Operational Risk Assessment for NBFCs : Understanding The Basics

Simrat Singh | finserv@vinodkothari.com

Operational risk, as defined by the Basel framework, refers to the possibility that a financial institution’s routine operations may be disrupted due to failures in processes, systems, people, or external events. While historically treated as secondary to credit and market risk, it has increasingly become a central focus of risk management, particularly for institutions with complex operations, heavy technology dependence, extensive outsourcing, and stringent regulatory obligations. Reflecting this shift, the RBI’s 2024 Guidance Note on Operational Risk Management and Resilience expands its expectations for operational risk management to all NBFCs.

Having previously discussed the guidance note (refer here), this article now explains the fundamentals of operational risk assessment and outlines its process.

Operational Risk Management

Operational risk poses unique challenges because many of the events that cause losses arise from internal factors, making them difficult to generalise or predict. Large operational losses are often viewed as rare, which can make it difficult to get sustained management attention on the steady, routine work required to identify issues and track trends1. Operational risks typically stem from people, processes, systems and external events, ironically, the same resources essential for running the business. Unlike credit and market risk which are modelled and hedged, operational risks are often idiosyncratic, event-driven and subject to human, process and system failure.

Relevance For Financial Institutions

Financial institutions operate with complex processes, large transaction volumes, strict regulatory reporting requirements and often heavy dependence on technology, outsourcing arrangements and third-party service providers. Because of this, operational failures, such as system glitches, fraud, compliance breaches or breakdowns in business continuity, can result in substantial financial losses, regulatory sanctions, reputational harm and other disruptions to business operations.

Given these risks, regulators have placed growing emphasis on the measurement and management of operational risk. Based on our experience, RBI has frequently raised queries regarding the operational risk frameworks of NBFCs during its supervisory inspections. Under Basel II, for instance, banks using the Advanced Measurement Approach were required to maintain strong, demonstrable operational risk management systems. Recognising the importance of operational risk, the Bank of England’s FSA0732 report, which is applicable on banks and large investment firms, requires firms to record the top ten operational risk loss events for each reporting year. This provides a clear view of what went wrong, where it occurred and the scale of the financial impact.

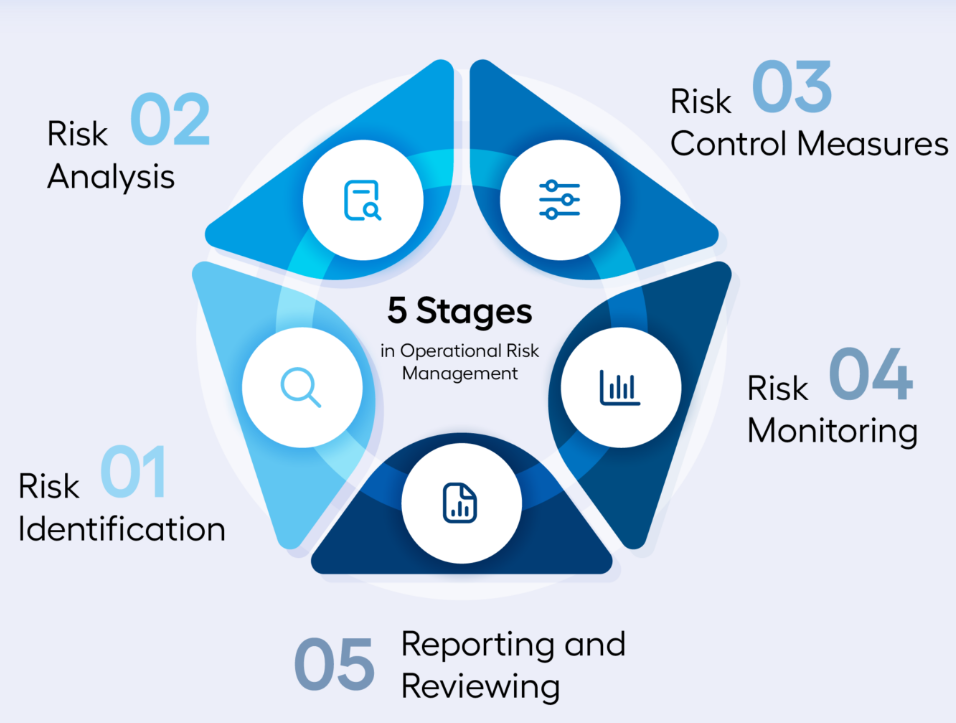

Operational Risk Assessment Process

In its guidance note for operational risk, RBI at many places underscored the importance for risk assessment. One such example is given below:

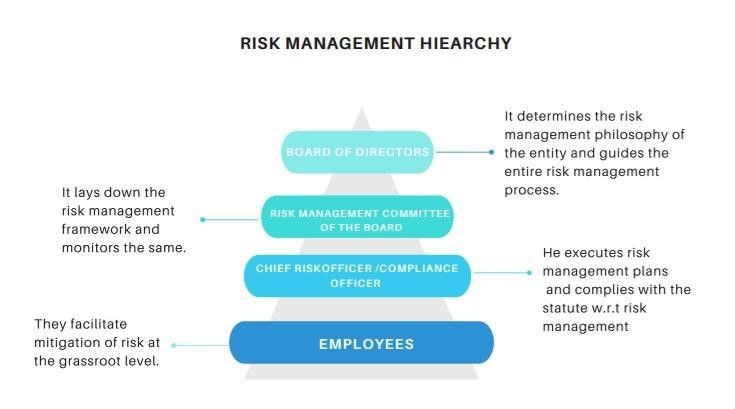

Principle 6: Senior Management should ensure the comprehensive identification and assessment of the Operational Risk inherent in all material products, activities, processes and systems to make sure the inherent risks and incentives are well understood. Both internal and external threats and potential failures in people, processes and systems should be assessed promptly and on an ongoing basis. Assessment of vulnerabilities in critical operations should be done in a proactive and prompt manner. All the resulting risks should be managed in accordance with operational resilience approach.

6.1 Risk identification and assessment are fundamental characteristics of an effective Operational Risk Management system, and directly contribute to operational resilience capabilities. Effective risk identification considers both internal and external factors. Sound risk assessment allows an RE to better understand its risk profile and allocate risk management resources and strategies most effectively.

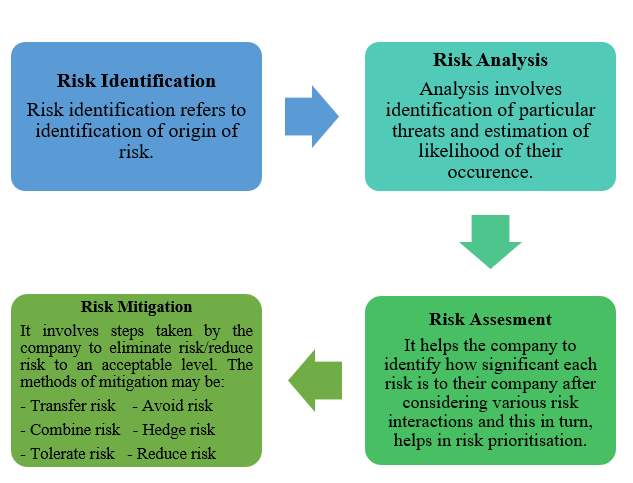

Figure 1: Operational Risk Assessment Process

Risk identification

Risk identification means figuring out what exactly you need to assess. It involves recognising the different risk sources and risk events that may disrupt your business. A risk source is the underlying cause, something that has the potential to create a problem. A risk event is when that problem actually occurs. For example, a weak password is a risk source, while a data breach caused by that weak password is the risk event.

As per the RBI’s Guidance Note, REs are expected to take a comprehensive view of their entire “risk universe”. This means identifying all categories of risks, traditional or emerging, that could potentially affect their operations. These may include insurance risk, climate-related risk, fourth- and fifth-party risks, geopolitical risk, AML and corruption risk, legal and compliance risks, and many others. The underlying expectation is simple: an RE should systematically identify everything that can go wrong within its business model, processes, people, systems, and external dependencies, and ensure that no material source of risk is overlooked.

There are many ways to identify risks. You may use questionnaires, self-assessments by business or functional heads, workshops with staff involved in risk management, or you may review past failures within the company. Industry reports, experiences of peers, and linking organisational goals to potential obstacles can also reveal important risks. You can even look at upcoming strategic initiatives and think ahead about the risks that may arise when these changes are implemented.

Every organisation has its own risk profile. A lender may worry about borrowers not repaying, untrained staff, biases in an AI underwriting model, IT system failures, employee fraud, or suppliers not delivering on time. These risks should be recorded in a risk register, but it is important that this register reflects your business. A company offering only physical loans may not face digital lending risks, and should not simply copy any generic list. The goal is to identify risks that genuinely matter to your day-to-day operations.

Assessment

Once you know which risks matter, the next step is to assess each of them. For every risk, ask yourself two basic questions:

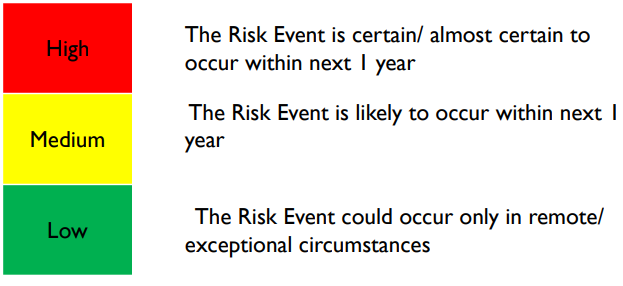

- What is the likelihood of this risk actually happening? This is simply the chance that the event might occur; You may assign parameters to determine the likelihood – for eg if the risk event is almost certain to occur in the next 1 year or is it likely to occur or it will occur only in remote situations?

Figure 2: Illustrative likelihood assessment criterias

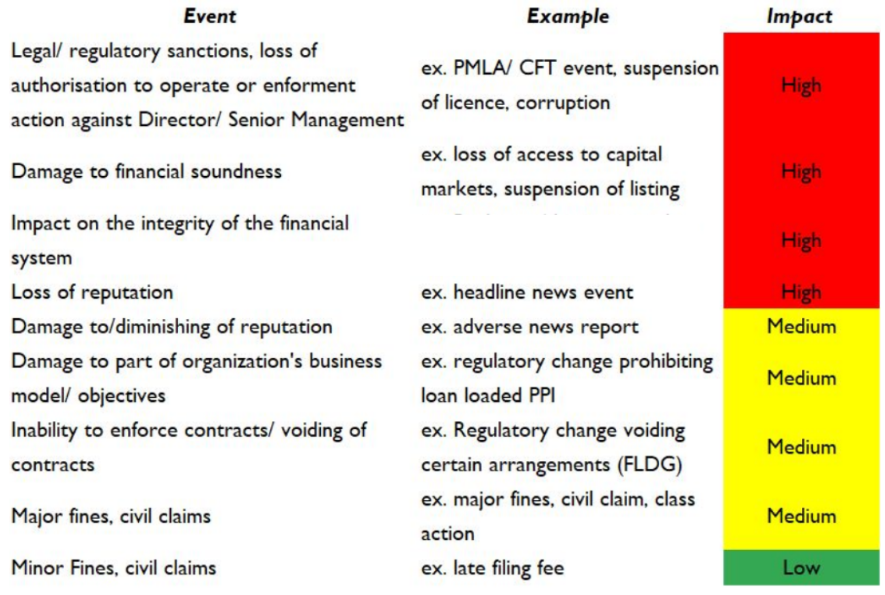

- If it does happen, what impact will it have on my organisation? Will it hurt my reputation? Lead to financial loss? Negative feedback from customers? Cause a data leak? One can record the impact of the risk as High, medium or low based on its gravity

Figure 3: Illustrative impact assessment of risks

These two questions help you understand how serious the risk is inherently (inherent risk level) i.e, before considering whether you have any controls in place. Note that at this stage, you’re only interested in the natural level of risk that exists ignoring any controls you might already have.

Evaluating Controls

Once the inherent risks are understood, the next step is to look at how these risks are currently being managed. These risk-reducing efforts are your controls or mitigation measures. Controls are simply the actions, checks, or processes already in place to lower the likelihood or impact of a risk. For example: Is your underwriting model checked for bias? Are board committees meeting regularly? Do you have proper maker–checker checks in your V-CIP process? Controls can take many forms such as policies, procedures, tools, system checks, reviews, or even day-to-day practices followed by employees. In essence, a control is any measure that maintains or modifies risk and helps the organisation manage it more effectively.

Residual Risk

After evaluating the controls, you can determine the residual risk i.e. the level of risk that remains even after your mitigation measures have been applied. Residual risk shows whether the remaining exposure is acceptable or whether additional controls are needed. By definition, residual risk can never be higher than inherent risk. Generally, residual risk can be interpreted as follows:

- Low Residual Risk: When the effectiveness of internal controls fully covers or even exceeds the inherent risk;

- Medium Residual Risk: When controls reduce most of the risk, leaving only a small gap;

- High Residual Risk: When controls address only part of the risk and a significant gap still remains;

| Category | Risk Source | Risk event | Root cause | Likelihood | Consequence | Level of inherent risk | Control Effectiveness | Level of Residual Risk |

| People Risk | Employees / Staff | Employee fraud, misappropriation, or collusion | Weak internal controls, poor background checks | Highly Likely | Medium | High | Weak | HIGH |

| Information Technology & Cyber Risk | IT Infrastructure / Systems | System downtime or core platform failure | Server outage, inadequate IT resilience | Possible | Low | Low | Strong | LOW |

| Process & Internal Control Risk | Onboarding / KYC Processes | Non-compliance with KYC or onboarding procedures | Inadequate verification, manual errors | Possible | High | High | Adequate | MEDIUM |

| Legal & Compliance Risk | Outsourcing / LSP Arrangements | Non-compliance in outsourcing / LSP arrangements | Weak SLA oversight, inadequate due diligence | Unlikely | Low | Low | Adequate | LOW |

| External Fraud Risk | Borrowers / External Parties | Borrower fraud – identity theft, fake borrowers, or collusion | Forged documents, weak KYC | Possible | Low | Low | Strong | LOW |

| Model / Automation / Reporting Risk | Data Aggregation / Systems | Failure in data aggregation across systems for regulatory returns | System inconsistencies, poor data governance | Highly Likely | Medium | High | Strong | LOW |

| Reputation Risk / Customer Experience | Customer Communication / Sales Practices | Miscommunication of terms or conditions to customers | Poor training, unclear communication scripts | Possible | Medium | Medium | Weak | MEDIUM |

Figure 5: An illustrative Snapshot of Operational Risk Assessment

Understanding residual risk helps decide where further action is required and where the organisation may still be vulnerable.

Conclusion

The goal, therefore, is to move away from a simple “tick-box” approach and make the operational risk assessment truly tailored to the organisation. For ML and above NBFCs, the ICAAP requirement to set aside capital for operational risk is useful, but it covers only a narrow part of what operational risk really involves. A comprehensive assessment goes much further by examining the strength of the entity’s internal controls and how effectively they manage real-world risks. If the residual risk exceeds the organisation’s tolerance level, it should trigger a closer look at those controls and prompt corrective action. Ultimately, the focus should be on building a risk framework that is meaningful, proactive, and aligned with how the organisation actually operates. The ultimate goal is therefore to develop ‘operational resilience’ which as per Bank of England3 is the ability of firms and the financial sector as a whole to prevent, adapt, respond to, recover from, and learn from operational disruptions.

Our other resources on risk management:

- Tracking Your Material Risks – Importance of Risk Register for NBFCs

- Risk Management Policy: A Tool Of Risk Management

- Operational Risk Management – A Guidance Note

- Revamped Fraud Risk Management Directions

- Enterprise Risk Management

- Understanding Risk Management Framework in NBFCs

- A Need To Integrate Operational Risk Management & Resilience