneration, extendable to 200% with shareholder approval. A minimum of 40% of variable pay must be deferred, rising to 60% where variable pay is ‘of a particularly high amount’, for at least four to five years (five years for senior managment). Malus and clawback provisions are mandatory during the deferral and retention periods. Payout schedules must be ‘sensitive to the time horizon of risks.’

Refer here: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32019L0878

Australia: APRA CPS 511

CPS 511 is among the most granular remuneration standards globally. For Significant Financial Institutions (SFIs): (i) the CEO must defer 60% of variable pay for a minimum of six years; (ii) other senior managers must defer 40% of variable pay for at least four years; (iii) the clawback window extends to a minimum of two years from the date of payment or vesting. Clawback criteria explicitly include ‘material misstatements of financial statements.’ CPS 511 also requires boards to link individual accountability (under the Banking Executive Accountability Regime) directly to the deferral and clawback framework.

Refer here: https://handbook.apra.gov.au/standard/cps-511

United Kingdom: SMCR / PRA Remuneration Code

Under the Senior Managers and Certification Regime, each Senior Manager holds a personal ‘Statement of Responsibilities.’ SYSC 19D mandates that MRTs face: (i) malus and clawback for a minimum of five to seven years (seven years for Senior Managers); (ii) minimum deferral of 40% of variable pay (rising to 60% for higher amounts); and (iii) a minimum deferral period of four years.

Compensation Regulation in Banks and NBFCs: A Comparative Regulatory Assessment

A comparison of the compensation frameworks prescribed under Paras 61–67 of the Reserve Bank of India (Commercial Banks – Governance) Directions, 2025 and Paras 29–37 of the Reserve Bank of India (Non-Banking Financial Companies – Governance) Directions, 2025 reveals a clear regulatory distinction. Banks are subject to a rule-based compensation regime with defined quantitative thresholds and risk-adjustment mechanisms, whereas NBFCs operate under a principles-based framework that affords greater implementation flexibility.

| Parameter | Commercial Banks | NBFCs | Key Difference |

| Board-approved Compensation Policy | Required | Required (Para 29) | Similar requirement: the NBFC framework is principle-based. |

| Nomination & Remuneration Committee (NRC) | Required | Required (Para 30) | Similar requirement. |

| NRC-Risk Management Committee Coordination | Mandatory; compensation outcomes to be aligned with capital adequacy and cost-to-income ratio | Required (Para 31) | Banks have more prescriptive alignment requirements. |

| Variable Pay – Minimum Share | At least 50% of total compensation for senior executives and MRTs | No prescribed minimum | Significant flexibility for NBFCs. |

| Variable Pay – Maximum Cap | Maximum 300% of fixed pay | Not prescribed | No regulatory cap for NBFCs. |

| Fixed vs Variable Pay Structure | Quantitatively prescribed | Principle-based (Para 33) | Banks subject to detailed limits. |

| Deferral of Variable Pay | Minimum 60% deferred | Deferral contemplated (Para 35) | NBFCs have no specified percentage. |

| Deferral Period | Minimum 3 years | Not specified | NBFCs may determine internally. |

| Deferral of Cash Component | At least 50% of cash component deferred (subject to threshold exemption) | Not specified | No equivalent requirement for NBFCs. |

| Vesting Schedule | No faster than a pro rata cumulative basis over deferral period | Not specified | Banks are subject to structured vesting norms. |

| Share-linked Instruments | Minimum 50%–67% of variable pay depending on pay structure | Not required | No specific requirement for NBFCs. |

| Alternative to Share-linked Instruments | All-cash permitted only in limited cases; variable pay capped at 150% of fixed pay | Not prescribed | No comparable restriction for NBFCs. |

| Material Risk Taker (MRT) Identification | Mandatory identification beyond KMPs | Not prescribed | The NBFC framework does not define MRTs. |

| Control Function Independence | Implied through governance framework | Specifically required (Para 35(4)) | Explicit requirement under NBFC Directions. |

| Malus and Clawback Framework | Mandatory | Mandatory (Para 37) | A framework is required for both. |

| Malus/Clawback Scope | Must cover at least deferral and retention periods | No prescribed period | Banks have detailed implementation standards. |

| NPA-specific Malus Trigger | Mandatory prohibition on unvested variable pay where NPA divergence exceeds RBI disclosure threshold | Not prescribed | Unique requirement for banks. |

| Guaranteed Bonus | Prohibited except for a sign-on bonus for new hires | Prohibited except for a sign-on bonus (Para 36) | Broadly aligned. |

| Hedging of Variable Pay | Prohibited | Not prescribed | No express prohibition for NBFCs. |

| Compensation Disclosure Requirements | Prescribed under governance framework | No specific disclosure framework | Banks are subject to greater transparency obligations. |

| Alignment with Risk Outcomes | Detailed linkage to risk, capital and performance metrics | Principle-based requirement | Banks have significantly greater regulatory prescription. |

Conclusion

The regulation of compensation is fundamentally a question of governance. While remuneration frameworks are intended to reward performance, financial sector experience has repeatedly demonstrated that performance measured over a short horizon may not accurately reflect the risks embedded in business decisions. Accordingly, modern compensation regulation seeks to align remuneration outcomes not merely with current profitability, but with the sustainability of that profitability over time.