– Vinita Nair and Saloni Khant | corplaw@vinodkothari.com

– Updated on May 3, 2026

Being the 10th largest[1] in the world, the Indian Insurance market grows at 10-15% annually but insurance penetration is only at 3.7% of the GDP[2] as against the global average of 7.3%. With a view to boost growth in the sector and implement the vision of ‘”Insurance for All by 2047’, amendmentsin the existing insurance laws were placed before the public for consultation in November, 2024. Following the due process of legislation, the draft bill underwent several changes, was passed by both the houses of the parliament, assented to by the president and finally notified in the Official Gazette as the Sabka Bima Sabki Raksha (Amendment Of Insurance Laws) Act, 2025 (“Amendment Act”) on December 21, 2025. The Amendment Act, that amends the Insurance Act, 1938, Life Insurance Corporation Act, 1956 and Insurance Regulatory and Development Authority Act, 1999, introduces fundamental reforms by liberalising foreign investments and reducing capital requirements but at the same time, strengthens regulatory oversight on the market participants with additional measures to protect the interest of the policyholders.

The Amendment Act became effective from February 5, 2026. The amendment relating to prohibition on common MD and officers among insurance companies, banking companies and investment companies (Section 32A of the Insurance Act), has not been made effective, in view of industry representation made to IRDA, refer the discussion below.

It is quite common that whenever a borrower wishes to apply for a loan, lenders require the borrower to purchase an insurance policy, as a pre-condition for sanction. One may wonder if availing insurance can be a mandatory requirement for availing any loan? Insurance is not a regulatory requirement that is needed in loans, however, lenders prefer the same to safeguard their interest in the event of default.

In this article, the author examines the prevalent practice of lenders requiring borrowers to obtain insurance as a prerequisite for loan sanction and evaluates its permissibility within the regulatory framework.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-11 01:13:092025-10-13 10:29:16Insure to Ensure Your Loan?

The Insurance Regulatory and Development Authority of India (IRDAI) has been committed to nurturing a regulatory environment to accomplish its vision, undertaking significant steps towards ensuring that insurance products and services are accessible to all segments of society. At the 125th meeting held on March 19, 2024, the Authority approved the consolidation of 34 regulations into 6 and 2 new regulations after reviewing the existing regulatory framework in the insurance sector. These regulations span crucial areas such as the protection of policyholders’ interests, responsibilities towards rural and social sectors, the establishment of an electronic insurance marketplace, regulation of insurance products, and the operation of foreign reinsurance branches. Additionally, they cover aspects related to registration, actuarial practices, finance, investment, and corporate governance highlighting IRDAI’s focus on making regulations clearer and more effective.

These regulations result from consultations with a diverse range of stakeholders, including experts in the insurance industry, representatives, and the general public. The new regulations have been notified vide separate gazette notifications on 22nd March 2024 and onwards.

While the new Regulations primarily consolidate the existing Regulations as stated above, these also bring in certain new requirements and relaxations for the insurers. In this article, we attempt to discuss the changes brought by the IRDAI (Registration, Capital Structure, Transfer of Shares and Amalgamation of Insurers) Regulations, 2024 (“Registration Regulations, 2024”), and the implications thereof. The amendments in the new regulation are as follows:

Insertion of the definition of Competent Authority

Withdrawal of application of registration as insurer

Non-applicability of lock-in for listed insurers

Issuance of shares at face value and in the same proportion

Temporary relaxation from restrictions on investment by the promoter of the insurer

Fit and Proper Criteria

Basis of valuation of equity shares of promoter SPV of insurer

Relaxation in lock-in requirements

Reduction in lock-in requirements for shareholding in the insurer

Nomination of Director

Prior approval of IRDA for the listing of the insurer

Effective date

The effective date of the Registration Regulations, 2024 shall be the date of publication in the official gazette, i.e., 20th of March 2024.

New requirements introduced vide the Registration Regulations, 2024

Regulation No.

Topic

Text of the Regulation

Our Remarks

2 (g)

Competent Authority

Competent Authority meansChairperson or Whole-Time Member or Committee of the Whole-Time Members or Officer(s) of the Authority, as may be determined by the Chairperson.

The concept of “Competent Authority” has been introduced, vide which the recognition of delegated authority has been made explicit in the Regulations.

In the Registration Regulations, 2024, the reference to the “Authority”, i.e., IRDAI has been substituted with “Competent Authority” in a few matters like approval for the R1 stage, extension for commencement of business, withdrawal of application, etc. where powers have been delegated to the Competent Authority.

6(7)

Withdrawal of application of registration as insurer

(a) Any applicant may apply to the Competent Authority for withdrawal of the application for registration at any stage of application, along with reasons.

(b) The Competent Authority may approve or reject the said request for withdrawal for the reasons to be recorded in writing.

(c) In case of rejection of request for withdrawal of application, the R1 application or R2 application, as the case may be, may be rejected in accordance with Regulation 6(6)

The Erstwhile Regulations did not contain express provisions with respect to the withdrawal of registration by a proposed insurer, however, the conditions for disqualification of an applicant included a case of withdrawal of the former application by the applicant.The manner in which an application may be withdrawn by an issuer has been specifically provided for under the Registration Regulations 2024.

12(3)

Issuance of shares at face value and in the same proportion

Till the time of commencement of insurance business:(i)The equity shares of the Applicant and SPV shall be issued at its face value;

(ii)The infusion of funds in the Applicant and SPV, by its shareholders, shall be commensurate with the percentage of their equity stake in the Applicant and SPV:

Provided that the issuance of equity shares of insurer or SPV may be permitted to be issued at premium, after the commencement of business.

Till the commencement of business of the insurer, shares are to be issued at face value only and to the existing shareholders in proportion to their existing holding indicating maintenance of a similar shareholding pattern from application till actual commencement of business.This should ideally mean the commencement of business operations as an insurer, and not obtaining the certificate of commencement as under Section 10A of the Companies Act, 2013.

Proviso to Reg 13(1)

Temporary relaxation from restrictions on investment by the promoter of an insurer

Provided that the Competent Authority may permit a person to be promoter of more than one insurer engaged in the same class of insurance business on a temporary basis if the same is part of the Scheme filed with the Authority under section 35 of the Act.

The new proviso facilitates the provision of temporary relaxation by the Competent Authority for a person to act as a promoter in more than one insurer of the same if it is a part of the scheme of amalgamation or transfer filed with the Authority.

Schedule 1

Fit and Proper Criteria

(c) Compliance with all applicable laws in India including Prevention of Money Laundering Act, FEMA and taxation law.

Specific reference to the Prevention of Money Laundering Act has been introduced.

Express mention of the term “individual” to signify applicability to individuals along with entities. The Erstwhile Regulations referred to “entity” only. However, even before the insertion, the insurer and the promoters were required to ensure compliance with the criteria. The interpretation before the insertion was the same.

Amendments to existing requirements under Erstwhile Regulations

Regulation No.

Topic

Provisions under Registration Regulations, 2024 vis-a-vis Erstwhile Regulation

Our Remarks

8

Relaxation in lock-in requirements

Provided that the Competent Authority may relax the lock-in period in following circumstances: i.(i) To enable the insurer to list its shares on the stock exchange(s) in India.; or (ii) Under circumstances of distressed financial position or, amalgamation or reorganization pursuant to change in applicable law of the any insurer or the its shareholder(s):

Provided further that the lock-in period shall not be applicable in case of equity shares allotted to employees or directors of the insurer pursuant to any scheme formed for the benefit of the employees or directors of the insurer:

Provided further that the lock-in period shall not be applicable in case of investor holding not more than one percent of the equity shares of the insurer.

Exemption at the discretion of the Competent Authority:

The new Registration Regulations, 2024 contain enabling powers with the Competent Authority to provide relaxation from lock-in in case of circumstances of distressed financial position or amalgamation/ re-organisation pursuant to legal requirements.

Absolute exemptions: Exemption is given from the applicability of lock-in period for: a. investor holding less than 1% of insurer’s equity; or b. Shares are held under employee benefit scheme.

8

Reduction in lock-in requirements for shareholding in insurer

Investment after 10 years but before 15 years post grant of R3:

In case of change in shareholding pattern: Promoter: 2 years from the date of investment Investor: 1 year from the date of investment

Investment after 15 years post grant of R3 Promoter: 1 year from the date of investment Investor: Nil

The Erstwhile Regulations required prior approval of IRDAI before listing of shares of the insurer. Under the new Regulations, 2024, only prior intimation is required subject to satisfaction of the following conditions: I. Listing of equity shares is in the interests of policyholders; II. The insurer shall comply with the regulatory framework. III. The listing of equity shares shall not be used as a medium to raise capital or transfer shares which would be in contravention of the applicable regulatory provisions. IV. The insurer shall seek approval for the transfer of shares. V. The insurers specified under section 10A of the General Insurance Business (Nationalization) Act, 1972 shall ensure compliance with the provisions of section 10B of the said Act. VI. Such other conditions as may be specified.

10

Basis of valuation of equity shares of promoter SPV of insurer

The equity shares to be issued by the SPV shall be valued at a price determined on the basis of valuation certificate issued by two oneSEBI Registered Category-I Merchant Banker.

Valuation of shares of the SPV can be determined based on a valuation certificate issued by one SEBI Registered Category-I Merchant Banker instead of two as required under the Erstwhile Regulations

16

Nomination of Director

Provided that the investor may nominate a director on the Board of the insurer if its investment exceeds 10 percent of the paid up capital of the respective insurer.

New Regulations 1.The investors may nominate not more than one director on the Board of the insurer if its investment exceeds 10 percent of the paid-up capital of the respective insurer. 2. If the investment in the insurer does not exceed ten percent of the paid-up capital of the respective insurer. The investor shall not nominate any director on the Board 3. No shareholder shall nominate any director on the board of any insurer if it has already nominated a director on the board of any other insurer engaged in the same class of insurance business.

The 2024 Regulations provide stringent requirements with respect to the appointment of a nominee director, allowing only 1 nominee director to be appointed. Further, the restriction of appointing only one nominee director is across insurers.

Will this mean that an investor and the insurer can not mutually agree to have representation on the insurer’s Board or, seek express permission from the Authority for such representation?

29

Prior approval of IRDA for listing of insurer

No Indian insurance company transacting the General insurance or Health insurance or Reinsurance business shall approach the SEBI for public issue of shares and for any subsequent issue, by whatsoever name called, under the ICDR Regulations without the specific previous approval of the Authority in writing under these Regulations.

New Regulations: An insurer may approach the appropriate financial sector regulator for listing of its equity shares, by way ofdivestment of equity shares by existing shareholders or fresh issue of equity shares by the insurer or both, on thestock exchange(s) recognized under Securities Contracts (Regulation) Act, 1956 upon fulfilment of following conditions: (1) The Board of the insurer resolves that such listing of equity shares is in the interests of policyholders. (2) The Board of the insurer resolves that the insurer shall be able to comply with the regulatory stipulations of the said financial sector regulator(s). (3) The listing of equity shares on stock exchange(s) shall not be used as medium to raise capital or transfershares which would otherwise be in contravention to the applicable regulatory provisions. (4) All the regulatory provisions stipulated by the Authority shall be complied with scrupulously.(5) The insurer shall have obtained prior approval for transfer of shares for offer for sale and/or fresh issuanceof shares, as may be required vide section 6A of the Act read with Regulation 21 of these regulations:Provided that the submission of the details of transferee shall not be mandatory. (6) The insurers specified under section 10A of the General Insurance Business (Nationalization) Act, 1972shall ensure compliance with the provisions of section 10B of the said Act. (7) The insurer shall file an intimation with the Authority at least 15 days before it approaches the appropriate financial sector regulator for listing of its equity shares. The insurer shall also keep the Authority informed regarding the subsequent developments in the said matter. (8) Any documents filed by the insurer under this chapter or any communications between insurer and the Authority with regard to proposed listing of equity shares shall not in any manner be deemed to be orserve as a validation by the Authority of the facts, representations, assertions or anything written in theoffer documents. This fact shall be disclosed in bold letters in the offer document. (9) Such other conditions as may be specified.

The Erstwhile Regulations required prior approval of IRDAI before listing of shares of the insurer. Under the new Regulations, 2024, only prior intimation is required subject to satisfaction of the following conditions: I. Listing of equity shares is in the interests of policyholders; II. The insurer shall comply with the regulatory framework. III. The listing of equity shares shall not be used as a medium to raise capital or transfer shares which would be in contravention to the applicable regulatory provisions. IV. The insurer shall seek approval for the transfer of shares. V. The insurers specified under section 10A of the General Insurance Business (Nationalization) Act, 1972 shall ensure compliance with the provisions of section 10B of the said Act. VI. Such other conditions as may be specified.

Conclusion

One of the key objectives of the IRDAI includes the promotion of competition to enhance customer satisfaction through increased consumer choice and fair premiums while ensuring the financial security of the Insurance market. The Registration Regulations, 2024 largely revolve around encouraging and providing flexibility to the insurers in notable areas like registration, lock-in relaxations, and listing of the insurers. By consolidating regulations, the process of starting and operating an insurance company is expected to become more efficient, having a single regulation may improve clarity and transparency for insurers regarding these processes, and a simplified procedure would encourage investment and participation in the Insurance Sector. The consolidation of various regulations is a step to pave the way for a more inclusive insurance sector, attracting new insurers, and ultimately achieving IRDAI’s vision of ‘Insurance for All’ by 2047.

Our resource centre on Insurance Law can be accessed here.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00surabhichurahttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngsurabhichura2024-04-25 14:29:592024-07-28 11:40:34IRDAI is a step closer to the vision of Insurance for All by 2047

The Guidelines for Corporate Governance (‘2016 Guidelines’) for insurers in India have been around for close to a decade now. These Guidelines were initially brought as an update to the then 2009 Guidelines for the purpose of aligning the same with the extensive changes to the governance of companies brought about by the Companies Act, 2013. As such, the new Guidelines were framed to be mostly in line with the Act of 2013 except certain provisions such as requiring the CEO to be a WTD of the Board (where the chairman is NED), prescribing fit and proper criteria for directors, requiring certain additional committees, having only profit criteria for CSR applicability, etc.

Through the years, these Guidelines have served as a valuable source of direction in ensuring corporate governance for insurers; laying down guidance for the composition, roles and responsibilities of the Board, functions of various Board Committees, appointment and remuneration of KMPs, disclosures in financial statements, etc.

On 14th November, 2023, the IRDAI released an Exposure Draft EOM Regulations, 2023 (‘Exposure Draft’) which proposes to repeal the following regulations:

Insurance Regulatory and Development Authority of India (Expenses of Management of Insurers transacting General or Health Insurance Business) Regulations, 2023;

Insurance Regulatory and Development Authority of India (Expenses of Management of Insurers transacting Life Insurance Business) Regulations, 2023 and

Insurance Regulatory and Development Authority of India (Payment of Commission) Regulations, 2023.

The Exposure Draft is seemingly a consolidation of the aforesaid regulations with a few modifications. Further, most of these so-called modifications are essentially in the nature of rephrasing certain statements, for instance, formulation of business plan ‘in advance’ being replaced with ‘prior to commencement of financial year’.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00mahakagarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngmahakagarwal2023-11-24 14:31:052023-11-24 14:33:04What’s new under the IRDAI’s Exposure Draft on Expenses of Management Regulations?

As the new financial year 23-24 commences, we look back at where we stand at the end of FY 22-23, in terms of the regulatory developments. While there has been no substantial traffic in terms of regulatory developments to the Companies Act, the migration of various forms in MCA’s V3 portal proved to be (and still continues to be so in some cases) a turmoil, with a standstill in the fundraising process, and other practical difficulties, even resulting in levy of additional fines.

There has been significant traction on the part of SEBI too. While Structured Digital Database (SDD) remained the buzzword for the listed entities with the stock exchanges requiring them to submit quarterly compliance certificates, the stress for proper controls on insider trading remained the focal point. Having stiffed the nerves of the Compliance Officers in the listed entities through the quarterly compliance certificates, the same has been finally absorbed in the annual secretarial compliance reports under the Listing Regulations.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Payal Agarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPayal Agarwal2023-04-03 17:12:532023-04-03 17:12:54Entering in FY 23-24: Regulatory review of corporate law developments

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Kaushal Shahhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngKaushal Shah2022-10-17 20:59:562022-11-02 10:59:13Guidelines on Information and Cyber Security extended to Insurance Intermediary

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Kaushal Shahhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngKaushal Shah2022-10-13 19:55:472022-11-02 10:59:07IRDA relaxes stringent norms for Common Directors among insurance intermediaries

Insurance relationships are fundamentally built on trust between insurers and their customers. (Insurance and Regulatory Development Authority of India (‘IRDA’) has been quite stringent with respect to curbing instances of conflicts of interest in case of insurance companies and/ or insurance intermediaries.

As per Exposure Draft on IRDAI (Conflict of Interest) Guidelines, 2019[1], “Conflict of Interest” means a situation in which a person or organization is involved in multiple interests, financial or otherwise, and serving one interest could involve working against another and includes situations when a person’s impartial and objective performance of duties or decision-making could be jeopardized because of personal interests being involved;

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2022-09-08 12:48:002022-10-13 12:54:01IRDA rolls out conditions for common directorship in insurance company and intermediary

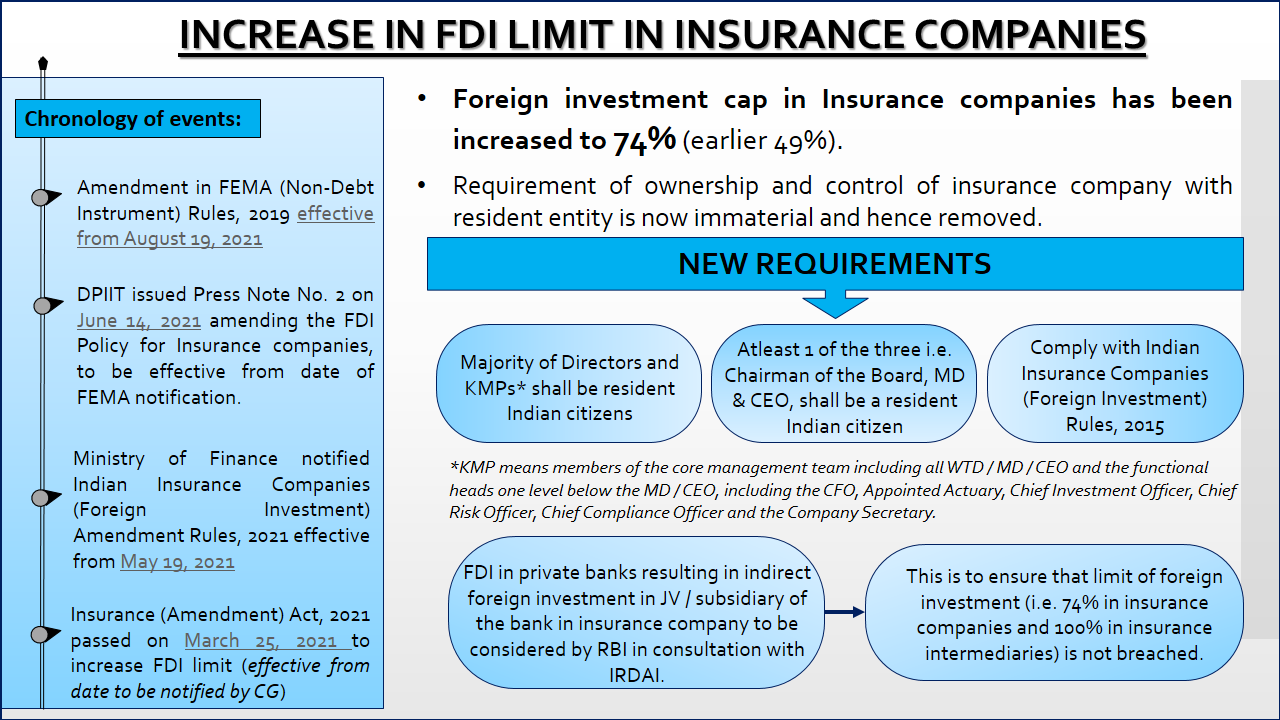

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2021-08-24 16:20:312021-09-07 12:03:41Increase in FDI Limit in Insurance Companies