Shashtrarth 27: Type 1 NBFC Exemption

Watch our youtube video: https://www.youtube.com/watch?v=IBv09etJb2g

Loading…

Loading…

Watch our youtube video: https://www.youtube.com/watch?v=IBv09etJb2g

Loading…

Subhojit Shome, Senior Manager | Finserv@vinodkothari.com

The payments ecosystem is often described as the “plumbing” of commerce—rarely visible to consumers, yet fundamental to economic activity. For decades, this plumbing has been dominated by credit and debit card systems, operated by banks and card networks under tightly regulated frameworks. In recent years, however, global technology platforms have begun experimenting with alternative payment infrastructures, particularly those built on blockchain technology, with the aim of reducing remittance fees and achieving faster settlement.1

One such initiative is the payment infrastructure jointly developed by Shopify and Coinbase (“Shopify–Coinbase Payment Infrastructure”), which enables merchants to accept payments using stablecoins, most notably USD Coin (USDC), without relying on traditional card networks.

Shopify–Coinbase Payment Infrastructure has been initially launched in at least 34 countries where merchants can accept USDC payments via the Base (blockchain) network. This includes a range of markets across the United States, most of Europe, Canada, Australia, Japan, Singapore2. A number of these countries/ regions (e.g. United States3, EU4, Japan5, Singapore6) have statutorily recognised, and regulate the use of stablecoins.

This article examines the Shopify–Coinbase Payment Infrastructure in comparison with traditional card payment rails and analyses the regulatory concerns that would arise if such a system were to operate in India, with particular reference to the Payment and Settlement Systems Act, 2007 (“PSS Act”) and the regulatory stance of the RBI.

To appreciate what Shopify and Coinbase seek to replace, it is first necessary to understand the traditional debit/ credit card “payment rails”. The term “rails” is a metaphor, referring to the underlying infrastructure that carries a payment transaction from the payer to the payee—much like railway tracks carry trains.

In a credit or debit card transaction, the rails consist of several interconnected elements. When a customer uses a card, the merchant does not receive money immediately. Instead, the transaction is routed through the card network (such as Visa, Mastercard, or RuPay), which communicates with the customer’s bank (the issuer) and the merchant’s bank (the acquirer). The customer’s bank first checks whether sufficient funds or credit are available and places a temporary hold on that amount. This is known as authorisation (“auth”). The actual transfer of money happens later, when the merchant confirms the transaction—a step known as capture. Settlement between banks typically occurs after a delay of one or two business days.

This system is heavily regulated in India – card networks operate under RBI oversight, settlement occurs through RBI-regulated banking channels, and consumers are protected through structured dispute resolution mechanisms, including chargebacks7. The entire system functions within the legal framework of the PSS Act and the RBI’s directions on payment systems and card networks, payment aggregators, and consumer protection.

The Shopify–Coinbase Payment Infrastructure proposes a fundamentally different way of moving money. Instead of using banks and card networks as intermediaries, it relies on stablecoins, which are digital tokens designed to maintain a stable value by being backed by traditional currency reserves. The stablecoin USDC, for example, is designed to track the value of the US dollar.

In this system, when a customer pays a merchant, the payment is executed on a blockchain network. The funds are first locked in a digital escrow mechanism controlled by software (a “smart contract”) and once the merchant fulfils the order, the funds are automatically released to the merchant. This process replicates the familiar card concepts of authorisation and capture (“auth and capture”), but replaces banks and card networks with software rules and cryptographic verification.

From the user’s perspective, the checkout experience may look familiar. From a legal perspective, however, the system represents a shift from institution-based trust (banks and regulators) to code-based execution. Settlement is near-instant, global, and does not depend on banking infrastructure.

Auth/ Capture using Stablecoins and Smart Contracts

In card payment systems, authorisation and capture are two distinct but linked stages in how a transaction is processed and settled. One of the unique characteristics of the Shopify–Coinbase Payment Infrastructure is that it is able to replicate such an auth/ capture settlement process which is observed in traditional card rails.8

Authorisation is the preliminary step. When a customer enters card details at checkout, the merchant seeks confirmation that the cardholder has sufficient funds or credit and that the transaction is permitted. At this stage, no money actually moves. Instead, the issuing bank places a temporary hold on the relevant amount, effectively earmarking those funds. From a legal perspective, authorisation represents a conditional and revocable promise by the issuer to honour the transaction, subject to subsequent validation and compliance with network rules.

Capture occurs later, when the merchant confirms that the goods or services have been provided (or are about to be provided) and formally requests payment. Upon capture, the transaction becomes final for settlement purposes. The temporary hold created at the authorisation stage is converted into an obligation to transfer funds through the card network’s clearing and settlement process. Only after capture does the merchant acquire an enforceable right to receive payment, subject to chargeback and dispute mechanisms.

The Shopify–Coinbase Payment Infrastructure seeks to recreate this familiar commercial logic—authorisation first, settlement later—while removing traditional card networks entirely. In this model, the customer pays using a stablecoin (typically denominated in a foreign currency such as the US dollar). Rather than immediately transferring funds to the merchant, the payment is first routed into a smart contract–based escrow. This escrow functions as the economic equivalent of card authorisation. The funds are not credited to the merchant and cannot be unilaterally withdrawn. They are effectively “locked,” signalling the payer’s intent and financial capacity, much like a card authorisation hold. The legal character of this stage differs fundamentally from card authorisation. In card systems, the issuer’s promise is conditional and revocable, and the funds remain within the regulated banking system. In a blockchain escrow, by contrast, the customer has already transferred the funds out of their wallet. Control is no longer exercised by a regulated intermediary but by pre-programmed contractual logic embedded in code.

The equivalent of capture occurs when the merchant satisfies predefined conditions—such as confirmation of shipment or lapse of a dispute window. Once those conditions are met, the smart contract automatically releases the stablecoins to the merchant’s wallet. Settlement is thus executed not through interbank clearing, but through an on-chain state change that is immediate, final, and typically irreversible. From a legal standpoint, this mechanism replaces discretionary decision-making by regulated institutions with deterministic execution by software.

The contrast between card rails and the Shopify–Coinbase model is not merely technical; it is institutional and legal.

Card payments are embedded within a regulated financial ecosystem. Every participant—issuer banks, acquirers, networks, payment aggregators—is subject to licensing, capital requirements, audit obligations, and RBI supervision. Settlement occurs in Indian Rupees, and consumer protection is enforced through mandatory refund and dispute resolution frameworks.

By contrast, the stablecoin model shifts settlement outside the traditional banking system. Funds are represented not as bank deposits but as digital tokens. Settlement does not occur through RBI-regulated systems such as RTGS, NEFT, or card clearing arrangements, but on a distributed ledger maintained by a global network of computers. While this may reduce costs and increase speed, it also raises fundamental questions about regulatory oversight, legal accountability, and consumer protection.

The Payment and Settlement Systems Act, 2007 establishes a comprehensive legal framework under which the RBI is the sole authority empowered to regulate and supervise payment systems.

No person, other than the Reserve Bank, shall commence or operate a payment system except under and in accordance with an authorisation issued by the Reserve Bank under the provisions of this Act (Section 4 of the PSS Act)

Under the PSS Act, no person may operate a payment system in India without authorisation from the RBI. A “payment system” is defined broadly to include any arrangement that enables payments to be effected between a payer and a beneficiary. This definition is technology-neutral and focuses on function rather than form. Consequently, even a novel digital arrangement may fall within the regulatory perimeter if it facilitates payment and settlement.

In addition to the PSS Act, the RBI has issued detailed regulations governing card payments, payment aggregators and payment gateways, which impose obligations relating to customer funds, escrow arrangements, settlement timelines, dispute resolution, and grievance redressal. These regulations reflect the RBI’s core concern: protecting consumers and preserving the integrity of the payment system.

From an Indian statutory and regulatory standpoint, several concerns arise if a Shopify–Coinbase-type payment infrastructure were to be used by Indian merchants or consumers.

First, there is the issue of authorisation under the PSS Act. A stablecoin-based payment system that enables Indian users to make payments would likely qualify as a “payment system” under the Act. In the absence of explicit RBI authorisation, operating such a system in India would be impermissible, regardless of its technological sophistication.

Second, there is the question of settlement in Indian Rupees. Domestic payment systems in India settle in INR through RBI-regulated channels. Online card payments made in India using Indian cards cannot be routed through foreign banks or settled in foreign currency — they must be handled by Indian banks and settled in INR.9 Also, “Wallets”, i.e., prepaid payment instruments (PPI) essentially need to be loaded in INR.10 Stablecoin settlement, particularly when denominated in a foreign currency such as the US dollar, bypasses these channels. While stablecoins may be created so as to be denominated in INR, no recognition currently exists for stablecoins as settlement instruments for domestic payments.

Third, custody and consumer protection pose significant challenges. RBI regulations require that customer funds be held with regulated entities, typically banks, and that clear mechanisms exist for refunds, reversals, and dispute resolution. Blockchain-based escrow mechanisms are governed by software rather than law, and once a transaction is final, reversing it may be impossible without voluntary cooperation by the merchant. This stands in tension with RBI’s consumer-centric regulatory approach.

Fourth, there are foreign exchange and monetary policy considerations. Stablecoins backed by foreign currency reserves raise concerns under India’s foreign exchange regime and broader monetary sovereignty objectives. RBI has repeatedly expressed caution about private digital currencies and stablecoins, citing risks to financial stability and policy transmission.11

The Shopify–Coinbase Payment Infrastructure represents a significant evolution in global commerce, demonstrating how technology can replicate—and potentially outperform—traditional card systems in terms of speed and cost. However, from an Indian legal perspective, innovation in payments is not evaluated solely on efficiency. It is assessed through the lens of statutory compliance, regulatory oversight, consumer protection, and monetary stability.

While the logic of authorisation and capture may be technologically reproduced through blockchain-based escrow mechanisms, the legal foundations of payment systems in India remain firmly anchored in the PSS Act and RBI regulation. Until stablecoin-based payment infrastructures are brought within this framework—through authorisation, INR settlement mechanisms, and enforceable consumer protections—their direct adoption in the Indian domestic payments landscape would face substantial legal and regulatory hurdles.

See our other resources

Simrat Singh | finserv@vinodkothari.com

When nature unsettles the ordinary course of life, the regulatory hand should neither be withdrawn nor clenched; it should extend a humane touch, easing distress and guiding the return of order. In this spirit, the RBI has released draft directions on Relief Measures in Areas Affected by Natural Calamities, setting out a framework under which banks, NBFCs and other Regulated Entities (REs) may provide relief to borrowers impacted by natural calamities or similar external events. The framework enables REs to extend resolution plans to eligible borrowers, while permitting retention of standard asset classification and lower provisioning, benefits that would otherwise not be available if such restructuring were undertaken under the normal IRACP framework.

It may be noted that earlier RBI had issued guidelines for banks in connection with matters relating to relief measures to be provided in areas affected by natural calamities consolidated under ‘Master Direction – Reserve Bank of India (Relief Measures by Banks in Areas affected by Natural Calamities) Directions 2018 – SCBs’ dated October 17, 2018. In 2016, these guidelines were made applicable, mutatis mutandis, to all NBFCs as well, in areas affected by natural calamities as identified for implementation of suitable relief measures by the institutional framework viz., District Consultative Committee (DCCs)/ State Level Bankers’ Committee (SLBCs). However, given that the provisions were drafted considering the banking operations, the implementation by NBFCs was ambiguous and the provisions were often overlooked.

While the proposed framework applies to both banks (Commercial, RRB, Local area banks etc) and NBFCs, there are separate draft Directions issued for each RE. In case of banks the provisions carry additional system-level and public service responsibilities, reflecting their role within SLBCs and DCCs.

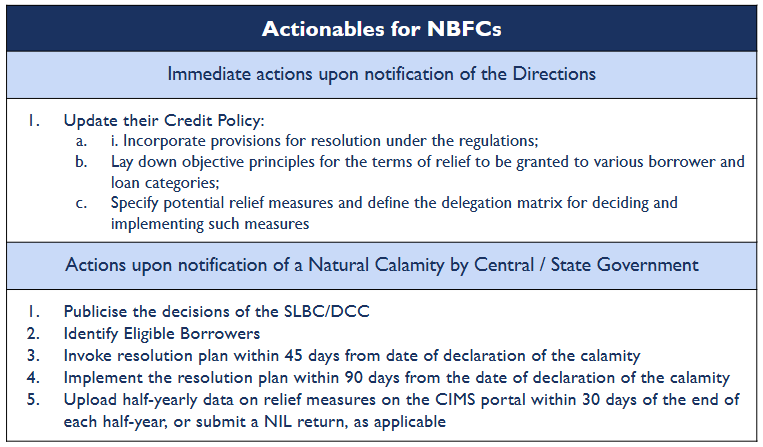

Fig 1: Actionables for NBFCs under the draft directions

The draft directions are proposed to come into effect from 1 April 2026, after the final directions are notified. The framework is triggered upon formal notification of a natural calamity by the Central Government or the concerned State Government.

Where a calamity affects a substantial part of a State, it is proposed that a special meeting of the SLBC shall be convened within 15 days of such declaration. If the impact is confined to one or more districts, the corresponding DCC(s) are required to meet within the same timeframe. These committees assess the severity of the impact on economic activity, determine objective criteria for identifying impacted borrowers and indicate the nature and extent of relief such as moratoriums that may be extended by regulated entities operating in the affected areas. The decisions taken in these meetings are communicated to regulated entities and are required to be given adequate publicity, primarily by banks, through field outreach and public communication. The relief framework becomes operational in line with such Government notifications and the decisions of the SLBC or DCC, as applicable.

The draft directions propose that the REs update their credit policies to incorporate a structured and pre-defined framework for dealing with borrower stress arising from natural calamities. The credit policy is expected to provide for resolution in line with the provisions and to set out objective principles governing the terms of relief across different borrower segments and loan categories.

While the precise parameters may vary depending on the nature and severity of the calamity, the decisions of the SLBC/DCC/Governments, the credit policy is expected to lay down a consistent framework to be applied by the REs when extending relief. This includes identifying potential relief measures, specifying verifiable parameters for determining eligibility of borrowers and extent of relief and defining the delegation matrix for approval and implementation. The emphasis is on ensuring timely decision-making, particularly in relation to restructuring of existing exposures and sanction of additional finance.

Relief under the draft Directions is proposed to be available only to borrowers who meet the prescribed eligibility conditions as on the date of occurrence of the natural calamity. To qualify, the borrower’s account must be classified as ‘Standard’ and must not be in default for more than 30 days with the concerned RE in respect of any facility. Other additional conditions may be laid down in the credit policy.

Borrowers who do not meet these conditions fall outside the scope of the calamity relief framework and may instead be considered for resolution under the applicable Resolution of Stressed Assets Directions. In such cases, however, the RE does not receive the benefit of standard asset classification or lower provisioning (see discussion below). The framework extends its shelter only to those borrowers who, till the moment the calamity struck, had kept their financial obligations substantially intact. The protection is not meant to rescue infirm credit, but to steady sound accounts momentarily shaken by forces beyond human control.

Where a RE decides to extend relief, the resolution plan is to be structured based on an assessment of the borrower’s post-calamity viability. The draft Directions propose a range of relief measures, including rescheduling of repayments, grant of moratorium, and conversion of accrued or future interest into another credit facility. Regulated entities may also consider sanctioning additional or fresh finance to address temporary financial stress, subject to appropriate assessment of viability and credit risk.

Notably, the framework is enabling rather than mandatory. It does not require automatic restructuring of all eligible accounts, thereby allowing REs to exercise credit judgement while operating within the prescribed regulatory parameters.

It is proposed that resolution under the framework must be invoked within 45 days from the date of declaration of the natural calamity, unless an extension is granted by the Regional Director or Officer-in-Charge of the Reserve Bank. This would mean that the aggrieved borrower must approach the lender and the terms of restructuring must be agreed between both of them within the said timeframe. Once invoked, the resolution plan must be implemented within 90 days from the date of invocation.

In practice, this means that following the Government notification and the SLBC or DCC meeting, typically held within the first 15 days from the notification, REs have a limited 30-day window to complete borrower identification, viability assessment, documentation and approval. Failure to adhere to these timelines results in loss of the regulatory benefits available under the framework.

The most significant regulatory benefit under the proposed framework relates to asset classification. Where a resolution plan is implemented in compliance with the Directions, borrower accounts classified as ‘Standard’ may be retained as such upon implementation instead of facing any downgrade. Further, accounts that may have slipped into NPA status between the date of occurrence of the calamity and the implementation of the resolution plan are permitted to be upgraded to ‘Standard’ upon implementation. However, as per the ECL Policy of the RE, generally any restructuring would automatically be treated as a SICR and therefore, the staging may change and a higher ECL would be required to be provided on such restructuring which may nullify the benefit.

After implementation, subsequent asset classification is governed by the applicable IRACP norms. The proposed framework also addresses cases of repeated restructuring. Where a borrower account is restructured again under these Directions before the reversal of additional provisions (see below), it may continue to be classified as ‘Standard’, subject to recognition of interest on a cash basis from the second restructuring onwards and maintenance of an additional specific provision of five per cent of the outstanding debt for each restructuring, subject to an overall ceiling of 100 per cent.

For restructured accounts, it is proposed that interest income may be recognised on an accrual basis. At the same time, REs are required to maintain an additional specific provision of 5% of the outstanding debt, over and above the applicable provisioning under IRACP norms. Reversal of this additional provision can happen only where the borrower repays at least 20% of the outstanding debt, the account does not slip into NPA status after implementation of the restructuring and no further restructuring is undertaken during the relevant period. Specifically for banks, if the outstanding debt post-restructuring is only in the form of non-fund-based facilities or facilities in the nature of cash credit / overdraft, the additional provisions can be reversed after one year, post implementation of the restructuring, provided the borrower was not in default at any point of time during the period concerned.

It is proposed that the REs be required to extend interest subvention or prompt repayment incentive benefits notified by the Government to all eligible borrowers. They must also ensure that any relief already provided, or being provided, by the Central or State Governments is duly factored into the resolution process.

For agricultural loans secured by land, the draft Directions propose acceptance of certificates issued by Revenue Department officials where original title documents have been lost due to the calamity. In areas governed by community ownership arrangements, certificates issued by competent community authorities may also be accepted. REs may also, at their discretion, provide additional relief such as waiver or reduction of fees and charges for borrowers in affected areas, for a period not exceeding one year. Expected proceeds from insurance policies may also be kept while deciding the relief. Additionally for banks it is proposed that they shall open small accounts for displaced borrowers and take immediate action to restore ATM services in the impacted areas. They may operate their natural calamity affected branches from temporary premises under advice to the RBI. For continuing the temporary premise beyond 30 days, banks may obtain specific approval from the concerned Regional Office of RBI. A bank shall also make arrangements to render banking services in the affected areas by setting up satellite offices, extension counters or mobile banking facilities etc. under intimation to the RBI.

It is proposed that the REs shall upload data on relief measures extended under the framework in the prescribed format on a half-yearly basis. The data points include ‘Outstanding eligible for restructuring as on the date of notification of natural calamity’, ‘Credit facilities restructured/rescheduled during the half year’, ‘Additional/fresh loans provided to affected borrowers during the half year’ etc. The data must be submitted within 30 days from the end of each half-year, i.e., as of 30 September and 31 March, through the CIMS portal. Where no relief measures are extended during a reporting period, a NIL statement is required to be submitted.

See our other resources:

Simrat Singh | finserv@vinodkothari.com

The Economic Survey 2026 takes an honest view of India’s microfinance sector. Rather than celebrating credit growth alone, it frames microfinance as a household balance-sheet business, where the real test of success is whether borrowing improves stability and resilience at the last mile or not. NBFC-MFIs, as the primary delivery channel, sit at the heart of this assessment. In this short note, we explore major observations of the Survey w.r.t infrastructure financing and microfinance.

The Survey reiterates the importance of microfinance in extending formal credit to underserved households. Women account for the vast majority of borrowers and most lending continues to be rural. Over the past decade, the sector has expanded rapidly in both outreach and scale, with NBFC-MFIs accounting for the largest share of lending, followed by banks and small finance banks.

This expansion has made microfinance one of the most effective channels for last-mile credit delivery but it has also exposed the sector to sharper credit cycles.

The slowdown seen in FY25 is presented as a supply-side correction rather than a failure of the model. The Survey attributes the stress primarily to over-lending and borrower over-indebtedness in certain regions, driven by multiple lenders targeting the same customer base after the pandemic. The key takeaway being that access to credit was not the constraint credit discipline was.

NBFC-MFIs remain indispensable to microfinance, but the Survey recognises their structural vulnerability during rapid growth phases. Unsecured lending and limited visibility into borrowers’ total debt make the model sensitive to concentration risks. Regulatory responses have therefore focused on restoring balance rather than tightening credit indiscriminately. The RBI’s decision to lower the minimum qualifying asset requirement has given NBFC-MFIs room to diversify, while self-regulatory measures have reinforced borrower-level safeguards. The Survey notes early signs of stabilisation in asset quality and disbursement trends.

A recurring concern in the Survey is the lack of reliable tools to assess household income and repayment capacity. Many borrowers carry obligations beyond microfinance such as gold loans or agricultural credit that are not always visible at the point of lending. The Survey sees digital public infrastructure as a gradual solution. Wider use of digital payments, data sharing frameworks and account aggregators is expected to improve cash-flow assessment and reduce reliance on informal income proxies. Using all this information about its borrowers, the MFIs are expected to improve their credit assessment.

One of the Survey’s most important observations is its critique of how success in microfinance is measured. While private capital has helped scale the sector, growth-centric metrics can unintentionally encourage repeated lending without sufficient regard for borrower outcomes. The Survey argues for a shift towards welfare-oriented indicators such as income stability, reduction in distress borrowing and sustainable debt levels rather than portfolio size alone. In doing so, it challenges the assumption that more credit automatically translates into better outcomes.

The Survey neither dismisses microfinance nor romanticises it. It acknowledges its critical role in inclusion, while warning that unchecked expansion can weaken household balance sheets. Long-term sustainability, it suggests, depends less on how fast credit grows and more on how responsibly it is delivered. The Economic Survey’s message is simple: the future of microfinance lies in lending better, not lending more. For NBFC-MFIs, this means aligning growth with borrower capacity, using data more intelligently and treating household stability, not loan volumes, as the true measure of success.

Read our other resources

Climate Finance: domestic resources insufficient to bridge funding gaps

Harshita Malik | finserv@vinodkothari.com

Refer our detailed write-up on the topic titled as Bank-NBFC Partnerships for Priority Sector Lending: Impact of New Directions

Manisha Ghosh, Senior Executive | finserv@vinodkothari.com

Loading…

– Team Corplaw | corplaw@vinodkothari.com

Continuing with the spree of regulatory changes brought in 2025, RBI has issued Amendment Directions on Lending to Related Parties by Regulated Entities. Separate notifications have been issued for each regulated entity, based on the draft Directions for lending and contracting with related parties issued on 3rd October, 2025. We discuss the changes brought in for commercial banks by way of the RBI (Commercial Banks – Credit Risk Management) – Amendment Directions, 2026 and RBI (Commercial Banks – Financial Statements: Presentation and Disclosures) – Amendment Directions, 2026.

| Point of comparison | CRM Amendment Directions | Listing Regulations | Companies Act |

| Scope of coverage | Loans, non-funded facilities, investment in debt securities | Any transfer of resources, obligations or services | Contracts as enumerated u/s 188 (1) |

| Meaning of related party | Directors, KMPs, promoter, their relatives, entities in which either of them have specified interest (partnership, shareholding, control, etc).Does not include Company’s own holding company, subsidiaries or associates | Wide definition, including sec 2 (76) of CA, accounting standards, promoter, promoter group entities, shareholders with 10% or more shareholding | As defined in sec. 2 (76), primarily including directors, KMPs, their relatives, private cos where such persons are a director or member, public companies with directors’ 2% shareholdings.Includes entity’s own subsidiaries, associates, JVs, holding company |

| Concept of “reciprocally related party” | In line with the statutory restrictions, includes directors/relatives on the boards of other banks, AIFIs, trustees of mutual funds set up by other banks | Does not exist; however, a purpose-and-effect test exists whereby surrogate transactions may be covered. | Does not exist |

| Primary approving body | Committee on Lending to Related Parties, or the Board | Audit Committee | Audit Committee; or the Board |

| Shareholders’ approval | Not required | Required if crossing materiality threshold | Required if not on in ordinary course of business+ arm’s length, and crossing materiality threshold |

| Materiality threshold | Being linked with a single loan exposure, ranges from Rs 5 crores to Rs 25 crores depending on Bank’s capital | Being aggregated for transactions during a FY, ranges from 10% of the entity’s consolidated turnover to Rs 5000 crores based on consolidated turnover of the entity | Usually based on 10% of turnover or net worth (depending on transaction type) |

See our related resources here:

https://vinodkothari.com/2026/01/shastrarth-26-loans-to-related-parties-by-banks-and-nbfcs/

Simrat Singh & Sakshi Patil | finserv@vinodkothari.com

India’s lending landscape is evolving from traditional, branch-led lending to digital and now “phygital” models, involving multiple intermediaries connecting borrowers and lenders. For regulated entities (REs), three different terms referring to loan intermediaries are commonly seen: Lending Service Providers (LSPs), Direct Selling Agents (DSAs) and Referral Partners.

At first glance, these roles may appear similar since all “bring in business.” But as far as the RBI is concerned, the difference determines how much regulatory oversight the lender must exercise over these participants. This article attempts to answer who’s who in this lending chain, and more importantly, where a simple referral ends and a regulated lending function begins.

In the digital lending framework, the most central participant is the LSP who are engaged by the REs to carry out some functions of RE in connection with its functions on digital platforms. These LSPs may be engaged in customer acquisition, underwriting support, recovery of loan, etc. The RBI’s Digital Lending Directions, 2025 define an LSP as:

“An agent of a RE (including another RE) who carries out one or more of the RE’s digital lending functions, or part thereof, in customer acquisition, services incidental to underwriting and pricing, servicing, monitoring, or recovery of specific loans or loan portfolios on behalf of the RE, in conformity with the extant outsourcing guidelines issued by the Reserve Bank.”

The emphasis on the term “agent” is crucial since being an agent becomes a precondition to becoming an LSP. An agent is a person employed to act for another; to represent another in dealings with third persons within the overall authority granted and can legally bind the principal by their actions (more discussion on agency later). This distinguishes an agent from a mere vendor or service provider who delivers a contracted service but has no authority to affect the principal’s relationship with third parties and neither is subjected to a degree of control from the principal.

DSAs, though not formally defined by the RBI, their appointment, conduct and RE’s oversight on them is governed by Annex XIII of the SBR Directions (Instructions on Managing Risks and Code of Conduct in Outsourcing of Financial Services by NBFCs) for NBFCs and by Guidelines on Managing Risks and Code of Conduct in Outsourcing of Financial Services by Banks for Banks. DSAs operate largely in physical or “phygital” lending models, focusing on loan sourcing. They represent the lender while dealing with potential borrowers. However, their functions are narrower than those of an LSP. A DSA’s role typically ends with lead generation and preliminary documentation, without involvement in underwriting, servicing or recovery. While the DSA is an agent, it plays a more limited role in the lending value chain and has minimal borrower-facing obligations post origination.

Referral Partners perform the most limited role. They simply share leads or basic borrower information with the lender and have no authority to represent or bind the lender. Their role is confined to referral i.e. the providing the first nudge to the lender. They are treated as independent contractors or service providers, not agents and operate under commercial referral agreements. The RE does not exercise control over their operations, nor is it responsible for their actions beyond the agreed referral activity. The distinction lies not in what they do (introducing borrowers) but in what they cannot do i.e. represent the lender or perform any of its lending functions.

The most important question then arises “How does one determine whether a person is an LSP, DSA, or a referral partner?”. All three may assist in borrower acquisition, but the answer might lie in distinguishing referring from representing. To be classified as an LSP (or even a DSA), the person must first be the agent of the RE, not just a vendor or service provider. The test of agency has been laid down in the Supreme Court’s decision in Bharti Cellular Ltd. v. Commissioner of Income Tax1. The Court, in para 8, observed that the existence of a principal–agent relationship depends on the following elements:

Further, the Court clarified in para 9 that the substance of the relationship, not just its form, determines whether agency exists. If a person is neither authorised to affect the principal’s relationship with third parties nor under its control, and owes no fiduciary obligation, the person is not an agent, regardless of what the contract calls them.

Similarly, in Bhopal Sugar Industries v. Sales Tax Officer2, the Supreme Court had observed that the mere word ‘agent’ or ‘agency’ is not sufficient to lead to the inference that parties intended the conferment of principal-agent status on each other. Mere formal description of a person as an agent is not conclusive to show existence of agency unless the parties intend it so hence, “the true relationship of the parties in such a case has to be gathered from the nature of the contract, its terms and conditions, and the terminology used by the parties is not decisive of the said relationship.”

On the aspect of supervision and control, the Supreme Court in para 40 of the Bharti Cellular ruling stated:

An independent contractor is free from control on the part of his employer, and is only subject to the terms of his contract. But an agent is not completely free from control, and the relationship to the extent of tasks entrusted by the principal to the agent are fiduciary….The distinction is that independent contractors work for themselves, even when they are employed for the purpose of creating contractual relations with the third persons. An independent contractor is not required to render accounts of the business, as it belongs to him and not his employee.

In lending transactions, therefore, the relevant considerations to determine whether an agency exists or not may be:

To illustrate the difference between LSP/DSA and Referral Partner, consider a simple example. You stop at your neighbourhood paanwala for your regular paan or pack of mints. Between the faded ads for mobile recharges and UPI QR codes, one new poster catches your eye “Need a personal loan? Look No Further ! Fast approvals”. Curious, you ask if the shopkeeper has joined the finance world. Smiling, he replies, “Arre nahi sahib, I just share numbers! You give me your name and phone number, I’ll send it to my guy. If your loan gets approved, I get a small tip!” No exchange of KYC documents, no app, no credit score. Now, does this make the paanwala an LSP under the Digital Lending Directions? He may appear as performing a part of the customer acquisition function of the lender so should he now comply with outsourcing norms, data protection protocols and grievance redressal requirements? Of course not.

The paanwala is a pure referral partner. His role ends with introducing a potential borrower to a contact connected to a lender. He does not represent the lender, verify or collect documents, underwrite, service, or recover loans, nor can he legally bind the lender through his actions. Mere referral, without agency and without performing a lending function, does not make one an LSP. Passing a phone number over a cup of chai does not amount to digital intermediation.

| Basis | Referral Partner | LSP |

|---|---|---|

| Scope of activity | Limited to sharing leads with the lender | Performs one or more of the lenders functions w.r.t in customer acquisition, services incidental to underwriting and pricing, servicing, monitoring, recovery |

| Access to prospective customer’s information and documents | Only basic contact information necessary for the lender to approach the customer for the loan is shared | To the extent relevant for carrying out its functions |

| Representation | Does not represent the RE | Represents the RE |

| Agency & Principal | Not an agent | Appointed as an agent |

| DLG | Cannot provide | Can provide (in case of Digital Lending and Co-lending) |

| Applicability of Outsourcing Guidelines | Not applicable | Applicable |

| Mandatory due diligence before appointment | Not applicable | Applicable |

| Appointment of GRO | No such requirement | LSP having interface with borrower needs to appoint a GRO |

| Right to audit | No right of RE | RE has a right |

| Disclosure on the website of the lender | Not applicable | Applicable |

Table 1: Distinction between Referral Partner and LSP

As digital lending continues to expand in India, ensuring that every intermediary’s role aligns with its true legal character is essential. The key in determining the true nature of the relationship would ultimately rest on the contractual terms that must reflect the true nature of the relationship. Misclassifying these entities can expose lenders to compliance risks under RBI’s outsourcing and digital lending guidelines.

Our resources on the same:

– Harshita Malik | finserv@vinodkothari.com

On April 30, 2025, the Supreme Court of India delivered a landmark judgment in Pragya Prasun & Ors. v. Union of India, declaring digital access as an intrinsic component of the fundamental right to life under Article 21. The Court issued comprehensive directions to make digital KYC processes accessible to persons with disabilities, particularly acid attack survivors and visually impaired individuals.

This judgment fundamentally transforms how banks and NBFCs must approach customer onboarding through digital means, with immediate compliance requirements and potential legal consequences for non-adherence.

Pursuant to the directives issued by the Supreme Court, the RBI has amended the Master Direction – Know Your Customer (KYC) Direction, 2016 (‘KYC Directions’) vide Reserve Bank of India (Know Your Customer (KYC)) (2nd Amendment) Directions, 2025 (‘KYC 2nd Amendment’).

The petitioners in these cases highlight significant barriers faced by persons with disabilities in accessing digital KYC processes. WP(C) No. 289 of 2024 involved acid attack survivors who were unable to complete digital KYC, while WP(C) No. 49 of 2025 involves a visually impaired individual facing similar difficulties. A notable incident involved Pragya Prasun, who was denied the opening of a bank account due to her inability to perform the blinking required for liveness verification. These cases are grounded in the protections afforded by the Rights of Persons with Disabilities Act, 2016, and the fundamental right to life and personal liberty under Article 21 of the Constitution.

The Court recognized that existing digital KYC processes create obstacles for persons with disabilities:

| Barrier Type | Specific Issues | Affected Population |

| Liveness Detection | Mandatory blinking, head movements, reading displayed codes | Acid attack survivors, visually impaired |

| Screen Compatibility | Lack of screen reader support, unlabeled form fields | Visually impaired persons |

| Visual Dependencies | Selfie capture, document alignment, front/back identification | Persons with visual impairments |

| Signature Verification | Non-acceptance of thumb impressions in digital platforms | Persons unable to sign consistently |

“Digital access is no longer merely a matter of policy discretion but has become a constitutional imperative to secure a life of dignity, autonomy and equal participation in public life.”

– Justice R. Mahadevan

The Supreme Court has firmly declared that digital access is no longer just a policy choice but a constitutional necessity to ensure individuals’ dignity, autonomy, and equal participation in society. This constitutional and legal mandate is grounded in several provisions: Article 21 guarantees the right to life with dignity, requiring digital services to be accessible to everyone; Section 3 of the Rights of Persons with Disabilities (RPwD) Act, 2016, ensures equality and prohibits discrimination against persons with disabilities; Section 40 mandates that all digital platforms adhere to established accessibility standards and Section 46 sets a two-year timeline within which service providers must achieve compliance with these accessibility requirements.

The Supreme Court issued twenty directives in the said judgement to ensure that services are not denied based on disability and digital services are accessible to all the citizens irrespective of the impairments. Most of these are for the regulators, while a few are for regulated entities.

Following is the list of actionables arising out of the directives for banks and NBFCs:

Changes have been introduced in the KYC Directions via the KYC 2nd Amendment as a result of the SC verdict, these are captured in the diagram:

Implementation Plan

Based on the Supreme Court directive in Pragya Prasun & Ors. vs Union of India and the subsequent RBI notification, here is a comprehensive stage-wise action plan for implementing digital accessibility requirements for banks and NBFCs:

Actionables for REs under phase 1 are listed below:

Actionables for REs under phase 2 are listed below:

Actionables for REs under phase 3 are listed below:

Actionables for REs under phase 4 are listed below:

Actionables for REs under phase 5 are listed below:

Actionables for REs under phase 6 are listed below:

The Supreme Court’s judgment in the Pragya Prasun case elevates digital accessibility from a moral imperative to a constitutional mandate. Banks and NBFCs must view this not as a burden but as an opportunity to transform compliance into competitive advantage by becoming an accessibility leader.

[1] List of Empanelled Web Accessibility Auditors with Department of Empowerment of Persons with Disabilities, Ministry of Social Justice & Empowerment, Govt. of India.

Read More: Resources on KYC

Archisman Bhattacharjee | finserv@vinodkothari.com

The National Payments Corporation of India (NPCI), vide its notification NPCI/2024-25/e-KYC/003 dated 10 March 2025, formally introduced the e-KYC Setu facility. As outlined on NPCI’s official platform, e-KYC Setu enables Aadhaar-based e-KYC authentication under the Aadhaar (Targeted Delivery of Financial and Other Subsidies, Benefits and Services) Act, 2016 (Aadhaar Act), without disclosing the individual’s Aadhaar number to the requesting (verification-seeking) entity.

Designed as a one-stop onboarding solution for regulated financial-sector entities, e-KYC Setu leverages Aadhaar-based e-KYC services while ensuring compliance with privacy safeguards under the Aadhaar Act. A key feature and a significant compliance advantage is that regulated entities using e-KYC Setu are not required to obtain a separate notification under Section 11A of the Prevention of Money-laundering Act, 2002 (PMLA). This allows financial sector regulator entities to conduct Aadhaar-based authentication without directly collecting Aadhaar numbers or integrating with UIDAI as a licensed AUA/KUA, thereby reducing both operational complexity and regulatory burden.

In this article, we examine the regulatory implications for RBI-regulated entities, the legal permissibility for non-AUA/KUA entities to conduct authentication through e-KYC Setu, process how e-KYC setu operatives and the operational and business benefits of adopting this framework.

Read more →