Archive for year: 2020

Another couple of stepladders for the MSMEs

-Kanakprabha Jethani (kanak@vinodkothari.com)

Background

On June 24, 2020, Ministry of Finance (MoF) issued two press releases with respect to further measures to support the MSME sector during the current situation of crisis. One of these launched the Credit Guarantee Scheme for Subordinate Debt (CGSSD)[1] (‘Debt Scheme’) and the other one announced an interest subvention of 2% for a period of 12 months, to all Shishu loan accounts under Pradhan Mantri Mudra Yojana (PMMY) to eligible borrowers[2] (‘Subvention Scheme’).

The COVID-19 disruption and subsequent downfall of the economy has impacted the MSME sector drastically. MSMEs are a crucial component of the Indian economy and hence, it is necessary to uplift them, so as to bring the economy back on track. In this backdrop, the Government of India (GoI) has been taking various measures and introducing schemes to provide the much needed liquidity to MSME sector. The recently introduced schemes are yet another step in that direction. The following write-up provides runs through the basics of these schemes focusing on the practical issues that may arise while implication.

SEBI’s measures towards resuscitation of financially “stressed” companies

Henil Shah | Executive

Introduction & Background

In layman’s term, a company with falling share prices, inability to pay off its obligations is said to be a company with financial distress. In most of the times, it is seen that the conventional means of fund raising such as borrowings, issuance of debt securities etc. do not work for such companies due to their ongoing stressed status even though generating cash is the foremost priority for them to fund their operations. Additionally, insolvency/ bankruptcy also becomes a matter of concern which may be caused due to the lack of funding and the resultant disruption in operation.

SEBI’s Primary Market Advisory Committee (PMAC) deliberated on the topic and came out with a Consultation Paper dated April 22, 2020[1] providing for the proposed measures for resuscitation of the stressed companies. The changes so proposed were w.r.t certain amendments under the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (ICDR Regulations) and SEBI (Substantial Acquisitions of Shares and Takeovers) Regulations, 2011 (SAST Regulations). Based on the public comments, SEBI vide Notifications dated June 23, 2020 has prescribed the final text of the amendments under the ICDR Regulations[2] and SAST Regulations[3]

The article covers a brief synopsis and the relevant impact/ actionable pursuant to the said amendments.

Rationale behind the proposed changes

Preferential issue seems to be one of the most sought options of fund raising by the companies due to the administrative as well as regulatory convenience it carries. Further, knowing the probable investors ready to invest in the company makes a preferential issue one of the most commonly used ways for raising funds.

For a listed company, under a preferential issue, the issue price has to be determined as per the pricing provisions of Chapter V of ICDR Regulations. The ICDR Regulations provides the pricing mechanism for both frequently traded shares and infrequently traded shares.

In case of frequently trades shares, the price shall be determined as per the provisions of Regulation 164(1) (a) & (b) of the ICDR Regulations which are as follows.

Even though a preferential issue may be a convenient way of fund raising for a well performed company, the same may not be the case for a company with financial distress for the following reasons:

1. Onerous pricing mechanism

Considering the continuous falling prices of the shares over a period of 26 weeks due to the company being in stress, the determination of the price as per the pricing mechanism provided in Regulation 164(1) (a) becomes too onerous for the investor. Further, the price under Regulation 164(1) (a) is much higher than that as determined as per Regulation 164(1) (b). Hence, the pricing mechanism acts as a major deterrent for the investors from subscribing to the shares offered under the preferential issue.

2. Exemptions only to 5 QIBs restricting investor pool

Though the ICDR Regulations allow issuance to QIBs at a price determined as per regulation 164(1) (b) however, the same is restricted to only 5 QIBs and is not applicable to the investors other than QIBs thereby restricting the investor pool.

3. Open offer obligations for the acquirer

Another roadblock which the issuers tend to face is from the view point of the investors i.e. an incoming investor who has an impending burden on complying with an open offer obligation in case where the subscription to the preferential offer leads to the triggering of the open offer obligations under SAST Regulations. In view of the procedural requirements and the huge costs involved, making an open offer discourages the investors seeking to have a substantial stake in the company in order to take control and thereby reverse the stress.

As per the extant provisions, the acquisition pursuant to a resolution plan approved under the Insolvency and Bankruptcy Code, 2016 is exempted from meeting the open offer obligations but no such exemption has been provided in case for acquisition in the financially distressed entity which are not under any resolution plan.

Rescue mechanism brought through the amendments

Insertion of regulation 164A in ICDR Regulations

The newly inserted provisions incorporate the changes that were proposed by PMAC into the existing regulations as discussed below:

When to consider a company at ‘stress’?

For a company to be classified as financially stressed and issue equity share in pursuance of regulation 164A of ICDR regulations it has meet certain conditions. Below is a comparative presentation between the text of the Consultation Paper and the final text of the Regulations. Further, any two of the three conditions shall have to be satisfied for considering a company as stressed.

| PMCA Recommendations | Final text of the Regulations | Remarks |

| A listed company which has made disclosure of defaults on payment of interest/ principal amount of loans from banks/ financial institutions and listed and unlisted debt securities for 2 consequent quarters in terms of the SEBI Circular dated November 21, 2019[4] issued in this regard.

|

The issuer has disclosed the default relating to the payment of interest/ repayment of principal amount on loans from banks/ financial institutions/ NBFCs- ND-SI and NBFCs-D and/ or listed on unlisted debt securities in terms of SEBI circular dated November 21, 2019 and such default is continuing for a period of at least 90 days after occurrence of such default.

|

The amendment regulation in slight contrast to the PMAC recommendations provided shorter timeline for calculating continuity of the default.

Further, even though NBFCs-ND-SI and NBFCs- D already get covered under the definition of Financial Institution provided under RBI Act, they have been specifically covered under the list of creditors. |

| Existence of Inter-Creditor agreement in terms of Reserve Bank of India (Prudential Framework for Resolution of Stressed Assets) Directions 2019[5] (RBI Directions)

|

Same as PMCA Recommendations | Inter-Credit agreement as provided in the RBI Directions stands for the agreement executed among all the lenders of a defaulting borrower, providing for ground rules for finalisation and implementation of resolution plan in respect to the borrower. |

| Credit rating of the listed instruments of the company has been downgraded to “D”. | The credit rating of the financial instruments (listed or unlisted), credit instruments/ borrowings (listed or unlisted) of the listed company has been downgraded to “D” | The final text of the amendments, in addition to the listed instruments, also brings unlisted instruments and as well as borrowings under its purview. |

Pricing of preferential issue of shares of companies having stressed assets

Unlike the current pricing requirements as provided in Regulations 164(1) (a) & (b) of ICDR Regulations for a preferential issue, the price of the shares to be issued by a stressed company as aforesaid shall be a price which shall not be less than the average of the weekly high and low of the volume weighted average prices of the related equity shares quoted on a recognised stock exchange during the two weeks preceding the relevant date. Therefore, the price as determined under Regulations 164(1) (a) & (b) of ICDR Regulations shall not be considered.

Negative list of proposed investors

The following person(s) shall not be eligible to participate in the preferential issue under Regulation 164:

- Persons/entities part of promoter or promoter group will not be eligible to participate in the preferential issue;

- Undischarged insolvent in terms of Insolvency and bankruptcy Code, 2016 (IBC, 2016);

- Wilful defaulter as per RBI guidelines issued under the Banking Regulations Act, 1949;

- A person disqualified to act as director as per Companies Act, 2013

- Person debarred from trading in securities or accessing securities market by SEBI and period of debarment has not been over

- Person declared as fugitive economic offender

- Person is convicted of offence punishable with imprisonment

- For a period of 2 years or more under any as specified under 12th schedule of IBC, 2016

- 7 years or more under any law for time being in force

and a period of 2 years has not been subsisted from his release form imprisonment.

- Person who has executed a guarantee in favour of a lender of the issuer and such guarantee has been invoked by the lender and remains unpaid in full or part.

Approval from shareholders falling under ‘public’ category

For companies with identifiable promoters

The amendments provides for an approval for the preferential issue by the majority of the shareholders in the ‘public’ category. The ‘public’ category of shareholders does not include promoter shareholders and also any proposed allottee who is already a holder of specified securities of the issuer. Therefore, the same is said to be an approval with majority of the minority.

For companies with identifiable promoters

For companies with no identifiable promoters, the resolution shall have to be passed by 3/4th majority. Though in this case, there is no specific mention in the Regulation as regards the eligibility of voting by the proposed allottees being a security holder in the issuer, the same should apply here also.

Contents of explanatory statement annexed with the notice of shareholder’s meeting

The proposed use of the issue proceeds shall be mentioned in the explanatory statement sent for the purpose of the shareholders resolution. This requirement is already in existence as the provisions of regulation 163 of ICDR Regulations and Rule 13 of the Companies (Share Capital and Debenture) Rules, 2014 do provide for mandatorily mentioning object for which the preferential issue is being made in the explanatory statement of the notice.

Restriction on use of proceeds

Additionally it’s restricted to use the issue proceeds for the purpose of repayment of loans from promoters/ promoter group/ group companies effectively deterring the companies to raise funds to pay-off its promoters.

Appointment of public financial institution or schedule commercial bank as monitoring agency:

As per the amendments, it shall be mandatory for the issuer company to appoint a monitoring agency whoc shall be responsible to submit report on quarterly basis to the issuer until 95% of the proceeds are utilised in the format as specified in Schedule XI ICDR Regulations. All though there is no requirement of appointing a monitoring agency as per the provisions of chapter V (Preferential Issue) requirement of ICDR Regulations, the concept of the monitoring agency is not new as several chapters of the regulations provide for appointment and functions to be performed by the monitoring agency in case where offer size exceeds a predefined limit. However the considering issue by a financially stressed company there is no monetary limit set for the purpose of appointment of monitoring agency.

Responsibilities of Board of Directors

The board of directors and the management of the issuer shall be required to provide their comments on the findings in the report of monitoring agency and disseminate the same within 45 days of end quarter by publishing it on the website of the company as well as submitting the same with the stock exchange(s) were equity shares of the company are listed.

Responsibilities of Audit Committee

Additionally the audit committee of the issuer is entrusted with responsibility to monitor the utilization of the proceeds. This is nothing new the same already falls under the responsibility of the audit committee as laid in the SEBI (Listing Obligations and Disclosure Requirements), 2015.

Further, the audit committee of the company shall also be required to certify about the meeting of all conditions at the time of dispatch of notice and at the time of allotment.

Responsibilities of statutory auditors

The amendments require the statutory auditor also to certify about the meeting of all conditions at the time of dispatch of notice and at the time of allotment.

Lock in period

The allotment shall be lock-in for a period of 3 years from the date of trading approval.

Amendments to SAST Regulations

On same lines as mentioned in the Consultations Paper, SEBI has vide its amendments under the SAST Regulations inserted regulation 10 (2B) of SAST Regulations thereby granting immunity from open offer obligations to the investors under the preferential issue in compliance with regulation 164A of ICDR Regulations. Irrespective of the fact that equity shares are frequently traded or not.

Conclusion

Considering the stressed status of the company, it is believed that aligning the pricing requirement with that of pricing requirement in case of preferential issue to QIBs, shall effectively increase the pool of investors. Similarly, the proposed exemption from making of an open offer shall lessen the additional burden on an incoming investor to comply with the stringent requirements thereby attracting investors to put in money in such companies.

Accordingly, SEBI’s intention behind the changes may be said to be a welcome move as it will definitely help the financially stressed companies to revive.

Link to our other articles:

SEBI’s proposal to aid financially “stressed” companies: https://vinodkothari.com/2020/04/sebis-proposal-to-aid-financially-stressed-companies/

Prudential Framework for Resolution of Stress Assets: New Dispensation for dealing with NPAs: https://vinodkothari.com/2019/06/fresa/

[1] https://www.sebi.gov.in/reports-and-statistics/reports/apr-2020/consultation-paper-preferential-issue-in-companies-having-stressed-assets_46542.html

[2] http://egazette.nic.in/WriteReadData/2020/220093.pdf

[3] http://egazette.nic.in/WriteReadData/2020/220094.pdf

[4] https://www.sebi.gov.in/legal/circulars/nov-2019/disclosures-by-listed-entities-of-defaults-on-payment-of-interest-repayment-of-principal-amount-on-loans-from-banks-financial-institutions-and-unlisted-debt-securities_45036.html

[5] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11580&Mode=0

RBI amends mode of payment and remittance norms for units of Investment vehicles

Permits FPIs and FVCIs to use Special Non-Resident Rupee (SNRR) account

CS Burhanuddin Dohadwala| Manager, Aanchal Kaur Nagpal| Executive

corplaw@vinodkothari.com

The Reserve Bank of India (‘RBI’) vide notification dated October 17, 2019 had notified the Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt instrument) Regulations, 2019[1] (‘the Regulations’) governing the mode of payment and reporting of non-debt instruments consequent to the Foreign Exchange Management (Non-Debt Instrument) Rules, 2019[2] framed by the Ministry of Finance, Central Government.

RBI has recently vide its notification dated June 15, 2020 notified Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt Instruments) (Amendment) Regulations, 2020[3] amending Reg. 3.1 dealing with Mode of Payment and Remittance of sale proceeds in case of investment in investment vehicles.

Let us discuss few terms to understand the recent amendments to the Regulations.

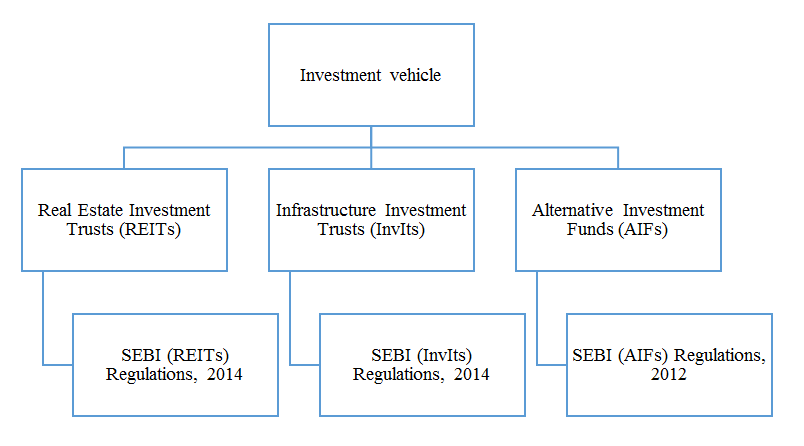

Investment Vehicles under FEMA:

According to FEMA (Non-Debt Instruments) Rules, 2019, investment vehicles mean:

Different types of account available under FEMA (Deposit) Regulations, 2016[1] (‘Deposit Regulations’)

The following are the major accounts that can be opened in India by a non-resident:

| Particulars | Eligible Person |

| Non-Resident (External) Rupee Account Scheme-NRE Account |

Non-resident Indians (NRIs) and Person of Indian Origin (PIOs) |

| Foreign currency (Non-Resident) account (Banks) scheme – FCNR (B) account | |

| Non-Resident ordinary rupee account scheme-NRO account |

Any person resident outside India. |

| Special Non-Resident Rupee Account – SNRR account |

Any person resident outside India. |

A significant advantage of SNRR over NRO is that the former is a repatriable account while the latter is non-repatriable.

What is Special Non-Resident Rupee (‘SNRR’) Account?

Any person resident outside India, having a business interest in India, may open SNRR account with an authorised dealer for the purpose of putting through bona fide transactions in rupees. The business interest, apart from generic business interest, shall include the following INR transactions, namely:-

- Investments made in India in accordance with Foreign Exchange Management (Non-debt Instruments) Rules, 2019 dated October 17, 2019 and Foreign Exchange Management (Debt Instruments)

- Import of goods and services in accordance with Section 5 of the Foreign Exchange Management Act 1999 Regulations, 2019;

- Export of goods and services in accordance with Section 7 of the Foreign Exchange Management Act 1999;

- Trade credit transactions and lending under External Commercial Borrowings (ECB) framework;

- Business related transactions outside International Financial Service Centre (IFSC) by IFSC units at GIFT city like administrative expenses in INR outside IFSC, INR amount from sale of scrap, government incentives in INR, etc;

Rationale behind the amendment:

Position under Master Direction – Foreign Investment in India by RBI

According to Annex 8 of Master Direction – Foreign Investment in India by RBI, investment made by a PROI was permitted with effect from 13th September, 2016. The provisions specify that the amount of consideration of the units of an investment vehicle should be paid out of funds held in NRE or FCNR(B) account maintained in accordance with the Deposit Regulations as one of the modes of payment.

Further it also specifies that the sale/ maturity proceeds of the units may be remitted outside India or credited to the NRE or FCNR(B) account of the person concerned.

Position under the erstwhile provisions of the Regulations

Schedule II of the Regulations (Investments by FPIs) stated earlier that of units of investment vehicles other than domestic mutual fund may be remitted outside India.

However, balances in SNRR account were permitted to be used for making investment only in units of domestic mutual fund and not in Investment Vehicles.

As discussed above, the NRO account is a non-repatriable account while the SNRR account is a repatriable account. Due to the above provisions, investment in Investment Vehicles could not be transferred to the SNRR account for repatriation resulting in ambiguity.

Owing to the above and to increase the inflow of foreign investment, the Government has amended the said provision and allowed FPIs & FVCI to invest in listed or to be listed units of Investment vehicle.

Brief comparison of the pre and post amendment is covered in our Annexure I.

Annexure-I

Comparison of the pre and post amendment

| Schedule | Post amendment | Prior to amendment | Remarks |

| Schedule II w.r.t Investments by Foreign Portfolio Investors | A. Mode of payment

1. The amount of consideration shall be paid as inward remittance from abroad through banking channels or out of funds held in a foreign currency account and/ or a Special Non-Resident Rupee (SNRR) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016.

2. Unless otherwise specified in these regulations or the relevant Schedules, the foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule.

|

A. Mode of payment

1. The amount of consideration shall be paid as inward remittance from abroad through banking channels or out of funds held in a foreign currency account and/ or a Special Non-Resident Rupee (SNRR) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016. Provided balances in SNRR account shall not be used for making investment in units of Investment Vehicles other than the units of domestic mutual fund. 2. The foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule.

|

The erstwhile provisions restricted use of SNRR account balance for making investments in investment vehicles other than mutual funds.

As a result FPIs could not use their SNRR account and had to resort to other types of accounts for investment in investment vehicles such as REITs, and InViTs. The recent amendment has removed this restriction. The amendment has been made to provide for the amendment made in Schedule VIII dealing with Investment by a person resident outside India in an Investment Vehicle. |

| B. Remittance of sale proceeds

The sale proceeds (net of taxes) of equity instruments and units of REITs, InViTs and domestic mutual fund may be remitted outside India or credited to the foreign currency account or a SNRR account of the FPI. |

B. Remittance of sale proceeds

The sale proceeds (net of taxes) of equity instruments and units of domestic mutual fund may be remitted outside India or credited to the foreign currency account or a SNRR account of the FPI. The sale proceeds (net of taxes) of units of investment vehicles other than domestic mutual fund may be remitted outside India. |

To align with the amendment made in Schedule VIII dealing with Investment by a person resident outside India in an Investment Vehicle. | |

| Schedule VII w.r.t Investment by a Foreign Venture Capital Investor (FVCI) | For Para A(2):

Unless otherwise specified in these regulations or the relevant Schedules, the foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule. |

For Para A(2):

The foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule. |

The insertion has been made to align with the amendments proposed in Schedule VIII dealing with Investment by a person resident outside India in an Investment Vehicle. |

| Schedule VIII w.r.t Investment by a person resident outside India in an Investment Vehicle | A. Mode of payment:

The amount of consideration shall be paid as inward remittance from abroad through banking channels or by way of swap of shares of a Special Purpose Vehicle or out of funds held in NRE or FCNR(B) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016. Further, for an FPI or FVCI, amount of consideration may be paid out of their SNRR account for trading in units of Investment Vehicle listed or to be listed (primary issuance) on the stock exchanges in India. |

A. Mode of payment:

The amount of consideration shall be paid as inward remittance from abroad through banking channels or by way of swap of shares of a Special Purpose Vehicle or out of funds held in NRE or FCNR(B) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016. |

Further, it is clarified that the SNRR account may be used for trading in units of listed as well as to be listed units of investment vehicles and the sale/ maturity proceeds can be credited to the said account. |

| B. Remittance of Sale/maturity proceeds:

The sale/ maturity proceeds (net of taxes) of the units may be remitted outside India or may be credited to the NRE or FCNR(B) or SNRR account, as applicable of the person concerned. |

B. Remittance of sale/maturity proceeds

The sale/maturity proceeds (net of taxes) of the units may be remitted outside India or may be credited to the NRE or FCNR(B) account of the person concerned. |

Link to our other articles:

Introduction to FEMA (NDI) Rules, 2019 and recent amendments:

https://vinodkothari.com/2020/04/introduction-to-fema-ndi-rules-2019-and-recent-amendments/

RBI rationalises operation of Special Non-Resident Rupee A/c:

https://vinodkothari.com/wp-content/uploads/2019/11/RBI-rationalises-operation-of-SNRR-Account.pdf

[1] https://vinodkothari.com/wp-content/uploads/2019/11/RBI-rationalises-operation-of-SNRR-Account.pdf

[1] http://egazette.nic.in/WriteReadData/2019/213318.pdf

Extension of FPC on lending through digital platforms

A new requirement or reiteration by the RBI?

– Anita Baid (finserv@vinodkothari.com)

Ever since its evolution, the basic need for fintech entities has been the use of electronic platforms for entering into financial transactions. The financial sector has already witnessed a shift from transactions involving huge amount of paper-work to paperless transactions[1]. With the digitalization of transactions, the need for service providers has also seen a rise. There is a need for various kinds of service providers at different stages including sourcing, customer identification, disbursal of loan, servicing and maintenance of customer data. Usually the services are being provided by a single platform entity enabling them to execute the entire transaction digitally on the platform or application, without requiring any physical interaction between the parties to the transaction.

The digital application/platform based lending model in India works as a partnership between a tech platform entity and an NBFC. The technology platform entity or fintech entity manages the working of the application or website through the use of advanced technology to undertake credit appraisals, while the financial entity, such as a bank or NBFC, assumes the credit risk on its balance sheet by lending to the customers who use the digital platform[2].

In recent times many digital platforms have emerged in the financial sector who are being engaged by banks and NBFCs to provide loans to their customers. Most of these platforms are not registered as P2P lending platform since they assist only banks, NBFCs and other regulated AIFIs to identify borrowers[3]. Accordingly, electronic platforms serving as Direct Service Agents (DSA)/ Business Correspondents for banks and/or NBFCs fall outside the purview of the NBFC-P2P Directions. Banks and NBFCs have th following options to lend-

- By direct physical interface or

- Through their own digital platforms or

- Through a digital lending platform under an outsourcing arrangement.

The digitalization of credit intermediation process though is beneficial for both borrowers as well as lenders however, concerns were raised due to non-transparency of transactions and violation of extant guidelines on outsourcing of financial services and Fair Practices Code[4]. The RBI has also been receiving several complaints against the lending platforms which primarily relate to exorbitant interest rates, non-transparent methods to calculate interest, harsh recovery measures, unauthorised use of personal data and bad behavior. The existing outsourcing guidelines issued by RBI for banks and NBFCs clearly state that the outsourcing of any activity by NBFC does not diminish its obligations, and those of its Board and senior management, who have the ultimate responsibility for the outsourced activity. Considering the same, the RBI has again emphasized on the need to comply with the regulatory instructions on outsourcing, FPC and IT services[5].

We have discussed the instructions laid down by RBI and the implications herein below-

Disclosure of platform as agent

The RBI requires banks and NBFCs to disclose the names of digital lending platforms engaged as agents on their respective website. This is to ensure that the customers are aware that the lender may approach them through these lending platforms or the customer may approach the lender through them.

However, there are arrangements wherein the platform is not appointed as an agent as such. This is quite common in case of e-commerce website who provide an option to the borrower at the time of check out to avail funding from the listed banks or NBFCs. This may actually not be regarded as outsourcing per se since once the customer selects the option to avail finance through a particular financial entity, they are redirected to the website or application of the respective lender. The e-commerce platform is not involved in the entire process of the financial transaction between the borrower and the lender. In our view, such an arrangement may not be required to be disclosed as an agent of the lender.

Disclosure of lender’s name

Just like the lender is required to disclose the name of the agent, the agent should also disclose the name of the actual lender. RBI has directed the digital lending platforms engaged as agents to disclose upfront to the customer, the name of the bank or NBFC on whose behalf they are interacting with them.

Several fintech platforms are involved in balance sheet lending. Here, the lending happens from the balance sheet of the lender however, the fintech entity is the one assuming the risk associated with the transaction. Lender’s money is used to lend to customers which shows up as an asset on the balance sheet of the lending entity. However, the borrower may not be aware about who the actual lender is and sees the platform as the interface for providing the facility.

Considering the risk of incomplete disclosure of facts the RBI mandates the disclosure of the lender’s name to the borrower. In this regard, the loan agreement or the GTC must clearly specify the name of the actual lender and in case of multiple lender, the name along with the loan proportion must be specified.

Issuance of sanction letter

Another requirement prescribed by the RBI is that immediately after sanction but before execution of the loan agreement, a sanction letter should be issued to the borrower on the letter head of the bank/ NBFC concerned.

Issue a sanction letter to the borrower on the letterhead of the NBFC may seem illogical since the lending happens on the online platform. The sanction letter may be shared either through email or vide an in-app notification or otherwise. Such sanction letter shall be issued on the platform itself immediately after sanction but before execution of the loan agreement.

Further, the FPC requires lender NBFCs to display annualised interest rates in all their communications with the borrowers. However, most of the NBFCs show monthly interest rates in the name of their ‘marketing strategy’. This practice though have not been highlighted by the RBI must be taken seriously.

Sharing of loan agreement

The FPC laid down by RBI requires that a copy of the loan agreement along with a copy each of all enclosures quoted in the loan agreement must be furnished to all borrowers at the time of sanction/ disbursement of loans. However, in case of lending done over electronic platforms there is no physical loan agreement that is executed.

Given that e-agreements are generally held as valid and enforceable in the courts, there is no such insistence on execution of physical agreements. The electronic execution versions are more feasible in terms of cost and time involved. In fact in most of the cases, the loan agreements are mere General Terms and Conditions (GTC) in the form of click wrap agreements.

Usually, the terms and conditions of the loan or the GTC is displayed on the platform wherein the acceptance of the borrower is recorded. In such a circumstance, necessary arrangements should be made for the borrower to peruse the loan agreement at any time. The loan agreement may also be in the form of a mail containing detailed terms and conditions, along with an option for the borrower to accept the same.

The requirement from compliance perspective is to ensure that the borrower has access to the executed loan agreement and all the terms and conditions pertaining to the loan are captured therein.

Monitoring by the lender

Effective oversight and monitoring should be ensured over the digital lending platforms engaged by the banks/ NBFCs. As RBI does not regulate the platform entities, hence the only way to regulate the transaction is though the lenders behind these platforms.

The outsourcing guidelines require the retention of ultimate control of the outsourced activity with the lender. Further, the platform should not impede or interfere with the ability of the NBFC to effectively oversee and manage its activities nor shall it impede the RBI in carrying out its supervisory functions and objectives. These should be captured in the servicing agreement as well as be implemented practically.

Grievance Redressal Mechanism (GRM)

Much of the new-age lending is enabled by automated lending platforms of fintech companies. The fintech company is the sourcing partner, and the NBFC is the funding partner. However, the grievance of the customer may range from issue with the usage of platform to the non-disclosure of the terms of loan.

A challenge that may arise is to segregate the grievance on the basis of who is responsible for the same- the platform or the lender. There must be proper mechanism to ensure such segregation and adequate efforts shall be made towards creation of awareness about the grievance redressal mechanism.

[1] Read our detailed write up here- https://vinodkothari.com/2020/03/moving-to-contactless-lending/

[2] Read our detailed write up here- https://vinodkothari.com/2020/03/fintech-regulatory-responses-to-finnovation/

[3] RBI’s FAQs on P2P lending platform- https://www.rbi.org.in/Scripts/FAQView.aspx?Id=124

[4] Read our detailed write up here- https://vinodkothari.com/2019/09/the-cult-of-easy-borrowing/

[5] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11920&Mode=0

Fifty years of global securitisation – list of chapters

List of chapters for the anthology on fifty years of global securitisation –

Go back to fifty years of securitisation page.

Limits on creeping acquisition by promoters increased during COVID-19 crises

Shaifali Sharma | Vinod Kothari and Company

Introduction

SEBI has been taking several proactive measures to relax fund raising norms and thereby making it easier for companies to raise capital amid the COVID-19 pandemic. With a view to further facilitate fund raising by the companies, SEBI vide its notification dated June 16, 2020[1], has relaxed the obligation for making open offer for creeping acquisition under Regulation 3(2) of the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (Takeover Code).

The relaxation allows creeping acquisition upto 10% instead of the existing 5%, for acquisition by promoters of a listed company for the financial year 2020-21. The relaxation is specific and limited to acquisition by way of a preferential issue of equity shares and therefore excludes acquisitions through transfers, block and bulk deals etc. Also recently, SEBI in its Board Meeting[2] held on June 25, 2020 has proposed to provide an additional option to the existing pricing methodology for preferential issue under which the minimum price for allotment of shares will be volume weighted average of weekly highs and low for twelve weeks or two weeks, whichever is higher.However, this new rule shall apply till December 31, 2020 with 3 years lock-in condition for allotted shares. Further, by way of the same notification, SEBI has also relaxed the provisions of voluntary open offer where an acquirer together with PAC will be eligible to make voluntary offer irrespective of any acquisition in the previous 52 weeks from the date of voluntary offer, this will promote investments into various companies in future.

This article tries to discuss on whether the relaxation given by SEBI to the promoters are as encouraging as it seems to be, when connected with the pricing norms for preferential issue under the SEBI (Issue of Capital and Disclosures Requirement) Regulations, 2018 (‘ICDR Regulations’) and how the new pricing methodology proposed by SEBI can leverage the situation.

What is Creeping Acquisition?

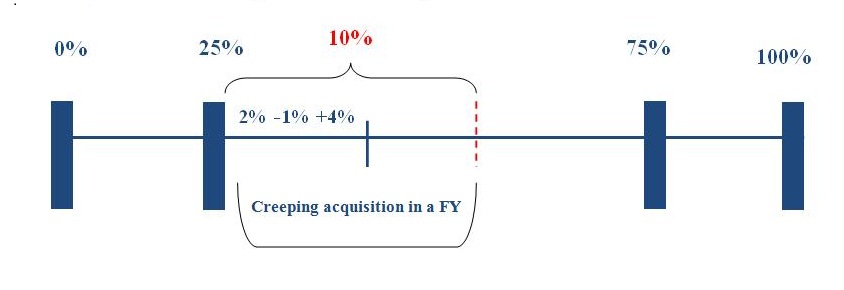

Creeping acquisition, governed by Regulation 3(2) of the Takeover Code, refers to the process through which the acquirer together with PAC holding more than 25% but less than 75%, to gradually increase their stake in the target company by buying up to 5% of the voting rights of the company in one financial year. Any acquisition of further shares or voting rights beyond 5% shall require the acquirer to make an open offer. Further, for the purpose of creeping acquisition, SEBI considers gross acquisitions only notwithstanding any intermittent fall. The same is projected in Figure 1 below. Also, in all cases, the increase in shareholding or voting rights is permitted only till the 75% non-public shareholding limit.

Figure 1: Creeping acquisition limit increased from 5% to 10%

Rationale for easing the norms of Creeping Acquisition

While the companies are currently struggling to manage their cash flows due to the financial challenges faced on account of COVID-19, the amendment will allow companies to raise funds from promoters to tide over their difficulties for the financial year 2020-21. This revision will also boost the sagging stock market and help sustain the stock prices of the company.

Promoters, on the other hand, owning 25% or more of the shares or voting rights in a company will be able to increase their shareholdings up to 10% in a year versus the previously allowed threshold limit of 5%.

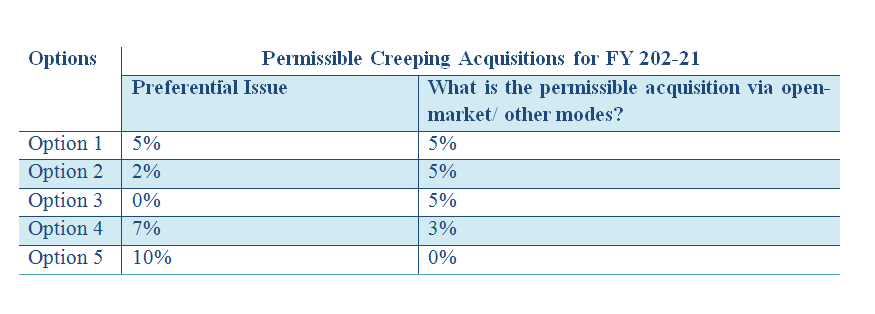

Permutations and Combinations of Creeping Acquisition during FY 2020-21

Since the enhanced 10% limit applies only in case of acquisition under preferential issue, the total acquisition of 10% may be achieved by any of the following combinations:

Option 1: Acquire upto 5% shares via open-market purchase or any other form and the remaining 5% shares can be acquired through subscribing to a preferential issue.

Option 2:Acquire 10% shares through preferential issue

Accordingly, in a block of 12 months of financial year 2020-21, if the promoterwants to acquire share through open market, bulk deals, block deals or in any other form, the 5% threshold shall remain in force and additional 5% can be acquired through preferential issue.

Identified below are the permitted acquisitions through open market, transfers or other forms in case promoter opts for preferential issue:

Whether the relaxation in open offer is actually encouraging when read with the pricing norms under ICDR Regulations?

As stated above, the relaxation can be availed only in the cases where the investments are done undera preferential issue. Regulation 164 of the SEBI (Issue of Capital and Disclosures Requirement) Regulations, 2018 (‘ICDR Regulations’) deals with the pricing norms under preferential issue. It provides that the issue price in cases where the shares have been listed for more than 26 weeks on a recognized stock exchange as on the relevant date, the issue price has to be higher of the following:

- the average of the weekly high and low of the volume weighted average price of the related equity shares quoted on the recognized stock exchange during the twenty six weeks preceding the relevant date; or

- the average of the weekly high and low of the volume weighted average prices of the related equity shares quoted on a recognized stock exchange during the two weeks preceding the relevant date.

The computation of the prices as per the above stated regulation will lead to a wide gap between the pricing at the beginning of the twenty-six week period and the current price when the company raises funds.

During this time of stock market crises, the stock prices of many companies have dropped sharply from their respective all-time high values recorded 6 months back. Further, in the cases where the market price is lower than the minimum price calculated as per ICDR Regulations for preferential issue, the promoters will be discouraged to acquire shares under preferential allotment as they will end up paying higher values.

Due to the challenges faced by the economy in view of COVID-19, the trading prices of the listed companies have gone down sharply. Accordingly, the price determined under ICDR Regulations may not be a motivating factor for the promoters to subscribe to the additional shares though, elimination of the costs involved in a public offer may compensate the same.

However, to curb the above situation, SEBI in its Board meeting held on June 25, 2020, has proposed an additional option to the existing pricing methodology for preferential issuance as under:

In case of frequently traded shares, the price of the equity shares to be allotted pursuant to the preferential issue shall be not less than higher of the following:

- the average of the weekly high and low of the volume weighted average price of the related equity shares quoted on the recognized stock exchange during the twelve weeks preceding the relevant date; or

- the average of the weekly high and low of the volume weighted average prices of the related equity shares quoted on a recognized stock exchange during the two weeks preceding the relevant date.

The new option will consider the weighted average price of equity shares preceding 12 weeks instead of the preceding 26 weeks and therefore reflect the accurate price during the pandemic period. This may prove to be the solution to above crises,making fundraising through preferential issue easier for the corporates and simultaneously encouraging the promoters as well to infuse funds.

Compliances for preferential issue to promoters under PIT Regulations

Considering the fact that promoter is one of the designated person as per the SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’), the companies, in addition to the procedural requirements for preferential issue prescribed under the Companies Act, 2013, ICDR Regulations and other applicable laws, shall also comply with the provisions of PIT Regulations.

Closure of trading window in case of preferential allotment

Designated persons and their immediate relatives shall not trade in securities when the trading window is closed. The trading restriction period shall apply from the end of every quarter till 48 hours after the declaration of financial results.

Further, the trading window shall also be closed when the compliance officer determines that a designated person (DP) or class of designated persons can reasonably be expected to have possession of unpublished price sensitive information (UPSI). Therefore, the trading window shall be closed and communicated to all DPs as soon as the date/notice of board meeting to approve issue of share via preferential allotment is finalized upto 2nd trading day after communication of the decision of the Board to the Stock Exchanges.

Accordingly, promoter/ class of promoters acquiring shares under preferential issue shall conduct all their dealings in the securities of the company only in a valid trading window i.e. once the trading widow is open subject to the pre-clearance norms prescribed under PIT Regulations and the Code of Conduct for prevention of insider trading of the Company.

Concluding Remarks

Given the lack of liquidity in the market, the proposed amendments maybe seen as an opportunity for target companies to raise capital from its promoters. Further, promoters can also infuse funds through equity issuance and will be able to increase their shareholding in the target company without the formalities of making the open offer.

Having said that since the market might take some time to recover, this relaxation provides a gateway for promoters to avoid open offer requirements which would otherwise have involved compliance burden on the promoter. However, the pricing factor may seem to be the only hindrance or a demotivation for actually availing this relaxation which seems to be resolved through the new pricing method proposed by SEBI in its Board meeting.

[1]To view the notification, click here

[2]https://www.sebi.gov.in/media/press-releases/jun-2020/sebi-board-meeting_46929.html

Other reading materials on the similar topic:

- ‘SEBI revisits Takeover Code’ can be viewed here

- ‘Takeover Code 2011’ can be viewed here

- ‘Decoding Takeover Code’ can be viewed here

- Our other articles on various topics can be read at: https://vinodkothari.com/

Email id for further queries: corplaw@vinodkothari.com

Our website: www.vinodkothari.com

Our Youtube Channel: https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

Fifty years of global securitization

– Vinod Kothari

Some people love it; some love to hate it, and some just live it. No matter which one of the clubs one belongs to, but there is no doubt that securitization is a major financial phenomenon.

Year 2020 marks 50 years of the inaugural mortgage-backed pass-through transaction done in 1970 by Ginnie Mae. Securitization has turned fifty.

The world is not in exactly right environment to do either a champagne party or otherwise – however, one should not gloss over the massive change that securitization has made, to the financial landscape of the world, over these five decades. Irrespective of the jury verdict on whether it was responsible for the Global Financial Crisis, the fact is that it had such a major impact that its short-lived absence from the scene could put world’s financial system into doldrums. And now, there are regulators’ reports looking at this very instrument with optimism to lead the recovery out of the COVID disruption.

To commemorate 50 years of securitization, we propose to bring an anthology of write-ups by senior securitization professionals, particularly those who have seen its boom and bust. The write-ups may be along the following lines:

- Historical write-ups, recounting the development of early MBS by the agencies, the way it was perceived then and major economists’ remarks about this instrument

- Contribution of securitization to mortgage markets globally, particularly in mortgage availability and affordability

- Contribution of securitization to financial inclusion, making smaller and community lenders reach out to capital markets through larger intermediaries

- Securitization and emerging markets

- Lessons learnt from the GFC and how regulatory systems have evolved thereafter

- Legal robustness of securitization – has it proved itself over decades of crises?

- Off-balance securitization – development of accounting standards over the years, and does off-balance sheet securitization have any relevance left?

- Significant risk transfers and capital relief

- Market reports from major countries.

List of Chapters

For a work-in-progress list of Chapters, see here.

Publication details

The anthology is proposed to be a compilation in e-book form. We will be in touch with some publishers to seek interest in publication.

Structure of the Chapters

The anthology will be collaborative effort of several leading authors, experts, researchers and practitioners from all over the world. Each of the contributors are leading luminaries in their own field. So while substantial discretion will be used by the contributors, some pointers for contributors are as follows:

- This e-book will hopefully have a very long shelf-life. Hence, the stance of the write-ups is not contemporaneous state of the market. Rather, the write-ups trace developments over time, to identify trends. The contributors deploy their wisdom to think of the trends that will continue, wither away, or strengthen. The commemorative is all about continuity and change.

- We are wanting to minimise current market data or statistics, for reasons discussed above.

- Each of the write-ups may provide a larger, macro view before narrowing down on micro aspects.

- One of our very important objectives is to have the contribution of securitization to development of financial markets, financial inclusion, stability and robustness of systems, etc. It is not merely a historical account, but an important document on lessons to be learnt, and to provide a place from where one may look at the decades to come.

- For scholars/practitioners who have been watching the industry grow over the years, if there are details of one’s personal association with the industry – as to how it developed and changed over time – that may of interest to readers. This may be added with generalisation of the market.

Invitation for contributions

Needless to say, it is a massive project – it has to be collaborative. We need the support of scholars, authors, stakeholders – those who have been practising, teaching, consulting or regulating securitization over the years. Hence, if you are one such contributor, or you know one who may be such a contributor, your contribution/assistance is most welcome.

For interest in contribution to the anthology, please do write to timothy@vinodkothari.com. Please indicate your background, proposed contents, length of the article, etc. After hearing from us positively, you may start writing your article, for submissions by end of August, 2020.

Sponsoring/advertising opportunities

From our side, this project is completely non-pecuniary. We just felt that we can steer this effort which may be valuable for a long time.

However, this project will involve massive research effort, editing, and production. Hence, there may be substantial expense.

If you want to sponsor in any manner, or want to put up a befitting advertisement about your company/products, the same is welcome. Please feel free to discuss with finserv@vinodkothari.com.

Timeline for publication

Tentatively, we may put the e-publication in public domain by November, 2020.