Presentation on Controls over RPTs.

Read more on RPTs here.

Read more on RPTs here.

Harshita Malik and Anshika Agarwal (finserv@vinodkothari.com)

-Subhojit Shome (subhojit@vinodkothari.com)

The tokenisation of real-world assets (RWA) using cryptographic technology is rapidly emerging as a transformative innovation in the financial ecosystem. Note here that the term RWA refers to all traditional assets including both real assets as well as traditional financial assets that exist in the physical world. By leveraging blockchain technology, tokenisation enables the representation of tangible assets, such as real estate, commodities, and artwork, or intangible assets like intellectual property, as digital tokens on a distributed ledger. This development is reshaping the way assets are managed, traded, and accessed, creating new opportunities and challenges.

RWA tokenisation has garnered attention due to several converging factors. Blockchain technology offers a streamlined alternative to traditional systems by reducing intermediaries, lowering transaction costs, and ensuring faster settlement times. Fractional ownership of high-value assets makes them accessible to a broader range of investors, enhancing market liquidity. Blockchain’s immutable nature provides a transparent record of transactions and ownership, reducing fraud and enhancing trust. Additionally, tokenised assets are borderless, enabling seamless cross-border trading and investment opportunities.

According to market reports, the capital locked in tokenised RWA is expected to touch $50 billion by the end of 2025 surpassing all previous records. In 2024, the ecosystem had achieved a 32% annual growth rate.

In this article, we look at the impetus behind this technology, its status of adoption in India and critical issues that act as roadblocks in its development.

The tokenisation market has witnessed significant advancements in a number of areas. Real estate tokenisation has enabled properties to be tokenised for fractional ownership, reducing entry barriers for smaller investors. Similarly, commodities like gold and other precious metals have been tokenised, providing an efficient means of trading and ownership. High-value artworks and collectibles are being tokenised to allow multiple investors to own shares in masterpieces. Tokenisation has also extended into private equity and debt markets, enabling innovative funding mechanisms and the development of secondary market opportunities. Moreover, the emergence of regulated tokenisation platforms in certain developed economies (e.g. the UK) underscores the growing maturity of this market.

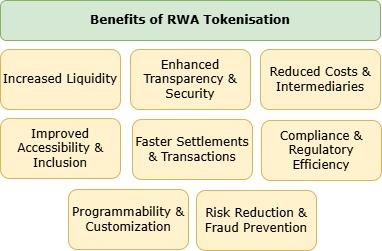

Figure 1: Benefits of Tokenisation of Real-World Assets using Blockchain

Fractional ownership creates liquidity in traditionally illiquid assets. It also democratises investment by enabling wider participation through reduced minimum investment thresholds. Here the emphasis is not on reduction of any regulatory investment threshold but rather, being represented in the digital world, RWA tokenisation allows infinitesimally fractional parts of an asset to be bought and sold. Cost efficiency is achieved by reducing reliance on intermediaries, which lowers transaction and administrative costs. Blockchain’s transparency increases trust and reduces fraud risks. Furthermore, smart contracts enable automation of compliance, dividend distribution, and other processes.

The process of RWA tokenisation broadly involves the following steps –

Figure 2: Process of RWA tokenisation

In the tokenisation process one may note that the custody of the underlying asset is separated from the ownership of the asset. While the ownership is represented by use of tokens, the underlying asset may need to be held with a custodian ‘off-chain’ (i.e. in the physical world).

However, tokenisation is not without challenges. Regulatory uncertainty remains a significant hurdle due to inconsistent global regulatory frameworks. Technology risks, such as cybersecurity concerns and vulnerabilities in smart contracts, could undermine trust. Market volatility is another concern, as tokens may experience higher price fluctuations compared to their underlying assets. Some tokenised assets may face illiquidity risks if the secondary markets lack sufficient depth. Additionally, legal ambiguity regarding ownership rights and the enforceability of tokenised claims persists in many jurisdictions.

Several key regulatory considerations must be addressed. Asset classification is crucial for defining whether tokenised assets are securities, commodities, payment instruments or another category altogether.

In India, regulatory uncertainty remains the key issue in the implementation of RWA tokenisation. Say, for instance, there is tokenisation of real estate in which the management of the property is overseen by the issuer or by a manager appointed by such issuer and fractional ownership units are offered for sale to retail investors. Such a transaction starts to take on the colour of a collective investment scheme and SEBI may intervene and mandate the issuer to register as such with the regulator. In the case of real estate these schemes can also be viewed as having a structure akin to a REIT especially SM REIT.

The SEBI is yet to notify any regulatory prescription specifically for the purposes of regulating crypto-assets and or token offerings to the retail public and it has been reported in the press1 that the securities market regulator has informed the Parliamentary Standing Committee on Finance that regulation of crypto-assets would be difficult given the nature of technology that sustains them. In the matter of, An RTI enquiry, as referenced in the matter of Appeal No. 4532 of 2021 filed by Rohith Methayil Rajagopal, was raised with the SEBI’s CPIO as to the stand of Regulator with regard to “digital trading and possession of Cryptocurrencies by the Indian Citizens” and if SEBI had any “legal document and its date that permits digital trading of Bitcoin / Cryptocurrencies in India”. The response of the CPIO, as affirmed by the appellate authority, was that it did not have the knowledge of either matter. Based on this one can conclude that the Regulator has not, yet, formalised its stance over dealings in crypto assets. Recently, however, the Regulator has expressed an openness to a multi-regulator based oversight framework for crypto-assets.2

There have been interest shown by mutual fund houses to invest in ETFs or indices on blockchain-based projects and crypto-assets and draft scheme information documents were filed with the Regulator. SEBI, however, has expressed its reservations3 on approving such funds/ fund of funds. Highlighting high degree of regulatory uncertainty when it comes to crypto-assets which is not an ideal situation either for business houses looking to raise funds using crypto-assets or for investors who have invested in such assets.

Another major inhibitor is the tax treatment of such tokenised assets. This is because given the construct of such token it will get classified as virtual digital asset under section 2(47A)4 of the Income Tax Act, 1961. The implication of this is that income on sale of such assets will get taxed at a flat rate of 30%. Other than the cost of acquisition, any other expenses incurred with respect to such assets are not allowed to be deducted while computing the income. Further, any loss from the transfer of such assets are also not allowed to be set-off against such income or under income computed under any provision of the act. Accordingly, such losses are also not allowed to be carried forward to any succeeding assessment years.

Recently, however, there has been some headway in asset tokenisation in Gujarat International Finance Tec-City (GIFT City) which may be poised to host India’s inaugural regulated platform for the tokenization of real estate and infrastructure assets. This initiative aims to democratize investment opportunities by enabling fractional ownership through digital tokens, leveraging blockchain technology to enhance liquidity and transparency in the sector. To this extent the IFSCA has constituted an ‘Expert Committee on Asset Tokenization’; the terms of reference of this committee are as follows –

Tokenisation is a transformative technology that has the capability to change the very nature of real world assets in the way they are managed and traded. The flow of capital into this sector is an indication of the potential of this sector in contributing to the economic growth of a country. In the formation of the working group on crypto-assets to reform US digit asset regulations, the US has taken stock of this development in the market and the need to make such technologies mainstream. It is encouraging to see India’s intention to move ahead with such innovation in the GIFT City. It is now time to wait and watch whether tokenisation will find acceptance in the economic mainstream and for this to happen a clear regulatory architecture has to emerge in India.

February 03, 2025

-Prapti Kanakia, Manager & Anjali Singh, Executive | corplaw@vinodkothari.com

Read More:

FEMA facilitates acquisition of foreign entity by Indian companies through cross border swaps

RBI revamps Master Directions on Compounding under FEMA

Powers of RBI Officers enhanced for compounding FEMA offences

– Sourish Kundu, Executive | resolution@vinodkothari.com

Disclosure in 24 hours for new matters; updates of ongoing litigations in Integrated Filing (Governance)

– Nitu Poddar, Partner and Simrat Singh, Executive | corplaw@vinodkothari.com

Based on the recommendation of the Expert Committee for facilitating EODB, SEBI, vide Circular dated December 31, 2024 have made a distinction in stock exchange disclosure relating to tax litigations and non-tax litigations. While matters pertaining to “new” tax litigations are required to be disclosed based on materiality under Reg 30(4), updates on such “ongoing” / existing tax litigations are supposed to be disclosed quarterly in the Integrated Filing (Governance). In this note1, we discuss the probable questions that may come up around this disclosure.

Read more →– Barsha Dikshit and Neha Malu | resolution@vinodkothari.com

The provisions related to the carry forward and set-off of business losses in the context of corporate restructuring have been a critical aspect of corporate taxation. The Budget 2025[1] proposes certain amendments concerning carry forward of losses in cases of amalgamation, pursuant to which mergers shall not be used for evergreening of losses. That is to say, the benefit of carry forward shall be limited to eight years from the onset of losses, and not eight years from the merger.

Read more →The Master Direction on Foreign Investment in India, recently updated on January 20, 2025, goes beyond a mere consolidation of the recent amendments in the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (‘NDI Rules’), providing clarifications in several areas of legislative silence. One of the key areas of clarification include the rules around downstream investments.

In this note, we have discussed downstream investment through stock deals and other significant clarifications provided in the Master Direction.

Rule 6(a) of the NDI Rules deals with the investment by a person resident outside India (‘PROI’) in the equity instruments of an Indian company. The said rule refers to Schedule I, which, amongst others, specifies the modes of payment of consideration. Prior to the FEM (Non-Debt Instruments) (Fourth Amendment), Rules, 2024 dated August 16, 2024 (“Fourth Amendment Rules”), the Schedule contained an enabling provision for Indian companies to issue its equity instruments to PROI by way of swap of equity instruments. Since the term “equity instruments”, as defined under Rule 2(k) of Principal NDI Rules, means equity shares, convertible debentures, preference shares and share warrants issued by an Indian company, the provision permitting share swaps was read narrowly to refer to swap of shares of an Indian company against that of another Indian company only.

However, pursuant to the Fourth Amendment Rules, the Schedule was further amended to expressly provide for the swap of equity capital, as defined under rule 2(1)(e) of Foreign Exchange Management (Overseas Investment) Rules, 2022. The same is defined as “equity shares or perpetual capital or instruments that are irredeemable or contribution to non-debt capital of a foreign entity in the nature of fully and compulsorily convertible instruments.”

Downstream investment, on the other hand, is governed by the provisions of Rule 23 of the NDI Rules. While the said rule specified certain requirements to be complied with in the context of downstream investment, including the sources through which funds can be brought in for the purpose of such investments, the rule neither explicitly provided for the share swaps as a permitted mode of payment, nor contained any reference to Schedule I of the NDI Rules. As a result there was uncertainty among industry stakeholders on permissibility of share swaps as a form of consideration in case of downstream investment.

The explanation to Rule 23 (also contained in Para 9.1.13 of the Master Direction) states that:

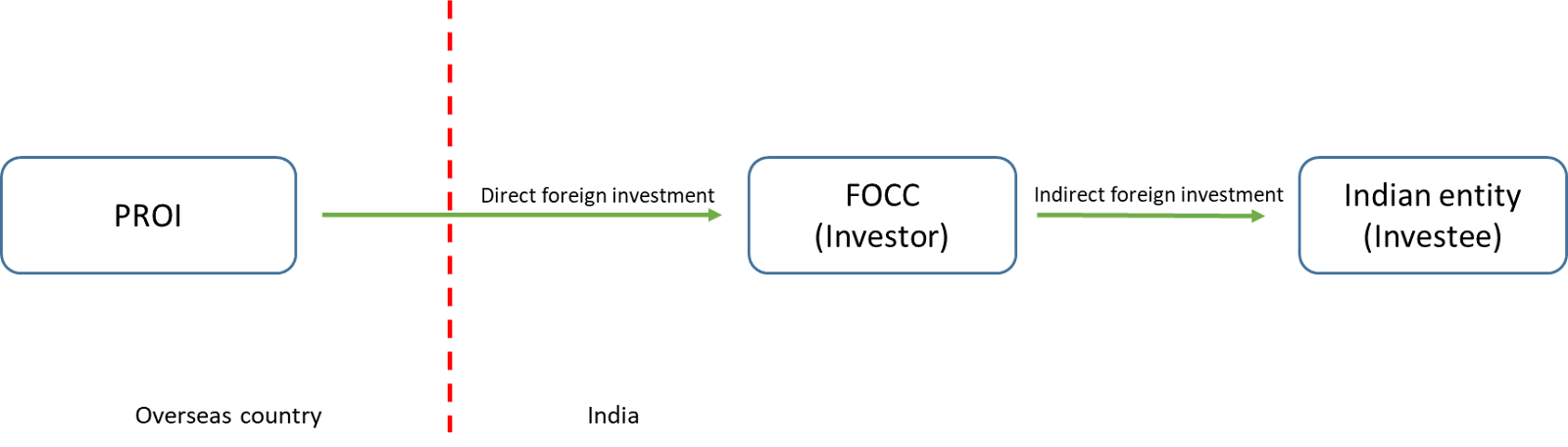

Downstream Investment is an investment made by an Indian entity which has received foreign investment or an Investment Vehicle in the equity instruments or the capital, as the case may be, of another Indian entity.

In other words, when an Indian entity owned or controlled by PROI [commonly referred to as a Foreign Owned and Controlled Entity (FOCC)] makes investments in the equity instruments/ capital of an Indian entity, such an investment will be considered as downstream investment for the PROI. Such arrangements enable PROI to hold investment in other Indian entities indirectly, thus, considered as an indirect foreign investment. As a result, the restrictions, prohibitions and limitations as applicable to direct foreign investments will be applicable at the time of downstream investment as well. For better understanding, refer to the figure below:

The recent updates in the Master Directions provide for the guiding principles of downstream investments, thereby clarifying that all permissions and prohibitions vis-à-vis direct foreign investment under the NDI Rules will be applicable to indirect foreign investment (i.e. downstream investment) as well.

Para 9 of the Recent Master Direction reads as below:

“The guiding principle of the downstream investment guidelines is that “what cannot be done directly, shall not be done indirectly”. Accordingly, downstream investments which are treated as indirect foreign investment are subject to the entry routes, sectoral caps or the investment limits, as the case may be, pricing guidelines, and the attendant conditionalities for such investment as laid down in the NDI Rules.”

Giving reference to above guiding principles, the Master Directions explicitly refers to the permissibility of the arrangements which are available for direct investment such as investment by way of swap of equity instruments/equity capital, payment arrangements/mechanism as per Rule 9(6) of the Rules etc, for the purpose of downstream investment as well.

The above clarification has paved a way for Foreign Owned or Controlled entities (FOCC) to make further investments in Indian entities by way of swapping equity capital of foreign companies held by it in addition to other sources as already available. This arrangement of swapping of securities is known as a stock deal.

Previously, for making downstream investment, an FOCC was allowed to raise fresh funds from abroad by way of issue of securities including non-convertible debentures or by utilising internal accruals such as profits after tax. For more clarity refer to the table below:

| Sources of making investment by FOCC in another Indian entity | Position prior to the clarification | After clarification |

|---|---|---|

| Internal accruals (i.e., profits transferred to reserve account after payment of taxes) | Allowed | Allowed |

| Fresh funds from abroad including issue of NCD | Allowed | Allowed |

| Swap of equity instruments/ capital | No express provision | Allowed |

| Using funds borrowed in the domestic markets | Not allowed | Not allowed |

As per the guiding principle on downstream investments as discussed above, an Indian entity which has received indirect foreign investment is subject to permissions and prohibitions as applicable to direct foreign investment under NDI Rules. Further, the onus of ensuring such compliances are on the FOCC making such investments, and not on the Indian investee entity receiving such indirect FDI.

In order to curb opportunistic takeovers/ acquisitions of Indian companies due to COVID-19 pandemic, the Government of India restricted investment from countries sharing land borders with India or where the beneficial owner of an investment into India is situated in or is a citizen of any such country, by way of issue of Press Note-3. As a result, any foreign direct investment from such countries would be permitted with prior approval of the Government of India in permissible sectors.

This will be applicable in case of investment by FOCC as well, where such FOCC, in turn, has received investment from such countries as discussed above.

Similarly, the facility of making deferred payment of up to 25% in case of transfer of equity instruments between PROI and Person Resident in India (PRI) will also be applicable in case of downstream investment. This is, subject to the compliance with the conditions as laid down in Rule 9(6) of the NDI Rules.

The Master Directions further state that a transaction intended to be undertaken using above arrangement(s) shall require the share purchase/transfer agreement to contain the respective clause and related conditions for such arrangement.

Where an Indian entity (i.e., investor) at the time of making further investment in another Indian entity (i.e., investee) was not an FOCC at the time of investment, but subsequently becomes an FOCC, then such investment in another Indian entity would need to be reclassified as downstream investment from the date when investor entity becomes FOCC. Consequently, such downstream investment shall be in compliance with the applicable entry route and sectoral cap compliances and shall be required to be reported by the investor entity within 30 days from the date of such reclassification in form DI.

As per para 8.4 of the Recent Master Direction, in case of swap of equity instruments, irrespective of the amount, valuation will have to be made by a Merchant Banker registered with SEBI or an Investment Banker outside India registered with the appropriate regulatory authority in the host country.

The investments made by NRIs/OCIs on non-repatriation basis is treated as deemed domestic investment. Accordingly, an investment made by an Indian entity which is owned and controlled by a Non-Resident Indian or an Overseas Citizen of India including a company, a trust and a partnership firm incorporated outside India and owned and controlled by a Non-Resident Indian or an Overseas Citizen of India, on a non-repatriation basis in compliance with Schedule IV of these rules, shall not be considered for calculation of indirect foreign investment.

To know more about foreign investment, check out our YouTube repository on:

– Team Finserv (finserv@vinodkothari.com)

Loading…

Loading…