RBI amends mode of payment and remittance norms for units of Investment vehicles

Permits FPIs and FVCIs to use Special Non-Resident Rupee (SNRR) account

CS Burhanuddin Dohadwala| Manager, Aanchal Kaur Nagpal| Executive

corplaw@vinodkothari.com

The Reserve Bank of India (‘RBI’) vide notification dated October 17, 2019 had notified the Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt instrument) Regulations, 2019[1] (‘the Regulations’) governing the mode of payment and reporting of non-debt instruments consequent to the Foreign Exchange Management (Non-Debt Instrument) Rules, 2019[2] framed by the Ministry of Finance, Central Government.

RBI has recently vide its notification dated June 15, 2020 notified Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt Instruments) (Amendment) Regulations, 2020[3] amending Reg. 3.1 dealing with Mode of Payment and Remittance of sale proceeds in case of investment in investment vehicles.

Let us discuss few terms to understand the recent amendments to the Regulations.

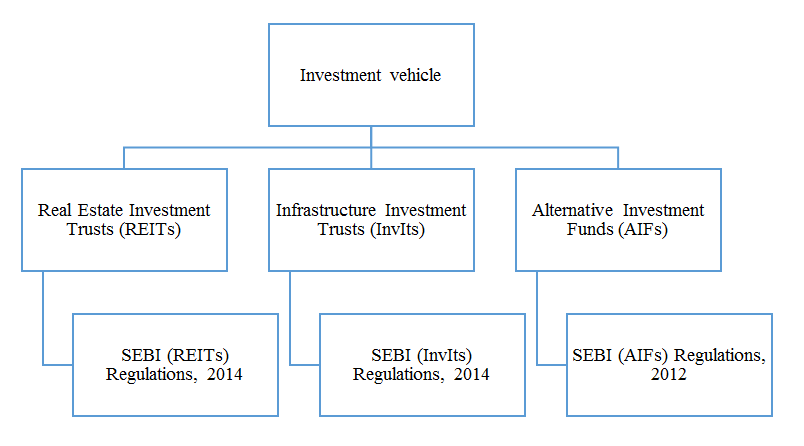

Investment Vehicles under FEMA:

According to FEMA (Non-Debt Instruments) Rules, 2019, investment vehicles mean:

Different types of account available under FEMA (Deposit) Regulations, 2016[1] (‘Deposit Regulations’)

The following are the major accounts that can be opened in India by a non-resident:

| Particulars | Eligible Person |

| Non-Resident (External) Rupee Account Scheme-NRE Account |

Non-resident Indians (NRIs) and Person of Indian Origin (PIOs) |

| Foreign currency (Non-Resident) account (Banks) scheme – FCNR (B) account | |

| Non-Resident ordinary rupee account scheme-NRO account |

Any person resident outside India. |

| Special Non-Resident Rupee Account – SNRR account |

Any person resident outside India. |

A significant advantage of SNRR over NRO is that the former is a repatriable account while the latter is non-repatriable.

What is Special Non-Resident Rupee (‘SNRR’) Account?

Any person resident outside India, having a business interest in India, may open SNRR account with an authorised dealer for the purpose of putting through bona fide transactions in rupees. The business interest, apart from generic business interest, shall include the following INR transactions, namely:-

- Investments made in India in accordance with Foreign Exchange Management (Non-debt Instruments) Rules, 2019 dated October 17, 2019 and Foreign Exchange Management (Debt Instruments)

- Import of goods and services in accordance with Section 5 of the Foreign Exchange Management Act 1999 Regulations, 2019;

- Export of goods and services in accordance with Section 7 of the Foreign Exchange Management Act 1999;

- Trade credit transactions and lending under External Commercial Borrowings (ECB) framework;

- Business related transactions outside International Financial Service Centre (IFSC) by IFSC units at GIFT city like administrative expenses in INR outside IFSC, INR amount from sale of scrap, government incentives in INR, etc;

Rationale behind the amendment:

Position under Master Direction – Foreign Investment in India by RBI

According to Annex 8 of Master Direction – Foreign Investment in India by RBI, investment made by a PROI was permitted with effect from 13th September, 2016. The provisions specify that the amount of consideration of the units of an investment vehicle should be paid out of funds held in NRE or FCNR(B) account maintained in accordance with the Deposit Regulations as one of the modes of payment.

Further it also specifies that the sale/ maturity proceeds of the units may be remitted outside India or credited to the NRE or FCNR(B) account of the person concerned.

Position under the erstwhile provisions of the Regulations

Schedule II of the Regulations (Investments by FPIs) stated earlier that of units of investment vehicles other than domestic mutual fund may be remitted outside India.

However, balances in SNRR account were permitted to be used for making investment only in units of domestic mutual fund and not in Investment Vehicles.

As discussed above, the NRO account is a non-repatriable account while the SNRR account is a repatriable account. Due to the above provisions, investment in Investment Vehicles could not be transferred to the SNRR account for repatriation resulting in ambiguity.

Owing to the above and to increase the inflow of foreign investment, the Government has amended the said provision and allowed FPIs & FVCI to invest in listed or to be listed units of Investment vehicle.

Brief comparison of the pre and post amendment is covered in our Annexure I.

Annexure-I

Comparison of the pre and post amendment

| Schedule | Post amendment | Prior to amendment | Remarks |

| Schedule II w.r.t Investments by Foreign Portfolio Investors | A. Mode of payment

1. The amount of consideration shall be paid as inward remittance from abroad through banking channels or out of funds held in a foreign currency account and/ or a Special Non-Resident Rupee (SNRR) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016.

2. Unless otherwise specified in these regulations or the relevant Schedules, the foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule.

|

A. Mode of payment

1. The amount of consideration shall be paid as inward remittance from abroad through banking channels or out of funds held in a foreign currency account and/ or a Special Non-Resident Rupee (SNRR) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016. Provided balances in SNRR account shall not be used for making investment in units of Investment Vehicles other than the units of domestic mutual fund. 2. The foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule.

|

The erstwhile provisions restricted use of SNRR account balance for making investments in investment vehicles other than mutual funds.

As a result FPIs could not use their SNRR account and had to resort to other types of accounts for investment in investment vehicles such as REITs, and InViTs. The recent amendment has removed this restriction. The amendment has been made to provide for the amendment made in Schedule VIII dealing with Investment by a person resident outside India in an Investment Vehicle. |

| B. Remittance of sale proceeds

The sale proceeds (net of taxes) of equity instruments and units of REITs, InViTs and domestic mutual fund may be remitted outside India or credited to the foreign currency account or a SNRR account of the FPI. |

B. Remittance of sale proceeds

The sale proceeds (net of taxes) of equity instruments and units of domestic mutual fund may be remitted outside India or credited to the foreign currency account or a SNRR account of the FPI. The sale proceeds (net of taxes) of units of investment vehicles other than domestic mutual fund may be remitted outside India. |

To align with the amendment made in Schedule VIII dealing with Investment by a person resident outside India in an Investment Vehicle. | |

| Schedule VII w.r.t Investment by a Foreign Venture Capital Investor (FVCI) | For Para A(2):

Unless otherwise specified in these regulations or the relevant Schedules, the foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule. |

For Para A(2):

The foreign currency account and SNRR account shall be used only and exclusively for transactions under this Schedule. |

The insertion has been made to align with the amendments proposed in Schedule VIII dealing with Investment by a person resident outside India in an Investment Vehicle. |

| Schedule VIII w.r.t Investment by a person resident outside India in an Investment Vehicle | A. Mode of payment:

The amount of consideration shall be paid as inward remittance from abroad through banking channels or by way of swap of shares of a Special Purpose Vehicle or out of funds held in NRE or FCNR(B) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016. Further, for an FPI or FVCI, amount of consideration may be paid out of their SNRR account for trading in units of Investment Vehicle listed or to be listed (primary issuance) on the stock exchanges in India. |

A. Mode of payment:

The amount of consideration shall be paid as inward remittance from abroad through banking channels or by way of swap of shares of a Special Purpose Vehicle or out of funds held in NRE or FCNR(B) account maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016. |

Further, it is clarified that the SNRR account may be used for trading in units of listed as well as to be listed units of investment vehicles and the sale/ maturity proceeds can be credited to the said account. |

| B. Remittance of Sale/maturity proceeds:

The sale/ maturity proceeds (net of taxes) of the units may be remitted outside India or may be credited to the NRE or FCNR(B) or SNRR account, as applicable of the person concerned. |

B. Remittance of sale/maturity proceeds

The sale/maturity proceeds (net of taxes) of the units may be remitted outside India or may be credited to the NRE or FCNR(B) account of the person concerned. |

Link to our other articles:

Introduction to FEMA (NDI) Rules, 2019 and recent amendments:

https://vinodkothari.com/2020/04/introduction-to-fema-ndi-rules-2019-and-recent-amendments/

RBI rationalises operation of Special Non-Resident Rupee A/c:

https://vinodkothari.com/wp-content/uploads/2019/11/RBI-rationalises-operation-of-SNRR-Account.pdf

[1] https://vinodkothari.com/wp-content/uploads/2019/11/RBI-rationalises-operation-of-SNRR-Account.pdf

[1] http://egazette.nic.in/WriteReadData/2019/213318.pdf

Leave a Reply

Want to join the discussion?Feel free to contribute!