HFC Regulations Harmonised with NBFC Regime

-Anita Baid (anita@vinodkothari.com)

Introduction

In 2019, pursuant to the amendments proposed by the Finance Act, 2019, it was proposed to shift the regulations of Housing Finance Companies (HFCs) from National Housing Bank (NH) to the Reserve Bank of India (RBI). Further, the RBI had in its press release[1] stated that HFCs will be treated as one of the categories of Non-Banking Financial Companies (NBFCs) for regulatory purposes with effect from August 09, 2019. It was expected that the RBI shall carry out a review of the extant regulatory framework applicable to HFCs and come out with revised regulations in due course, and till such time HFCs shall continue to comply with the directions and instructions issued by NHB.

In this regard, the RBI has undertaken a review and has identified a few changes which are proposed to be prescribed for HFCs[2]. While certain guidelines in the NBFC Master Directions is proposed to be made straight away applicable to HFCs, in some other cases, changes have been proposed to ensure a seamless shift in the regulations. Most of these regulations are not new to the world at large, banks and NBFCs are already complying with the guidelines issued by the RBI on similar lines. The scope has now been extended to include HFCs under its ambit.

Some of the major changes proposed by the new regulator have been discussed herein below-

Defining the phrase ‘providing finance for housing’ or ‘housing finance’

The NHB Directions defined the term “housing finance company” [section 2(d)] as a company incorporated under the Companies Act, 1956 which primarily transacts or has as one of its principal objects, the transacting of the business of providing finance for housing, whether directly or indirectly. However, the term ‘providing finance for housing’ or ‘housing finance’ was not formally defined. It has been proposed to define the said terms to mean financing, for purchase/ construction/ reconstruction/ renovation/ repairs of residential dwelling units. Further, an illustrative list has been provided to determine the loans that would fall under the category of housing finance.

There was a NHB Circular dated September 26, 2011[3] which provided an illustrative list of loans which can be classified as housing/ non housing loans. The comparative table showing the difference is provided herein below:

| Illustrative list prescribed in 2011 | Proposed list of ‘Qualifying Asset’ |

| a. Loans to individuals or group of individuals including co-operative societies for construction/ purchase of new dwelling units.

b. Loans for purchase of old dwelling units. c. Loans to individuals for purchasing old/new dwelling units by mortgaging existing dwelling units. d. Loans for purchase of plots for construction of residential dwelling units provided a declaration is obtained from the borrower that he intends to construct a house on the said plot, with the help of bank/HFC finance or otherwise, within a period of three years from the availment of the said loan. e. Loans for renovation/ reconstruction of existing dwelling units. f. Lending to professional builders for construction of residential dwelling units. g. Lending to public agencies including state housing boards for construction residential dwelling units. h. Loans to corporates/ Government (through loans for employee housing) i. Loans for construction of educational, health, social, cultural or other institutions/ centers, which are part of a housing project and which are necessary for the development of settlements or townships; j. Loans for shopping complexes, markets and such other centers catering to the day to day needs of the residents of the housing colonies and forming part of a housing project; k. Loans for construction meant for improving the conditions in slum areas for which credit may be extended directly to the slum-dwellers on the guarantee of the Government, or indirectly to them through the State Governments; l. Loans given for slum improvement schemes to be implemented by Slum Clearance Boards and other public agencies; m. Loans provided to the bodies constituted for undertaking repairs to houses; n. Investment in the guarantee/non-guaranteed bonds and debentures of NHB/HUDCO in the primary market, provided investment in non-guaranteed bonds is made only if guaranteed bonds are not available |

a. Loans to individuals or group of individuals including co-operative societies for construction/ purchase of new dwelling units.

b. Loans to individuals for purchase of old dwelling units. c. Loans to individuals for purchasing old/ new dwelling units by mortgaging existing dwelling units. d. Loans to individuals for purchase of plots for construction of residential dwelling units provided a declaration is obtained from the borrower that he intends to construct a house on the plot within a period of three years from the date of availing of the loan. e. Loans to individuals for renovation/ reconstruction of existing dwelling units. f. Lending to public agencies including state housing boards for construction of residential dwelling units. g. Loans to corporates/ Government agencies (through loans for employee housing). h. Loans for construction of educational, health, social, cultural or other institutions/centres, which are part of housing project in the same complex and which are necessary for the development of settlements or townships; i. Loans for construction of houses and related infrastructure within the same area, meant for improving the conditions in slum areas for which credit may be extended directly to the slum-dwellers on the guarantee of the Government, or indirectly to them through the State Governments; j. Loans given for slum improvement schemes to be implemented by Slum Clearance Boards and other public agencies; k. Lending to builders for construction of residential dwelling units |

The proposed list is similar to the illustrative list prescribed by NHB earlier. However, the list prescribed as ‘qualifying asset’ for HFCs seems to focus more on individual borrowers. It has also excluded the following-

- Loans for shopping complexes, markets and such other centers catering to the day to day needs of the residents of the housing colonies and forming part of a housing project

- Loans provided to the bodies constituted for undertaking repairs to houses;

- Investment in the guarantee/non-guaranteed bonds and debentures of NHB/HUDCO in the primary market, provided investment in non-guaranteed bonds is made only if guaranteed bonds are not available

Specifically, loans given for furnishing dwelling units, loans given against mortgage of property for any purpose other than buying/ construction of a new dwelling unit/s or renovation of the existing dwelling unit/s, have been regarded as non-housing loans. This was mentioned in the 2011 circular as well.

The idea behind laying out the periphery of ‘housing loans’ is to ensure consistency and certainty in ‘principality’ of business of the HFCs. Only such loans, which “qualify” as “housing loans” would be treated as “qualifying assets” for the purpose of determining “principality” of business of the entity, as we see below.

An entity which falls short of such qualifying assets below 50% cannot be regarded as HFC. This provision is also expected to minimise the practice of giving mortgage loans (LAP-type loans) by HFCs, which would often be granted to meet working capital requirements, etc. of other entities and not for housing purposes; thereby restricting the portfolio deviations of the HFC. The specific definition of housing finance would avoid confusion and ensure better governance as well as reporting for HFCs.

Defining principal business and qualifying assets

The amendment to section 29 A of the NHB Act vide Finance Act, 2019 provided as follows:

(1) Notwithstanding anything contained in this Chapter or in any other law for the time being in force, no housing finance institution which is a company shall commence housing finance as its principal business or carry on the business of housing finance as its principal business without—

(a) obtaining a certificate of registration issued under this Chapter; and

(b) having the net owned fund of ten crore rupees or such other higher amount, as the Reserve Bank may, by notification, specify.

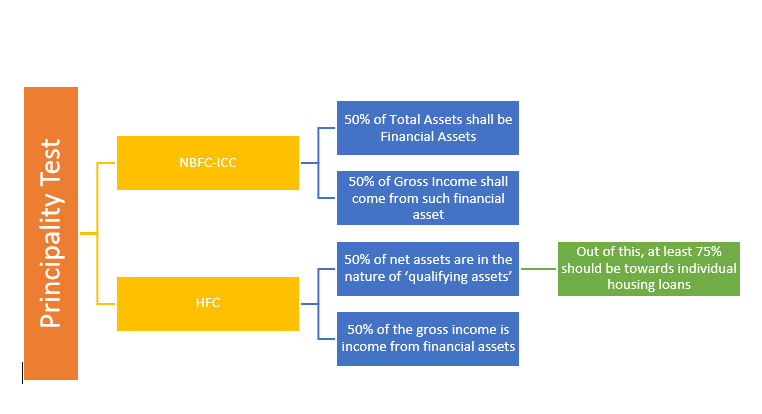

Prior to the amendment in Finance Act, the term ‘principal business’ was not referred in NHB Act. Further, for the purposes of registration, NHB was recognizing companies as HFCs if such company had, as one of its principal objects, transacting of the business of providing finance for housing (directly or indirectly). With the aforesaid amendment to NHB Act, there was a need to define the term ‘principal business’ for HFCs. The principal business criteria for NBFCs is well known- an NBFC must have financial assets more than 50% of its total assets and income from financial assets must be more than 50% of the gross income. The same has been proposed to be extended to HFCs as well along with the concept ‘qualifying assets’ which would mean asset qualifying as ‘housing finance’ or ‘providing finance for housing’

The principality test for HFCs has been proposed as follows (both these tests are required to be satisfied as the determinant factor for principal business):

- Not less than 50% of net assets are in the nature of ‘qualifying assets’ of which at least 75% should be towards individual housing loans as prescribed. Here, net assets shall mean total assets other than cash and bank balances and money market instruments

- Not less than 50% of the gross income is income from financial assets

The RBI has also proposed the following timeline for achieving the aforesaid principality:

| Timeline | At least 50% of net assets as qualifying assets i.e., towards housing finance | At least 75% of qualifying assets towards housing finance for individuals |

| March 31, 2022 | 50% | 60% |

| March 31, 2023 | – | 70% |

| March 31, 2024 | – | 75% |

The concept of ‘qualifying asset’ is similar to that in case of NBFC-MFIs wherein they are specifically focused on micro lending. Though in spirit the HFCs would primarily focus on housing loans only however, the HFCs offering home loans along with other related products would now be required to maintain the principality of individual housing loans. Further, the requirement of minimum concentration towards ‘individuals’ is a new concept and possibly to protect the HFCs from systemic exposures. Though the guidelines do not intend to prohibit the HFCs from providing non-housing loans, however, it limits the same. The remaining 50% can be extended in the form of non-housing loans, including LAP. An HFC which falls short of such qualifying asset criteria has to get registration as NBFC-ICC and consequentially, all laws applicable to such NBFC-ICC shall apply to the HFC.

Classifying HFCs into SIs and NSIs

At present, HFC regulations are common for all HFCs irrespective of their asset size and ownership. It is proposed to issue HFC regulations by classifying them as systemically important and non-systemically important.

- Non-deposit taking HFCs (HFC-ND) with asset size of ₹500 crore & above and all deposit taking HFCs (HFCD), irrespective of asset size, will be treated as systemically important HFCs-

- The larger HFCs may continue with existing regulations under NHB regulations or be harmonised with NBFC-SI regulations

- However, there are separate regulations for deposit taking NBFCs which might become applicable on deposit taking HFCs as well

- Non-deposit taking HFCs with asset size below ₹500 crore will be treated as non-systemically important HFCs (HFC-non-SI)-

- For the non-systemically important HFCs, it is proposed to bring the regulations at par with Master Directions for NBFC-ND-non-SI

The existing regulations for HFCs are similar to NBFCs. The intention is to bring the non-systemically important HFCs at par with NBFC-NSI and hence, the applicability of the existing Master Directions for NBFC-ND-NSI can be extended to HFC-non-SI as well.

Minimum Net Owned Fund (NOF)

It is proposed to increase the minimum NOF for HFCs from the current requirement of ₹10 crore to ₹20 crore. For existing HFCs the glide path would be to reach ₹15 crore within 1 year and ₹20 crore within 2 years.

The increased capital requirement is to strengthen the capital base of the HFCs. However, as compared to an NBFC the NOF requirement is very high. The registration requirement for both NBFC-ICC and HFC will also be the same, since both will have to apply to the RBI.

An important question that will arise here is that why should an entity register as an HFC- given the fact that even an NBFC-ICC can extend housing loan, one would have to consider the various factors to carry on housing finance as a principle activity under an HFC or non-principal activity under an NBFC-ICC. As per the provisions of section 29A and 2(d) of the NHB Act (mentioned earlier) read along with the RBI guidelines issued in this regard, an HFC will have to satisfy the principality of 50% housing loans as well as 75% loans to individuals.

Double Financing

In order to address concerns on double financing due to lending to construction companies in the group and also to individuals purchasing flats from the latter, it is proposed to provide the option to the concerned HFC to choose to lend only at one level. The proposition is that HFC can either undertake an exposure on the group company in real estate business or lend to retail individual home buyers in the projects of group entities, but not do both. The language of the notification is not very clear that it is referring to internal group or external group as well, however, it seems that the restriction should not be just for internal group but also for external group.

In case the HFC decides to take any exposure in its group entities (lending and investment) directly or indirectly, such exposure cannot be more than

- 15 per cent of owned fund for a single entity in the group and

- 25 per cent of owned fund for all such group entities.

The aforesaid limit on ‘Group Exposure’ seems to include both housing and non-housing loans to such group entity. Also, the limits are more stringent than the existing concentration norms, which provide the limit for lending and investment of upto 25% of the owned fund to a single party and 40% of its owned fund to a single group of parties. There is an exemption in the existing concentration norms for investment and lending to group companies to the extent it has been reduced from the owned funds. Hence, the limit of 15% and 25% may not be relevant if the HFC has already knocked off the exposure from its owned funds. This must be clarified by the RBI.

Since, the intent is to stop double finance that is to say ongoing exposure should not be there on both- in case funding has been extended to the builder then already the flat is funded, however, after construction once the loan is repaid by the builder, the individual may be given loan for the flat- this should not be regarded as double financing.

As regards to extending loans to individual, it is required that the HFC must satisfy the arms’ length requirement for retail loans to group’s customers. However, this mutual exclusion clause does not seems to apply to companies outside group and their retail customers – but in case the intent is to bar double financing, the external group companies must also be included.

Foreclosure Charges

In case of NBFCs, no foreclosure charges/pre-payment penalties is levied on any floating rate term loan sanctioned for purposes other than business to individual borrowers with or without co-obligors.

In case of HFCs, the foreclosure penalty is waived off in case of housing loans depending on the category of borrower and the source of funds for prepayment. The probable scenarios are provided herein below:

| Rate of Interest | Borrower/ Co-borrower | Source of pre-closure funding | Levy of foreclosure

charges / prepayment penalty |

| Fixed*

|

Individual | Own source ** | No |

| Borrowed Funds | Yes | ||

| HUF/Sole Proprietor/Company/Firm | Own source ** | No | |

| Borrowed Funds | Yes | ||

| Floating | Individual | Own source ** | No |

| Borrowed Funds | |||

| HUF/Sole Proprietor/Company/Firm | Own source ** | Yes | |

| Borrowed Funds | |||

| Dual Rate/ Special Rate

(Combination of fixed and floating) |

Individual | Own source ** | Pre-closure norms applicable to fixed/floating rate shall apply depending on whether at the time of pre-closure, the loan is on fixed or floating rate.

|

| Borrowed Funds | |||

| HUF/Sole Proprietor/Company/Firm | Own source ** | ||

| Borrowed Funds |

*Fixed rate loan is one where the rate is fixed for the entire tenure of the loan.

**The expression “own sources” for the purpose means any source other than by borrowing from a bank/HFC/NBFC and/or a financial institution.

There are no regulations prescribed for HFCs for not levying the foreclosure charge for non-housing loans such as in case of term loans availed for other than business purpose. Hence, it is proposed to extend these instructions to HFCs as well. This would ensure uniformity with regard to repayment of various term loans by borrowers. Though the language is not very clear and hence, it seems that the foreclosure charges shall be waived off for all floating rate term loans to individual borrowers, including housing loans as well.

Other provisions to be made applicable to HFCs

- It is proposed to align the definitions of capital (both Tier I and Tier II) of HFCs with that of NBFCs. It is proposed to align the definitions of capital (both Tier I and Tier II) of HFCs with that of NBFC, specifically PDIs shall form part of HFCs capital (both Tier I and Tier II) component on the same lines as NBFCs. However, with the following differences-

- PDIs shall be treated as Tier I/ Tier II capital only by HFCs-ND-SI

- PDIs or any other debt capital instrument in the nature of PDIs already issued by HFCs-D and HFCs-non-SI shall be reckoned as Tier I/Tier II for a period not exceeding 3 year

Further, since HFCs are treated as a category of NBFCs for regulatory purposes, investments in shares of other HFCs and also in other NBFCs (whether forming part of group or not), shall be reduced from the Tier I capital to the extent it exceeds, in aggregate along with other exposures to group companies, ten per cent of the owned fund of HFC.

- It is proposed to align the definition of public deposit as given under RBI Master Direction with an addition that any amount received by HFCs from NHB or any public housing agency shall also be exempt from the definition of public deposit.

- It is proposed to extend the Liquidity Risk Management (LRM) guidelines to all non-deposit taking HFCs with asset size of ₹100 crore & above and all deposit taking HFCs. There is however, no mention about the applicability of LCR framework. It seems that the same shall also be extended to HFCS with asset size of ₹5000 crore or more in a phased manner. The LRM framework was recently introduced for NBFCs in November, 2019[4] and the extension to HFCs would require similar actionable.

- It is proposed to make the fraud reporting directions applicable to HFCs in place of present guidelines issued by NHB. However, the reporting requirement shall continue to be submitted to the NHB itself. The limits for quarterly review by Audit Committee would also be revised to that applicable on NBFCs, that is, ₹1crore as against the existing ₹50 lacs for HFCs.

- It is proposed that the Information Technology (IT) Framework for NBFCs shall be extended to HFCs and the existing guidelines issued by NHB in this regard would be withdrawn. The existing IT framework for HFCs were categorised into two parts- for public deposit accepting HFCs and HFCs not accepting public deposit with asset size Rs. 100 crore and above; and for HFCs not accepting public deposit with asset size below Rs. 100 crore. However, the proposed applicability of IT framework would be on the basis of classification as systemically important or non-systemically important HFC.

- It is proposed to bring all HFCs (systemically important and non-systemically important) under the ambit of guidelines on securitisation transaction as applicable to NBFCs, which is proposed to undergo amendments. In the absence of any specific guidelines, the HFCs were already complying with the RBI guidelines on securitization and direct assignment. This would avoid any confusion in terms of the applicability of the securitisation guidelines.

- It is proposed to extend instructions applicable to NBFCs to lend against the collateral of listed shares to HFCs as well, who do not have any guidelines in this regard at present.

- It is proposed to extend the guidelines with regard to outsourcing of Financial Services for NBFCs, to all HFCs.

- It has been proposed that the RBI instructions on Implementation of Indian Accounting Standards will be extended to HFCs. The RBI circular was applicable to NBFCs as covered in rule 4 of the Companies (Indian Accounting Standards) Rules, 2015 which already includes HFCs under the definition of NBFCs. However, there was confusion wrt its applicability on HFCs. The proposed change further clarifies the applicability of the said RBI circular to HFCs.

Harmonizing the regulations

There are certain major differences between extant regulations of the HFCs and that for NBFCs. It is being proposed to harmonise these regulations in a phased manner over a period of two to three years:

- Capital requirements (CRAR and risk weights)

The minimum CRAR prescribed for HFCs currently is 12% and which was to be progressively increased to 14% by March 31, 2021 and to 15% by March 31, 2022. Further, the risk Review of extant regulatory framework for Housing Finance companies (HFCs) weights for assets of HFCs are in the range of 30% to 125% based on asset classification, LTV, type of borrower, etc. However, for NBFCs, the minimum CRAR is 15% and risk weights are broadly under 0%, 20% and 100% categories.

- Income Recognition, Asset Classification and Provisioning (IRACP) norms

The major differences in provisioning norms applicable to standard, substandard and doubtful assets in HFCs’ books. In case of standard loans, the HFCs are required to create a provision ranging from 0.4% to 2% and for substandard the requirement is 15%, whereas, in case of NBFC-ND-SI, the provision is 0.4% for standard and 10% for sub-standard.

- Norms on concentration of credit / investment

The credit concentration norms for NBFCs and HFCs are similar. NBFCs enjoy certain exceptions in this regard which was also introduced for HFCs in 2018.

- Limits on exposure to Commercial Real Estate (CRE) & Capital Market (CME)

The limits prescribed for HFCs for exposure to CRE by way of investment in land & building shall not be more than 20% of capital fund and for CME shall not be more than 40% of net worth total exposure of which direct exposure should be 20% of net worth. However, there are no limits prescribed for NBFCs.

- Regulations on acceptance of Public Deposits

- Period of public deposit (12 months to 120 months for HFCs against 12 months to 60 months for NBFCs),

- Ceiling on quantum of deposit (3 times of NOF for HFCs against 1.5 times for NBFCs with minimum investment grade rating),

- Interest on premature repayment of deposits (ranging from 1% to 4% below prescribed rate for HFCs as against 2% to 3% below prescribed rate for NBFCs depending upon duration and prescription of rate),

- Maintenance of liquid assets (13% for HFCs against 15% for NBFCs), etc.

Conclusion

Though HFCs are now another form of NBFCs, the RBI draft proposes to carve out a slightly separate set of rules for the HFCs in certain cases. Further, the proposed harmonisation of regulations will be done over a period of two years and till such time the HFCs will follow the extant NHB norms. Thus enabling the HFCs a breather period and to ensure seamless transition.

Other relevant articles-

- https://vinodkothari.com/2018/06/it-framework-for-the-hfcs/

- https://vinodkothari.com/wp-content/uploads/Corporate_Governance_Standards_for_HFCs.pdf

[1] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=47871

[2] https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/HFC7B2AB6B6997544B88136D80AC3C094F9.PDF

[3] https://www.nhb.org.in/Regulation/polcir-41.pdf

[4] Our snapshot on the same can be read here- https://vinodkothari.com/wp-content/uploads/2019/11/Liquidity-risk-framework.pdf

A point by point comparative of the existing in proposed guidelines may be viewed here:

Will customer get benefit like reduction on rate of interest in there existing home loan? Pls check and update?

Good analysis

If a HFC subsidiary merges with its NBFC parent subsidiary will risk weights be calculated as per NBFC norms or HFC norms

We understand that post merger, the resultant entity shall be registered as an NBFC and hence the risk weights must be as per the applicable NBFC norms.

Thanks

In the proposed test of principality for HFCs, at least 50% of net assets should be in the nature of qualifying assets (housing loans), out of which at least 75% should be towards individual housing loans. What if the company has 100% of its net assets as qualifying assets?

The principality test proposed for HFCs requires the companies to maintain a minimum threshold. Accordingly, an HFC would need to have a minimum of 37.5% (75% of 50%) of its portfolio as individual loans. In the given case, although the company has 100% of its net assets as qualifying assets, the principality test prescribes the minimum criteria, which requires to maintain at least 50% as housing loans and out of that 75% towards individual housing loans. For example, let us consider that an HFC has net assets of Rs. 100 crores and all are qualifying assets, i.e. 100%, in such a case, it will be required to maintain a minimum of Rs. 37.5 crores (75% of 50% of 100 crores) towards individual housing.

Fantastic comparison …. you have got awesome team to explain each and every regulatory matter in very clear language.

thank you