Step-by-step guide for disclosure for Analysts/Investors Meet

Do’s and don’ts to be ensured by listed companies

- CS Aisha Begum Ansari, Senior Manager corplaw@vinodkothari.com

Updated as on September 28, 2023 , pursuant to the SEBI LODR (Second Amendment) Regulations, 2023

Brief Background

In order to disseminate information regarding performance of the company, its future prospects etc. listed companies usually conduct gatherings of analysts/investors after dissemination of quarterly results or atleast once in a year. Such meets generally include conference calls or meeting with group of investors or one-to-one meet or calls with investors or analysts, including those in the nature of walk-in. The idea behind conducting such meets is to provide transparency for the company’s performance figures, to address the queries of the analysts/investors and to ensure that the company’s information is available to the stakeholders. However, the risk of information asymmetry in such meets or gatherings is very inherent.

While the regulatory framework of SEBI i.e. SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘Listing Regulations’) provided for disclosure of adequate and timely information to enable investors to track the performance of a company including the information pertaining to occurrence of investors meet/conference call with analysts, however, several inconsistencies were observed in the disclosures made by the companies. For instance, some entities were not divulging the details of what transpired in such investors’ meetings and were merely disclosing the limited presentations w.r.t. the meetings. As such, minority shareholders, who did not attend these meetings, were not privy to the information shared with a select group of investors, thereby creating information asymmetry among different classes of shareholders.

Realizing this, SEBI, on November 20, 2020, came up with the Consultation Paper and recommended enhanced disclosure requirements w.r.t. post earning calls and one-to-one meets. Our write-up analyzing the said consultation paper can be viewed here.

Later, vide notification dated May 05, 2021, SEBI enhanced the disclosure requirements w.r.t. Investors’/ Analysts’ meet. In this article, the author has made an attempt to discuss the changes made in the disclosure requirements w.r.t. analyst meet step by step.

Post amendment in Listing Regulations

On May 05, 2021, SEBI amended the Listing Regulations which inter alia, covered analyst meet. Pursuant to the said amendment, the companies are required to include enhanced disclosure requirements with respect to analyst/ investors meets so as to avoid selective disclosure and information asymmetry and to ensure market integrity and to safeguard the interest of investors. The said amendments were voluntary for FY 2021-22, and became mandatory from FY 2022-23. The synopsis of the amendment is provided below:

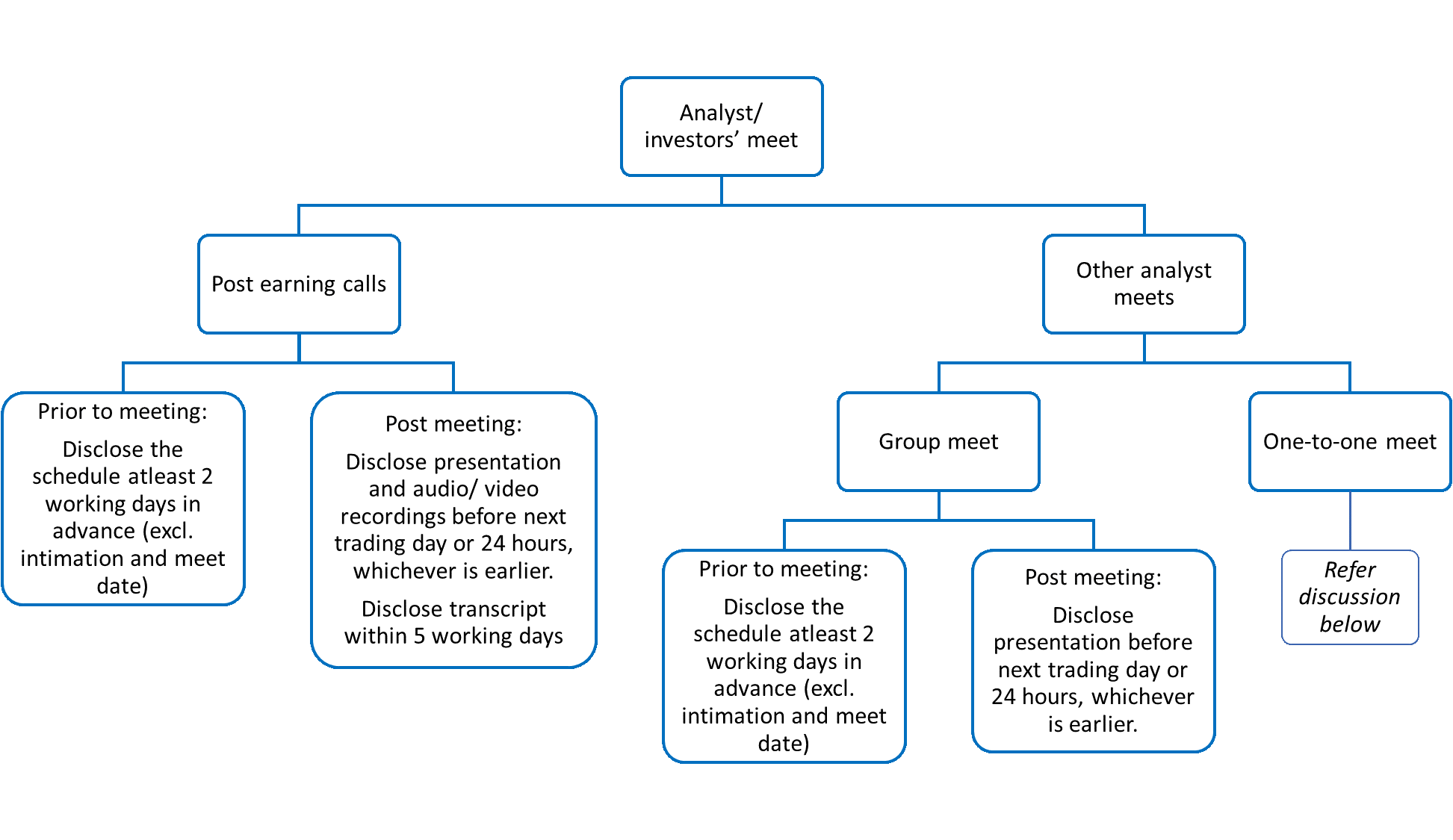

Figure 1: Disclosure requirement for analyst meet

Regulatory requirements in case of one-to-one meet

In respect of one-to-one meet, there are no explicit disclosure requirements as such. However, considering the intent of the Listing Regulations and SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’), the following things are explicitly clear:

- One-to-one meets, even though unregulated, should be discouraged looking at the high possibility of leakage of UPSI; and

- Even if the entity has one-to-one meet, it cannot share any UPSI.

Regulation 8 of PIT Regulations mandates every listed company to frame a code of practices and procedures for fair disclosure of UPSI in line with the principles set out in Schedule A to PIT Regulations. Para 6 of Schedule A requires the company to ensure that information shared with analysts and research personnel is not UPSI. Para 7 provides for developing best practices to make transcripts or records of proceedings of meetings with analysts and other investor relations conferences on the official website to ensure official confirmation and documentation of disclosures made.

The PIT Regulations do not distinguish between group meets and one-to-one meets. It requires the company to record such meets and develop best practices to disclose the same on its website. The practice of recording the meet also safeguards the company officials participating in the meeting from any possible allegation of having divulged UPSI.

Whether sharing of UPSI is allowed in a group meet or one-to-one meet?

The PIT Regulations prohibit sharing of UPSI in any manner to any person including analysts/ investors and require the companies to take all required steps to ensure the same. Considering the same, the fact whether it is a group meet/ call or otherwise or whether such meet/ call was organized by the company itself or not, becomes irrelevant and the prohibition shall apply in all cases.

Therefore, there is a remote chance of sharing such UPSI until and unless the same is as per the provisions of code of fair disclosure framed by the company. Accordingly, if any UPSI is shared, legitimately in terms of the said code or otherwise, the entity will have to disclose the audio/ video recordings or the transcripts of such meeting to the stock exchange promptly.

Guidance Note of Analyst/ Institutional investors’ meet

The amendment in the Listing Regulations came up with various interpretations and ambiguities w.r.t. disclosure requirements. We have discussed such anomalies in our previous article which can be viewed here.

In order to clear the ambiguities w.r.t the disclosure requirements, BSE, vide circular dated 29th June, 2021 and July 29, 2022, provided further clarifications and recommendations. In this article, we have tried to provide step-by-step guide for disclosure on analyst meets and post earning calls. Further, we have also provided the do’s and don’ts to be ensured by the companies.

Disclosure requirements w.r.t. Analyst meets

In order to comply with the provisions of Listing Regulations in letter and spirit, the companies are required to ensure that it makes timely disclosure to stock exchanges and on their own website. The compliance requirement as per the amended provisions w.r.t. analysts/ investors meet are jotted down below:

| Sr. No. | Cases | Disclose what? | By When? | Other Points to be ensured |

| 1. | Post earning calls/ Quarterly calls, by whatever name called (after disclosure of quarterly financial results) | Schedule of such meeting | Atleast 2 working days in advance (excluding the date of intimation and date of the meet). | Mandatory only for group meets. |

| Presentation and the audio/ video recordings of such meeting | Before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier. | Mandatory for both group meets and one to one meets.To be disclosed whether conducted by a company or any other entity.To be hosted on the website of the company for minimum 5 years and thereafter as per the archival policy of the company. To be disclosed simultaneously to the stock exchange. | ||

| Transcripts of such meeting | Within 5 working days of conclusion of the meet. | Mandatory for both group meets and one-to-one meets.To be disclosed whether conducted by a company or any other entity.To be hosted on the website of the company and preserved permanently.To be disclosed simultaneously to the stock exchange. | ||

| 2. | Other Analysts/ Investors meets | Schedule of such meeting | Atleast 2 working days in advance (excluding the date of intimation and date of the meet) | Mandatory only for group meets. |

| Presentation made in such meeting | Before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier.. | Mandatory only for group meets.To be disclosed on the website of the company, whether conducted by company or any other entity.To be disclosed simultaneously to the stock exchange. | ||

| In case any UPSI is shared | Audio/video recordings or transcripts of such meeting | Promptly | Applicable to both group as well as one-to-one meets.To be disclosed on the website of the company, whether conducted by a company or any other entity.To be disclosed simultaneously to the stock exchange. |

Best practices that may be adopted by companies

Disclosure of schedule of meet/ call

While making disclosure of schedules, the company may also provide the details pertaining to the meet/ call, mode of attending, details pertaining to registrations, disclaimers/ note to complete/ ease registration/ attending the call, details regarding specific platform requirements, if any, inclusions/ exclusions of audience/ participants if any, etc.

Further, a disclaimer or a confirmation may be added in the intimation stating that ‘Company will be referring to publicly available documents for discussions’ or ‘No UPSI is proposed to be shared during the meeting / call’. This will create confidence amongst the investors and will maintain sanctity of the meet / call.

Disclosure of transcripts of the meet/ call

While disclosing the transcripts of the meet/ call, the companies may also consider providing the list of attendees and record the dialogues, Q&As and assents and dissents of the analysts/ investors. Further, a confirmation may be added in the disclosure that no unpublished price sensitive information was shared/ discussed in the meeting / call.

Do’s and Don’ts to be ensured by the companies

The companies will be required to observe some crucial points while scheduling or attending analysts’/ investors’ meet, conference calls, post earning calls etc. Briefly, the following are the do’s and don’ts:

| Sr. No. | Do’s | Don’ts |

| 1. | Always conduct scheduled meets. | Avoid unscheduled meets. |

| 2. | Always schedule group meets. | Avoid scheduling one-to-one meet. |

| 3. | Upload the schedule of group meets/ calls on the website atleast 2 working days in advance (excluding the date of intimation and date of the meet) and also simultaneously submit the same with the stock exchange. | Do not forget to upload and send the schedule on the website and to the stock exchanges, respectively beyond the prescribed time. |

| 4. | Upload the presentation made to analysts/ investors in the scheduled group meet on the website promptly before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier and also simultaneously submit the same with the stock exchange. | Do not forget to upload and send the schedule on the website and to SE, respectively beyond the prescribed time. |

| 5. | Ensure to make audio and video recording of the post earnings/ quarterly calls, whether conducted physically or through digital means, either conducted by company or any other entity including one- to-one meets. | Do not avoid making audio/video recording of such calls irrespective the same was conducted by the company itself or by any other entity. |

| 6. | Ensure transcripts of the post earnings/quarterly calls, whether conducted physically or through digital means, either conducted by company or any other entity including one-to-one meets. | Do not avoid making transcripts of the proceedings of such calls irrespective the same was conducted by the company itself or by any other entity. |

| 7. | Ensure that the information shared with the investors is already available in the public domain. | Do not share UPSI with the investors. |

| 8. | Maintain a silence period, if any, as provided in the code of fair disclosure framed by the entity. | Discourage any sort of meets either group meet or one-to-one meets (including walk-in investors) during silence period. |

| 9. | Upload all audio/video recordings and presentation of the post earning/ quarterly calls on the website of the company within 24 hours of conclusion of such calls or next trading day, whichever is earlier. | Avoid uploading audio/video recording beyond the prescribed time. |

| 10. | Upload all transcripts of the post earning/ quarterly calls on the website of the Company within 5 working days of conclusion of such calls. | Avoid uploading transcripts of the post earning/ quarterly calls on the website of the company after 5 working days of conclusion of calls. |

| 11. | Simultaneous to uploading audio/video recording and transcripts on the website of the company, submit the same to the recognized stock exchange. | Do not forget to send audio/video recording and transcripts of the meets to the recognized stock exchange |

| 12. | Preserve the disclosures made on the website of the Company (a) Audio/video recording- for minimum 5 years and thereafter as per archival policy of the company; (b) Transcripts: permanently | Do not avoid preserving of audio/video recording and transcripts of the meets |

Conclusion

The amendment in Listing Regulations and guidance note by the stock exchanges give us the clear view that the companies are required to make timely disclosure of audio/ video recordings, transcripts of post earning calls and only presentations of analyst meet to the stock exchange. Even though this seems to be the compliance burden on part of the listed companies which are already pressed with various disclosure requirements, this step is surely a welcome move as it will help the watchdog of capital markets to curb insider trading and information asymmetry.

Our other article on similar topics can be read here – https://vinodkothari.com/2020/11/sebi-proposes-enhanced-disclosures-for-meetings-with-analyst-investors-etc/

Our Podcast on the topic: https://open.spotify.com/episode/2oVRo2iEOV7cVVqYwcqb2c?si=b860b48d6f924ad6&nd=1

Our Resource Centre on LODR:

Leave a Reply

Want to join the discussion?Feel free to contribute!