Key Takeaways – 12th Securitisation Summit, 2024

Loading…

Loading…

Access our Publication launched during the 12th Securitisation Summit here.

Interest Imbalance: Will the disproportionate interest Split in Loan Transfers be liable to withholding tax?

ITAT Ruling Clarifies Taxation on Disproportionate Interest share in Loan Transfers

– Dayita Kanodia | Finserv@vinodkothari.com

Direct Assignment of a loan or transfer of loan exposures refers to the process where financial institutions, such as banks, purchase a pool of loans or assets from other entities, typically NBFCs, without the involvement of a third-party intermediary. In this arrangement, the buying institution directly acquires the ownership of the loans or assets and the associated rights, including the right to receive future payments from the borrowers. This method allows the selling NBFC to offload its loans, thereby freeing up capital, while the purchasing institution gains the opportunity to enhance its loan portfolio and earn interest income from the acquired loans. This Direct Assignment is essentially what is popularly known as the transfer of loan exposure.

The RBI issued the transfer of loan exposures directions in 2021 regulating all transactions among regulated entities involving transfer of loan exposures.

Interest sharing and servicing after the transfer

Pursuant to a transfer of loan, it is not necessary that the future interest income arising from the loans would be shared in the same proportion as that of the transfer. For instance, if an NBFC assigns 90% of the loan portfolio to a bank, there is no mandate that all interest income received in the future would be shared in the same proportion of 90:10. Generally, the borrower is not made aware of the transfer and therefore it is important that the NBFC continues to service the loan. In such cases it is only fair that the NBFC gets a higher proportion of interest. Accordingly, it is quite common in direct assignment transactions to have a disproportionate interest share.

The question which now arises is whether this excess interest income retained by the NBFC would be taxable under the provisions of the income tax act.

ITAT Ruling and taxation on disproportionate interest share in loan transfers

A recent ITAT ruling of May 7, 2024 clarifies the taxation treatment for disproportionate interest share in case of loan transfers. In this case, NBFC assigned 90% of the loan portfolio to a bank via the direct assignment route. However, the bank was not receiving the entire interest on the 90% loan assigned but was only entitled to a fixed percentage of share while the NBFC retained the excess interest. Accordingly, the revenue department was of the view that the assessee was responsible to deduct TDS on the excess interest allowed to be retained by the NBFC under section 194A of the Income Tax Act.

The revenue department further raised the question on deduction of TDS under SEction 194J and 194H of the Income Tax Act.

Interest Retained not a result of money borrowed or debt incurred by the transferee

For the deciding the fate of the NBFC under section 194A of the Income Tax Act, the following was observed by the ITAT:

- For TDS to be deducted under section 194A of the Income Tax Act, the crucial aspect to be satisfied was whether the part interest allowed to be retained by the originating NBFC by the bank is payment in the nature of interest to the NBFC for any money borrowed or debt incurred by the bank.

- It was acknowledged that the 90% of the loan portfolio was assigned to the bank and consequently any default among the assigned loans would result in loss to the bank.

- Any amount collected from the borrowers was initially getting deposited in an escrow account and was subsequently distributed between the NBFC and the bank in accordance with the agreement entered into by the entities.

- It could not be shown that the interest allowed to be retained with the NBFC was a result of any money borrowed or debt incurred by the bank from the NBFC.

- Accordingly, the assessee was under no obligation to deduct TDS on the excess interest retained by the NBFC under section 194A.

Interest retained not in the nature of fees for any professional / technical services rendered by the transferor

The next issue which was adjudicated in the case was whether the interest allowed to be retained with the NBFC was a consideration for rendering professional / technical services by the transferor NBFC to the transferee bank.

As per section 194J of the Act, any person, not being an individual or HUF, who is responsible for paying to a resident any sum, inter alia, by way of fees for professional services or fees for technical services shall at the time of credit of such sum to the account of payee deduct tax at source.

For this purpose the ITAT observed the following:

- The NBFC and the Bank entered into a tripartite service agreement pursuant to which the originating NBFC was appointed as servicer for the loans. The NBFC was therefore responsible for managing, collecting and receiving payment of the receivable and depositing the same in the ‘Collection and Payout Account’ to enable the distribution of the payout therefrom and providing certain other services.

- As per the service agreement, a one time service fee of Rs.1 Lakh was agreed to be payable by the bank to the NBFC as consideration for the services rendered.

- The ITAT brushed aside the contention of the revenue department that service fee of Rs 1L was inadequate and the excess interest allowed to be retained by the NBFC should in fact be considered as fee for rendering the services by the transferor NBFC.

- There was a separate tripartite Deed of Assignment of receivables entered into by the parties according to which the bank paid the entire principal amount equivalent to 90% of the entire pool to the NBFC upfront. However, it was observed that the transfer being an independent commercial transaction cannot be on a cost to cost basis without there being any markup.

- Accordingly, the bank opted to pay the consideration for the loans assigned partially by way of an upfront payment equivalent to the principal amount of the loan assigned to it and partly by agreeing to earn a lower rate of interest on its portion of assigned loans and allowing the NBFC to retain the part interest received from the borrower.

- Therefore the liability under section 194J of the Income Tax Act was only for the service fee of Rs.1 L and cannot be extended to the excess interest share retained by the NBFC.

- Accordingly, the assessee was under no obligation to deduct TDS on the excess interest share retained by the NBFC under section 194J of the Income Tax Act.

Interest retained not in the nature of commission / brokerage

The last issue in this case to be decided before the ITAT was whether the retained interest would fall in the category of commission or brokerage and was liable to TDS under section 194H of the Income Tax Act.

As per section 194H of the Act, any person, not being an individual or HUF, who is responsible for paying to a resident, any income by way of commission or brokerage, shall at the time of credit of such income to the account of the payee deduct tax.

For determining the tax treatment under this section, the ITAT observed the following:

- It could not be said that the loans originated by the NBFC were on behalf of the bank.

- For the services rendered by the NBFC, it was observed that the same was pursuant to a separate service agreement which provides for payment of separate service fees in lieu of such services.

- Accordingly, it cannot be contended that the transferor NBFC was acting as an agent of the transferee bank.

- Accordingly, the liability to deduct TDS on the excess interest retained by the NBFC under section 194H of the Income Tax Act does not arise.

Concluding Remarks

In conclusion, the recent ITAT ruling has provided significant clarity on the taxation treatment of disproportionate interest shares in loan transfers, particularly in the context of Direct Assignment transactions.

In this case, the ITAT emphasized that the interest retained by the NBFC was not a result of any money borrowed or debt incurred by the bank. Additionally, it was clarified that the interest retained did not constitute fees for professional or technical services rendered by the transferor NBFC, nor did it fall within the ambit of commission or brokerage.

As the financial landscape continues to evolve, such judicial pronouncements play a crucial role in fostering transparency, compliance, and fairness in taxation.

Online workshop on Verification of Market Rumour by listed entities and other related amendments

| Register here |

Loading…

Other resources on the amendment:

- YouTube video on aforesaid amendment: https://www.youtube.com/watch?v=-BvHsUtR4TI&feature=youtu.be

- Article on Top companies forced to respond to rumours on big price spikes: Changes in Listing Regulations relate rumour responses to “material price movement”

- Snippet summarizing the amendment: https://lnkd.in/gSJM-YUj

SEBI notifies rumour verification requirements, application of market cap based provisions etc

Ankit Singh Mehar, Senior Executive and Khushi Hariyani, Executive | corplaw@vinodkothari.com

Loading…

Also see our related resources:

- FAQs on Verification of Market rumour by Listed Entities

- Presentation on Verification of Market Rumour by listed entities and other related amendments

- Top companies forced to respond to rumours on big price spikes: Changes in Listing Regulations relate rumour responses to “material price movement”

- Silence no more golden: New regulatory regime forces top listed companies to respond to rumours

- Getting material on “material” events and information: SEBI notifies amendments to Listing Regulations

- Demystifying rumour verification by listed entities

Top companies forced to respond to rumours on big price spikes: Changes in Listing Regulations relate rumour responses to “material price movement”

– This version: 21st May, 2024

Team Corplaw | corplaw@vinodkothari.com

| Given the significance of the amendments, we are organizing an online workshop on Verification of Market Rumours by listed entities and other related amendments on Monday, 27th May, 2024. Details of workshop can be accessed here Register here |

Regulatory instruments and standards on rumour response:

- Reg 30(11) as amended

- Framework on Material Price Movement (in Equity Cash Markets) with respect to Rumour Verification by Listed Entities by stock exchanges

- Framework for considering unaffected price for transactions upon confirmation of market rumour

- Industry Standards Note on verification of market rumours under Regulation 30(11) of LODR Regulations

- SEBI Circular granting regulatory recognition to ISF standards

What is the change? And applicable from when?

- Reg 30 (11) & (11A) of Listing Regulations dealing with rumour verification. There was a work in progress at SEBI on making the regulation more certain and easier-to-implement. Changes were made in Re. 30 (11) requiring top 100/top 250 companies to mandatorily respond to market rumours, but there were several issues in implementation. SEBI Consultation Paper w.r.t. Verification of Market Rumours (‘CP’) based on the recommendations of the Industry Standards Forum (ISF) and subsequently, SEBI Board decision taken in the meeting held on March 15, 2024 resulted into these changes.

- Original implementation dates were October 1, 2023 and thereafter, extended twice to February 1, 2024/ August 1, 2024 and thereafter to June 1, 2024/ December 1, 2024 for top 100/ top 250 companies1. It is now confirmed that the implementation dates remain the same.

- Further, SEBI vide Circular dated May 21, 2024 has given recognition to the Industry Standards Forum (‘ISF’)2 that released the Industry Standards Note (ISN) on rumour verification in order to facilitate uniform approach and set out an SOP for compliance with rumour verification requirement. The compliance with Industry Standards are mandatory for the listed entities [SEBI Circular dated 21 May, 2024]. The ISN inter alia covers following aspects:

- Delineation of “mainstream media” (as requirement to respond will only be applicable to rumours reported in specific media sources (see below) ;

- Guidance on rumour responses through illustrative scenarios pertaining to potential M&A transactions, ;

- Guiding principles through some illustrative non M&A transaction scenarios, such as whistleblower complaints, internal investigations, potential change in KMPs, ill health of MD/ CEO etc.

- Who will be impacted, and from when?

- Top 100/top 250 companies based on market capitalisation.

- Presently as per March 31, 2024

- Effective from December 31, 2024 based on the average market capitalisation from July 1 to December 31 of that calendar year

- Top 100 companies – 1st June 2024

- Top 250 companies – 1st Dec 2024

- For the rest of the companies, the framework is still voluntary, but logically, the reference point being “material price movement” may be extended to these companies too.

- What will affected companies be required to do?

- If:

- There is a material price movement (MPM)

- There is a rumour in mainstream media

- About some definitive event or information

- Which is “impending”, that is, about to happen or waiting to be disclosed by the Company.

- The company shall respond:

- Either confirm that rumour

- Or deny it

- Or make a statement that the rumoured event has not become disclosable at the present time

- Or remain silent, if the rumour does not qualify for a response in terms of the ISN

- And for either confirmation or denial, if the company needs further information from a promoter, director, KMP, or SMP (that is, the rumoured information pertains to them), the company shall promptly seek the same, and the counterparty shall promptly, accurately and adequately respond to the same.

- The company shall do the confirmation or denial or provide a clarification within 24 hours from the trigger of the MPM

- The company need not respond:

- If the rumoured event or information is not “specific”, or does not otherwise qualify for a response

- If the rumoured event/information pertains to the pre-intimated items in a notice of Board meeting u/r 29 (1) of Listing Regulations .

- Appropriate disclosure to be made after conclusion of the Board meeting.

- However, if the rumour goes beyond the information in the pre-intimation, and otherwise qualifies for response, the company will respond.

- Basic attributes of a rumour requiring response:

- Should be relating to the Company and not generally about sector, industry, geography, etc

- Should be specific, that is, should give some facts/information likely to influence the decision of investors, or should have quoted a source which can be relied for the information in question

- Should be relating to an event/development which is impending, that is, imminent, at a stage of development

- Should not be an elaboration of something that has already been disclosed by the Company, unless new material facts or information not disclosed by the company are contained

- Should be contained in “mainstream media”

- Should have caused an MPM

- There should be a reasonable nexus between the rumour and the MPM, so as to lead to a conclusion that the MPM has been triggered by the rumour

- What is the trigger point of the MPM (MPM Trigger)?

- Since MPM (see discussion below) is based on price movements during a day, the trigger point may happen at any time during trading hours.

- What is MPM?

- As per the Framework provided by NSE, the parameters for MPM are as under:

- Cut off percentages [that is, 5, 4 or 3%, +/- relevant index variation in the same direction as the MPM – see below] for price variation, or the price band being hit ;

- Relevant index changes: Nifty 50 in case of NSE listed entity/ Sensex in case of BSE listed entity/ both in case listed on both, to be seen at the start of the trading day i.e. at 9.30 a.m. That is, change in the index is frozen at the start of the trading day.

- ISN intends to classify rumoured news into “positive news” or “negative news”, and correlate the price change with the same (that is, require response only where prices have gone up with a positive news and gone down with a negative news). However, for many news pieces, the ascertainment of whether the news is positive or negative will not be possible. Therefore, the only basis for determination of the direction of the news is the direction of the prices. For instance, disposal of a division may be negative news, if the sustainable income from the same will be lost, but may be taken as positive if the rate of return from the outgoing division was suboptimal.

- However, the reflection of the movement in the Index (provided is equal to or more than 1%) needs to be done on the MPM cut off percentages only if the Index movement is in the same direction as the MPM.

- As for the stock, the price movements are taken at any time during the trading day..

- Percentage variation in share price and the benchmark index movement will be calculated wrt the closing price of the immediately preceding trading day.

| Price range of the listed equity shares | Percentage variation in share price which shall be treated as material price | ||

| Benchmark index movement (+/-) is less than 1% at 9.30 am | Benchmark index movement (+/-) is greater than 1% at 9.30 am, and MPM is in the same direction as the Index change | In cases not covered by column on LHS | |

| Rs. 0 to 99.99 | ≥ 5% | ≥ 5% + % change in Benchmark index at 9:30 am) or Band hit | ≥ 5% |

| Rs. 100 to 199.99 | ≥ 4% | ≥4% + % change in Benchmark index at 9:30 am) or Band hit | ≥ 4% |

| Rs. 200 and above | ≥ 3% | ≥3% + % change in Benchmark index at 9:30 am) or Band hit | ≥ 3% |

- Assuming there is an MPM in my scrip at 12.30, which subsides later in the day, shall we still say the MPM has occurred? Answer seems to be yes. In case of intraday price movement (i.e. after 9:30 am), only the price range-based price variation in the scrip to be considered, irrespective of the Index movement.

- While there may be price movement due to a combination of various factors such as rumour, announcements or other events (other than the rumoured event), then MPM is deemed attributed \to the rumour.

- Where should one look for rumour?

- ISN has restricted the scope of “mainstream media” to the following:

- English national dailies satisfying the following conditions:

- Top English dailies with a circulation of 1 lakh or more copies as per RNI data; currently 14 newspapers along with the editions have been listed by ISN.

- Business/ Financial News Dailies: Economic Times, Business Standard, Live Mint, Financial Express and Hindu Business Line.

- Regional Dailies: the top 2 (two) regional dailies having the highest circulation, for each of the 22 (twenty two) official languages of India, subject to meeting the RNI Circulation Threshold, as per the list of regional dailies given in ISN.

- Digital versions of the newspapers covered above

- Digital/ online news sources: specified news sources meeting the following Business News Parameters:

- English national dailies satisfying the following conditions:

- Specified sources are – Bloomberg, BQ Prime, Money Control, Business Today, Business World, Reuters, Reuters India, and Press Trust India.

- International media :

- Top business/ finance dailies (from top 5 jurisdictions from where foreign portfolio investments are concentrated) comprise –

- Wall Street Journal and Financial Times for USA;

- Business Times and Financial Times for Singapore; and

- Financial Times for UK;

- For other jurisdictions where the Company has “material operations” (in our view, the Policy may define what is “material” operation), the Board is required to identify list of English business/ financial news sources from such jurisdictions. List to be published in the materiality policy.

- Top business/ finance dailies (from top 5 jurisdictions from where foreign portfolio investments are concentrated) comprise –

- Business News Channels: satisfying the following conditions:

- English news channels – CNBC TV-18, ET Now and NDTV Profit

- Other Business news channels – CNBC Awaaz, ET Swadesh, Zee Business and CNBC Bazaar

- Exclusions: News aggregators (for e.g. google news, inshorts, daily hunt etc.) and social media platforms (for e.g. whatsapp, twitter, facebook, instagram etc.) will not get covered under mainstream media.

- Inclusions: Social media handles of news sources identified above, will be included. However, quotes/ re-tweets/ re-posts made from such social media handles will not be included.

- What are the actionable for companies w.r.t. Mainstream media?

- Companies to put in place appropriate technology solutions, engage external media agencies;

- For identifying and tracking the digital news sources set out above.

- Implement internal systems for prompt reporting, coordination and communication between investor relations, corporate communications and compliance teams.

- Companies are required to respond only once and not when the same or similar rumour is published in another news source.

- Question – are companies expected to track all that is written about the company, in all the “mainstream media”, at all times? Answer should be No. However, the company may have to keep sources/media agencies on the standby, that is, to trigger them into action when there is MPM.

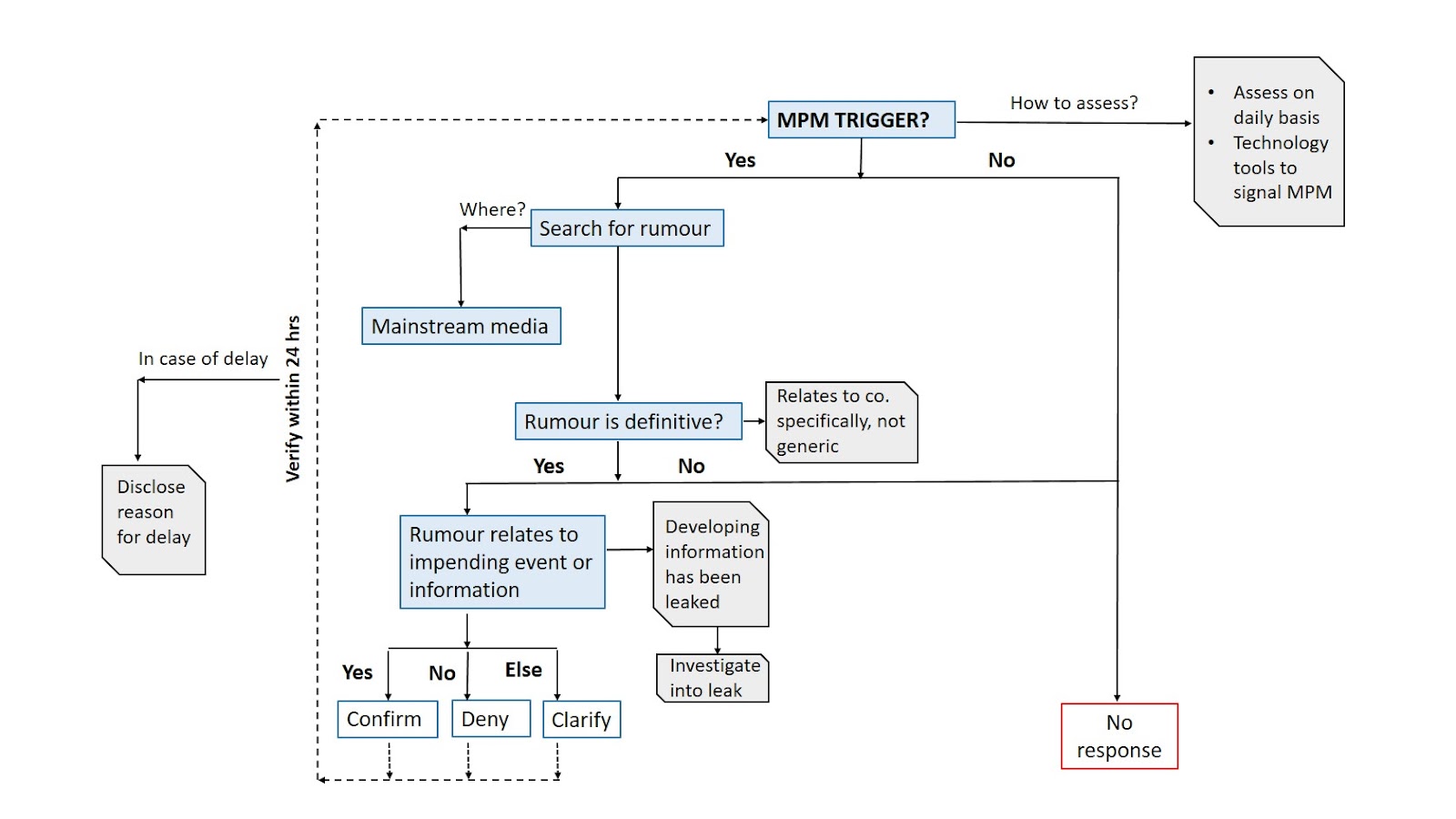

- What is the guidance for action?

- Companies have to be alert on MPM. MPM is assessed on a daily basis – therefore, companies may have appropriate technology tools to give a signal if there is an MPM.

- If there is an MPM, the company will have to search for “rumour” in “mainstream media”.

- Here, while companies may be required to keep appropriate technology/ arrangements with external media agencies in place, the same should not be taken to mean that the company is required to track rumour on a daily basis, irrespective of the MPM trigger.

- The tracking has to be done for a reasonable period of time backwards. Ideally speaking, the impact of a rumour on price will be reflected within 24-48 hours itself, however, companies may consider keeping a window of 5-10 trading days or any other specific period as part of their internal SOP for the tracking back of rumour in case of an MPM trigger.

- What does the rumour relate to? Is it about some “definitive” event or information, or generic in nature (say performance, prospects, etc)? Is it about the company or relates to the company specifically, and not generic (for example, sector, country, economy, etc)? If the answer to these questions are yes, see below.

- If the answer is yes, does the rumour relate to an “impending” event or information? That is, there is some event or information within the company which is developing, but the rumour has leaked the same. If yes, confirm it. If no, then deny.

- Do all of this within 24 hours of the MPM Trigger.

[Note – Where a prior intimation of Board meeting of the company has been given under Reg 29 of LODR for such “impending” event or information, the company need not respond to the rumour till the conclusion of the Board meeting.]

In the Table below, we take few situations to understand the applicability of verification of market rumour:

| MPM | Impending specific event under reg. 30 | Rumour in mainstream media | Verification of rumour by company required? |

| Yes | Yes | Yes | Yes |

| Yes | No | Yes | Yes, as the existence of MPM by itself satisfies the condition for rumour verification |

| Yes | Yes | No | No, there is no rumour to be verified. The company may disclose based on the information/event reaching the appropriate stage. |

| Yes | No | No | There is no rumour to be verified. |

| No | Yes | Yes | Rumour verification is not required, but the general principles of disclosure of events or information at an appropriate stage will be followed. |

- What happens if the rumour is confirmed?

- Any reported event or information on which below mentioned pricing norms apply, the effect on the price of the equity shares of the listed entity due to MPM and confirmation of the reported event or information to be excluded for calculation of the unaffected price for that transaction.

- Chapter V (preferential issue) of the ICDR Regulations (refer amendment including as part of a scheme of arrangement; or

- Chapter VI (QIP) of the ICDR Regulations (refer amendment);

- Regulation 8 (17) (offer price) or Regulation 9 (6) (listed securities offered as consideration) of the SAST Regulations (refer amendment);

- Regulation 19 (price in case of open market buy-back) or Regulation 22B (vi) (computation of lower end of price range in case of buy-back through book building) of the Buy-back regulations (refer amendment).

- scheme of arrangement involving a listed company (irrespective of whether the scheme involves a preferential issue or not), undertaken in compliance with the requirements of the SEBI Master Circular on Schemes of Arrangement, dated June 20, 2023; or

- any other transaction where the pricing is regulatorily required to be linked to the traded price of the scrip, including but not limited to cross border transactions involving the equity instruments (as defined in FEMA NDI Rules) of a listed company (i.e. purchase, sale, issuance of such equity instruments).

- What happens if the rumor is not verified?

- Unverified event or information cannot be considered as generally available information for the purpose of PIT Regulations. The definition has been amended to exclude unverified event or information reported in print or electronic media (refer amendment). That is to say, merely because the event/information is rumoured, but not confirmed by the company, it cannot be said to be generally available information.

- No “unaffected price” computation; that is, all price movements will be taken into consideration for the purpose of corporate actions

- Are any changes in materiality policy required?

- Amendments in law will override. The timeline for responding may be aligned from 24 hours from the reporting of the event or information to 24 hours from the trigger of MPM. The obligation cast on the promoter, director, KMP or SMP may also be inserted in the policy.

- Specific amendments to be made in line with the ISN as indicated below:

- In addition to the specified international news sources for top 100 listed entities, all listed entities covered by mandatory rumour verification requirement are required to identify the foreign jurisdictions where the company has material business operations, along with a list of English business/ financial news sources from such foreign jurisdictions to be tracked. List of such news sources and parameters applied for determining what would constitute ‘material business operation’ to be published in the materiality policy.

- SOP may be framed additionally to add the responsibility centers, timelines and other operational aspects.

- This may also cover the time frame upto which rumours will be tracked in mainstream media, in the event of an MPM trigger.

- Who will be responsible to ensure compliance?

- Companies will have to define responsibility. Generally speaking, the compliance officer remains responsible to ensure compliance with LODR Regulations [Reg. 6(2)(a)], but internally, for rumours and responses, companies may define the ownership/responsibility centre.

- The Industry Standards refer to “officers” u/s 2(59) of Companies Act. The definition therein is a very broad and inclusive definition. For the purpose of compliance with these regulations, the company may specify the meaning of “officers” to refer to the KMPs and SMPs of the company.

- If the information has been sought by the company from the promoter, director, KMP, SMP, then the respective promoter, director, KMP, SMP is responsible to give adequate, accurate and timely response to queries raised or explanation sought.

- The stock exchanges shall independently continue to seek clarification from the listed entities on news/rumours pertaining to the listed entity as part of their existing surveillance measures.

- What are the Industry Standards w.r.t. M&A Transaction Specific Aspects?

- Scope of M&A Transactions

- transactions concerning purchase, sale, buyback, delisting of securities of listed company;

- Preferential issue or any other fund-raising;

- Scheme of arrangement involving listed entity or any of its subsidiaries

- Acquisition / sale of undertaking or shareholding of another company;

- Proposed joint venture between listed entity and another entity.

- Exclusions – transactions undertaken in the ordinary course of business

- An on-market bulk/ block deal transaction, in respect of listed entity’s securities.

- An on-market treasury transaction or non-strategic transaction (pursuant to treasury management policies/ objectives – for e.g. investing surplus funds to acquire 0.5% equity stake undertaken by a listed entity in respect of another listed company)

- Treasury transaction/ non-strategic transaction would generally have the following features –

- pertains to the treasury function, i.e., investment of surplus funds of the company,

- indicates the regular investments made by the company in the stock market,

- is not intended to fulfil any strategic expectations of the company,

- the size of such investments are similar to other frequent investments,

- the company has not raised funds specifically for making such investments, and

- decisions with respect to such investments are generally taken by a delegated authority under section 179 of the Companies Act, 2013.

- Transaction stages –

- Preparatory stage (where the name of the target/ counterparty is not disclosable); and

- Signing of NDA, non-binding term sheet, letter of intent, commencement of DD, engagement of professionals for DD, evaluating overall viability of the deal (including for internal management) or engaging registered valuers;

- Constitution of sub-committee of Board to evaluate material terms/ assess viability, Committee granting an in-principle approval subject to further evaluation.

- Illustrative language of disclosure provided for each of the two sub-stages discussed above.

- Advanced stages (where the name of the target/ counterparty is disclosable)

- Multi-party bid process is ongoing and sole/ exclusive bidder is pending to be identified/ confirmed or has been confirmed,

- parties have entered into binding term-sheet w.r.t. listed target,

- where all material commercial terms have been agreed and final approval of Board or delegated board committee is being sought,

- Illustrative language of disclosure provided for listed bidder(s) and for listed target.

- Unaffected price to be considered only in case of advanced stages.

- Preparatory stage (where the name of the target/ counterparty is not disclosable); and

- Where company is not a party to the deal/ does not have ‘knowledge of the deal’3

- no specific confirmation/ denial would be required.

- What are the Industry Standards w.r.t. Non M&A Transaction Specific Aspects?

- Illustration of Non-M&A Transactions

- Whistle-blower complaint received by the Company;

- Internal Review or Investigation i.r.o. operational / financial aspects of the Company;

- Potential change in KMPs4 (including resignation and/ or removal of KMPs);

- Situation where MD/CEO is indisposed or unavailable to carry out the role in a regular manner for more than 45 days in any rolling period of 90 days on account of ill health.

- Guiding Principles for rumour verification of non-M&A Transactions

- The market rumour should provide specific identifiable details:

- details of the matter/ event; or

- Should provide quotes or be attributed to sources who are reasonably expected to be knowledgeable about the matter,

- Excludes market rumours that are vague or general in nature.

- The market rumour should be i.r.o impending event i.e imminent event, close at hand or about to happen,

- The market rumour should result in MPM.

- The market rumour should provide specific identifiable details:

Also see our related resources:

- SEBI notifies rumour verification requirements, application of market cap based provisions etc.

- Silence no more golden: New regulatory regime forces top listed companies to respond to rumours

- Getting material on “material” events and information: SEBI notifies amendments to Listing Regulations

- Youtube lecture: Demystifying rumour verification by listed entities

Capital Treatment, Loan Loss Provisioning and Accounting for Default Loss Guarantees

Vinod Kothari (finserv@vinodkothari.com)

The FinTech sector is booming and is a market disruptor as well as facilitator, based on the report published by Inc42, the estimated market opportunity in India fintech is around $2.1 Tn+ and currently there are 23 FinTech “unicorns” with combined valuation of $74 Bn+ and 34 FinTech “soonicorns” with combined valuation of $12.7Bn+.

The unprecedented growth of the fintech sector has transformed guarantees specifically First Loss Default Guarantees (FLDG) into a commonly employed tool for emerging players like fintechs. They leverage these guarantees to take exposures on loan transactions using low-cost funding from established entities such as large NBFCs and Banks. Fintechs issue guarantees that enable them to garner trust from prominent lenders, facilitating the origination of new loans through their digital platforms.

One of the crucial concerns in DLG arrangements is navigating the complexities surrounding capital treatment and NPA accounting covering both lenders and guarantors. In this article, we delve into an in-depth exploration of these crucial issues.

Capital Treatment

We organise this section into the following parts:

- Capital treatment for the lender availing the guarantee

- Capital treatment for the guarantor

- Expected credit loss treatment for the lender availing the guarantee

- Expected credit loss treatment for the guarantor

- Provisioning requirement for the lender availing the guarantee

- Provisioning requirement for the guarantor

Capital Treatment for Lenders:

Capital requirement is linked with the credit risk on the exposure: hence, before getting into the regulatory prescription, let us examine what is impact on the credit risk of the lender. For capital rules, a guarantee is regarded as a case of credit risk mitigation, provided the guarantee satisfies several conditions (e.g., it should be explicit, enforceable, guarantor’s financial resources adequate, etc). The lender, on the basis of the guarantee, shifts the risk of the first (or subsequent, as may be the nature of the guarantee) layer of the losses to the guarantor. Thus, there is a substitution of risk from the borrowers in the pool to the guarantor. The remaining exposure remains unprotected – hence, to that extent, there is no credit risk transfer. Therefore, if the risk weight of the guarantor is lesser than the risk weight of the underlying pool, there was a case to expect a reduction in the capital requirements.

The regulatory prescription is as follows: DLG Guidelines states that for the purpose of capital computation, i.e., computation of exposure and application of Credit Risk Mitigation benefits on individual loan assets in the portfolio shall continue to be governed by the extant norms. The “extant norms” for this purpose would be the norms on credit risk mitigation. These norms are applicable in case of banks [see part 7 of the Basel III Master circular ] However, in case of NBFCs, there is no equivalent.

However, FLDG is expected to be backed by either a cash deposit, or a bank guarantee. If it is backed by cash deposit, cash is to be assigned 0 risk weight. Similarly, if it is backed by a bank guarantee, the risk shifts to the bank, and therefore, a 20% risk weight as applicable to banks may be assigned by the NBFC. Note that the above risk weights are only for the part backed by the guarantee. That is, if there is a 5% FLDG, the 5% of the loan pool will be risk weighted as above, and the remaining 95% will attract the risk weight applicable to the borrower pool.

Capital Treatment for the guarantor

When we talk about capital treatment, the same would depend on the capital rules applicable to the guarantor entity. If the guarantor entity is an RBI regulated lender, it will be covered by the capital rules. If the guarantor not a regulated lender, it is unlikely to have any capital rules.

We discussed above the nature of a structured default loss guarantee. A structured DLG (first loss, second loss, or subsequent loss) integrates the risk of a pool of loans and then strips the same into multiple tranches. Therefore, it becomes a case of structured risk transfer.

The generic rule in case of any structured risk transfer is that the acquirer of the first loss tranche acquires the risk of the entire pool. Therefore, a first loss default guarantor is required to keep capital on the pool size (and not the size of the guarantee). However, the size of the guarantee is the loss limit of the guarantor – therefore, the capital requirement, computed by applying the risk weight to the pool size, will be limited to the size of the guarantee. We discuss this further below.

First Loss

If the guarantee is first loss in nature, then, as the principle goes, the RE will have to maintain capital on the entire pool, since, it is exposed to all the risks associated with all loan accounts individually, subject to a ceiling on the the amount of guarantee it has provided.

For instance, if the guarantor provides a 5% FLDG for a pool of loans aggregating to Rs. 100 crores, and the regulatory capital requirement of the guarantor is 15%, then the capital required to be maintained against such pool is:

Lower of

- 15% of Rs. 100 crores * 100% (Assuming 100% is the applicable risk weight of such loans)

- 5% of Rs. 100 crores

= Rs. 5 crores.

As per the RBI FAQs, RE providing DLG shall deduct “the full amount of the DLG which is outstanding” from its capital. The above is in line with the RBI FAQs on the subject.

This prescription should be taken as applicable in case of first loss guarantees.

Further, the apparent question that arises here is in what proportion should the capital be reduced from Tier I and Tier II. In absence of any specifications in this regard in the regulations or the FAQs, it is only logical to deduct the capital from the Tier I and Tier II in their respective ratios. That is, if the Tier I is 10% and Tier II is 5%, then the capital reduction should also happen in the ratio of 2:1.

Second Loss

If the guarantee is second loss in nature, then, the losses will start piling up on the guarantor only once the first loss support is exhausted. Unlike the other case, here, the guarantor is not exposed to all the risks associated with all loan accounts individually. Therefore, the capital will have to be maintained on the amount of guarantee provided instead of the entire pool.

Using the same example, as used in the earlier case, the capital requirement for the RE will be:

Rs. 100 crores * 5% * 15% = Rs. 0.75 crores.

Of course, this is applicable only where the first loss guarantee is sufficient to absorb losses upto a level sufficient to absorb a certain multiple of “expected losses”. Usually, the multiple should be sufficient so as to render the second loss facility to achieve an investment grade rating.

Expected credit loss for the recipient of the guarantee

Expected credit losses are for the potential for the loan or pool of loans to result in credit losses. If the lender has the benefit of first loss guarantee, the situation is that to the extent of the FLDG, the lender has exposure on the guarantor, and for the remaining pool size, the lender has exposure on the borrowers.

As regards a potential credit loss on the guaranteed amount, the RBI rules require the guarantee to be either fully backed by cash, or backed by a bank guarantee. Hence, the question of any credit loss on the same does not arise.

Hence, the lender will be exposed to losses only on so much of the expected credit losses as exceed the FLDG cover. For instance, if the FLDG is 5%, and the ECL estimated by the lender is 6.8%, the lender may create ECL provision only for 1.8%.

Note that ECL for any pool is a dynamic number – while estimations of the default probabilities and the exposure change over time, there are also changes due to unwinding of the discounting factor applied in computing present value of the ECL. Therefore, ECL estimation is bound to change every reporting period. For that matter, FLDG will remain fixed as 5% of the originated pool, but this number will also be dynamic as the loan pool matures – partly due to amortisation of the pool, and partly due to utilisation of the guarantee. Therefore, on an ongoing basis, the lender may compare the ECL with the percentage of FLDG still available, and create ECL for the differential amount.

Expected credit loss for the guarantor

If the guarantor is covered by ECL requirements, the guarantor needs to estimate the losses likely to be caused to the guarantor. As against the guarantee, the payoff of the guarantor may be (a) fixed guarantee fees (b) right to get a variable fee, usually linked with the excess spreads from the pool.

Note that ECL computation is required not only for loans, but also for financial guarantees. Therefore, the guarantor will need to compute the expected credit losses from the underlying loans using exactly the same basis as if the loans were on the books of the guarantor. Of course, the maximum ECL will be the limit of the guarantee.

Provisioning for the recipient of the guarantee

In this regard, the RBI has clearly specified that no benefit will be given for provisioning requirements – that is, the regulatory provisioning will continue irrespective of the guarantee.

Provisioning for the guarantor

As regards the guarantor, while a financial guarantee is regarded as a direct credit substitute, however, there are no explicit provisioning requirements. To the extent the guarantee has already been utilised, it will be taken as a loss (even though recovery may happen subsequently, but it will be contingent).

Accounting

Given that the recoveries are against an outstanding asset, receipts from DLG invocation should not be treated as income. The recoveries made from the accounts, for which the lender has already invoked DLG, in our view,should be recorded as a liability. This is because any recoveries from borrowers after receiving DLG payout would be liable to be remitted back to the DLG provider, and the lender will only hold it in trust. Hence creating a back to back obligation on the RE. It is important to note that, in general, a lender may not relinquish their legal right to recover a loan, even after the loan has been written off. Consequently, the obligation to pass on the recoveries from the borrower may also persist indefinitely.

To support this perspective, we suggest that the lender establish a timeline in agreement with the DLG provider. This timeline should specify the duration during which any recoveries from loans, for which DLG payouts were made, will be passed on to the DLG provider. After the specified period, the lender will no longer be obligated to transfer such recoveries. Consequently, upon completion of the agreed period, the RE can write off the liability associated with the credit protection payouts received.

Treatment of an NPA account in case the guarantee is invoked.

Through the DLG Guidelines RBI has stated that the NPA classification would be the responsibility of the RE and would be as per the extant asset classification and provisioning norms irrespective of any DLG cover available at the portfolio level [para 7 of the DLG Guidelines]. The amount invoked by the DLG cannot be set off against the underlying individual loans and thus, asset classification and provisioning would not be affected by any DLG cover. However, any future recovery by the RE from the loans on which the DLG cover was invoked and realised can be shared with the DLG provider in terms of their contractual arrangements.

Since the guarantee invoked cannot be set off against the loan, how would the guarantee amount be shown in the books of the RE?

Accounting-wise, if the amount has been recovered, it is set off from the outstanding pool However, there is a departure here between accounting treatment and the NPA/capital requirements, as the RBI expects the NPA recognition to be continued in the books of the lender.

Similarly, capital requirements will also remain unaffected. However, it will be wrong to show the amount recovered from the guarantor as a liability as it is not a liability – though there may be an understanding that any recovery from the loans will be paid back to the guarantor. It is also wrong to treat the amount received from the guarantor as income, as the payment consists of both interest and principal.

Invocation of DLG will not affect NPA classification of borrower

It shall be noted that despite the FLDG being invoked against the borrowers outstanding amount, the capital requirements and asset classification remain unaffected. Further, reporting to CIC and NESL pertains to the borrowers performance, and therefore, the invocation of FLDG shall not influence these reporting. Repayment as well as defaults of the borrower should continue to be reported without any impact from FLDG invocation. Therefore, the borrowes account will continue to be classified as NPA and reported accordingly to the CIC and other relevant reporting entities.

Related Articles –

FAQs on Default Loss Guarantee in Digital Lending

Lend, Recover, Replenish: A guide to revolving lines of credit

Risk Management Function of NBFCs – A Need to Integrate Operational Risk Management & Resilience

An examination of the RBI Guidance Note on Operational Risk Management and Resilience

Subhojit Shome & Archisman Bhattacharjee | finserv@vinodkothari.com

Loading…

Related articles –

- COMPLIANCE RISK ASSESSMENT

- RISK-BASED INTERNAL AUDIT FOR NBFCS – APPLICABILITY & IMPLEMENTATION

- IT Governance, Risk, Controls and Assurance Practices Direction, 2023

- DRAFT MASTER DIRECTION ON IT GOVERNANCE, RISK, CONTROLS AND ASSURANCE PRACTICES

12th Securitisation Summit

The who’s who of structured finance is joining the 12th edition of our flagship event, the Securitisation Summit on May 15, 2024, in Mumbai. Be shoulder-to-shoulder with leading originators, investors, lawyers, rating agencies, consultants, regulators, mediators, market makers, and everyone else who matters.

For details of the event and to book your seat, please visit our Summit page – HERE

Agenda – 12th Securitisation Summit | May 15, 2024

Summit home page can be viewed here: https://vinodkothari.com/secsummit/

Loading…

Relinquishment of source of profit in favour of an RP: also an RPT

– Mahak Agarwal | corplaw@vinodkothari.com

– Updated on December 13, 2025

The broad spectrum of the definition of Related Party Transactions (RPTs) under the Listing Regulation, continues to be an error prone area in terms of compliance. A recent SEBI ruling1 has further strengthens this aspect where the phrase ‘transfer of resources, services or obligations’ has been explained in an extremely new dimension with a commendable insight from the authorities which again shows that the regulators can no more be restricted by the imaginary boundaries placed by the corporates when it comes tightening the loose ends of corporate governance.

This article delves into the basis which the Regulators considered for concluding a mutual understanding and agreement between related parties to be an RPT notwithstanding the contention of the company. The essential question of law involved in this case was whether the allocation of certain products and geographic areas between RPs constitutes an RPT. The article contains our analysis of SEBI’s order and highlights the recent order passed by the SAT upon appeal in the matter, reaffirming the said stand.

Read more →