Introducing Financial Services on ONDC: Opportunities & Challenges for Digital Lenders

– Shreshtha Barman | finserv@vinodkothari.com

Read more →– Shreshtha Barman | finserv@vinodkothari.com

Read more →– Chirag Agarwal | Executive | finserve@vinodkothari.com

The Reserve Bank of India (“RBI” or “Regulator”) plays a pivotal role in India meeting its anti-money laundering (AML) and combating financing of terrorism (CFT) obligations as part of its membership with the Financial Actions Task Force (FATF). As the Regulator of the credit sector and payment systems it does so by ensuring the implementation of robust and up-to-date Know Your Customer (KYC) norms vide its Master Direction – Know Your Customer (KYC) Direction, 2016 (“KYC Directions”). With a possible FATF evaluation around the corner, on October 17, 2023, the RBI introduced significant amendments to these KYC directives through its notification titled – Amendment to the Master Direction on KYC (“Amendment”), impacting various regulated entities, including Non-Banking Financial Companies (NBFCs).

Read more →Eliza Bahrainwala, Executive| eliza@vinodkothari.com

Loading…

Loading…

Our related resources on the topic:-

Our Resource Centre on SBR:

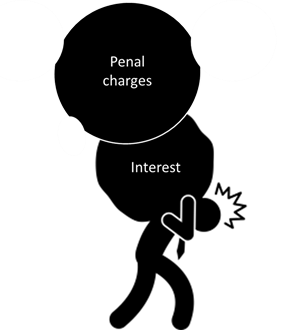

RBI issues draft guidelines on fair lending practices for penal charges

– Aanchal Kaur Nagpal, Manager and Dayita Kanodia, Executive | finserv@vinodkothari.com

Levying of penal interest/ charges is a punitive measure adopted by lenders on borrowers defaulting in making repayments and/ or breaching any terms and conditions mutually agreed in the loan agreement. The Reserve Bank of India also allows lenders to charge such rates as long as the same are communicated to the borrower and are in accordance with the Board approved policy framed in this behalf.

However, lenders, cashing in on such autonomy and flexibility, have adopted varied practices which are often prejudicial to the borrower. These include charging exorbitant rates, capitalisation of penal charges, charging of penal interest on the loan amount and not the defaulted portion etc.

The RBI, in its Statement on Developmental and Regulatory Policies dated February 08, 2023[1], announced policy measures for introduction of guidelines for regulating the penal charges levied by financial institutions[2]. Pursuant to the same, RBI, on April 12, 2023 has issued a draft circular on Fair Lending Practice – Penal Charges in Loan Accounts (‘Draft Circular’) to persuade lenders to use penal charges for their true compensatory nature and not as a revenue enhancement tool.

While the Draft Circular comes with good intentions, there are certain provisions that may seem ambiguous and contradictory, and the final guidelines would need to provide sufficient clarity to achieve the desired execution.

Read more →-Team Finserv | finserv@vinodkothari.com

Financial sector entities have to follow PMLA and related rules, including by way of KYC Directions. The Finance Ministry came up with various amendments pertaining to the Prevention of Money-Laundering Act, 2002 (“PML Act”) and the Prevention of Money-Laundering (Maintenance of Records) Rules, 2005 (‘PML Rules’). The amendments pertain to revised thresholds for ascertainment of beneficial ownership (25% to 10%), implementation of group wide policies for compliance with provisions of Chapter IV, expanding the obligations under PMLA to service providers of virtual digital assets, etc.

The amendment shall be effective from the same date, i.e. March 07, 2023. It may be noted that the Master Direction – Know Your Customer (KYC) Direction, 2016 (‘KYC Directions’) are issued and updated by the regulator based on the amendment in PML Act and PML Rules. However, the Regulated Entities (RE) are required to ensure compliance with the provisions of PML Act and PML Rules, as amended from time to time. Hence, necessary steps must be taken based on the amendments.

Customer Due Diligence (as required under the PML Act and Rules) is required to be undertaken at the time of commencement of a financial transaction or account-based relationship with the customer. Accordingly, necessary steps must be taken by the RE to ensure compliance with the Amendment Rules for all new customers or new financial transactions undertaken with existing customers after March 07, 2023. However, it is also pertinent to note rule 9(12) of the PML Rules which requires reporting entities to exercise continuous due diligence with respect to the business relationship with every clients.

Read more →– Aanchal Kaur Nagpal, Manager | finserv@vinodkothari.com

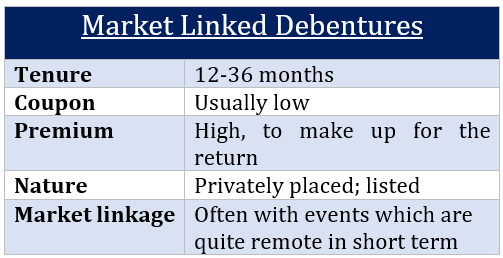

Tax proposal to tax gains on MLDs as short-term capital gains

The Budget proposes that the capital gains on market linked debentures (MLDs) will be taxed as short term capital gain.

Presently, MLDs are mostly listed, and as listed securities they have 2 advantages:

Market linked debentures is a concept that prevails world-over, with different names such as equity-linked bonds, index-linked bonds, etc. However, in India, the issuance of MLDs was being exploited as a regulatory and tax arbitrage device.

As per reports available on public domain[1], the RBI intends to intensify regulatory audits of non-banking finance companies, to find dormancy, non-compliance, non clarity of business models, or other risks that the regulator may wish to check. The intent seems to be weed out the truant ones out of the crowd of over 9000 NBFCs that exist. It is a fact that in the recent years, the RBI has been granting lesser new registrations, and canceling more of existing registrations, causing the number to come down. It is also important to note that if the number of NBFCs looks overwhelming, it is not because so many companies are into real operation: it is because the regulations currently define a company investing its owned capital into financial investments, with absolutely no access to either public funds or customer interface, as an NBFC, by imputing the public interest that actually does not exist. The number would have been a lot lesser had the regulator had the realisation that if there are no public funds, no customer interface and investment of owned funds being done, there is no reason for the regulator to interfere, as the intent of the country’s Central Bank cannot be to regulate investment activity that one does with one’s own money.

While this issue remains to be advocated for a potential reform, in the meantime, it is important for NBFCs to brace up for the RBI’s inquisitorial interest.

This article is intended to help NBFCs to be better prepared for such regulatory interface.

Read more →

Loading…

| Our services and Assistance for ICAAP Implementation can be viewed here – https://vinodkothari.com/2022/09/services-and-assistance-for-icaap-implementation/ |

Our resources on the topic:

Our resources on the topic:

Loading…

Click here to view our firm profile – https://vinodkothari.com/2021/09/vkcpl-team-profile/