IPO Financing, as the name suggests, is providing finance for the purpose of subscribing to initial public offers done by companies. In case of IPO Financing, the exposure is based on the borrower, and the securities/ shares, if allotted, are taken as collateral for securing the obligations under the loan. The investor will realise the shares so allotted in the IPO and pay-off the loan taken from the Banks/NBFCs.

How does IPO Financing work?

IPO Financing is widely used by High Networth Individuals (HNIs) as a tool to leverage the funds available with an intent to make profits from the IPO allotment price and the price at the time of listing. Typically, the lender would provide a short-term loan to the borrower at a certain interest rate, till the shares are listed. The transaction forces the investor to sell the shares once listed. Out of the proceeds, the lender would retain the repayment of loan and payment of interest plus other charges, as may be levied; and the balance is taken home by the investor as profits. Hence, the idea is not to “invest” in an IPO and eventually earn investment rewards; rather, the intent usually is to “enter” and “exit” by booking possible gains in the shortest time span.

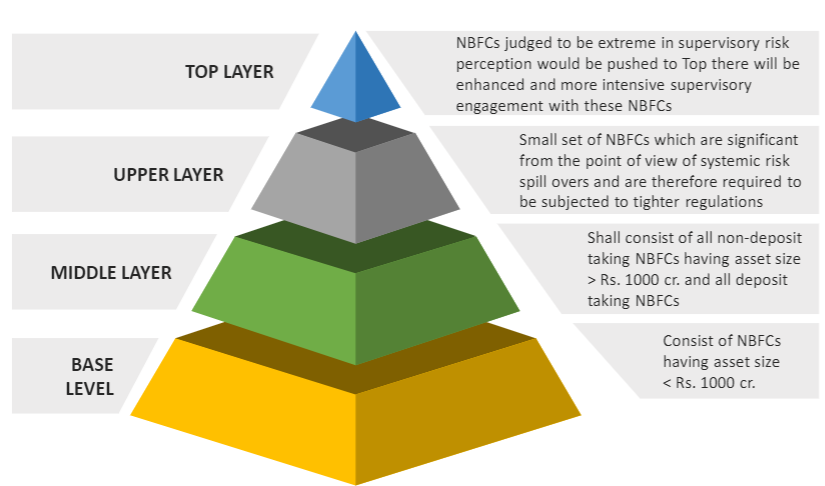

Recently, the RBI has released Scale Based Regulation (SBR): A Revised Regulatory Framework for NBFCs (SBR) on October 22, 2021. While the SBR provides for broad contours of the revised framework, concrete regulations in the form of ‘Directions’ are awaited from RBI. SBR fixes a ceiling of Rs. 1 crore per borrower in case of IPO financing by any NBFC.

We have tried to figure out the probable questions arising out of the aforesaid proposal and respond to the same in the form of these FAQs. However, these are subject to final directions yet to be issued by RBI in this regard. We shall update this FAQ once there are clear directions in this regard. These FAQs shall be read accordingly.

Read more →

Loading…

Loading…