Presentation on Controls over RPTs.

Read more on RPTs here.

Read more on RPTs here.

Team Corplaw | corplaw@vinodkothari.com

Refer our related resources:

Read our other resources:

– Team Corplaw | corplaw@vinodkothari.com

SEBI in its Board meeting dated December 18, 2024, has approved amendments pertaining to BRSR, HVDLEs, DTs, SMEs, Intermediaries, etc. This article gives a brief overview of the approved amendments.

Immediate actionables for Listed entities:

VKCo comments: In addition to the corresponding obligations on the issuer, CP also proposed to mandate Depositories and Stock exchanges to provide requisite information to DTs, which is yet to be approved. The right to call information from issuers and market participants including corresponding obligations on them will enable DTs to perform their functions efficiently.

VKCo comments: While the introduction of model DTD is appreciated, the draft model DTD proposed in the CP was not aligned with the general market practices followed by the DTs as well as the applicable laws such as SEBI Listing Regulations, NCS Regulations, Indian Trust Act, etc.

Under this segment of changes discussed by SEBI, most of the proposals are in alignment with the Consultation Paper dated 31st October, 2024, except for few changes in relation with PSUs coming together with public enterprises under Public Private Partnership.

VKCo Comments: The proposal to enhance the extant threshold is encouraging in terms of governing the maximum value of outstanding debt while at the same time achieving the same without bearing the burden of compliance by an increased number of purely debt listed entities. Subsequently, effective implementation of such a proposal aligns it with the identification criteria of Large Corporates.

VKCO Comments: While this proposal is noteworthy, however, instead of rolling out a new chapter, there could have been certain modifications in the existing regulations by way of a proviso to align with the needs of an HVDLE. Further, one also needs to wait to see the fine print -of the provisions once the same is issued.

VKCo Comments: The proposal is welcome since it clearly sets the HVDLEs free from the barrier of once an HVDLE so always an HVDLE. This proposal sets a clear nexus between the compliance and the size of the debt outstanding, for the protection of which in the very first place, the compliance triggered.

VKCo Comments: Given the close construct of debt listed entities, it is often observed that the constitution of such committees becomes more of a hardship than in smoothing compliance and discussing specific matters. Accordingly, it looks appropriate to redirect the functions of NRC and RMC to the Audit Committee and that of the SRC to the Board.

VKCo Comments: The rationale completely aligns with the proposal made and seems to be justified. Further, as far as the exclusion is concerned, this seems more from excluding those members who are part of the board not on the basis of their appointment but their current tenure being served in a particular position in the company.

VKCo Comments – While the CP suggested two ways of seeking approval for material RPTs of an HVDLE. The Board has only considered the alternative mode of first seeking NOC of DT and thereafter approaching the shareholders. Further, as discussed in our related write up on the CP, there does not seem to be any incentive to first approach the DT and thereafter the DT to approach the NCD holders. Instead the approval of the NCD holders can be taken up directly by the HVDLE.

VKCo Comments: The inclusion of a voluntary provision in the legislation with respect to a comprehensive report like BRSR is not likely to be submitted given the huge details under the BRSR. However, an opportunity to submit BRSR can be a game changer for an HVDLE from the perspective of being able to raise funds based on its reporting standards in this regard.

One of the changes discussed by the Board is relaxation to HVDLEs set up under the PPP mode from composition requirements of directors. While this was not a part of the CP, however, even if we have to understand that change proposed, this looks like relaxing the composition requirement of the Board of Directors.

CHANGES NOT APPROVED:

VKCo Comments: This proposal was with an objective to align and standardize the filing of quarterly CG compliance report for bringing parity as in the case of equity listed entities

VKCo Comments: While SEBI refers to the introduction of similar exclusion for equity listed entities, however, it has also mentioned the subsequent amendment wherein the same was omitted. The proposal not being notified is in alignment with the position of equity listed entities, however, the same would have been a welcome change since it would have helped such entities to give preference to their principal statutes and not an ancillary one like LODR.

Our detailed write up on the CP can be accessed here.

Refer to our discussion on CP in: Laundry List: SEBI’s proposal to elongate list of deemed UPSIs

– Vinita Nair, Senior Partner (corplaw@vinodkothari.com)

This version: 3rd April, 2025 (Updated as per SEBI Circular dated 1st April, 2025)

With the enforcement of recent amendments in LODR Regulations effective December 12, 2024 a qualified company secretary appointed as a Compliance Officer (‘CO’) is required to be an officer, who is in whole-time employment of the listed entity, not more than one level below the board of directors, designated as a Key Managerial Personnel (‘KMP’) and form part of senior management.

Listed entities now face the question of whether this entails a re-look at the organisation structure, hierarchy, profile of the CO? Whether the board of directors needs to be sensitised of this requirement and the impact, if any?

Watch our YouTube video on the same here.

Scope of “compliance”

The Basel paper of 2005 gives clarity on what is compliance, and the ambit of compliance function. First of all, the scope of the word “compliance” is not limited to laws and regulations only. “Compliance laws, rules and standards have various sources, including primary legislation, rules and standards issued by legislators and supervisors, market conventions, codes of practice promoted by industry associations, and internal codes of conduct applicable to the staff members of the bank. For the reasons mentioned above, these are likely to go beyond what is legally binding and embrace broader standards of integrity and ethical conduct.”

The compliance function is a cornerstone of an entity’s governance, internal control, and risk management framework. It includes the systems, procedures, and organisational infrastructure required to ensure:

Appointment of Compliance Officers (‘COs’)

Appointment of COs is required under different statutes. In case of listed entities, for the purpose of ensuring compliance with securities law, appointment of CO is specified in the initial listing regulations viz. SEBI ICDR[1], SEBI ILNCS[2] Regulations and the responsibility of CO for continuous listing requirement is included in the common obligations under LODR. In case of LODR the person is required to be a qualified Company Secretary (‘CS’) and in case of ILNCS, the CS of the issuer is required to be the CO. Similarly, the requirement under the Listing Agreement[3] was to appoint the CS of the issuer as the CO.

SEBI PIT Regulations (applicable to a listed entity as well as an intermediary/ fiduciary) requires appointment of a senior officer, who is financially literate and is capable of appreciating requirements for legal and regulatory compliance under PIT regulations as the CO, who reports to the board of directors and ensures compliance of policies, procedures, UPSI preservation, implementation of codes etc, under the overall supervisions of the board of directors.

Additionally, Banks, NBFCs, Insurance companies, SEBI registered intermediaries, etc all are required to appoint CO as per laws specifically applicable to the company operating in that particular sector.

Whether one person can serve as CO for each of the above requirements? This is surely feasible, unless there is an express bar. For e.g., in case of banking regs/ NBFCs regs, there is a bar on dual hatting – that is, the CO as per those laws should not be dealing with any other line function.

Position of CO under LODR post amendment

It may be contended that the role of a CS is a mix of compliance and ministerial functions. He/ she may be tasked with several other functions as well – depending on the organization. The provision of the LODR Regs is obviously not concerned with either other functions performed by the CO, nor with other compliance roles.

The intent of the provision, as we read it, is that the compliance function pertaining to LODR Regs is directly discharged by the CO under the supervision of the board of directors. The board has the supervisory responsibility, and the CO has the executive responsibility. The provision is intended to attach significance to the organisation-wide role of compliance function.

As observed from the report of the Expert Committee, recommendations were made for strengthening the position of the CO. The challenge faced by the CO, despite forming part of ‘senior management’, was inability to advise the management to act in accordance with the law and being in a position to get influenced by other people in senior management due to the reporting structure. Therefore, the suggestion was for appropriate positioning to get adequate power, commensurate with the responsibilities cast upon the CO, to be able to advise the management on points of law and ensure effective discharge of statutory duties and responsibilities.

In the light of above, the regulations now clarify the position of the CO by having them one level below the board of directors. Here the intent of the regulator, in our reading, did not seem to define the organisational structure, but to clear the path for the CO for effective discharge of its responsibilities. In our view, the amendment results in fixing the responsibility of the CO and that the CO, now, cannot shirk its responsibility or cannot take the pretext of being a junior person, having no power or access, having a reporting line limited to someone in senior management. It now provides the CO with straight access to the board of directors, when it comes to ensuring compliance with LODR requirements. To the extent of the compliance function the CO will now be directly accountable to the board.

The way we read this requirement is that it certainly attaches significance to the compliance function, and therefore, may result in repositioning of compliance officers in the organization hierarchy. But is the law concerned with organisation hierarchy, designations, scales, ranks, etc? In our view, the objective of the law is attained by a functional reporting line to the board. This is also evident from SEBI’s analysis of the suggestions/ comments received,[4] that the objective is to empower COs to perform their duties and discharge their responsibilities effectively. Some companies do have the practice of having a CO report to the Managing Director / CEO. However, it is for the listed entity to decide the reporting structure of its KMPs and senior management while ensuring compliance with the regulatory requirements.

However, SEBI has issued a Circular dated April 1, 2025, where SEBI states: “it is clarified that the term ‘level’ used in regulation 6(1) refers to the position of the Compliance Officer in the organization structure of the listed entity. Therefore, ‘one level below the board of directors’ means one level below the Managing Director or Whole-time Director (s) who are part of the Board of Directors of the listed entity.” After issuing this Circular, SEBI staff has also issued two Informal Guidance letters, being for DCB Bank Ltd and Pakka Ltd.

Hence, SEBI seems to be clearly opining that SEBI is intending the organisational hierarchy of the entities to also be adjusted to reflect the CO’s position at one level below the board.

Reporting structure of CO post amendment

Organizational hierarchy is a matter of many things. Regular reporting structure for the various functions that a position has: lines of authority and responsibility, scales and other benefits related to the scale, promotion policies, regular administrative roles such as approval of claims, benefits, etc

The CO stands empowered to manage the compliance function independently and without fear, and to that extent the CO needs to report to the board. However, boards meet infrequently. The company may or may not have an MD/ WTD – it may be working with a CEO/president reporting to the board. It is quite possible in an organisation to have one or more WTDs who report to the MD. There are several officers who report to the MD but their level in the organisation is not the same as those of other seniors placed at one level below the board. In such cases, whether the CO reporting to an MD is a sufficient compliance? SEBI’s IG, specifically in the matter of DCB Bank Ltd , seems to answer in the negative. Therefore, SEBI suggests the organisational levels also to align to the expected reporting lines. Therefore, the amendment, seen in the SEBI’s circular of 1st April, is concerned with both reporting lines as well as organisational hierarchy of the CO. Irrespective of the SEBI Board agenda dated 30th September, 2024 stating that organisational structure is an internal matter for companies, “…it is for the listed entity to decide the reporting structure of its KMPs and senior management while ensuring compliance with the regulatory requirements”, it seems that the regulator has done so in the 1st April 2025 circular. Although, in general, the organisational hierarchy usually corresponds to and is commensurate with functional hierarchy; however, the law has sought to interfere with the organisational structure.

CS as CO under LODR

Does the amendment necessitate a relook on whether the CS can continue as CO? The answer to this also seems negative, as law only prescribes who can be the CO. SEBI has also clarified that the CO and CS may be different persons. While law admits having different persons occupying the position, practically, it seems less feasible in view of the overlap and interconnectedness in the functions discharged by a CS in terms of Companies Act, 2013 and by a CO under LODR.

Actionable for listed entities

The amendment is certainly required to be sensitised to the board of directors. However, do the regulations expect companies across the country to revisit their organisational structures? SEBI has expressed its views in the 1st April, 2025 circular. Therefore, listed entities need to evaluate if the functional level and organisational level of the CO is in line with the regulatory requirements and expectations. If no, listed entities may want to revisit the same.

Power brings onus

Everyone may also readily understand that SEBI’s intent in empowering the CO is not just to confer a new power, but to be able to hold the CO answerable for any compliance gaps. Therefore, if it is a new cap that the CO is donning, the cap is made of flowers and nettles both.

[1] Reg 23 (8) ICDR – The issuer shall appoint a compliance officer who shall be responsible for monitoring the compliance of the securities laws and for redressal of investors’ grievances.

[2] Reg 27 (4) of ILNCS – The lead manager(s) shall ensure that the draft offer document clearly specifies the names and contact particulars including the postal and email address and telephone number of the compliance officer who shall be a Company Secretary of the issuer.

[3] The requirement was notified on May 18, 1999 pursuant to the recommendations of the Accounting Standards Committee constituted by SEBI under the Chairmanship of Shri Y. H. Malegam to the effect that Compliance officer to be appointed by Listed companies in Compliance with Circular No. SMD/POLICY/CIR-06/98 dated February, 12, 1988 (every company shall appoint a Senior Officer as Compliance Officer) shall be the Company Secretary of the Company.

[4] Agenda of SEBI BM dated September 30, 2024 [Clause (iii) (a) of Para 28.3.2].

Other Resources on LODR:

Loading…

Loading…

Read our other resources:

SEBI notifies changes that take immediate effect

– By Team Corplaw (corplaw@vinodkothari.com)

– Updated as on 24.01.2025

Please find details about our workshop on the same here: https://vinodkothari.com/2024/12/online-workshop-on-sebi-lodr-3rd-amendment-2024/

Loading…

Other Resources on LODR:

– SEBI cautions investors from transacting in securities of unlisted public companies on electronic platforms

– Burhanuddin Kholiya (corplaw@vinodkothari.com)

From rental rooms to cabs to domestic furniture, almost everything is made available using technological aggregators. But the moment one tries to sell securities on public platforms, the chances of potential investors being duped by dream merchants increase – something which regulators have very carefully barred over the years. Hence, unless it is a recognised stock exchange, making securities available on public platforms constitutes “offer for sale”. Sometimes, people look at the number of investors as less than 200 and tend to argue that is not a deemed public offer, but it is important to understand that if the offer has gone to people in general, the actual number of investors who bite the bait does not matter.

Many platforms encourage investments in unlisted or pre-IPO stocks. At times bunching either securities or investors. SEBI, in its press release dated December 9, 2024, warned investors against transacting on such platforms, emphasizing the risks involved and clarifying that these platforms operate outside SEBI’s regulatory framework.

On the intermediaries front, stock brokers are permitted to deal only on recognised stock exchanges and are prohibited from facilitating trading outside these exchanges. In 2022, SEBI extended its regulatory framework to Online Bond Platform Providers (‘OBPP’) by mandating them to register as stock brokers in the debt segment and restricted their offerings to listed debt securities or debt proposed to be listed through a public offering. Only recognized stock exchanges are authorised to provide a platform for fund raising and trading in securities of “to be listed” and “listed” companies.

Apart from above, today, numerous platforms have emerged offering unlisted securities to the public at large. However, being unregulated, it poses significant risks to investors. While SEBI’s mandate may not extend to unlisted securities, it continues to caution investors about platforms dealing with such securities. Recognizing the potential risks and lack of oversight, SEBI and the Registrar of Companies (ROC) have issued several orders against platforms offering unlisted securities to the public. These actions aim to protect investors from being misled and address violations of private placement & public issue related provisions under the Companies Act, 2013.

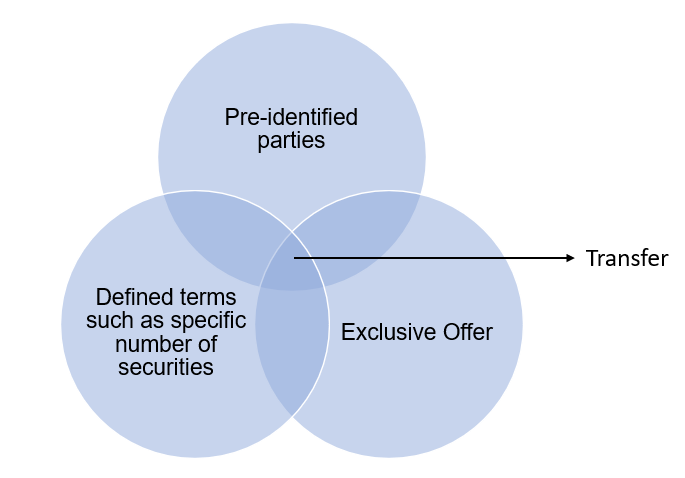

Unlisted securities are primarily traded by way of a transfer. Traditionally, the transfer of securities is a private arrangement between two identified parties, namely the transferor and the transferee, who explicitly agree on the sale and purchase of a fixed number of securities.

The key distinction between transfer of securities and public offer of securities lies in the pre-identification of parties, exclusive offer and defined terms.

Therefore, when securities are offered for sale to unidentified persons without limiting the number of purchasers, this could effectively constitute an indirect public offer (which also includes an offer for sale).

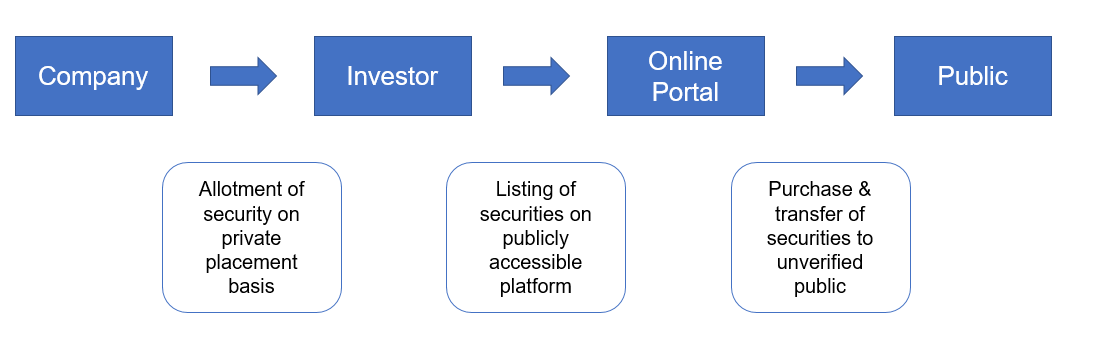

As pointed out above, many unregistered platforms offering unlisted securities have emerged. These platforms often target unidentified persons and provide no limit on the number of purchasers, effectively transforming such offers into indirect public offers in the form of “offer for sale”.

Listing securities for sale on a publicly accessible platform may, intentionally or unintentionally, transform a private arrangement into an offer resembling a public offer. Unlike private transfers, public offers are subject to stringent regulatory requirements, such as issuing prospectus, detailed disclosures, and continuous regulatory oversight. Failing to adhere to these requirements could undermine investor protection and market integrity.

The practice of structuring transactions as secondary sales is an innovative strategy employed by fintech platforms to broaden market access while navigating regulatory challenges. However, this approach raises significant concerns about compliance, investor protection, and market integrity. Striking a balance between innovation and regulatory compliance is essential to establish a transparent, fair, and robust investment ecosystem.

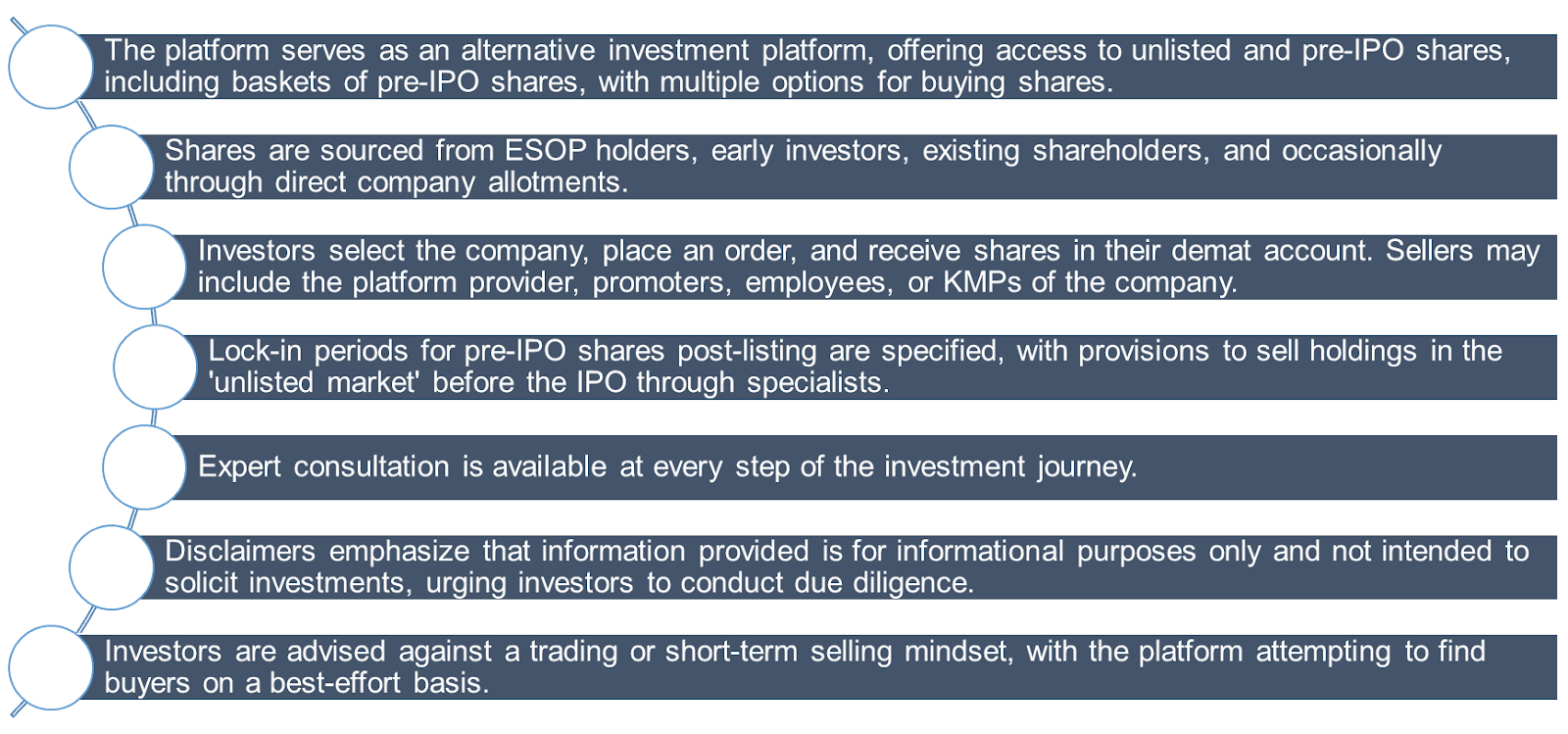

In this model, a fintech platform, operating through its legal entity, subscribes to securities offered via private placement by a company. Often, these platforms are the sole or principal investors in such placements. Once the securities are acquired, the platform lists them on its portal as available for investment by way of transfers from itself to individual investors, presenting them as secondary market transactions ostensibly outside the scope of public offer regulations. The interface almost resembles a broking app, where one can click and ‘buy 1 share’ instantly.

In some cases, the platform and the warehousing entity are separate. Additionally, some platforms claim that the transferors comprise of promoters, employees, KMPs of those enlisted public companies.

Motivations behind structuring as Secondary Sale are twofold:

1. Avoiding Public Offer Regulations:

Public offers of securities are subject to extensive regulatory oversight, including stringent disclosure requirements and mandatory listing. By structuring transactions as secondary sale, platforms consider to bypass these regulations.

2. Enabling Retail Investor Access:

Structuring investments as secondary sale allows platforms to make securities available to retail investors who might otherwise be ineligible to participate in private placements.

As discussed earlier, an offer that can be accepted by anyone effectively qualifies as a public offer, regardless of how it is officially labeled. In contrast, private placements are designed for a limited, pre-identified group of investors and are subject to stricter regulatory controls to maintain their exclusivity.

Fintech platforms, however, challenge this distinction by leveraging technology to make securities accessible to a broad audience of unverified users, thereby creating a regulatory gray area. By listing securities on their portals—accessible to anyone who registers—these platforms effectively transform private placements into publicly available investment opportunities.

Moreover, these platforms often lack stringent verification processes to ensure that users meet the criteria for accredited or eligible investors. Instead, they use digital advertising, user-friendly applications, and social media campaigns to promote investment opportunities, indirectly engaging in general solicitation. This practice, while sometimes technically compliant, directly conflicts with the principles governing private placements, which prohibit public solicitation.

These practices raise significant concerns regarding investor protection and compliance with the existing regulatory framework. By making securities easily accessible to a wide, largely unverified audience, fintech platforms blur the line between private and public offerings. This not only undermines the purpose of private placement regulations but also exposes retail investors to potential risks without the safeguards typically associated with public offers.

While fintech platforms argue that their practices promote financial inclusion and innovation, they also highlight the urgent need for regulatory clarity. Striking a balance between fostering innovation and ensuring compliance is critical to maintain market integrity and protect investors.

Fintech platforms often claim that the pricing of unlisted shares is driven by demand and supply, similar to listed securities. However, this approach diverges significantly from standard practices for valuing privately placed securities, which typically rely on Fair Market Value (FMV) mechanisms.

Unlisted securities, being inherently illiquid and less transparent, are usually valued based on financial fundamentals, such as earnings, book value, or discounted cash flows, rather than speculative demand and supply dynamics. The reliance on a demand-supply pricing mechanism for illiquid securities can result in significant price distortions. Prices may be artificially inflated or deflated, often without any material change in the underlying company’s fundamentals.

This speculative approach to pricing can mislead investors into believing that the listed price represents a fair valuation of the security. In reality, such pricing mechanisms expose investors to risks of overvaluation or mispricing, especially in the absence of robust valuation methodologies.

Furthermore, the process for investors seeking to liquidate their unlisted shares on these platforms is often vague and lacks the transparency necessary for informed decision-making. Without clear guidelines on how prices are determined or how liquidity is managed, investors may face challenges in accurately assessing the risks and returns associated with their investments.

The aforementioned two modes of issuance differs from each other on various parameters:

| Parameters | Private Placement | Public Offer |

| Meaning | Offer or invitation to a select group of persons to subscribe to securities, excluding the general public. | Includes IPO or FPO of securities to the public or an offer for sale of securities by an existing shareholder through issue of prospectus. |

| Who can invest? | Restricted to pre-identified investors addressed in the private placement offer-cum-application letter. | Open to the public at large. |

| Maximum number of investors | 200 persons in a financial year, excluding QIBs and employees offered securities pursuant to ESOP scheme under Section 62 (1) (b) of CA, 2013. | No maximum limit on number of investors. |

| Offer Communication | Communicated directly to the identified investor; cannot be advertised to the general public. | Communicated via advertisements, circulars, or a prospectus to the public. |

| Process | Conducted via a private placement offer-cum-application, adhering to specific conditions outlined in Section 42 of Act. | Requires a prospectus with mandatory disclosures and regulatory oversight, governed by SEBI (ICDR) Regulations, 2018 |

In terms of Section 25(2) of CA, 2013 a private placement will be considered as securities being offered for sale to the public if it is shown that an offer of the securities or any of them was made within 6 months after the allotment or agreement to allot; or on the date when offer was made, the consideration was not received by the company in respect of the securities. Therefore, subscribing to private placement merely with the intent to warehouse temporarily and downsell to the public will attract the public issue norms. Penal provisions for flouting private placement norms, not following public issue norms are quite stringent.

While securities of public companies are freely transferable, it cannot be traded on unregulated platforms. The fintech platform’s current modus operandi raises concerns about pricing practices, process transparency, and regulatory compliance. SEBI’s advisory underscores the need for vigilance, as these platforms often lack regulatory oversight, investor safeguards, and transparency. Unlike public issues, which ensure grievance redressal mechanisms like SCORES and SMART ODR transactions on these platforms leave investors without formal recourse. The numerous platforms offering unlisted equity shares need to revisit in view of SEBI’s caution letter.