Stock exchange reporting of tax litigations made less taxing

Disclosure in 24 hours for new matters; updates of ongoing litigations in Integrated Filing (Governance)

– Nitu Poddar, Partner and Simrat Singh, Executive | corplaw@vinodkothari.com

Based on the recommendation of the Expert Committee for facilitating EODB, SEBI, vide Circular dated December 31, 2024 have made a distinction in stock exchange disclosure relating to tax litigations and non-tax litigations. While matters pertaining to “new” tax litigations are required to be disclosed based on materiality under Reg 30(4), updates on such “ongoing” / existing tax litigations are supposed to be disclosed quarterly in the Integrated Filing (Governance). In this note1, we discuss the probable questions that may come up around this disclosure.

What is the change?

- Tax litigations have been distinguished from non-tax litigations on two fronts:

- Determination of materiality

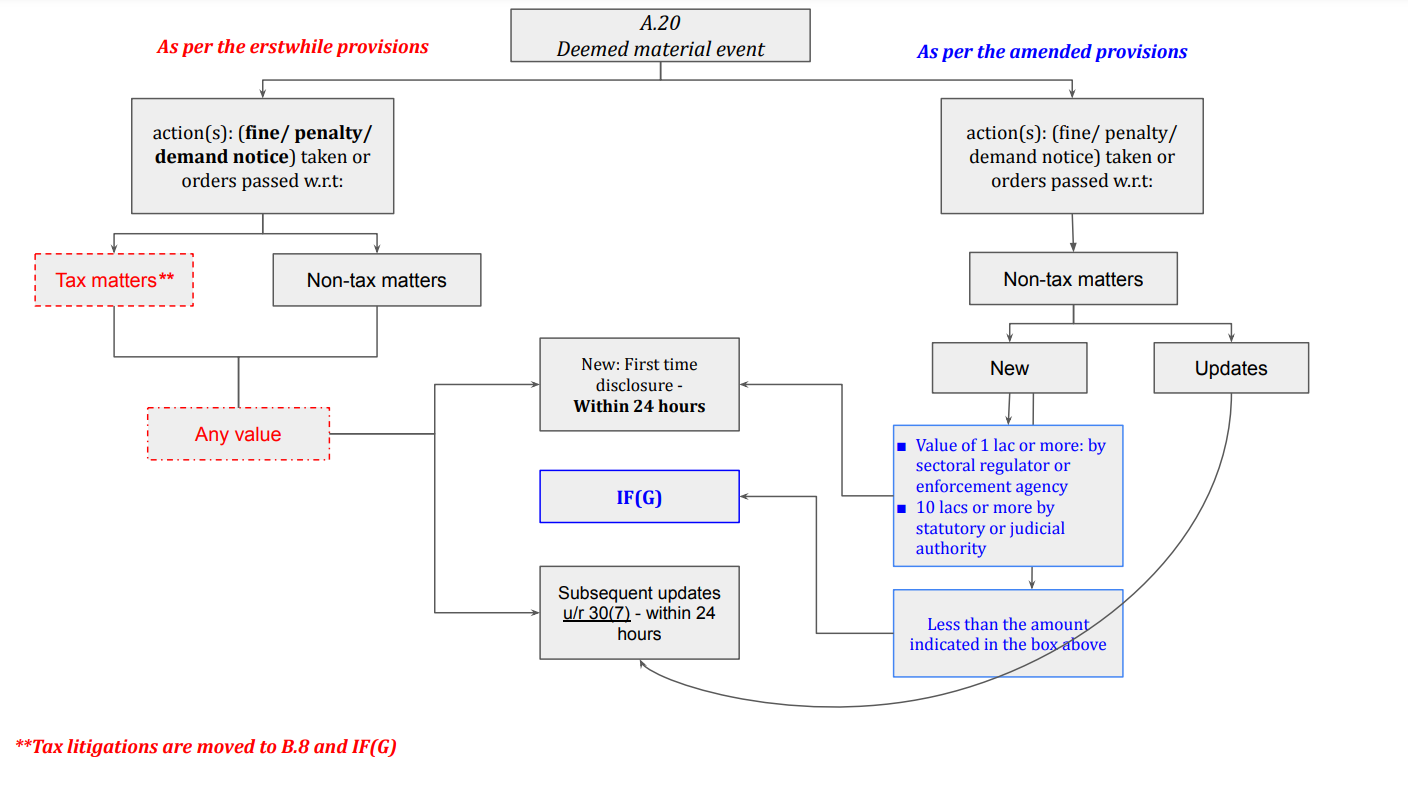

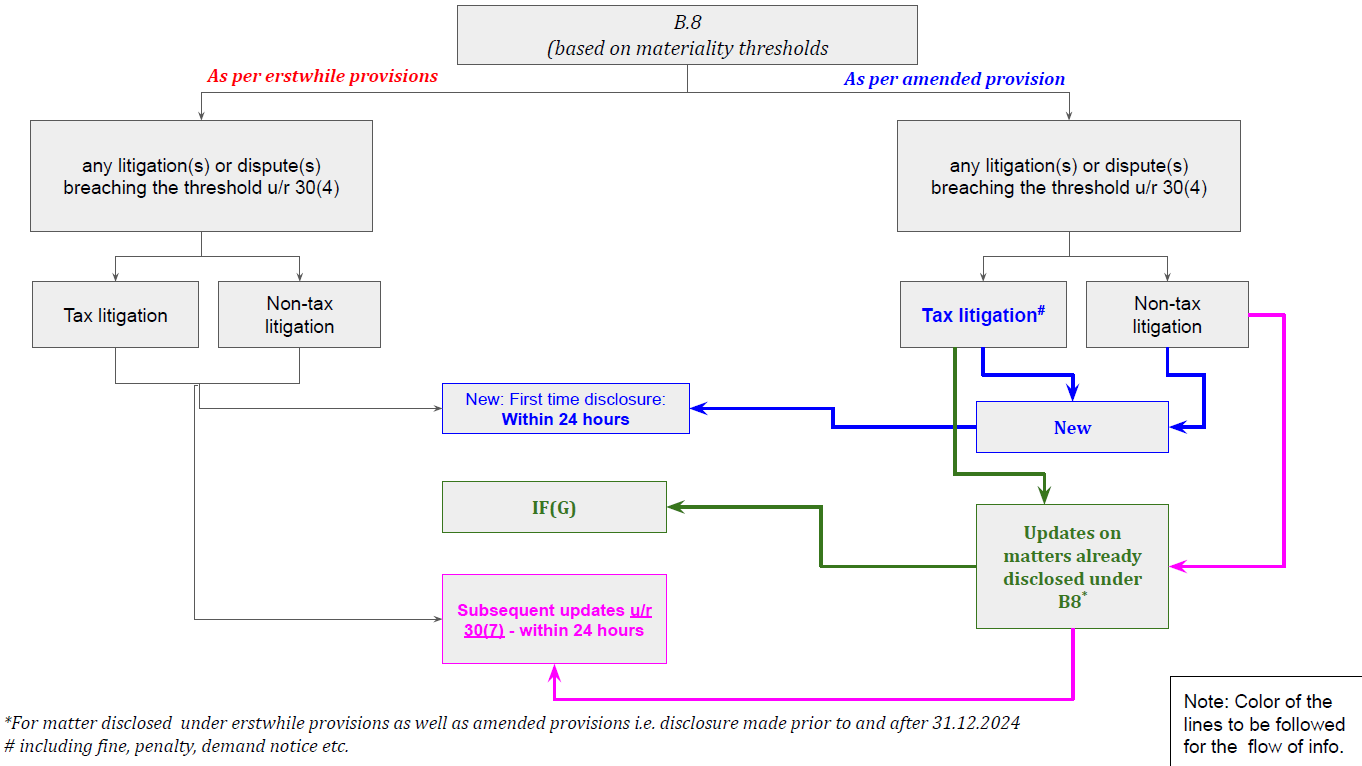

Tax litigations or disputes, including demand notices, penalties shall be disclosed only under clause 8 of para B based on the material thresholds of reg. 30(4). No disclosure in respect of tax litigation (including for penalty imposed) is required to be made u/c 20 of para A as a deemed material event.

- Timeline of disclosing updates on material tax litigations:

New tax litigations are required to be disclosed based on materiality u/r 30(4) within 24 hours from the receipt of notice by the listed entity. For the purpose of determination of materiality:

- matters, outcome of which are likely to have high correlation, should be cumulated.

- Amount of demand, penalty, interest which arise from the same cause of action should be clubbed. Illustration: if a certain non-allowable tax deduction was taken in FY 23-24 which gave rise to a tax proceeding and subsequently another proceeding was initiated in FY 25-26 for the same non-allowable deduction, in such case, outstanding tax demands for these 2 proceedings should be clubbed as they arise from the same cause of action.

Updates on ongoing tax litigations are required to be disclosed on a quarterly basis as part of Integrated Filing (Governance). This is an “update” only on the “ongoing” tax litigations and not a new filing. Unlike the timeline mentioned u/r 30(7) for disclosure of material development done on a “regular basis” for all other material event / information disclosed, for tax litigation matters are to be done on a quarterly basis.

This does not warrant assessing the materiality of all tax litigations to which the company is a party. Only updates on matters which have already been disclosed to the stock exchange in the past are required to be disclosed through this quarterly disclosure. As discussed in SEBI Board Meeting dated 30th September, 2024, quarterly update will provide relaxation for the listed entities to provide updates on material tax litigations on a quarterly basis rather than immediately.

Note that the template of IF(G) requires the listed entity to inter-alia mention the ‘status of the litigation / dispute as per last disclosure’ as well as the ‘current status of the litigation / dispute’ which supports the argument that screening of all current tax litigations against the listed entity to determine if they are material or not is not required. What is required is to provide an ‘update’ on the already disclosed tax litigations.

| Type of litigation | Applicability of Clause 20, para A | Applicability of Clause 8, para B | Timeline of disclosure | |

| Tax litigation | New | ✘ | ✔ (based on materiality) | Within 24 hours of receipt of notice |

| Updates | ✘ | ✘ | Quarterly in IF(G) | |

| Non-tax litigation | New | ✔ (based on the authority involved and the nature of action taken against the listed entity falling under sub-clause (a) to (i) of clause 20) | ✔ (based on materiality) | If all relevant information is maintained in SDD – within 72 hours from the receipt of notice. In other cases – within 24 hours from the receipt of notice. |

| Updates [specific disclosure to be made to the stock exchange. This is not part of IF(G)] | To check material developments u/r 30(7) | Within 24 hours from the occurrence of material development u/r 30(7). | ||

Intent of the change:

Considering that matters relating to tax demand, penalty, notices, disputes etc under IT Act, GST, etc are in the ordinary course of business of the entity, clubbing them with other (non-tax) litigation leads to spamming the investors with too much data scattered throughout. Therefore segregation.

Further, given the likelihood of litigation of any tax demand / dispute and the same getting turned down by the higher authorities, regular updates may be premature / adds up to the compliance burden, therefore quarterly updates through IF(G).

Disclosure of new tax litigation vs updates

FAQs:

- What factors are to be considered to determine materiality of any tax litigation?

Materiality of any tax litigation is based on the impact of its outcome on the listed entity. The “impact” is judged by the quantum of tax demanded, penalty imposed or penal interest charged in the proceeding.. As indicated above, tax litigations whose outcomes have high correlation should be clubbed to assess their materiality.

- At what stage of the litigation, applicability of materiality for the purpose of disclosure to be checked?

Parameters for checking applicability of materiality of tax litigations

| Type of litigation covered: | Who has to be the party to litigation: | When is the materiality to be checked: |

| assessment adjudication arbitration or dispute in conciliation proceedings; | the entity, its directorits, KMP, SMP, promoter and its subsidiary | Upon any of the above entities becoming party to the litigation; or Upon institution of any litigation (as mentioned above); or Upon passing of any ad-interim or interim orders, against or in favour of the listed entity the outcome of which can reasonably be expected to have an impact. |

- Will a notice of penalty from tax authority be disclosed under clause 20, Para A Part A of Schedule III?

No disclosure is required to be made u/c 20 of para A part A for w.r.t any tax litigation.

Gist of the amendment:

Our other resources:

Dear Team

Thanks for such a detailed analysis. Have one doubt w.r.t. fines and penalties order received from the Tax Authorities above threshold as prescribed in Clause 20 Part A Para A of Sch. III. As per my understanding, the Tax penalty order if crossing said limit need to be covered and disclosed under clause 20, and any litigation done thereafter will be regulated by Tax Litigation provisions. Please suggest w.r.t. FAQ point 3 above….regards