Presentation on Basics of KYC

Loading…

Loading…

Loading…

Loading…

Abhirup Ghosh | abhirup@vinodkothari.com

It is not uncommon to have Indianised version of global dishes when introduced in India, and we are very good in creating fusion food. We have a paneer pizza, and we have a Chinese bhel. As covered bonds, the European financial instrument with over 250 years of history were introduced in India, its look and taste may be quite different from how it is in European market, but that is how we introduce things in India.

It is also interesting to note that regulatory attempts to introduce covered bonds in India did not quite succeed – the National Housing Bank constituted Working Group on Securitisation and Covered Bonds in the Indian Housing Finance Sector, suggested some structures that could work in the Indian market[1] and thereafter, the SEBI COBOSAC also had a separate agenda item on covered bonds. Several multilateral bodies have also put their reports on covered bonds[2].

However, the market did not wait for regulators’ intervention, and in the peak of the liquidity crisis of the NBFCs, covered bonds got uncovered – first slowly, and now, there seems to be a blizzard of covered bond issuances. Of course, there is no legislative bankruptcy remoteness for these covered bonds.

There are two types of covered bonds, first, the legislative covered bonds, and second, the contractual covered bonds. While the former enjoys a legislative support that makes the instrument bankruptcy remote, the latter achieves bankruptcy remoteness through contractual features.

To give a brief understanding of the instrument, a standard covered bond issuance would reflect the following:

Therefore, covered bond is a half-way house, and lies mid-way between a secured corporate bond and the securitized paper. The table below gives comparison of the three instruments:

| Covered bonds | Securitization | Corporate Bonds | |

| Purpose | Essentially, to raise liquidity | Liquidity, off balance sheet, risk management,

Monetization of excess profits, etc. |

To raise liquidity |

| Risk transfer | The borrower continues to absorb default risk as well as prepayment risk of the pool | The originator does not absorb default risk above the credit support agreed; prepayment risk is usually transferred entirely to investors. | The borrower continues to absorb default risk as well as prepayment risk of the pool |

| Legal structure | A direct and unconditional obligation of the issuer, backed by creation of security interest. Assets may or may not be parked with a distinct entity; bankruptcy remoteness is achieved either due to specific law or by common law principles | True sale of assets to a distinct entity; bankruptcy remoteness is achieved by isolation of assets | A direct and unconditional obligation of the issuer, backed by creation of security interest. No bankruptcy remoteness is achieved. |

| Type of pool of assets | Mostly dynamic. Borrower is allowed to manage the pool as long as the required “covers” are ensured. From a common pool of cover assets, there may be multiple issuances. | Mostly static. Except in case of master trusts, the investors make investment in an identifiable pool of assets. Generally, from a single pool of assets, there is only issuance. | Dynamic. |

| Maturity matching | From out of a dynamic pool, securities may be issued over a period of time | Typically, securities are matched with the cashflows from the pool. When the static pool is paid off, the securities are redeemed. | From out of a dynamic pool, securities may be issued over a period of time. |

| Payment of interest and principal to investors | Interest and principal are paid from the general cashflows of the issuer | Interest and principal are paid from the asset pool | Interest and principal are paid from the general cashflows of the issuer. |

| Prepayment risk | In view of the managed nature of the pool, prepayment of loans does not affect investors | Prepayment of underlying loans is passed on to investors; hence investors take prepayment risk | Prepayment risk of the pool does not affect the investors, as the same is absorbed by the issuer. |

| Nature of credit enhancement | The cover, that is, excess of the cover assets over the outstanding funding. | Different forms of credit enhancement are used, such as excess spread, subordination, over-collateralization, etc. | No credit enhancement. Usually, the cover is 100% of the pool principal and interest payable. |

| Classes of securities | Usually, a single class of bonds are issued | Most transactions come up with different classes of securities, with different risk and returns | Single class of bonds are issued. |

| Independence of the ratings from the rating of the issuer | Theoretically, the securities are those of the issuer, but in view of bankruptcy-proofing and the value of “cover assets”, usually AAA ratings are given | AAA ratings are given usually to senior-most classes, based on adequacy of credit enhancement from the lower classes. | There is no question of independent rating. |

| Off balance sheet treatment | Not off the balance sheet | Usually off the balance sheet | Not applicable. |

| Capital relief | Under standardized approaches, will be treated as on-balance sheet retail portfolio, appropriately risk weighted. Calls for regulatory capital | Calls for regulatory capital only upto the retained risks of the seller | Not applicable |

This article would briefly talk about the issuance of Covered bonds world-wide and in India, and what are the distinctive features of the issuances in India.

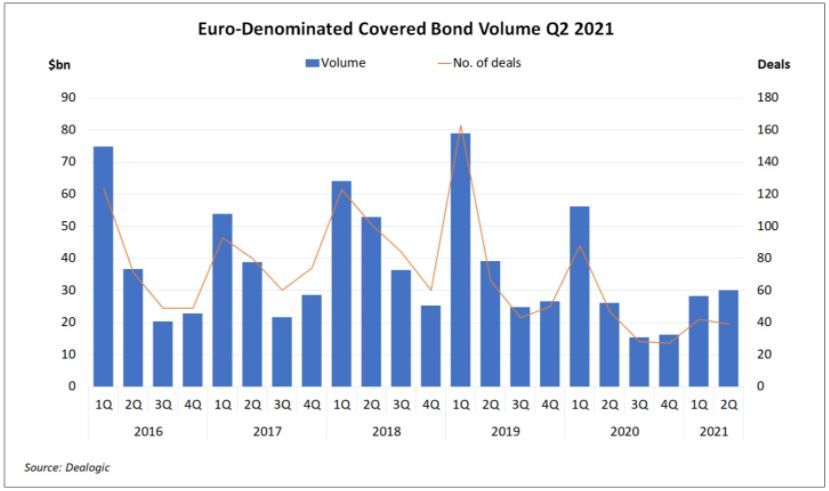

Since most volumes for covered bonds came from Europe, there has been a decline due to supply side issues. This is evident from the latest data on Euro-Denominated Covered bonds Volume. The performance in FY 2020 and FY 2021 has been subdued mainly due to COVID-19. Though, the volumes suffered significantly in the Q3 and Q4 of FY 20, but returned to moderate levels by the beginning of FY 2021.

The figure below shows Euro-Denominated Covered bond Issuances until Q2 2021.

Source: Dealogic[3]

Countries like Denmark, Germany, Sweden continues to be dominant markets for covered bond issuances. The countries in the Asia-Pacific region like Japan, Singapore, and Australia continues to report moderate level of activities. In North America, Canada represents all the whole of the issuance, with no issuances in the USA.

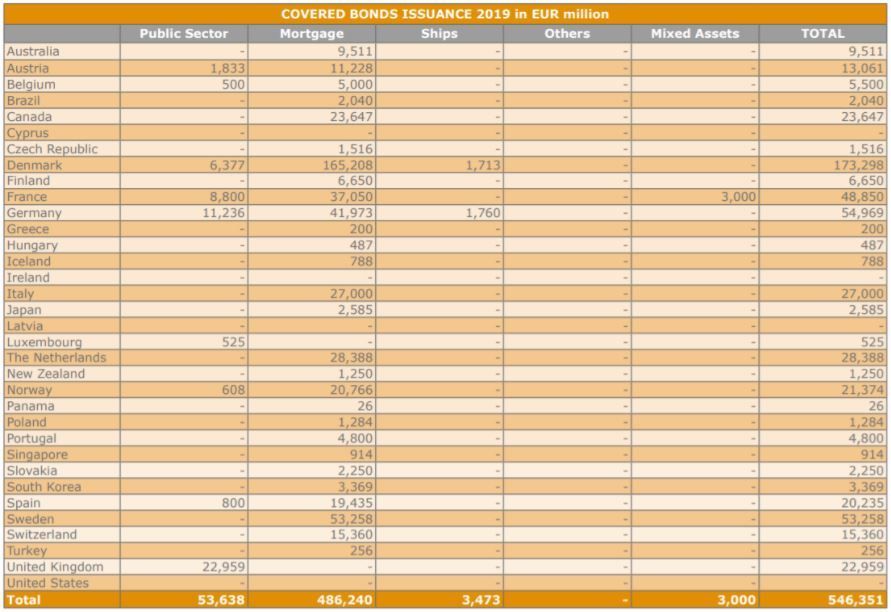

The tables below would show the trend of issuances in different jurisdictions in 2019 (latest available data):

Source: ECBC Factbook 2020[4]

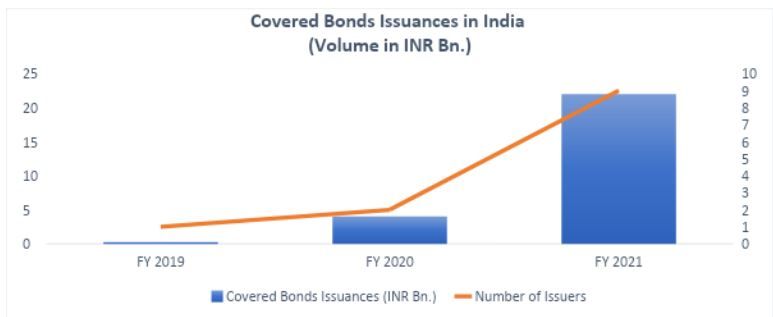

In India, the struggle to introduce covered bonds started way back in 2012, when the National Housing Bank formed a working group[5] to promote RMBS and covered bonds in the Indian housing finance market. Though the outcome of the working group resulted in some securitisation activity, however, nothing was seen on covered bonds.[6]

Some leading financial institutions attempted to issue covered bonds in the Indian market, but they failed. Lastly, FY 2019 witnessed the first instance of covered bonds, which was backed by vehicle loans.

In India, issuance of covered bonds witnessed a sharp growth in FY 2021, as the numbers increased to INR 22 Bn, as against INR 4 Bn in FY 2020. Even though the volume of issuances grew, the number of issuers failed to touch the two-digit mark. The issuances in FY 2021 came from 9 issuers, whereas, the issuances in FY 2020 were from only 2 issuers. Interestingly, all were non-banking financial companies, which is a stark contrast to the situation outside India.

The figure below shows the growth trajectory of covered bonds in India:

Source: ICRA, VKC Analysis

The growth in the FY 2021 was catapulted by the improved acceptance in Indian market in the second half of the year, given the uncertainty on the collections due to the pandemic, and the additional recourse on the issuer that the instrument offers, when compared to a traditional securitisation transaction.

Almost 75% of the issuances were done by issuers have ‘A’ rating, the following could be the reasons for such:

The Indian covered bonds market is however, significantly different from other jurisdictions. Traditionally, covered bonds are meant to be long term papers, however, in India, these are short to medium term papers. Traditionally covered bonds are backed by residential mortgage loans, however, in India the receivables mostly non-mortgages, gold loans and vehicle loans being the most popular asset classes.

In terms of investors too, the Indian market has shown differences. Globally, long term investors like pension funds and insurance companies are the most popular investor classes, however, in India, so far only Family Wealth Offices and High Net-worth Individuals have invested in covered bonds so far.

Another distinct feature of the Indian market is that a significant share of issuances carry market linked features, that is, the coupon rate varies with the market conditions and the issuers’ ability to meet the security cover requirements.

But the most important to note here is that unlike any other jurisdiction, covered bonds don’t have a legislative support in India. In Europe, the hotspot for covered bonds, most of the countries have legislations declaring covered bonds as a bankruptcy-remote instruments. In India, however, the bankruptcy-remoteness is achieved through product engineering by doing a legal sale of the cover pool to a separate trust, yet retaining the economic control in the hands of the issuer until happening of some pre-decided trigger events, and not with the help of any legislative support. In some cases, the legal sale is done upfront too.

Considering the importance and market acceptability of the instrument, rating agencies in India have laid down detailed rating methodologies for covered bonds[7].

Covered Bonds issued in India will not match most of the features of a traditional covered bond issued in Europe, however, the fact that finally the investors community in India has started recognizing it as an investment opportunity is very encouraging.

The real economics of covered bonds will come to the fore only when the market grows with different classes of investors, like the mutual funds, pension funds, insurance companies etc. in the demand side, which seems a bit far-fetched for now.

[1] A working group was constituted by the National Housing Bank to promote RMBS and Covered Bonds, the report of the working group can be viewed here: https://www.nhb.org.in/Whats_new/NHB%20Covered%20Bond%20Report.pdf

[2] In 2014-15, the Asian Development Bank appointed Vinod Kothari Consultants to conduct a Study on Covered Bonds and Alternate Financing Instruments for the Indian Housing Finance Segment

[3] https://www.icmagroup.org/resources/market-data/Market-Data-Dealogic/#14

[4] https://hypo.org/app/uploads/sites/3/2020/10/ECBC-Fact-Book-2020.pdf

[5] A working group was constituted by the National Housing Bank to promote RMBS and Covered Bonds, the report of the working group can be viewed here: https://www.nhb.org.in/Whats_new/NHB%20Covered%20Bond%20Report.pdf

[6] Vinod Kothari Consultants has been a strong advocate for a legal recognition of Covered Bonds in India. They were involved in the initiatives taken by the NHB to recognize Covered Bonds as a bankruptcy remote instrument in India.

[7] The rating methodology adopted by ICRA Ratings can be viewed here: https://www.icra.in/Rating/ShowMethodologyReport/?id=709

The rating methodology adopted by CRISIL can be viewed here: https://www.crisil.com/mnt/winshare/Ratings/SectorMethodology/MethodologyDocs/criteria/crisils%20criteria%20for%20rating%20covered%20bonds.pdf

—

Our Video on Covered Bonds can be viewed here <https://www.youtube.com/watch?v=XyoPcuzbys4>

Some resources on Covered Bonds can be accessed here –

Introduction to Covered Bonds by Vinod Kothari: https://vinodkothari.com/2015/01/introduction-to-covered-bonds-by-vinod-kothari/

The Name is Bond. Covered Bond. By Vinod Kothari: http://www.vinodkothari.com/wp-content/uploads/covered-bonds-article-by-vinod-kothari.pdf

NHB’s Working Paper on Covered Bonds: https://www.nhb.org.in/Whats_new/NHB%20Covered%20Bond%20Report.pdf

Do’s and don’ts to be ensured by listed companies

Updated as on September 28, 2023 , pursuant to the SEBI LODR (Second Amendment) Regulations, 2023

In order to disseminate information regarding performance of the company, its future prospects etc. listed companies usually conduct gatherings of analysts/investors after dissemination of quarterly results or atleast once in a year. Such meets generally include conference calls or meeting with group of investors or one-to-one meet or calls with investors or analysts, including those in the nature of walk-in. The idea behind conducting such meets is to provide transparency for the company’s performance figures, to address the queries of the analysts/investors and to ensure that the company’s information is available to the stakeholders. However, the risk of information asymmetry in such meets or gatherings is very inherent.

While the regulatory framework of SEBI i.e. SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘Listing Regulations’) provided for disclosure of adequate and timely information to enable investors to track the performance of a company including the information pertaining to occurrence of investors meet/conference call with analysts, however, several inconsistencies were observed in the disclosures made by the companies. For instance, some entities were not divulging the details of what transpired in such investors’ meetings and were merely disclosing the limited presentations w.r.t. the meetings. As such, minority shareholders, who did not attend these meetings, were not privy to the information shared with a select group of investors, thereby creating information asymmetry among different classes of shareholders.

Realizing this, SEBI, on November 20, 2020, came up with the Consultation Paper and recommended enhanced disclosure requirements w.r.t. post earning calls and one-to-one meets. Our write-up analyzing the said consultation paper can be viewed here.

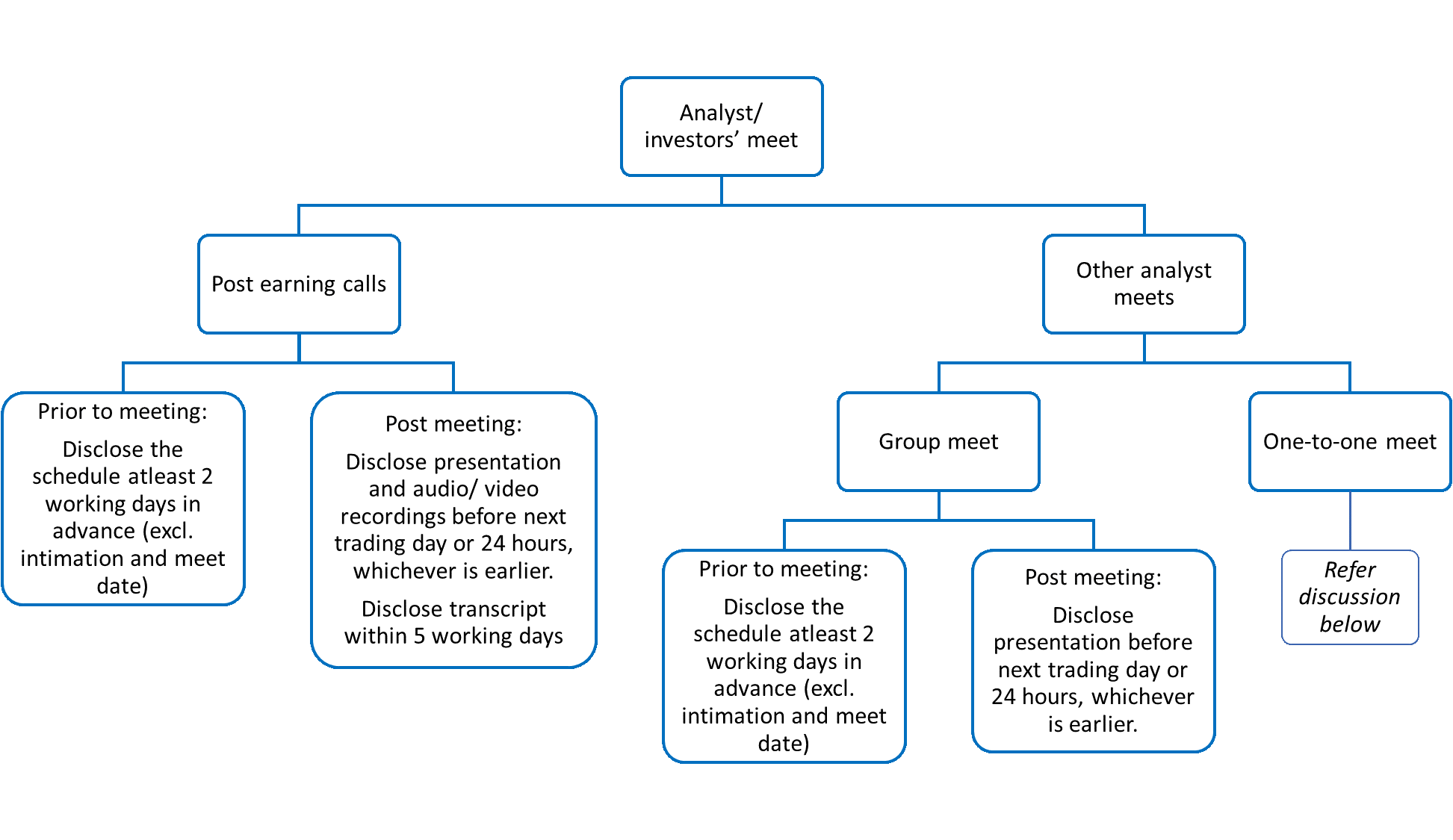

Later, vide notification dated May 05, 2021, SEBI enhanced the disclosure requirements w.r.t. Investors’/ Analysts’ meet. In this article, the author has made an attempt to discuss the changes made in the disclosure requirements w.r.t. analyst meet step by step.

On May 05, 2021, SEBI amended the Listing Regulations which inter alia, covered analyst meet. Pursuant to the said amendment, the companies are required to include enhanced disclosure requirements with respect to analyst/ investors meets so as to avoid selective disclosure and information asymmetry and to ensure market integrity and to safeguard the interest of investors. The said amendments were voluntary for FY 2021-22, and became mandatory from FY 2022-23. The synopsis of the amendment is provided below:

Figure 1: Disclosure requirement for analyst meet

In respect of one-to-one meet, there are no explicit disclosure requirements as such. However, considering the intent of the Listing Regulations and SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’), the following things are explicitly clear:

Regulation 8 of PIT Regulations mandates every listed company to frame a code of practices and procedures for fair disclosure of UPSI in line with the principles set out in Schedule A to PIT Regulations. Para 6 of Schedule A requires the company to ensure that information shared with analysts and research personnel is not UPSI. Para 7 provides for developing best practices to make transcripts or records of proceedings of meetings with analysts and other investor relations conferences on the official website to ensure official confirmation and documentation of disclosures made.

The PIT Regulations do not distinguish between group meets and one-to-one meets. It requires the company to record such meets and develop best practices to disclose the same on its website. The practice of recording the meet also safeguards the company officials participating in the meeting from any possible allegation of having divulged UPSI.

The PIT Regulations prohibit sharing of UPSI in any manner to any person including analysts/ investors and require the companies to take all required steps to ensure the same. Considering the same, the fact whether it is a group meet/ call or otherwise or whether such meet/ call was organized by the company itself or not, becomes irrelevant and the prohibition shall apply in all cases.

Therefore, there is a remote chance of sharing such UPSI until and unless the same is as per the provisions of code of fair disclosure framed by the company. Accordingly, if any UPSI is shared, legitimately in terms of the said code or otherwise, the entity will have to disclose the audio/ video recordings or the transcripts of such meeting to the stock exchange promptly.

The amendment in the Listing Regulations came up with various interpretations and ambiguities w.r.t. disclosure requirements. We have discussed such anomalies in our previous article which can be viewed here.

In order to clear the ambiguities w.r.t the disclosure requirements, BSE, vide circular dated 29th June, 2021 and July 29, 2022, provided further clarifications and recommendations. In this article, we have tried to provide step-by-step guide for disclosure on analyst meets and post earning calls. Further, we have also provided the do’s and don’ts to be ensured by the companies.

In order to comply with the provisions of Listing Regulations in letter and spirit, the companies are required to ensure that it makes timely disclosure to stock exchanges and on their own website. The compliance requirement as per the amended provisions w.r.t. analysts/ investors meet are jotted down below:

| Sr. No. | Cases | Disclose what? | By When? | Other Points to be ensured |

| 1. | Post earning calls/ Quarterly calls, by whatever name called (after disclosure of quarterly financial results) | Schedule of such meeting | Atleast 2 working days in advance (excluding the date of intimation and date of the meet). | Mandatory only for group meets. |

| Presentation and the audio/ video recordings of such meeting | Before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier. | Mandatory for both group meets and one to one meets.To be disclosed whether conducted by a company or any other entity.To be hosted on the website of the company for minimum 5 years and thereafter as per the archival policy of the company. To be disclosed simultaneously to the stock exchange. | ||

| Transcripts of such meeting | Within 5 working days of conclusion of the meet. | Mandatory for both group meets and one-to-one meets.To be disclosed whether conducted by a company or any other entity.To be hosted on the website of the company and preserved permanently.To be disclosed simultaneously to the stock exchange. | ||

| 2. | Other Analysts/ Investors meets | Schedule of such meeting | Atleast 2 working days in advance (excluding the date of intimation and date of the meet) | Mandatory only for group meets. |

| Presentation made in such meeting | Before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier.. | Mandatory only for group meets.To be disclosed on the website of the company, whether conducted by company or any other entity.To be disclosed simultaneously to the stock exchange. | ||

| In case any UPSI is shared | Audio/video recordings or transcripts of such meeting | Promptly | Applicable to both group as well as one-to-one meets.To be disclosed on the website of the company, whether conducted by a company or any other entity.To be disclosed simultaneously to the stock exchange. |

While making disclosure of schedules, the company may also provide the details pertaining to the meet/ call, mode of attending, details pertaining to registrations, disclaimers/ note to complete/ ease registration/ attending the call, details regarding specific platform requirements, if any, inclusions/ exclusions of audience/ participants if any, etc.

Further, a disclaimer or a confirmation may be added in the intimation stating that ‘Company will be referring to publicly available documents for discussions’ or ‘No UPSI is proposed to be shared during the meeting / call’. This will create confidence amongst the investors and will maintain sanctity of the meet / call.

While disclosing the transcripts of the meet/ call, the companies may also consider providing the list of attendees and record the dialogues, Q&As and assents and dissents of the analysts/ investors. Further, a confirmation may be added in the disclosure that no unpublished price sensitive information was shared/ discussed in the meeting / call.

The companies will be required to observe some crucial points while scheduling or attending analysts’/ investors’ meet, conference calls, post earning calls etc. Briefly, the following are the do’s and don’ts:

| Sr. No. | Do’s | Don’ts |

| 1. | Always conduct scheduled meets. | Avoid unscheduled meets. |

| 2. | Always schedule group meets. | Avoid scheduling one-to-one meet. |

| 3. | Upload the schedule of group meets/ calls on the website atleast 2 working days in advance (excluding the date of intimation and date of the meet) and also simultaneously submit the same with the stock exchange. | Do not forget to upload and send the schedule on the website and to the stock exchanges, respectively beyond the prescribed time. |

| 4. | Upload the presentation made to analysts/ investors in the scheduled group meet on the website promptly before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier and also simultaneously submit the same with the stock exchange. | Do not forget to upload and send the schedule on the website and to SE, respectively beyond the prescribed time. |

| 5. | Ensure to make audio and video recording of the post earnings/ quarterly calls, whether conducted physically or through digital means, either conducted by company or any other entity including one- to-one meets. | Do not avoid making audio/video recording of such calls irrespective the same was conducted by the company itself or by any other entity. |

| 6. | Ensure transcripts of the post earnings/quarterly calls, whether conducted physically or through digital means, either conducted by company or any other entity including one-to-one meets. | Do not avoid making transcripts of the proceedings of such calls irrespective the same was conducted by the company itself or by any other entity. |

| 7. | Ensure that the information shared with the investors is already available in the public domain. | Do not share UPSI with the investors. |

| 8. | Maintain a silence period, if any, as provided in the code of fair disclosure framed by the entity. | Discourage any sort of meets either group meet or one-to-one meets (including walk-in investors) during silence period. |

| 9. | Upload all audio/video recordings and presentation of the post earning/ quarterly calls on the website of the company within 24 hours of conclusion of such calls or next trading day, whichever is earlier. | Avoid uploading audio/video recording beyond the prescribed time. |

| 10. | Upload all transcripts of the post earning/ quarterly calls on the website of the Company within 5 working days of conclusion of such calls. | Avoid uploading transcripts of the post earning/ quarterly calls on the website of the company after 5 working days of conclusion of calls. |

| 11. | Simultaneous to uploading audio/video recording and transcripts on the website of the company, submit the same to the recognized stock exchange. | Do not forget to send audio/video recording and transcripts of the meets to the recognized stock exchange |

| 12. | Preserve the disclosures made on the website of the Company (a) Audio/video recording- for minimum 5 years and thereafter as per archival policy of the company; (b) Transcripts: permanently | Do not avoid preserving of audio/video recording and transcripts of the meets |

The amendment in Listing Regulations and guidance note by the stock exchanges give us the clear view that the companies are required to make timely disclosure of audio/ video recordings, transcripts of post earning calls and only presentations of analyst meet to the stock exchange. Even though this seems to be the compliance burden on part of the listed companies which are already pressed with various disclosure requirements, this step is surely a welcome move as it will help the watchdog of capital markets to curb insider trading and information asymmetry.

Our other article on similar topics can be read here – https://vinodkothari.com/2020/11/sebi-proposes-enhanced-disclosures-for-meetings-with-analyst-investors-etc/

Our Podcast on the topic: https://open.spotify.com/episode/2oVRo2iEOV7cVVqYwcqb2c?si=b860b48d6f924ad6&nd=1

Our Resource Centre on LODR:

Sale and Leaseback transaction. 2

Unlocking value, the hidden value of asset 2

Taxation of SLB transactions. 3

Example of GST Calculations on Sale and Leasebacks. 6

Accounting of Sale and leasebacks. 7

Transfer of asset does not qualify as sale. 10

Transfer of asset qualifies as sale. 10

Sale at a discount or premium.. 10

Example of Sale and Leaseback Accounting under Ind AS 109. 11

Accounting Entries at Inception. 12

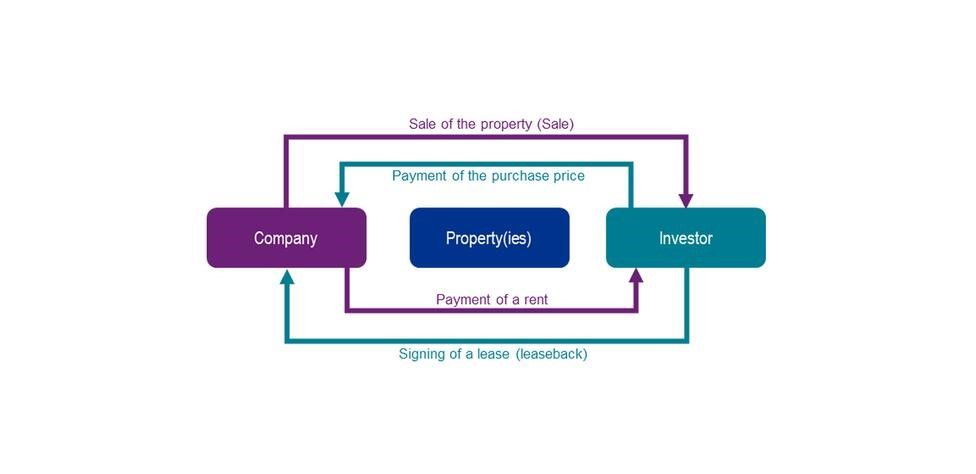

A Sale and Leaseback (SLB) is a special case of application of leasing technique. Lease is a preferred mode of using the asset without having to own it. In case of leases, the lessee does not own the asset but acquires the right to use the asset for a specified period of time and pays for the usage.

SLB is a simple financial transaction which allows selling an asset and then taking it back on lease. The transaction thus allows a seller to be able to use the asset and not own it, at the same time releasing the capital blocked by the asset.

SLB allows the lessee to detach itself with legal ownership yet continuing to use the asset as well. In effect there is no movement of asset however on paper there is a change in the title of the asset.

Sale and Leaseback transactions are globally common in the Real estate investment trusts (REITs) and Aviation industry.

As is evident from the mechanics of SLB above, SLB results in taking the asset off the books of the lessee and results in upfront cash which could be used for paying off existing liabilities. Hence this does not impact the existing lines of credit the lessee may be availing.

SLB can help entities raise finance for an amount equal to fair market value of the asset which may be significantly higher than its book value. Though there might be taxation challenges attached to it in Indian context. Nevertheless, SLB may bring about a financial advantage as well wherein a high-cost debt can be substituted with a low-cost lease liability.

Most of the assets considered for SLB have been used by the lessee for a substantial period of time and the value of the physical assets may be insignificant. Hence SLB is sometimes referred to as junk financing.

SLB may sometimes lead to tax benefits as well (we shall see this in detail in the sections below). This has been one of the major drivers of SLB transactions in India and has its own downsides as well. One of the major pitfalls to SLB is the danger of excess leveraging; the lessee may tend to overvalue the asset. Considering that SLB is a mode of asset-backed lending but the asset has may not have much value and the lessee may exercise discretion on the application of funds poses threat of misuse of the product.

The legal validity of SLB was discussed by the U.S Supreme Court in the landmark ruling of Frank Lyon and Company[1]. In Frank Lyon’s case the bank took the building on SLB. Under the lease terms the bank was liable to pay rentals periodically and had the option to purchase the building at various times at a consideration based on its outstanding balance. The bank took possession of the building in the year it was completed and the lessor claimed deductions on depreciation, interest on construction loan, expenses related to sale and lease back and accrued the rent from the bank.

The Commissioner of Internal Revenue denied the claims of the petitioner on the grounds that the petitioner was not the owner of the building and the sale and leaseback was a mere financing transaction. The Hon’ble Court held that –

Where, as here, there is a genuine multiple-party transaction with economic substance that is compelled or encouraged by business or regulatory realities, that is imbued with tax-independent considerations, and that is not shaped solely by tax-avoidance features to which meaningless labels are attached, the Government should honor the allocation of rights and duties effectuated by the parties; so long as the lessor retains significant and genuine attributes of the traditional lessor status, the form of the transaction adopted by the parties governs for tax purposes.

The fundamental principle is that the Court should be concerned with the real substance of the transaction rather than the form of the same. If there are reasons to believe that the form of the transaction and its real substance are not aligned, the Court must not be simply concerned by the form of the transaction nor by the nomenclature that the parties have given to it.

In India too, the legality of SLB transactions have been questioned in several cases; sometimes the transactions have come out clean while in some cases, SLBs were considered an accounting gimmick.

The legality of SLB transactions and analysis of various judicial pronouncements on the same, have been discussed in detail in our write up “Understanding Sale and leaseback”

Tax aspects specifically direct tax acts as a major motivation behind such transactions, SLB provides a creative playground for finance professionals to structure transactions in a manner that can lead to substantial benefit to the entity, and taxation acts as a major tool at their disposal.

Though tax benefits have been a motivator for SLB transaction, the same has also been the reason for near wipe-out of SLB from Indian markets.

During the 1996-98 period one of the most infamous cases was the sale and leaseback of electric meters by state electricity boards (SEBs). For SEBs it made perfect sense as it amounted to cheap borrowing by the cash starved SEBs who had practically no other source of borrowing.

For leasing companies and others looking for a tax break, it was a perfect deal as there was 100% write off in case of assets costing Rs 5000 or less. Thus, an electric meter will qualify for 100% deduction. Several SEBs had undertaken such transactions in those days. Obvious enough the sole motive was tax deduction no one would care about the value, quality, existence etc of the meters. In some cases, the asset was bought on 30th March to be used only for a day, assets revalued heavily at the time of sale to leasing companies etc. Lease of non-existing assets such as electric meters, computers, glass bottles, tools, etc, lure of depreciation allowances caused the tax authorities to come down hard on sale and leaseback transactions calling them tax evading transactions. The whole fiasco of such sham transactions resulted in leasing going off the market completely. The burns of the past continue to linger even after a decade and half since SLB transactions were completely written off.

The most significant consideration in lease transactions is the depreciation claim. For tax purposes, depreciation is calculated on the block of the assets and not on the written down value of each asset separately.

Section 2(11) of the Income Tax Act, 1961 (IT Act) defines block of assets to mean

“”block of assets” means a group of assets falling within a class of assets comprising—

(a) tangible assets, being buildings, machinery, plant or furniture;

(b) intangible assets, being know-how, patents, copyrights, trade-marks, licences, franchises or any other business or commercial rights of similar nature, in respect of which the same percentage of depreciation is prescribed.”

The sale proceeds of the assets sold are deducted from the written down value of the block. In case of SLB transaction, assets are sold at higher than written down value, and the gain made on such a sale results in reduction in depreciable value of the block of assets. The reduction in depreciation will be allowed over a number of years. Similar would be the case in case the asset was sold at less than written down value, sale consideration would be reduced from the block of the assets.

Once the asset is sold and taken off the books of the lessee, the lessee is able to account for an immediate accounting profit without having to pay tax on it instantly. As under the block concept of depreciation, when the lessee sells the capital assets, the sale proceeds including the profits on sale are allowed to be deducted from the block of assets and hence there is no immediate tax on the accounting profits.

Also, typically the asset is recorded on historical costs which may be lower than the intrinsic value of the asset. SLB sometimes allows the entities to unlock the appreciation in value. However, it is not always necessary that the asset would have appreciated value. In some cases, the asset may have become junk completely.

To avoid the same revenue has introduced following provisions in the IT act, in order to restrict undue benefits being passed by use of sham SLB transactions:

Section 43 (1) provides for treatment of sale and lease back transactions for tax purposes, the relevant extracts are reproduced below –

“Explanation 3.—Where, before the date of acquisition by the assessee, the assets were at any time used by any other person for the purposes of his business or profession and the Assessing Officer is satisfied that the main purpose of the transfer of such assets, directly or indirectly to the assessee, was the reduction of a liability to income-tax (by claiming depreciation with reference to an enhanced cost), the actual cost to the assessee shall be such an amount as the Assessing Officer may, with the previous approval of the Joint Commissioner, determine having regard to all the circumstances of the case.”

“Explanation 4A.—Where before the date of acquisition by the assessee (hereinafter referred to as the first mentioned person), the assets were at any time used by any other person (hereinafter referred to as the second mentioned person) for the purposes of his business or profession and depreciation allowance has been claimed in respect of such assets in the case of the second mentioned person and such person acquires on lease, hire or otherwise assets from the first mentioned person, then, notwithstanding anything contained in Explanation 3, the actual cost of the transferred assets, in the case of first mentioned person, shall be the same as the written down value of the said assets at the time of transfer thereof by the second mentioned person.

Explanation 3 and 4A of Section 43 (1) restricts the consideration at which the lessor purchases the assets to written down value of the asset as appearing in the books of the lessee before it was sold and taken back on lease. The explanation explicitly states that the sale value for such sale and lease back transactions will be ignored and depreciation will be allowed on the first seller’s depreciated value. Take, for instance, A purchased machinery for Rs. 10 crores from B, though the WDV in the books of B is Rs. 2 crores. A can claim depreciation on Rs. 2 crores and not on Rs. 10 crores.

The said provisions removes any motivation for the lessor to carryout transactions at inflated values. Hence preventing junk financing to enter into SLB transactions.

Pre-GST indirect taxation regime acted as a major road block in the development of leasing industry as a whole, the legal differentiation as well as non-availability of credit among central and state taxes made leasing transactions costly.

Introduction of GST is playing a key role in development of leasing industry, from a stage where it had nearly become extinct. We have further discussed GST implications on leasing.

The first leg of the transaction would involve sale of Assets by lessee to lessor.

In terms of section 7(1)(a) “all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business;”

The taxability under GST arises on the event of supply accordingly the sale of capital assets for a consideration would fall under the ambit of supply and accordingly GST shall be levied.

The second part of transaction would lease back that is when the asset is leased back from buyer -lessor to seller lessee. The leaseback would be subject to GST like any other lease transaction.

The term lease has not been defined anywhere in GST Act or Rules. To classify a lease transaction as either supply of goods or supply of service, we have to refer Schedule II of the CGST Act, 2017 where in clear guidelines for classification of a transaction as either “supply of goods” or “supply of services” has been enumerated, based on certain parameters: –

Undoubtedly, the SLBs do not involve movement of goods, the seller lessee continuous to be in possession of leased asset even after the sale. Hence, In the case of such sale, there is no physical movement of the asset from the premises of the lessee to the premises of the lessor. The ownership gets transferred in the premise of the lessee.

In terms of Section 10(1)(c) of the IGST Act, the place of supply of goods where the supply does not involve movement of the said goods whether by the supplier or the recipient shall be the location of such goods at the time of delivery to the recipient. Accordingly, the place of supply in this case will be same as the location of the supplier. Accordingly, the sale of the asset will be considered as an intra-state supply as per Section 8 of the IGST Act and will be subjected to CGST + SGST.

Applications of GST on disposal of capital assets is one of the major deterring factors of in SLBs. Section 18(6) of the CGST Act,2017 state that:

“In case of supply of capital goods or plant and machinery, on which input tax credit has been taken, the registered person shall pay an amount equal to the input tax credit taken on the said capital goods or plant and machinery reduced by such percentage points as may be prescribed or the tax on the transaction value of such capital goods or plant and machinery determined under section 15, whichever is higher:”

Entry no. (6) Of Rule 44 of CGST Rules, 2017: Manner of Reversal of ITC under Special Circumstances which reads as under: –

“The amount of input tax credit for the purposes of sub-section (6) of section 18 relating to capital goods shall be determined in the same manner as specified in clause (b) of sub-rule (1) and the amount shall be determined separately for input tax credit of central tax, State tax, Union territory tax and integrated tax:”

“……………..Clause (b) of sub rule 1 of same rules states that :

(b) for capital goods held in stock, the input tax credit involved in the remaining useful life in months shall be computed on pro-rata basis, taking the useful life as five years………….”

Generally, the lessor procures the capital Assets at WDV due to Income tax Act implication. In that case WDV as per Income tax act would be the transaction value.

Let’s consider a numerical example: an Entity A enters into SLB arrangement with an Entity B. A sells its machinery to B for Rs. 5,00,000/- as on 31st May 2021. The entity had purchased the asset for Rs. 6,00,000/- as on 31st March 2019.

B then leases back the asset to A for a yearly rental of Rs, 1,00,000/- for 3 years term with a purchase option at the end of 4th year at Rs. 2,50,000. (Assumed to be exercised)

(GST @ 18%)

On disposal asset, GST will be charged on the selling price of the asset. However, the amount to be deposited to the government with respect to this sale transaction shall be higher of the following:

Portion of ITC availed on the asset, attributable to the period during which the transferor used the asset:

6,00,000 * 18% * (5% * 8) = 43200

Remaining ITC = (6,00,000 * 18%) – 43200 = 64800

GST on the selling price = 500000 * 18% = 90000

Therefore, GST to be paid to the government is 90000, that is higher of the two amounts discussed above.

As mentioned above GST shall be chargeable to lease rental, at the rate similar to that charged on acquisition of leased asset. Accordingly, Entity B shall charge GST on rentals for an amount of Rs. 18,000/- (Rs. 1,00,000/- * 18%).

Further GST shall also be charged on sale of asset at the end of lease tenure for an amount of Rs. 45,000/-(2,50,000*18%).

IAS 17 covered the accounting for a sale and leaseback transaction in considerable detail but only from the perspective of the seller-lessee.

As Ind AS 116/IFRS 16 has withdrawn the concepts of operating leases and finance leases from lessee accounting, the accounting requirement that the seller-lessee must apply to a sale and leaseback is more straight forward.

The graphic below shows how SLB transactions should be accounted for:

IFRS 16/Ind AS 116 state that

“ An entity shall apply the requirements for determining when a performance obligation is satisfied in Ind AS 115 to determine whether the transfer of an asset is accounted for as a sale of that asset.”

Accordingly, when a seller-lessee has undertaken a sale and lease back transaction with a buyer-lessor, both the seller-lessee and the buyer-lessor must first determine whether the transfer qualifies as a sale. This determination is based on the requirements for satisfying a performance obligation in IFRS 15/Ind AS 115 – “Revenue from Contracts with Customers”.

The accounting treatment will vary depending on whether or not the transfer qualifies as a sale.

The para 38 of Ind AS 115/IFRS 15- Performance obligations satisfied at a point in time, provides ample guidance on determining whether the performance obligation is satisfied.

The para states that:

“If a performance obligation is not satisfied over time in accordance with paragraphs 35– 37, an entity satisfies the performance obligation at a point in time. To determine the point in time at which a customer obtains control of a promised asset and the entity satisfies a performance obligation, the entity shall consider the requirements for control in paragraphs 31–34. In addition, an entity shall consider indicators of the transfer of control, which include, but are not limited to, the following:

(a) The entity has a present right to payment for the asset—if a customer is presently obliged to pay for an asset, then that may indicate that the customer has obtained the ability to direct the use of, and obtain substantially all of the remaining benefits from, the asset in exchange.

(b) The customer has legal title to the asset—legal title may indicate which party to a contract has the ability to direct the use of, and obtain substantially all of the remaining benefits from, an asset or to restrict the access of other entities to those benefits. Therefore, the transfer of legal title of an asset may indicate that the customer has obtained control of the asset. If an entity retains legal title solely as protection against the customer’s failure to pay, those rights of the entity would not preclude the customer from obtaining control of an asset.

(c) The entity has transferred physical possession of the asset—the customer’s physical possession of an asset may indicate that the customer has the ability to direct the use of, and obtain substantially all of the remaining benefits from, the asset or to restrict the access of other entities to those benefits. However, physical possession may not coincide with control of an asset. For example, in some repurchase agreements and in some consignment arrangements, a customer or consignee may have physical possession of an asset that the entity controls. Conversely, in some bill-and-hold arrangements, the entity may have physical possession of an asset that the customer controls. Paragraphs B64–B76, B77–B78 and B79–B82 provide guidance on accounting for repurchase agreements, consignment arrangements and bill-and-hold arrangements, respectively.

(d) The customer has the significant risks and rewards of ownership of the asset—the transfer of the significant risks and rewards of ownership of an asset to the customer may indicate that the customer has obtained the ability to direct the use of, and obtain substantially all of the remaining benefits from, the asset. However, when evaluating the risks and rewards of ownership of a promised asset, an entity shall exclude any risks that give rise to a separate performance obligation in addition to the performance obligation to transfer the asset. For example, an entity may have transferred control of an asset to a customer but not yet satisfied an additional performance obligation to provide maintenance services related to the transferred asset.

(e) The customer has accepted the asset—the customer’s acceptance of an asset may indicate that it has obtained the ability to direct the use of, and obtain substantially all of the remaining benefits from, the asset. To evaluate the effect of a contractual customer acceptance clause on when control of an asset is transferred, an entity shall consider the guidance in paragraphs B83–B86.”

It shall be noted that no single criteria can be taken as a determining factor for concluding that sale has taken place. Each criterion should be individually assessed every case. Needless to say, substance of the transaction should be adjudge based on principles set.

The criteria set out in the para 38 specified above can be summarised as follows:

If the transfer does not qualify as a sale the parties account for it as a financing transaction. This means that:

Where the transfer qualifies as sale, there can be further two situations:

If the transfer qualifies as a sale and is on fair value basis the seller-lessee effectively splits the previous carrying amount of the underlying asset into:

The seller-lessee recognises a portion of the total gain or loss on the sale. The amount recognised is calculated by splitting the total gain or loss into:

The leaseback itself is then accounted for under the lessee accounting model.

The buyer-lessor accounts for the purchase in accordance with the applicable standards (eg IAS 16 ‘Property, Plant and Equipment’ if the asset is property, plant or equipment or IAS 40 ‘Investment Property’ if the property is investment property). The lease is then accounted for as either a finance lease or an operating lease using IFRS 16’s lessor accounting requirements.

The accounting methodology shall remain the same, However, Adjustments would be required to provide for the discounted or premium price.

These adjustments would be as follows:

A sample spreadsheet calculations for the below example can be accessed here

| Particular | Amount | Remarks |

| Sale considerations | ₹ 10,00,000.00 | |

| Carrying Amount | ₹ 5,00,000.00 | |

| Term | 15 | year |

| Rentals/year | ₹ 80,000.00 | year |

| Fair Value of Building | ₹ 9,00,000.00 | |

| Incremental borrowing rate | 10% | |

| PV of rentals | ₹ 6,08,486.36 | |

| Additional Financing | ₹ 1,00,000.00 | Sale Consideration – Fair Value |

| Payments towards Lease Rentals | ₹ 5,08,486.36 | PV of Rentals – Additional Financing |

| Ratio of PV of rentals and Payment towards lease Rentals |

16% | |

| Yearly payments towards Add. Financing | ₹ 13,147.38 | Rental X Ratio |

| Yearly payments towards Lease Rental | ₹ 66,852.62 | Rental – Payment toward Add. Fin. |

| ROU of Asset | ₹ 2,82,492.42 | Carrying Amount X [Payments towards Lease Rentals/Fair Value of Building] |

| Total Gain on sale | ₹ 4,00,000.00 | Fair Value – Carrying Amount |

| Gain recognised Upfront | ₹ 1,74,006.06 | Total Gain X [(Fair Value of Building-Payments towards Lease Rentals) /Fair Value of Building] |

| NPV | NPV | |

| ₹ 5,08,486.36 | ₹ 1,00,000.00 | |

| Year | Lease Rentals | Additional Financing |

| 0 | ||

| 1 | ₹ 66,852.62 | ₹ 13,147.38 |

| 2 | ₹ 66,852.62 | ₹ 13,147.38 |

| 3 | ₹ 66,852.62 | ₹ 13,147.38 |

| 4 | ₹ 66,852.62 | ₹ 13,147.38 |

| 5 | ₹ 66,852.62 | ₹ 13,147.38 |

| 6 | ₹ 66,852.62 | ₹ 13,147.38 |

| 7 | ₹ 66,852.62 | ₹ 13,147.38 |

| 8 | ₹ 66,852.62 | ₹ 13,147.38 |

| 9 | ₹ 66,852.62 | ₹ 13,147.38 |

| 10 | ₹ 66,852.62 | ₹ 13,147.38 |

| 11 | ₹ 66,852.62 | ₹ 13,147.38 |

| 12 | ₹ 66,852.62 | ₹ 13,147.38 |

| 13 | ₹ 66,852.62 | ₹ 13,147.38 |

| 14 | ₹ 66,852.62 | ₹ 13,147.38 |

| 15 | ₹ 66,852.62 | ₹ 13,147.38 |

| Buyer-Lessor | ||

| Building | ₹ 9,00,000.00 | |

| Financial Asset | ₹ 1,00,000.00 | |

| Bank | ₹ 10,00,000.00 | |

| *Lease accounted as per Finance or operating lease accounting | ||

| Seller-Lessee | ||

| Bank | ₹ 10,00,000.00 | |

| ROU | ₹ 2,82,492.42 | |

| Building | ₹ 5,00,000.00 | |

| Financial Liability | ₹ 6,08,486.36 | |

| Gains on Asset Transfer | ₹ 1,74,006.06 | |

[1] 435 U.S. 561 (1978)

Sharon Pinto, Manager, corplaw@vinodkothari.com

Proxy advisors are entities that undertake research on corporate governance norms and practices followed across different corporates. They formulate their policies based on their research and appropriately established benchmarks. The proxy advisory firms play a role in strengthening the corporate governance as investor clients access the reports and recommendation of the said advisory firms while forming their opinions. As investors due to their vast shareholding may not be privy to the working of the company, they may rely on the analysis done by the proxy advisors and their recommendations. We have discussed the scope of guidelines issued by proxy advisors in a separate article[1].

While such reports and guidelines as mentioned above can act as a guidance for the investors to take a sound decision, the legal standing of the report can be considered a hiccup in the said process as the same does not obtain regulatory approval. We have discussed the scope and legal validity of such guidelines in a separate article.[2]

One such guideline has been issued w.r.t. re-appointment of Independent Directors under Section 149 (10) of the Companies Act, 2013 (‘the Act’). The said contention has been a question of interpretation with different practices being followed by various companies. In this article we have discussed the interpretation of the said provision while stating the process of re-appointment of Independent Directors (‘IDs’).

Section 149 (6) of the Act read with Rule 5 of the Companies (Appointment & Qualification of Director) Rules, 2014 states the criteria that shall determine the independence of the director proposed to be appointed. In case of an entity with its specified securities listed on the stock exchange, the conditions set forth by Regulation 16 (1) (b) of SEBI (Listing Obligation and Disclosure Requirements) Regulations (‘SEBI Regulations’) shall also be fulfilled in order to be eligible for appointment as an ID. The said provisions under the Act and SEBI Regulations entail certain pecuniary limits which are necessary to ascertain any monetary relationship of the director with the company, which may affect their independence. As the given criteria is a pre-requisite at the time of appointment of a director, it shall also be mandatory to be fulfilled at the time of re-appointment. Thus, if an ID continues to be eligible as per the said conditions, they shall be proposed to be re-appointed for a second term in the company.

Pursuant to the SEBI (Listing Obligation and Disclosure Requirements), 2021 (Third Amendment Regulations), the criteria of independence prescribed under Regulation 16 (1) (b) has been revised aligning the same with the provisions of the Act. However, while the Act provides for the period of 2 immediately preceding financial years for determining whether the person or his relatives have any material pecuniary relationship with the company, the revised SEBI Regulations now prescribe for a period of 3 immediately preceding financial years for determination of the same.

Further, the conditions prescribed under the Act relating to holding of any interest or security, indebtedness, any guarantee or security provided in connection to indebtedness of a third person or any other pecuniary relationship with the company or its holding or subsidiary or associate company have also been inserted in the SEBI Regulations, which provide for stricter period of compliance of the said conditions. While, the relatives may be employees in the entities stated above, they are prohibited from holding the position of a KMP. As the criteria of independence is to be observed even in the case of re-appointment, these conditions will ensure the independence of the ID.

In addition to the criteria of independence, the existing IDs of the company are required to abide by the code of conduct prescribed under Schedule IV of the Act. Any breach of the code by the directors shall make them ineligible for continuing in the position of ID of the company.

The re-appointment of an existing director for a second term, in addition with the establishment of their independence shall also be subject to performance evaluation. The Act under Section 178 (2) states that the Nomination and Remuneration Committee (‘NRC’) of the company shall formulate a criteria for determining the qualifications, positive attributes, independence for appointment of a director. Further the committee shall also establish a criteria for the evaluation of performance of the Board as well as individual directors. Thus on the basis of such performance evaluation and establishment of independence and possession of requisite skills by the director, the NRC shall recommend the appointment or in case of an existing director, re-appointment of the said director to the Board.

SEBI[3] has detailed an elaborated process to be followed by NRC for selection of ID, including more transparent and enhanced disclosures regarding the skills required for appointment as an ID and how the proposed candidate fits into that skillset. As per the Third Amendment Regulations, the said additional disclosures stating the skills and capabilities required for the role and the manner in which the proposed person meets the requirements, will be required to be provided in the notice in the case of re-appointment of an ID. Thus, NRC of the company will be required to undertake an assessment determining whether the person proposed to be re-appointed as the ID possesses the skills required for the position in addition to performance evaluation even in the case of re-appointment.

SEBI under Regulation 17 (10) of the SEBI Regulations has stated that the performance evaluation of the IDs shall be done by the entire Board of Directors where the concerned ID shall not participate in the said discussion. The Board shall consider performance of the director in addition to fulfilment of independence criteria similar to the provisions stipulated under Companies Act, 2013 as discussed above. Thus the director proposed to be re-appointed has to satisfy the afore-mentioned dual conditions.

Section 149 (10) of the Act has specified the process of reappointment of an ID. It states that a director shall be eligible for re-appointment by passing of a special resolution. Thus we may infer that in order to be re-appointed as an ID, a special resolution is required to be passed. Regulation 17 (11) of SEBI Regulations provides for stating recommendation of the Board for every for every special item of business in the explanatory statement annexed to the notice. As discussed above, Board on the basis of performance evaluation carried out and the recommendation of the NRC shall recommend the re-appointment of the ID. Criteria of independence being a pre-requisite for such re-appointment as established herein, the director shall be considered as an additional independent director until approval of shareholders is obtained at the general meeting of the Company.

Further, SEBI vide its consultation paper on Independent Directors[4] had proposed prior approval of shareholders for appointment and re-appointment of IDs, while stating that the existing procedure entails proposal of candidate by the NRC and appointment/re-appointment by Board which is subsequently approved by shareholders by an ordinary resolution in case of appointment whereas special resolution in case of re-appointment. Accordingly, seeking prior approval of shareholders is not a pre-requisite at present.

After end of first tenure of the ID, the office of director shall cease. Accordingly, Board will approve appointment as additional director till ensuing AGM and propose re-appointment as an ID for second term of upto 5 consecutive years.

As discussed above, re-appointment after the end of the tenure is required to be considered akin to fresh appointment of the person, thereby necessitating the confirmation with criteria of independence, assessment of skills and capabilities and the manner in which such appointee continues to meet the requirements of the company. Therefore, the Board has a power to appoint the person as an additional ID, whose appointment shall thereafter be approved at the general meeting.

In order to understand the timeline in the case of re-appointment, we will have to consider the revised Regulation 17(1C) SEBI Regulations. Regulation 17 (1C) provides for approval of appointment of a person as a director of the company to be done within the next general meeting or 3 months, whichever is earlier. Since, re-appointment on account of end of term results into fresh appointment, the same shall also apply in case of re-appointment of an ID. Further, Regulation 25 (2A) has now provided for a special resolution to be obtained in case of appointment as well as re-appointment. The same prescribes for the mode of obtaining approval but is silent on the timeline, to be followed, requiring reference to Regulation 17 (1C). For a better understanding of the same, let us look at the following cases.

Case 1: Re-appointment of a person as an ID before the end of his/her tenure:

Case 2: Re-appointment of a person as an ID post the end of tenure:

The provisions of the Act mandate the shareholders to approve appointment of IDs at general meeting but does not mandate appointment from the date of general meeting. ‘Independent Director’ is the nature of directorship and ‘Additional Director, Non-Executive’ is the category of directorship. It cannot be inferred that the said director was not independent from the date of Board resolution appointing him as Additional Director till the date of general meeting. Therefore, the effective date of appointment can be considered from the date of Board resolution or any subsequent date prescribed by the Board.

The recent changes in the provisions as stated above will result in reducing the gap between appointment of an ID on the Board of the company and approval of the said appointment by shareholders. While it is seen that some companies take up the re-appointment of the IDs by way of postal ballot before the end of tenure in case there exists a gap between the AGM and the end of term, the same shall be construed as a good governance practice, as prior approval of shareholders has not been mandated by law on account of the same not being specifically stated. Thus in case of re-appointment post end of tenure, the same cannot be viewed as a violation of provisions.

The ambit of proxy advisors in India is as prescribed under SEBI regulations and guidelines issued in this regard. While they may issue guidelines based on the best governance practices as established by them and recommend the same to the investors, there is a need to incorporate a check for discerning the nature and scope of such guidelines, so the investor may have a clear view of the propositions put forth. With the process of appointment of IDs being enhanced in the manner specified above, in addition to the newly inserted disclosure requirements, will make the appointment/re-appointment process of IDs more transparent and effective while ensuring greater conformity of their independence.

Related presentation – https://vinodkothari.com/2021/08/ensuring-board-continuity-and-balance-of-capabilities/

[1] https://vinodkothari.com/2021/06/scope-of-proxy-advisors-to-issue-general-voting-guidelines/

[2] https://vinodkothari.com/2021/07/proxy-advisors-corporate-decision-making/

[3] https://www.sebi.gov.in/media/press-releases/jun-2021/sebi-board-meeting_50771.html

[4]https://www.sebi.gov.in/reports-and-statistics/reports/mar-2021/consultation-paper-on-review-of-regulatory-provisions-related-to-independent-directors_49336.html

Sharon Pinto, Manager, corplaw@vinodkothari.com

Introduction

The right to vote on decisions of the Company is one of the most significant rights of the investors. Proxy advisors are entities that enable shareholders to function this right effectively. They undertake research on corporate governance practices across various entities and formulate their policies in order to establish benchmarks of the best practices. Based on the said benchmarks, the proxy advisors also provide voting recommendations to the client investors. SEBI had formulated a working group[1] for determining issues relating to proxy advisors in November, 2018 and reviewing the existing provisions of SEBI (Research Analysts) Regulations, 2014 (‘SEBI Regulations’), that govern proxy advisory entities in India.

We have in our previous articles deliberated the concept of proxy advisors and their role in corporate democracy[2] as well as analysed the above-mentioned report of the working group[3] [4]. In recent times, there has been huge hue and cry regarding the certain voting recommendations put forth by proxy advisors. As the advisors have significant influence over institutional investors and may thus affect the voting results, it is necessary to understand the legal ambit of such guidelines and recommendations issued by these entities.

In this article we have discussed the scope of proxy advisors while ascertaining the legal validity of their opinions. The guidelines issued on re-appointment of ID have been discussed in a separate article.

Scope of Proxy Advisors

1.USA

Investment advisors are required to be registered with the United States Securities and Exchange Commission (‘SEC’) under the Investment Adviser Act of 1940 and Rules[5] made thereunder. Rule 204A-1 of the said Act has prescribed that the investment advisors establish, maintain and enforce a written code of ethics that, at a minimum, includes:

“(1) A standard (or standards) of business conduct that you require of your supervised persons, which standard must reflect your fiduciary obligations and those of your supervised persons;

(2) Provisions requiring your supervised persons to comply with applicable Federal securities laws;

(3) Provisions that require all of your access persons to report, and you to review, their personal securities transactions and holdings periodically as provided below;

(4) Provisions requiring supervised persons to report any violations of your code of ethics promptly to your chief compliance officer or, provided your chief compliance officer also receives reports of all violations, to other persons you designate in your code of ethics; and

(5) Provisions requiring you to provide each of your supervised persons with a copy of your code of ethics and any amendments, and requiring your supervised persons to provide you with a written acknowledgment of their receipt of the code and any amendments.”

Institutional Shareholder Services (‘ISS’) is a registered investment advisor which provides general proxy voting guidelines[6] on various resolutions put forth at the meetings of investors. However, the following disclaimer forms part of the document:

“The Information has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), or a promotion or recommendation of, any security, financial product or other investment vehicle or any trading strategy, and ISS does not endorse, approve, or otherwise express any opinion regarding any issuer, securities, financial products or instruments or trading strategies.”

Similar guidelines and policies have been issued by Glass Lewis & Co.[7] stating that these proxy voting guidelines are grounded in corporate governance best practices, which often exceed minimum legal requirements. Accordingly, unless specifically noted otherwise, a failure to meet these guidelines should not be understood to mean that the company or individual involved has failed to meet applicable legal requirements.

Proxy advisers in Australia hold Australian financial services (AFS) licenses for only a portion of the services they provide – giving advice to wholesale investors on votes that relate to dealings in financial products. Providing voting recommendations on other matters (such as director elections and remuneration reports) does not require an AFS licence.

Further, as per the provisions of Section 912A of the Corporations Act, 2001 proxy advisors shall:

ASIC in its ‘Review of proxy advisor engagement practices’[8] has stated that a draft report shall be provided to the Company for fact-checking or where clarification is sought from the company, proxy advisers should endeavour to provide sufficient time for the company to consider the request and respond. Further, if it is intended that a draft report will be provided to the subject company, proxy advisers may wish to consider doing this in a controlled way, for example, without communicating recommendations or opinions that would be included in the final report. This may reduce disagreements between proxy advisers and companies as to whether errors reported by companies relate to fact or opinion. In case proxy advisors propose to recommend ‘against’ recommendations, ASIC has recommended that they shall notify companies of such recommendations and explain the reasons for those recommendations, to assist companies in understanding concerns held by the proxy adviser and responding to investors in the context of those concerns.

Further, proxy advisors are recommended to disclose the following in their reports:

At present, there is no prior engagement of the proxy advisors with the client. Similar provisions have been stated under SEBI Regulations and procedural guidelines which are applicable to proxy advisors operating in India, which state that the report shall be provided to the company and the client at the same time.

However, as per the consultation paper issued by The Treasury in April 2021[9], it has been recommended that the proxy advisors in Australia shall provide the report to the corporate entities prior to issuing of the same to clients. Further, communication with the company prior to issue of report in order to diminish any factual errors or mis-interpretation has also been proposed.

The discussion paper on proxy advisory industry[10] issued by European Securities and Market Authority (ESMA), state that European proxy advisors generally tend not to develop their own guidelines but follow client’s policies or general recommendations. The voting policies and guidelines prepared are based on the relevant corporate governance standards. In the majority of cases these policies are usually formulated through a bottom-up process where information is collected from a diverse range of market participants (including issuers) through multiple channels. This policy can be fully adapted to local circumstances in a given country, or can incorporate more general beliefs about what constitutes good governance. Corporate governance codes, listing rules, company law, local regulations, new market trends, practices and academic research are used to create a set of guidelines against which corporate disclosures can be benchmarked. Moreover, it is a common practice for proxy advisors to integrate feedback from clients and, if available, issuers.

It further states that, certain proxy advisor may hold roundtables with various industry groups or other experts are also a way of receiving information and hearing different perspectives. Some proxy advisors are open for discussion about their policies and guidelines throughout the year while others are only open for discussion after the general meeting session. Proxy advisors, have to make sure voting policies and guidelines are sufficiently flexible to be applicable to the circumstances of each jurisdiction, sector and issuer. There may be issues arising on the accuracy, independence and reliability of the ultimate voting recommendations/proxy advice.

Proxy advisors that have their registered office or head office in United Kingdom or European Economic Area or in Gibraltar or provide proxy advisor services through an establishment located in the United Kingdom, are governed by the Proxy Advisors (Shareholders’ Rights) Regulations, 2019[11].

Following are the some of the provisions prescribed under the said regulations:

Further, where the proxy advisors where no such code of conduct has been adopted, the proxy advisors must provide a clear and reasonable explanation for not doing so.

Proxy advisors are governed by SEBI Regulations. The entities functioning as proxy advisors or research analysts are required to obtain a certificate of registration from the Board under these regulations. The regulations have stipulated the following w.r.t. contents of the report published by the advisory firms:

Further, the procedural guidelines issued by SEBI for proxy advisors[12] states that the report of the proxy advisors shall be shared with its clients and the company at the same time. The timeline for receiving comments from the Company may be defined by the proxy advisors and all comments/clarifications received from the company, within timeline, shall be included as an addendum to the report. It also states that if the company has a different viewpoint on the recommendations stated in the report of the proxy advisors, then proxy advisors, after taking into account the said viewpoint, may either revise the recommendation in the addendum report or issue an addendum to the report with its remarks, as considered appropriate.

Similar to the regulatory provisions in USA, the proxy advisors registered in with SEBI shall abide by the code of conduct prescribed under Regulation 24 of SEBI Regulations.

As the views of proxy advisors are based on the best corporate governance practices and research thereon, they are required to clearly disclose in their recommendations the legal requirement vis-a-vis higher standard they are suggesting if any, and the rationale behind the recommendation of higher standards.

Legal position of guidelines issued by proxy advisors

Proxy advisors undertake extensive research of the corporates to determine and set benchmarks. As evident from the global scenario and the working of proxy advisors in India as discussed above, one can opine that such guidelines are formed on the basis of the research undertaken by the said entities.

2.Interpretation of law

The said guidelines are a manifestation of the best governance practices that the companies may strive to achieve, which may at times exceed the prescribed legal requirements. They form the basis of opinions of the proxy advisory firms and are specifically the views of the issuing firms. Thus, the opinions of the advisory firms may be subject to other interpretations.

3.Generality of policies

Due to the generality of the guidelines issued, certain factual or practical factors may not be considered if the said guidelines are applied to the agenda items of various companies. The case to case specific factors, company or director backgrounds, etc may not be considered while applying the policies and hence may not depict a comprehensive view of the decision of the company.

4. Lack of overview by regulator

Since, these guidelines are not subject to approval of regulators, they are solely the opinions of the proxy advisory firms. Hence, a deviation from these guidelines cannot be construed as non-compliance of the prescribed laws. There is thus a need for including a statement to the said effect to establish a comprehensive standing of the recommendation or guidelines issued.

Safeguards against misleading statements

The procedural guidelines[13] issued by SEBI state that in case the proxy advisors have provided their recommendation based on higher standard, the rationale and such higher standard along with the legal requirement shall be clearly stated in the report published. Further, they shall provide their to the clients and the company simultaneously and are required to add as an addendum to their report, the comments and clarification received by the company in case of difference of opinions.

The report of the Working Group stated above recommended that if the proxy advisors have a different interpretation from the company and the same is not on the basis of factual errors, the proxy advisors are not obligated to publish both view-points, in case the company has enough resources to publish their response.

In case of any dispute arising between the proxy advisor and the corporate, which is a violation of the code of conduct prescribed under the SEBI (Research Analyst) Regulations, 2014, the same may be referred to SEBI. However, the same shall not be a means to refute the interpretation of the proxy advisor, rather only cases of misuse of power in violation of the said code of conduct can be reported to SEBI. However, there is no statutory requirement prescribed for including a disclaimer in the report of the proxy advisor stating that the views mentioned in the report are solely of the advisory firm and there may exist other interpretations as the said report is not sanctioned by any regulator.

Conclusion

It is necessary that the investors take an independent view bearing into mind the scope of the guidelines while considering the voting recommendations of the proxy advisors. They must also be aware of the scope of policies issued by the advisory firms. While the concept of proxy advisors acts as a tool for strengthening corporate governance and enabling investors to take sound investment decisions, there is a need for establishing better safeguards for portraying a clear picture to the investors so that they may formulate independent views.

[1]https://www.sebi.gov.in/reports/reports/jul-2019/report-of-working-group-on-issues-concerning-proxy-advisors-seeking-public-comments_43710.html

[2]https://vinodkothari.com/wp-content/uploads/2017/03/Dance_of_Corporate_democracy-_rise_of_proxy_advisors-1.pdf

[3] https://vinodkothari.com/wp-content/uploads/2020/08/SEBI-prescribes-stricter-regime-for-proxy-advisors.pdf

[4]https://vinodkothari.com/wp-content/uploads/2019/08/SEBI-revisits-the-regulatory-framework-for-Proxy-Advisors.pdf

[5]https://www.ecfr.gov/cgi-bin/text-idx?SID=e0ff318417c1a2b70a9ea2ce5f0307aa&mc=true&node=pt17.5.275&rgn=div5

[6] https://www.issgovernance.com/file/policy/active/asiapacific/Asia-Pacific-Regional-Voting-Guidelines.pdf

[7] https://www.glasslewis.com/wp-content/uploads/2020/11/US-Voting-Guidelines-GL.pdf?hsCtaTracking=7c712e31-24fb-4a3a-b396-9e8568fa0685%7C86255695-f1f4-47cb-8dc0-e919a9a5cf5b

[8] https://www.asic.gov.au/media/4778954/rep578-published-27-june-2018.pdf

[9] https://treasury.gov.au/sites/default/files/2021-04/c2021-169360_consultation_paper.pdf

[10] https://www.esma.europa.eu/sites/default/files/library/2015/11/2012-212.pdf

[11] https://www.legislation.gov.uk/uksi/2019/926/made

[12] https://www.sebi.gov.in/legal/circulars/aug-2020/procedural-guidelines-for-proxy-advisors_47250.html

[13] https://www.sebi.gov.in/legal/circulars/aug-2020/procedural-guidelines-for-proxy-advisors_47250.html

| Category | Eligibility Requirement | Quantum* |

| NBFCs (including SDPs) meeting prudential requirements | ● Complies with applicable regulatory capital adequacy requirements/leverage restrictions/Adjusted net-worth for each of the last three financial years including the financial year for which the dividend is proposed

○ For SPDs, minimum CRAR of 20% to be maintained for the financial year for which dividend is proposed. ● Net NPA ratio shall be less than 6% in each of the last three years, including as at the close of the financial year for which dividend is proposed to be declared.○ Calculation of NNPA ● Complies with the provisions of Section 45 IC of the RBI Act/ Section 29 C of the NHB Act, as the case may be, that is to say, has transferred 20% of its net profits to the regulatory reserve fund ● No explicit restrictions placed by the regulator on declaration of dividend |

● Type I NBFCs- No limit● CICs and SPDs- 60% ● Other NBFCs- 50% |

| NBFCs (other than SPDs) not meeting prudential requirements | ● Complies with the applicable capital adequacy requirements/ leverage restrictions in the financial year for which dividend is proposed to be paid● Has net NPA of less than 4% as at the close of the financial year. | 10% |

| Criteria | Bank | NBFCs |