Guidelines on Settlement of Dues of borrowers by ARC

– Team Finserv (finserv@vinodkothari.com)

Loading…

Loading…

– Team Finserv (finserv@vinodkothari.com)

Loading…

-Anshika Agarwal (finserv@vinodkothari.com)

Core Investment Companies (CIC) and Alternative Investment Funds (AIF) are two very common modes to channelise investments in the Indian market. Both are regulated by different regulators; while CICs are regulated by the RBI, AIFs are regulated by the SEBI. Under their respective regulatory frameworks, both are technically permitted to invest in one another. However, this permissibility introduces an intriguing paradox, especially for a CIC, which is allowed to invest in group companies. It points out that this approach effectively creates two investment pools—one directly under the CICs and another through the AIFs. This dual-pool structure complicates what could otherwise be a straightforward process, introducing unnecessary layers of complexity, thus deviating from the primary purpose of CICs to hold and manage investments efficiently within group companies.

The following article examines the implications of Paragraph 26(a)1 of the Master Direction – Core Investment Companies (Reserve Bank) Directions, 2016 (“CIC Master Directions”), but before delving into the specifics, it may be worthwhile to discuss in brief the concepts of AIF and CIC.

AIFs have gained prominence as a pivotal part of the financial ecosystem, providing investors with access to diverse and innovative investment opportunities. The key features of an AIF are as follows:

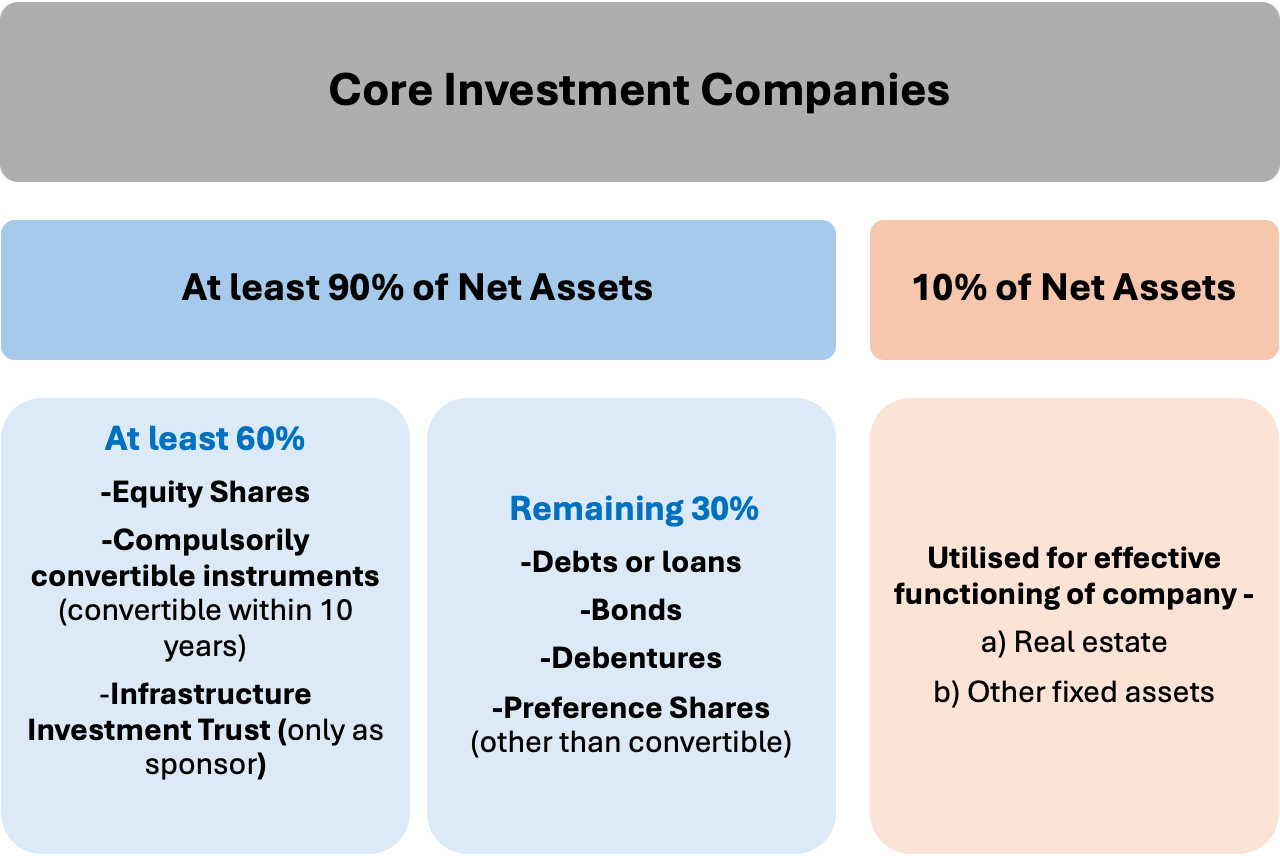

CICs are a specialized subset of Non-Banking Financial Companies (NBFCs) established with the primary purpose of holding and managing investments in group companies. CICs do not engage in traditional financial intermediation but play a vital role in maintaining financial stability within the ‘group companies’. CICs are governed under the CIC Master Directions to ensure that their activities align with regulatory standards.

Below given graph explains the regulatory permissibility of the kind of investments a CIC can make:

In addition with the aforesaid, it may further be noted that CICs are permitted to carry out the following financial activities only:

It may be noted that the RBI’s FAQs on Core Investment Companies, particularly Question 92 has clarified about the 10% of Net Asset –

“What items are included in the 10% of Net assets which CIC/CIC’s-ND-SI can hold outside the group?

Ans: These would include real estate or other fixed assets which are required for effective functioning of a company, but should not include other financial investments/loans in non group companies.”

The term “group companies” is defined under Para 3(1)(v) of the CIC Master Directions. It refers to an arrangement involving two or more entities that are related to each other through any of the following relationships:

| Subsidiary – Parent (as defined under AS 21), Joint Venture (as defined under AS 27), Associate (as defined under AS 23), Promoter-Promotee (as per the SEBI [Acquisition of Shares and Takeover] Regulations, 1997 for listed companies), Related Party (as defined under AS 18), Entities sharing a Common Brand Name, or Entities with an investment in equity shares of 20% or more |

Para 26A of the CIC Master Directions deals with Investments in AIFs. The language of the provisions suggest that CICs are permitted to invest in AIFs. However, this provision introduces a significant legal contradiction that undermines the regulatory framework governing CICs. According to the Doctrine of Colorable Legislation, a legal principle ensuring legislative consistency, what cannot be achieved directly cannot be permitted indirectly. By allowing CICs to invest in AIFs, Para 26(a) effectively circumvents the explicit restriction on investments outside group companies. This indirect allowance is inconsistent with the foundational objectives of the CIC Master Directions and creates substantial legal and operational confusion.

Under the SEBI (Alternative Investment Funds) Regulations, 2012, the primary objective of an Alternative Investment Fund (AIF) is to pool funds from investors and allocate them across diverse investment opportunities. However, structuring an AIF to invest predominantly or exclusively in entities within the same group raises concerns regarding compliance with SEBI’s regulatory framework, particularly its diversification. SEBI imposes strict investment concentration limits, as outlined in one of its Circular3.

For Category I and II AIFs, no more than 25% of their investable funds can be allocated to a single investee company, while Category III AIFs are restricted to 10%. These regulations inherently prevent AIFs from focusing solely on group entities unless the investment structure strictly adheres to these limits. For CICs intending to invest in AIFs, these restrictions pose significant limitations if the goal is to channel funds primarily into group companies.

Technically, the answer is affirmative—AIFs can be part of a group entity within a group if it satisfies any of the conditions mentioned in the definition. However, if CICs invest in AIFs within the same group structure, it fails to resolve the underlying issue. AIFs often invest outside the group companies, exposing CICs indirectly to entities external to the group. This contradicts the core purpose of CICs, which is to focus investments within their own group companies. Such a structure not only undermines the original intent of CICs but also raises compliance concerns. The RBI adopts a pass-through approach in these cases and is likely to view such practices as non-compliant.

The regulatory paradox of allowing CICs to invest in AIFs under Para 26(a) of the CICs Master Direction raises important questions about the practicality and purpose of this provision. At its core, CICs are meant to simplify and streamline the management of investments within their group companies. However, the inclusion of AIFs creates an unnecessary layer of complexity, dividing investments into dual investment pools and making it harder to track, manage, and maintain transparency.

This arrangement doesn’t just complicate operations, it also moves CICs away from their original purpose. By routing investments through AIFs, CICs are exposed to entities outside their group, which can lead to compliance risks, regulatory confusion, and inefficiencies. Even from a taxation perspective, the setup offers no real benefits, adding financial burdens without meaningful gains. Paragraph 26(a) of the CICs Master Direction has been taken from the SBR Master Direction, which is applicable to NBFCs. However, including it in the CICs Master Direction, which provided regulation specifically for CICs NBFC does not appear to serve any purpose. Even if it were to be amended, its relevance of stating the same for CICs NBFC would still remain questionable.

– Anshika Agarwal (finserv@vinodkothari.com)

The Reserve Bank of India (RBI) has consistently emphasized the significance of robust internal control systems; where gaps are found by the supervisor, it has penalised regulated entities for non-compliance. Recently, the RBI imposed a penalty on an NBFC for outsourcing one of its core management functions, i.e., internal audit to an external auditor, thereby raising doubts as to whether internal audit for NBFCs can be conducted by external auditors. Does the very fact that internal audit is being conducted not internally but by an external chartered accountancy firm amount to “outsourcing” of core management function? This article examines outsourcing in the context of internal audit function, and the conditions subject to which internal audit may be conducted by external agencies.

Outsourcing is defined under the Basel 2005 document1 as “a regulated entity’s use of a third party (either an affiliated entity within a corporate group or an entity that is external to the corporate group) to perform activities on a continuing basis that would normally be undertaken by the regulated entity, now or in the future.” Similarly, the IOSCO Consultation Paper2 refers to outsourcing as “a business practice in which a regulated entity uses a service provider to perform tasks, functions, processes, or activities that could otherwise be undertaken by the regulated entity itself.”

NBFCs, especially those with asset-light models or limited resources, opt for outsourcing to manage financial as well as non-financial functions. Outsourcing by NBFCs typically involves delegating tasks such as loan application processing, collection of documents, data processing, IT support, customer service, and back-office operations to third-party providers. While outsourcing boosts operational efficiency, they also carry risks, particularly when core management functions are outsourced. Notably, outsourcing is distinct from availing professional services like legal, audit, consulting, or property management, which are ancillary to the NBFC’s core business. In case of outsourcing of financial functions by regulated entities, there are specific guidelines issued by the RBI to regulate the arrangements. Clear regulatory oversight is crucial to strike a balance between leveraging external expertise and maintaining ethical, efficient practices in the financial services sector.

The RBI guidelines are specifically aimed at managing risks related to outsourcing of financial services. Master Direction – Reserve Bank of India (Non-Banking Financial Company – Scale Based Regulation) Directions, 2023 (‘SBR Directions’)3, particularly Annexure 13 on Instructions on Managing Risks and Code of Conduct in Outsourcing of Financial Services by NBFCs (‘Outsourcing Guidelines’), Para 2 lays down stringent conditions for outsourcing to ensure compliance, accountability, and effective risk management. While outsourcing can support operational efficiency, core management functions must remain under the direct control of the regulated entity.

The Outsourcing Guidelines explicitly prohibits NBFCs from outsourcing core management functions vital to governance, decision-making, and risk management. The core management functions are those that are vital and crucial for the existence as well as operations of the entity. These have been defined to include:

These functions are critical for ensuring the organization’s stability and operational integrity. For example, internal audit functions identify risks, ensure regulatory compliance, and assess control effectiveness. Entrusting such functions to external entities could compromise decision-making and erode organizational trust.

While the internal audit function itself is a core management process, the Outsourcing Guidelines in the same lines allows regulated entities to engage internal auditors on a contractual basis. This means external professionals can be brought in to execute internal audits, provided their engagement adheres to regulatory standards, independence is maintained, and the entity retains oversight and control rather than putting all the responsibility on a third party.

For example, an entity may handle several operational tasks related to an audit, such as preparing documentation, organizing records, or conducting initial reviews. However, the ultimate responsibility for decision-making, oversight, and ensuring compliance with regulations rests with the audit committee or the entity’s senior management. This approach ensures that the internal management retains control over key aspects of the audit process, even while delegating specific tasks or availing expertise support. In contrast, the action of outsourcing shifts the entire responsibility for the audit to a third-party. This means the external firm is accountable for managing and executing all aspects of the audit, from operational tasks to final implementation. Such an outsourcing may reduce the internal workload, however, it also transfers control and accountability to an external entity, which may not align entirely with the entity’s internal objectives and strategic priorities.

In other words, what is permitted is to avail the expertise services of a third party for carrying out the internal audit function but not the transfer of the entire responsibility of carrying out internal audit to a third party.

The Institute of Chartered Accountants of India (ICAI) Standards on Internal Audit4 states that “Where the Internal Auditor lacks certain expertise, he shall procure the required skills either though in-house experts or through the services of an outside expert, provided independence is not compromised”.

The aforesaid guidance from the ICAI emphasizes maintaining expertise and independence. While not explicitly addressing outsourcing, these standards recognize that internal auditors may lack certain specialized skills. In such scenarios, they encourage engaging in-house or external experts while safeguarding independence.

The standards indirectly allow for outsourcing when:

By availing the services of experts ensures that internal audit teams possess the necessary skills to perform effective reviews, while the entity retains oversight and accountability.

Section 138 of the Companies Act, 2013 (‘CA 2013’)5, specifies the requirement for internal audits for certain classes of companies. It allows the appointment of internal auditors, which may include chartered accountants, cost accountants, or other professionals, as decided by the Board. Explanation of Rule 13 of the Companies (Accounts) Rules, 2014, states that “the internal auditor may or may not be an employee of the company”.

The aforesaid provision also enables companies to engage external auditors to perform internal audits, even if they are not part of the organization. While the CA 2013 does not explicitly prohibit outsourcing of internal audit functions, it places the ultimate responsibility for conducting and reporting on internal audits with the Board. This also clarifies that companies may utilize external expertise while maintaining oversight and control of the audit process.

In conclusion, the RBI’s recent penalties underscore the importance for regulated entities to maintain strict compliance with outsourcing regulations, particularly regarding core management functions. While the Outsourcing Guidelines as well as the provisions of CA 2013 permit engaging external auditors on a contractual basis to perform operational tasks related to audits, accountability and strategic control such as having audit plan approved by the audit committee, regular reporting to the audit committee, discussion of the board and audit committee on the conduct of audit,implementing remedial measure on the oversight of the audit committee or senior management must remain firmly within the organization. Adherence to these principles will help maintain the fine distinction between outsourcing the internal audit function and appointing external auditors as internal auditors, specifically in the context of internal audits.

Read our other related resources –

In this edition of Shastrath, we address key concerns and considerations for lenders in light of the Draft DPDP Rules published on January 03, 2025, and discuss steps to take in order to ensure readiness and compliance.

Register your interest here: https://docs.google.com/forms/d/e/1FAIpQLSf0uZidJDf8oqK0GfGygo0BmuCKRg9wMo2bXRtwRMIra7Zx5Q/viewform

– Anshika Agarwal (finserv@vinodkothari.com)

Loading…

– Vinod Kothari (vinod@vinodkothari.com)

Paragraph 42 of the Master Direction – Reserve Bank of India Non-Banking Financial Company – Scale Based Regulation) Directions, 2023 (‘SBR Directions’), mandates obtaining prior approval from the RBI for any change in shareholding of 26% or more or any change in management amounting to 30% or more. Before we get into details of the requirement, it is important to start with two observations.

First, this regulation, requiring RBI’s approval for change of control, shareholding or management, applies to all NBFCs, large or small. Given the expanse of the definition, exacerbated by the lack of clarity, this regulation is a constant pain for most NBFCs, particularly the smaller ones.

The second point – the regulation is worded quite vaguely. As the discussion below will reveal, what is change in shareholding of 26% does not come clearly from the language at all. When the language is unclear, the subjects are exposed to erring on the safer side of the law, and end up doing superfluous compliances.

Language may not be clear, but the intent or object of the regulations is clear; one would wish the interpretation of the provision does justice to the intent.

NBFCs must seek the prior permission/ approval from the RBI before strategic changes such as takeovers, acquisition of major shareholding, or significant management changes from the viewpoint of entry of new persons on board. What is the intent of seeking this approval: the RBI granted registration to an NBFC after examination of its control, shareholding and management. The RBI had to satisfy itself that the persons behind the NBFC are “fit and proper”. In a manner of speaking, the RBI is handing the keys of an access to the financial system – therefore, it wanted to be fully sure of who the person taking the keys are.

It is a person acquiring control, coming into management, or building up a significant shareholding, who needs to be tested from the viewpoint of “fit and proper”. There is no question of the person, who is admittedly already in control, from earning that qualification. Also, there is no question of the person walking out of control or transferring out significant shareholding to need approval.

There are two exceptions, viz., if shares are bought back with court (now NCLT) approval, or, in case of change of management, if directors are re-elected on retirement by rotation. But even with exceptions, NBFCs still need to inform the regulator about any changes in their directors or management.

Note that the carve-out in case of buybacks is only for such buybacks as are coming for NCLT approval, which would mean reduction of capital u/s 66 of Companies Act 2013. As regards buybacks done with board or shareholders’ approval, in view of the limit of 10%/25% of the equity shares, usually a single buyback should not cause a change of control, but it may so happen that one significant shareholder stays back, and other takes a buyback and exits, causing the former’s shareholding to gain majority or significant shareholding (as discussed below). In such a case, exceptions from RBI approval will not be available.

And the other carve-out of reappointment of directors is not a change in management at all. If, at a general meeting, the existing director(s) is rotated out, and a new director comes in place, there is surely no exception in that case.

There are three situations requiring approval of the RBI; all of these have to be seen in light of the purpose of getting the supervisor’s sign off by way of a “fit and proper” person check. The three situations are:

This is required to be read in light of the definition of “control” in SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (‘SAST regulations’) [by virtue of reg 5.1.5]. There is an inclusive definition of “control” in SAST Regulations, which is far from giving any bright-line test of when control is said to have been acquired[1]. There is no definition of “takeover” in the SAST Regulations, even though the title of the Regulations is “substantial acquisition of shares” and “takeovers”. A view might be that “substantial acquisition of shares” is a case of takeover. In that case too, there are two different situations covered by SAST Regulations – first time acquisition of 25% or more of the equity shares [Reg 3 (1), or a creeping acquisition of 5% or more in a financial year, by a person already holding 25% or more [Reg 3 (2)].

Acquisition of control is covered separately by Reg 4. The question, in the context of NBFCs is, whether “takeovers” and “change of control” are to be read as two separate situations, and if yes, what will be the meaning of “takeover”? Can it be said that every “substantial acquisition of shares” is a takeover, and if so, whether only the first-time acquisition or the creeping acquisition as well? First of all, there is no reason to include creeping acquisition here, as the relevance of the same is limited to equity listed companies. In fact, the way creeping acquisition is defined in SAST Regulations, there may actually be no change in shareholding at all, and still an acquirer may have hit the creeping acquisition limit.

Acquisition of “control”, though subjective, has been interpreted in several leading SC and SAT rulings. The definition of “control” in sec. 2 (27) of the Act and Reg. 2 (1) (e) of SAST Regulations is an inclusive one: it does not define control, but extends the meaning of the term to include management control or the right to appoint majority directors. The more common mode of control is voting control. The expression “control” has been subject matter of several leading rulings such as Arcelormittal India Private V. Satish Kumar Gupta, in which the Supreme Court defined the expression “control” in 2 parts; de jure control or the right to appoint a majority of the directors of a company; and de facto control or the power of a person or persons acting in concert, directly or indirectly, in any manner, can positively influence management or policy decisions. In Shubhkam Ventures V. SEBI, the meaning of control was extensively discussed by the SAT, it was held that the test is to see who is in the driving seat, the question would be whether he controls the steering, the gears and the brakes. If the answer to this question is affirmative, then alone would he be in control of the company. In other words, the question to be asked in each case would be whether he is the driving force behind the company and whether he is the one providing motion to the organization. If yes, he is in control but not otherwise.

Note that control may be direct or indirect. Indirect control typically arises when the controlling person controls an intermediate entity or entities, which in turn have a control over the target entity.

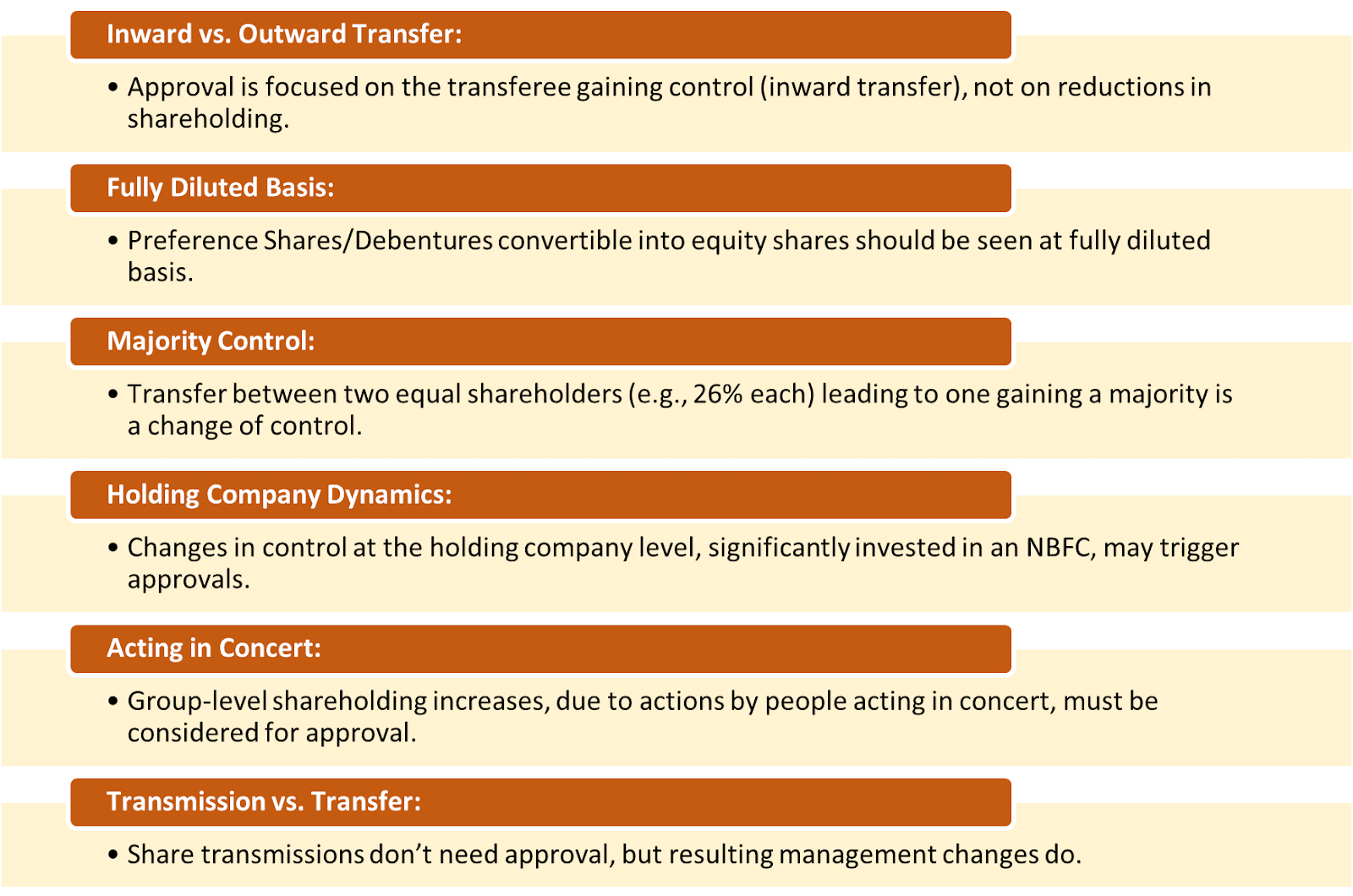

This clause may have a lot of interpretational difficulties. First question – is 26% the magnitude of change in shareholding, or is the threshold which cannot be crossed? For example, if a shareholder was holding 25% shares in the NBFC, and now proposes to acquire another 1%, is this subject to regulatory approval? The answer should be clearly yes, because the shareholder will now be having what is regarded by the regulation as significant shareholding. On the contrary, if the person is already holding 26%, he is a significant shareholder already, either by virtue of having such shareholding at the time of formation of the NBFC, or based on the acquisition approved by the RBI. So, what will be the next level that will require regulatory approval? Logically, it seems that the person has already been approved to come as a significant shareholder, and therefore, an increase in shareholding should not require any intervention. In other words, the regulatory approval is required for the first time acquisition and not for the creeping acquisition. It may, however, be argued that if the creeping acquisition makes the equity holding cross 50%, then it amounts to acquisition of control, and that falls under the first clause.

In short, regulatory approval is required for first time acquisition of 26% equity stake or higher, or 50% or higher.

There are many other points that arise in connection with the change in shareholding.

First, is the transfer in shareholding here inward transfer, or can it mean outward transfer as well? Every transfer has a transferor and a transferee, but it is logical to assume the context of the regulation requires the supervisor to approve the transferee. It is the transferee who is coming in control. This is also evident from the word of the proviso to reg 42.1.1 (ii), which is obviously an exception to the main clause, and uses the words “prior approval would not be required in case of any shareholding going beyond 26 percent”. It implies that the concern of the regulator can only be for shareholding going beyond 26% and not reduction of the level of shareholding. The same intent also becomes evident from use of the word “progressive increases over time”. Note that there is inclusivity in the regulation – evident from words like “including”. Further, someone may extract a meaning from the language “transfer” – saying even a transfer out is also a transfer. This is precisely the point we made earlier – that this provision, worded loosely and applied universally, gives a lot of scope for an ambitious regulator to ask for approvals where approvals may not have any relevance.

Secondly, the expression is transfer of “shareholding” – should it include preference shares and convertible debt instruments as well? On the face of it, a preference shareholder or debenture holder does not have control over the entity. If the shares or debentures are either compulsorily or optionally convertible, then the threshold of 26% should be computed by taking the post-dilution equity base. Also, sometimes, preference shares may come with terms which give the preference holders some degree of control. For example, several decisions may be made subject to preference holders’ okay. Or the preference shares may be participating preference shares. In these cases, excluding preference shares altogether may not be proper.

Third, if there are two shareholders, both holding 26% each, and now, one transfers the holding to the other, this may be a case of change of control, as the acquirer now will have 52% holding.

Fourth, when it comes to acquisition of control or significant shareholding, one must take a substantive view, and should not be hamstrung by literal interpretation. For example, if entity A is the NBFC, and entity B is the holding company whose business or assets, almost entirely, constitutes the holding of shares in the NBFC, then, one should apply the change of control at the holding company level as well. Note that even as per SAST Regulations, if a holding vehicle is, to the extent of 80% or above, invested in the target company, acquisition of stake in the holding vehicle will be taken as direct acquisition of stake in the target entity.

Fifth, if some shareholders are acting in concert, or are deemed to be acting in concert, the increase in shareholding should be seen at a group level. Whether certain persons are acting in concert is left to facts or the surrounding situations.

Sixth, transfers of shares may require approval, but if the vesting of shares happens due to a transmission, there is no question of approval for the acquisition. However, if this leads to a change in management, the same shall require approval.

Change in Control:

This clause is admittedly the most vague clause, and may result into situations which have no correlation with a change in control, yet coming for regulatory approval. The actual language says: “Any change in the management …which would result in change in more than 30 percent of the directors”. This should really mean a change in management or directorships, which is connected with or arising out of a change of control. If control changes or shifts, usually management also shifts. However, there may be a change in board positions irrespective of any change in control or real change of management at all. Appointment and removal of independent directors are not considered for this purpose. However, nominee directors have not been excluded. Therefore, any appointment or removal of nominee directors will require prior approval if such appointment breaches the limit of 30%.

In reality, the language rules the meaning, and the interpretation is that if there is a change in directorships to the extent of 30% or more, excluding independent directors, the same will require a change of control process, even though there is not even a slightest change in control.

Here again, one may use literal interpretation and argue that “change in directorships” may include directors going out, or coming in. However, in the context, there can never be an intent to control the exit of directors. Exit may happen purely for involuntary or personal reasons – death, resignation, incapacity, etc. The supervisor is to be concerned with the directors who come in, who have to earn the label of being “fit and proper”.

In case of entities with smaller boards, say having 2 or 3 board members, change of even one director may cause change of 30% or more, though there is no real change of management or management control.

Another point to discuss here is, like in case of shareholding, does the change in directorships include progressive changes too? For example, if a company’s board consists of 6 directors, and one is rotated out or replaced in year 1, and the other one, say, after a year or two, without any concerted action, have we reached a change in directorships of 30% or more? In case of shareholding, progressive increases are specifically included; not so in case of change of directorships.

In the author’s view, the provisions of Reg 42 cannot be stretched to imply that every appointment of a director in an NBFC requires RBI’s approval – if such was the intent, the intent could have been spelt out. Neither is there a reason for such micro regulation, since the focus has to be on change of control. However, as a practical expedient, NBFCs are encouraged to intimate the periodic changes in board positions to the RBI by way of an intimation. Therefore, the regulator has an intimation of the changes that take place over time. If the changes in board positions are part of the same intent or design, and are merely phased over time, the same will usually also be associated with a change in shareholding. In any case, if even independent of a shareholding change, if the changes in management happening over time are mutually connected and a part of the attempt to gain management of the NBFC, the same will require regulatory approval. Given the subjectivity involved, NBFCs may want to play safe and place the facts before the RBI for its guidance.

The meaning of “intra- group” transfers is the shareholding which is spread across members of a group. A group should mean here entities either have common control, or common significant influence, or those where persons have been disclosed as acting in concert for holding shares in the NBFC. The following is a question from the RBI’s FAQs relating to intra-group transfers. It is difficult to get the meaning of the response. Once again, the 26% is not the total magnitude of change, but crossing the threshold. Therefore, in the answer below, 26% cannot be read as the total shifting of shares within the group. The group is already above 26%, and now, there is movement of shares within the group. Is the regulator trying to say once the group is holding 26%, any realignment of shares within the group will require approval? Also, in most cases, the shifting of intra-group shareholding does not happen within a closed group. For example, if there are 4 entities of a group holding shares, one of the members of the group may transfer shares to a 5th entity. The lack of any basis for the response is evident from the approach – apply to us by way of a letter, and then we will let you know whether approval is needed or not. It is sad that a regulator/supervisor sits to decide whether the matter comes within the regulatory ambit.

Here is an excerpt from the RBI FAQs:

26. Whether acquisition/ transfer of shareholding of 26 per cent or more of the paid up equity capital of an NBFC within the same group i.e. intra group transfers require prior approval of the Bank?

Yes, prior approval would be required in all cases of acquisition/ transfer of shareholding of 26 per cent or more of the paid up equity capital of an NBFC. In case of intra-group transfers, NBFCs shall submit an application, on the company letter head, for obtaining prior approval of the Bank. Based on the application of the NBFC, it would be decided, on a case to case basis, whether the NBFC requires to submit the documents as prescribed at para 3 of DNBR (PD) CC.No. 065/03.10.001/2015-16 dated July 9, 2015 for processing the application of the company. In cases where approval is granted without the documents, the NBFC would be required to submit the same after the process of transfer is complete.

Corporate restructuring in the NBFC sector involves reorganizing the company’s structure, operations, or finances to improve efficiency, address financial distress, or comply with regulatory requirements. This process can include mergers, demergers, amalgamations, and such other changes in corporate structure.

Given that corporate restructuring is a strategic decision for the structure and existence of the NBFC, it becomes important to evaluate the need for regulatory approvals in this regard. The intent of the regulator, as discussed above, is to require the prior approval in case of substantial acquisitions and change in shareholding beyond the threshold of 26%, with the intent to acquire ‘control’. Hence, in case the corporate restructuring leads to such a change in control or shareholding, with or without the change in management, the same must be done with the consent of the RBI.

For instance, if ABC Ltd. is the holding company of an NBFC and the NBFC intends to merge with the holding company. There is no change in control as such pursuant to such merger. However, as per RBI FAQ No. 84, this shall require the prior approval from RBI.

Another instance could be that ABC Ltd (being non-NBFC) intends to merge with an NBFC. As per RBI FAQ No. 85, where a non-NBFC mergers with an NBFC, prior written approval of the RBI would be required if such a merger satisfies any one or both the conditions viz.,

Even if an NBFC intends to amalgamate with another NBFC, as per FAQ No. 86, the NBFC being amalgamated will require prior written approval of the RBI.

It may be noted that the prior written approval of the RBI must be obtained before approaching any Court or Tribunal for seeking orders for merger/ amalgamation in all such cases which would ordinarily fall under the scenarios discussed above.

[1] Read our detailed analysis on the topic here- https://vinodkothari.com/2017/09/sebi-aborts-brightening-of-fine-lines-of-control/ (last accessed in November, 2024)

[2] Refer to our article on- https://indiacorplaw.in/2016/03/choosing-between-blurred-line-and.html

[3] Read Our FAQs on Change in Management and Control : https://vinodkothari.com/2016/06/faqs-on-change-in-control-or-management-of-an-nbfc/

-Vinod Kothari (vinod@vinodkothari.com)

Against the backdrop the action against 4 specific lender, RBI now expects all NBFCs to appraise their boards of the action taken by the regulator, and in specific terms, have the interest rate policy examined with respect to, at least, the following, in “unambiguous terms”:

Usually, it is believed that if a penal or disciplinary action is taken against some, it is in relation to aberrations by the respective entities. While others need to sit up and take notice it is but natural, but it is a bit different this time – the regulator itself is expecting that all NBFCs need to sensitise their boards on the action taken. The action taken by the RBI is hardly a surprise and therefore, all boards of all NBFCs know it for sure – however, what is not known is what was the background for the action taken. Generic expressions such as “fair, reasonable and transparent pricing, especially for small value loans” have been used in the press release, but these have always been there and have always been the abstractions that everyone talks about, and tried to walk. But what boards of every NBFC will need to know is the nature of the aberrations. Other than just expressing concerns and sending alert signals, NBFCs may need to do self introspection and course correction, for which they would have expected granular observations, as in the case of gold lending vide circular dated September 30, 2024.

It may be the expectation of the regulator that interest rate models, based on which the actual setting of interest rates by business is done, are not vague or subjective, and leave room for opportunistic pricing. For example, the risk premium on loan is imposed on the price: this should be a reflection of the expected loss models. There may be loan acquisition costs and servicing costs – which may be either fixed, variable or semi variable. These may be translated into a mark-up based on appropriate pricing models. The most important component of loan pricing, of course, is the cost of capital – including the cost of equity, which may be priced on the basis of actual (in case of equity, expected) costs of each of the sources of capital. In essence, there is entity-wide or product-wide pricing, such as cost of capital and servicing, and loan-specific pricing, such as cost of acquisition and credit risk premium.

These models may be granularly put before the Boards of NBFCs. Boards do not get into pricing, but with the kind of shocks that RBI has given to some lenders, boardrooms rather get into details of pricing being charged.

Another very important factor in pricing are the “extras”, which have become increasingly important over time. These may be fees that NBFCs get from allied services, or subventions from vendors, etc. These constitute part of the returns, but are not shown as cost to the borrower. These may also eventually be a matter of concern.

Vinod Kothari Consultants did a webinar recently on the RBI crackdown – here is the link to the recording of the webinar: https://youtu.be/poy6_HehPgU?feature=shared.

Other related resources:

Virtual Webinar | 28th October 2024 | 6:15 PM.

To watch the webinar, click here.

Click here to register: https://forms.gle/BtiZdmEDrU7Y9Tcb9

Loading…

-Chirag Agarwal | chirag@vinodkothari.com

On October 10, 2024, RBI updated the Master Direction – Non-Banking Financial Company – Housing Finance (‘HFC Directions’) applicable to HFCs. The HFC Directions were updated to consolidate various circulars that have been issued since its last update on March 21, 2024. A significant change in this edition is the introduction of a new format for the Most Important Terms and Conditions (MITC) following the rollout of the Key Facts Statement (KFS) vide circular no DOR.STR.REC.13/13.03.00/2024-25 dated April 15, 2024.

In this article, we will be discussing the changes introduced by the October 10th update to the HFC Directions.

Previously, Para 85.8 of the HFC Directions mandated that to facilitate a quick, and better understanding of the terms and conditions of the housing loan, a document containing the ‘Most Important Terms and Conditions’ (MITC) must be furnished to the borrower. However, when the KFS circular was first introduced, there was some ambiguity regarding whether both the MITC and KFS would apply to HFCs. This confusion arose because both disclosures contained overlapping information. However, with the recent updates to the HFC Directions on October 10, 2024, clarity has been provided on this matter. The revised regulations clearly state that “the HFCs shall additionally obtain a document containing the other most important terms and conditions (MITC) of such loan (i.e., other than the details included in KFS)”.

Notably, the MITC has now been renamed as Other Most Important Terms and Conditions (‘OMITC’). The OMITC will no longer include disclosures that are already covered in the KFS. The revised format no longer includes an obligation to disclose details of the loan amount, interest rate, type of interest, details of moratorium, date of reset of interest, installment type, loan tenure, the purpose of the loan, fees and other charges, as well as the details of the grievance redressal mechanisms now exclusively appear in the KFS. Further, other substantive aspects have been retained, i.e., details of the security/collateral for the loan, details of the insurance, conditions for disbursement of the loan, repayment of the loans and interest, procedure to be followed for recovery, the date on which annual outstanding balance sheet will be issued, and details of the customer services.

This updated approach simplifies the compliance process for HFCs by clearly defining where specific information should be disclosed. It reduces redundancy and ensures that borrowers can find critical information in a consolidated format without surfing through repetitive disclosures.

The following circulars and notifications have been consolidated under the HFC Directions pursuant to the update:

To summarise, the recent updates to the HFC Directions not only consolidate past circulars but also clarify the relationship between the MITC and KFS. HFCs can now navigate their disclosure requirements more effectively, enhancing transparency and making it easier for consumers to understand the terms of their loan.

Our other resources on the topic are:-