It is quite common that whenever a borrower wishes to apply for a loan, lenders require the borrower to purchase an insurance policy, as a pre-condition for sanction. One may wonder if availing insurance can be a mandatory requirement for availing any loan? Insurance is not a regulatory requirement that is needed in loans, however, lenders prefer the same to safeguard their interest in the event of default.

In this article, the author examines the prevalent practice of lenders requiring borrowers to obtain insurance as a prerequisite for loan sanction and evaluates its permissibility within the regulatory framework.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-11 01:13:092025-10-13 10:29:16Insure to Ensure Your Loan?

In the Monetary Policy Statement dated October 1, 2025, the RBI Governor announced several measures to strengthen consumer protection. Some of the measures introduced for enhancing consumer protection are as follows:

The Draft IOS Scheme has enhanced the scope of the grievance redressal mechanism and introduced a more structured procedural framework for complaint processing. The Draft Internal Ombudsman Directions further strengthen grievance redressal, enhance procedural clarity, and improve transparency through reporting requirements. This write-up analyses the proposed changes.

Reserve Bank – Integrated Ombudsman Scheme, 2021 (“RB-IOS, 2021”) and Reserve Bank – Ombudsman Scheme, 2025 (“Draft Scheme”)

Heads

Current Requirement

Proposed Requirement/Change

Implication

Definition of Customer

The term “Customer” is not defined

Defined under Para 3(1)(j) as: “Customer” means any person who engages, in a financial service /product or activity related thereto with a Regulated Entity, irrespective of whether such person has an account-based relationship with the Regulated Entity;

The scope of financial services included within the ambit of the Scheme has been widened. For eg:All types of credit facilities extended by the borrower to the customer;Guarantees or other non-fund based facilities offered by RE to customer;Demand Draft facilities offered by Banks; Services by RE, acting as an LSP, to other REs;

Compensation Ceilings

Up to ₹20 lakh for consequential loss ₹1 lakh for consolatory damages

Increased to ₹30 lakh for consequential loss & ₹3 lakh for consolatory damages

There was no cap on the value of dispute that can be brought before the Ombudsman. The same has been retained. Increment in the compensation limits

“Advisory” Mechanism

Not provided

Para 14(4) empowers the Ombudsman to encourage settlement between parties through a written agreement, subject to the fact that all communications are documented. Para 14(6) allows the Ombudsman to issue advisory for settlement as a measure for the resolution of complaints.

RBI Ombudsman can now help parties resolve disputes by settlement.Draft IOS Scheme permits advisories i.e., communications from the Ombudsman advising REs to take actions for full or partial complaint resolution.Advisories are non-binding and serve as a pre-award tool to facilitate quicker settlements.

Change in the Appellate Authority

Executive Director in charge of the Department of the Reserve Bank administering the Scheme;

The Draft IOS Scheme clearly mentions that the executive director in charge of the Consumer Education and Protection Department (CEPD) is the Appellate Authority

Explicitly mentions the independent department under the RBI to act as the Appellate Authority.

Guidance on filing of the complaint form

Guidance was provided under the Scheme at several places, but not at one place, along with the form

Added under Part A of Annexure, along with the Complaint Form

Minor edits in the complaint form with guidance to clarify the process for filing complaints and reduce errors.It will enable quicker allocation and segregation of complaints.The clear filing mechanism will improve ease and understanding for customers.Improved accessibility by the Launch of a 24×7 Contact Centre (#14448) with multilingual IVRS support.

Ombudsman Report

Earlier, the Ombudsman was required to submit an annual report to the Deputy Manager of the RBI; however, the RBI was not obligated to publish it

Under the Draft IOS Scheme, it has now been made mandatory for the RBI to publish an annual report on the functioning and activities carried out under the Scheme.

It will enable the regulator to understand the issues raised under the complaints and assess the effectiveness of the measures introduced.

Addition of an RE as third party to proceedings

Not provided

The Ombudsman can make any other RE as a party to the proceedings.

Expands the powers of the ombudsman to include connected REs as well (for instance, in the case of co-lending or TLE transactions)

Power of CRPC to classify and close complaints

Not explicitly mentioned

RBI Ombudsman and CRPC remain responsible for receipt and examination of complaints.The Complaints shall be treated as follows:Complaints in the nature of suggestions or queries shall be treated as non – valid at the stage of CRPFFurther, Para 10 specifies certain grounds for non maintainability of complaints for complaints to be rejected by the RBI Ombudsman.However the grounds of non-maintainability under Para 10 shall be specifically provided by the Competent Authority.

This clarifies the hierarchy for complaint handling and enables early elimination of frivolous or ineligible complaints before they reach the RE.

It may also be noted that the RBI has, vide notification dated 07th October 2025, extended the applicability of the existing RBI-IOS to include State Co-operative Banks and Central Co-operative Banks.

Draft Master Direction – Reserve Bank of India (Internal Ombudsman for Regulated Entities) Directions, 2023

Particulars of the Provision

Current Requirements

New Requirements

Implication

Eligibility of the IO (Para 5)

No such requirement prescribed

If the person is a serving officer, he/she is required to relinquish the same before assuming charge as IO. The IO shall previously not have been employed, nor presently be employed, by the RE or a holding, associate or subsidiary company of the RE.

To ensure the IO’s independence and impartiality, in case the proposed IO is a serving officer, he/she must relinquish the existing position before assuming charge, enabling objective and credible grievance redressal within the RE. Further, conflict of interest positions clarified by specifically defining the scope of Related Parties of the RE.

Same IO appointment in a number of entities

No such clause restricting the number of REs.

The IO can work in more than one RE simultaneously, with specific approval from the CEPDSuch approval shall be obtained by the appointing RE.However, the deputy IO cannot be appointed in more than one RE simultaneously

IO (but not deputy IO) has been permitted to be appointed in more than one RE simultaneously, subject to the approval from CEPD. Approval to be obtained by the appointing RE. Impact:To allow efficient deployment of an experienced IO across multiple REs under CEPD oversight, while ensuring sufficient focus at each entity so that the role and effectiveness are not compromised.

Terms of Appointment of IO

No clause that specifies the minimum no of IOs or the responsibility of the Board or its Committees w.r.t assessing the need for multiple IOs or the factors to be considered when doing so.

Every RE shall appoint at least one IO. The Board or its committees shall, at least annually, determine the number of IO/ Dy. IO to be appointed. This must be determined with due regard to the volume and complexity of the complaints received.

To ensure effective grievance redressal, clarity has been provided on the minimum number of IOs to be appointed and the annual assessment of the need for IOs. Actionables for the REs:All REs shall appoint at least one IO The Committee of the RE shall be required to assess the need of the no of IOs at least once in a yearFactors to be considered include complexity of complaints, sufficiency of the time, diversity of experience etc

Auto-escalation of complaints

All complaints that are partly or wholly rejected by the RE’s internal grievance redress mechanism shall be auto-escalated to the IO within 20 days of receipt for a final decision.

Auto-escalation of partly resolved or wholly rejected complaints to the office of the IO has been specified to be 25 days in case of CICs (Credit Information Companies)

To ensure timely escalation of unresolved complaints, the draft directions require auto-escalation to the IO within 20 days, with a relaxed timeline of 25 days for CICs, balancing prompt redressal with operational feasibility for CICs.

Board oversight – rotation of IOs

No such clause to ensure rotation of IOs in REs with multiple IOs exists in the current directions.

In REs having multiple IOs, a view shall be taken by the Board or Customer Service Committee / Consumer Protection Committee of the Board to have representation of more than one IO or having a system of rotation.

Actionables for REs:To ensure diversity in perspectives in grievance handling, REs with multiple IOs should consider Board-approved rotation or representation of more than one IO, enhancing fairness and effectiveness in complaint resolution.

Complaint Management System (CMS)

Under the current directions, REs do not have to provide specific categories in the CMS.

The REs shall provide only three categories i.e. ‘Fully Resolved’, ‘Partly Resolved’ and ‘Wholly Rejected’ in its CMS for recording the decision on the complaints before escalation to the office of IO.

RE shall be required to have in place a fully automated Complaint Management System. To standardise complaint recording, REs must limit CMS decision categories to ‘Fully Resolved’, ‘Partly Resolved’, and ‘Wholly Rejected’ before escalation to the IO, ensuring consistency and clarity in complaint tracking.

Procedure for Complaint Redress by IO / Dy. IO

The current directions allow the IO to only rely on documents that are furnished to it by the RE.

The IO / Dy. IO may, if they find it necessary, seek written or oral submission (including additional information and documents) from the complainant.

Strengthening the principle of hearing, enhances procedural transparency, and facilitates effective complaint redressal.

Reporting to Reserve Bank

The current directions have different disclosure requirements pertaining to categorisation of complaints and periodicity of reporting.

In addition to the existing details to be provided to the CEPD, the draft directions have included the additional details to be included such as Date of Birth and the Date of intimation to the Reserve Bank in its intimation to the CEPD. Further an additional periodic reporting requirement on quarterly basis instead of the previously annual requirement has been introduced for the REs.

These additional details enable the regulator to verify that the eligibility of the IO, as prescribed in the regulations, is being complied with specifically, ensuring the age limit of 70 years based on the date of birth and that the intimation to the RBI is duly sent. Further, the quarterly reporting requirement allows the CEPD to track the status of complaints and the IOs reported, enabling the regulator to assess implementation and the overall compliance position of the entity.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-10 18:34:572025-10-10 18:34:58RBI’s Draft on Integrated and Internal Ombudsman

The proposed ECL framework marks a major regulatory shift for India’s banking sector; it is long overdue, and therefore, there is no case that the RBI should have deferred it further. However, it comes coupled with regulatory floors for provisions, which would cause a major increase in provisioning requirements over the present requirements. Our assessment, on a very conservative basis, is that the first hit to Bank P/Ls will be at least Rs 60000 crores in the aggregate.

A major impact that the draft directions will have on the Banking sector is the need to maintain increased provisioning pursuant to a shift from an incurred loss framework to the ECL framework. Under the existing framework, banks make provisions only after a loss has been incurred, i.e., when loans actually turn non-performing. The proposed ECL model, however, requires banks to anticipate potential credit losses and set aside provisions for such anticipated losses.

Banks presently classify an asset as SMA1 when it hits 30 DPD, and SMA2 when it turns 60. Both these, however, are standard assets, which currently call for 0.4% provision. Under ECL norms, both these will be treated as Stage 2 assets, which calls for a lifetime probability of loss, with a regulatory floor of 5%. Thus, the differential provision here becomes 4.6%.

Once an asset turns NPA, the present regulatory requirement is a 15% provision; the ECL framework puts these assets under Stage 3, where the regulatory minimum provision, depending on the collateral and ageing, may range from 25% to 100%. Our Table below gives more granular comparison.

Type of asset

Asset classification

Existing requirement

Proposed requirement

Difference

Farm Credit, Loan to Small and Micro Enterprises

SMA 0

0.25%

0.25%

–

SMA 1

0.25%

5%

4.75%

SMA 2

0.25%

5%

4.75%

NPA

15%

25%-100% based on Vintage

10%-85% based on Vintage

Commercial real estate loans

SMA 0

1%

Construction Phase -1.25%

Operational Phase – 1%

Construction Phase -0.25%

Operational Phase – Nil

SMA 1

1%

Construction Phase -1.8125%

Operational Phase – 1.5625%

Construction Phase -0.8125%

Operational Phase – 0.5625%

SMA 2

1%

Construction Phase -1.8125%

Operational Phase – 1.5625%

Construction Phase -0.8125%

Operational Phase – 0.5625%

NPA

15%

25%-100% based on Vintage

10%-85% based on Vintage

Secured retail loans, Corporate Loan, Loan to Medium Enterprises

SMA 0

0.4%

0.4%

–

SMA 1

0.4%

5%

4.6%

SMA 2

0.4%

5%

4.6%

NPA

15%

25%-100% based on Vintage

10%-85% based on Vintage

Home Loans

SMA 0

0.25%

0.40%

0.15%

SMA 1

0.25%

1.5%

1.25%

SMA 2

0.25%

1.5%

1.25%

NPA

15%

10%-100% based on Vintage

(-)5% – 85% based on Vintage

LAP

SMA 0

0.4%

0.4%

–

SMA 1

0.4%

1.5%

1.1%

SMA 2

0.4%

1.5%

1.1%

NPA

15%

10%-100% based on Vintage

(-)5% – 85% based on Vintage

Unsecured Retail loan

SMA 0

0.4%

1%

0.6%

SMA 1

0.4%

5%

4.6%

SMA 2

0.4%

5%

4.6%

NPA

25%

25%-100% based on Vintage

0%-75% based on Vintage

The actual impact of such additional provisioning will be a hit of more than 3% to the profit of banks1. Based on the RBI Financial Stability Report of FY 24-252, the current level of SMA and NPA is estimated to be ₹3,78,000 crores (2%) and ₹4,28,000 crores (2.3%), respectively.

Accordingly, an additional provision of approximately₹ 18,000 crores (4.6% of SMA volume) and ₹ 42,000 crores (10% of NPA volume) will be required for SMA and NPA respectively, leading to a total impact of at least ₹60,000 crores. This estimate has been arrived at by considering the % of NPAs and SMA-1 & SMA-2 portfolios of banks. The actual impact may be higher, as lot of loans may be unsecured, and may have ageing exceeding 1 year, in which case the differential provision may be higher.

It may be noted that while the draft directions allow Banks to add back the excess ECL provisioning to the CET 1 capital, it does not neutralize the immediate profitability impact, as the additional provisions would still flow through the profit and loss account.

How do we expect banks to smoothen this hit that may affect the FY 27-28 P/L statements? We hold the view that it will be prudent for banks, who have system capabilities, to estimate their ECL differential, and create an additional provision in FY 25-26, or do technical write-offs.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-09 13:30:392025-10-09 17:53:13Expected to bleed: ECL framework to cause ₹60,000 Cr. hole to Bank Profits

When AIF Regulations were formally introduced in 2012, the regulatory approach was deliberately light. The framework targeted sophisticated investors, allowing flexibility with limited oversight. Over the years, however, AIFs have become significant participants in capital markets. Market practices over the decade exposed regulatory loopholes and arbitrages. For example, some investors who did not individually qualify as QIBs accessed preferential benefits indirectly through AIF structures and investors who were restricted to invest in certain companies started investing through AIF making AIF an investment facade. There were concerns regarding circumvention of FEMA norms as well1. In the credit space, regulated entities such as banks and NBFCs started channeling funds through AIFs to refinance their stressed borrowers, raising concerns around loan evergreening2. These developments prompted regulatory response. RBI first issued two circulars, one in 2023 and the other in 2024. Finally, in 2025 formal directions governing investments by regulated entities in AIFs were also issued3. These Directions introduced exposure caps and provisioning requirements.4

While the RBI addressed prudential risks arising from regulated entities’ participation in AIFs, SEBI focused on investor protection, governance within the AIF ecosystem and curbing the regulatory arbitrages. First it mandated on-going due diligence by AIF Managers5. It then mandated specific due diligence6 of investors and investments of AIF to prevent indirect access to regulatory benefits. Fiduciary duties of sponsors and investment managers and reporting obligations were progressively codified through circulars. Managers were expected to maintain transparency vis-a-vis their investment decisions, maintain written policies including ones to deal with conflict of interest with unitholders and submit accurate information to the Trustee. What were once broad, principle-based expectations have evolved into detailed, enforceable rules. Regulatory tightening has been matched by a more assertive enforcement approach. SEBI’s recent settlement order7 against an AIF underscores its increasing scrutiny of governance lapses, mismanagement of conflicts and inaccurate reporting. This clearly signals that any compliance gaps will no longer be overlooked and are likely to attract regulatory action. In a separate adjudication order, SEBI imposed penalties on both the Trustee and the Manager for the delayed winding-up of the scheme, underscoring that accountability within an AIF structure extends to all key parties and is not limited to the Manager alone.

However, SEBI’s approach has not been solely restrictive. Alongside regulatory tightening, it has also sought to preserve commercial flexibility and respond to market needs. Examples include the introduction of the co-investment framework8 for AIFs, framework for offering differential rights to select investors and a revamp for angel funds9.

Together, these measures are reshaping the regulatory landscape for AIFs and their managers. Investors can no longer rely on AIF structures to indirectly obtain regulatory advantages otherwise unavailable to them. As AIFs have grown in scale and importance, what is emerging is a more transparent, prudentially sound and closely supervised regulatory regime designed to align investor protection and commercial flexibility.

See SEBI’s Consultation paper on proposal to enhance trust in the AIF ecosystem ↩︎

See our write-up on AIFs being used for regulatory arbitrages here. ↩︎

See our write-up on changes w.r.t Angel Funds here↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-09 10:45:482025-10-10 10:19:44AIF Regulatory framework evolves from light-touch to right-hold

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-09 10:37:052025-10-09 17:38:55The Law of Prepaid Payment Instruments (PPIs): A Guide For New Market Entrants

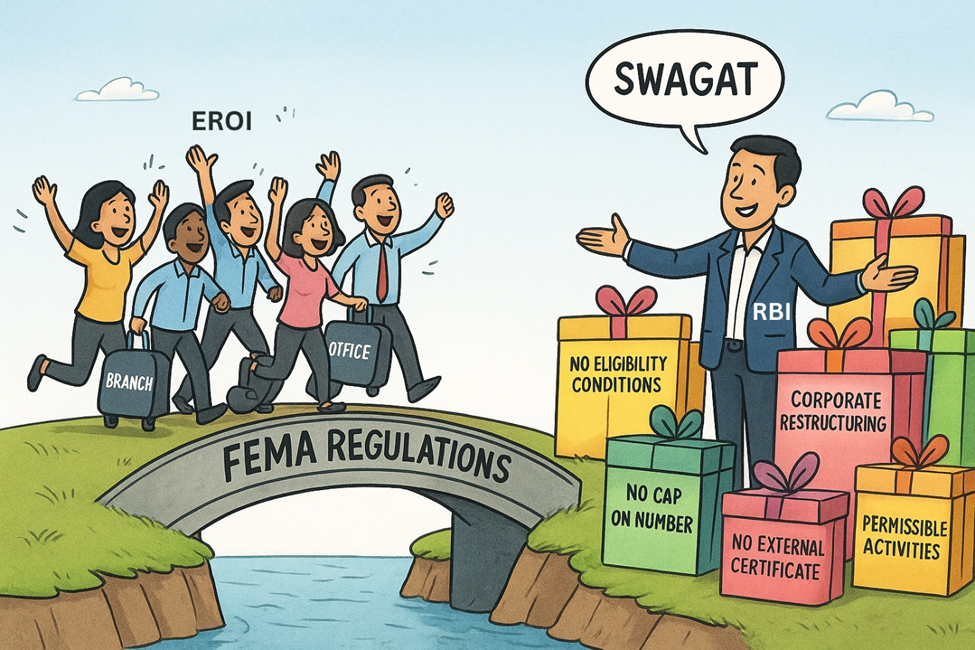

As a part of its efforts to rationalise the regulations for establishment of a place of business in India by overseas entities[1], RBI has issued Draft Foreign Exchange Management (Establishment in India of a branch or office) Regulations, 2025. The proposals primarily aim to enable delegation of more powers to AD banks and reduction of compliance burden, thereby further enhancing the ease of doing business in India.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2025-10-06 16:41:442025-10-06 16:48:03SWAGAT to foreign branches or offices in India: RBI proposes draft regulations on such establishments

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-05 21:54:262025-10-05 22:39:04Revised Form IEPF-5 paves way for simplified claim process

Debentures, one of the most common means for raising debt funding, where investors lend money to the issuer in return for periodic interest and repayment of principal at maturity. While the basic feature of any debenture is a fixed coupon rate and a defined tenure (commonly referred to as plain vanilla instruments), sometimes these instruments may be topped up with enhanced features such as additional credit support, market-linked returns, convertibility option, etc., thus referred to as structured debt securities.

Structured debt securities: motivation for issuers

Apart from the economic favouring such structural modifications, a primary motivation for the issuer in issuing such structured instruments might be the regulatory advantages that these securities offer. For instance,

Chapter VIII of SEBI NCS Master Circular provides an extra limit of 5 ISINs for structured debt securities & market-linked securities, thus more room for the issuers to issue debt securities, compared to the restriction of a maximum of 9 ISINs for plain vanilla debt.

In addition, as per NSE Guidelines on Electronic Book Provider (EBP) mechanism, market-linked debentures are not required to be routed through EBP, allowing issuers to place such instruments almost like an over-the-counter trade. This allows issuers to structure the debt securities on a tailored basis and offer them directly to specific investors.