Archive for year: 2020

Recent Trends in Crypto-Industry: India & Abroad

-Megha Mittal

“Opportunity amidst tragedy” would likely be the most suitable phrase to summarise the journey of cryptos during the Global Pandemic- with disruption taking a toll on people and economies, and physical proximities massively restrictred, cryptos have outshone traditional assets, by virtue of its inherent features- easy liquidity, access and digitalisation.

Further, as countries around the globe attempt to stimulate their economies by opening floodgates of liquid funds, the ‘digital natives’ have and are expected to increasingly venture into adventure-some investments- think, cryptos. And while such adventurous investing may be short-lived, the results may infact have a long-lasting impact- it is this expected impact that has sets the ‘bull’ stage for cryptos in times to come.

In this brief note, we cover the recent highlights and developments in the crypto-industry, also discussing developments in the relatively new concepts of stablecoins, crypto-lending.

Udyam Portal: The pristine MSME Registration Process

-Qasim Saif (finserv@vinodkothari.com)

The Indian government has been taking a number of measures to tackle the disruptions caused by the pandemic, giving special focus on small businesses. The small and medium size businesses form the backbone of any economy, specially developing economies like India, hence, the Micro, Small and Medium Enterprises (MSME) are seen as a key player in promoting momentum in economy once movement restrictions and social distancing norms are lifted. In order to stimulate the post-Covid economic scenarios, it is crucial to focus on the growth and development of the MSME sector.

The definition of MSME comes from section 7 of the Micro, Small and Medium Enterprises Development Act, 2006 (‘Act’) . Based on the proposal of the Finance Minister, he Ministry of Micro, Small and Medium Enterprises on 1st June 2020 via notification, amended the definition of MSME in order to increase the scope and hence bringing larger number of firms within the ambit of MSME. As per the revised definition, the classification is based on the investment and turnover of the entity.

The latest definition of MSME as per the notification is as follows-

| Revised Classification applicable w.e.f 1st July 2020 | |||

| Composite Criteria: Investment in Plant & Machinery/equipment and Annual Turnover | |||

| Classification | Micro | Small | Medium |

| Manufacturing Enterprises and Enterprises rendering Services | Investment in Plant and Machinery or Equipment: Not more than Rs.1 crore and Annual Turnover; not more than Rs. 5 crores |

Investment in Plant and Machinery or Equipment: Not more than Rs.10 crore and Annual Turnover; not more than Rs. 50 crores |

Investment in Plant and Machinery or Equipment: Not more than Rs.50 crore and Annual Turnover; not more than Rs. 250 crores |

The aforesaid definition removes the bifurcation of investment limits for Manufacturing and Service industry which were previously existent. Hence, it is expected that large number of service providers would be covered as they tend to have lesser investment in plant and machinery or equipment and turnover as compared to Manufacturing entity with similar profits.

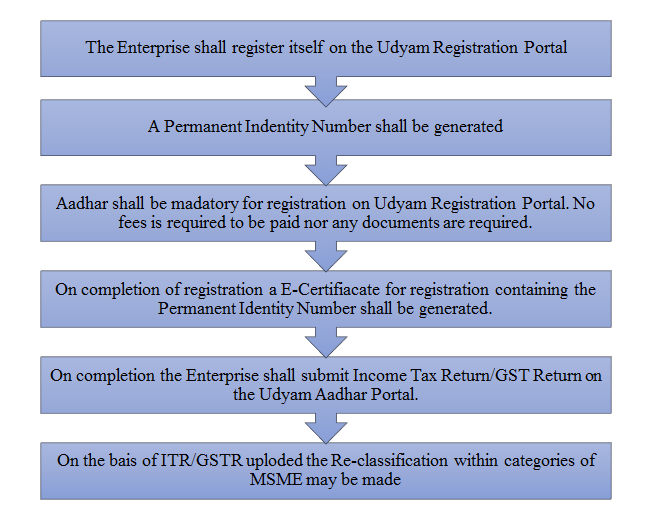

As the changes in classification are to be applicable from 1st July 2020, the Ministry of Micro, Small and Medium Enterprises have come up with a Notification dated 26-06-2020 which provide for a novel method of registration for MSME (‘Udyam Registration’).

The said notification provides for process for registration of MSME which shall become applicable from 1st July 2020, the requirement of Udyam Registration shall also be applicable on existing MSME’s.

Pursuant to the amendment in the definition of MSME and the introduction of procedure for filing the memorandum under the Udyam Registration, it seems that registration as an MSME shall be a necessity and accordingly be considered as a pre-requisite for availing benefit under the various schemes introduced by the Ministry.

The Process of Registration

Registration on the basis of self-declaration

As per the Udyam Registration requirement it is evident that Udyam Registration can be done on the basis of filing a self-declaration. The relevant extract of the notification states as follows-

“Any person who intends to establish a micro, small or medium enterprise may file Udyam Registration online in the Udyam Registration portal, based on self-declaration with no requirement to upload documents, papers, certificates or proof.”

On review of the registration process on the Udyam Registration portal, it is been observed that the list of major activities contains a specific head for trading activities, land transport as well as an option for selecting ‘Others’. Thus, it may be concluded that trading, transportation and such other activities are included under activities of a service enterprise and shall be required to be registered as an MSME on the Udyam Registration portal.

Requirement of Aadhar

The Aadhaar of following persons shall be required for registration as an MSME.

| Type of Entity | Aadhar of |

| Proprietorship Firm | Proprietor |

| Partnership Firm | Managing Partner |

| HUF | Karta |

| Company / LLP / Co-operatives / Trust / Organisations* | Authorised Signatory |

*PAN and GSTIN of enterprise shall also be required

Non-Availability of Aadhar

In case the person does not have Aadhar, he/she can approach MSME-Development Institutes or District Industries Centres (Single Window Systems) with his Aadhaar enrolment identity slip or copy of Aadhaar enrolment request or bank photo pass book or voter identity card or passport or driving licence and the Single Window Systems will facilitate the process including getting an Aadhaar number and thereafter in the further process of Udyam Registration

Calculation of Investment in Plant, Machinery and Equipment, and Annual Turnover

In order to determine whether the enterprise falls within the limits of MSME and under which category Calculation of amount for Investment in Plant, Machinery and Equipment, and Annual Turnover is required to be calculated.

Plant, Machinery and Equipment.

The Plant, Machinery and Equipment shall have same meaning as under Income Tax Rules, 1962 hence not include land, building and furniture and fittings. Further it shall not include items mentioned in Explanation 1 to Section 7(1) of MSME Act 2006 shall be excluded.

All units with Goods and Services Tax Identification Number (GSTIN) listed against the same Permanent Account Number (PAN) shall be collectively treated as one enterprise and investment figures for all of such entities shall be seen together and only the aggregate values will be considered for deciding the category as micro, small or medium enterprise.

The calculation of investment in plant and machinery or equipment will be linked to the Income Tax Return (ITR) of the previous years. In case of a new enterprise, where no prior ITR is available, the investment will be based on self-declaration of the promoter of the enterprise and such relaxation shall end after the 31st March of the financial year in which it files its first ITR.

However, it shall be noted that in case of new enterprise without any ITR, where calculation is made on self-declaration basis, the purchase (invoice) value of a plant and machinery or equipment, whether purchased first hand or second hand, shall be taken into account excluding Goods and Services Tax (GST).

Turnover

On the similar grounds as investment the turnover shall also be calculated on collective basis for all units with Goods and Services Tax Identification Number (GSTIN) listed against the same Permanent Account Number (PAN) and all such units shall be treated as one enterprise and turnover figures for all of such entities shall be seen together and only the aggregate values will be considered for deciding the category as micro, small or medium enterprise.

Further it shall be noted that the Exports of goods or services or both, shall be excluded while calculating the turnover of any enterprise.

Information as regards turnover and exports turnover for an enterprise shall be linked to the Income Tax Act or the Central Goods and Services Act and the GSTIN. The figures of enterprise which do not have PAN will be considered on self-declaration basis for a period up to 31st March, 2021 and thereafter, PAN and GSTIN shall be mandatory.

Registration by existing MSMEs

In case of existing MSMEs, the registration shall be valid till March 2021. They are required to register themselves under the Udyam Registration portal before the expiry of their registration under Udyog Aadhaar or EM-II.

Updation of information

The registration as an MSME may be obtained based on a self-declaration by the applicant, without submitting any other documents, certificates or proofs of investment in plant and machinery or equipment or turnover. However, once the URM is granted, the MSME is required to update details on the portal, including details of the ITR and the GST Return for the previous financial year and such other additional information as may be required, on self-declaration basis.

Failure to update the relevant information within the period specified [to be specified] in the online Udyam Registration portal will render the enterprise liable for suspension of its status.

Changes in classification

On the basis of information furnished and updated from time to time as well as information from Government sources including ITR/GSTR the classification of enterprise may be changed to a lower to higher category (graduation) or from higher to lower category (reverse-graduation).

In case of graduation an enterprise will maintain its prevailing status till expiry of one year from the close of the year of registration. In case of reverse-graduation of an enterprise, the enterprise will continue in its present category till the closure of the financial year and it will be given the benefit of the changed status only with effect from 1st April of the financial year following the year in which change happened.

Accordingly, it can be inferred that the limits of investment and turnover shall be reckoned on the basis of the ITR and GST returns filed for the previous financial year.

Grievance redressal

The Champions Control Rooms functioning in various institutions and offices of the MSME-Development Institutes along with District Industries Centres in their respective districts shall act as Single Window Systems for facilitating the registration process and further handholding the micro, small and medium enterprises in all possible manner.

In case of any discrepancy or complaint, the General Manager of the District Industries Centre shall undertake an enquiry for verification of the details of Udyam Registration and thereafter forward the matter to the Director or Commissioner or Industry Secretary concerned of the State Government who after giving an opportunity to present its case and based on the findings, may amend the details or recommend to the Ministry of MSME’s, Government of India, for cancellation of the Udyam Registration Certificate.

Further it shall be noted that, if provision for registration under MSME Act, 2006, is violated Section 27 of the Act, provides for a fine which may extend upto one thousand rupees for first conviction and a fine ranging from one thousand to ten thousand rupees for second and subsequent conviction.

Conclusion

The new process provides an easy, quick and simple method for registration that will be linked to information submitted under Income Tax and GST, hence being user friendly as well as keeping a check on reliability of information. The move is intending to promote ease of doing business in lieu of the introduction of Atmanirbhar Bharat scheme.

This process and amended definition would help more MSME to take benefit of government schemes for MSME hence providing them an elevated pedestal to provide a push to kick-start economy after the covid restrictions are lifted.

Our other relevant articles may be referred here:

Partitioning of advisory services from distribution activities

– Harshil Matalia (finserv@vinodkothari.com)

Updated as on July 04, 2020

The Securities and Exchange Board of India (SEBI) had notified SEBI (Investment Advisers) Regulations, 2013 (IA Regulations)[1] in 2013, to regulate activities of Investment Adviser (IA). IA is a person who provides investment advices with respect to financial and investment products to its clients for a consideration. Regulation 3 (1) of the IA Regulations mandates every person which acts as an IA or holds itself out as an IA to register itself unless the person is exempted from registration under regulation 4 of IA Regulations.

A series of consultation papers were issued in 2016, 2017 and 2018, which was followed by another consultation paper[2] proposing amendments in the IA regulations released by SEBI on January 15, 2020. Subsequently, SEBI in its meeting held on February 17, 2020[3] approved the proposals on regulatory changes based on comments received on consultation paper. On July 03, 2020, SEBI has amended IA regulations by introducing SEBI (IA)(Amendment) Regulations, 2020[4] (Amendment Regulations) which shall come into force on September 30, 2020. The main objective to bring such regulatory amendments is to protect the interest of investors and prioritize investors’ interest over the interest of IA.

This write-up provides a brief note on amendments brought by SEBI and its implications on the sector.

Segregation of Advisory & Distribution Activities

As per regulation 15(5) of the IA Regulations, there is an obligation on IA to disclose all conflicts of interest that arises while serving its clients. There is a possibility that IA would advise to invest in products which shall fetch maximum commission or products that may be risky and less sellable in the market. To overcome such a situation, IA must disclose potential conflict of interest to the client.

An IA may be engaged in activities other than investment advisory and hence it is necessary to ensure an arms-length relationship between its activities as an IA and other activities as prescribed under regulation 15(3). Individuals registered as IAs are not allowed to provide distribution or execution services under amended IA Regulations. However, corporate entities registered as IAs can offer execution or distribution services provided that the investment advisory services are offered through separate identifiable division or department.

Further as per recent amendments in Regulation 22 of IA Regulations, “family of IA” shall not provide distribution services to the same client advised by IA. SEBI has inserted a definition of ‘Family of IA’ which shall include individual IA, spouse, children and parents. SEBI has also prescribed the requirement for non-individual IAs to have client level segregation at a group level which means that client can either take advisory or distribution services from the IA and the same client cannot avail any other service, as the case may be, by the same IA or its group entities. Group for this purpose shall mean:

- For Company- an entity which is a holding, subsidiary, fellow subsidiary, associate or an investing company or venturer of the company as per the provisions of Companies Act, 2013 or;

- In any other case- an entity which has controlling interest or which is subject to controlling interest of a non-individual investment adviser.

Implementation of Advice (Execution)

IAs also offer implementation services to its clients i.e. execution of advice provided to the client by charging some reasonable consideration. Thus, the client finds ‘all in one shop’ by availing such services. It has been suggested that IA should clearly declare to the client that it will not seek any power of attorney or authorisations from its clients for auto implementation of investment advice. However, SEBI in Amendment Regulations emphasis that whether to avail implementation services would be sole choice of client and the IA cannot force its client to avail implementation services. Further, IA shall provide implementation services to its advisory clients only through direct schemes/products in the securities market. IA or group or family of IA shall not charge directly or indirectly any consideration including commission or referral fees for providing implementation services. SEBI has also mandated IAs to provide declaration that no consideration shall be received by IA for implementation of advice or execution services. The said declaration has been inserted under item 5 of the First schedule of IA Regulations.

Terms and Conditions of Investment Advisory Services

As per regulation 19, an IA shall maintain copy of agreement with the client, if any, along with other records specified under the said regulation. Since the requirement of advisory agreement is not mandatory under the erstwhile IA Regulations, most of the clients always remain unaware about the terms and conditions of the advisory services that they are going to obtain from IAs.

SEBI has been receiving numerous investor complaints against IAs that they charge exorbitant advisory fees, promising false returns, non-disclosure of detailed fees structure etc. In absence of written agreement between adviser and client, client may not be able to prove his claim.

Therefore, SEBI has mandated an execution of agreement between IA and client which shall specify key terms and conditions, as may be prescribed by SEBI, regarding investment advisory services and this would in turn facilitate transparency.

Advisory Fees

As per the Code of Conduct for IAs prescribed under third schedule of IA Regulations, IAs shall charge fair and reasonable fees to the clients in lieu of providing advisory services. There have been several complaints received by SEBI regarding unreasonable fees being charged by IAs. To restrain such instances and unfair practices, SEBI has inserted Regulation 15A regarding advisory fees that can be charged by IAs to its clients.

The discussion paper has provided two modes of charging fees to clients. IAs can either charge fees by opting Assets under Advice (AUA) mechanism or they can charge fixed fees. SEBI inserted the definition of AUA in Regulation 2(aa) of IA Regulations which shall mean aggregate net asset value of securities and investment products for which IA has rendered investment advice irrespective of whether the implementation services are provided by investment adviser or concluded by the client directly or through other service providers. Under AUA mechanism, fees shall be charged on the basis of underlying assets under advice subject to maximum 2.5 percent of AUA per annum per family across all schemes/ products/ services provided. On other hand, as per fixed fees terms, IA can charge maximum Rs. 75,000 p.a. per family across all schemes/ products/ services provided. The option of choosing mode for charging fees is available with IA, however, change of mode can be effected only after 12 months of on boarding/last change of mode.

In practice, it would be difficult to implement maximum ceiling limit proposed by SEBI. There are certain portfolios that contain high risk products which requires effective skills and essential time to provide any investment advice. In such cases, maximum ceiling would be discouraging for IAs to charge a particular fees to compensate for their efforts. Therefore, in Board memorandum, SEBI has proposed to reconsider and enhance fixed fees from Rs. 75,000 to Rs. 1,25,000 p.a. per ‘family of client’ and fees under AUA mechanism shall be 2.5 percent of AUA per annum per ‘family of client’ across all schemes/ products/ services offered by IA. SEBI inserted a definition of ‘Family of client’ which constitutes individual, dependent spouse, dependent children and dependent parents. IAs would also be required to mention detailed fees structure along with adequate calculations under terms and conditions of advisory agreement. The above-mentioned proposed fees structure is not yet finalised; and is expected to be specified by the SEBI at the earliest. Also, SEBI is expected to bring more clarity that whether IA can charge fees using different fees structure to different categories of customers.

Eligibility Criteria for IAs

The eligibility criteria for IA includes qualification and net worth requirement. Under the erstwhile IA Regulations, regulation 7 and 8 deals with the qualification and net worth requirements respectively. IAs or a principal officer of non-individual IAs shall have minimum qualification as prescribed under the regulation 7.

SEBI has amended the qualification and net worth requirement. SEBI has introduced the definition of “persons associated with investment advice” and “principal officer” in Amendment Regulations. All client facing persons such as sale staff, service relationship managers, client relationship managers, etc. shall be deemed to be persons associated with investment advice, whereas principal officer shall mean managing director/managing partner, designated director etc. who is responsible for overall business operations of non-individual IAs. In terms of the erstwhile IA Regulations, IA shall have either professional qualification/post-graduation or graduation along with five year experience of advisory as mentioned in regulation 7(1). However, as per recent amendments, an individual IA and principal officer in case of non-individual IA shall be required to meet both the criteria that is to have professional qualification/post-graduation along with 5 years experience at all times. The requirement of certification on financial planning (NISM) remains unchanged.

In terms of the erstwhile IA Regulations, IAs which are body corporate shall have a net worth of not less than twenty-five lakh rupees and for IAs who are individuals or partnership firms shall have net tangible assets of value not less than rupees one lakh. However, SEBI has increased minimum net worth criteria to rupees fifty lakhs and rupees five lakhs for non-individual and individual IAs respectively. However, all persons associated with investment advice shall comply with the qualification requirements with minimum two years of experience. The existing IAs shall comply with new eligibility norms within 3 years from the date of commencement of Amendment Regulations. The summary of erstwhile eligibility criteria along with recent amendments is given below:

|

For Individual IAs |

|||

|

Requirement |

Erstwhile |

Amended |

Persons associated with Investment Advice including representatives |

|

Education |

Professional qualification/post-graduation | Professional qualification/post-graduation with 5 years of experience | Professional qualification/post-graduation with 2 years of experience |

| Graduation with 5 years of experience | |||

|

Certification |

NISM | NISM | NISM |

|

Net Worth |

Rs. 1 lakh | Rs. 5 lakhs |

Not applicable |

|

For Non-individual IAs |

|||

|

Requirement |

Erstwhile for representatives |

Amended for principal officer |

Persons associated with Investment Advice including representatives |

|

Education |

Professional qualification/post-graduation | Professional qualification/post-graduation with 5 years of experience | Professional qualification/post-graduation with 2 years of experience |

| Graduation with 5 years of experience | |||

|

Certification |

NISM | NISM | NISM |

|

Net Worth |

Rs. 25 lakhs | Rs. 50 lakhs |

Not applicable |

Use of Nomenclature

In order to obviate misunderstanding and confusion amongst investors regarding the roles and responsibilities of distributors including mutual fund distributors who refer to themselves as ‘independent financial adviser’ or ‘wealth adviser’, it is relevant that the nomenclature should not mislead the investors. Therefore, SEBI has inserted Regulation 3(3) which specifies that any person other than IA registered with SEBI, dealing in distribution of securities shall not use the nomenclature “Independent Financial Adviser (IFA) or Wealth Adviser or any other similar name.

Conversion of Individual IAs to Non-individual IAs

SEBI has inserted additional criteria under regulation 13 which directs individual IA to apply for registration as non-individual IA, in case number of clients of such individual IA exceeds 150 in total.

Conclusion

With these amendments, SEBI took efforts to make robust regulation for investment advisers. Some of the changes would definitely pick up the slacks, however, SEBI should reassess the proposal for ceiling limit on advisory fees and bring more clarity.

[1]https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/jun-2020/1591597643206.pdf#page=1&zoom=page-width,-15,842

[2]https://www.sebi.gov.in/reports-and-statistics/reports/jan-2020/consultation-paper-on-review-of-regulatory-framework-for-investment-advisers-ia-_45685.html

[3] https://www.sebi.gov.in/media/press-releases/feb-2020/sebi-board-meeting_46013.html

[4] http://egazette.nic.in/WriteReadData/2020/220363.pdf and https://www.sebi.gov.in/media/press-releases/jul-2020/sebi-notifies-amendments-to-sebi-investment-advisers-regulations-2013_47006.html

Special Liquidity Scheme – providing short term liquidity relief for NBFCs

Timothy Lopes | Senior Executive

Vinod Kothari Consultants

In light of the disruption caused by the pandemic, the Government of India announced a Rs. 20 lakh crores economic stimulus package. The first of the several reforms were announced on 13th May, 2020 which announced the Emergency Credit Line, the partial credit guarantee scheme 2.0 (PCG 2.0), TLTRO 2.0 and much more.

The PCG 2.0 scheme permitted banks to purchase CPs and bonds issued by NBFCs/MFIs/HFCs. These purchases were then guaranteed by the Government of India up to 20% of the first loss. For more details of the scheme see our write up here.

The announcement also proposed launching a Rs. 30,000 crores “Special Liquidity Scheme” for NBFCs/HFCs including MFIs. The Cabinet approved this scheme on 20th May, 2020[1].

On 1st July, 2020, RBI has released the details of the Special Liquidity Scheme[2]. The scheme is intended to avoid potential systemic risk to the financial sector. The scheme seems to be a short term relief for NBFCs acting as a bail-out package for near term maturity debt instruments. The scheme is intended to supplement the existing measures already introduced by the Government.

The scheme will provide liquidity to eligible NBFCs defined in the notification which is similar to the eligibility criteria specified under the PCG 2.0 scheme. The Government will implement the scheme through SBICAP which is a subsidiary of SBI. SBICAP has set up a SPV called SLS Trust to manage the operations. More details about the trust can be found on the website of SBICAP[3].

Under the scheme, the SPV will purchase the short-term papers from eligible NBFCs/HFCs. RBI will provide liquidity to the Trust depending on actual purchases by the Trust. The utilisation of proceeds from the scheme will be only towards the sole purpose of extinguishing existing liabilities.

Eligible instruments

Instruments eligible for the scheme are relatively short term. The scheme specifies that CPs and NCDs with a residual maturity of not more than three months (90 days) and rated as investment grade will be eligible instruments. These dates, however, may be extended by Government of India. The SPV would invest in securities either from the primary market or secondary market subject to the conditions mentioned in the Scheme.

The actual investment decisions will be taken by the Investment Committee of the SPV.

Validity of the Scheme

The scheme is available only up to 30th September, 2020 as the SPV will cease to make purchases thereafter and would recover all the dues by 31st December, 2021 or any other date subsequently modified.

Investment by the SPV

The SPV set up under the scheme comprises of an investment committee. The investment committee will decide the amount to be invested in a particular NBFC/HFC. The FAQs available on the website of SBICAPs specifies that the Trust shall invest not more than Rs. 2000 crores on any one NBFC/HFC subject to them meeting conditions specified in the scheme. The Trust may have allocation up to 30% to NBFCs/HFCs with asset size of Rs. 1000 crores or less.

Rate of Return and collateral

Rate of Return (RoR) and other specifics under the scheme will likely be based on mutual negotiation between the NBFCs and the trust. According to the FAQs, the yield on securities invested by SPV shall be decided by the Investment Committee subject to the provisions of the scheme.

The Trust may also require an appropriate level of collateral from the NBFCs/ HFCs as specified under the FAQs.

Conclusion

The scheme is a welcome move likely to provide sufficient liquidity to the NBFC sector for the near term and act as a bail-out package for their short term liabilities.

The press release dated 20th May, 2020, approving the Special Liquidity Scheme states that “Unlike the Partial Credit Guarantee Scheme which involves multiple bilateral deals between various public sector banks and NBFCs, requires NBFCs to liquidate their current asset portfolio and involves flow of funds from public sector banks, the proposed scheme would be a one-stop arrangement between the SPV and the NBFCs without having to liquidate their current asset portfolio. The scheme would also act as an enabler for the NBFC to get investment grade or better rating for bonds issued. The scheme is likely to be easier to operate and also augment the flow of funds from the non-bank sector.”

Our related write ups may be viewed below –

https://vinodkothari.com/2020/05/pcg-scheme-2-0-for-nbfc-pooled-assets-bonds-and-commercial-paper/

https://vinodkothari.com/2020/05/guaranteed-emergency-line-of-credit-understanding-and-faqs/

https://vinodkothari.com/2020/05/self-dependent-india-measures-concerning-the-financial-sector/

https://vinodkothari.com/2020/04/would-the-doses-of-tltro-really-nurse-the-financial-sector/

[1] https://pib.gov.in/PressReleasePage.aspx?PRID=1625310

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11925&Mode=0

MCA widens CSR for defence personnel

Measures for the CAPF and CMPF veterans and dependants now a part of CSR activity

Ankit Vashishth, Executive, Vinod Kothari and Company; corplaw@vinodkothari.com

Introduction

Schedule VII of the Companies Act, 2013 (‘Act’) currently includes measures taken for the armed forces veterans, war widows and their dependants as one of the CSR activities. The Ministry of Corporate Affairs (“MCA”) vide its Notification[1] dated 23rd June, 2020 has included contribution made towards the benefit of Central Armed Police Forces (CAPF) and Central Para Military Forces (CPMF) veterans and their dependents including widows, within the ambit of CSR.

MCA has issued several notifications either to clarify or broaden the ambit of Schedule VII. This Notification is yet another step taken by the MCA for widening the scope of CSR activities to include CAPF and CMPF veterans and their dependants and war widows.

This note tries to provide a quick coverage on the said amendment.

Difference between Armed Forces and CAPF/CPMF

| Armed Forces | CAPF | CPMF |

| The term “armed forces” basically means – Indian Armed Forces which are the military forces of the Republic of India. It comprises three professional uniformed services :

1. The Indian Army 2. The Indian Navy 3. The Indian Air Force |

CAPF (Central Armed Police Force)[2] consists of :

1. Assam Rifles (AR); 2. Border Security Force (BSF); 3. Central Industrial Security Force (CISF); 4. Central Reserve Police Force (CRPF); 5. Indo Tibetan Border Police (ITBP); 6. National Security Guard (NSG); and 7. Sashastra Seema Bal (SSB) |

The nomenclature CAPF will be used uniformly for CPMF as per the Office Memorandum [3]issued by the Ministry of Home Affairs issued on March 18, 2011 |

Current CSR spending pattern and changes expected due to the amendment

The current pattern for CSR spending for armed forces veterans, war widows and their dependants include contributions to several funds like:

- Armed Forces Flag Day Fund (AFFDF)[4]

- Army Wives Welfare Association (AWWA)[5]

- The Army Welfare Fund Battle Casualties[6]

Apart from donating to these funds, companies have also provided financial relief to the martyr’s families and have conducted workshops for the children of war widows as a part of their CSR projects.

Further, in addition to the above, contribution to “National Defence Fund” which is used for the welfare of the members of the Armed Forces (including Para Military Forces) should be eligible for being a CSR activity.

As a result of the enhanced scope for CSR spending for CAPF/ CAMF, contribution to the fund “Bharat Ke Veer Corpus Fund”[7], which was previously not eligible for CSR considering the fact that it specifically benefits CAPF, will now be covered as per the amendment. Accordingly, any contribution to this fund will now qualify as a CSR activity.

High Level Committee on CSR

MCA had constituted[8] a High Level Committee (HLC) on CSR in February, 2015 under the Chairmanship of Secretary (Corporate Affairs) to review the existing CSR framework and formulate a coherent policy on CSR and further make recommendations on strengthening the CSR ecosystem, including monitoring implementation and evaluation of outcomes. Later, the HLC on CSR was re-constituted[9] in November, 2018. The scope of HLC was widened to include recommendation of guidelines for enforcement of CSR provisions. Though the Report discussed on amending Schedule VII in line with promoting sports, senior citizens’ welfare, welfare of differently abled persons, disaster management, and heritage, however, it did not consider widening the clause relating to the scope of armed forces in the Schedule.

Further, as evident from the data given in the HLC Committee Report[10], CSR expenditure made on armed force veterans, war widows/ dependents have seen an upward trend over the years, however it forms a very small proportion of the total CSR expenditure made.

Concluding Remarks

The service spirit of CAPF is no less than that of the Indian Army. Acknowledging this fact MCA has brought this amendment. While all the areas for CSR are extremely important for the overall socio-economic welfare and development, the measures taken for the benefit of veterans and dependants of the armed forces and CAPF/ CPMF is an extremely noble activity.

Link to our other articles:

CSR: A ‘Corporate Social Responsibility’ or a ‘Corporate Social Compulsion’?

Proposed changes in CSR Rules

https://vinodkothari.com/2020/03/proposed-changes-in-csr-rules/

FAQs on Corporate Social Responsibility

https://vinodkothari.com/2019/11/faqs-on-corporate-social-responsibility/

Read our other articles on Corplaw : https://vinodkothari.com/category/corporate-laws/

Link to our Youtube Channel : https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

[1] http://egazette.nic.in/WriteReadData/2020/220133.pdf

[2] https://www.mha.gov.in/about-us/central-armed-police-forces

[3] Office Memorandum can be viewed here

[4] http://ksb.gov.in/armed-forces-flag-day-fund.htm

[5] https://awwa.org.in/contribution-under-csr-awwa

[6] The Army Welfare Fund Battle Causalities

[7] https://www.bharatkeveer.gov.in/about

[8] https://www.mca.gov.in/Ministry/pdf/General_Circular_01_2015.pdf

[9] https://www.mca.gov.in/Ministry/pdf/OfficeOrderCommitteeOnCorporate_26112018.pdf

[10] https://www.mca.gov.in/Ministry/pdf/CSRHLC_13092019.pdf

MoF rolls out draft rules for foreign investment in Pension Funds

After 4 years of providing sectoral cap for the same.

Aanchal Kaur Nagpal | Executive

corplaw@vinod kothari.com

Pension Funds (‘PF’) are responsible for receiving contributions and managing pension corpus through various schemes[1] under National Pension System (‘NPS’) in accordance with the provisions specified by the PFRDA and carry out functions as per the directions of the NPS Trust. Presently, there are 3 companies registered as PF for government sector and 7 companies registered as PF for private sector. According to regulation 8(e) of the PFRDA (Pension Fund) Regulations, 2015[2], a sponsor of a PF is required to incorporate the pension fund as a separate limited company under the Companies Act, 2013. As on date, all existing PFs are unlisted companies.

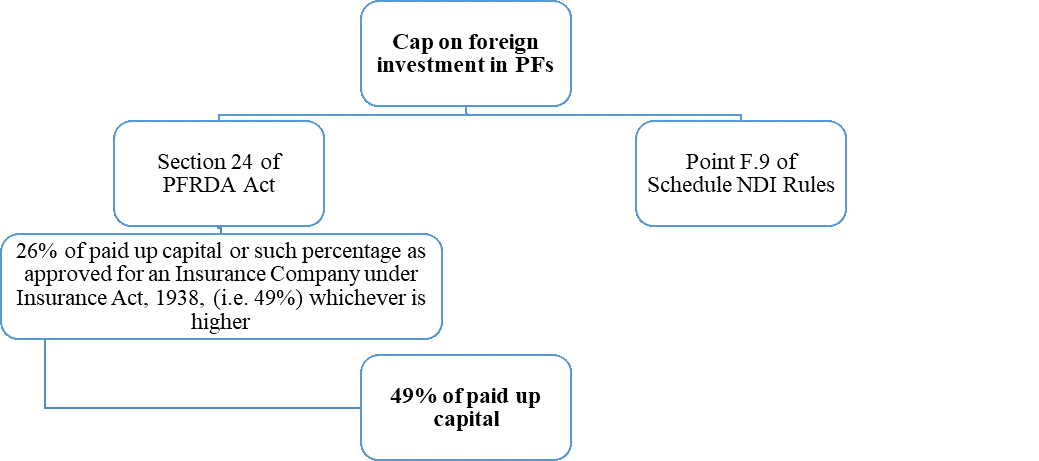

Foreign investment in pension sector is permitted upto 49% under automatic route as per para F.9 of Schedule I to Foreign Exchange Management (Non-debt instruments) Rules, 2019 (‘NDI rules’). This was inserted in 2016 vide DIPP press note no. 2 of 2016[3]. Foreign investment in PF is required to be in accordance with Pension Fund Regulatory and Development Authority (PFRDA) Act, 2013 (‘PFRDA Act’). Foreign investment in PF is subject to the condition that entities investing in capital instruments issued by an Indian Pension Fund as per section 24 of the PFRDA Act are required to obtain necessary registration from the PFRDA and comply with other requirements as per the PFRDA Act[4] and Rules and Regulations framed under it for so participating in Pension Fund Management activities in India. An Indian pension fund needs to ensure that its ownership and control remains at all times with resident Indian entities as determined by the Government of India/ PFRDA as per the rules or regulation issued by them.

With a view to regulate foreign investment in PFs, the Ministry of Finance has introduced draft rules viz. Pension Fund (Foreign Investment) Rules, 2020 (‘Draft PF Rules’) on 19th June, 2020 for public comments[5]. The Draft PF Rules continue to refer to FEMA (Transfer of Issue of Securities by a Person Resident outside India) Regulations, 2000 (‘TISPRO Regulations’) which was repealed in 2017 vide FEMA (Transfer of Issue of Securities by a Person Resident outside India) Regulations, 2017 and thereafter by FEMA (Non-Debt Instrument) Rules, 2019. Accordingly, the anomalies arising out of reference to TISPRO Regulations instead of NDI Rules are pointed in Annexure I.

Components of foreign investment

Foreign investment has been defined under rule 2(d) of the Draft PF Rules that means and includes investment made by following in the equity shares of a Pension Fund in India:

- a foreign company, either by itself or through its subsidiary companies or its nominees; or

- an individual; or

- an association of persons, whether registered or not, under any law or a country outside India;

- Foreign Venture Capital Invesment;

- other eligible entities .

*Equity capital has been defined to have the same mean as section 43 of the Companies Act, 2013.

The total foreign investment will include both direct as well as indirect investment made by foreign investment.

Comment: The definition of foreign investment should be aligned with NDI Rules. The extent of foreign investment should be basis the investment made in equity instruments, as opposed to equity share capital.

Ceiling on quantum of foreign investment

Both, the PFRDA Act and NDI Rules restrict foreign investment in PFs upto 49%. The Draft PF Rules also follow the lead of these provisions and state that the aggregate holding in a PF by foreign investors, including foreign portfolio investors, should not exceed 49% of its paid-up equity share capital. [Rule 3 of the Draft PF Rules]. Further, foreign investment up to 49% is allowed through automatic route. [Rule 5 of the Draft PF Rules]

The total foreign investment would be a total of direct and indirect foreign investment calculated as per the PFRDA regulations read with the FDI policy. [Rule 2 (p) of the Draft PF Rules]

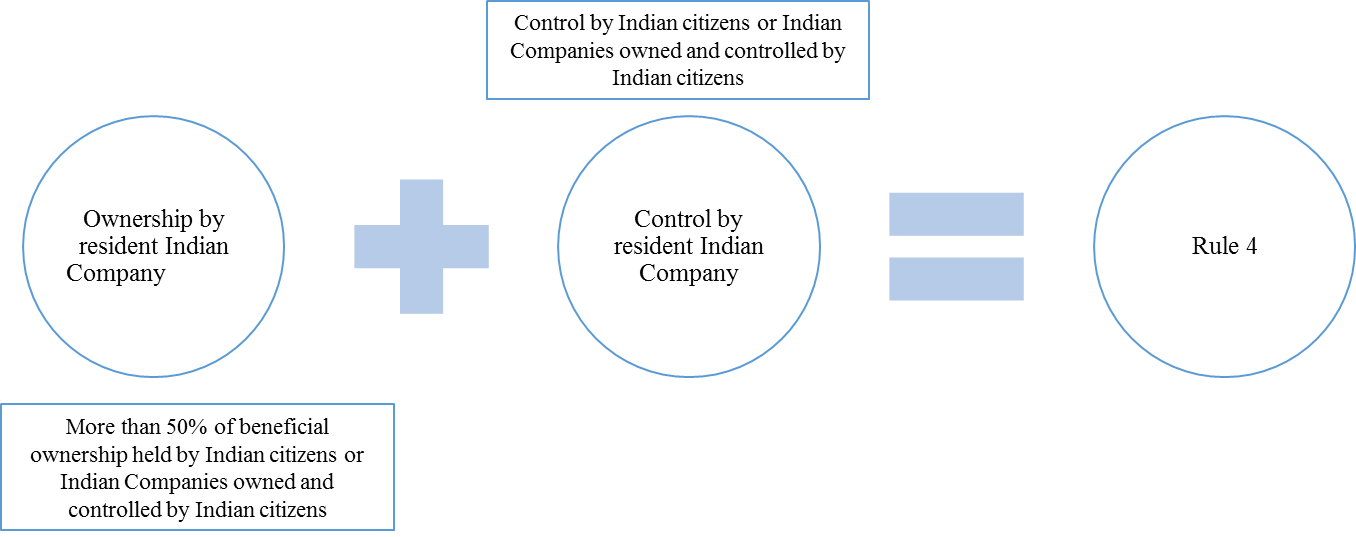

Indian ownership and control at all times

Rule 4 of the Draft PF Rules lays down that PFs in India must at all times ensure that their ‘ownership and control’ remains in the hands of resident Indian entities. For this purpose the rules have also defined ‘Indian Control’ and ‘Indian Ownership’ in Rule 2 (i) and (j) respectively. The same has been illustrated in the figure below:

This dual condition of ownership and control has been laid down to ensure that the decision making power of PFs stays with Indian investors at all times. PFs are vital institutional investors in the equity, debt and G-secs market. Handing out the controlling power to a foreign investor would affect the Indian capital markets and in turn the economy as a whole.

Foreign Portfolio Investment in PFs

FPI in PFs will be governed by the FEMA Regulations, 2000 along with SEBI (FPI) Regulations, 2019. [Rule 6 of the PF Rules]

Comment: The definition of foreign portfolio investment should be aligned with NDI Rules.

Increase in Foreign Investment in PFs

Pricing guidelines specified under FEM Regulations will have to be followed for increase in foreign investment of PFs. [Rule 7 of the PF Rules]

Comment: Reference of Rule 21 of NDI Rules to be inserted.

The great wall for China

As a consequence of the COVID-19 pandemic lockdown as well as the increasingly strained relations between India and China, the former has imposed various restrictions on foreign investment by the latter.

The government has, vide the FEMA (NDI) Amendment Rules, 2020 dated 22nd April, 2020 posed the requirement of prior approval for any foreign investment by an entity of a country that shares land border with India in order to avoid opportunistic takeovers. This would even apply in cases where the beneficial ownership of the investment is situated in any of the restricted countries as well as to any case of transfer of ownership[1].

[1] To read out write-up on the same- https://vinodkothari.com/wp-content/uploads/2020/04/India-seals-its-borders-to-corporate-acquistions-ver-30.04.2020.p

In furtherance to this the Draft PF Rules specify that government approval will be required for investment in PF by foreign investors (entities as well as individuals) from any bordering countries including China. [Rule 8 of the Draft PF Rules]

Comment: Need to align with recent amendments made in Rule 6 (a) of NDI Rules restricting investments from countries sharing land border with India.

Link to our other articles:

- MoF amends FDI norms for rights issue and insurance sector:

https://vinodkothari.com/2020/04/mof-amends-fdi-norms-for-rights-issue-and-insurance-sector/

- Introduction to FEMA (NDI) Rules, 2019 and recent amendments

https://vinodkothari.com/2020/04/introduction-to-fema-ndi-rules-2019-and-recent-amendments/

- India seals its borders to corporate acquisitions

https://vinodkothari.com/2020/04/india-seals-its-borders-to-corporate-acquisitions/

- FPI can invest up to the sectoral cap in an Indian Company

https://vinodkothari.com/2020/04/fpi-can-invest-upto-the-sectoral-cap-in-an-indian-company/

Annexure I

Suggested amendments

| Sr. no. | Provision | Details of the provision | Remarks |

| 1. | Rule 2(d) | ‘Foreign Investment means…..

xx in the equity shares of a PF in India under clause (i) of sub regulation (1) of regulation 5 of the Foreign Exchange Management (Transfer of issue of security by a person resident outside India) Regulations, 2000

|

The definition of foreign investment makes reference to guidelines as specified under the TISPRO Regulations which have been repealed.

The corresponding provisions are covered under rule 6(a) of the NDI Rules. |

| 2. | Proviso to Rule 2(d) | Provided that for the purpose of these rules, foreign investment shall include investment by Foreign Venture Capital Investment (FVCI) as permissible under regulation 6 of FEMA Regulations, 2000 | As stated above, reference has been made to the repealed regulations.

Investments made by an FVCI are governed by rule 16 read with Schedule VII of the NDI Rules. As per the schedule, PFs are not included in the list of sectors permitted for investment by an FVCI. However, in the Draft PF Rules, the same is permitted and included under foreign investment.

|

| 3. | Rule 2(f) | Foreign portfolio investment means and includes investments in the equity share of a pension fund in India by Foreign Institutional Investors, Foreign Portfolio Investors, Non-Resident Indian, Qualified Foreign Investors and other eligible portfolio investor entities or persons in accordance with provisions contained in sub-regulations 2, (2A), 3, and 8 of Regulation 5 of FEMA Regulations, 2000

|

Firstly, reference has been made to the repealed regulations.

Secondly and more importantly, the definition is not in line with that provided under the NDI Rules and thus creating conflict.

According to the NDI Rules, foreign portfolio investment means any investment made by a person resident outside India through equity instruments where such investment is less than 10% of the post issue paid-up share capital on a fully diluted basis of a listed Indian company or less than 10% of the paid-up value of each series of equity instrument of a listed Indian company;

The Draft PF Rules consider FPI in equity shares (as defined under rule 2(c) which states that equity share capital will have the same meaning as defined under section 43 of the Companies Act, 2013) of the Company while the NDI Rules compute FPI on the basis of equity instruments (as defined under rule 2k of the NDI Rules).

Accordingly reference of ‘investing in equity shares’ should be substituted with ‘investing in equity instruments’ of PF in India.

Further, as per NDI rules, any foreign investment in an unlisted Company is treated as a foreign direct investment (FDI) irrespective of the quantum. In case of listed companies, investment up to 10% is treated as FPI. However, in case of the definition as provided under the Draft PF Rules, investment in equity shares of a PF would be treated as FPI. Furthermore, most of the PFs in India are unlisted companies. This creates huge discrepancy as to the fact whether foreign investment would be treated as FDI if it exceeds 10 % (as per NDI Rules) or PFI (as per Draft PF Rules)

Hence, alignment with the existing definition specified under rule 2(t) of the NDI Rules does not seem to be a relevant solution.

|

| 4. | Rule 2(i) | “Indian Control” of a pension fund means Control of a pension fund in India by resident Indian citizens or Indian Companies, which are owned and controlled by resident Indian citizens. | According to Rule 23(7)(e) of the NDI Rules, “company controlled by resident Indian citizens” means an Indian company, the control of which is vested in resident Indian citizens and/ or Indian companies which are ultimately owned and controlled by resident Indian citizens……

According to Rule 23(7)(d) of the NDI Rules “control” shall mean the right to appoint majority of the directors or to control the management or policy decisions including by virtue of their shareholding or management rights or shareholders agreement or voting agreement…….

The definition under the Draft PF Rules more or less are similar to that provided under the NDI Rules. However, the term used in the former is ‘Indian control’ which should be aligned with the NDI Rules using the term ‘controlled by resident Indian citizens’.

Also, control has not been defined under the Draft PF Rules.

|

| 5. | Rule 2(j) | “Indian Ownership” of a pension fund in India means more than 50% of the equity capital in it is beneficially owned by resident Indian citizens or Indian companies, which are owned and controlled by resident Indian citizens provided that the manner of the computation of foreign holding of such Indian promoter or Indian investment company shall be construed with the relevant Rules and PFRDA Regulations/ Guidelines.

|

According to Rule 23(7)(b) of the NDI Rules, “company owned by resident Indian citizens” shall mean an Indian company where ownership is vested in resident Indian citizens and/ or Indian companies, which are ultimately owned and controlled by resident Indian citizens……

According to Rule 23(7)(a) of the NDI Rules, “ownership of an Indian company” shall mean beneficial holding of more than fifty percent of the equity instruments of such company…

Both the definitions specify the same percentage. However, the Draft PF Rules make reference to equity capital which has been defined therein to have the same meaning as that specified in section 43 of the Companies Act, 2013. As per section 43, “equity share capital”, with reference to any company limited by shares, means all share capital which is not preference share capital. This means in case of Draft PF Rules, only equity capital will be considered. As opposed to this, the NDI Rules refer to equity instruments which include shares, convertible debentures, preference shares and share warrants subject to conditions specified.

The same should be aligned with the NDI Rules along with the terminology used.

|

| 6. | Rule 2 (n) | ‘Resident Indian investment’ shall have the same meaning assigned to it in the FDI policy issued from time to time.

|

In case there is a specific clause to that effect in the FDI Policy, then the same may be retained else, the definition should be modified to mean ‘investment made by a person resident in India not resulting in indirect foreign investment’. |

| 7. | Rule 2 (q) | All other words and expression used in these rules but not defined, and defined in the Act and Rules, regulations made thereunder shall have the same meanings respectively assigned to them.

|

As certain terms may not be defined in PFRDA Act, Rules and Regulations but may be defined in NDI Rules, reference of NDI Rules should be included. |

| 8. | Rule 6 | Foreign Portfolio Investment in a Pension Fund in India shall be governed by the provisions contained in sub-regulations 2, (2A), 3, and 8 of Regulation 5 of FEMA Regulations, 2000 and Securities Exchange Board of India (Foreign Portfolio Investors) Regulations

|

Reference has been made to the repealed TISPRO Regulation, 2000.

Corresponding provisions under NDI Rules · For regulation 5(2A) of the TISPRO regulations for investment by Foreign Portfolio investors- Chapter 4 read with Schedule II of the NDI Rules; · For regulation 5(3) of the TISPRO regulations dealing with investment by Non-resident Indians and Overseas Corporate Body – Chapter V read with Schedule III and Chapter VI read with Schedule V of the NDI Rules; · For regulation 5(8) of TISPRO regulations dealing with investment in depository receipts- rule 6(d) read with Schedule IX of the NDI Rules.

Further, the TISPRO Rules mention of the Foreign Portfolio Scheme which was foregone in the TISPRO Regulations, 2017 and later by the NDI Rules as well.

|

| 9. | Rule 8 | A Government approval will be required for the investing entity or individual from any of the bordering countries including China.

|

While the Draft PF Rules make use of the term ‘bordering countries’, the same should be aligned with the NDI rules that makes reference to ‘a country which shares land border with India’. |

[1] https://www.pfrda.org.in/index1.cshtml?lsid=187

[2] http://www.npstrust.org.in/sites/default/files/PFRDA_PFReg2015.pdf

[3] https://dipp.gov.in/sites/default/files/pn2_2016_1.pdf

[4] http://legislative.gov.in/sites/default/files/A2013-23.pdf

[5] By July 18, 2020.