Materiality thresholds increased, significant RPTs relaxed for small-value RPTs and newly incorporated subsidiaries

Highlights:

Following a 32-pager consultation paper proposing significant amendments to RPT provisions, towards ease of doing business, rolled out by SEBI on August 4, 2025, several amendments were approved by SEBI in its Board Meeting on 12th September, 2025. The SEBI (Listing Obligation and Disclosure Requirements) (Fifth Amendment) Regulations, 2025 have been notified on 19th November, 2025 amending the RPT framework for listed entities.

Some of our comments on the proposals, as recommended to SEBI, have also been accepted in the approved decisions. Our comments on the Consultation Paper may be read here.

Applicability of the Amendment Regulations

While the Amendment Regulations have been notified, the amendments with respect to the RPT framework are effective from the 30th day of the notification of the Amendment Regulations, that is, with effect from 19th December, 2025.

1. Materiality Thresholds: From One-Size-Fits-All to several sizes for the short-and-tall

A scale-based threshold mechanism has been approved, such that the RPT materiality threshold increases with the increase in the turnover of the company, though at a reduced rate, thus leading to an appropriate number of RPTs being categorized as material, thereby reducing the compliance burden of listed entities. The maximum upper ceiling of materiality has been kept at Rs. 5,000 crores, as against the existing absolute threshold of Rs. 1000 crores. The thresholds have been provided in Schedule XII, along with an illustration towards better understanding of the materiality thresholds.

Materiality thresholds as specified in Schedule XII:

Annual Consolidated Turnover of listed entity (in Crores)

Approved threshold (as a % of consolidated turnover)

Maximum upper ceiling (in Crores)

< Rs.20,000

10%

2,000

20,001 – 40,000

2,000 Crs + 5% above Rs. 20,000 Crs

3,000

> 40,000

3,000 Crs + 2.5% above Rs. 40,000 Crs

5,000 (deemed material)

Back-testing the proposal scale on RPTs undertaken by top 100 NSE companies show a 60% reduction in material RPT approvals for FY 2023-24 and 2024-25 with total no. of such resolutions reducing from 235 and 293, to around 95 to 119. The 60% reduction may itself be seen as a bold admission that the existing regulatory framework was causing too many proposals to go for shareholder approval.

Our Analysis and Comments

With the amendments becoming effective, RPT regime is all set to be a lot relaxed, with the absolute threshold for taking shareholders’ approval to be doubled to Rs. 2000 crores. In addition, for larger companies, there will be a scalar increase in the threshold, rising to Rs. 5000 crores. A lot lesser number of RPTs will now have to go before shareholders for approval in general meetings.

In times to come, a multi-metric approach, depending on the nature of the transaction, may be adopted, drawing on a consonance-based criteria as seen in Regulation 30 of the LODR Regulations, thus offering a more balanced and effective approach. See detailed discussion in the article here.

2. Significant RPTs of Subsidiaries: Plugging Gaps with Dual Thresholds

Extant provisions vis-a-vis Amended Regulations

Pursuant to the amendments in 2021, RPTs exceeding a threshold of 10% of the standalone turnover of the subsidiary are considered as Significant RPTs, thus, requiring approval of the Audit Committee of the listed entity. The following modifications have been approved with respect to the thresholds of Significant RPTs of Subsidiaries:

‘Material’ is always ‘Significant’: RPTs of subsidiary would require listed holding company’s audit committee approval if they breach the lower of following limits:

10% of the standalone turnover of the subsidiary or

Material RPT thresholds as applicable to listed holding company

This is a mathematical impossibility, since materiality threshold is based on “consolidated turnover”, and hence, includes the turnover of the subsidiary. Further, unlike networth, turnover cannot be a negative number, and hence, even if one or more of the subsidiaries of the listed entity are loss-making entities, the same cannot reduce the consolidated turnover of the listed entity to a number below the standalone turnover of its subsidiaries, whose accounts are being consolidated with the entity.

Exemption for small value RPTs: The threshold for Significant RPTs is subject to an exemption for small value RPTs based on the absolute value of Rs. 1 crore. Thus, where a transaction between a subsidiary and a related party (of the listed entity/ subsidiary), on an aggregate, does not exceed Rs. 1 crore, the same is not required to be placed for approval of the Audit Committee of the listed entity, even if the aforesaid limits are breached.

Alternative for newly incorporated subsidiaries without a track record: For newly incorporated subsidiaries which are <1 year old, consequently not having audited financial statements for a period of at least one year, the threshold for Significant RPTs to be based on lower of:

10% of aggregate of paid-up capital and securities premium of the subsidiary, or

Material RPT thresholds as applicable to listed holding company

The aggregate value of paid-up capital and securities premium, to be considered for the purpose of determination of Significant RPTs, should not be older than three months prior to the date of seeking AC approval. Since the value of paid-up capital and securities premium would be available with the company on a real-time basis, the same does not result in any additional compliance burden.

Our Analysis and Comments

For newly incorporated subsidiaries, the Consultation Paper proposed linking the thresholds with net worth, and requiring a practising CA to certify such networth, thus leading to an additional compliance burden in the form of certification requirements. Following the approval in SEBI BM, the Amendment Regulations provide a threshold based on paid-up share capital and securities premium, and hence, certification requirement does not arise.

3. Clarification w.r.t. validity of shareholders’ Omnibus Approval

Existing provisions vis-a-vis Amended Regulations

The existing provisions [Para (C)11 of Section III-B of LODR Master Circular] permit the validity of the omnibus approval by shareholders for material RPTs as:

From AGM to AGM – in case approval is obtained in an AGM

One year – in case approval is obtained in any other general meeting/ postal ballot

Pursuant to the Amendment Regulations, the timelines have been incorporated as a proviso to Reg 23(4). Further, a clarification has been incorporated that the AGM to AGM approval will be valid till the date of next AGM held within the timelines prescribed as per section 96 of the Companies Act.

4. Exclusions for retail purchases

Proviso (e) to Regulation 2(1)(zc) of the extant SEBI LODR Regulations exempted transactions involving retail purchases by employees from being classified as Related Party Transactions (RPTs), even though employees are not technically classified as related parties. Conversely, it includes transactions involving the relatives of directors and Key Managerial Personnel (KMPs) within its ambit.

The CP proposed that the exemption related to retail transactions should be expressly limited to related parties (i.e., directors, KMPs, or their relatives) to grant the appropriate exemption.

Under the extant framework, retail purchases made on the same terms as applicable to all employees were excluded from the meaning of RPTs when undertaken by employees, but not when made by relatives of directors or KMPs. This led to an inconsistent treatment, where similarly situated individuals receive different regulatory treatment solely on the basis of their relationship with the company.

Pursuant to the Amendment Regulations, the exclusion for retail purchases has been extended to the relatives of the directors/ KMP, when undertaken on “terms which are uniformly applicable/offered to all employees, directors, key managerial personnel and relatives of directors or key managerial personnel ”. While the language refers to terms offered to “employees, directors, key managerial personnel and relatives of directors or key managerial personnel”, the same cannot be read to mean that preferential terms can be granted to “director”, “KMPs” or “relatives of such directors/ KMPs” as a separate class. The terms need to be uniform to what is otherwise offered to “employees” by such a listed entity/ its subsidiaries.

5. Exemptions for RPTs between holding company and WoS

Regulation 23(5)(b) provides an exemption from audit committee and shareholder approvals for transactions between a holding company and its wholly owned subsidiary. However, the term “holding company” used in this context has remained undefined, leaving ambiguity as to whether it refers only to a listed holding company or includes unlisted ones as well.

A clarification has been inserted to provide the interpretational guidance that the term ‘holding company’ refers to the listed entity. The relevance of the aforesaid clarification would primarily be in cases where the unlisted subsidiary of the listed entity enters into a significant RPT with its wholly owned subsidiary (step-down subsidiary of the listed entity). Pursuant to the aforesaid proposal, as approved, no exemption will be available in such a case.

Conclusion

The amendments seem more or less welcoming, relaxing the RPT regime for listed entities. With the new leadership at SEBI meant to rationalise regulations, it was quite an appropriate occasion to do so. In sum, SEBI’s iterative approach to RPT governance demonstrates commendable responsiveness, contributing to the ease of compliances and in turn, of doing business by the companies.

Designated persons, being insiders with regular privileged information flow, cannot be doing what other investors can do. Several option trades may be devices to skim short term swings in share prices. can designated insiders do these? This interesting question, mostly ignored in Indian corporate practice, is explored in this article.

Derivatives trading is becoming increasingly popular in India, including amongst the retail investors. A recent address by SEBI’s Chairman urges the retail investors to assess their risk capacity while dealing in derivatives and avoid speculative trades. A July 2025 study by SEBI on trading activity of investors in Equity Derivatives Segment (EDS) indicates a relatively very high level of trading in EDS, as compared to other markets, particularly in index options. Further, within EDS, options segment (in premium terms) has shown growth at the fastest rate with average daily premium traded growing at the CAGR of 72% for index options and 54% for single stock options.

Given the large volumes of derivatives trading, in addition to the concerns on loss of investor’s money (nearly 91% of individual traders incurred net loss in EDS in FY 2025), it is also important to examine the concerns which would arise from an insider trading perspective. Pertinent questions would be whether derivatives trading also comes within the purview of insider trading, and if the answer to this is yes, whether it will also attract the prohibition around contra-trade, where the market participants bet on the short-term future value of the underlying assets to make a profit.

This article examines the aforesaid questions in the light of extant laws, and global position.

Prohibition on insider trading

The prohibition on insider trading comes from Section 12A of SEBI Act –

“No person shall directly or indirectly—

(d) engage in insider trading;”

Reg. 4(1) of PIT Regulations applicable universally to all insiders, also puts a blanket prohibition on trading when in possession of UPSI:

“No insider shall trade in securities that are listed or proposed to be listed on a stock exchange when in possession of unpublished price sensitive information:”

Para 4 of Schedule B (model CoC for listed entities) specifically pertains to trading by Designated Persons (DPs). They can trade subject to compliance with the Regulations – which provide for monitoring through the concept of “trading window” that is, during which a DP can be reasonably expected to have access to UPSI. Therefore, at such times, the trading window is closed, and the DP cannot trade in securities of that company. When the trading window is open, trading can take place after getting pre-clearance from the Compliance Officer.

In case of a fiduciary, the monitoring happens through a grey list. The concerned persons have to take preclearance from the Compliance Officer. Here, trading restrictions are applicable for securities of such listed companies, for which the person/s is/are acting as fiduciary.

Derivative trading vis-a-vis insider trading norms in India

Prohibition on derivative transactions under 1992 Regulations

“4.2 All directors/ officers/ designated employees who buy or sell any number of shares of the company shall not enter into an opposite transaction i.e. sell or buy any number of shares during the next six months following the prior transaction. All directors/ officers/ designated employees shall also not take positions in derivative transactions in the shares of the company at any time.”

Thus, under the 1992 Regulations, there was a complete and explicit prohibition on derivative transactions for designated employees. Note that the ban was for “any time” and not restricted to only while in possession of UPSI.

Position under the 2015 Regulations

While the contra-trade restrictions have been retained in the existing (2015) Regulations, the provision explicitly calling for blanket prohibition on derivative transactions was omitted. The Sodhi Committee Report does not contain any specific discussions in this regard.

Nonetheless, derivatives, qualifying the definition of “securities”, continue to be covered by the insider trading regulations. Reg 6(3) of the 2015 Regulations specifically refers to trading in derivatives, for the purpose of disclosure of trading in securities.

The disclosures of trading in securities shall also include trading in derivatives of securities and the traded value of the derivatives shall be taken into account for purposes of this Chapter.

As regards the value of derivatives for such disclosures, the same refers to the “traded value” of the derivatives. The format for such disclosures, as specified in the SEBI Master Circular on Surveillance of Securities Market (Annexure – I), also refers to disclosure of trading in derivatives on the securities of the company, and requires calculation of notional value of options based on premium plus strike price of the options.

Further, trading in equity derivative instruments i.e. Futures and Options of the listed company are covered by the system driven disclosures [Para 3.3.3. of the SEBI Master Circular].

Whether the immediate relative of the designated person can trade in the derivatives of the company?

Answer

Yes. Designated person and its immediate relative can trade in derivatives when not in possession of UPSI and such trades are accordingly governed by the code of conduct.

Thus, the following points may be noted –

A person cannot undertake insider trading in securities – directly or “indirectly”. Derivatives are defined under Section 2(ac) of the Securities Contracts (Regulation) Act, 1956.

“Derivative”—includes

(A) a security derived from a debt instrument, share, loan, whether secured or unsecured, risk instrument or contract for differences or any other form of security;

(B) a contract which derives its value from the prices, or index of prices, of underlying securities;

(C) commodity derivatives; and

(D) such other instruments as may be declared by the Central Government to be derivatives;

Therefore, trading in derivatives may technically tantamount to trading in underlying securities – indirectly. This is irrespective whether the transaction results in actual delivery or is only net-settled in cash.

The definition of “securities” includes derivatives – hence, there should not be any confusion as to why trading in derivatives of the underlying securities should be excluded from the scope of “trading”

Chapter III of PIT Regs. which is applicable to all insiders (note, that DPs are closest insiders), explicitly says that trading in securities includes trading in derivatives.

SEBI FAQ (Q. 52 above) makes it clear that trading in derivatives is only possible when the DP/ immediate relative is not in possession of UPSI[1]. Of course, whether or not the DP/immediate relative is having possession of UPSI or not, is to be seen at the time the trading is proposed to be done.

Therefore, what is clear is that unlike the 1992 Regulations, there is no explicit provision calling for blanket prohibition on the derivative transactions by DPs and their immediate relatives. However, restrictions as are applicable otherwise in relation to securities of a listed company, would also apply to derivatives having such securities as underlying. Of course, the restriction is not a blanket prohibition as was in 1992.

In simple terms, a derivative should be treated no differently than the underlying security itself. Consequently, in view of the author:

When the trading window is closed, a DP should not be allowed to enter into a derivative in securities as well.

When the trading window is open, trading in derivatives should be subjected to preclearance.

The above position is also apparent in other jurisdictions, where, in the context of insider trading norms, dealing in derivatives is equivalent to dealing in underlying securities.

Once it is clear that trading in derivatives is equivalent to trading in underlying security, then it is obvious to conclude that trading in derivatives will also be governed by contra-trade prohibition in the same manner as trading in the underlying itself. See detailed discussion below.

Issues concerning contra-trade

Rationale for prohibiting contra-trade

The insider trading norms around the world prohibit contra trade or short swing trades by the persons privy to or likely to be privy to unpublished price sensitive information (UPSI) about the listed securities. The SEBI (Prohibition of Insider Trading) Regulations, 2015 restricts the Designated Persons (DPs) and their immediate relatives from undertaking reversal trades, within six months from undertaking the previous trade transaction. The intent is to prevent the abuse of UPSI by making short-term profits through unfair means.

The 2008 Consultation Paper states, “It is assumed that insiders have a long term investment in the company and are not expected to make rapid buy/sell transactions, which are assumedly based on at least some level of superior access to information, whether material or not.”

Hence, whenever there is a contra-trade within a short span of time (6 months), there is a presumption that the said trade is based on some “superior” access to information – as such, contra-trades are simply prohibited. The DP cannot undertake a contra-trade even if it is contended that he does not have UPSI.

Contra-trade in case of derivatives

Naturally, a question arises on whether DPs can trade in derivatives, and if so, when does the same qualify as contra-trade or otherwise, and the consequences that follow. Let’s take a simple illustration – Mr. A, a DP of X Ltd. purchases 100 shares of X Ltd. on 1.11.2024. Then purchases a put option on 15.11.2024, for all 100 shares. On 01.02.2025, on maturity of the put option, A exercised the put option and sold all the 100 shares. All these transactions, as one would note, are happening within a period of 6 months. The question is – whether A was allowed to undertake the 2nd transaction of purchasing a put option within 6 months of the 1st transaction.

There is a question appearing in SEBI FAQ, as follows:

37.Question

In case an employee or a director enters into Future & Option contract of Near/Mid/Far month contract, on expiry will it tantamount to contra trade? If the scrip of the company is part of any Index, does the exposure to that index of the employee or director also needs to be reported?

Answer

Any derivative contract that is physically settled on expiry shall not be considered to be a contra trade. However, closing the contract before expiry (i.e. cash settled contract) would mean taking contra position. Trading in index futures or such other derivatives where the scrip is part of such derivatives, need not be reported.

This question above clearly deals with treatment of expiry of a derivative contract or settlement of a derivative contract as to whether those events would be treated as contra-trade. That is, a culmination of a derivative contract, resulting in the delivery of the underlying will, of course, not amount to a separate “trade” – therefore, there is no question of a contra-trade. On the other hand, where no physical delivery is taken, rather, settled in cash (payment of the difference between the contract’s entry price and market price at expiry), the same amounts to a “sell” trade, thereby, a reversal of the position of the DP. Thus, where the contract is proposed to be settled prior to expiry, it would result in a different transaction/trade – thus, it should be treated as a contra-trade.

Now, if seen in a practical context, in India, the validity of derivatives contract would usually be less than 6 months (typically 1-3 months[2]). And, typically, these derivative transactions in such cases are net-settled before expiry, rather than culminating in actual delivery of securities[3]. Options enable the investors to speculate in shares of higher values and volumes as compared to the cash segment since the only amount payable would be the premium and the net difference in the strike price and spot price later on. Further, cash settlement in derivatives provides a higher leverage to the trader.

In the above scenario, there will always be a higher possibility of a contra-trade. The illustrations below explain the same:

S. No

Transaction

Remarks (assuming T1 and T2 happen within a period of 6 months)

1

T1 – Buy call option T2 – Cash settlement

Contra trade. Buying call option is equivalent to a “buy” transaction. Subsequent cash settlement indicates a “sale” transaction.

2

T1 – Buy call option T2 – Physical settlement

Not a Contra trade. Buying call option is equivalent to a “buy” transaction, subsequent physical settlement only results in delivery of such shares.

3

T1 – Buy call option T2 – Expiry of option on account of out-of-the money

Not a Contra trade. Buying call option is equivalent to a “buy” transaction, however, did not result in delivery on account of the strike price > market price at the time of expiry.

2

T1 – Sell call option T2 – Cash settlement

Contra trade. Selling call option is a “sale” transaction. Cash settlement indicates a “buy” transaction.

3

T1 – Buy put option T2 – Cash settlement

Contra trade. Buying put option is a “sale” transaction. Not taking physical delivery of the shares and carrying out cash settlement indicates a “buy” transaction.

4

T1 – Sell put option T2 – Cash settlement

Contra trade. Selling put option is a “buy” transaction. Cash settlement is deemed to be a “sale” transaction.

As such, trading in derivatives would be much more vulnerable to chances of insider trading, than actual trading in securities. Hence, it becomes extremely important to put mechanisms in place to ensure that derivatives trading be subjected to enhanced restrictions and controls, as suggested below.

Enhanced safeguards in respect of derivative transactions by DPs

It is quite clear that a derivative transaction that results in cash settlement construes a contra-trade. On the other hand, where physical delivery is taken (although it is not very common to close a derivative contract in physical settlement), the derivative transaction is not considered as a contra-trade (although the same is also to be matched against the previous trade in cash segment). Therefore, in order to ensure that the trade does not result in contra-trade, it is essential that the derivative is either settled by delivery or simply expires on the maturity date, and that there is no cash settlement.

In order to ensure this, in case of purchase of options (put/ call) by the DP, pre-clearance may be provided by the Compliance Officer subject to receipt of a declaration that the DP shall necessarily undertake physical settlement of such trades at the maturity date. Of course, there would be no concerns in case of an out-of-the money option, that is, where prior to the expiry of the contract, the market price remains below the strike price. An out-of-the money option does not result in any profits in the hands of the option holder, however, prevents additional loss in the face of exercising an option where the strike price at which the option is exercised and shares are acquired is higher than the current market price at the time of such exercise of option (upon maturity of the contract).

On the other hand, in case of sale of options (put/ call) by the DP (that is, where the DP is the writer of the option), the physical settlement cannot be guaranteed by the DPs, and chances of contra-trade are higher, as the counterparty (that is, buyer of the option) may choose to have cash settlement before the expiry of the derivative contract. Therefore, in order to obviate the possibility of a contra-trade happening, it might be necessary to completely prohibit sale/writing of options by DPs. This prohibition may be enabled through the code of conduct. . In fact, it is seen that several large listed companies have put a blanket prohibition on derivative transactions by DPs and their immediate relatives.

Contra-trade where there is a preceding/succeeding trade in securities

Besides, this FAQ does not deal with a scenario where a DP who has traded in securities already, now proposes to enter into a derivative contract within a span of 6 months from the date of original contract.

However, one thing is clear from this FAQ – the very entering into the derivative contract (and not expiry/maturity thereof) has been considered to be a trade by SEBI. Also, as discussed in the first part of this article, trading in derivatives should be considered as trading in securities itself. As such, if there has been a trade in securities, and there is a subsequent trade, although in derivatives of those very securities, it would result in contra-trade. That is, if in the above example, A enters into a “put option” – then he will have the right but not the obligation to “sell” the underlying shares, within 6 months of buying the shares. Whether to actually “sell” or have a concrete “right to sell” at a future date at or above a given price – it is nothing but a clear case of “contra-trade”.

For instance, assume a DP purchases shares of the listed company on 1.1.2025. Subsequently, on 1.3.2025, the DP purchased a put option. The put options, akin to a sale transaction, results in contra-trade when matched against the previous “buy” transaction in the cash segment, within a gap of less than 6 months between the two transactions. Similarly, where a call option is bought within 6 months of a previous sale transaction, the same results in contra trade.

Compliances in relation to trading in derivatives by DPs

(1) Appropriate mechanisms in the Code of Conduct

Prior to making trades in the derivatives, it is important for the DP to ensure that the Code of Conduct does not prohibit such trades. Unless expressly prohibited, the Code of Conduct may contain necessary clauses as discussed above, in order to enable derivative trading by DPs, subject to enhanced controls on the same.

(2) Manner of identification of derivative trades

The trading in equity derivative instruments i.e. Futures and Options of the listed company are covered by the system driven disclosures [Para 3.3.3. of the SEBI Master Circular]. Hence, an instance of contra trade through derivative instruments is easily identifiable by the Compliance Officer.

(3) Pre-clearance for the purpose of trading

Not all trades of DPs are pre-cleared by the Compliance Officer. The pre-clearance is required only for such trades that exceed the thresholds provided in the CoC of the respective listed entity, generally Rs. 10 lacs or more. Here, the value of trade becomes important, and cannot be just limited to the premium payable/ receivable at the time of purchase/sale of such contract. The price of the securities is also relevant. Pre-clearance may be granted by the Compliance Officer, subject to such conditions and undertaking as suggested above.

(4) Trading during closure of trading window

The DPs cannot trade in the derivatives of a company’s securities during the trading window closure period. In order to ensure the trades are not done during the trading window closure period, the concept of freezing of PAN has been introduced – both at the level of the DP as well as their immediate relatives (see an article here). However, the freezing of PAN is applicable only to the quarterly TW closure pending announcement of financial results.

The DP to ensure that neither him, nor his DPs trade in the derivatives of the company during the closure of trading window period.

(5) Reporting of trades in derivatives

As regards the reporting of trade in derivatives, the SEBI Master Circular provides guidance on calculation of notional value of trades, to be calculated based on premium plus strike price of the options. The disclosure of trades are primarily system-driven, based on the PAN details of the DPs updated with the designated depository. Having said that, in case of trades of the immediate relatives of the DPs, or where the PAN details are not updated with the depository, manual disclosures are required for such trades.

(6) Consequences of violation – disgorgement of profits and penal actions

A breach of contra trade restriction leads to disgorgement of profits made and its remittance to SEBI for credit to IPEF. Here, the question arises on what is considered the value of profits for disgorgement to IPEF, in the context of derivatives.

Where the transaction pertains to ‘sale’ of options, the profits would usually be the premium earned by the seller of options. On the other hand, in case of ‘purchase’ of options, the profits should be the difference between the buy and sale value, net of other expenses in connection with such option contracts.

Guidance may also be taken from 17 CFR § 240.16b-6(d) of the SEC Act, which states that the amount of profit shall be calculated as the profits that would have been realized had the subject transactions involved purchases and sales solely of the derivative security valued as of the time of the matching purchase or sale, and calculated for the lesser of the number of underlying securities actually purchased or sold. The amount of such profit shall not exceed the premium received for writing the option.

In addition to disgorgement of profits, penalty may also be levied. For instance, in an adjudication order dated 29th April 2022, the purchase and sale of options on consecutive days resulted in contra trade violation attracting a penalty of Rs. 2 lacs.

Global view on contra-trade in derivatives

Section 16(b) of the Securities and Exchange Commission Act, 1934 of the USA, restricts contra trade in equity securities, for a beneficial owner holding more than 10% of any class of any equity security, director and officer, including a security-based swap agreement involving any such equity securities. Exemptions have been prescribed for derivative transactions in certain cases in CFR § 240.16b-3 of the General Rules and Regulations.

The General Rules and Regulations of the SEC provides detailed guidance on when a derivative trade qualifies as a short swing trade and vice versa. The same has been summarised here:

Transactions that qualify as “purchase” of underlying securities:

establishment/ increase of a call equivalent position

liquidation/ decrease of a put equivalent position

Transactions that qualify as “sale” of underlying securities:

establishment/ increase of a put equivalent position

liquidation/ decrease of a call equivalent position

Transactions that are exempt from short swing restrictions:

increase/ decrease pursuant to fixing of the exercise price of a right initially issued without a fixed price, where the date the price is fixed is not known in advance and is outside the control of the recipient

Closing as a result of exercise or conversion of the option, that is,

Acquisition of underlying securities at a fixed exercise price due to the exercise or conversion of a call equivalent position

Except in case of out-of-the money option, warrant or right

Disposition of underlying securities at a fixed exercise price due to the exercise of a put equivalent position.

Where the person trading is not a major beneficial holder, and thus, an insider, at the time of both the transactions which are being termed as contra trade [Section 16-b of SEC Act].

Other exemptions apply w.r.t. transactions with the issuer, subject to certain conditions and transactions pursuant to tax conditioned plans [CFR § 240.16b-6]

Article 164 of the Financial Instruments and Exchange Act, 1948 of Japan also restricts reverse trades in specified securities, by major shareholders and officers etc, who may have obtained secret information in the course of their duty or by virtue of their position. Specified securities, for the purpose of the said provision, include Derivatives [Article 163 r/w Article 2(xix)].

Judicial precedents on contra trade transactions

In Allaire Corporation v. Ahmet H. Okumus, the Circuit Court held that when the option is written by the insider, he has no control over whether the options buyer will exercise the option or square it off. Thus, trade carried out pursuant to selling an option shall not be considered a transaction for the purpose of determining whether a set of transactions is a contra trade or not. The facts of the case involved writing another option within six months of expiry of the first option remaining un-exercised. Note that the expiration of the first set of options does not constitute a purchase matchable to the later sale of a different set of call options.

However, as clarified in Roth v. The Goldman Sachs Group, Inc., et al., No. 12-2509 (2d Cir. 2014), when matched against its own writing, the expiration of an option within six months is a “purchase transaction” for the purpose of section 16-b.

The danger of misuse of non-public information exists at the time the option is written, and the expiration of that option is the moment of profit. Matching writings with expirations of different options does not clearly advance the purposes of the statute. Options written at different times are less likely to give rise to speculative abuse, and matching the expiration of an option only to its own writing recognizes the more evident danger.

In Chechele v. Sperling,the Circuit Court held that where pursuant to the settlement of the futures contract, the pledge on shares is revoked, the revocation is not considered to be a ‘purchase’ transaction to be combined with the open market sale of such shares to identify these trades as contra trades.

The exercise of a traditional derivative security is a “non-event” for section 16(b) purposes.

In the case of Macauley Whiting v. Dow Chemical Company, the Court held that where the insider has exercised an option to purchase shares and his spouse has sold shares within a period of 6 months, these transactions shall be considered to be short swing trades (contra trades).

In the context of § 16(a), the Commission has evolved a dual test of an insider’s beneficial ownership of his or her spouse’s shares. Such beneficial ownership may derive from the insider’s “power to revest” in himself title to those shares.[6] Or it may result from his enjoyment of ‘benefits substantially equivalent to those of ownership.’

In the case of Kern County Land Co. v. Occidental Petr. Corp., a person fails in his attempt of a takeover due to a defensive merger carried out by the target company. During the period when the merger was being finalised, the acquirer entered into an option agreement with the transferee company. The option agreement stipulated that if and when the merger succeeds, the transferee company would buy the shares held by the acquirer pursuant to the takeover attempt. The US Supreme Court held that such a set of trades would not result in contra trade because the actions of the acquirer were involuntary.

The option was grounded on the mutual advantages to respondent as a minority stockholder that wanted to terminate an investment it had not chosen to make and Tenneco, whose management did not want a potentially troublesome minority stockholder; and the option was not a source of potential speculative abuse, since respondent had no inside information about Tenneco or its new stock.

Concluding Remarks

In practice, several large listed companies continue to prohibit trading in derivatives by the Designated Persons and their immediate relatives through their Code of Conduct. The regulations do not enforce such blanket prohibition, although no trading can be done that falls foul of other requirements of the Regulations – viz., trading while in possession of UPSI, contra trades, trading during closure of trading window, trading without pre-clearance etc.

Having said that, derivatives, by nature, are short term trades based on the expectations of the movement in price of the securities in a certain direction within a short period of time. Therefore, in case of trades by DPs, the chance of such trades being motivated by an information asymmetry is comparatively higher, thereby potentially resulting in an insider trading allegation on such DP.

[1] Annexure VII of ICSI Guidance Note on Prevention of Insider Trading states “The designated persons and their immediate relatives shall not take any positions in derivative transactions in the Securities of the company at any time.” However, the source of such stipulation is not clear, as currently there is no corresponding provision in PIT Regulations.

Since the introduction of High Value Debt Listed Entities (HVDLEs) as a category of debt-listed entities placed on a similar pedestal to equity-listed entities in terms of corporate governance norms, the regime has undergone several rounds of extensions and regulatory changes. After several extensions towards a mandatory applicability of corporate governance norms, a new Chapter V-A was introduced in LODR, vide amendments notified on 27th March 2025 (see a presentation here), amending, amongst others, the thresholds towards classification of an entity as HVDLE (increased from Rs. 500 crores to Rs. 1000 crores). The new chapter, however, was not updated for the changes brought for equity-listed entities vide the LODR 3rd Amendment Regulations, 2024 and required some refinement, particularly, in respect of provisions pertaining to related party transactions (see an article – Misplaced exemptions in the RPT framework for HVDLEs and the representation made to SEBI).

In order to address the gaps as well as providing some relaxations to HVDLEs, SEBI released a Consultation Paper on 27th October, 2025 (CP) primarily proposed an increase in the threshold for identification as HVDLEs and alignment of provisions of Chapter V-A with the corresponding provisions in Chapter IV subsequent to LODR 3rd Amendment Regs, 2024 facilitating ease of doing business, including measures related to RPTs. The proposals were approved by SEBI in its Board Meeting held on 17th December, 2025.

SEBI vide Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2026 (‘LODR Amendment 2026’), has notified the following amendments effective from January 22, 2026.

Threshold for identification of HVDLEs

Increased from extant Rs. 1000 crores to Rs. 5000 crores . Further, the sunset clause of 3 years as per Reg 15 (1AA) & Reg. 62C(2) will not be applicable to entities that cease to be HVDLE due to revised thresholds.

Based on the data of pure debt listed entities as on June 30, 2025, revision in threshold will reduce the number of HVDLE entities from 137 to 48 entities (apprx. 64% entities)

VKCO Comments: The increase in the threshold was necessitated on account of the huge compliance burden placed on HVDLEs coupled with the fact that such threshold is disproportionately low for NBFCs engaged in substantial fundraising through debt issuances. Further, the proviso to Reg. 15 (1AA) & Reg. 62C (2) expressly clarifies the position for entities ceasing to be an HVDLE as on January 22, 2026 with the revised threshold coming into effect, that it need not continue to comply with the CG requirements for a period of 3 years. Earlier there had been instances of entities that ceased to be HVDLEs due to outstanding value of listed debt securities as on March 31, 2025 receiving notices from SEs for non-compliance with CG norms despite such entities ceasing to meet the revised threshold.

Alignment of corporate governance norms for HVDLEs with that for equity-listed entities

Board composition, committees, filing of vacancy of director/ KMPs etc.

Insertion of proviso to clarify that prior approval of shareholders is required for directorship as NED beyond the age of 75 years at the time of appointment or re-appointment or any time prior to the NED attaining the age of 75 years to ensure alignment with similar amendment made for equity listed entities [Reg 62D(2)/ Reg 17(1A)]

Time taken to receive approval of regulatory, government or statutory authorities, if applicable, to be excluded from the 3 months’ timeline for shareholders’ approval for appointment of a person on the Board [Reg 62D(3)/ Reg 17(1C)]

Exemption from obtaining shareholders’ approval for nominee directors of financial sector regulators or those appointed by Court or Tribunal, since such nomination is for the purpose of oversight and upholding public interest, and by SEBI registered Debenture Trustee registered under a subscription agreement for debentures issued by HVDLEs [Reg 62D(3)/ Reg 17(1C)]

Any vacancy in the office of a director of an HVDLE resulting in non-compliance with the composition requirement for board committees i.e., AC, NRC, SRC and RMC to be filled within 3 months [Proviso to Reg 62D(5)/ Reg 17(1E)]

Any vacancy in the office of a director of an HVDLE on account of completion of tenure resulting in non-compliance with the composition requirement for board committees i.e.. AC, NRC, SRC and RMC to be filled by the date such office is vacated [Second proviso to Reg 62D(5)/ Reg 17(1E)]

Additional timeline of 3 months for filling vacancy in the office of KMP in case of entities having resolution plan approved, subject to having at least 1 full-time KMP [Reg 62P (3)/ Reg 26A (3)]

Secretarial Audit

Alignment of the provisions of Secretarial Audit and Secretarial Compliance Report with Reg 24A as applicable to equity listed entities, to strengthen the secretarial audit and to prevent conflict of interests, which mandates the following: [Reg 62M(1)/ Reg 24A]

An individual may be appointed for a term of 5 years and a firm may be appointed for a maximum of 2 terms of 5 years each subject to approval of shareholders in the annual general meeting. Thereafter a cooling-off period of 5 years will be applicable;

Requirements relating to eligibility (being a Peer Reviewed Company Secretary) and disqualifications, removal of secretarial auditors prescribed.

The Secretarial Compliance Report also to be submitted by a Peer Reviewed Company Secretary or Secretarial Auditor fulfilling the eligibility requirements indicated in Reg. 24A.

VKCO Comments: Further disqualifications for Secretarial Auditor and list of services that cannot be rendered by the Secretarial Audit was prescribed vide Annexure 2 and Annexure 3 of SEBI Circular dated December 31, 2024 and further clarified vide SEBI FAQs on Listing Regulations (FAQ no. 5) and list of services provided by ICSI.

The amendments made in Reg 24A in December, 2024 were required to be ensured by the equity listed companies with effect from April 1, 2025 for appointment, re-appointment or continuation of the Secretarial Auditor of the listed entity. Therefore, it was amply clear that the applicability is prospective and to be ensured while appointing Secretarial Auditor for FY 2025-26 onwards. Reg. 24A (IC) clarifies that any association of the individual or the firm as the Secretarial Auditor of the listed entity before March 31, 2025 is not required to be considered for the purpose of calculating the tenure.

Pursuant to LODR Amendment 2026, Reg. 62M (1) cross refers to the requirements under Reg 24A which in turn mandates compliance with effect from April 1, 2025. However, it may not be practically feasible for HVDLEs to ensure compliance towards the end of the financial year and a transition time may be required by such HVDLEs. In our view, the requirements should be applicable for Secretarial Auditor appointments with effect from April 1, 2026 which will be required to be done with shareholders’ approval at the AGM 2026 and not impact the existing tenure/ appointments already done by HVDLE.

Related Party Transactions

Alignment of RPT related provisions with Reg 23, instead of reproducing each of the amendments made in Reg 23 effective from December 13, 2024 and November 19, 2025 [Reg 62K (1)]

Turnover scale based materiality thresholds for RPTs and other amendments applicable to equity-listed entities are now applicable to HVDLEs (see an article on the approved amendments here)

NOC of debenture-holders through DT to be obtained in the manner prescribed by SEBI [Reg 62K (5)] (see our FAQs here)

Aligning the exemptions from RPT approval and clarification on ‘listed’ holding company, with amendments made in Reg. 23 (5) [Reg 62K (7)]

VKCO Comments: Pursuant to the above amendments, HVDLEs will be able to avail the benefits of recent amendments made in Reg 23 as detailed below:

Remuneration and sitting fees paid by the listed entity or its subsidiary to its director, key managerial personnel or senior management, except who is part of promoter or promoter group, shall not require audit committee approval or disclosure if it is not material.

Independent directors of the audit committee, can provide post-facto ratification to RPTs within 3 months from the date of the transaction or in the immediate next meeting of the audit committee, whichever is earlier, subject to certain conditions like transaction value does not exceed rupees one crore, is not material etc. The failure to seek ratification of the audit committee can render the transaction voidable at the option of the audit committee and if the transaction is with a related party to any director, or is authorised by any other director, the director(s) concerned shall indemnify the listed entity against any loss incurred by it. Audit committee can grant omnibus approval for RPTs to be entered by its subsidiary in addition to listed entity subject to the certain conditions.

Exemption for RPTs in the nature of payment of statutory dues, statutory fees or statutory charges entered into between an entity on one hand and the Central Government or any State Government or any combination thereof on the other hand or transactions entered into between a public sector company on one hand and the Central Government or any State Government or any combination thereof on the other hand.

Scale based threshold for determining material RPTs ranging from minimum of 10% of annual consolidated turnover to Rs. 5000 crore based on the consolidated turnover of the HVDLE.

Prior approval of the audit committee of the listed entity required for a subsidiary’s RPTs above Rs. 1 crore if it exceeds the lower of 10% of the annual standalone turnover of the subsidiary (or 10% of paid-up share capital and securities premium, if no audited financials of at least one year) or the listed entity’s material RPT threshold under Regulation 23(1) of LODR.

Omnibus shareholder approvals for RPTs granted at an AGM shall be valid up to the next AGM held within the timelines prescribed under Section 96 of the Companies Act, 2013 (currently maximum 15 months), while such approvals obtained in general meetings (other than AGMs) shall be valid for a maximum of one year

The most critical point that remains pending to be addressed is the nature of disclosures to be made before the audit committee and shareholders while approving RPTs – as to whether the existing disclosure requirements as per Chapter VIII of SEBI Master Circular dated July 11, 2025 will apply or the threshold based disclosure requirement as applicable to equity listed companies i.e. disclosure as per Annexure 13A of SEBI Circular dated October 13, 2025 for RPTs not exceeding 1% of annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity or ₹10 Crore, whichever is lower, and disclosure as per ISN on Minimum information to be provided to the Audit Committee and Shareholders for approval of Related Party Transactions for RPTs exceeding the aforesaid limit. Considering that HVDLEs will be proceeding with obtaining omnibus approval for RPTs proposed to be undertaken during FY 2025-26, in the absence of any clarification or amendment in the Master Circular, the HVDLEs will continue to follow the existing disclosure requirements.

Other amendments

Recommendations of board to be included along with the rationale in the explanatory statement to shareholders’ notice [Reg 62D(17)/ Reg 17(11)]

Exemption from shareholders’ approval requirements for sale, disposal or lease of assets between two WoS of the HVDLE [Reg 62L (6)/ Reg 24(6)]

Minor terminology changes from year to financial year, income to turnover etc.

Disclosure requirement of material RPTs in quarterly corporate governance report omitted. Format and timeline of period CG compliance report to be prescribed by SEBI [Reg 62Q(2)/ Reg 27(2)]

VKCO Comments: For equity-listed entities, reporting on compliance with corporate governance norms are a part of Integrated Filing – Governance, required to be filed within 30 days from end of each quarter. The move to provide flexibility to SEBI in prescribing timelines for corporate governance filings may be in order to extend the applicability of Integrated Filing requirements to HVDLEs as well.

Conclusion

While the present amendment strictens the compliance requirement for the HVDLEs with outstanding listed debt securities of Rs. 5000 crore or more, it also provides the ease of compliance as provided for certain matters to equity listed companies. The actionable for HVDLEs will be mainly amending the RPT policy to align with the amended requirements, evaluate the eligibility of the existing secretarial auditor in the light of amended requirements. The entities that cease to be HVDLEs can evaluate the need to retain the committees and policies, in the light of applicable laws.

The position of a compliance officer is a reflection of challenges. As much as the individual holding this position enjoys reputation and superintendence, there is a constant expectation from regulatory authorities of ensuring compliance and active enforcement of the law. In the context of PIT regulations, SEBI does not expressly specify the extent of a Compliance Officer’s role(hereinafter referred to as CO) in supervising a particular compliance; however, various adjudication orders throw light on the expectations from CO. In recent cases, the regulatory watchdog has held the CO, amongst others, liable for lapses in complying with the PIT regulations, whereas in some cases, it has exonerated the CO from any liability imposed by default, owing to its superlative position in the company. The article delves into the nuances of the role of a CO, aiming to propose a clear, definitive line of duty to be observed and appreciated by the SEBI during instances of violation of this law.

2. Identifying a CO- SEBI (PIT) Regulations 2015

Reg 2(1)(c) of the SEBI (PIT) Regulations defines a Compliance Officer as: 1. Any senior officer, designated so and reporting to the board of directors 2. A financially literate person capable of deciding compliance needs. 3. A person responsible for compliance with policies, procedures, maintenance of records, and monitoring adherence to the rules for the preservation of:

Unpublished price-sensitive information (hereinafter referred to as UPSI)

Monitoring of trades, and

The implementation of the codes specified in these regulations is under the supervision of the board of directors of the listed company.

It is to be noted that the definition gives way for any senior officer to be a compliance officer to perform obligations[1] stated in the following segment. The SEBI had also noted in a matter that the interim company secretary of a company who has not been appointed as the compliance officer under PIT during the UPSI period cannot be forthwith held liable.[2] The above duties (monitoring, implementation, maintenance, etc) are, though explanatory of the role of a compliance officer, not definitive or fenced in form and substance. The SAT held in a case that a CO cannot be blamed for disclosures under the above regulation, of board-approved misstatements.[3] Relevant extracts are given below:

“The Compliance Officer works under the direction of the Board of Directors of the Company. It was not open to the Compliance Officer to comply with Clause 36 of the Listing Agreement. At the end of the day, the Compliance Officer is only an employee of the Company and works on the dictates and directions of the management of the Company. Thus, when the entire management is being penalised, it was not open to the AO to also book the Compliance Officer for the said fault.”

Now this brings us to the question as to the actual duties and obligations of a CO, and its viable extent to avoid stretched expectations. There cannot be a straight-jacket formula, as this depends on the nature of the violation of a particular category of regulations under SEBI PIT.

3. Responsibilities of a CO – SEBI (PIT) Regulations 2015

Before proceeding to the liabilities of a CO, it is important to delineate the main obligations of a CO as per SEBI (PIT) Regulations. These are given below:

Every listed company, intermediary and other persons formulating a code of conduct shall identify and designate a compliance officer to administer the code of conduct and other requirements under these regulations [Reg 9(3)].

The CO must review the trading plans submitted by designated persons. For doing so, he can ask them to declare that he does not have UPSI or that he must ensure that the UPSI in his possession becomes generally available before he commences his trades [Reg 9(3)]. The CO shall report to the board and shall provide reports to the Chairman of the Audit Committee, or to the Chairman of the board at such frequency stipulated by the board, being not less than once a year [Reg 9(3)].

All information shall be managed within the organisation on a need-to-know basis, and no UPSI shall be conveyed to any person except in furtherance of legal duties, subject to the Chinese wall procedures [Reg 9(3)].

When the trading window is open, trading by designated persons shall be subject to pre-clearance by the compliance officer if the value of the proposed trades is above such thresholds [Reg 9(3)].

The timing for re-opening of the trading window shall be determined by the CO, upon considering several factors, including the UPSI becoming generally available and being capable of assimilation by the market, which shall not be earlier than forty-eight hours after it becomes generally available [Reg 9(3)].

Before approving any trades, the compliance officer shall seek declarations to the effect that the applicant for pre-clearance is not in possession of any UPSI. He shall also have regard to whether such a declaration is capable of being inaccurate. The compliance officer shall confidentially keep a list of certain securities as a “restricted list”, which shall be the basis for reviewing applications for pre-clearance of trades [Reg 9(3)].

These are some of the duties specified in the Regulations. However, the extent of liability of the CO arising from the aforesaid duties requires determination.

4. Potential liabilities of CO:

To determine the extent of obligations of a CO with respect to disclosures, records, or any compliance, there is a need to segregate the duties of a CO into specific categories crafted according to the several aspects to be considered while ensuring adherence to the PIT regulations. In this direction, an effort has been made below:

Closure of Trading window:

A CO cannot be held responsible for not closing the window for certain traders, if the UPSI was not disclosed by the designated person or if the person executed a trade much before the UPSI becomes generally available, in contravention of the trading plans approved or if the disclosure was concealed inadvertently by the board[4].

A CO can also not be held liable if an insider trades in the securities of the company with UPSI, without obtaining pre-clearance from him, even after asking the person to disclose UPSI. He cannot claim that he did not close the trading window on the grounds of lack of awareness of a demand notice received from an operational creditor, which was the start date of UPSI, upon being disclosed to the stock exchange.[5]

So, it is important to understand that a Compliance Officer is not expected to possess perfect foresight, but to exercise prudent diligence. When the trading window is closed in good faith, established procedures are adhered to, and no proof of negligence or systemic failure exists, regulatory liability cannot be imposed on a CO merely on the basis of retrospective evaluation of his inherent duty[6]. He must tend to certain nuances (such as whether the issue of ESOPs is permissible during the window closure)[7], and employ the best professional judgment to red-circle information as UPSI to ensure effective closure of the trading window without breaches.[8]

Maintenance of structured digital database (SDD):

A CO can be held liable for not maintaining SDD as per Annexure 9 of the guidance note on insider trading. However, the SDD must be “real-time and tamper-proof”. The CO would not be held liable if no particular system/controls existed, such as an audit trail mechanism to secure the SDD and prevent leaks. However, citing delay in procurement of software, accidental omissions[9] or the lack of manpower to scrutinise bulky entries of transactions[10] cannot be regarded as valid arguments by a CO.

It is also pertinent that the CO of a listed company adheres to the standard operating procedure for filing the SDD certificate with the stock exchange within a particular deadline. Failure to do so shall attract the following actions by the exchange within 30 days from the due date of filing the SDD certificate: a. Display the name of the company as “non-compliant with SDD” and the name of the compliance officer on the SE website; b. No new listing approvals will be granted (except for bonus issue and stock split); among other actions.[11]

Verifying documents given by the Board:

The SAT has held in the appellate order of V Shanker vs SEBI, taking reference from the case of Prakash Kanungo, that compliance officers are not responsible for re-auditing board-approved documents related to any information on securities, transactions, etc, to test their financial literacy[12]. As seen in the definition, a CO shall work under the supervision of the board and cannot question the decisions of the board. Ergo, he cannot be held liable for making invalid, board-approved disclosures per Reg 7 of the regulations.

Trading by designated persons: Granting of Pre-Clearance and Contra trade restrictions

Pre-clearance becomes a mandatory action in cases where a trading plan has not been submitted/approved by him. The CO must ensure that no designated person executes a trade after expiry of 7 days from the date of granting pre-clearance [13] and must consider the possibility that the declaration given by the person may turn inaccurate.

Prima facie, it is important that the CO can effectively assess and discern a piece of information as UPSI, and the possibility of traders possessing UPSI, before giving a nod. The SEBI has held that a CO is expected to comprehend that the materiality of an event lies not only in its price tag but in its ability to shape market perception. He can be held liable if he limits his view to on-record numerical data, and not the quantum of the event.[14] For instance, the knowledge related to setting up a branch in a higher strategic area amounts to UPSI, and if clearance was granted to those in possession thereof, the CO will be penalised for lack of diligence.[15] Furthermore, his inaction is tagged as dereliction of duty when he couldn’t foresee a contra trade by a person who was granted pre-clearance for “dealing in the shares of the company”, on grounds of being “occupied with work”.[16]

However, a CO cannot be held liable for a bona fide lack of knowledge of the exposure of a Designated person to UPSI on the very date of granting pre-clearance to that person. In such a case, the CO cannot be held responsible for any trade executed by such a person while in possession of UPSI [17], but compelling evidence must be furnished by the CO to back his claim of genuine unawareness.

Finally, it is the core duty of the CO to promptly inform the same to the stock exchange(s) where the concerned securities are traded, in case any violation of Regulations is observed[18]. The CO can take assistance from the chief investor relations officer (CIRO) if it is the company’s discretion to designate two separate persons as CIRO and CO, respectively, for meeting specified responsibilities as to the dissemination of information or disclosure of UPSI[19].

5. Conclusion

A compliance officer is designated as a key managerial person. His role is not one of flawless foresight but of demonstrable diligence. As underscored in Rajendra Kumar Dabriwala v. SEBI[20], the responsibility for compliance must not be burdened on a single individual—it must be embedded within the organisational fabric in the backdrop of PIT regulations. To that end, building a resilient compliance ecosystem can enable a CO to define its limitations effectively while ensuring that inherent obligations are fulfilled with efficiency. This requires adopting formalised Standard Operating Procedures (SOPs), automated monitoring tools, structured checklists[21] for promoters, directors, and intermediaries to map recurring corporate events, and AI-assisted detection of UPSI, among other measures.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-16 21:00:562025-10-16 22:40:24Defining Duty: Extent of Liability of a Compliance Officer under Insider Trading Regulations

When AIF Regulations were formally introduced in 2012, the regulatory approach was deliberately light. The framework targeted sophisticated investors, allowing flexibility with limited oversight. Over the years, however, AIFs have become significant participants in capital markets. Market practices over the decade exposed regulatory loopholes and arbitrages. For example, some investors who did not individually qualify as QIBs accessed preferential benefits indirectly through AIF structures and investors who were restricted to invest in certain companies started investing through AIF making AIF an investment facade. There were concerns regarding circumvention of FEMA norms as well1. In the credit space, regulated entities such as banks and NBFCs started channeling funds through AIFs to refinance their stressed borrowers, raising concerns around loan evergreening2. These developments prompted regulatory response. RBI first issued two circulars, one in 2023 and the other in 2024. Finally, in 2025 formal directions governing investments by regulated entities in AIFs were also issued3. These Directions introduced exposure caps and provisioning requirements.4

While the RBI addressed prudential risks arising from regulated entities’ participation in AIFs, SEBI focused on investor protection, governance within the AIF ecosystem and curbing the regulatory arbitrages. First it mandated on-going due diligence by AIF Managers5. It then mandated specific due diligence6 of investors and investments of AIF to prevent indirect access to regulatory benefits. Fiduciary duties of sponsors and investment managers and reporting obligations were progressively codified through circulars. Managers were expected to maintain transparency vis-a-vis their investment decisions, maintain written policies including ones to deal with conflict of interest with unitholders and submit accurate information to the Trustee. What were once broad, principle-based expectations have evolved into detailed, enforceable rules. Regulatory tightening has been matched by a more assertive enforcement approach. SEBI’s recent settlement order7 against an AIF underscores its increasing scrutiny of governance lapses, mismanagement of conflicts and inaccurate reporting. This clearly signals that any compliance gaps will no longer be overlooked and are likely to attract regulatory action. In a separate adjudication order, SEBI imposed penalties on both the Trustee and the Manager for the delayed winding-up of the scheme, underscoring that accountability within an AIF structure extends to all key parties and is not limited to the Manager alone.

However, SEBI’s approach has not been solely restrictive. Alongside regulatory tightening, it has also sought to preserve commercial flexibility and respond to market needs. Examples include the introduction of the co-investment framework8 for AIFs, framework for offering differential rights to select investors and a revamp for angel funds9.

Together, these measures are reshaping the regulatory landscape for AIFs and their managers. Investors can no longer rely on AIF structures to indirectly obtain regulatory advantages otherwise unavailable to them. As AIFs have grown in scale and importance, what is emerging is a more transparent, prudentially sound and closely supervised regulatory regime designed to align investor protection and commercial flexibility.

See SEBI’s Consultation paper on proposal to enhance trust in the AIF ecosystem ↩︎

See our write-up on AIFs being used for regulatory arbitrages here. ↩︎

See our write-up on changes w.r.t Angel Funds here↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-09 10:45:482025-10-10 10:19:44AIF Regulatory framework evolves from light-touch to right-hold

Debentures, one of the most common means for raising debt funding, where investors lend money to the issuer in return for periodic interest and repayment of principal at maturity. While the basic feature of any debenture is a fixed coupon rate and a defined tenure (commonly referred to as plain vanilla instruments), sometimes these instruments may be topped up with enhanced features such as additional credit support, market-linked returns, convertibility option, etc., thus referred to as structured debt securities.

Structured debt securities: motivation for issuers

Apart from the economic favouring such structural modifications, a primary motivation for the issuer in issuing such structured instruments might be the regulatory advantages that these securities offer. For instance,

Chapter VIII of SEBI NCS Master Circular provides an extra limit of 5 ISINs for structured debt securities & market-linked securities, thus more room for the issuers to issue debt securities, compared to the restriction of a maximum of 9 ISINs for plain vanilla debt.

In addition, as per NSE Guidelines on Electronic Book Provider (EBP) mechanism, market-linked debentures are not required to be routed through EBP, allowing issuers to place such instruments almost like an over-the-counter trade. This allows issuers to structure the debt securities on a tailored basis and offer them directly to specific investors.

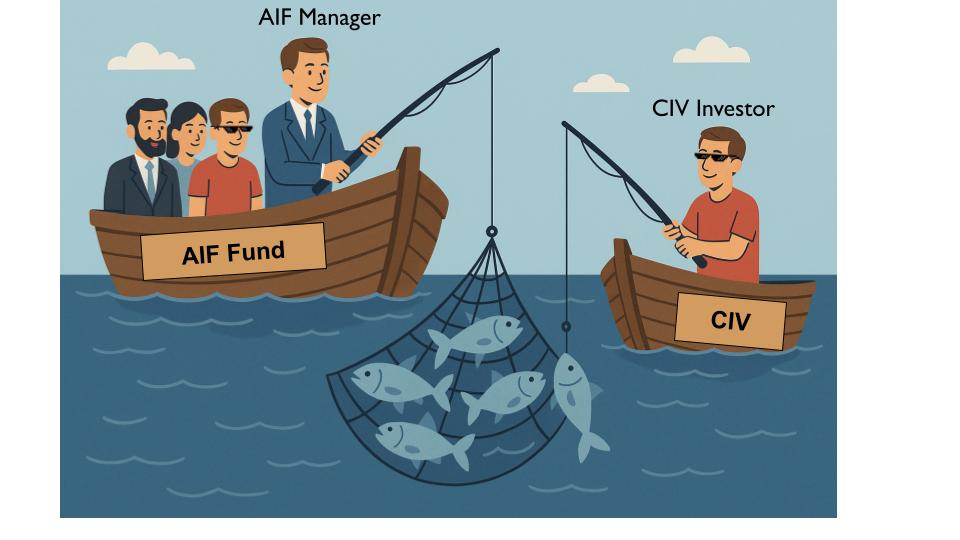

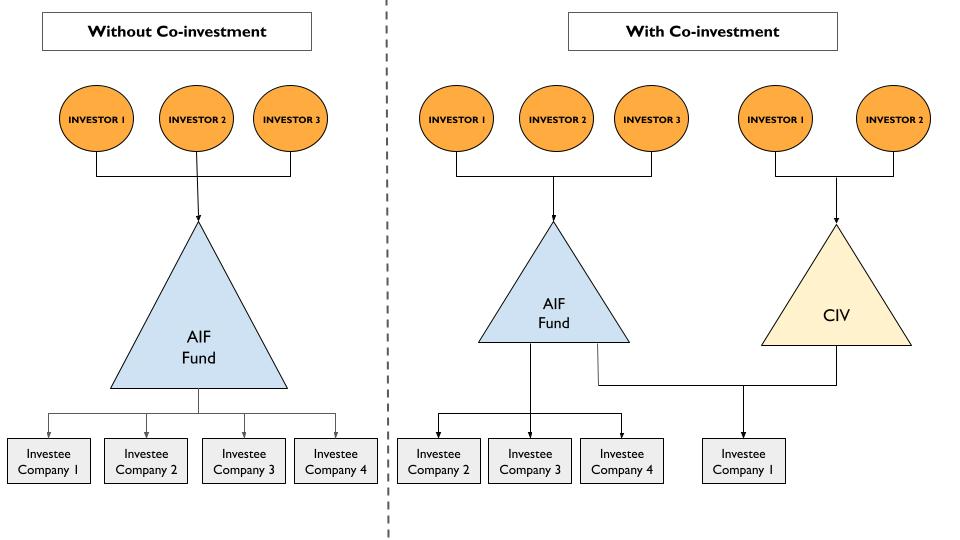

Within an AIF structure, funds are committed by the investors and the AIF in turn, through its Investment Manager, makes investments in investee entities in line with the fund’s strategy. Situations may arise where an investee company of the AIF may require additional capital, that the Investment Manager may not be willing to provide out of the fund’s corpus possibly due to multiple reasons such as over-exposure, non-alignment with funding strategy, capital constraints etc.

In such cases, the Manager may encourage investors to commit further funds directly into the investee. This gives rise to what is known as ‘co-investment’ –an investment by limited partners (LPs or investors) in a specific investee alongside, but distinct from, the flagship fund. Globally, these are also called ‘Sidecar’ funds or ‘parallel’ funds.1

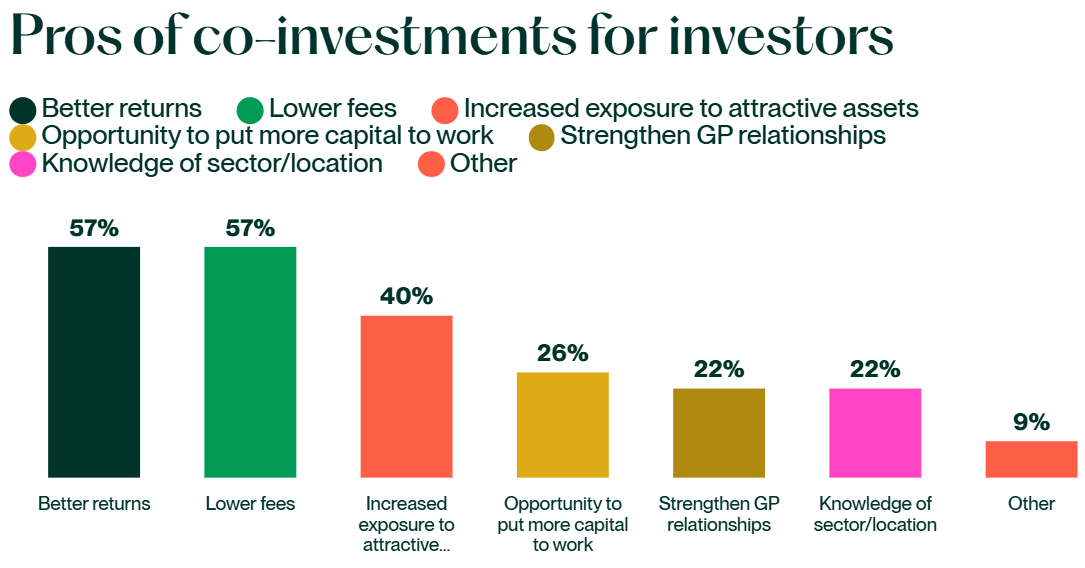

Benefits of co-investments

Investors benefit from co-investments primarily in terms of cost efficiency, in the following ways:

No or lower management fees and a reduced rate of carried interest.2

Reducing/ removing operational and administrative expenses such as in due diligence process & deal sourcing

Where management and incentive fees are directly charged on co-investments, they are usually capped and lower than when investing directly into the PE Fund.3

Not only are headline rates4 typically lower, but management fees are often charged on invested rather than committed capital, reducing fee drag and mitigating the J-Curve.5

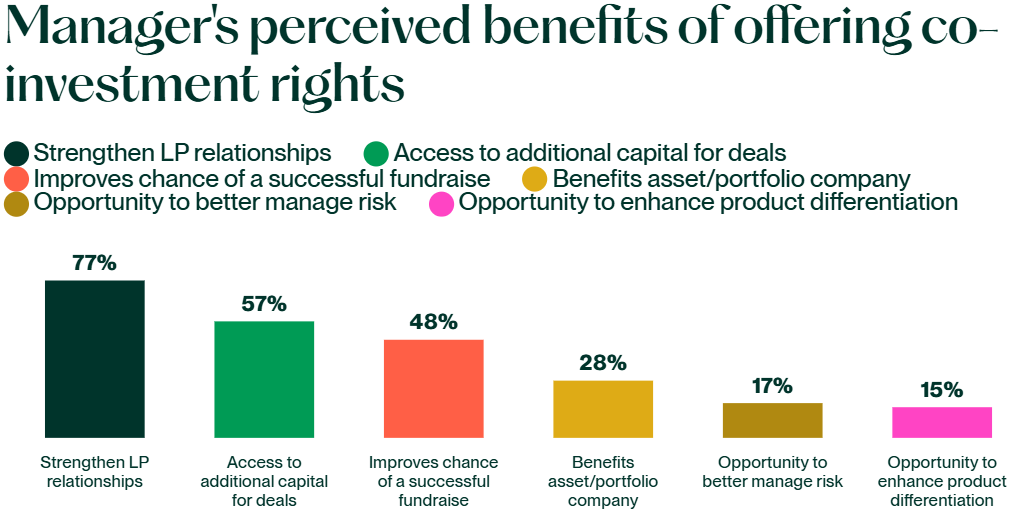

For Managers co-investment offers the following advantages:

Provide access to expanded capital;

Enables it to pursue larger transactions without over extending the main fund

A Preqin study6 found that 80% of LPs reported better performance from equity co-investments than traditional fund structures.

Fig 2: Investor’s perceived benefits of co-investment

Co-investments by AIF investors in the investees of AIF were primarily offered in accordance with the SEBI (Portfolio Managers) Regulations, 2020 (“PM Regulations”). In 2021, PM Regulations were amended to regulate AIF Managers offering co-investments by acting as a portfolio manager of the investors (see need for regulating the co-investment structure below). The AIF Regulations, in turn, required the investment manager to be registered under PM Regulations, for providing co-investment related services.

Keeping in view the rising demand for co-investments, SEBI, based on a recent Consultation Paper issued on 9th May 2025, has amended the AIF Regulations, vide notification dated 9th September, 2025 and issued a circular in September 2025 introducing a dedicated framework for co-investments within the AIF regime itself. Note that the recently introduced framework is in addition to and does not completely replace the co-investment framework through PM as provided in the PM Regulations.

The newly introduced framework refers to co-investments as an affiliate scheme within the main scheme of the fund, in the form of a Co-investment Vehicle Scheme (CIV) and does not require a separate registration by the Investment Manager in the form of Portfolio Manager under PM Regulations.

Interestingly, in May 2025, IFSCA also issued a Circular specifying operational aspects for co-investments by venture capital funds and restricted schemes operating in the IFSC. In this article, we discuss the new framework vis-a-vis the existing PMS route.

Need for regulating co-investments

Conflicts of interest

Especially around the timing of exit. Main fund vs. co-investors may have different preferences.

Voting rights alignment

Misalignment can fragment decision-making.

Risk concentration for investors

Exposure to a single company rather than a diversified portfolio.

Disclosure and transparency obligations for managers

Other fund investors need clarity on why the deal was structured as a co-investment.

Questions may arise on whether the main fund had sufficient capacity to invest.

Risk of concerns about preferential treatment of select investors.

Operational issues:

Warehousing: main fund may initially acquire the investment until co-investment vehicle is ready; requires proper compensation to the fund for interim costs.

Expense allocation: management costs must be fairly shared between the fund and the co-investment vehicle.

Co-investment through PMS Route – the existing framework

Under the PMS Route, the AIF Manager intending to offer co-investment opportunities to its investors shall first register itself as a ‘Co-investment Portfolio Manager’ (see reg. 2(1)(fa) of PM Regulations) post which it can invest the funds of investors subject to the following conditions:

100% of AUM shall be invested in unlisted securities [see reg. 24(4B)];

Only a manager of a Cat I & II AIF is allowed to offer co-investment;

The terms of co-investment in an investee company by a co-investor, shall not be more favourable than the terms of investment of the AIF [see proviso to reg. 22(2)]:

Terms relating to exit of co-investors shall be identical to that of exit of AIF [see proviso to reg. 22(2)];

Early termination/withdrawal of funds by co-investor shall not be allowed. [see reg. 24(2)(a)]

The AIF Manager, registered as a Co-investment Portfolio Manager, is subject to all the compliances as required under the PM Regulations, read with the circulars issued thereunder, except the following:

The minimum investment limit of Rs. 50 Lac per investor in case of PMS will not apply [see reg. 23(2)];

Min. net worth criteria of Rs. 5 Crore shall not apply to such a PM [see reg. 11(e)];

Appointment of a custodian is not required. (see reg. 26)

Roles and responsibilities of the compliance officer can be discharged by the principal officer of the Manager. [see reg. 34(1)]

Particulars

Discretionary

Non-discretionary

Co-investment

No. of clients

1,92,548

6,733

609

AUM (Rs. Crores)

33,05,958

3,18,685

4,674

Table 1: No. of co-investment clients and their total AUM as on 31.07.2025.

As per Table 1, it is evident that co-investment under the PMS Regulations has not taken off yet. One of the major reasons is the additional registration & compliance burden associated with this route.

Co-investment through CIV : the recently approved framework

“Co-investment” means investment made by a Manager or Sponsor or investor of a Category I or II Alternative Investment Fund in unlisted securities of investee companies where such a Category I or Category II Alternative Investment Fund makes investment;”

The framework is restricted to “unlisted securities” only, for the following reasons:

There is a greater information symmetry in case of unlisted securities;

In case of investment in listed securities, it is difficult to establish whether an investor’s decision to invest is driven by the fund manager’s advice or based on the investor’s own independent assessment;

Co-investments are typically undertaken in unlisted entities.

Reg 2(1)(fa) defines co-investment scheme as:

“Co-investment scheme” means a scheme of a Category I or Category II Alternative Investment Fund, which facilitates co-investment to investors of a particular scheme of an Alternative Investment Fund, in unlisted securities of an investee company where the scheme of the Alternative Investment Fund is making investment or has invested;”

The conditions for co-investment through the AIF route is prescribed through the newly inserted Reg 17A to the AIF Regulations read with the Circular dated September 09, 2025. Additionally, the Circular also refers to the implementation standards, if any, formulated by SFA with regard to offering of the co-investment schemes by the AIFs. Since the CIV operates as an affiliate AIF, in order to make it operationally feasible, a CIV has been granted the following exemptions under the AIF Regulations [See reg. 17A(10) of AIF Regulations]:

No minimum corpus of ₹20 Cr.

No continuing sponsor/manager interest (2.5%/₹5 Cr).

Exempt from Placement Memorandum contents, filing modalities, tenure requirement.

Exempt from 25% single-investee company concentration limit

Investment via PMS vs Investment via CIV of an AIF

Post the AIF Amendment, investors have a choice for investing either through the PMS Route or through the CIV route under AIF Regulations. A comparison between the 2 routes is listed below:

Aspects

Investing through CIV

Investing through PMS

Regulatory framework

SEBI (Alternative Investment Funds) Regulations, 2012

SEBI (Portfolio Managers) Regulations, 2020

Limit on investment by each investor

Upto 3 times of investment made by such investor in the investee company through AIF.

Directly in the securities of the investee company.

Co-terminus exit

Timing of exit of CIV = Timing of exit of AIF Scheme from such investee company.

Co-terminus exit

Eligibility of investor

Only Accredited Investors

Any investor

No regulatory bypass

CIV cannot: – Give indirect exposure to such investees where direct exposure is not permitted to the investors; – Create situations needing additional disclosures; – Channel funds where investors are otherwise restricted.

Considered as direct investment by the investor.

Ineligibility of investors