Whether private NBFCs-ML are required to appoint IDs?

– Neha Malu, Associate | finserv@vinodkothari.com

Independent directors have long been regarded as critical instruments of corporate governance. They bring fresh perspectives, specialized knowledge and most importantly, an element of unbiased oversight to board deliberations. Think of them as neutral referees who ensure fair play in business operations and uphold the integrity of boardroom decisions. Their presence helps reduce conflicts of interest, curb excessive promoter influence and encourage more balanced and professionally informed decision-making.

Under the Companies Act, 2013, section 149 read with rule 4 of the Companies (Appointment and Qualifications of Directors) Rules, 2014 lays down the categories of companies that are mandatorily required to appoint independent directors[1]. These categories do not include private companies. The rationale is intuitive: private companies, by their very nature of being closely held, are presumed to function under greater internal control, thereby reducing the perceived need for external board oversight. The whole basis of “privacy” of a private company will be frustrated if there are independent persons on its board.

Further, wholly owned subsidiaries are explicitly exempted from the requirement to appoint independent directors under rule 4(2), regardless of their nature or size.

And accordingly, a point of regulatory discussion arises in the case of (i) private NBFCs and (ii) NBFCs that are wholly owned subsidiaries, classified in the middle layer or above under the SBR Master Directions. While the Companies Act, 2013 does not mandate the appointment of independent directors for private companies and explicitly exempts WOS from such requirement, the corporate governance provisions under the SBR Master Directions require the constitution of certain committees, the composition of which hints towards the presence of independent directors.

This gives rise to a key question: Does a private NBFC or a wholly owned subsidiary, solely by virtue of its classification under the middle layer or above, become subject to an obligation to appoint independent directors?

Committees for NBFC-ML and above, the composition of which includes IDs

Upon classification as an NBFC-ML or above, conformity with corporate governance standards becomes applicable. Below we discuss specifically about the committees, the composition of which also includes IDs:

Audit Committee, consisting of not less than three members of its Board of Directors. If an NBFC is required to constitute AC under section 177 of the Companies Act, 2013, the Committee so constituted shall be treated as the AC for the purpose of this para 94.1.

As per section 177, an AC shall comprise a minimum of three directors, with Independent Directors forming a majority. Hence, in case the NBFC is not covered under the provisions of section 177, the same may be constituted with any three directors, not necessarily being independent directors.

Composition will be as per section 178 of the Companies Act, 2013.

The provisions indicate that the NRC shall have the constitution, powers, functions and duties as laid down in section 178. In this context, Companies Act requires every NRC to consist of at least three non-executive directors, out of which not less than one-half should be independent directors.

The Committee shall be a Board-level IT Strategy Committee (a) Minimum of three directors as members (b) The Chairperson of the ITSC shall be an independent director and have substantial IT expertise in managing/ guiding information technology initiatives (c) Members are technically competent (d) CISO and Head of IT to be permanent invitee

Chairperson of the Committee is required to be an ID.

The Composition of the Committee shall be as follows: The MD/ CEO as chairperson; and Two independent directors or non-executive directors or equivalent officials serving as members.

Where the NBFC has not appointed IDs, NEDs or equivalent officials to serve as members of the Committee.

Divergent Market Practices

With respect to appointment of IDs on the Board and induction in the Committees, two interpretations are seen in practice in the case of private companies and WOS:

First, since the Companies Act does not mandate the appointment of independent directors in the case of private companies and explicitly exempts WOS, private NBFCs and WOS often rely on these statutory exemptions. The SBR Master Directions make a general reference to the Companies Act without distinguishing between company categories, which further supports the view that these entities constitute the relevant committees without appointing independent directors.

Second, given that NBFCs in the middle layer or above have crossed the ₹1,000 crore asset threshold and fall under enhanced regulatory scrutiny, some take the view that such entities should align with the intended governance standards and appoint independent directors, even if not required under the Companies Act.

Closing thoughts

The SBR Framework takes into account the systemic concerns associated with different NBFCs and thus classifies them into different layers. The corporate governance norms are applicable to ML, UL and TL NBFCs, which, given their asset sizes, are expected to operate at huge volumes and carry a great magnitude of risks. Such NBFCs may have access to public funds (by way of bank borrowings, debenture issuance etc.), wherein large lenders or public would have exposures and consequent high systemic risks. Hence, looking at the constitution (that is whether the NBFC is a private limited or public limited) becomes less important, and looking at the size, activity and function becomes more important.

Thus, it may not be right to conclude that NBFCs registered as private companies and WOS can do away with the mandatory composition prescriptions merely due to the constitutional form of their entity. Looking at the intent and idea of SBR Framework, the applicable NBFCs may be required to appoint independent directors irrespective of the form of their constitution. The scale-based regulation emanates from the idea that NBFCs having high risk should be effectively monitored. Thus, the regulations should be followed in spirit to effectively mitigate the risks arising in the course of the NBFC’s functioning.

[1] Pursuant to the provisions of section 149(4) of the Companies Act read with rule 4 of the Companies (Appointment and Qualifications of Directors) Rules, 2014, following companies are mandatorily required to appoint independent directions: listed companies, public companies having paid up share capital of ten crore rupees or more; or turnover of one hundred crore rupees or more; or having in aggregate, outstanding loans, debentures and deposits, exceeding fifty crore rupees as per the latest audited financial statements.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-07-16 17:16:422025-07-16 17:36:56Paradox of privacy

In our previous article, we discussed the expectations of the regulator along with a probable approach for NBFCs towards ICAAP. Notably, while ICAAP is applicable to banks as well as NBFCs (middle and upper layer), our present write-up focuses on ICAAP in the context of NBFCs. The inclusion of ICAAP for NBFCs marks a significant shift, from a one-size-fits-all capital adequacy regime, towards a more tailored, risk-sensitive approach that reflects the unique risk profile of each NBFC.

While RBI has not mandated a rigid format or methodology for ICAAP, it has emphasised the need for internal capital assessments that are proportional to the nature, scale, and complexity of operations. The challenge, however, lies in the absence of detailed guidance or templates. Unlike banks that have had years to mature their ICAAP practices, most NBFCs are at the beginning of this journey.

This article attempts to fill that gap. As a sequel to our previous overview, it delves further into how different elements & each category of risk—credit, market, operational, liquidity, concentration, and others—should be considered for ICAAP.

It may be noted that while the RBI has not issued specific guidelines for NBFCs to undertake ICAAP, they are instructed to be guided by the Master Circular – Basel III Capital Regulations to the extent applicable.

Need of ICAAP for NBFCs

The goal of ICAAP is not merely compliance, it is an internal assessment to ensure that the capital maintained by the NBFC is adequate, not just by regulation, but by the realities of its risk environment.

The risk weights prescribed for computing the minimum capital adequacy are based on the general experience of the regulators with respect to the respective asset classes. However, risks associated with the assets also depend on the credit underwriting qualities of the originator, the geography in which it operates, concentricity, borrower composition, nature of underlying collateral, etc. As a result, regulatory risk weights may not always reflect the true risk. This is where ICAAP comes in.

ICAAP helps NBFCs assess whether they hold enough capital based on their specific risk profile, going beyond the regulatory minimum. This self-assessment often goes beyond the basic rules. For example, an NBFC might consider capital required for additional risks, such as market risk, reputational risk, operational risk, etc, even though these aren’t always covered by the minimum capital requirements set by regulators. It might also use its own methods to evaluate more common risks like credit, market, or operational risks.

Apart from these risks, there are several other factors that are often overlooked but are essential to consider under ICAAP. These include off-balance sheet exposures, the NBFC’s future strategic plans, its compensation practices, etc.

NBFCs approach to ICAAP

An NBFC should not treat ICAAP as a mere compilation of regulatory templates such as capital adequacy, liquidity, or other prescribed formats. Doing so would reduce ICAAP to a regulatory compliance exercise, rather than a genuine internal assessment of how capital relates to the NBFC’s inherent risks.

In addition to serving as an assessment of capital adequacy, ICAAP also functions as a key decision making tool for the management. For instance, it helps evaluate whether the company’s existing capital levels are sufficient to support proposed business plans, assess the potential adverse impact of riskier asset classes on business continuity, and determine if planned growth would require capital infusion alongside debt raising. It also allows the company to assess whether its current trajectory is sustainable. In this manner, ICAAP effectively serves as a business continuity check for NBFCs.

Considering the above, the framework of ICAAP should be robust enough to assist management sufficiently. Accordingly, we discuss key elements of ICAAP in the subsequent section.

Key Elements under ICAAP

ICAAP consists of various elements. The detailed discussion on each element is discussed in subsequent sections. The various elements under ICAAP are as follows:

Listing and Assessment of Key Risk

The most critical element of ICAAP is the assessment of risks faced by the NBFC. It is important to note that there are two possible approaches: one, to consider only material risks, and the other, to consider all risks faced by the NBFC. The former approach is for NBFCs with simpler operations, while the latter is more appropriate for NBFCs with moderately complex operations, based on the management’s assessment.

Based on this assessment, a comprehensive list of risks should be identified and categorised as follows:

Quantitative Risks: Risks that can be measured and quantified reliably should be assessed using the best available data, tools, and methodologies. The methods employed will naturally differ across NBFCs, depending on their risk profile, operational scope, and internal systems. NBFCs are exposed to various types of risks, including credit risk, market risk, operational risk, interest rate risk, credit concentration risk, etc.

Qualitative Risks: While the aforementioned risks can be quantified, there are certain other risks which cannot be quantified such as reputational risk and business or strategic risk, and may be equally important for an entity and, in such cases, should be given same consideration as the more formally defined risk types. For example, an entity may be engaged in businesses for which periodic fluctuations in activity levels, combined with relatively high fixed costs, have the potential to create unanticipated losses that must be supported by adequate capital. Additionally, an entity might be involved in strategic activities (such as expanding business lines or engaging in acquisitions) that introduce significant elements of risk and for which additional capital would be appropriate.

Other key elements under ICAAP

Off-Balance Sheet Items: Off-balance sheet items represent potential obligations that do not appear directly on the institution’s balance sheet but can lead to substantial future liabilities. Examples include loan commitments, letters of credit, derivatives, securitizations, and guarantees.

While these exposures may not currently affect a firm’s capital or liquidity metrics, they carry contingent risks that can materialize under stress conditions. If not adequately monitored and incorporated into risk assessments, off balance sheet items may result in underestimated capital needs, particularly under adverse scenarios.

ICAAP Implications:

Institutions must employ robust risk identification frameworks to capture the nature, size, and likelihood of off-balance sheet exposures becoming on-balance sheet liabilities.

Stress testing should simulate adverse market or credit conditions to evaluate how these contingencies might impact capital adequacy.

Capital buffers should be calibrated to reflect not just current exposure, but also potential future liabilities from these items under both baseline and stressed conditions.

Compensation Practices: Compensation structures have a direct influence on employee behavior and, by extension, the institution’s risk culture. When short-term incentives are misaligned with long-term stability goals, they may encourage excessive risk-taking, leading to undesirable financial outcomes and reputational damage.

ICAAP Implications:

The capital adequacy framework must consider how incentive structures align with the institution’s risk appetite. Compensation policies should be reviewed to ensure they do not drive behaviors that conflict with prudent risk management.

NBFCs should establish compensation deferral mechanisms (e.g., clawbacks, performance-based vesting) and ensure these are factored into risk planning to reinforce sound decision-making.

Future Strategic Plans: Strategic initiatives such as geographic expansion, launching new products, or entering new markets often involve heightened or novel risks. These initiatives may expose the institution to unfamiliar regulatory environments, new credit or operational risks, or increased competition.

ICAAP Implications:

Future business plans must be embedded into capital planning and risk modeling. This includes estimating the impact of new initiatives on capital demand, funding needs, and operational capacity.

Scenario analysis should test how strategic changes could affect capital ratios under both expected and stressed conditions, especially when entering volatile or unfamiliar sectors.

Management must ensure that adequate risk mitigation strategies are in place, and that the institution holds sufficient capital to support growth without compromising its resilience.

Stress Testing: As part of the ICAAP, NBFCs must, at a minimum, conduct periodic stress tests, with a focus on material risk exposures. These tests are designed to assess the institution’s vulnerability to unlikely but plausible adverse events or significant changes in market conditions that could negatively impact its financial position. By implementing a structured stress testing framework, management gains a deeper understanding of the entity’s potential exposures under extreme but realistic scenarios—thereby improving preparedness and resilience. But what exactly is stress in this context? In ICAAP, stress refers to adverse deviations from the base case or normal operating conditions. It could be in the form of macroeconomic shocks, sector-specific downturns, or internal events—such as operational breakdowns or large-scale defaults. The purpose of stress testing is not to predict the future but to examine what could happen if things go wrong.

There is no fixed threshold for the severity of stress scenarios. However, the scenarios should be severe enough to test the NBFC’s capital and liquidity buffers, yet plausible enough to remain relevant. For example:

Interest rate shock of +250 basis points

30% increase in delinquency rates

Sudden collapse in collateral valueNBFCs should ideally run multiple stress levels—mild, moderate, and severe—to observe performance across a range of conditions.

Adverse regulatory action halts lending in a key segment.

Widespread borrower fraud in a key region.

Natural disaster (e.g., flood or earthquake) affecting multiple branches, etc

Quantitative Risks

Credit Concentration Risk

Credit concentration risk arises when a financial institution’s exposures are not well-diversified—either across counterparties, sectors, geographies, asset classes, or even business models. In simple terms, it is the risk of putting too many eggs in one basket. Risk concentrations are arguably the single most important cause of major problems in entities. Credit risk concentrations, by their nature, are based on common or correlated risk factors, which, in times of stress, have an adverse effect on the creditworthiness of each of the individual counterparties making up the concentration. The credit concentration risk calculations shall be performed at the counterparty level (i.e., large exposures), at the portfolio level (i.e., sectoral and geographical concentrations) and at the asset class level (i.e., liability and assets concentrations). There could be several approaches to the measurement of credit concentration in the entity’s portfolio. One of the approaches commonly used for the purpose involves the computation of Herfindahl-Hirschman Index (HHI). Under the HHI approach, an entity first decides what level of portfolio diversification it considers to be ideal—this is called the target HHI. The HHI for the actual credit portfolio is then calculated and compared with the target HHI. If the actual HHI is higher than the target, it indicates that the portfolio is more concentrated (i.e., riskier) than desired.

To compensate for this additional concentration risk, the NBFC needs to hold extra capital. The amount of additional capital is determined by using a multiplier. This multiplier increases in proportion to how far the actual HHI exceeds the target. The multiplier is the interpolated value of Loss given Default at the current HHI level where the minimum LGD is at the target HHI level and the maximum LGD occurs at the highest possible HHI level i.e. 1. Essentially, the more concentrated the portfolio is, the higher the capital buffer required.

Stress Testing: Stress scenarios for concentration risk can involve:

Counterparty default stress, where the largest or top 20 borrowers default simultaneously.

Sectoral collapse, where an entire sector (e.g., real estate or microfinance) underperforms.

Geographic shocks, like drought or political disruption in a key operating region.

The stress scenarios would result in higher Loss Given Defaults and consequently higher capital requirements for stress scenarios.

Credit Risk

Credit Risk is the most important component of capital required for lending institutions. Despite implementing the most rigorous credit underwriting processes, it is impossible to completely eliminate the possibility of credit defaults. This is because certain factors can evolve over time, potentially leading to heightened strain within the portfolio. Companies use Expected Credit Loss (ECL) models to estimate credit risk. However, it’s important to understand that ECL models are designed to capture only the ‘expected’ portion of credit losses—those that are likely to occur based on current conditions and historical data. Hence, entities should also consider using additional models or approaches to estimate the capital required to cover unexpected losses—those rare, extreme events that could have a significant financial impact but are not captured by ECL models. NBFCs may apply stress scenarios to the probability of default and loss given default parameters in their Expected Credit Loss models, beyond what is assumed in the base case, in order to capture potential unexpected losses.

Stress Testing: To stress credit risk, NBFCs can alter the assumptions used in their ECL models or conduct additional simulations to capture unexpected losses. Examples include:

Increasing default rates by 50% to 100% over historical averages.

Reducing recovery rates by 20% to simulate distressed recoveries.

Assuming sector-specific shocks, such as stress in MSME lending or rural portfolios.

Market Risk

An entity should be capable of identifying risks arising from trading activities due to movements in market prices. This assessment should take into account factors such as instrument illiquidity, concentrated exposures, one-way market conditions, non-linear or deep out-of-the-money positions, and the likelihood of substantial changes in correlations. Stress testing exercises incorporating extreme events and market shocks should be specifically designed to highlight key vulnerabilities within the portfolio in relation to relevant market developments.

Stress Testing: For market risk, NBFCs should simulate movements in interest rates, exchange rates, and asset prices. Examples of stress scenarios include:

A 250–300 bps rise in interest rates, increasing cost of funds and decreasing bond portfolio values.

Drop in collateral prices (e.g., gold or real estate) by 20%–30%.

Liquidity contraction in trading instruments, rendering assets difficult to exit.

The idea is to identify exposures where market volatility could result in valuation losses or income shocks.

Operational Risk

An entity should be equipped to evaluate potential risks arising from deficiencies or failures in internal processes, personnel, and systems, as well as from external events. This assessment should also consider the impact of extreme events and shocks associated with operational risk. Such events may include a sudden surge in process failures across multiple business units or a major breakdown in internal controls. As a general practice, companies often use the Business Indicator Component Model for computing the capital requirement for operational risk. In this model, the risk is computed by multiplying the average income of the entity with a prescribed factor.

Stress Testing: Stressing operational risk requires assumptions about adverse internal or external events. For instance:

Simulating a cyberattack that shuts down core systems for 5–10 days.

Widespread process failures during a system migration or staff shortage.

Vendor risk, where a critical third-party service fails.

Qualitative Risks

Compliance Risk

NBFCs in India operate within a highly regulated environment. NBFCs usually are regulated by multiple regulators, and non-compliance with applicable norms would not only result in imposition of penalties/fines but in few cases may even threaten the continuity of operations of the business. Compliance risk may further act as a trigger factor for other risks faced by the Company, as non-compliance may threaten reputation, operations, profitability as well as other aspects of the Company’s operations. Accordingly, compliance risk is considered as a significant risk for the NBFCs. For ICAAP purposes, entities may begin by identifying the sources of risk and evaluating the internal controls and mitigation measures already in place. Based on this assessment, they can then determine the residual risk—the portion of risk that remains unaddressed—and accordingly estimate the capital required to cover it.

IT Risk

In the current business environment, almost all the businesses, including that of the NBFCs, are assisted by information technology infrastructure, while these assets assist entities in streamlining its processes and reducing risk due to human errors it also poses a significant risk, due to possibility of malfunctioning and downtime.

Off-balance sheet items

An entity may have various contingent liabilities and on occurrence of certain events if these liabilities were to materialize, they could lead to expenses / losses for the entity.

Hence, despite the uncertainty surrounding these arrangements, it is essential that the entity maintains sufficient capital considering the likelihood of happening of these events.

Compensation practices

An effective compensation framework plays a critical role in aligning employee behaviour with the long-term objectives of the organization to manage human resource risk. It shall be ensured that the compensation policy does not inadvertently prioritize short-term gains for senior management over the long-term interests of the organization. These measures are designed to prevent compensation practices that may incentivize excessive risk-taking or compromise the Company’s long-term goals in pursuit of short-term performance.

To strike the right balance between performance incentives and long-term business objectives, the entity shall maintain an appropriate mix of variable and fixed pay for its employees. This approach aims to encourage improved performance while safeguarding the Company’s overall long-term interests.

These practices fosters a culture of responsible decision-making and ensures that the employees are motivated to achieve sustainable success and growth, aligning individual performance with the broader objectives of the organization.

Future projections

In ICAAP, making future projections is important to check if the institution will have enough capital to stay strong in the coming years, even if things go wrong. These projections usually cover the next 3 to 5 years and include key numbers like expected CRAR (capital to risk-weighted assets ratio), future income, asset growth, and risk levels. The CRAR should be estimated by looking at how much capital the institution will earn and keep, how much new capital it might raise, and how much its risk-weighted assets are likely to grow. Income should be projected based on how much the institution expects to earn from interest, fees, and other sources, while also considering possible loan losses and other costs. The growth in assets should reflect the business plans and also think about where and to whom loans will be given. Based on this, the risk-weighted assets should also be estimated to understand how risky the future asset base might be.

Conclusion

ICAAP represents more than just a regulatory formality—it is a critical framework for NBFCs to understand and manage their unique risk landscape. By systematically identifying, assessing, and planning for both quantifiable and unquantifiable risks, and by applying stress testing to challenge their assumptions, NBFCs can ensure they are adequately capitalised for both expected and unexpected events. A well-executed ICAAP also considers various “blind spots” which often gets overlooked which includes off balance sheet items, compensation practices, future projections, etc. ICAAP not only strengthens financial resilience but also fosters a risk-aware culture, enabling NBFCs to navigate uncertainty with greater confidence and strategic clarity.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-07-12 08:57:252025-07-16 10:50:20Mind the Gap: Plugging Risk Blind Spots with ICAAP for NBFCs

On June 09, 2025, the Tamil Nadu Money Lending Entities (Prevention of Coercive Actions) Act, 2025 was notified (hereafter referred to as ‘Act’). The Act aims to protect vulnerable groups from the coercive recovery practices perpetrated by microfinance institutions, money-lending agencies, and organisations operating in the state of Tamil Nadu. Violations of the Act are subject to penalties, including imprisonment and fines.

While the Act is not generally applicable to RBI-regulated entities, certain provisions on coercive recovery practices (Sections 20 – 26), are made applicable upon NBFCs functioning in Tamil Nadu. The term “functioning” is quite broad, and would appear to include in its ambit entities with branches, and also those conducting business in the state.

Non-compliance with these provisions can also result in the concerned persons of the NBFCs being punished with imprisonment and fines.

What is curious, however, is the differentiation made between banks and NBFCs. The said provisions are not made applicable to banks, but apply to NBFCs. This is notwithstanding the fact that NBFC recovery practices are just as heavily regulated by the RBI, as those of banks, and borrowers already have recourse available to them through the RBI ombudsman, and consumer protection courts.

Indeed, such recourse may be more speedy, and efficacious (as those bodies specialise in such matters), as compared to the police machinery and criminal procedure (which are already burdened with backlogs and heavy case-load). The provisions are also quite subjective and ambiguous in their interpretation (as will be outlined below), and there is certainly a risk that this will result in a slew of complaints by delinquent borrowers, which will serve to stall recoveries further.

Hence, one is at the outset unable to trace the rational nexus behind the differential classification/treatment (between the banks and NBFCs), and the object sought to be achieved[1].

Unpacking the applicable provisions

NBFCs functioning in the state of Tamil Nadu would need to ensure that “no borrower or any of his family members shall be subject to coercive recovery action by a money lending agent, or its agents while recovering a loan from the borrower”. It is to be noted that “coercive recovery action” is nowhere defined in the Act. Section 3(a) states that “coercive actions” are as understood under Section 20, and Section 20 gives only an indicative list of what such coercive actions may be.

Hence, what is “coercion” is only understood by inference, however reference may also be made to the definition of coercion under Section 15 of The Indian Contract Act, 1872, where coercion is the “the committing, or threatening to commit, any act forbidden by the Indian Penal Code (45 of 1860) or the unlawful detaining, or threatening to detain, any property, to the prejudice of any person whatever, with the intention of causing any person to enter into an agreement. “

Under Section 20(2) of the Act, the following may be flagged as coercive, and hence, NBFCS would need to take note of the same:

Coercive actions under Section 20(2) of the Act

Provision: Obstructing/using violence to, or insulting, or intimidating the borrower or any of his family members Punishment for contravention: Imprisonment for a term which may extend to three years / fine of five-lakhs / or both.

Provision: Persistently following the borrower or any of his family members from place to place, or interfering with any property owned or used by them, or depriving them of or hindering them in the use of, any such property Punishment for contravention: Imprisonment for a term which may extend to three years / fine of five-lakhs / or both. Our comments: Sticky borrowers may be reluctant to repay unless persistently followed up with, particularly when the borrowers themselves are moving “from place to place” to avoid repaying amounts due. However what seems to be prohibited here is “stalking” the borrower, and obstructing their daily activities. As regards hindering the borrower in the use of “any property”, in our view, the property here should not be understood to mean the collateral provided by the borrower, or the primary security created out of the disbursed funds. Such an interpretation would cast a chilling effect on the basic assurances available to lenders in secured lending.

Provision: Frequenting the house or other place where the borrower resides or works, or carries on business, or happens to be, with an intention of taking coercive action Punishment for contravention: Imprisonment for a term which may extend to three years / fine of five-lakhs / or both. Our comments: Frequenting the borrower’s house or workplace may be inevitable in cases of high DPDs, and persistent defaults. However, whether or not there was an “intention of taking coercive action” is an entirely fact-sensitive matter, which would require analysis by the courts. Such subjectivity may become an avenue for frivolous complaints by defaulting borrowers.

Provision: Using the service of private or outsourced or external agencies, to negotiate or urging the borrower to make payment using coercive and undue influence; Punishment for contravention: Imprisonment for a term which may extend to five years / fine of five-lakhs / or both. Our comments: What appears to be restricted here is not the mere use of business correspondents or outsourced agents for recovery, but rather using them as an instrumentality for the coercive recovery. Essentially, even if the coercive recovery is not directly done by the lenders themselves they will still be held accountable for the same.

Provision: Seeking to take forcibly any document of the borrower which entitles him to a benefit under any Government programme, any other vital documents, articles or household belongings Punishment for contravention: Imprisonment for a term which may extend to five years / fine of five-lakhs / or both. Our comments: Refer to comments under Row 2, specifically with regards to collateral property and security.

Who would be punished?

In case of NBFCs, the punishment may be imposed on the following persons (See Section 26 of the Act):

Every person who, at the time of the offence being committed, was in charge of and responsible for the business of the Company. Provided that, such persons shall not be liable to punishment if: (i) they prove the offence was committed without their knowledge; and (ii) all due diligence was exercised to prevent the commission of the offence.

In addition to the above, the director, manager, secretary, or other officer, due to whose consent/connivance/neglect/ the offence had been committed, shall also be liable to be proceeded against and punished accordingly.

Should it apply to RBI regulated entities?

Notwithstanding the noble sentiments around protecting borrowers from Shylockian lending, the question here is, can/should such a state money-lending enactment also apply to RBI-regulated entities? Especially considering that there are already exhaustive regulations around the recovery practices (including for MFIs, the concerns around which the Act purports to address).

The Apex Court had ruled on this in Nedumpilli Finance Company Ltd. v. State of Kerala. Here, the Court held that because the RBI Act and control over NBFCs are traceable to entries under List I of the Seventh Schedule of the Constitution, Article 246(1) of the Constitution would come into play. This grants parliament exclusive law-making power over the said entries. Further, Section 45Q of the RBI Act provides an overriding effect to Chapter III of the RBI Act and regulations made thereunder (which are of a statutory nature).

Hence, it is understood that such state money lending enactments cannot apply to NBFCs. For interested readers, we have written on this judgment here, and have also covered the constitutional analysis from an earlier judgment by the Gujarat HC, here.

In the final analysis, the RBI (already) regulates NBFCs from “cradle to grave”. As observed by the Hon’ble Supreme Court, unlike state enactments, which have a one-eyed approach of borrower protection, the RBI Act takes a holistic approach to lending business. And, “all activities of NBFCs automatically come under the scanner of the RBI. As a consequence, the single aspect of taking care of the interest of the borrowers, which is sought to be achieved by the State enactments, gets subsumed in the provisions of Chapter IIIB”.

[1] Referring to the doctrine of reasonable classification under Article 14 of the Constitution.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-28 11:01:432025-06-30 14:58:26New Tamil Nadu Law on Coercive Recovery - Alarm bells for NBFCs?

Probably the first in India, green securitisation has finally found an entry with the recent issuance of pass-through certificates backed by residential rooftop solar loan receivables in India. The loans were originated by a ‘green-only’ NBFC focussed on climate-positive lending. The present issuance is in the form of green collateral securitisation – since the securitised receivables qualify as ‘green’. Further, given the activities of the originator, it seems that the same may qualify to be a green capital securitisation, with the freed capital of the originator being utilised towards creation of green assets.

Notably, as per a recent publication of Climate Policy Initiative, the Global Landscape of Climate Finance 2025, India has been ranked as the leading country in the South Asia region in terms of mobilisation of climate finance (as per the data for 2023). Green securitisation may act as a catalyst to the growth of green finance in India. See a whitepaper on the same here.

A broader concept in the context of climate finance is sustainable securitisation, our whitepaper on the same can be accessed here. The recent guidelines of SEBI also permits the issuance and listing of sustainable securitised debt instruments, based on the recommendations of the Working Group constituted for the review of SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, chaired by Mr. Vinod Kothari. An article on the concept of sustainable SDIs may be accessed here.

The evolution of Electronic Trading Platform (‘ETPs’) is rooted in the market’s need for speed, efficiency, and enhanced transparency in dissemination of trade information. Traditional floor based trading methods struggled with sluggish processes, limited data dissemination, and inefficiencies that couldn’t pace with a global financial landscape. In response, industry players and regulators recognised the need for a digital overhaul, a system that could streamline trade execution, provide real-time market data, and foster a more accurate price discovery mechanism. This led to the emergence of specialised platforms, such as those designed for government securities trading, where primary dealers are entrusted with membership and operations. One such platform is ETP.

An ETP is a computarised system that facilitates the buying, selling and management of a wide range of financial instruments (listed down below). These platforms enable real-time market data dissemination, order execution, and efficient trade processing. For instance, in India, platforms such as the NDS-OM (Negotiated Dealing System – Order Matching) are well-known examples that specialize in government securities (g-sec) trading. Other entities include various bank-operated ETPs such as BARX operated by Barclays Investment Bank (international) and proprietary systems developed by financial institutions such as 360TGTX operated by Three Sixty Trading Networks (India) Pvt. Ltd.

Entities operating ETPs facilitating transactions in eligible instruments,under the New ETP Directions,

Grandfathering clause:

Any entity already authorised under the Erstwhile ETP Directions shall deemed to have been authorised under the New ETP Directions, or

any action already taken under the Erstwhile ETP Directions “shall be deemed to have been taken” under the New ETP Directions.

In practical terms, operators need not re-submit applications, seek fresh authorisations or revisit past actions as long as compliant under the Erstwhile ETP Directions.

Effective Date:

Effective immediately i.e. from June 16, 2025.

All about Electronic Trading Platforms (‘ETPs’)

Before going ahead to analyse the changes let us understand what ETPs are. ETPs are electronic systems, other than recognised stock exchanges, on which transactions in eligible instruments are contracted. But why would someone prefer trading on ETP rather than other exchanges/ platforms such as stock exchanges? ETPs offer eligible entities multi-instrument trading platforms (dealing with money-market, G-Secs, FX, swaps etc.) with tailored tenures and faster settlement process while stock exchanges cater to listed equities and futures with standardised contracts, retail participation and fixed trading hours.

Who operates these electronic systems?

Any entity as defined in the New ETP Directions incorporated in the form of a company and authorised by the RBI in this regard can operate an ETP. Currently, there are 12 authorised ETP operators under the Erstwhile ETP Directions who shall continue to operate under the New ETP Directions.

Types of ETP: Single Dealer Platform v. Multi-Dealer Platform

Basis

Single Dealer Platform

Multi-Dealer Platform

Seller

A single bank or financial institution

Several banks and financial institutions

Pricing

Tailored pricing from one provider.

Competitive pricing with options from several liquidity providers.

Liquidity

Low

High

Liquidity source

Provided by a single bank or institution.

Aggregated liquidity from multiple banks/institutions.

Customisation

Tailored interfaces and services designed for specific clients.

More standardized interfaces across multiple dealers; less tailored.

Execution quality

Stable and consistent execution within one controlled environment

Best execution can be sought across multiple quotes and providers

Suitability

Clients who value a close banking relationship and prefer a dedicated, controlled trading environment

Clients who want to compare and execute trades across a range of prices and liquidity providers

Example

NDS-OM, operated by Clearcorp Dealing Systems (India) Ltd., provides a secondary market platform for government securities owned by RBI

360TGTX, operated by Three Sixty Trading Networks (India) Pvt. Ltd., provides a platform for trading in FX Spot, Forwards, Swaps and Options

Players on ETP

Primary Dealers- In 1995, the RBI introduced the system of PDs in the Government Securities (G-Sec) Market. The objectives of the PD system are to strengthen the infrastructure in G-Sec market, development of underwriting and market making capabilities for G-Sec, improve secondary market trading system and to make PDs an effective conduit for open market operations (OMO).

The RBI currently extends various facilities to the PDs to enable them to fulfill their obligations, including memberships of electronic dealing, trading and settlement systems (NDS platforms/INFINET/RTGS/CCIL).

PDs are classified as below:

Standalone Primary Dealers- NBFC-ML

Bank Primary Dealers- Scheduled Commercial Banks and Central Banks- National and International

Basis

Standalone Primary Dealer

Bank Primary Dealers

Entity Structure

Operate as independent legal entities, often registered as NBFCs or as dedicated subsidiaries/joint ventures.

Operate as a departmental function within a scheduled commercial bank (or its branch, including foreign banks).

Regulatory Framework

RBI guidelines

RBI Guidelines and bank specific norms

Business focus

Primarily focused on government securities trading and related activities, often with more flexibility to diversify (e.g., underwriting, trading derivatives).

The primary dealer function is one element of a larger suite of banking services and is more integrated with the bank’s overall operations.

Operational Independence

Greater operational autonomy, being solely focused on the government securities market

Functions as an integral part of the bank’s operations, with decisions influenced by the broader business strategy of the bank

PDs registered with RBI

SBI DFHI Limited

Bank of Baroda, Bank of America

Traders

Analysis of Change

Having understood the nomenclature, we may proceed to analyse the changes and what they mean for Regulated Entities. The primary change and intent of the Draft Directions was to curb unregulated entities and platforms, specifically offshore platforms dealing with foreign exchange trading involving inshore/ domestic investors. Please note that foreign exchange instruments have been a part of eligible instruments, however, due to not being defined, the question whether such offshore ETPs would be covered, was always a question. The Draft Directions recommended certain changes, however, the major change was bringing offshore ETPs under the domain of RBI. However, the finalised New ETP Directions do not deal with this aspect.

While the RBI largely accepted the foundational architecture proposed in the draft, it has revised certain provisions to provide clarity in many areas, especially around risk and operational aspects which are now expressed in more precise terms along with addition of new provisions around enforcement and transitional mechanisms.

Highlights of Major Changes:

Expanded applicability to include outsourcing entities under the purview of the New ETP Directions in essence

Carve out to single dealer banks and Standalone Primary Dealer (‘SPD’)

Transition to an electronic application process: Moving away from physical submission, the application process is now streamlined through the PRAVAAH portal

Quarterly and annual reporting requirements for the operators introduced mandating regular updates thereby tightening regulatory oversight

Framework for data preservation and sharing post-authorisation

Comparison at a Glance:

Area

Erstwhile ETP Directions

New ETP Directions

Implications

Application process for authorisation

Physical submission

Through PRAVAAH Portal of RBI

Streamlining the process, enhancing accessibility, efficiency, and real-time tracking for applicants as well as regulators

Quarterly reporting

No such requirement

Quarterly reporting on functioning of ETPs by Operators (details covered below)

Operators to provide periodic updates on operational performance, ensuring regulatory oversight

Annual Reporting

No such requirement

Annual reporting on compliance of the New ETP Directions and terms and conditions prescribed (details covered below)

Operators to yearly confirm their adherence to updated regulatory guidelines and contractual conditions

Eligibility Criteria

Did not apply to ETPs operated by SCBs

Apply to all the entities including SCBs operated ETPs (except exemption covered below)

Banks must now play by the same rulebook as other operators, additionally Public Sector Banks shall have to incorporate (or spin off) a Companies Act vehicle, infuse requisite capital and adhere to technological standards. Until now, Public Sector Banks that operate an ETP slipped neatly around the RBI’s “company‐only” eligibility gate. The New ETP Direction takes away that privilege. From the day the change takes effect, every ETP, bank-owned or not must meet the same bar

Preservation, access and use of data

Did not have a provision for treatment of data in the event of cancellation of authorisation

Specifies the requirement to share data, along with form and manner, with the RBI or any agency in the event of cancellation of authorisation as may be called upon by the RBI or any other agency.

Enhanced regulatory oversight and post-termination accountability on operators

Definition of ‘Entity’

“….an agency formed as a ‘company’ and incorporated under the Companies Act, 2013 (or earlier acts)”

“….any person, natural or legal.”

Language of the New ETP Directions seems to widen the scope of entity, however reading the impact along with para 6(f)(iii), it only brings the outsourcing entities under the widened scope

Grandfathering Rule

Not needed (first issue)

All licenses/actions under Erstwhile ETP Directions shall be treated as valid

No fresh registration required

Exemption

ETPs operated by banks for their customer on a bilateral basis as long as no market is being created for the securities

Carve out to SCBs (including branches of Foreign Banks operating in India) and SPDs wherein the bank or the SPD operating the electronic system is the sole quote/price provider and a party to all transactions contracted on the system.

Banks and SPDs can operate proprietary trading platforms without the full weight of the standard compliance requirements set for multi-dealer platforms. This can streamline their internal processes and reduce regulatory and technological burdens.Acting as the sole quote provider makes these institutions both the operator and counterparty. This can improve execution speed and reduce inter-dealer friction.A single market maker model may lead to faster execution but can constrain competitive pricing, potentially resulting in wider spreads if the operator does not face rival pricing pressures from other dealers.While banks and SPDs gain efficiency due to lesser compliances, they must remain vigilant about disclosure and transparency requirements to avoid any adverse effects on market integrity.Banks and SPDs may develop more tailored platforms, exclusive systems to capture niche market segments.Synchronization with global norms that treat single-dealer platforms as an extension of the dealer’s book and not that of an exchange.

Reporting Requirements:

These new requirements shall have to be complied with along with the existing reporting requirements under the Erswhile ETP Directions from the effective date of the New ETP Directions. Accordingly, the first quarterly report shall be required to be submitted on or before 15th July, 2025 and the annual report shall be submitted on or before 30th April, 2026. The manner of reporting by ETP operators as per the New ETP Directions has been listed below:

Reporting Requirement

Reporting Authority

Frequency

Format

Timeline

New

Functioning of the platform, including but not limited to the following points:Events resulting in disruption of activities, during the quarter, if anyInstances of market abuse, during the quarter, if anyDetails about any material change in trading procedure or technology carried out during the quarter

On or before 15th day of the month following the quarter

Compliance with the New ETP Directions and terms and conditions prescribed at the time of authorisation

RBI

Annually

Not specified

on or before the 30th of April of the succeeding financial year

Data relating to activities on the ETP

RBI

Post cancellation of authorisation

As may be prescribed

As may be prescribed

Existing

Transaction information

Trade repository or trading platform

As may be prescribed

As may be prescribed

As may be prescribed

Other report, data and/or information as required by RBI

RBI

As may be prescribed

As may be prescribed

As may be prescribed

Data/information

Any agency as required by Indian Laws

Not specified

Not specified

Not specified

Event resulting in disruption of activities or market abuse

RBI

Event-based

Not specified

Not specified

Conclusion:

By introducing defined protocols for risk management, data governance and reporting, the updated framework seeks to close existing regulatory gaps. Key provisions of the New ETP Directions include, amongst others, a clear exemption for single–dealer platforms and a streamlined application process via the PRAVAAH portal. These measures ensure legal continuity. Ultimately, this transformative framework not only reinforces the integrity of the trading ecosystem but also cultivates an environment conducive to innovation.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-23 19:18:342025-06-23 19:33:47Master Direction on ETPs: Key Changes & Compliance Guide

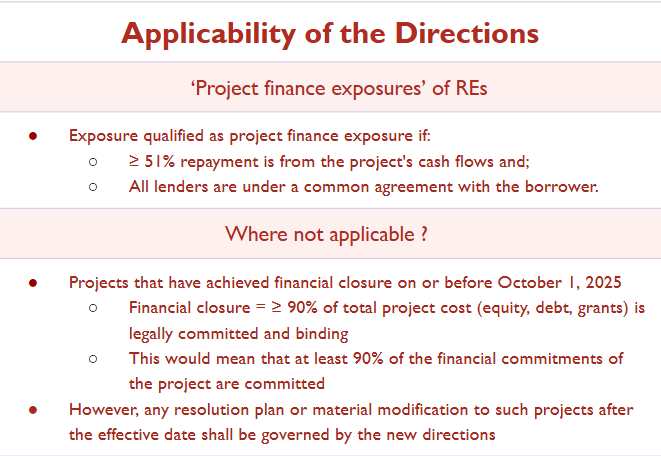

Project loans, used to finance large infrastructure and industrial ventures like highways, power plants and railways etc., are fundamentally different from regular business or personal loans. Unlike typical loans that are repaid from either the borrower’s existing operations and balance sheet (in case of the former) or the borrower’s own credit worthiness (in case of the latter), project loans are forward-looking: they primarily rely on cash flows of the project, generated onlyafterthe project becomes operational. Because of this, delays in project completion due to various factors such as land acquisition issues and regulatory delays which may be beyond the control of the developer are common. These may arise from. Such delays, though being routine and not necessarily indicating borrower’s stress, triggered adverse asset classifications under the existing rules.

When the RBI introduced its 2019 prudential framework to enable early recognition and time bound resolution of stressed assets, it excluded such project loans from its scope (see para 25). As a result, these continued to be governed by old norms, specifically para 4.2.5 of the 2015 IRCAP and later, para 3 of Annex III under the RBI SBR Directions. However, these norms did not reflect the unique risks faced by project finance especially during the construction phase.

To address these issues, the RBI released the Draft Project Finance Directions in May 2024, proposing a dedicated regulatory framework tailored to project loans. The Project Finance Directions(‘Directions’) have been issued on 19 June, 2025. This article explores the need for such a framework, the changes brought in the regulatory regime, and their impact on borrowers and lenders.

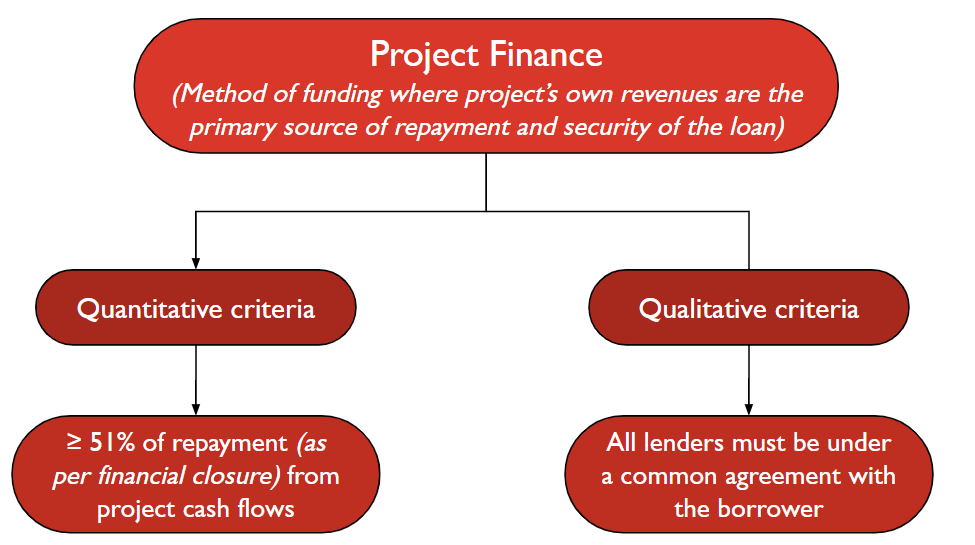

Project finance vs other kinds of finance

In corporate lending, credit decisions are primarily based on the borrower’s balance sheet strength, existing cash flows and overall financial health. where the lender primarily assumes credit risk

In contrast, in project finance, repayments as well as the primary security depend primarily on the successful implementation and projected cash flows of a specific project, rather than the borrower’s overall financial position. Accordingly, the lender takes two different risks:

Project riski.e. the risk that the project may face commencement delays due to factors like regulatory bottlenecks, land acquisition issues or construction delays and;

Credit riski.e. the risk of inadequacy of cashflows to make the scheduled contractual payouts.

Importantly, in project finance, delays in cashflows often happen due to non-credit factors linked to project execution, mainly project delays. As a result, automatic downgrading of classification due to any project delay may not only fail to provide a true risk profile of the loan but also cause increased provisioning burden on the lender.

Overview of the Directions

The Directions deal with the following broad aspects:

Classification of projects and project finance;

Prudential requirements for extending project loans including:

Provisioning requirements;

Conditions for sanction, disbursement and monitoring.

Resolution and restructuring of project loans

Either due to stress;

Extension/ delays in DCCO.

Applicability

Classification of ‘project’ and ‘project finance’

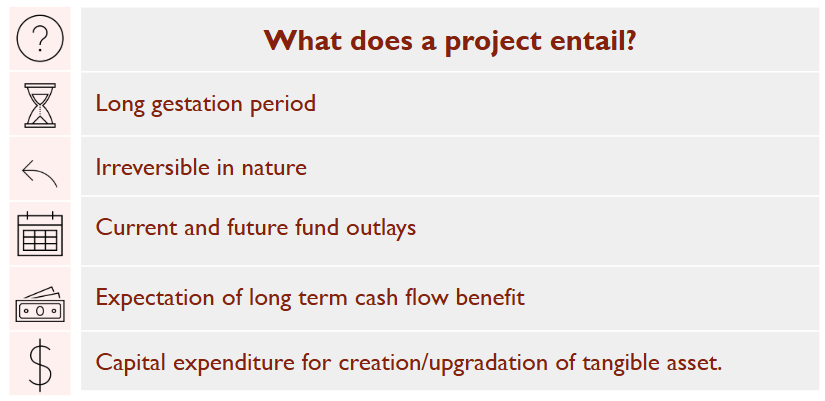

Under the Directions, a project is defined as to involve capital expenditure for the creation, expansion or upgradation of tangible assets or facilities, with the expectation of long-term cash flow benefits [see para 9(l)], with the following features:

Project finance is a method of funding where the project’s cash flows/ revenue own revenues are the primary source of repayment as well as the and security for the loan [see para 9(m)].

It can be:

Greenfield (new project);

Brownfield (existing project enhancement).

To qualify as project finance under the Directions:

Note: Loan terms can differ across lenders if agreed by all parties

The earlier definition of project finance under the SBR Directions was generic and vague, referring merely to a “project loan” as any term loan extended for setting up an economic venture. The Directions have provided more clarity on what would be considered as project finance and have linked it to the definition of project finance under the Basel Framework, while also providing a quantitative threshold of 51%.

Project finance envisages the lender’s exposure in a project, which is typically in the process of being set up. The repayment will be from the project cashflow i.e. the payout structure is connected with the commencement of commercial operations of the project. The lending is based on the projected cash flows of the project rather than the balance sheet of the developer. It is distinct from asset finance, where loans are backed by existing assets generating income. Further, project finance differs from a working capital loan/general corporate purpose loan where the latter is towards financing the working capital needs of the developer entity based on the overall health of the entity.

Would it mean that project loans cannot have any other collateral and must solely rely on the project as the security? The answer is negative since the threshold specified allows to have other/ additional collateral, say, personal guarantee of the developer etc., however, the primary security shall be the project cashflows.

Other important terminology

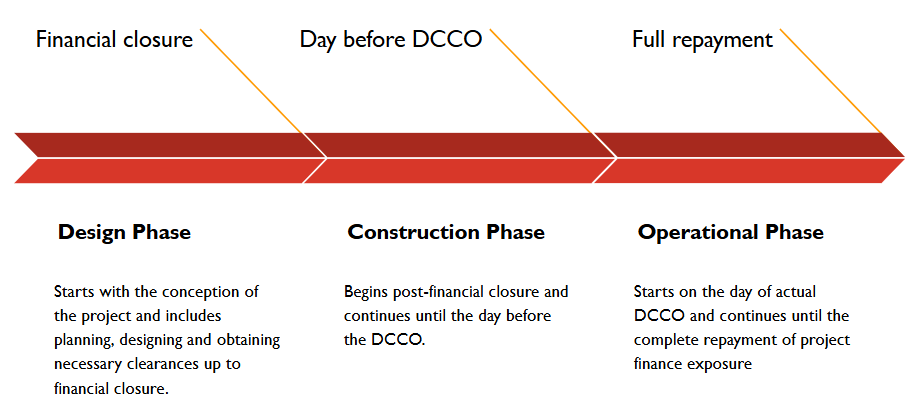

DCCO

The Date of Commencement of Commercial Operations (DCCO) is a key milestone in project finance, marking the transition from construction to operational phase when a project begins to generate revenue.The Directions recognises three forms of DCCO. [see Para 9(e) to (m)]

CRE and its sub-category CRE-RH

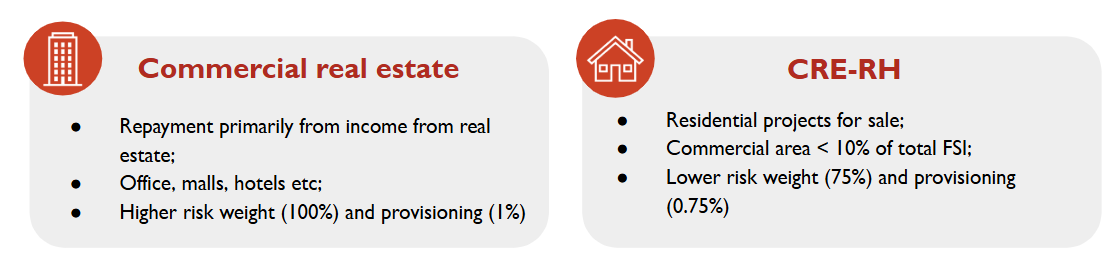

Defined in Directions on Classification of Exposures as Commercial Real Estate Exposures, CRE refers to loans or exposures where repayment primarily depends on income generated by the real estate asset itself. This typically includes office spaces, malls, warehouses, hotels and multi-family housing complexes that are leased or sold in the open market. Since CRE is a sub-head of project finance, it also follows similar characteritics of project finance i.e.both repayment of the loan and recovery in case of default are closely tied to the cash flows from the real estate asset such as rental income or sale proceeds. [see para 9(b)]. The definition is aligned with the definiton of income-producing real estate (IPRE) under Basel norms. Our article discussing CRE can be assessed here. https://vinodkothari.com/2023/04/commercial-real-estate-lending-risks-and-regulatory-focus/

Commercial Real Estate – Residential Housing (CRE-RH) [see para 9(c)]

Since residential housing projects generally pose lesser risk and volatility compared to commercial properties, the RBI created a distinct sub-category within CRE called CRE-RH vide notification dated June 21, 2013. CRE-RH includes loans given to builders or developers for residential housing projects meant for sale.To classify as CRE-RH, the project must be predominantly residential and commercial components like shops or schools should not exceed 10% of the total built-up area (FSI). If the commercial area crosses this 10% threshold, the entire project will be CRE. This distinction isn’t just semantic, it has regulatory benefits. Since CRE-RH are subject to lower risk due to various reasons such as diversified cash flows and lower dependency on a single occpnt, RBI has assigned lower capital risk weights i.e. 75% to CRE-RH compared to standard CRE 100% and lower provisioning provisioning requirements (0.75% vs. 1%).

Prudential requirements

Provisioning requirements

In the context of project finance, where risks vary across different phases of a project’s lifecycle, a one-size-fits-all provisioning approach throughout the project life may not be relevant. .

Under the SBR, provisioning norms made no distinction between the construction and operational phases of a project. A uniform provisioning rate was applied i.e. 0.75% for CRE-RH and 1% for CRE while other loans were provisioned at 0.4% irrespective of whether the project was just starting construction or had already begun generating revenue. This approach, while simple, failed to reflect the heightened risks associated during the construction phase , such as delays, cost overruns, or regulatory hurdles.

To address this gap, the Draft Directions, proposed a conservative approach calling for a 5% provision during the construction phase and 2.5% during the operational phase, with the operational rate reducible to 1% if following conditions were met:

the project demonstrated positive net operating cash flows sufficient to service all current repayment obligations, and

there was a minimum 20% reduction in long-term debt from the level outstanding at the time of achieving DCCO.

These draft norms were considered overly harsh, particularly for long-gestation infrastructure projects where cash flows stabilise gradually.

Taking stakeholder feedback into account, the Directions adopted a more balanced g structure as follows:

Project type

Construction Phase

Operational phase – after commencement of repayment interest and principle

Commercial real estate (CRE)

1.25%

1%

CRE – Residential Housing

1%

0.75%

Other projects

1%

0.40%

DCCO deferred projects:

Additional provisioning to be maintained depending on the type of project:0.375% per quarter for infra projects0.5625% per quarter for non-infra projects

NPA project finance accounts

As per extant instructions

Provisionig for existing projects

Continued to be governed by extant norms;If resolution is done for any fresh credit event or change in terms occur after the effective date of these directions, then provisioning as per these Directions

RBI’s draft proposal for lower risk-weights for high quality infrastructure projects

The RBI has issued a draft amendment to the Scale Based Regulations, 2023 on 27th October, 2025, proposing a lower risk weight framework for ‘High-Quality Infrastructure Projects’. Once finalised, the provisions would be applicable from April 1, 2026, or from an earlier date when adopted by an NBFC in entirety. The intent of the amendment is to recognise and incentivise lending to stable, well-performing infrastructure projects by prescribing reduced risk weights for such exposures. Under the draft, “High-Quality Infrastructure Projects” are defined as infrastructure projects meeting all of the following conditions:

The project has completed at least one year of satisfactory operations post achievement of the actual DCCO;

The exposure is classified as ‘standard’ in the books of the lender;

The obligor’s revenue depend on one main primary counterparty, which shall be the Central Government or a Public Sector Entity, and the contractual terms ensure certainty of payment, such as through availability-based1 or take-or-pay arrangements2;

The contractual provisions offer strong creditor protection such as escrow of cash flows, legal first charge on project assets and other appropriate safeguards in case of early termination;

The obligor has adequate internal or external funding arrangements to meet current and future working capital or other funding needs, as assessed by the lender;

The obligor is restricted from undertaking actions detrimental to creditors, such as raising additional debt secured by the project’s cash flows or assets without lender’s consent.

Projects meeting all of the above criteria will qualify as high-quality infrastructure assets and will attract lower risk weights, as follows:

50%, where the obligor has repaid at least 10% of the sanctioned amount;

75%, where the obligor has repaid at least 5% but less than 10% of the sanctioned amount.

If a project subsequently fails to meet any of the qualifying conditions, it will cease to be treated as a high-quality asset and will instead attract the standard risk weight of 100% applicable to regular infrastructure exposures.

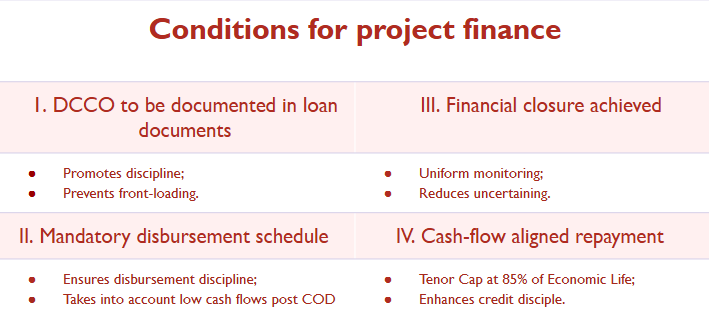

Conditions of project finance

The onus is on the lender to ensure that the following conditions are met before extending any project finance. These conditions will ensure that the facility is structured prudently and is aligned with the implementation as well as cash flows of the project, thereby mitigating both credit as well as project risk. The requirements are more or less similar to the earlier Directions.

Repayment schedule during operational phase is designed to factor initial cash flows

Repayment tenor, including the moratorium period, if any, shall not exceed 85% of the economic life of a project.

This means there is a mandatory 15% tail period i.e. if the project has an economic life of 20 years and the loans are to be repaid in 17 years, the last 3 years are the tail period.Tail period gives comfort to the lender that in case of any default or delay in repayment by the time of maturity, there is still some period left to recover dues from the project cash flows after the scheduled loan maturity.

Would this mean that a borrower cannot obtain a top-up loan after the expiry of 85% of the loan tenure?

The requirement applies to loans with all kinds of tenures, either short or long.

One borrower, multiple lenders

If a project is financed by more than one lender, RBI mandates that the DCCO, whether original, extended or actual, shall be the same across all lenders. This will ensure that:

DCCO is uniform across all lenders

Project progress as well as any delays are uniform across all lenders

Uniform asset classification, preventing any lender from having a different provisioning status.

To ensure balanced risk sharing, the Directions have put consortium lending limits (Para 15): Where projects are under-construction:

Aggregate exposure of all lenders is ≤ ₹1,500 crore: each lender shall hold at least 10% of total exposure;

For projects with exposure > ₹1,500 crore: each lender must hold at least 5% or ₹150 crore, whichever is higher.

These caps essentially require participating lenders to hold sufficient skin in the game and thereby promote responsible credit appraisal as well as avoid risk from being concentrated in a few lenders, especially where other lenders have negligible exposure and hence, less incentive to ensure monitoring.

Inter-lender transfer

These minimum exposure norms will not apply to operational phase projects;

In design or construction phase, lenders are permitted buy/sell exposure only under syndication arrangements as per TLE, and within the exposure limits

In operational phase, exposures can be freely transferred as per TLE norms.

This may be because construction and pre-operational stages are inherently more uncertain and riskier, and therefore, the regulator requires lenders who are willing to remain committed and not exit easily to avoid creating instability.

Project lifecycle – 3 different phases

A project has been divided into 3 phased viz Design, Construction and Operational.

Why does this classification matter?

The regulatory framework treats each phase differently for various risk, compliance and prudential reasons.

Disbursement discipline (Para 21)

Disbursal of funds must be linked to project completion milestones i.e. completion of phases.

Lenders must also track progress in equity infusion and other financing sources as agreed at financial closure

Asset classification (Para 22 & 29)

In design and construction phases, loans can be classified as NPA based on recovery performance, as per IRACP norms.

Once an account is classified as NPA, it can only be upgraded after demonstrating satisfactory performance during the operational phase

Resolution trigger (Para 23)

If any credit event (e.g., default) occurs with any lender during the construction phase, a collective resolution process is triggered

Provisioning norms (Para 32)

Provisioning rates are higher for projects under construction

Once the project enters the operational phase, provisioning reduces, reflecting lower credit risk.

Mandatory requirements before sanctioning a project finance loan: (13)

Achievement of financial closure and documentation of original DCCO;

Project specific disbursement schedule vis a vis stage of completion is included in loan agreement

Post DCCO repayment schedule designed to factor initial cash flows

Prudential conditions related to disbursement and monitoring:

Lender to ensure the following:

Clearances are obtained by the lender:

All requisite approvals/clearances for implementing/constructing the project are obtained before financial closure.(examples: environmental clearance, legal clearance, regulatory clearances, etc.)

Approvals/clearances contingent upon achievement of certain milestones would be deemed to be applicable when such milestones are achieved.

Availability of sufficient (prescribed) minimum land/right of way with the lender before disbursal of funds

This would mean that lender must ensure that the builder executing the project has either:

Ownership of the land (through purchase, lease etc.) or

Legal rights to use/access the land i.e. Right of Way.

For PPP projects, disbursal of funds to occur only after declaration of the appointed date.

Except where non-fund based facilities are mandated by the concessioning authority as a pre-requisite for declaration of the appointed date itself;

Disbursal to be proportionate

To stages of completion of project, infusion of equity or other sources of finance and receipt of clearances

Lender’s Independent Engineer/Architect to certify the stages

Creation and maintenance of a project finance database (see para 37):

Every lender to capture and maintain, on an ongoing basis, project specific information relating to:

Debtor and project profile;

Change in DCCO;

Credit events other than deferment of DCCO;

Specifications of project

Any updation shall be made within 15 days from any change in information;

Necessary systems to be placed within 3 months from the effective date ie by 1st January, 2026

Resolution of Project Loans

Prudential norms for resolution

Lender to monitor performance of project on on-going basis;

Expected to initiate a resolution plan well in advance.

Collective resolution to be initiated by the lenders in case credit event happens with any one lender

In case of any credit event;

Lender to report the same:

to the Central Repository of Information on Large Credit and;

to all other lenders, in case of consortium lending.

Lender to take a review of debtor account within 30 days.

Inter creditor agreement and decision to implement a resolution plan may be done during this period.

Implement the resolution plan within 180 days from the end of the review period.

Resolution plans involving extension of DCCO

Paragraphs 26 to 28 provide a structured framework under which project loans may continue to be classified as ‘standard’ despite delays in project completion, provided specific conditions are met. The objective is to offer flexibility to lenders and borrowers in addressing genuine project delays or cost escalations, without triggering an immediate downgrade to NPA so long as the resolution is timely and prudently implemented.

Permitted DCCO deferment

The DCCO may be deferred, with a corresponding adjustment in the repayment schedule. However, such deferment is subject to the following maximum limits:

Up to 3 years for infrastructure projects

Up to 2 years for non-infrastructure projects (including commercial real estate)

Cost overrun associated with the DCCO deferment:

A cap of 10% of the original project cost, over and above Interest During Construction (IDC)

The overrun must be financed through a Standby Credit Facility sanctioned at the time of financial closure

Post-funding, key financial metrics such as the Debt-Equity ratio and credit rating must remain unchanged or show improvement in favour of the lender

Deferment in DCCO associated with change in scope and size

Rise in project cost (excluding cost overrun) is at least 25% or more of the original project outlay

Reassessment of project viability by the lender before approving the revised scope and DCCO

If the project has an existing credit rating, the new rating must not deteriorate by more than one notch; if unrated and aggregate lender exposure is ₹100 crore or more, the revised project must obtain an investment-grade rating

This benefit of maintaining ‘Standard’ classification due to a change in scope can be availed only once during the project’s life

Resolution plan (‘RP’) deemed successfully implemented only if:

Necessary documentation completed within 180 days from the end of the Review Period and;

Revised capital structure and financing terms are duly reflected in the books of both the lender and the borrower.

Immediate downgrading to NPA if the resolution plan is not implemented within the timeline and conditions above

Once NPA, account can be upgraded only after:

Satisfactory performance post actual DCCO, in case of non-compliance with conditions of resolution plan;

Successful implementation of resolution plan, in case of non-implementation of RP within the specified time.

See a detailed PPT on the Project Finance Directions here

A contractual model where the project earns fixed payments from the counterparty based on the asset’s availability and performance, irrespective of actual usage or demand ↩︎

A contract under which the buyer agrees to pay for a specified quantity of output (e.g., power, gas, water) whether or not it actually takes delivery, ensuring predictable cash flows for the project. ↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-23 16:44:502025-10-28 18:11:30Balancing flexibility and discipline: Analysis of RBI’s Project Finance Directions, 2025

Loan write-offs in case of banks has been a consistent practice, and has been sharply criticized in several forums. Loan write-offs constitute a significant amount: Between FY 2015 and FY 2024, Scheduled commercial banks wrote off loans worth ₹12.3 lakh crore, with a ₹9.9 lakh crore written off in just the last five years (FY 2020 to FY 2024).

Year

Amount (in INR Crore)

2023-24

1,70,270

2022-23

2,08,037

2021-22

1,74,966

2020-21

2,02,781

2019-20

2,34,170

Total

9,90,224

Table 1: Loan write-offs by banks in the last 5 years (FY 20 – 24)

On the other hand, global supervisors and developmental bodies have always advocated a sound loan write-off policy for uncollectable loans. In its 2014 paper, IMF says:

“Banking supervisors should have a general policy requiring timely write-off of uncollectible loans and assist banks in formulating sound write-off criteria. The benefits of timely write-offs of uncollectible loans are numerous … A bank should write off a loan or portion of a loan when it is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted. This does not have to be preceded by exhausting all legal means and giving up contractual rights on cash flows. This also does not mean that the loan has absolutely no recovery or salvage value, but rather that it is not practical or desirable to defer writing off this essentially worthless asset even though partial recovery may be realized in the future.”

The IMF paper also discusses the potential downside of the write-off – that the reported NPLs would be lower, however, it argues that the write-off gives a better picture of the provision coverage.

European regulators have also extensively recommended loan-write off policy. In a 2017 paper1, European Central Bank says:

“An entity should write off a financial asset or part of a financial asset in the period in which the loan or part of the loan is considered unrecoverable. For the avoidance of doubt, a write-off can take place before legal actions against the borrower to recover the debt have been concluded in full. A write-off does not involve the bank forfeiting the legal right to recover the debt; a bank’s decision to forfeit the legal claim on the debt is called “debt forgiveness”.

The World Bank in a 2019 paper2 has, likewise, given several benefits of a write-off as compared with provisioning:

“An ambitious NPL write-off policy provides several benefits for banks and the financial system.