An AIF raises capital by issuance of units, which are privately placed. Most AIFs follow a commitment–drawdown model, under which investors agree upfront to commit a specified amount of capital (‘committed capital’). The AIF manager then calls this committed capital, either in full or in tranches, as investment opportunities arise (‘drawdown’). This model helps the AIF to minimise the negative carry that would result from raising investments which are yet to be invested.

This fund-raising process is shaped not only by SEBI’s AIF framework but also by the oversight of the respective sectoral regulators of the relevant investors. AIFs are meant strictly for sophisticated investors, and as such, various categories of AIF investors, such as insurance companies, pension funds, banks and NBFCs, etc. are subject to their respective regulations. When they invest in an AIF, they must comply with SEBI’s rules as well as the investment norms prescribed by their own regulators, each seeking to regulate how the capital of the investor is deployed. In fact, SEBI regulations are agnostic as to who the investor is, hence, most of the SEBI regulations relate to the AIF or the manager, with limited provisions dealing with investors. For example, whether and to what extent an insurance company or a pension fund can invest in an AIF is driven by the guidelines issued by the sectoral regulators such as IRDAI or PFRDA.

In this article, we try to bring together, in one place, the key regulatory norms imposed by various regulators; while these are primarily meant for the investor, however, it will be useful for the AIF managers to keep in mind these restraints while expecting or inviting investments from different categories of investors.

Categories of investors and regulatory restrictions on each category

Minimum investment norms: Common across all categories

₹25 crore for investors in Large Value Funds (reduced from ₹ 70 Crore per investor vide SEBI (Alternative Investment Funds) (Third Amendment) Regulations, 2025) [Reg. 2(1)(pa)];

₹1 crore for other investors [Reg 10(c)];

₹25 lakh for employees or directors of the AIF, manager, or sponsor [Reg 10(c)];

No minimum for units issued to employees solely for profit-sharing (and not capital contribution) [Para 4.6 of AIF Master Circular];

For open-ended AIFs, the initial investment must meet the minimum threshold, and partial redemptions must not reduce the holding below this minimum [Para 4.7 of AIF Master Circular].

Individuals

An AIF may raise funds from individual investors, whether resident, non-resident (NRI), or foreign, through private placement, subject to the following conditions (Refer Reg. 10(a) of AIF Regulations r/w Chapter 4 of AIF Master Circular).

Foreign investors: A foreign investor must:

be a resident of a country whose securities market regulator is a signatory to the IOSCO Multilateral MoU (Appendix A) or has a Bilateral MoU with SEBI; or

be a government or government-related investor from a country approved by the Government of India, even if the above condition is not met.

Additionally, neither the investor nor its beneficial owner1:

If a foreign investor ceases to meet these conditions after admission, the AIF manager must stop making further drawdowns from that investor until compliance is restored.

Joint Investments: Joint investments, for the purpose of investment of not less than the minimum investment amount in the AIF, are permitted only between:

an investor and spouse;

an investor and parent; or

an investor and child.

A maximum of two persons may invest jointly. Any other combination of joint investors must individually meet the minimum investment threshold. (Refer Reg. 10(c) of AIF Regulations r/w Chapter 4 of AIF Master Circular)

Terms of Investment: The terms agreed with investors cannot override or go beyond the disclosures in the PPM [Para 4.3 of AIF Master Circular].

The total number of investors is limited to 1000 investors per scheme; also note that an AIF cannot make a public offer. AIF units are commonly offered through distributors; but even the distributors cannot make an open offer (Please refer to our resource on Dos and Don’ts for AIF Distributors and AIF Managers).

Category I AIFs: Infrastructure Funds, SME Funds, Venture Capital Funds, and Social Venture Funds (‘Specified Cat I AIFs’);

Category II AIFs: Only where at least 51% of the corpus is proposed to be invested in infrastructure entities, SMEs, venture capital undertakings, or social venture entities (‘Specified Cat II AIFs’).

Investment in a Fund of Fund (‘FoF’) is allowed only if such FoF does not directly or indirectly invest funds outside India (Refer Section 27E of Insurance Act, 1938). This is to be ensured by inserting a clause in the Fund offer Documents executed by FoF to restrain such FoF investing into AIFs which invest in overseas companies/funds. Further, investment is not allowed in an AIF which in-turn has an exposure to a FoF in which the insurer already invested. Lastly, no investment in an AIF is allowed which undertakes leverage/borrowing other than to meet operational requirements.

Compliance of conditions laid down in (iii) are to be certified by the concurrent auditor of the insurer and filed along with quarterly periodical returns. Notably, insurance companies are prohibited from investing in Cat III AIFs

Prohibited Structures: Insurers shall not invest in AIFs that:

offer variable rights attached to units.

invest funds outside India either directly or indirectly [s. 27E of Insurance Act, 1938];

are sponsored by persons forming part of the insurer’s promoter group;

are managed a manager who is controlled, directly or indirectly, by the insurer or its promoters;

Investment Limits:

For life insurers, combined exposure to AIFs and venture capital funds is capped at 3% of the relevant insurance fund2.

For general insurers, the cap is 5% of total investment assets3.

Exposure to any single AIF cannot exceed the lower of 10% of the AIF’s corpus or 20% of the insurer’s total AIF exposure. For Infrastructure Funds, the 10% limit is enhanced to 20%.

Banks and other Regulated Entities (REs)

Banks and other REs may invest in Category I and Category II AIFs, subject to layered limits:

Bank level: Not more than 10% of the AIF corpus.

Group level: Up to 20% without RBI approval, and up to 30% with prior RBI approval, subject to capital adequacy and profitability conditions.

System level: Aggregate investments by all regulated entities cannot exceed 20% of the AIF corpus.

Banks must ensure that AIF investments do not circumvent banking regulations by creating prohibited indirect exposures. Banks are not permitted to invest in Category III AIFs, except for the minimum sponsor contribution where a bank subsidiary sponsors such a fund. For a more detailed discussion on Banks’ investment in AIFs, refer to our resource here.

NBFCs

An NBFC shall not individually contribute more than 10 percent of the corpus of an AIF Scheme. [See Para 8 of RBI ( NBFC – Undertaking of Financial Services) Directions, 2025]. The system-level investment limit of 20% for all REs shall also apply. Notably, unlike banks, NBFCs can invest in Cat III AIFs.

Pension, Provident and Gratuity Funds

Pursuant to a 15 March 2021 notification, non-government Provident Funds, Superannuation Funds, and Gratuity Funds may invest up to 5% of their investible surplus in Specified Cat I AIFs and Specified Cat II AIFs, classified as “Asset Backed, Trust Structured and Miscellaneous Investments”.

Key conditions include:

Minimum AIF corpus of ₹100 crore;

Maximum exposure of 10% to a single AIF (not applicable to government-sponsored AIFs);

Investments restricted to India-based entities only;

The AIF sponsor and manager must not be part of the fund’s promoter group.

For Government Sector Schemes such as UPS/NPS/NPA Lite/Atal Pension Yojna and Corporate CG schemes, the conditions are the same as above for non-government pension funds.

Mutual Funds

Mutual funds are governed by the SEBI (Mutual Funds) Regulations, 1996. The Seventh Schedule to these regulations sets out the permissible investment universe. Units of AIFs are not included, and accordingly, mutual funds cannot invest in AIF units.

beneficial owner as determined in terms of sub-rule (3) of rule 9 of the Prevention of Money-laundering (Maintenance of Records) Rules, 2005 ↩︎

The relevant insurance fund would refer to the specific fund of a life insurer from which an investment is made, rather than the insurer’s overall balance sheet. This is because Life insurers maintain separate, ring-fenced funds for different lines of business, such as the life fund, pension fund, annuity fund or ULIP fund and investments must be made out of, and limits calculated with reference to, the particular fund whose money is being deployed. ↩︎

Investment assets would refer to the total pool of assets held by a general insurer that are available for investment, across all lines of non-life insurance business. Unlike life insurers, general insurers do not maintain separate, ring-fenced policyholder funds for each product. Instead, premiums collected from various non-life insurance policies are invested as a consolidated portfolio, and regulatory investment limits such as exposure to AIFs are calculated with reference to the insurer’s aggregate investment assets shown on its balance sheet. ↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-12-24 16:23:482025-12-24 18:17:23A Guide for AIF Managers on Investor Eligibility and Regulatory Restrictions

When AIF Regulations were formally introduced in 2012, the regulatory approach was deliberately light. The framework targeted sophisticated investors, allowing flexibility with limited oversight. Over the years, however, AIFs have become significant participants in capital markets. Market practices over the decade exposed regulatory loopholes and arbitrages. For example, some investors who did not individually qualify as QIBs accessed preferential benefits indirectly through AIF structures and investors who were restricted to invest in certain companies started investing through AIF making AIF an investment facade. There were concerns regarding circumvention of FEMA norms as well1. In the credit space, regulated entities such as banks and NBFCs started channeling funds through AIFs to refinance their stressed borrowers, raising concerns around loan evergreening2. These developments prompted regulatory response. RBI first issued two circulars, one in 2023 and the other in 2024. Finally, in 2025 formal directions governing investments by regulated entities in AIFs were also issued3. These Directions introduced exposure caps and provisioning requirements.4

While the RBI addressed prudential risks arising from regulated entities’ participation in AIFs, SEBI focused on investor protection, governance within the AIF ecosystem and curbing the regulatory arbitrages. First it mandated on-going due diligence by AIF Managers5. It then mandated specific due diligence6 of investors and investments of AIF to prevent indirect access to regulatory benefits. Fiduciary duties of sponsors and investment managers and reporting obligations were progressively codified through circulars. Managers were expected to maintain transparency vis-a-vis their investment decisions, maintain written policies including ones to deal with conflict of interest with unitholders and submit accurate information to the Trustee. What were once broad, principle-based expectations have evolved into detailed, enforceable rules. Regulatory tightening has been matched by a more assertive enforcement approach. SEBI’s recent settlement order7 against an AIF underscores its increasing scrutiny of governance lapses, mismanagement of conflicts and inaccurate reporting. This clearly signals that any compliance gaps will no longer be overlooked and are likely to attract regulatory action. In a separate adjudication order, SEBI imposed penalties on both the Trustee and the Manager for the delayed winding-up of the scheme, underscoring that accountability within an AIF structure extends to all key parties and is not limited to the Manager alone.

However, SEBI’s approach has not been solely restrictive. Alongside regulatory tightening, it has also sought to preserve commercial flexibility and respond to market needs. Examples include the introduction of the co-investment framework8 for AIFs, framework for offering differential rights to select investors and a revamp for angel funds9.

Together, these measures are reshaping the regulatory landscape for AIFs and their managers. Investors can no longer rely on AIF structures to indirectly obtain regulatory advantages otherwise unavailable to them. As AIFs have grown in scale and importance, what is emerging is a more transparent, prudentially sound and closely supervised regulatory regime designed to align investor protection and commercial flexibility.

See SEBI’s Consultation paper on proposal to enhance trust in the AIF ecosystem ↩︎

See our write-up on AIFs being used for regulatory arbitrages here. ↩︎

See our write-up on changes w.r.t Angel Funds here↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-09 10:45:482025-10-10 10:19:44AIF Regulatory framework evolves from light-touch to right-hold

Alternative Investment Funds (AIFs) are private investment vehicles registered with and regulated by SEBI. Private investment vehicles, as is understood, are investment vehicles that pool investments from investors on a private basis, and make investments in investee entities based on the investment objectives disclosed to the investors. The returns from such investments, net of the expenses incurred by the vehicle, is distributed back to the investors. A typical AIF structure would look like:

The general obligations of AIFs are provided in the SEBI (Alternative Investment Funds) Regulations, 2012 read with the circulars issued from time to time. In addition to that, the Standard Setting Forum for AIFs (SFA) formulates implementation standards for various compliance requirements, as required by SEBI from time to time.

As may be understood, the AIF takes funds from its investors and makes investments in the investees. As between the sponsor/ manager of the Fund and the investors, there is a fiduciary relationship – since the investment decisions taken by the fund manager is on behalf of the investors, and in accordance with the investment objectives disclosed to the investors. Investor protection and transparency and proper due diligence of the investees become crucial in the context of an AIF. As compared to a traditional company, the AIFs are intermediaries between the investors and investees. This article discusses the various compliance requirements as applicable to AIFs.

Governance structure of AIFs

Governing body of AIF: Depending on the legal form of the AIF, the governing body of the AIF may compose of trustee (in case of a trust), directors (in case of a company) or designated partners (in case of an LLP).

Manager: The primary responsibility of ensuring compliance with the applicable provisions by an AIF is on the manager of the AIF. Similarly, ensuring compliance with the internal policies and procedures of an AIF is also the responsibility of the manager. The manager is appointed by an AIF, and the Sponsor may also be the manager of the Fund.

Investment Committee: Constituted by the manager, the Investment Committee approves the decisions of the AIF and is responsible for ensuring that such decisions are in compliance with the policies and procedures laid down by the AIF. The Investment Committee may be composed of internal members (employees, directors or partners of the Manager) as well as external investors (with the approval of the investors in the AIF/ Scheme). The external members may include ex-officio members who represent the sponsor, sponsor group, manager group or investors, in their official capacity. Pending clarification from RBI, currently non-resident Indian citizens are not permitted to act as an external member in the Investment Committee [Reg 20(7) of AIF Regulations read with Chapter 14 of AIF Master Circular].

The responsibilities of the Investment Committee may be waived by the investors (other than the Manager, Sponsor, and employees/ directors of Manager and AIF), if they have a commitment of at least Rs. 70 crores (USD 10 billion or other equivalent currency), by providing an undertaking to such effect, in the format as provided under Annexure 11 of the AIF Master Circular, including a confirmation that they have the independent ability and mechanism to carry out due diligence of the investments.

Key Management Personnel: Key Management Personnel (KMP) of the Manager has been defined to mean:

members of key investment team of the Manager, as disclosed in the PPM of the fund;

employees who are involved in decision making on behalf of the AIF, including but not limited to, members of senior management team at the level of Managing Director, Chief Executive Officer, Chief Investment Officer, Whole Time Directors, or such equivalent role or position;

any other person whom the AIF (through the Trustee, Board of Directors or Designated Partners, as the case may be) or Manager may declare as key management personnel. [Para 13.1.2. of the AIF Master Circular]

The responsibilities of the Manager are complied through the Key Management Personnel of such Manager.

Compliance Officer: The Compliance Officer is appointed by the Manager, and is responsible for monitoring of compliance with the applicable laws and requirements as applicable to the AIF. Compliance Officer, shall be an employee or director of the Manager, other than Chief Executive Officer of the Manager or such equivalent role or position depending on the legal structure of Manager [Para 13.1.1. of the AIF Master Circular].

The Compliance Officer is responsible to report any non-compliance observed by him within 7 days from the date of observing such non-compliance.

Custodian: The Sponsor/ Manager of the AIF is required to appoint a custodian, registered with SEBI, for safekeeping of the securities of the AIF. An associate[1] of the Sponsor/ Manager may also act as a custodian, subject to compliance with certain conditions[2]. The custodian provides periodic reports to SEBI with respect to the investments of AIFs that are under custody with the custodian in accordance with the standards formulated by SFA.

The various roles and responsibilities at the different levels of the governance structure is discussed below.

Code of Conduct for AIFs [Reg 20(1) of AIF Regulations]

The Code of Conduct, as prescribed under the AIF Regulations, puts forth various requirements applicable to the AIFs and other relevant entities. The Code of Conduct is applicable to various responsibility centers charged with the governance requirements in an AIF. The requirements are given in the Fourth Schedule to the AIF Regulations read with Para 13.3. of the AIF Master Circular.

The applicability to various stakeholders along with the requirements are given in the table below:

Person covered by the CoC

Requirements to be adhered to under the CoC

AIF

Undertake business activities and investments in accordance with the investment objectives in the placement memorandum and other fund documents [to be ensured by the Manager]

Be operated in the interest of all investors, and not limited to select investors, sponsor, manager etc [to be ensured by the Manager]

Ensure timely and adequate dissemination of information to all investors

Ensure existence of effective risk management process and appropriate internal controls

Have written policies for mitigation of any potential conflict of interest

Prohibition on use of any unethical means to sell, market or induce any investor to buy its units

Have written policies and procedures to comply with anti-money laundering lawsnot offer any assured returns to any prospective investors/unitholders.

Manager of AIF

KMP of Manager

KMP of AIF

Abide by the laws applicable to AIFs at all times

Maintain integrity, highest ethical and professional standards in all its dealings

Ensure proper care and exercise due diligence and independent professional judgment in all its decisions

Act in a fiduciary capacity towards investors of AIF and ensure that decisions are taken in the interest of the investors

Abide by the policies of AIF in relation to potential conflict of interests

Not make any misleading or inaccurate statement, whether oral or written, either about their qualifications or capability to render investment management services or their achievements

Record in writing, the investment, divestment and other key decisions, together with appropriate justification for such decisions;

Provide appropriate and well considered inputs, which are not misleading, as required by the valuer to carry out appropriate valuation of the portfolio;

Prohibition on entering into arrangements for sale or purchase of securities, where there is no effective change in beneficial interest or where the transfer of beneficial interest is only between parties who are acting in concert or collusion, other than for bona fide and legally valid reasons;

Abide by confidentiality agreements with the investors and not make improper use of the details of personal investments and/or other information of investors;

Not offer or accept any inducement in connection with the affairs of or business of managing the funds of investors;

Document all relevant correspondence and understanding during a deal with counterparties as per the records of the AIF, if they have committed to the transactions on behalf of AIF

Maintain ethical standards of conduct and deal fairly and honestly with investee companies at all times; and

Maintain confidentiality of information received from investee companies and companies seeking investments from AIF, unless explicit confirmation is received that such information is not subject to any non-disclosure agreement.

Ensure availability of the PPM to the investors prior to providing commitment or making investment in the AIF and an acknowledgment be received from the investor

Ensure scheme-wise segregation of bank accounts and securities accountsnot offer any assured returns to any prospective investors/unitholders.

Members of Investment Committee

Trustee/ Trustee company

Directors of Trustee company

Directors of AIF

Designated Partners of AIF

Maintain integrity and the highest ethical and professional standards of conduct

Ensure proper care and exercise due diligence and independent professional judgment

Disclose details of any conflict of interest relating to any/all decisions in a timely manner to the Manager of the AIF, adhere with the policies and procedures of the AIF with respect to any conflict of interest and wherever necessary, recuse themselves from the decision making process;

Maintain confidentiality of information received regarding AIF, its investors and investee companies; unless explicit confirmation is received that such information is not subject to any non-disclosure agreement.

Not indulge in any unethical practice or professional misconduct or any act, whether by omission or commission, which tantamount to gross negligence or fraud

Not offer any assured returns to any prospective investors/unitholders.

Compliance with Stewardship Code

The AIFs, being institutional investors, it is mandatory for AIFs to comply with the Stewardship Code in terms of Para 13.4 of the AIF Master Circular. This is applicable in respect of investments in listed equity instruments. Annexure 10 of the Master Circular specifies the broad principles of stewardship and provides guidance for its implementation. Further, the AIFs are required to report the status of implementation of the principles atleast on an annual basis (periodicity may differ for different principles), through the website of the AIFs. Such report may also be sent as a part of annual intimation to its clients/ beneficiaries. An article on the stewardship responsibilities of institutional investors may be read here.

Policies to be formulated by AIFs

In order to ensure that the decisions of the AIF are taken in compliance with all applicable laws and regulations, PPM, investor agreements and other fund documents, detailed policies and procedures are required to be kept in place in terms of Reg 20(3). The policies are jointly approved by:

Manager and

Relevant governing body of the AIF (viz., the trustee/ trustee company/ board of directors/ designated partners etc)

The Manager is required to ensure that the decisions taken by the AIF are in compliance with such policies and procedures.

Further, the policies should be reviewed periodically, on a regular basis and whenever required as a result of business developments, to ensure their continued appropriateness.

Audit

Annual Audit of terms of PPM

The AIF is required to file Private Placement Memorandum (PPM) with SEBI through a Merchant Banker for the launch of Schemes. The format of PPM is specified under Annexure 1 read with the requirements specified under various other circulars from time to time. In order to ensure that the activities of the AIF are in compliance with the terms of PPM, annual audit of the terms of PPM is required to be done. In this regard, the following needs to be noted:

Scope of audit: Compliance with all sections of the PPM. Further, audit of the following sections is optional, viz., ‘Risk Factors’, ‘Legal, Regulatory and Tax Considerations’ and ‘Track Record of First Time Managers’. The format of PPM audit report may be accessed here.

Eligibility to conduct audit: an internal or external auditor/legal professional

Periodicity of PPM audit: Annual

Timeline: within 6 months from the end of the Financial Year

Reported to: Governing Body (Trustee or Board of Directors or Designated Partners) of the AIF, Board of directors or Designated Partners of the Manager and SEBI

Non-applicability: if no funds are raised from investors, subject to submission of a certificate from CA to that effect within 6 months from end of FY

Exemptions: (i) Angel Funds, (ii) AIFs/ Schemes with each investor having a minimum commitment of Rs. 70 crores (USD 10 mn or equivalent), upon providing a waiver for the same.

Audit of accounts

Reg 20(14) of the AIF Regulations require the books of account to be audited by a qualified auditor annually.

Valuation of Investments of AIF

Reg 23 read with Chapter 22 of the AIF Master Circular specifies the requirements with respect to the valuation of the investments of AIF. The valuation is required to be done by an independent valuer, on a half-yearly basis (may be made an annual requirement subject to consent of 75% of investors in value).

Eligibility criteria have been specified for acting as an independent valuer:

shall not be an associate of manager or sponsor or trustee of the AIF

shall have at least three years of experience in valuation of unlisted securities

shall be a registered valuer with IBBI and a member of ICAI, ICSI or ICMAI or shall be a holding or subsidiary of SEBI-registered CRA

The Manager shall specifically inform the investors, the reasons/ factors for deviation in valuation, in case the deviation is more than:

20% between two consecutive valuations, or

33% in a financial year

In case of Cat III AIFs, the listed and unlisted debt securities are required to be valued by an independent valuer, and the NAV is required to be reported on a quarterly basis for close ended funds, and monthly basis for open ended funds.

Investor complaints and Grievance Redressal Mechanism

Resolution of investor complaints is a role of the Manager of AIF [Reg 24 of AIF Regulations]. Reg 24A requires the Manager to redress investor grievances in a prompt manner, but within a maximum of 21 days from receipt of grievances. The AIF is required to be registered on the SCORES portal for receipt of investor grievances. Further, in terms of Reg 25, the dispute resolution mechanism provided by SEBI (SMARTODR) is applicable to AIFs as well. Refer details under Master Circular for Online Resolution of Disputes in the Indian Securities Market dated 28th December, 2023.

Further, in terms of Para 17.4 of the AIF Master Circular, the AIFs are required to maintain data on investor complaints received against the AIF/ its Schemes on a quarterly basis within 7 days from the end of the quarter, in addition to the disclosure in the PPM. The data includes the following:

S. No.

Investor Complaints received from

Pending as at the end of the last quarter

Received

Resolved

Total Pending at the end of the quarter

Pending complaints > 3months

Average Resolution time ^(in days )

1

Directly from Investors

2

SEBI (SCORES)

3

Other Sources

Matters requiring consent of investors of AIF

The AIFs act in a fiduciary capacity towards the investors, and manage the funds of the investors invested in the AIF. Thus, the decisions of AIF are required to be taken in the interests of the investors. Some matters require approval of the investors of a specified majority, prior to undertaking such activity:

Regulatory reference

Matter requiring approval

Requisite majority in terms of value of investment

Reg 9(2)

Material alteration to fund strategy

2/3rd of unitholders

Reg 13(5)

Extension of tenure of close-ended funds (upto 2 years)

2/3rd of unitholders

Reg 15(1)(e)

Investment in associates or units of AIFs managed/ sponsored by its Manager, Sponsor or associates of its Manager or Sponsor

75% of investors

Reg 15(1)(ea)

Purchase or sale of investments from/ to: Associates Schemes of AIF managed or sponsored by its Manager, Sponsor or associates of its Manager or Sponsoran investor who has committed to invest at least fifty percent of the corpus of the scheme of AIF

75% of investors, excluding investor covered under (c) where purchase/ sale is from such investor

Reg 20(10)

Appointment of external members (other than ex-officio members) in Investment Committee other than as disclosed in the fund documents

75% of investors

Reg 23(2)

Reducing frequency of valuation of investments from six months to 1 year

75% of investors

Reg 29(9)

In-specie distribution of investments of AIF due to lack of liquidity or enter into liquidation period

75% of investors

Disclosure to investors

The funds of the investors invested in the AIF are managed by the Manager and Sponsor in a fiduciary capacity. In order to ensure transparency, various disclosure requirements apply in terms of Reg 22 of the AIF Regulations – either on a periodic basis or upon the happening of certain events.

Periodic disclosures

The periodic disclosures include:

financial, risk management, operational, portfolio, and transactional information regarding fund investments

any fees ascribed to the Manager or Sponsor; and any fees charged to the AIF or any investee company by an associate of the Manager or Sponsor

Further, in terms of clause (g) of Reg 22, the following information is required to be disclosed within 180 days from the year end (60 days from the end of each quarter for Cat III AIF):

financial information of investee companies.

material risks and how they are managed which may include:

concentration risk at fund level;

foreign exchange risk at fund level;

leverage risk at fund and investee company levels;

realization risk (i.e. change in exit environment) at fund and investee company levels;

strategy risk (i.e. change in or divergence from business strategy) at investee company level;

reputation risk at investee company level;

extra-financial risks, including environmental, social and corporate governance risks, at fund and investee company level.

Any changes in terms of PPM or other fund documents are required to be intimated to the investors on a consolidated basis within 1 month from the end of each financial year [Para 2.5.3. of AIF Master Circular]

Event-based disclosures

These events are required to be disclosed ‘as and when occurred’:

any inquiries/ legal actions by legal or regulatory bodies in any jurisdiction

any material liability arising during the AIF’s tenure

any breach of a provision of the placement memorandum or agreement made with the investor or any other fund documents

change in control of the Sponsor or Manager or Investee Company

any significant change in the key investment team

Matters requiring reporting to SEBI

Reg 28 provides power to SEBI to seek such information from the AIFs, as may be required, from time to time. In addition to such powers, there are various specific reporting requirements that are applicable on AIFs under various applicable provisions. These include:

Regulatory reference

Matters requiring reporting to SEBI

Timelines

Reg 20(12)

Any material change from the information provided at the time of application

Promptly

Reg 26

Information for systemic risk purposes (including the identification, analysis and mitigation of systemic risks)

when so required by SEBI

Para 2.5.2

Any changes in the terms of PPM and other fund documents, along with DD certificate from Merchant Banker

Any violations reported in the Compliance Test Report (refer detailed discussion below)

As soon as possible

Reg 20(11) r/w Para 15.4.

Investments of AIF that are in custody of the custodian

Quarterly

Compliance with provisions applicable to SEBI-registered intermediaries

An AIF, in its capacity of a SEBI-registered intermediary, is required to comply with the SEBI (Intermediaries) Regulations, 2008 read with the circulars issued thereunder. These include, for instance, compliance with the circulars/guidelines as may be issued by SEBI with respect to KYC requirements, Anti-Money Laundering and Outsourcing of activities [Para 13.5 of AIF Master Circular].

The guidelines with respect to anti-money laundering and KYC requirements are contained in a Master Circular dated 6th June, 2024 on the subject. Our various resources on KYC and anti-money laundering can be accessed here.

Compliance Test Report

The manager of AIF is required to report the compliances with various applicable provisions of the AIF Regulations read with the circulars made thereunder, on an annual basis. CTR is submitted within 30 days from the end of the financial year, to the sponsor and trustee (in case AIF is set up as a trust). The trustee/ sponsor provides their comments on the CTR to the manager within 30 days from the receipt of CTR, based on which the manager shall make necessary changes and provide a response within the next 15 days.

A significant aspect of the CTR is that any violation observed by the trustee/ sponsor is required to be intimated to SEBI, as soon as possible. This requirement is in addition to the obligation of the Compliance Officer to report a non-compliance, within 7 days of becoming aware of the same. The format of CTR is provided in Annexure 12 of the AIF Master Circular.

Other compliances

SEBI specifies various compliances applicable to the AIFs from time to time. The compliances as applicable to the AIFs for the first time during FY 25-26 has been dealt with in our article Regulatory landscape for AIFs: what’s new? Further, there are certain requirements applicable on special categories of AIFs, viz., angel funds, Special Situation Funds, Social Venture Funds etc. Further, there are various prudential requirements applicable to receipt of funds from investors and making of investments by the AIFs.

The RBI has issued Draft Reserve Bank of India (Investment in AIF) Directions, 2025 (‘Draft Directions’), vide Press Release dated 19th May, 2025, marking a significant revision to the existing regulatory framework governing investments by regulated entities (REs) in Alternative Investment Funds (AIFs). These new directions, once finalised, will replace the existing circulars dated December 19, 2023 (“2023 Circular”), and March 27, 2024 (“2024 Clarification”) (collectively, referred to as “Existing Directions”), which currently govern such investments.

The Existing Directions prohibit REs from making investments in any scheme of AIFs which has downstream investments either directly or indirectly in a debtor company of the RE. In case of any such investment full provision is required to be maintained by the RE. Such prohibition is imposed to address the concerns of evergreening while making investments by an RE. See our analytical article on the same here.

However, the Draft Directions now propose to allow investment by the RE in such AIF upto 5% of the corpus of the AIF scheme. Any investment exceeding this 5% limit will require full capital if AIF has made debt investments in the debtor company. Note that these norms are entirely directed towards debt or debt instruments (whether at the RE level or the AIF level), as all sorts of equity instruments (equity shares, compulsorily convertible preference shares and compulsorily convertible debentures) are excluded – detailed discussion follows.

Comparison of Existing and Draft Directions

Below is a snapshot of what is going to change once the Draft Directions are finalised and notified, and certain important implications are discussed further:

Particulars

2023 Circular read with 2024 clarification

Draft Directions

Investment by REs in scheme of AIF

RE completely prohibited from investing in any scheme of AIF which has downstream investments in debtor company of the RE.Any investment already made had to be liquidated within 30 days of the issuance of the Circular. Similarly, where the RE had already invested, but AIF makes investment in a debtor company of RE, RE shall liquidate investments in AIF within 30 days.

To be allowed subject to individual and collective limits:Max. contribution of single RE to an AIF scheme – 10% of its corpusMax. contribution of multiple REs – 15% of its corpusSee illustrations later in this article.

Debtor company

Shall mean any company to which the RE currently has or previously had a loan or investment exposure anytime during the preceding 12 months.

Shall imply any company to which the RE currently has or previously had a loan or investment exposure (excluding equity instruments) anytime during the preceding 12 months.

Provisioning requirements

Inability to liquidate investments within 30-day liquidation period would entail 100% provisioning against such investments.

Investment by the RE in such AIF allowed upto 5% of the corpus of the AIF scheme, without looking into the form of downstream investments made by AIF. Hence, no provisioning required. If investment by RE exceeds 5%, it will require full capital, if downstream investments by AIF in debtor company are not permissible investments (see below). See illustrations later in this article

Provisioning required proportionately and not on entire investments

Provisioning is required only to the extent of investment by the RE in the AIF scheme which is further invested by the AIF in the debtor company, and not on the entire investment of the RE in the AIF scheme

Norms remain the same – RE shall be required to make 100 per cent provision to the extent of its proportionate investment in the debtor company through the AIF Scheme

Permissible forms of investments by AIF scheme in debtor company

Investment in equity shares (by AIF scheme in debtor company) were excluded from the prohibition by 2024 clarification. However hybrid instruments were still included.

All forms permitted, if investment by RE does not exceed 5%. Therefore, even debt investments by AIFs are permissible.Only equity shares, CCPS, and CCDs allowed, if investments by RE exceeds 5%. If AIF makes other forms of investments in debtor company, RE will have to provide for full capital.Note that, irrespective of the form of downstream investments by AIF in the debtor company, RE can take a maximum exposure of 10% in an AIF.

Priority distribution model

investment by REs in the subordinated units of any AIF scheme with a ‘priority distribution model’ shall be subject to full deduction from RE’s capital funds. Deduction shall be made from Tier I and II equally.

Norms remain the same.

Investment policy

No specific requirement

Investment policy to have suitable provisions to ensure that investments in an AIF Scheme comply, in letter and spirit, with the extant regulatory norms. In particular, such investments shall be subject to the test of evergreening.

Exemption by regulator

No specific enabling provision

Exempted category to be decided by RBI in consultation with GoI.

Illustrations on investment limits by RE

Below are certain illustrations to explain the implications of the investment thresholds under Draft Directions:

Scenarios

Implications under Draft Directions

Investment of Rs. 10 Crores by an RE in an AIF scheme having corpus of 50 crores

Cannot make since the threshold limit of 10% will be breached.

Investment of Rs. 5 Cr by an RE in an AIF scheme having corpus of 50 crores with other REs contributing Rs. 15 Cr

While the investment by the RE individually is within the limit of 10%, the collective investment is more than 15%. Hence, such an investment cannot be made by the concerned RE. Further, since the total investment of 15 cr by other REs will also breach the threshold of 15%, the investments will not be possible.

Investment of Rs. 5 Cr by an RE in an AIF scheme having a corpus of 50 Cr. The AIF in turn has a downstream debt investment in a debtor company of the RE.

Cannot be made since the limit of 5% will be breached.

Investment of Rs. 1 Cr by an RE in an AIF scheme having a corpus of 50 Cr. The AIF in turn has a downstream debt investment in a debtor company of the RE.

This constitutes only 2% of the corpus of the AIF scheme. Hence, permissible – even when the downstream investment of the AIF is a debt investment.

Investment of Rs. 5 Cr by an RE in an AIF scheme having a corpus of 50 Cr. The AIF in turn has a downstream equity investment in a debtor company of the RE.

Can be made as the downstream investment of the AIF is in equity of the debtor company. However, the maximum cap of 10% would apply to the RE.

Certain points of discussion/implications

Prospective applicability: The Draft Directions, once notified, will be applicable prospectively. It says, “These Directions shall come into force from the date of final issue (‘effective date’), substituting the existing circulars. Provided that, all outstanding investments as on the effective date, or subsequent drawdowns out of commitments made prior to the effective date, shall continue to be guided by the provisions of the existing circulars.” Therefore, no relaxations would be available to the existing investments/commitments by REs. If the same had not been liquidated so far – those will require to be liquidated. The Draft Directions will apply only to fresh investments by REs.

Maximum cap on investments by RE in AIF: Under Existing Directions, there is a blanket prohibition on RE to invest in AIF scheme which has invested in a debtor company. However, if such downstream investment is in equity shares, such prohibition would not apply. As such RE could invest in the said AIF without any limits. However, now, even if the AIF has invested only in equity instruments of the debtor company (equity shares, CCPS and CCDs), RE can only invest upto 10% of the corpus of the AIF scheme. Hence, to that extent, the Draft Directions are more restrictive than the Existing Directions. Note that, SEBI Circular on specific due diligence with respect to investors and investments of the AIFs does not provide any carve out for equity investments.

Exclusion of equity instruments (equity shares, CCDs and CCPS) from investment exposure of REs in the debtor company: Such exclusion is not explicitly there in the Existing Directions; which might have led to a possible interpretation that investment would include any nature of investment, including equity. Although, it was evident from the use of terminology that a debtor company would only mean a company where RE has extended only debt. The Draft Directions has clarified the same through explicit exclusion. Therefore, the directions will be applicable only where RE has investment in debt/debt instruments of the investee company.

Investments in AIF through intermediary funds: Existing directions exclude investments by REs in AIFs through intermediaries such as fund of funds or mutual funds from the scope of the directions. However, Draft Directions are silent on the same. We are of the view that such exclusion should continue to apply – as funds such as mutual funds are required to be well-diversified in terms of the SEBI Regulations, and investment decisions are taken by an independent investment manager.

Closing Remarks

We had earlier indicated that the Existing Directions may need to be reviewed and softened. The Draft Directions take a step in the same direction – however, a few concerns may still remain open. For instance, the Draft Directions retain the outreach of these restrictions to all AIFs, and not only affiliated AIFs. In our previous article, we had discussed how the concerns as to evergreening, etc. would arise mostly in cases involving affiliated AIFs, and not those AIFs which are completely unrelated to the RE..Further, no distinction has been made between various categories of AIF – therefore, investments in any AIF (Cat I, II, III) would be governed by these directions.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-05-22 18:04:552025-05-22 18:07:20Capital subject to “Caps”: RBI relaxes norms for investment by REs in AIFs, subject to threshold limits

SEBI had raised concerns relating to evergreening of loans, circumvention of FEMA norms, QIB regulations and other concerns on regulatory arbitrage by Alternative Investment Funds (‘AIFs’) in its Consultation Paper issued in January, 2024. SEBI also recorded 40+ cases wherein the structure of AIF had been abused and used to circumvent extant financial sector regulations. Read our analysis in the article ‘AIFs ail SEBI: Cannot be used for regulatory breach’ dated January 31, 2024. Further, RBI had also barred all regulated entities (REs) with respect to their investments in AIFs, discussed in our article.

Subsequent to receipt of public comments, the proposal to mandate due-diligence (‘DD’) of investors and each of the investments made by the AIF was approved in the SEBI Board meeting held on March 15, 2024. SEBI notifiedSEBI(Alternative Investment Funds) (Second Amendment) Regulations, 2024 effective from April 25, 2024 amending Reg. 20 of the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’) dealing with general obligations thereby requiring every a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager, to exercise specific DD with respect to their investors and investments in order to prevent facilitation of circumvention of such laws as may be specified by SEBI from time to time.

The list of laws, thresholds and conditions for DD, reporting requirements etc. has been provided in SEBI circular dated Oct 8, 2024 (‘SEBI Circular’). DD is required to be carried out prior to making of investments as per implementation standards formulated by Standard Setting Forum for AIFs (‘SFA’) and published on websites of the industry associations which are part of the SFA, i.e., Indian Venture and Alternate Capital Association (‘IVCA’), PE VC CFO Association and Trustee Association of India.

Scope of laws covered under the ambit of due diligence

The list of laws provided in the SEBI Circular comprises of the following:

Provisions of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘ICDR Regulations’), and other regulations of SEBI wherein benefits or relaxations have been provided to entities designated as Qualified Institutional Buyers (‘QIBs’).

Provisions of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (‘SARFAESI Act’) wherein benefits are provided to entities designated as Qualified Buyers (‘QBs’).

Prudential norms specified by RBI for regulated lenders with respect to Income Recognition, Asset Classification, Provisioning and restructuring of stressed assets;

Rule 6 of FEMA (Non-Debt Instruments) Rules, 2019 (NDI Rules) for investment from countries sharing land border with India ( read with Press Note 3 dated April 17, 2020 of FDI Policy 2020)

Timing, thresholds for DD, reporting requirements

Pursuant to the SEBI Circular, the due diligence for various investors and investments is required to be carried out by a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager in accordance with the Implementation Standards. The table below indicates in brief the criteria, checkpoints and timelines for conducting due diligence along with the consequences of the outcome.

Sr. No

Objective intended to be achieved by investors through investments in AIF scheme

Regulations/ Directions/ Norms applicable

Applicability of requirement of DD for every scheme of AIF (refer Note 1)

Checkpoints for manager for specific DD

Timing of DD

Consequence of outcome of DD & reporting requirements, if any

1

Benefits designated for QIBs

ICDR and other SEBI Regulations

If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme.

Manager to check if such if investor/ investors of the same group is/are:(i) QIBs themselves or,(ii) Entities established, owned or controlled by the Central Government or a State Government or the Government of a foreign country, including central banks and sovereign wealth funds.Note: Where such investor is an AIF or fund set up in IFSC or outside India, above check to be carried out on a look through basis.

Prior to availing benefits available to QIBs

Refer Note 2 below for existing investments & Note 3 for proposed investments.Manager to provide confirmation to SE or lead manager or merchant banker on this.

2

Benefits designated for QBs

Under SARFAESI Act

If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme.

Same as above

Prior to making any investments or availing benefits

Refer Note 2 below for existing investments & Note 3 for proposed investments.

RBI norms on Income Recognition, Asset Classification, Provisioning and Restructuring of stressed loans/ assets

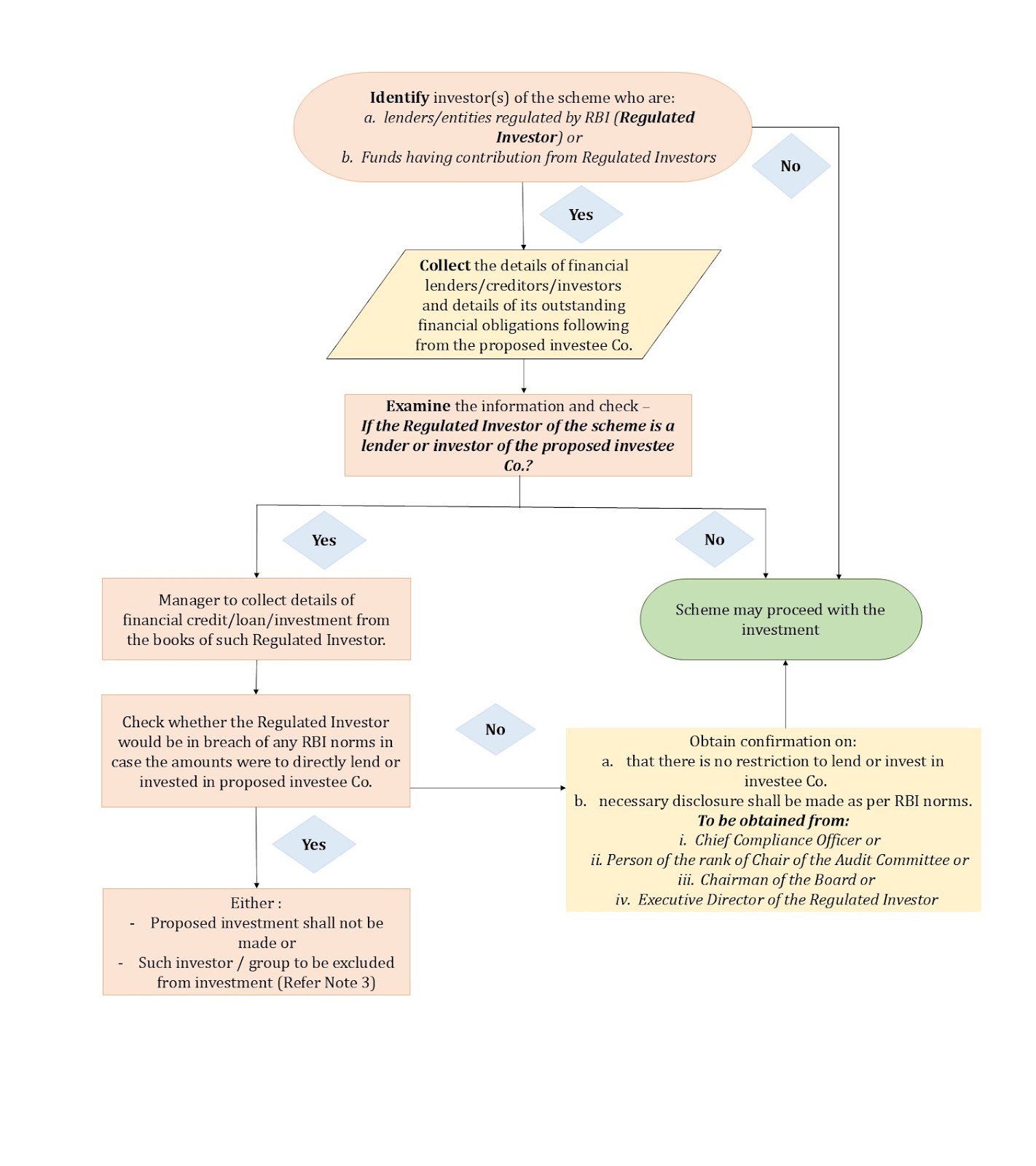

(a)whose manager or sponsor is an entity regulated by RBI; or,(b)that has investor(s)regulated by RBI who:(i)individually or along with investors of the same group contribute(s) 25% or more to the corpus of the scheme; or(ii) is an associate of the manager/ sponsor of the AIF;(iii) has majority or veto power [by itself, or through its representatives/ nominees] in voting over decisions of the investment committee set up by the manager to approve investment decisions of the scheme.Note: where investor is an AIF or fund set up in IFSC or outside India, criteria check to be carried out on a look through basis.

Refer Note 4.

Prior to making any investments, to avoid indirect investment by RBI regulated lender/ entity.

Refer Note 2 below for existing investments & Note 3 for proposed investments.

4

Investment from countries sharing land border with India

FEMA (NDI) Rules, 2019

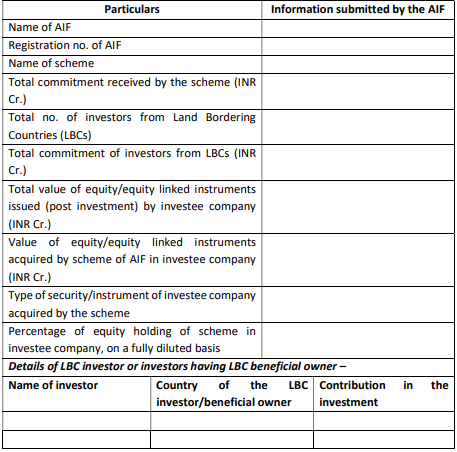

Where 50% or more of the corpus of the scheme is contributed by investors (a)who are citizens of/are from/are situated in a country which shares land border with India; or(b)whose beneficial owners, as determined in terms of Rule 9 (3) of the PMLA (Maintenance of Records) Rules, 2005, are citizens of/are from/are situated in a country which shares a land border with India.

If the proposed investment would result in the scheme holding 10 % or more of equity/equity-linked securities issued by the company (on a fully-diluted basis), the manager to check details stated in the previous column, by collecting information on the country of investors and their beneficial owners.

Prior to making any investment

Refer Note 2 below for existing investments & Note 5 for proposed investments.

Note 1: same group’ shall mean ‘related parties’ and ‘relatives’ as defined in SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Note 2:

For Sr nos 1 to 3: DD requirement is applicable for existing investments too, held by AIF schemes as on October 8, 2024:

If DD check not satisfactory – details of investment to be reported to AIF’s custodian on or before April 07, 2025, in the format as per Annexure 1 of the circular;

If DD check satisfactory – AIF manager to submit an undertaking to AIF’s custodian on or before April 07, 2025.

For Sr no. 4: Reporting is required to be made for existing investments held by AIF schemes as on October 8, 2024 if the scheme holds 10% or more of equity/ equity-linked securities on a fully-diluted basis, to AIF’s custodian on or before April 07, 2025 in the format prescribed by SFA.

Note 3:

Consequence of not satisfying requirements of DD checks specified by SFA for proposed investments in case of Sr nos 1 to 3:

Such investor or investor group to be excluded along with necessary disclosure in the private placement memorandum (PPM); or

Investment cannot be made.

Note 4:

Note 5: Details of investment, which would result in the scheme holding 10% or more of equity/ equity-linked securities on a fully-diluted basis, to be reported to the custodian within 30 days of investment, in the below format specified by SFA.

DD requirement – one-time or ongoing?

As discussed in the SEBI BM Agenda, the purpose of the due-diligence check is to prevent facilitation of any circumvention of provisions of financial sector regulators, which cannot be a time specific check. An entity who intends to circumvent can design the structure in such a way that, at a later date post investment, it acquires the units of AIFs post investment, such as buying the units of an existing investor or by acquiring control over the existing investor entity, as per prior arrangement. Accordingly, it has been indicated that due diligence around investors and investments will be an ongoing one.

Applicability of DD – prospective or retrospective?

As per the SEBI circular this is applicable for existing and prospective investments. Refer Note 2 above.

Obligations of Custodian to the AIF

Information received from AIFs under Note 2 to be furnished to SEBI on or before May 7, 2025.

Information received from AIFs in terms of Note 4 above on a monthly basis to be compiled and reported to SEBI within 10 working days from month end.

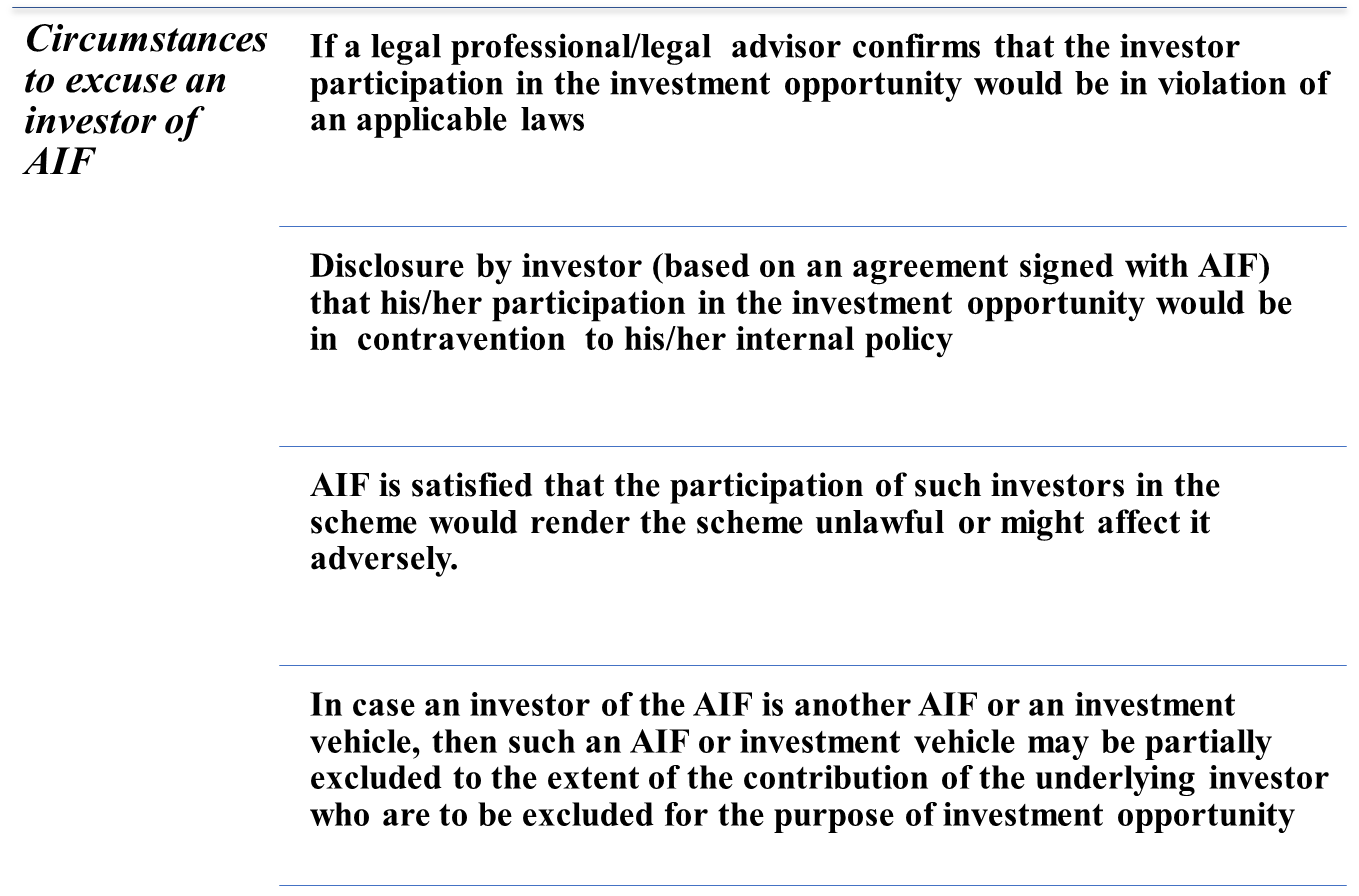

Power of AIF to exclude an investor

As per SEBI Circular, in cases where the outcome of DD is not satisfactory, in that case the AIF will either have to exclude the investor or investor group or abstain from making the proposed investment.

Figure 1: Circumstances to excuse an investor of AIF

Conclusion

The present amendment and SEBI Circular lays an onerous burden on the AIF, manager and KMP of the AIF and the manager. The DD requirement has become effective from October 8, 2024 and applies to existing investments as well. The AIFs have an actionable of evaluating the existing investments in the scheme in the light of the present amendment and ensure reporting in next 6 months. The obligation of on-going due diligence will result in a compliance burden, but is justified given the intent of law as “quando aliquid prohibetur ex directo, prohibetur et per obliquum” i.e. things that cannot be done directly should not be done indirectly either. AIFs will continue ‘trust, but verify’ using the DD standards for due diligence. The trustee/ sponsor of the AIF is required to ensure that compliance status of this amendment is reported to SEBI in the ‘Compliance Test Report’ prepared by the manager in terms of Chapter 15 of Master Circular for AIFs.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-05-03 20:07:492024-10-22 15:43:43Trust, but verify: AIFs cannot be used as regulatory arbitrage

The Reserve Bank of India on 19th December 2023 issued a notification[1] imposing a bar on all regulated entities[2] (REs) with respect to their investments in AIFs. We had covered the same in our earlier write-up. The Circular has already created some bloodshed as several banks took a hit in their Q3 results. Though late, yet welcome, the RBI has now come with some relief by a March 27 2023 circular. The following Highlights are based on the original circular, as amended by the March 27th circular :-

What has the RBI done?

Prohibited all regulated entities (REs), including banks, cooperative banks, NBFCs and All India Financial Institutions from making investments in Alternative Investment funds (AIFs), if the AIF has made any investment in a “debtor company”, other than by way of equity shares of the debtor company. Hence, if the AIF has made investment by way of bonds, structured capital instruments, etc., issued by a debtor company, the bar as above will apply.

Debtor company means a company in which the RE currently has or previously had a loan or investment exposure anytime during the preceding 12 months

The bar applies immediately, that is, effective 19th Dec 2023. No further investments to be made.

If investments already exist, the RE shall exit within 30 days, that is, by 18th Jan., 2024. Hindsight clearly shows that for most regulated entities, there was no way to cause exit, as AIF investments are evidently illiquid. Hence, most regulated entities took a hit on their P/L.

Further, if an RE has made an investment in an AIF, and the AIF invests in a debtor company, the RE shall make an exit within 30 days.

Investment by REs in the subordinated units of any AIF scheme with a ‘priority distribution model’ subject to full deduction from RE’s capital funds. See further discussion on priority distribution model below.

What was the intent?

Since several REs have affiliated AIFs, routing the money through AIFs to borrowers might have led to ever greening. That is, the AIF would invest the money into a debtor company, and consequently, the debtor company would keep its account as a performing asset. In essence, the AIF was acting as a stopover in the process of round tripping of the money back to a debtor company, from where it will be used to pay off the lender.

What will be the impact of the Circular?

Most of the larger REs have affiliated AIFs. Flow of funds to them from the RE would stop completely.

The sweep of the circular is wide and non-discriminatory. Not only affiliated AIFs, but any AIF in general will be dried of funding from REs. While the bar is only for those AIFs which have invested in “debtor companies”, it will be practically tough for REs to avoid overlapping investments. Given the severe implications of a breach, compliance-sensitive REs will avoid investing in AIFs.

There is an immediate disinvestment pressure on AIFs, as there may be overlapped investments. AIFs’ assets are mostly illiquid – ensuring exit to RE investors may be tough. In many cases, there are lock-in restrictions as well.

Not only has the RBI expressed concerns, SEBI also issued a consultation paper for enhancement of trust in the AIF ecosystem, citing use of AIFs for regulatory arbitrage. See our write up on the SEBI proposals.

Direct or indirect investments:

As the Circular is driven by concerns of round-tripping, widening the circuit by creating more stop-overs does not help. For example, if a lender invests in an AIF, which invests in an intermediate entity, which in turn invests in a debtor entity, the trail of the money is clear. Likewise, the lender may be making an indirect investment in an AIF.

However, where there is no round-tripping of the money to a “debtor company”, there should be no concern. For example, if a lender makes a loan to an entity, where an AIF of the group has also made investments, there is no flow of money from the lender to the AIF, for the purpose of the downstream investment by the AIF into the debtor company.

Investments through mutual funds and FOFs exempt:

The 27th March circular exempts instances where investments are made by lenders into mutual funds or FoFs, and those in turn have some exposure in either an AIF or in a debtor entity.

Priority distribution model or structured AIFs

In addition to the concerns on downstream investments by AIFs in debtor companies, the RBI also had concerns on the so-called structured AIFs or AIFs with a distribution waterfall. Whether AIFs can at all have a priority distribution waterfall is currently under SEBI examination and SEBI has stopped AIFs from using structured distribution schemes (by way of accepting fresh commitment or making investment in a new investee company) . However, several existing schemes have such models.

If a lender makes an investment in the subordinated units of a structured AIF scheme such investments will get deducted from the regulatory capital of the lender. The March 27 circular now clarifies that the deduction will be equally from Tier 1 and Tier 2 capital. Further, it also clarifies that the subordinated exposures in the AIF schemes could be in the form of subordinated exposures, including investment in the nature of sponsor units.

Concern areas

Ideally, the bar should have been limited to affiliated AIFs. Affiliated AIFs could have been defined appropriately – for example, a related party, or where the investment manager, or sponsor is a related party of the RE. Extending the bar to all AIFs is quite far from the intent of the circular – which is, admittedly, to curb evergreening. It is difficult to see how unrelated AIFs can be used by an RE to evergreen, as investment decisions of these AIFs are not exercised by the investors.

Ideally, the bar should have been limited only to Cat 1 and Cat 2 AIFs. Cat 3 AIFs, widely known as hedge funds, typically play in equity long/short strategies, or do other leveraged trades. REs find such investment a useful way to diversify their funds into hedge funds. Hedge fund investments are common by institutional investors all over the world; an outright curb on these investments by REs is, once again, beyond the stated intent. Notably, given the wide range of investments that Cat 3 AIFs make, avoiding an overlap with the RE’s borrowers will be quite impractical.

Practical implementation of this circular, if at all a RE invests in an AIF, will be quite tough. AIFs will have to share their potential investment list, which will be against any investment manager’s choice. Assuming there is an overlapped investment, the RE will have to exit within 30 days, which will create liquidity issues for AIFs, in addition to challenging the lock-in restrictions.

Most of the regulated entities took a provision in the 3rd quarter. The 27th March circular of the RBI gives some relief by saying that the provision will be required only to the extent of the downstream investment in a debtor entity.

In our view, there is a need to review the regulatory mechanism for AIFs, as currently, AIFs are being used as instruments of regulatory arbitrage.

The alternative investment management industry in India works in the form alternative investment funds (AIFs), a SEBI-regulated vehicle. Most of the PE, VC funds, and hedge funds in India work in this mode.

Now, SEBI, vide a Consultation Paper dated 19th January heaped a bunch of similar concerns, and required AIFs to affirm that the AIF or investments therein are not being used for regulatory breaches. These concerns, SEBI says, are a result of an ongoing thematic check on the AIF industry, and SEBI says it has already detected at least 40 cases, involving AUM over Rs 30000 crores, where the structure was used to create dents in existing financial regulations.

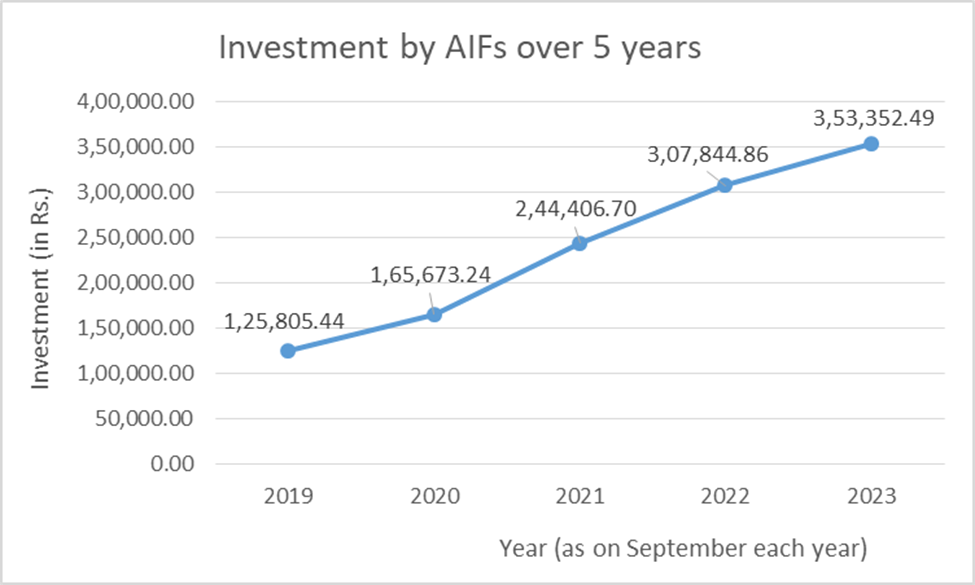

The AIF industry has demonstrated steady growth in recent years. As of September 2023, the assets under management (AUM) of AIFs have surged to 3.88 lakh crores, a substantial increase from the 13,000 crores recorded in September 2015. [See Graph above].

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kotharihttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari2024-01-31 16:48:142024-10-22 15:48:31AIFs ail SEBI: Cannot be used for regulatory breach

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00sanyaagrawalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngsanyaagrawal2023-12-18 13:01:382023-12-18 18:32:12Snippet on credit of existing & issue of new units of AIFs in demat form

The year 2020 – ‘Year of pandemic’, rather we can say the year of astonishing events for everyone over the globe. Without any doubt, this year has also been a roller coaster ride for Alternative Investment Funds (‘AIFs’) with several changes in the regulatory framework governing AIFs in India.

Recent Regulatory Changes for AIFs

In continuation to the stream of changes, Securities Exchange Board of India (‘SEBI’), in its board meeting dated September 29, 2020, has approved certain amendments to the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’). The said amendments have been notified by the SEBI vide notification dated October 19, 2020. The following article throws some light on SEBI (AIFs) Amendment Regulations, 2020 (‘Amendment Regulations’) and tries to analyse its impact on AIFs.

Clarification on Eligibility Criteria

Regulation 4 of AIF Regulations prescribes eligibility criteria for obtaining registration as AIF with SEBI. Prior to the amendment, Regulation 4(g), provided as follows:

“4 (g) the key investment team of the Manager of Alternative Investment Fund has adequate experience, with at least one key personnel having not less than five years experience in advising or managing pools of capital or in fund or asset or wealth or portfolio management or in the business of buying, selling and dealing of securities or other financial assets and has relevant professional qualification;”

The amended provision to 4 (g) extends the meaning of relevant professional qualification, the effect of which seems to add more qualitative criteria to the management team of the AIF, to be evaluated at the time of grant of certification. The newly amended section 4(g) of the AIF Regulations reads as follow:

“(g) The key investment team of the Manager of Alternative Investment Fund has –

adequate experience, with at least one key personnel having not less than five years of experience in advising or managing pools of capital or in fund or asset or wealth or portfolio management or in the business of buying, selling and dealing of securities or other financial assets; and

at least one key personnel with professional qualification in finance, accountancy, business management, commerce, economics, capital market or banking from a university or an institution recognized by the Central Government or any State Government or a foreign university, or a CFA charter from the CFA institute or any other qualification as may be specified by the Board:

Provided that the requirements of experience and professional qualification as specified in regulation 4(g)(i) and 4(g)(ii) may also be fulfilled by the same key personnel.”

It is apparent from the prima facie comparison of language that the key investment team of the Manager may have one key person with five years of experience (quantitative) as well as a personnel holding professional qualification (qualitative) from institutions recognised under the regulation. Further, clarity has been appended in form of proviso to the section that quantitative and qualitative requirements could be met by either one person, or it could be achieved collectively by more than one person in the fund.

With this elaboration, SEBI has harmonized the qualification requirements as that with the requirement specified for other intermediaries such as Investment Advisers, Research Analysts etc. in their respective regulations. Detailed prescription on degrees and qualifications for AIF registration by SEBI is a conferring move and is expected to aid as a clear pre-requisite on expectations of SEBI from prospective applications for registration of the fund.

Formation of Investment Committee

Regulation 20 of AIF Regulations specifies general obligations of AIFs. Erstwhile, the responsibility of making investment decisions was upon the manager of AIFs. It has been noticed by the SEBI from the disclosures made in draft Private Placement Memorandums (‘PPMs’) filed by AIFs for launch of new schemes, that generally Managers prefer to constitute an Investment Committee to be involved in the process of taking investment decisions for the AIF. However, there was no corresponding obligation in the AIF Regulations explicitly recognizing the ‘Investment Committee’ to take investment decisions for AIFs. Such Investment Committees may comprise of internal or external members such as employees/directors/partners of the Manager, nominees of the Sponsor, employees of Group Companies of the Sponsor/ Manager, domain experts, investors or their nominees etc.

These amendments are based on the recommendations to SEBI to recognize the practice followed by AIFs to delegate decision making to the Investment Committee.[1] The rationale behind amendments to AIF Regulations is based on the following merits as proposed in the recommendations::

Presence of investors or Sponsors or their nominees in an Investment Committee which may serve to improve the due diligence carried out by the Manager, as they are stakeholders in the AIF’s investments.

Presence of functional resources from affiliate/group companies of the Manager (legal advisor, compliance advisor, financial advisor etc.) in the Investment Committee may be useful to ensure compliance with all applicable laws.

Presence of domain experts in the committee may provide comfort to the investors regarding suitability of the investment decisions, as the investment team of the Manager may not have domain expertise in all industries/ sectors where the fund proposes to invest.

Thus, the insertion was made, giving the option to the Manager to constitute an investment committee subject to the following conditions laid down in the newly inserted sub-regulation, i.e. Regulation 20(6) of the AIF Regulations given below –

The members of the Investment Committee shall be equally responsible as the Manager for investment decisions of the AIF.

The Manager and members of the Investment Committee shall jointly and severally ensure that the investments of the AIF comply with the provisions of AIF Regulations, the terms of the placement memorandum, agreement made with the investor, any other fund documents and any other applicable law.

External members whose names are not disclosed in the placement memorandum or agreement made with the investor or any other fund documents at the time of on-boarding investors shall be appointed to the Investment Committee only with the consent of at least seventy five percent of the investors by value of their investment in the Alternative Investment Fund or scheme.

Any other conditions as specified by the SEBI from time to time.

The constitution of investment committee is a global standard practice followed by the Funds. However, funds structure in India might be altered with the new defining role of investment committee under the AIF Regulations. The investment committee generally comprises of nominees of large investors in the fund and at times other external independent professional bodies that act as a consenting body towards prospective deals of the fund. The amendment will alter the role of investors holding positions at investment committee as the new defining role might deter them from taking underlying obligations. From the funds perspective seeking external independent professionals might get costly as there is an obligation introduced by way of this amendment regulation. Further, it casts an onus on the investment committee to be involved in day to day functioning of the fund, which used to be otherwise (where members were usually involved in mere finalising the deals). Lateral entry of the members to investment committee post placement of memorandum with the consent of investors is aimed at greater transparency in funds functioning.

Test for indirect foreign investment by an AIF

As per Clause 4 of Schedule VIII of FEMA (Non-Debt Instrument) Rules, 2019 (‘NDI Rules’) any investment made by an Investment Vehicle into an Indian entity shall be reckoned as indirect foreign investment for the investee Indian entity if the Sponsor or the Manager or the Investment Manager –

(i) is not owned and not controlled by resident Indian citizens or;

(ii) is owned or controlled by persons resident outside India.

Therefore, in order to determine whether the investment made by AIFs in Indian entity is indirect foreign investment, it is essential to identify the nature of the Manager/Sponsor/investment manager, whether he is owned or controlled by a resident Indian citizen or person resident outside India.

RBI in its reply to SEBI’s query on downstream investment had clarified that since investment decisions of an AIF are taken by its Manager or Sponsor, the downstream investment guidelines for AIFs were focused on ownership and control of Manager or Sponsor. Thus, if the Manager or Sponsor is owned or controlled by a non-resident Indian citizen or by person resident outside India then investment made by such AIF shall be considered as indirect foreign investment.

Whether an investment decision made by the Investment Committee of AIF consisting of external members who are not Indian resident citizens would amount to indirect foreign investment?

In light of the above provisions of the NDI Rules and with the introduction of the concept of an “Investment Committee”, SEBI has sought clarification from the Government and RBI vide its letter dated September 07, 2020[2].

Conclusion

With the enhancement in eligibility criteria, SEBI has ensured that the investment management team of the AIF would have relevant expertise and required skill sets.

Further, giving recognition to the concept of an investment committee will cast an obligation on investment committee fiduciary like obligations towards all the investors in the fund. . However, there exists certain ambiguity under the NDI Rules, for applications wherein external members of investment committee who are not ‘resident Indian citizens’, which is currently on hold and pending receipt of clarification.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kothari Consultantshttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari Consultants2020-11-23 17:53:132020-11-23 17:54:562020 - Year of changes for AIFs

The Reserve Bank of India (‘RBI’) vide notification dated October 17, 2019 had notified the Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt instrument) Regulations, 2019[1] (‘the Regulations’) governing the mode of payment and reporting of non-debt instruments consequent to the Foreign Exchange Management (Non-Debt Instrument) Rules, 2019[2] framed by the Ministry of Finance, Central Government.

RBI has recently vide its notification dated June 15, 2020 notified Foreign Exchange Management (Mode of Payment and Reporting of Non-Debt Instruments) (Amendment) Regulations, 2020[3] amending Reg. 3.1 dealing with Mode of Payment and Remittance of sale proceeds in case of investment in investment vehicles.

Let us discuss few terms to understand the recent amendments to the Regulations.

Investment Vehicles under FEMA:

According to FEMA (Non-Debt Instruments) Rules, 2019, investment vehicles mean:

Different types of account available under FEMA (Deposit) Regulations, 2016[1] (‘Deposit Regulations’)

The following are the major accounts that can be opened in India by a non-resident:

A significant advantage of SNRR over NRO is that the former is a repatriable account while the latter is non-repatriable.

What is Special Non-Resident Rupee (‘SNRR’) Account?

Any person resident outside India, having a business interest in India, may open SNRR account with an authorised dealer for the purpose of putting through bona fide transactions in rupees. The business interest, apart from generic business interest, shall include the following INR transactions, namely:-

Investments made in India in accordance with Foreign Exchange Management (Non-debt Instruments) Rules, 2019 dated October 17, 2019 and Foreign Exchange Management (Debt Instruments)

Import of goods and services in accordance with Section 5 of the Foreign Exchange Management Act 1999 Regulations, 2019;

Export of goods and services in accordance with Section 7 of the Foreign Exchange Management Act 1999;

Trade credit transactions and lending under External Commercial Borrowings (ECB) framework;