Comparison between the proposed and existing regulatory framework for HFCs

– Henil Shah and Harshil Matalia (finserv@vinodkothari.com)

The Finance Act, 2019 amended the provisions of National Housing Bank, 1987 w.e.f August 09, 2019 thereby shifting the power to govern Housing finance Companies (HFCs) from National Housing Bank (NHB) to the Reserve Bank of India (RBI). Later, the RBI in its press release dated August 13, 2019 stated that HFCs shall be considered as a separate category of NBFCs.

A regulatory framework governing HFCs was long awaited. With a view to bring uniformity in the regulatory framework for HFCs and NBFCs, the RBI on 17th June, 2020 issued the report containing proposed changes in the regulatory framework for HFCs. The same is open for public opinions till 15th July,2020.

We have compared the proposed guidelines for HFCs with the existing guidelines.

| Sr. No. | Current Provisions Applicable to HFCs | Proposed Provisions | Remarks |

| Defining the phrase ‘providing finance for housing’ or ‘housing finance’ | |||

| 1 | The NHB Directions defined the term “housing finance company” as a company incorporated under the Companies Act, 1956 which primarily transacts or has as one of its principal objects, the transacting of the business of providing finance for housing, whether directly or indirectly. However, the term ‘providing finance for housing’ or ‘housing finance’ was not formally defined.

There was a NHB Circular dated September 26, 2011 which provided an illustrative list of loans which can be classified as housing/ non housing loans- 1. Loans to individuals or group of individuals including co-operative societies for construction/ purchase of new dwelling units. |

It has been proposed to define ‘Housing Finance” or “providing finance for housing” to mean financing, for purchase/ construction/ reconstruction/ renovation/ repairs of residential dwelling units, which includes:

a. Loans to individuals or group of individuals including co-operative societies for construction/ purchase of new dwelling units. |

The proposed list is largely similar to the illustrative list prescribed by NHB earlier. However, the list prescribed as ‘qualifying asset’ for HFCs seems to focus more on individual borrowers. It has also excluded the following- a. Loans for shopping complexes, markets and such other centers catering to the day to day needs of the residents of the housing colonies and forming part of a housing project b. Loans provided to the bodies constituted for undertaking repairs to houses; c. Investment in the guarantee/non-guaranteed bonds and debentures of NHB/HUDCO in the primary market, provided investment in non-guaranteed bonds is made only if guaranteed bonds are not availableThe idea behind laying out the periphery of ‘housing loans’ is to ensure consistency and certainty in ‘principality’ of business of the HFCs. Only such loans, which “qualify” as “housing loans” would be treated as “qualifying assets” for the purpose of determining “principality” of business of the entity, as we see below. Specifically, loans given for furnishing dwelling units, loans given against mortgage of property for any purpose other than buying/ construction of a new dwelling unit/s or renovation of the existing dwelling unit/s, have been regarded as non-housing loans. An entity which falls short of such qualifying assets below 50% cannot be regarded as HFC. This provision is also expected to minimise the practice of giving mortgage loans (LAP-type loans) by HFCs, which would often be granted to meet working capital requirements, etc. of other entities and not for housing purposes; thereby restricting the portfolio deviations of the HFC. |

| Defining ‘principal business’ and ‘qualifying assets’ for HFCs | |||

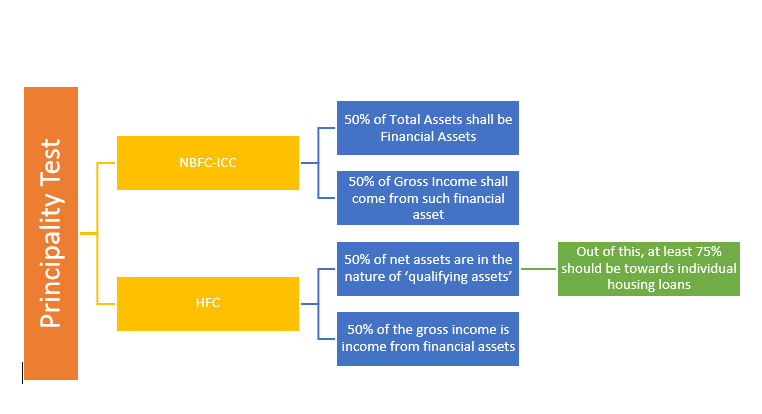

| 2 | The term ‘principal business’ was not referred in NHB Act prior to the amendment vide Finance Act . Further, for the purposes of registration, NHB was recognizing companies as HFCs if such company has, as one of its principal objects, transacting of the business of providing finance for housing (directly or indirectly) | The principality test for HFCs has been proposed as follows (both these tests are required to be satisfied as the determinant factor for principal business): (a) Not less than 50% of net assets are in the nature of ‘qualifying assets’ of which at least 75% should be towards individual housing loans as prescribed. Here, net assets shall mean total assets other than cash and bank balances and money market instruments (b) Not less than 50% of the gross income is income from financial assetsQualifying Assets refer to ‘housing finance’ or ‘providing finance for housing’ as mentioned above |

With the amendment to NHB Act, there was a need to define the term ‘principal business’ for HFCs. The concept of ‘qualifying asset’ is similar to that in case of NBFC-MFIs wherein they are specifically focused on micro lending. Though in spirit the HFCs would primarily focus on housing loans only however, the HFCs offering home loans along with other related products would now be required to maintain the principality of individual housing loans.

The requirement of minimum concentration towards ‘individuals’ is a new concept and possibly to protect the HFCs from systemic exposures. Further, principality is to be differentiated from ‘ordinary’ – that is, the guidelines do not prohibit the HFCs from providing non-housing loans- it limits the same. The remaining 50% can be extended in the form of non-housing loans, including LAP. An HFC which falls short of such qualifying asset criteria has to get registration as NBFC-ICC – consequentially, all laws applicable to such NBFC-ICC shall apply to the HFC. |

| Classification of HFCs as Systemically Important and Non-systemically Important entities | |||

| 3 | As per the current scenario a common set of regulations are applicable for all HFCs irrespective of asset size and ownership | In order to introduced a graded approach as applicable to NBFCs in general the proposed changes tend to classify HFCs if following categories:

1. All deposit taking HFCs (HFCs-D) irrespective of asset size and all non-deposit HFCs (HFCs-ND) with asset size of over INR 500 crores as systemically important HFCs; |

The existing regulations for HFCs are similar to NBFCs. The larger HFCs may continue with existing regulations under NHB regulations or be harmonised with NBFC-SI regulations. However, there are separate regulations for deposit taking NBFCs which might become applicable on deposit taking HFCs as well. For the non-systemically important HFCs, it is proposed to bring the regulations at par with Master Directions for NBFC-ND-non-SI |

| Minimum Net Owned Fund Requirement | |||

| 4 | For a company to commence or carry a principal business of housing finance it shall have a minimum net owned fund of INR 10 Crore. | Minimum net owned fund (NOF) requirement is proposed to be increased from 10 Crore to 20 crore.

Existing HFC shall be given a time period of 1 year to reach NOF of INR 15 Crore and another 1 year to reach INR 20 Cr minimum NOF mark |

The increased capital requirement is to strengthen the capital base of the HFCs.

However, as compared to an NBFC the NOF requirement is very high. The registration requirement for both NBFC-ICC and HFC will also be the same- they will have to apply to the RBI. An important question that will arise here is that why should an entity register as an HFC- given the fact that even an NBFC-ICC can extend housing loan, one would have to consider the various factors to carry on housing finance as a principle activity under an HFC or non principal activity under an NBFC-ICC. As per the provisions of section 29A and 2(d) of the NHB Act read along with the RBI guidelines issued in this regard, an HFC will have to satisfy the principality of 50% housing loans as well as 75% loans to individuals. |

| Harmonising definitions of Capital (Tier I & Tier II) with that of NBFCs | |||

| 5 | Tier- I Capital is defined under Para 2(1)(zf) of HFCs Master Directions as: “Tier-I capital” means owned fund as reduced by investment in shares of other housing finance companies and in shares, debenture, bonds, outstanding loans and advances including hire purchase and lease finance made to and deposits with subsidiaries and companies in the same group exceeding, in aggregate, ten percent of the owned fund;Tier- I Capital is defined under Para 2(1)(zg) of HFCs Master Directions as: “Tier-II capital” includes the following:- (i) preference shares (other than those compulsorily convertible into equity); (ii) revaluation reserves at discounted rate of fifty five percent; (iii) 10[general provisions (including that for standard assets) and loss reserves to the extent these are not attributable to actual diminution in value or identifiable potential loss in any specific asset and are available to meet unexpected losses, to the extent of one and one fourth percent of risk weighted assets]; (iv) hybrid debt; (v) subordinated debt to the extent the aggregate does not exceed Tier-I capital; |

As per Para 3 (xxxii) and 3 (xxxiii) of Master Directions for NBFC-ND-SI

“Tier I Capital” means owned fund as reduced by investment in shares of other non-banking financial companies and in shares, debentures, bonds, outstanding loans and advances including hire purchase and lease finance made to and deposits with subsidiaries and companies in the same group exceeding, in aggregate, ten per cent of the owned fund; and perpetual debt instruments issued by a non-deposit taking non-banking financial company in each year to the extent it does not exceed 15% of the aggregate Tier I Capital of such company as on March 31 of the previous accounting year; “Tier II capital” includes the following: (a) preference shares other than those which are compulsorily convertible into equity; (b) revaluation reserves at discounted rate of fifty five percent; (c) General provisions (including that for Standard Assets) and loss reserves to the extent these are not attributable to actual diminution in value or identifiable potential loss in any specific asset and are available to meet unexpected losses, to the extent of one and one fourth percent of risk weighted assets; (d) hybrid debt capital instruments; (e) subordinated debt; and (f) perpetual debt instruments issued by a non-deposit taking non-banking financial company which is in excess of what qualifies for Tier I Capital, to the extent the aggregate does not exceed Tier I capital. |

It is proposed to align the definitions of capital (both Tier I and Tier II) of HFCs with that of NBFC, specifically PDIs shall form part of HFCs capital (both Tier I and Tier II) component on the same lines as NBFCs. However, with the following differences-

1.PDIs shall be treated as Tier I/ Tier II capital only by HFCs-ND-SI |

| Public Deposits | |||

| 6 | Public deposits is defined under Para 2(1)(y) of the NHB Directions, 2010 | Subject to alignment of Public deposit provisions of HFC with NBFC following shall be: Additions to the existing exemptions from public deposits: 1. Rehabilitation Industries Corporation of India Ltd. 2. Corporation established by or under any Statute; or a cooperative society registered under the Cooperative Societies Act of any StateDeletion from the list of exemptions applicable to HFCs 1. Japan Bank for International Cooperation (JBIC) 2. Kreditanstalt fur Wiederaufbau (KfW) In addition to changes pursuant to the alignment, any amount received by the HFCs from NHB or any public housing agency shall be exempted |

There are no major changes arising from the alignment of definitions of public deposits, however it seems that at the time of alignment this may be taken care off. |

| Liquidity Risk framework and LCR | |||

| 7 | Under the present scenario HFCs are required to follow Guideline for Asset Liability Management System issued by NHB via Policy Circular No. 35 dated 11th October, 2011 | Guidelines for Liquidity risk management framework (LRM) and liquidity coverage ratio (LCR) as notified by the RBI on 04th November, 2019 applicable to NBFCs shall be extended to HFCs-ND with asset size of more than 100 crores and all HFCs-D subject to supervisory review of internal controls required to put in place by HFCs (Refer our presentation on LRM here- https://vinodkothari.com/2019/11/liquidity-risk-framework/) | Actionable from the Liquidity Risk Management Framework:

1. HFCs will be required to edit the current ALM policy or adopt a new LRM framework. However question arises in relation to the applicability of LCR as same is applicable in NBFCs-D and NBFC-ND-SI with asset size of 5000 crore or more whereas the its proposed to extended the guidelines in case of HFCs to all the HFCs-D and HFCs-ND-SI with asset Size of INR 100 crore or more. RBI may look into difference in applicability criteria while notifying the same. |

| Group entities Engaged in real estate business | |||

| 8 | Current provisions applicable to HFC does not contain any restrictions relating to double financing. | HFCs exposure to the below mentioned activity shall be mutually exclusive: 1. Group company in real estate business or 2. Lend to retail individual home buyers in the project of group entitiesAny direct or indirect exposure in group entity shall be limited 15% of owned funds for a single entity in the group and 25% of owned fund for all such group entities. As regards to extending of loans to individuals, who chose to buy housing units from entities in the group, Arm’s length principle shall be followed in letter and spirit |

The proposition is that HFC can either undertake an exposure on the group company in real estate business or lend to retail individual home buyers in the projects of group entities, but not do both. The laguage of the notification is not very clear that it is referrring to internal group or external group as well- our view is that the restriction should not be just for internal group but also for external group.

Further, the limit on ‘Group Exposure’ seems to include both housing and non-housing loans to such group entity. Also, the limits are more stringent than the existing concentration norms, which provide the limit for lending and investment of upto 25% of the owned fund to a single party and 40% of its owned fund to a single group of parties. There is an exemption in the existing concentration norms for investment and lending to group comanies to the extent it has been reduced from the owned funds. Hence, the limit of 15% and 25% may not be relvant if the HFC has already knocked off the exposure from its owned funds. This must be clarified by the RBI. Since, the intent is to stop double finance that is to say ongoing exposure should not be there on both- in case funding has been extended to the builder then already the flat is funded, however, after construction once the loan is repaid by the builder, the individual may be given loan for the flat- this should not be regarded as double financing. In case of loans to individual, the HFC must satisfy the arms’ length requirement for retail loans to group’s customers. This mutual exclusion clause does not seems to apply to companies outside group and their retail customers – but in case the intent is to bar double financing, the external group companies must also be included. |

| Monitoring of frauds | |||

| 9 | Applicable as per NHB policy circular No. 92 dated February 05, 2019 | Applicable as per Master Direction – Monitoring of Frauds in NBFCs (Reserve Bank) Directions, 2016. | HFCs should comply with the master directions for monitoring of frauds, however all reports in the formats given in Master Directions may continue to be forwarded to NHB, New Delhi. |

| 10 | Chapter IV para 2 – Frauds committed by unscrupulous borrowers: Frauds committed by unscrupulous borrowers including companies, partnership firms/proprietary concerns and/or their directors/partners, Group of Associations, Trusts etc. by various methods including the following: (a) Diversion of funds outside the borrowing units, (b) lack of interest or criminal neglect on the part of borrowers, their partners, etc., (c) due to managerial failure leading to the unit becoming sick and due to laxity in effective supervision over the operations in borrowal accounts on the part of the HFC functionaries rendering the advance difficult of recovery. |

As per Master Directions: Frauds committed by unscrupulous borrowers including companies, partnership firms/proprietary concerns and/or their directors/partners by various methods including the following: (a) Fraudulent discount of instruments; (b) Fraudulent removal of pledged stocks/disposing of hypothecated stocks without the NBFCs knowledge/inflating the value of stocks in the stock statement and drawing excess finance; (c) Diversion of funds outside the borrowing units, lack of interest or criminal neglect on the part of borrowers, their partners, etc. and also due to managerial failure leading to the unit becoming sick and due to laxity in effective supervision over the operations in borrowal accounts on the part of the NBFC functionaries rendering the advance difficult of recovery. |

Same as earlier. However, additionally the following 2 points would be henceforth applicable: (a) Fraudulent discount of instruments; (b) Fraudulent removal of pledged stocks/disposing of hypothecated stocks without the NBFCs knowledge/inflating the value of stocks in the stock statement and drawing excess finance. |

| 11 | Chapter VI para 2(iii) – Quarterly Review of Frauds: All the frauds involving an amount of INR. 50 lakh and above should be monitored and reviewed by the Audit Committee of the Board of HFCs. The periodicity of the meetings of the Committee may be decided according to the number of cases involved. However, the Committee should meet and review as and when a fraud involving an amount of INR. 50 lakh and above comes to light. |

As per Master Directions:

All the frauds involving an amount of INR 1 crore and above should be monitored and reviewed by the Audit Committee of the Board (ACB) of NBFCs. The periodicity of the meetings of the Committee may be decided according to the number of cases involved. However, the Committee should meet and review as and when a fraud involving an amount of INR 1 crore and above comes to light. |

Limit of INR 50 lakh would be increased to INR 1 crore as per Master Directions. |

| 12 | Chapter – VII – Provisioning Pertaining to Fraud Accounts | No such provisioning requirement under master directions. | The Master directions as applicable to NBFCs do not provide for any specific provisioning requirement pertaining to the account classifed as fruad. |

| Information Technology Framework | |||

| 14 | As per NHB policy circular No. 90 dated June 15, 2018: Information Technology framework for HFCs is categorised into 2 parts: Section A – For public deposit accepting HFCs and HFCs not accepting public deposit with asset size INR 100 crore and above; Section B – HFCs not accepting public deposit with asset size below INR 100 crore. |

As provided under Master Direction – Information Technology Framework for the NBFC Sector where:

Section A would apply to Systemically important HFCs; |

Currently applicability of IT framework for HFCs is segregated based on asset size of INR 100 crores. However, henceforth the applicability would be based on asset size of INR 500 crores, i.e. by segregating HFCs into systemically and non-systemically important category. |

| 15 | Para 5.4 – Periodicity of IS Audit: The periodicity of IS audit should ideally be based on the size and operations of the HFC but may be conducted at least once in two years. |

As per Master Directions – The periodicity of IS audit should ideally be based on the size and operations of the HFC but may be conducted at least once in a year. | All HFCs would be required to conduct IS audit at least once in a year as per Master Directions. This however is recomendatory. |

| Securitization | |||

| 16 | No guidelines prescribe by NHB | Provisions of Annex XXII of NBFC-ND-SI Directions, 2016 shall be extended to cover the HFCs | In the absence of any specific guidelines, the HFCs were already complying with the RBI guidelines on securitization and direct assignment. This would avoid any confusion in terms of the applicability of the securitisation guidelines. However, the existing RBI guidelines are also proposed to undergo amendments |

| Lending against Shares | |||

| 17 | Under the current ambit of HFC provisions there are no guidelines in place for lending against the security of shares by HFCs | Provisions as specified in Para 22 of NBFC-ND-SI Directions, 2016 shall mutatis mutandis be applicable to the HFCs | HFCs would be required to comply with the following while lending against shares: 1. Maintain Loan to Value (LTV) ratio of 50% at all times. Any shortfall would require to be made good within 7 working days. 2. In case where lending is being done for investment in capital markets, accept only Group 1 securities as collateral for loans of value more than INR 5 lakh. 3. Report on-line to stock exchanges on a quarterly basis, information on the shares pledged in their favour, by borrowers for availing loans in format as given in Annex V of Master Directions.. |

| Managing Risks and Code of Conduct in Outsourcing of Financial Services | |||

| 18 | There are no guidelines have been prescribed for HFCs with regard to outsourcing of Financial Services | Provisions of Annex XXV of NBFC-ND-SI Directions, 2016 shall be extended to cover the HFCs | HFCs will have to comply with the guidelines for outsourcing of financial services |

| Foreclosure charges | |||

| 19 | As per NHB policy circular No. 36 dated October 18, 2010 and NHB policy circular No. 43 dated October 19, 2011

HFCs should not charge pay-payment levy or penalty on pre-closure of housing loans under the following situations. 1. Where the housing loan is on floating interest rate basis and the loan is preclosed through any source. |

No foreclosure charges/prepayment penalties shall be levied on any floating rate term loan sanctioned for purposes other than business to individual borrowers with or without co-obligants. It is proposed to extend these instructions to HFCs. | There are no regulations prescribed for HFCs for not levying the foreclosure charge for non-housing loans such as in case of term loans availed for other than business purpose. Hence, it is proposed to extend these instructions to HFCs as well. This would ensure uniformity with regard to repayment of various term loans by borrowers. Though the language is not very clear and hence, it seems that the foreclosure charges shall be waived off for all floating rate term loans to individual borrowers, including housing loans as well. |

| Implementation of Indian Accounting Standards | |||

| 20 | NBFCs as covered in rule 4 of the Companies (Indian Accounting Standards) Rules, 2015 are required to comply with IndAS.

As per the Rule 2(1)(g) of the above mentioned rules, all the HFCs are covered under the definition of NBFCs thereby required to comply with IndAS. The RBI has also provided guidance on implementation of Indian Accounting Standards by NBFCs (including HFCs). |

RBI instructions issued vide circular dated 13th March, 2020 on implementation of IndAS to be extended to HFCs | The RBI circular was applicable to NBFCs as covered in rule 4 of the Companies (Indian Accounting Standards) Rules, 2015 which already includes HFCs under the definition of NBFCs.

However, there was confusion wrt its applicability on HFCs. The proposed change further clarifies the applicability of the said RBI circular to HFCs. Our write-up on implementation of IndAs for NBFCs may alos be refereed here– https://vinodkothari.com/2020/03/guidance-on-implementation-of-ind-as-by-nbfcs/ |

Our other write-ups may be viewed here: