Workshop on Insider Trading Regulations for Compliance Officers

See our resources on insider trading here: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/

See our resources on insider trading here: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/

– Abhishek Kumar Namdev, Assistant Manager | corplaw@vinodkothari.com

Open-market buyback through stock exchanges, earlier discontinued by SEBI in a phased manner based on a 2023 amendment (see an article here), is proposed to be brought back in the buy-back regime. SEBI has released two consultation papers, on April 02, 2026 and May, 08, 2026 proposing to re-introduce open market buy-back of shares through stock exchanges.

Buyback through the SE route would usually be preferred for the ease of compliances and flexibility available with the listed entity. The process is rather simple and cost-effective, as compared to the lengthy process of tender offer or reverse book-building.

Historically, buy-back through the stock exchange route was one of the recognized modes under the regulations, which was subsequently phased out pursuant to the 2023 amendments and discontinued w.e.f April 01, 2025. Reasons involved:

The primary rationale for bringing back buybacks through SE route is on account of the tax inefficiencies being resolved pursuant to the Finance Act, 2026. The taxation of buy-back proceeds has been rationalised, putting the tax burden on those shareholders whose shares are being bought back.

Additionally, to ensure that there is no misuse of the buyback provisions by the promoters or promoter group members, the new taxation regime imposes additional tax-rates on buyback by such shareholders. See an article on the changes in relation to buy-back taxation.

On the other hand, open-market buyback through the SE route is also recognized for enabling efficient price discovery, improved liquidity, and flexible capital management for companies. Thus, the balance is in favour of enabling buybacks through the SE route again.

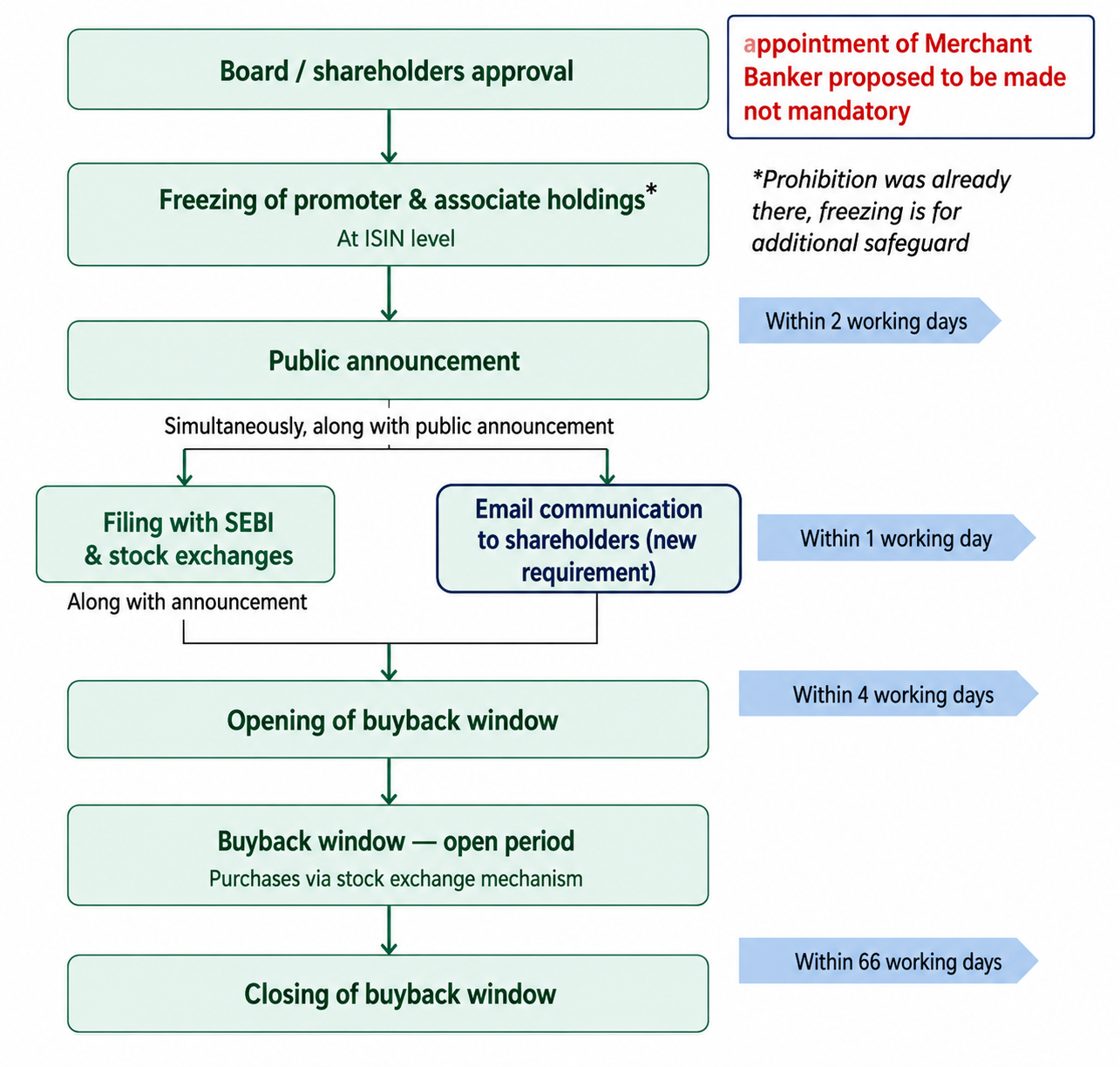

The proposal is neither a “revert”, nor a completely new framework. See figure below for proposed changes in the process of buyback through SE route:

The 8th May CP proposes certain modifications to the erstwhile provisions of the Buyback Regulations for ease of doing business and further strengthening the buyback framework, as tabulated below:

| Provision | Extant requirements | Proposed changes | Remarks |

| Public announcement (Reg. 16(iv)(b) | Newspaper publication within 2 working days of board/postal ballot resolution;also placed on the website of SE, merchant banker and company | Additional mandatory electronic intimation (including email communication) to shareholders as on the date of public announcement, within one working day from the date of such public announcement. | To ensure due information to shareholders in a timely manner. |

| Duration (Reg. 17(ii)) | 6 months – prior to 2023 amendment Reduced to 66 and thereafter 22 working days pursuant to 2023 amendments | 66 working days | To ensure timely execution while providing adequate flexibility to the issuers |

| Separate Trading Window (Explanation to reg. 16) | Through a separate trading window provided by the stock exchange. | To be done under the normal trading window | A separate trading window is not required in view of the uniformity in tax treatment. Accordingly, this is not required. |

| Disclosure of Company Identity in Buy-back Orders (Reg. 17) | The company’s identity as purchaser was required to be displayed on the electronic screen at the time of placing the order. | NA |

While the CP is primarily focussed on bringing back SE mechanism for buybacks, some proposals have been made for amendments in the existing regulations w.r.t. all forms of buyback:

| Provision | Extant requirements | Proposed changes | Remarks |

| Prohibition on trading by promoters and associates (Reg. 24(i)(e) | From buyback approval till offer closure – prohibition on promoters and their associates, including inter-se transfers | Promoters’ shareholding to remain frozen at an ISIN level during the buy-back period, Exception: for tendering shares in a tender offer buy-back | Freezing of PAN at an ISIN level provides an additional safeguard against use of buyback by promoters for market manipulation. Tendering of shares during tender offer is permitted, in view of the additional tax-rates imposed on promoters pursuant to the Finance Act. |

| Minimum public shareholding compliance | No explicit provisions | Buyback not to be announced in breach of MPS requirements | This is a clarificatory change; even though the Regulations did not explicitly mention about MPS requirements, the issuer is required to ensure compliance will all applicable laws at all times. |

| Interval between two Buy-Back offers (Reg. 4(vii)) | Lock-in of 1 year from expiry of the buy-back period | Reference to CA, 2013 instead of explicit provisions | The CLAB, 2026 proposes various amendments in relation to the buyback framework; this will ensure alignment between the SEBI Regulations and CA, 2013. See an article here. |

| Appointment of Merchant Banker (“MB”) | Mandatory | Functions of merchant banker to be re-distributed to LE, SEs and Secretarial auditor. | For reducing the procedural and compliance costs |

Overall, the proposal reflects a shift from prohibition to reinstatement of an earlier permitted mechanism of buyback through the SE route, with additional safeguards to ensure there are no regulatory loopholes. With changes proposed in CA, 2013 under the Corporate Laws Amendment Bill, and a favourable tax regime pursuant to the Finance Act, 2026, this seems to be an opportune time to revisit and revise the buyback framework applicable to the listed entities.

The rebirth of buyback through SE mechanism is expected to provide companies with greater flexibility in structuring buy-backs, while also ensuring a more equitable framework for shareholder participation and taxation outcomes. The proposal, therefore, seeks to strike a balanced approach between market efficiency and fairness, addressing past issues without dispensing with the benefits of the mechanism.

Simrat Singh | Finserv@vinodkothari.com

REITs and InvITs are often discussed together as parallel innovations in India’s capital markets, reflecting a push towards deploying capital in real estate and infrastructure. Both frameworks were introduced in 2014, share a trust-based structure and are subject to broadly similar regulatory principles, including mandatory cash distribution requirements and both also have a common tax provision in section 115UA of Income Tax Act, 1961 (section 223 in the 2025 Tax Act). Comparatively, InvITs have witnessed a significantly stronger growth, largely driven by the government’s sustained push towards infrastructure development. The data clearly reflects this divergence. As of April, 2026, there are 6 registered REITs and 28 InvITs in India, managing an AUM of ₹2,50,000 Crores and ₹6,20,000 Crores respectively. Among the InvITs, Road sector InvITs dominate the total AUM. (see our write-up on distribution of AUM of InvITs here). Notable, the national monetisation pipeline 2.0 proposed monetization of approx ₹3,35,000 Crores worth of highway assets under InvIT/TOT models (see our write-up on this here).

While InvITs are required to distribute 90% of their cash flows, the underlying SPVs, mandated to be in company form, are constrained by dividend distribution rules that rely on accounting profits rather than actual cash generation. In sectors such as roads and power, where assets are finite-life concession rights or long term power purchase agreements, such assets are subject to heavy amortisation which leads to SPVs report book losses despite generating steady cash flows. As a result, cash exists within the SPV but cannot be upstreamed efficiently as dividends. This issue stems from treating InvITs on par with REITs despite differences in investments and nature of assets and from disallowing flexibility in the legal form of SPVs.

Industry workaround has been towards debt-heavy (thin capitalisation) structures, enabling distributions through interest and loan repayments, though these might raise tax issues (discussed below). Beyond such workarounds, more durable solutions are explored in line with international models like US Master Limited Partnerships and Singapore Business Trusts such as permitting dividend declarations based on cash flows rather than accounting profits, reconsidering the mandated company form of SPVs to allow more flexible structures such as trusts or LLPs etc.

REITs and InvITs are different in the sense that one invests in a property and looks at long term appreciation/rentals. The other looks at an infra asset which gives cash flows only for a certain period

REITs hold income-generating real estate assets with no fixed economic life. These assets can be retained, redeveloped/renovated or replaced over time. At the SPV level, there is no restriction on holding multiple assets and the portfolio of assets can be managed through acquisitions and divestments.

In contrast, InvITs, particularly in the road sector, hold assets that are inherently finite. These assets are in the form of concession rights and are intangible assets where the concessioning authority (usually NHAI) grants a right to operate and collect revenue for a defined period, say 15 to 20 years. Note that the road asset is not the asset that is taken on the balance sheet of the SPV, rather it is the intangible right to collect revenue on the road that is capitalised. At the end of the concession period, the asset reverts back to the concessioning authority, leaving no residual economic value. At this stage, the SPV merely becomes a shell entity, holding in itself only residual litigations or tax demands awaiting its eventual outcome of being wound-up.

Moreover, there are certain constraints imposed by the concession agreement entered into between the SPV and NHAI. Under standard concession agreements, each road project is required to be housed in a separate SPV. Which is why the name of the SPVs are in the style “[Name of Road Stretch] Tollway/Toll Road Private Limited”. The “one project, one SPV” model prevents aggregation of road assets within the same SPV and keeps the rights, obligations and risk allocation clearly demarcated. While this mandatory housing of each project in a separate private limited entity has its advantages, such as lender protection, bankruptcy remoteness and clarity in enforcement of contractual rights, it also creates rigidity for the InvIT.

The inability to pool assets or recycle assets within the SPVs prevents capital recycling. Unlike REIT SPVs, InvIT SPVs cannot recycle capital either by selling assets or acquiring new ones within the same entity. As a result, while REITs can operate vehicles with a perpetual asset base, InvITs function as portfolios of wasting assets that are depleted over time and cannot be replaced within the same SPV.

Both REITs and InvITs (and their SPVs/HoldCos) are required to distribute at least 90% of their net distributable cash flows. This distribution can occur through interest on loan, loan repayment or dividends from the SPVs. The challenge for InvITs arises at the SPV level, in the case of dividend distribution. Under Section 123 of the Companies Act, a company can declare dividends only out of distributable profits or accumulated reserves. The books of such SPVs are loaded with high upfront capitalisation of construction costs and subsequent recognition of a concession asset. This asset is depreciated (or amortised in case of intangible assets such as concession right) over the concession period along with the amortization of the earlier capitalised expenditure, leading to significant non-cash expenses in the profit and loss account which continues to hit the Profit and Loss account even when the SPV starts collecting cash. As a result, even when the SPV generates operating cash flows from toll collections, it remains in ‘book losses’ for a portion of the concession life. The consequence is that such SPV is unable to declare dividend distribution to the InvIT despite the availability of cash.

Accounting principles require allocation of asset cost over its useful life. This is conceptually sound for assets that are expected to be replaced or reinvested in. A machinery may be required to be replaced once its useful life is over, therefore, it is only prudent to set aside a part of the cost so there is enough cushion when the entity goes to replace the machinery.

In the case of REITs, this logic holds good. Depreciation reflects the wear and tear of the replaceable asset and the entity has the ability to reinvest/replace the asset over time (i.e. purchase a new rent yielding building in the same SPV). The economic cycle supports the accounting treatment.

For InvIT SPVs especially in the road sector, the asset is not replaced at the end of its life; it is handed back to the concessioning authority. The SPV has no ability to deploy accumulated depreciation (or amortization in case of an intangible asset) towards acquisition of a new asset. Its economic life is co-terminus with the concession period. This creates a disconnect between accounting profits and economic cash flows. Depreciation suppresses book profits without corresponding economic relevance in terms of asset replacement within the SPV.

Singapore offers the clearest analogy to and resolution of this problem. The Business Trusts Act 2004 (BTA), administered by the Monetary Authority of Singapore (MAS), created a hybrid structure that combines features of a company (separate legal personality, professional management) with features of a trust (cash-based distributions). The defining advantage of the Singapore Business Trust (BT) is stated explicitly in the legislation and was articulated in the MAS’s explanatory brief for the Business Trusts (Amendment) Bill 2022:

“A key advantage of a BT structure is the ability of a trust to pay dividends to unitholders out of its cash profits. In contrast, a company can only pay dividends out of its accounting profits (i.e. after deducting non-cash expenses such as depreciation). The BT structure is thus particularly suited to businesses with stable growth and high cash flow.”

Singapore listed 15 Business Trusts as of 2026, covering assets including power generation, toll roads, and shipping. For infrastructure BTs, the cash-based distribution right is central to the investment proposition. Critically, the BT does not interpose a company-form SPV between the trust and the infrastructure asset; the trust itself holds the operational assets. This avoids the Section 123-equivalent constraint that would arise if a company-form subsidiary were the operating entity.

The Singapore model, however, is not directly transplantable to the Indian road sector context for the reason explained above ie NHAI’s requirement for a company-form concessionaire.

In the United States, the Master Limited Partnership (MLP) structure, originally developed for oil and gas pipelines and subsequently applied to other infrastructure sectors, avoids the dividend constraint through the partnership form. Partnerships are not subject to corporate dividend restrictions; distributions to limited partners (akin to unitholders in InvITs) are made based on cash available for distribution, a metric that is equivalent to NDCF and adds back non-cash charges including depreciation and amortisation. Interestingly, MLPs typically grant the General Partner (GP is somewhat analogous to the investment manager in an InvIT), a share in the distributable cash flows through Incentive Distribution Rights (IDRs). These rights are structured on a tiered basis, such that as distributions to Limited Partners increase, the GP becomes entitled to a progressively larger share of incremental cash flows. This creates a performance-linked incentive for the GP to enhance distributable cash. At the same time, the GP retains discretion over the quantum of cash to be distributed versus retained.

In the original consultation process leading to the introduction of InvITs, SEBI did take note of international structures such as the Master Limited Partnerships in the United States, which allow cash-based distributions without being constrained by law dividend rules. However, there was no discussion on the legal form of the SPV and the final regulations settled on a company structure for underlying entities. Had there been flexibility to allow SPVs to be structured as trusts and/or LLPs, the present issue may not have arisen in the first place.

A commonly adopted workaround is to maintain a thinly capitalised SPV, with the bulk of funding structured as loans from the InvIT rather than equity investment. In such cases, distributions are routed primarily through interest payments and loan repayments instead of dividends, a structure widely used in InvIT arrangements. However, this approach may attract limitations under Section 94B of the Income Tax Act, 1961 (section 177 in the 2025 Act), which operates as a Specific Anti-Avoidance Rule (SAAR) on excessive interest deductions. The provision applies where an Indian borrower incurs interest expenditure exceeding ₹1 crore in respect of debt from a non-resident associated enterprise (or even third-party debt backed by such an enterprise). In such cases, the deduction for interest is restricted to 30% of EBITDA or the actual interest payable to associated enterprises, whichever is lower and any excess interest is disallowed. Accordingly, in InvITs where non-residents usually hold the majority of the units, thin capitalisation may lead to disallowance of interest deductions for SPVs.

A more targeted solution would be a targeted regulatory relaxation by the Ministry of Corporate Affairs, permitting dividend declaration by InvIT SPVs based on NDCF rather than accounting profits. This would essentially create a sector-specific carve-out from Section 123’s profit test for companies that are 100% subsidiaries of registered InvITs or HoldCos of InvITs.

One possible approach is to reconsider the legal form of SPVs. Allowing SPVs to be structured as trusts could align the distribution framework more closely with cash flows rather than accounting profits. However, this would require a shift in regulatory and contractual frameworks as SEBI and NHAI both need to be onboarded on this. This solution seems far-fetched as Road assets vesting in a trust is a scenario which NHAI will not be comfortable with.

The principle is clear: regulation must follow the nature of the asset, not force the asset into an ill-fitting form. To mandate distribution without enabling it is, as in the tale of King Canute, to command the tide to rise while forbidding it a shore. An instruction complete in form, but wanting in effect. India’s InvIT framework is, without a doubt, a notable financial innovation, a bridge that has opened public infrastructure to private capital and supported the National Monetisation Pipeline. But the task is not merely to invite capital but to also ensure that the channels through which it flows are kosher. The present framework, in treating REITs and InvITs as parallel structures, overlooks divergence. While REITs rest on perpetuity of assets, InvITs are built on finite-life concessions that steadily deplete. This mismatch, compounded by accounting norms, contractual structures of NHAI and the Companies Act, creates a distribution bottleneck, where cash is generated but cannot be cleanly upstreamed. Industry has found workarounds, principally by way of intercompany loans. But the issue warrants policy attention. We can take guidance from comparative regimes, such as the Singapore Business Trust framework and U.S. MLPs and recognise infrastructure as a cash-flow distribution business and permit distribution mechanisms that reflect this reality. It is therefore imperative that SEBI, MCA, and NHAI act in concert to resolve this misalignment. Only then can InvITs evolve from a promising innovation into a durable pillar of India’s infrastructure architecture.

See our other resources on InvITs:

– Team Corplaw | corplaw@vinodkothari.com

Simrat Singh | Finserv@vinodkothari.com

Private credit is, in essence, shadow banking without corresponding discipline. Market reports indicate that Private Credit in India (and globally) is beginning to show signs of stress. Several global private credit fund managers have reportedly frozen withdrawals amid rising investor withdrawals. Given that private credit by its very nature is supposed to be illiquid, even a modest redemption pressure may hamper the ability of the fund manager to honor the withdrawals. Although this type of liquidity risk is limited in Indian private credit funds since they are usually close-ended category II funds in which investors are mandated to stay invested throughout the tenure of the fund. However, other risks such a opacity still loom. An equally important issue is the regulatory asymmetry, with private credit funds being regulated far less stringently than banks, NBFCs and other comparable lending institutions. Private credit funds take money from investors and lend to businesses; so do banks and NBFCs. Both carry systemic risks and can trigger panic on failure. Yet, only one is properly regulated.

In our earlier write-up on private credit funds we tried to list down the differences between regulated entities and these funds, a distinction which highlights the scarcity of controls and oversight in a lending fund that is expected in a lending vehicle. Notable examples include no uniform credit appraisal, no standardised reporting of performance of borrowers, no CRAR-like minimum capital requirement, no interest rate risk model etc. One may argue that the very absence of these requirements is what makes private credit funds tailor their deals according to the needs of the investee company; payment-in-kind, income-aligned repayment schedules are some of the examples. However, the absence of discipline also introduces opacity and potential systemic risks. Regulators globally have flagged these lending vehicles due to their opacity and market-wide risk (eg. RBI pointed out the systemic risk of private credit in its June 2024 Financial Stability Report). However, no action/mitigation measure has been taken as of now. In our view, atleast provisioning and NPA reporting-like safeguards should be there in such vehicles.

Note that these funds are not completely unregulated, SEBI AIF Regulations contain some safeguards such as concentration cap, valuation norms, no leverage at fund level etc. but these are generic safeguards and are not made keeping in mind the risks involved in a lending-based fund vehicle.

The case for regulatory intervention, therefore, is not about imposing bank-like rigidity, but about ensuring appropriate discipline for bank-like activities. Whether such oversight should fall within the domain of the RBI, given its expertise in regulating lending institutions, remains an open question. The more immediate concern is that these entities continue to operate outside a robust prudential framework. Importantly, the relatively small share of private credit funds in overall corporate lending (currently less than 2%) should not serve as a justification for regulatory inaction. Risks do not become relevant only at scale; by the time they do, the cost of inaction is often far greater. It is therefore for regulators to move beyond a form-based approach and adopt a substance-based framework for such lending vehicles.

You may register your interest and the questions that you’d like us to discuss at: https://forms.gle/1iR2xaFKGBU1kRJ3A

Our resource centre on RPTs can be accessed at: https://vinodkothari.com/article-corner-on-related-party-transactions/

Some of our recent resources on the subject:

SEBI approves relaxed norms on RPTs

Moderate Value RPTs : Interplay of disclosure norms and impracticalities

Tejasvi Thakkar and Simrat Singh | Finserv@vinodkothari.com

Pursuant to the RBI’s stated intent in the Statement on Developmental and Regulatory Policies to harmonise the conduct of Regulated Entities in relation to loan recovery, comprehensive draft instructions have been proposed, to be effective from July 1, 2026, consolidating and rationalising the existing scattered provisions. The instructions are applicable to all NBFCs, excluding Mortgage Guarantee Companies, Core Investment Companies, NBFC-Account Aggregators, Standalone Primary Dealers, Non-Operating Financial Housing Companies, and NBFCs not having any customer interface. The key requirements of the proposed framework are summarised below:

REs shall formulate a separate policy on recovery of loan dues, engagement of recovery agents and taking possession of security. The policy shall, inter-alia, cover:

Issue: Whether this can be combined with the policy on Code of Conduct for DSAs/DMAs?

Our view: Since the present requirement specifically deals with recovery conduct, possession and enforcement of security interest, and engagement of recovery agents, the same should ideally be maintained as a separate policy. The DSA/DMA CoC policy deals largely with sourcing-stage conduct such as mis-selling and consequent compensation-related aspects. However, where there are overlapping requirements, NBFCs may structure the same within a broader conduct framework, divided into separate sections. However, it should remain distinct from the outsourcing policy.

Issue: Whether the CoC prescribed earlier under HFC Directions stands subsumed?

Our view: Yes. The earlier HFC provisions largely stand harmonised and subsumed within the present draft framework, except for certain differences which have been captured in the Annexure below.

Recovery agents shall be required to carry recovery notice, identity card and authorisation letter, and shall adhere to the following conduct requirements:

REs shall:

Loan agreements shall contain a legally enforceable possession clause, clearly disclosed at the time of execution. The agreement shall, inter alia, specify:

REs shall put in place a management structure to monitor and control the activities of recovery agents and ensure that such agents refrain from actions that could harm the RE’s integrity and reputation. Accordingly, the RE should ensure:

Most of the proposed requirements are not entirely new in substance for HFCs, as they were already reflected in the Guidelines for Engaging Recovery Agents under paragraph 170 of the RBI HFC Directions, 2025. The proposal now is to delete those HFC-specific guidelines and require HFCs to comply with the proposed Directions.

However, while the underlying principles remain largely consistent, the proposed Directions significantly strengthen and formalise the recovery framework. The approach shifts from principle-based guidance to a more structured, prescriptive, and compliance-oriented regime. The key changes are as follows:

Recovery is as vital to lending as disbursement, if not more. Credit often begins with a courteous engagement by the lender, but too often, the standards of professionalism seen at the time of sanction weaken at the stage of enforcement. The right to recover is unquestionable; harassment is not. The proposed Directions seek to correct this imbalance by requiring lenders to uphold the same standards of fairness, transparency and discipline during recovery as at the time of origination.

See our other resources:

Simrat Singh | Finserv@vinodkothari.com

SEBI has issued a Consultation Paper on 05.02.2026 proposing amendments to the InvIT Regulations related to end-use of borrowings, status of SPVs and investment in under-construction projects. Further, it has also proposed to enhance the investible options for both REITs and InvITs w.r.t liquid mutual funds.

InvITs and REITs have continued on a strong upward growth trajectory. As of November 2025, the aggregate AUM of 27 InvITs stood at approximately ₹7,00,000 Crores after growing at a CAGR of approx 18% per annum since FY 21. The assets spann nine infrastructure sectors including roads, telecom, and power, as well as emerging asset classes such as warehouses and educational infrastructure. Reflecting their expanding scale and leverage capacity, aggregate borrowings of InvITs have crossed ₹2,03,000 Crores1. In contrast, REITs continue to trail InvITs in terms of scale, with the combined AUM of the five listed REITs amounting to approximately ₹2,35,000 Crores during the same period.2 May refer to our article “Roads to Riches: A Snapshot of InvITs in India”.

SEBI has consistently sought to create a more enabling regulatory environment for these vehicles. A notable example is the classification of REIT units as equity for mutual funds (as discussed below), which sought to enhance institutional participation and liquidity. Complementing these regulatory efforts, the Union Budget 2026 introduced several targeted measures to deepen infrastructure financing, including the proposed Partial Credit Enhancement (PCE) framework and the creation of a dedicated infrastructure fund (see our write-up on the Budget 2026 here). Lastly, RBI in its Statement on Developmental and Regulatory Policies also allowed Banks to lend to REITs, putting them on same footing as InvITs (see our write-up on RBI’s Statement here). Taken together, these developments indicate that the growth trajectory of InvITs and REITs is expected to remain firmly positive.

Read more →– Team Corplaw | corplaw@vinodkothari.com

NFRA moved the needle, and it is to be seen if the ocean starts boiling.! A 7th Jan 2026 circular from NFRA, addressed to listed entities and their auditors, seemed like an attention-drawer to standards of auditing which are already there, and yet, the auditing fraternity is holding meetings with boards and senior management of listed entities, to comply with what was always a compliance requirement. Does the 7th Jan circular bring up any new boxes to be ticked, any new procedures to be laid or responsibilities to be reiterated? As we detail out in this article, there may be need for action on several fronts on the part of listed entities – identification of nodal persons, listing developments that need to be communicated, constituting team for responding to the findings of the auditors in course of their audit other than those that sit in the audit report, formation of sub-groups of TCWG, etc.

Read more →– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

Finance Bill, 2026 brings tax relief to investors for share buybacks, by partially restoring the position that existed before the Finance Bill 2024 amendment. The 2024 Finance Bill changed the taxability of buybacks to impose tax on buyback consideration, taxing the entire “receipt” as “dividend”, implying tax at applicable regular tax rates rather than as capital gains.[See our article on the 2024 amendments here.]

The 2026 Bill proposes omission of Section 2(40) (f), [dealing with deemed dividend] and amendments to Section 69, [specifically dealing with tax on buybacks]. The net result of this:

Applicability of the amendments: The amended provisions apply for buybacks done on or after 1st April, 2026. The existing provisions were introduced effective 1st Oct., 2024 and therefore, they would have had a life of only 15 months.

Buyback is not merely a means of distribution of profits to the shareholders. There may be various reasons or motivations for which buyback may be done by a company, for example:

For detailed guidance on the procedure and compliances involved, refer to our FAQs on buyback here.

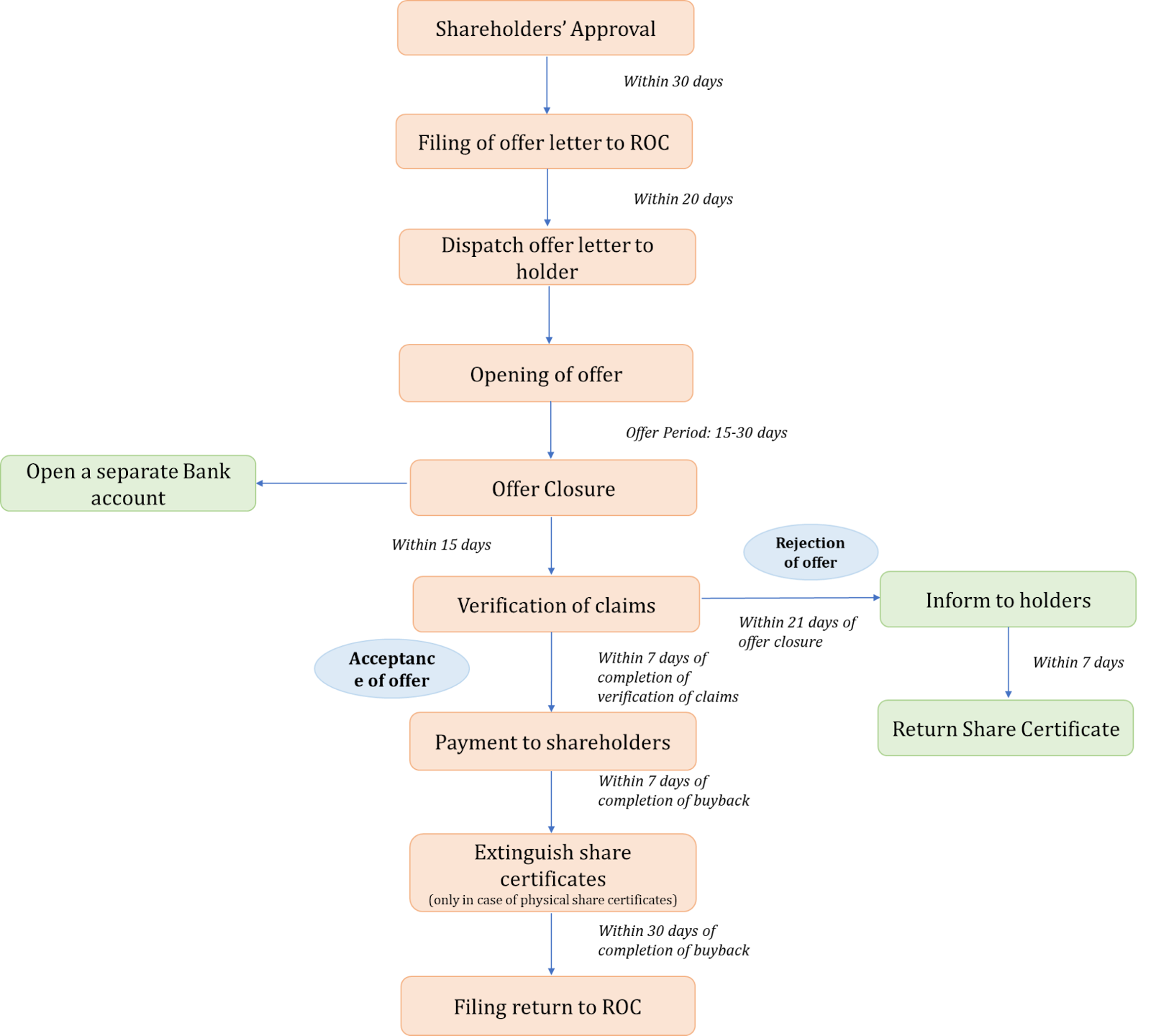

Figure 1: Buyback process and timelines under Companies Act

For buyback of capital beyond the statutory limits, the provisions of capital reduction u/s 66 apply. With the buyback consideration being taxed as deemed dividends, capital reduction through NCLT route was also being seen as an alternate route for scaling down capital in a relatively tax-efficient manner. There are rulings favouring capital reduction as an alternative to buyback, for instance, the ruling of NCLAT in the matter of Brillio Technologies Pvt. Ltd v. ROC, subsequently also referred to by NCLT Mumbai in the matter of Reliance Retail Ltd. Some of these rulings even permitted selective reduction of capital. See our article on reduction of capital here.

One of the primary deterrents in capital reduction u/s 66 of the Companies Act is the approval requirements – of the shareholders, creditors and even the NCLT.

The scope of dividend distribution is quite narrower as compared to share buybacks. The primary difference between the two is in the source of payment. Dividend distribution can be made only out of surplus; where free reserves are proposed to be utilised for dividend payment, additional conditions are applicable. In no case, can such declaration be made out of securities premium, or proceeds of fresh issuance – which are permissible sources for buyback. Buyback, on the other hand, requires mere liquidity, availability of profits is not mandatory. Therefore, dividends are merely a way to upstream the earned profits; buyback can even be the way to scale down, for example, by releasing the share premium, or using one class of shares to buy back the other.

Once dividend is approved by shareholders with requisite majority, there is no provision for a shareholder to waive off his right to the dividend [see our article on the same here], and unclaimed dividend, if any, are kept in a separate account to be transferred to IEPF. In case of buyback, while the same is also offered to all shareholders, the buyback consideration is paid only to such shareholders who tender their shares for buyback; the question of waiver of rights or unclaimed amounts does not arise.

| Particulars | Finance Bill, 2024 | Finance Bill, 2026 |

| Applicability for buybacks done | w.e.f. 1st October, 2024 | w.e.f. 1st April, 2026 |

| Taxable as | Deemed dividend. The holding cost of the bought back shares allowed as short term capital loss | Capital gains |

| Tax incidence on | Recipient shareholder | Recipient shareholder |

| Amount taxable | Entire buyback consideration | Gains on buyback, that is, Buyback consideration minus, cost of acquisition |

| Rate of tax | Applicable income tax slab rate | LTCG – 12.5%, subject to exemption upto Rs. 1.25 lacs STCG: 20% In case of promoters: 22%/ 30% (depending on whether domestic company/ otherwise) |

| Differential treatment for promoter shareholders | No | Yes, additional tax rates apply |

Under the erstwhile regime, the entire buyback consideration was taxable as deemed dividend, with the cost of acquisition claimable as capital loss. In such a case, the higher the cost of acquisition on such shares, higher would have been disincentive in the form of taxing the cost component as dividends. The benefits of capital loss depend on the existence of capital gains, and hence, the effective tax rates on buyback could not be ascertained.

In the amended tax regime, buyback consideration, minus, cost of acquisition, is taxed at flat rates of capital gains – 12.5%/ 20%, depending on whether the capital gains are long-term or short-term in nature.

The disincentives were two-fold:

Resultant market reaction: a sharp decrease in buyback offers during FY 24-25 as compared to previous financial years. As per the publicly available data in case of listed companies, the total buyback size for 2024-25 was ₹7,897 Crores when compared to 2023-24 with a buyback offer size of Rs. 49,836 crores, indicating a decrease of 84.2 per cent.

The number of buyback offers sharply declined, with only 17 instances of buyback offer by listed entities between 1st October 2024 till date (3rd February, 2026) as compared to about 36-40 instances in each of FY 22-23 and FY 23-24.

Pursuant to the Finance Bill, 2026, the buyback taxation appears to be rationalised in the following manner:

With this, while the tax incentive remains in the hands of the recipient shareholders, the tax treatment is rationalised in the form of value that is to be taxed and the manner in which tax is levied. However, the provision differentiates between a promoter and non-promoter shareholder.

In case of listed company

| Promoter | Promoter group |

| Person having control over the affairs of the company, or Named as promoter in annual return, prospectus etc. | Includes immediate relatives of promoters Entities in which >20% is held by promoters Entities that hold >20% in promoters etc. Persons identified as such under “shareholding of the promoter group” in relevant exchange filings |

The scope of “promoter group” thus, is much broader than “promoter”.

In case of an unlisted company

Question may arise on what does “indirect” shareholding mean? Does it include shareholding through relatives, or through other entities as well? The word “indirect” is not the same as “together with” or “persons acting in concert”. Indirect shareholding should usually mean shares held through controlled entities.

The amendments bring higher tax rates for promoters, in view of the distinct position and influence of promoters in corporate decision-making including in relation to buyback transactions. Promoters may want to influence buyback decisions for various reasons, for example:

In view of the promoter’s ability to influence buyback decisions to meet own objectives, additional tax is levied on buyback consideration received by the promoters, thus addressing any tax-arbitrage that could have been created through buybacks.

See our Quick Bytes on Budget, 2026 at here

Our other resources on buyback at here