Online money gaming: Financial Institutions to stay away

– Saloni Khant | finserv@vinodkothari.com

The Promotion and Regulation of Online Gaming Bill, 2025, passed by the Parliament, received the assent of the President on Friday, 22nd August, 2025. The law will come into force on its publication in the Official Gazette. As soon as it becomes effective, the immediate implication of the Bill will be to prohibit online money gaming services.

Online money game is defined as “an online game, irrespective of whether such game is based on skill, chance, or both, played by a user by paying fees, depositing money or other stakes in expectation of winning which entails monetary and other enrichment in return of money or other stakes”. In other words, an online game, irrespective of whether it involves skill or chance or combination, where money (or other stake) is paid to play, with the expectation of winning (which may either be money or other enrichment), will be barred.

Read more →From Trade Payables to Financial Liabilities: Ind AS Disclosure Reforms for Supply Chain Finance arrangements

Dayita Kanodia | finserv@vinodkothari.com

The amendments in Ind AS 7 emanate from similar amendments in IAS 7 by the IASB, made in May 2023, which itself is the culmination of a project that was initiated in 2020.

The amendments related to Supply Chain Financing (SCF) or reverse factoring arrangements. Globally, the SCF volumes increased by 8% to USD 2,462bn by the end of 2024.

Read our article explaining the Supply Chain Finance here.

The key features of a supply chain finance arrangement to require specific disclosure under the revised Standard are:

- The trade payables of the entity are paid by a financial institution; the entity then pays to the financial institution.

- The entity either gets extended payment terms, or the suppliers get earlier payment terms, than the terms as contained in the relevant supply invoices/agreements.

- Examples: X Ltd acquires goods/services from vendors with a 90 days’ credit. It organises a supply chain financing arrangement where Bank A discounts the receivables and pays off the vendor within 30 days, whereas the Bank will collect payment from X on 90 days of the invoice. The arrangement is covered.

- Same facts as above; but X is required to pay to the Bank in 180 days, whereas the Vendor is paid in 90 days. The arrangement is covered.

- If the due date of payment to the Bank is the same as the due date of payment to the vendor, the arrangement has no economic value, and does not impact either party’s cashflows – hence, does not require any specific disclosures.

- Note that the amendments do not affect asset side financing arrangements, that is to say, receivables financing or forward factoring.

Rights for wrongs: Potential deprivation of shareholders property rights using mandatory demat rule

– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

The mandatory dematerialisation provisions under the Companies Act, 2013 requires companies to issue their securities and facilitate transfer requests in dematerialised form only. For private companies, the mandate has become effective since 30th June 2025, hence, every private company (barring a small company) is now required to issue securities in dematerialised form only. Not only do new securities need to be in demat format, the shareholders having existing shareholding in physical form are deprived of their shareholding rights in the form of participation in further rights issue, bonus issue etc. The purpose of mandatory demat rule is to bring shareholders and shareholding in companies in a transparent, tractable domain. However, can it be contended that every person who has not dematerialised his holdings is a non existing persona, or deserves to have his property rights defeated and redistributed to other shareholders? Can such a person be compelled to lose his rights entitlement in further issuance brought by the private company? Even more stark, can such a shareholder lose his rights to the accumulated surplus piled up in the company if the board of directors of the company suddenly decides to issue bonus shares? In simple words, can the mandate of dematerialisation, that is applicable on a company, be interpreted for deprivation of shareholders’ property rights?

It is not that Rule 9B is new – since its original notification in October 2023, the applicability of the provisions was deferred from the original applicability date of 30th September, 2024 to 30th June, 2025. However, we need to understand that when it comes to private companies, there are lots of minority shareholders who have not converted their shareholdings into demat form. Reasons could be internal family issues, some issues with respect to holdings, or pure lethargy. Let no one make the mistake of assuming that private companies are small companies – private companies may be sitting with hundreds of crores of wealth – these may be family holding companies, JV companies, or even large companies with a restricted shareholding base. If the company is an old legacy company, for sure, the shares would have been in physical form, and may not have been demated. Now, suddenly, finding the law that has come into force, if the board of directors decides to come out with a bonus, the minority holding shares in physical form will be deprived of their right – which would mean, their share of wealth piled up over the years goes to the other shareholders.

Mandatory dematerialisation prior to subscription to securities

Sub-rule (4) of Rule 9B puts a condition on the securities holders to have the entire holding in demat form prior to subscription to the securities. The relevant extracts are as below:

(4) Every holder of securities of the private company referred to in sub-rule (2),-

XXX

(b) who subscribes to any securities of the concerned private company whether by way of private placement or bonus shares or rights offer on or after the date when the company is required to comply with this rule shall ensure that all his securities are held in dematerialised form before such subscription

The provision thus explicitly forbids a shareholder from participation in a rights issue or bonus issue – corporate actions that are very much a part of the pre-emptive rights of a person as an existing shareholder.

Seeking mandatory dematerialisation: powers under section 29 of the Act

Note that Rule 9B has been issued in accordance with the powers contained in Section 29 of CA, 2013. The title of section 29 reads as “Public Offer of Securities to be in Dematerialised Form”, indicating the regulator’s intent of requiring mandatory dematerialisation of ‘public offers’. Sub-section (1)(b) of the said section originally referred to ‘public’ companies, however, the term ‘public’ was subsequently omitted, and sub-section (1A) introduced, so as to require the notified classes of unlisted companies to ‘hold’ and ‘transfer’ securities in dematerialised form only. The amendment was brought in 2019, thus, enabling the Government to bring private companies too within the ambit of mandatory dematerialisation.

Bonus issue and the unfair treatment to physical shareholders

Rule 9B(4) explicitly refers to ‘bonus issue’, and states that physical shareholders are ineligible to ‘subscribe to the bonus issue’. First of all, the language of the provision is flawed in the sense that bonus issue is mere capitalisation of profits of the company – there is no ‘offer’ on the part of the issuer, and no ‘subscription’ on the part of the shareholder. The same is proportionally available to all shareholders in the ratio of their existing shareholding.

Since bonus issue leads to capitalisation of profits, there is an effective distribution of profits to the shareholders, though the company does not incur any cash outflow. Depriving a shareholder of his right to bonus issue does not only result in non-distribution of the profits to such shareholder, but also, redistribution of his share of profits to other shareholders. There is a disproportionate distribution of profits, and the physical shareholders stand at a loss.

Unclaimed dividend: why should the treatment not be the same?

A parallel reference may be drawn from the provisions applicable to payment of dividend, through which distribution of profit occurs, with an immediate cash outflow. Section 124 of CA, 2013 requires that any unclaimed/ unpaid dividend be transferred to a separate escrow account, and the details of the shareholders be placed on the website to provide notice to the shareholders for claiming the same. Even if the same is not claimed by the shareholders during the specified period, the same can still not be re-distributed amongst the other shareholders, rather, gets transferred to the Investor Education and Protection Fund, and may still be claimed by the shareholders.

The concept of bonus issue, being much similar to that of dividend, the rights of the physical shareholders should not be compromised and the bonus shares should ideally be set aside in a separate suspense account with any DP. Before keeping such shares in the suspense account the issuer company should send intimation letters to such shareholders at their latest known address.

Listed shares and Suspense Escrow Demat Account

Pending dematerialisation of holdings of a shareholder, any corporate benefits accruing on such securities are credited to the Suspense Escrow Demat Account, and may be claimed by the shareholder. Reg 39 read with Schedule VI of LODR Regulations require all such corporate benefits to be credited to such demat suspense account or unclaimed suspense account, as applicable for a period of seven years and thereafter transferred to the IEPF in accordance with the provisions of section 124 of CA, 2013 read with the rules made thereunder.

How physical shareholders are deprived of their rights to proportionate holding?

Under rights issue, an opportunity is given to the existing shareholders, in proportion to their existing shareholding, to subscribe to the further issue of shares by the company. Thus, any dilution in the voting rights and towards the value of the company is avoided. The alternative to rights issue is through preferential allotment, where the securities may be offered to any person – whether an existing shareholder or otherwise, in any proportion. Since this may lead to a dilution in the rights of the existing shareholders – the same requires: (a) approval of the shareholders through a special resolution and (b) a valuation report from the registered valuer.

Both of the aforesaid are meant to protect the interests of the existing shareholders. On the other hand, in case of rights issue – neither shareholders’ approval nor a fair valuation requirement applies – on the premise that there is no dilution of rights of the existing shareholders.

In fact, rights issue of shares can be, and in practice, are fairly underpriced, since there is no mandatory valuation requirement under the Companies Act, and while there are contradicting judgments on whether or not section 56(2)(x) of the Income Tax Act applies on dis-proportionate allotment under rights issue, the valuation under Rule 11UA may be based on historical values – and hence, may not reflect the fair value of the shares.

Not being entitled to rights is like losing the proportional wealth in a company, resulting in re-distributing the property of the physical shareholders to the demat shareholders. This effectively steals a physical shareholder of his existing holding in the company, that gets diluted to the extent of the disproportionate allotment, and a loss in value on account of the underpriced share issuance.

Listed companies and the approach followed for rights issue

For listed entities, there is no blanket prohibition on subscription of shares by physical shareholders, rather, necessary provisions are created to facilitate subscription to the rights issue by such shareholders as well [Chapter II of ICDR Master Circular read with Annexure I].

- Where the demat account details are not available or is frozen, the REs are required to be credited in a suspense escrow demat account of the Company and an intimation to this effect is sent to such shareholder.

- Physical shareholders are required to provide their demat account details to the Issuer/ Registrar for credit of Rights Entitlements (REs), at least 2 working days prior to the issue closing date.

- The REs lapse in case the demat account related information is not made available within the specified time.

Thus, there is no automatic deprivation of the rights of the physical shareholders to apply in a rights issue, rather, a systematic process is given to facilitate dematerialisation and subscription of shares.

The problem is bigger for private companies: necessitating additional measures

A listed entity has a large number of retail shareholders, however, with very small individual holdings. In contrast is a private company, where the number of shareholders are small and each shareholder would be holding a rather significant share. The larger the share of an individual shareholder, the more he is impacted by the nuisance of depriving participation in a rights issue.

The technical requirement of securities being dealt with in dematerialised form only, cannot give a private company the right to arbitrarily bring up corporate actions to deprive the existing physical shareholders from their rights over the company.

An ideal approach towards preventing companies from taking an unfair advantage of the non-dematerialised holdings of some shareholders vis-a-vis dematerialised holdings of other shareholders would be by requiring them to keep the corporate actions attributable to the physical shareholders in abeyance, pending dematerialisation of securities.

Therefore, for instance, in case of rights issue, along with the circulation of offer letter to the shareholders, a dematerialisation request form may be circulated, requiring the shareholders holding shares physically to apply for such dematerialisation. Pending dematerialisation of the securities, shares may be held in a suspense account or may be reserved for the shareholders in any form, and may be credited to the demat account of such shareholders, once the same is available.

In the absence of any measures for protection of interest of the physical shareholders, the disproportionate treatment to such shareholders pursuant to a corporate action, may be looked upon as the use of law with a mala fide intent, one done with the intent of differentiating between shareholders of the same class – which could not have been possible otherwise, if the shares were held in demat form.

Thus, one may contend that the ‘right’ is used for a ‘wrong’, thus challenging the constitutional validity of such law.

Deprivation of property rights require authority of law

Article 300A of the Constitution of India provides for the right to property, stating that “No person shall be deprived of his property save by authority of law”. The Article has been subject to various judicial precedents, although primarily in the context of land acquisition related matters. The Supreme Court, in the matter of K.T. Plantation Pvt. Ltd. vs State Of Karnataka, AIR 2011 SC 3430, has considered ‘public purpose’ as a condition precedent for invoking Article 300A, in depriving a person of his property.

117. Deprivation of property within the meaning of Art.300A, generally speaking, must take place for public purpose or public interest. The concept of eminent domain which applies when a person is deprived of his property postulates that the purpose must be primarily public and not primarily of private interest and merely incidentally beneficial to the public. Any law, which deprives a person of his private property for private interest, will be unlawful and unfair and undermines the rule of law and can be subjected to judicial review. But the question as to whether the purpose is primarily public or private, has to be decided by the legislature, which of course should be made known. The concept of public purpose has been given fairly expansive meaning which has to be justified upon the purpose and object of statute and the policy of the legislation. Public purpose is, therefore, a condition precedent, for invoking Article 300A.

Failure to dematerialise: can there be genuine reasons or mere lethargy?

One may argue that the shareholders have the responsibility to ensure their holding is dematerialised, and hence, a physical shareholder rightfully suffers the consequences of its own lethargic attitude. However, that should not be considered reason enough to deprive one of its rights to the property legally owned and held by it.

Practically speaking, there may be various reasons for which a shareholder may not be able to dematerialise its existing shareholding in a company, thus becoming ineligible for participation in rights/ bonus issues. For instance, the title of a shareholder might be in dispute, pending which, dematerialisation would not be possible. Another practical issue might be due to loss of share certificates, and the investee company, pending issuance of duplicate share certificates and dematerialisation thereof, may come up with a bonus issue.

Concluding Remarks:

The dematerialisation provisions, brought to do away with bogus shareholders, might be used to steal away the rights of validly existing shareholders, on the pretext of non-fulfilment of a technical requirement. In view of the mandatory issuance in demat form, a physical shareholder might not be able to ‘hold’ the shares pending dematerialisation, however, the same does not snatch away the ‘entitlement’ of the shareholder to such rights, and cannot, at all, be re-distributed to other shareholders. This cannot, and does not, seem to have been the intent of law, however, in the absence of clear provisions requiring the company to hold such rights in abeyance for the physical shareholders, may lead to inefficacy.

Read More:

Supreme Court Mandates Digital Accessibility: Action Points for Banks and NBFCs

– Harshita Malik | finserv@vinodkothari.com

Introduction

On April 30, 2025, the Supreme Court of India delivered a landmark judgment in Pragya Prasun & Ors. v. Union of India, declaring digital access as an intrinsic component of the fundamental right to life under Article 21. The Court issued comprehensive directions to make digital KYC processes accessible to persons with disabilities, particularly acid attack survivors and visually impaired individuals.

This judgment fundamentally transforms how banks and NBFCs must approach customer onboarding through digital means, with immediate compliance requirements and potential legal consequences for non-adherence.

Pursuant to the directives issued by the Supreme Court, the RBI has amended the Master Direction – Know Your Customer (KYC) Direction, 2016 (‘KYC Directions’) vide Reserve Bank of India (Know Your Customer (KYC)) (2nd Amendment) Directions, 2025 (‘KYC 2nd Amendment’).

Background: The Catalyst Case

The Petitioners’ Struggle

The petitioners in these cases highlight significant barriers faced by persons with disabilities in accessing digital KYC processes. WP(C) No. 289 of 2024 involved acid attack survivors who were unable to complete digital KYC, while WP(C) No. 49 of 2025 involves a visually impaired individual facing similar difficulties. A notable incident involved Pragya Prasun, who was denied the opening of a bank account due to her inability to perform the blinking required for liveness verification. These cases are grounded in the protections afforded by the Rights of Persons with Disabilities Act, 2016, and the fundamental right to life and personal liberty under Article 21 of the Constitution.

Current KYC Barriers Identified

The Court recognized that existing digital KYC processes create obstacles for persons with disabilities:

| Barrier Type | Specific Issues | Affected Population |

| Liveness Detection | Mandatory blinking, head movements, reading displayed codes | Acid attack survivors, visually impaired |

| Screen Compatibility | Lack of screen reader support, unlabeled form fields | Visually impaired persons |

| Visual Dependencies | Selfie capture, document alignment, front/back identification | Persons with visual impairments |

| Signature Verification | Non-acceptance of thumb impressions in digital platforms | Persons unable to sign consistently |

Legal Framework and Constitutional Mandate

Supreme Court’s Key Declarations

“Digital access is no longer merely a matter of policy discretion but has become a constitutional imperative to secure a life of dignity, autonomy and equal participation in public life.”

– Justice R. Mahadevan

The Supreme Court has firmly declared that digital access is no longer just a policy choice but a constitutional necessity to ensure individuals’ dignity, autonomy, and equal participation in society. This constitutional and legal mandate is grounded in several provisions: Article 21 guarantees the right to life with dignity, requiring digital services to be accessible to everyone; Section 3 of the Rights of Persons with Disabilities (RPwD) Act, 2016, ensures equality and prohibits discrimination against persons with disabilities; Section 40 mandates that all digital platforms adhere to established accessibility standards and Section 46 sets a two-year timeline within which service providers must achieve compliance with these accessibility requirements.

Supreme Court Directives: Banks & NBFCs Action Matrix

The Supreme Court issued twenty directives in the said judgement to ensure that services are not denied based on disability and digital services are accessible to all the citizens irrespective of the impairments. Most of these are for the regulators, while a few are for regulated entities.

Following is the list of actionables arising out of the directives for banks and NBFCs:

- Undergo mandatory periodic accessibility audits by certified professional[1], may involve PwD in user testing of apps/websites (SC directive ii);

- Procure or design devices or websites / applications / software in compliance of accessibility standards for ICT Products and Services as notified by Bureau of Indian Standards. This mandate applies to a broad spectrum of digital products and services, including :

- Websites and web applications;

- Mobile apps;

- KYC/e-KYC/video-KYC modules;

- Digital documents and electronic forms; and

- Hardware touchpoints (ATMs, self-service machines). (SC directive xi)

- Cannot reject PwD applications without proper human consideration, must record reasons for rejection. Banks and NBFCs may appoint a designated officer who shall be empowered to override automated rejections and approve applications on a case-by-case basis (SC directive xvi and KYC 2nd Amendment to Para 11 of the KYC Directions).

- In the process of customer due diligence, REs can accept Aadhaar Face Authentication as valid method for Authentication ( KYC 2nd Amendment to Para 16 of the KYC Directions).

- During the V-CIP process, REs cannot rely solely on eye-blinking for liveness verification. They must ensure liveness checks do not exclude persons with special needs. For this purpose, the officials of banks or NBFCs may ask varied questions to establish the liveness of the customer (KYC 2nd Amendment to Para 18(b)(i)).

Changes to the KYC Directions

Changes have been introduced in the KYC Directions via the KYC 2nd Amendment as a result of the SC verdict, these are captured in the diagram:

Implementation Plan

Based on the Supreme Court directive in Pragya Prasun & Ors. vs Union of India and the subsequent RBI notification, here is a comprehensive stage-wise action plan for implementing digital accessibility requirements for banks and NBFCs:

Phase 1: Immediate Compliance and Assessment

Actionables for REs under phase 1 are listed below:

- Stage 1.1: Current State Assessment

- Inventory all client facing platforms like digital platforms, mobile apps, websites, and KYC systems;

- Document current accessibility barriers and non-compliant features and identify high-risk areas requiring immediate attention.

- Stage 1.2: Policy Framework Development

- Amend the KYC Policy to incorporate accessibility clauses for PwD;

- Update existing KYC Policy to incorporate paper based KYC other than video based KYC (provided such verification methods shall not result in any discomfort to the applicant); and

- Make necessary changes to internal documents and SOPs to include disability-inclusive customer service protocols.

Phase 2: Technical Foundation and Alternative Methods

Actionables for REs under phase 2 are listed below:

- Stage 2.1: Alternative KYC Methods Implementation

- Implement alternative means of liveness detection other than blinking of an eye such as:

- Gesture-based verification (beyond eye blinking);

- Facial movement detection;

- Audio-based liveness checks; or

- Any other method feasible to the RE

- Provide notices regarding the alternative methods of KYC that the RE supports/provides to PwD

- In case of biometric based e-KYC verification, accept thumb impressions or AADHAAR face authentication or any other biometric alternatives.

- In case of paper-based KYC, strengthen offline processes as accessible alternatives in such a manner that the same shall not cause any discomfort to the applicant.

- Remove mandatory blinking requirements in video KYC.

- Implement alternative means of liveness detection other than blinking of an eye such as:

- Stage 2.2: Technical Infrastructure Updates

- Ensure that all digital platforms of the RE meet the accessibility standards for ICT Products and Services as notified by Bureau of Indian Standards

- Ensure that assistive technology is integrated into the current systems such as screen reader compatibility, voice navigation, etc.

- Stage 2.3: Data Capture Enhancements

- Modify KYC templates in such a way to add disability fields(type and percentage) to be able to serve better to the applicants

- Update database to capture disability-related information (including preferred communication and customer authentication methods) for appropriate service delivery

Phase 3: Process Redesign and Human Support

Actionables for REs under phase 3 are listed below:

- Stage 3.1: Human-Assisted Channels

- Establish dedicated helpline for PwD offering step-by-step assistance in completing the KYC process through voice or video support;

- Conduct staff sensitization and disability awareness programs across all offices/branches

- Authorise/allow support from nominated guardians/family members to assist in the KYC process

- In case of persons dependent on sign languages, video calling service with certified interpreters shall be provided

- Stage 3.2: Grievance Mechanism Setup

- May develop dedicated accessibility complaints system for disability-related issues

- Ensure manual assessment of rejected KYC applications

- Establish clear timelines and accountability for redressal of grievances

- Stage 3.3: Alternative Service Delivery

- Train BCs/agents for disability-inclusive KYC assistance

- Doorstep customer authentication for severely disabled applicants, provided that such facility shall not cause any discomfort to the applicant

Phase 4: Testing and Validation

Actionables for REs under phase 4 are listed below:

- Stage 4.1: User Acceptance Testing

- May involve PwD in testing phases

- Ensure a diverse disability testing- cover visual, hearing, physical, and cognitive impairments

- Ensure testing the complete customer journey from onboarding to service access

- Document and address all accessibility issues through feedback integration

- Stage 4.2: Third-Party Validation

- Engage an IAAP certified professional for conducting the accessibility audit

- Conduct security assessment of alternative authentication methods

Phase 5: Training and Capacity Building

Actionables for REs under phase 5 are listed below:

- Stage 5.1: Staff Development Programs

- Create comprehensive training modules for disability awareness and sensitivity, alternative KYC procedures, assistive technology usage, customer service best practices, etc.

- Conduct customized programs for different staff categories and ongoing skill development

- Stage 5.2: Vendor and Partner Training

- Ensure external partners such as BCs, tech-cendors, third-party service providers, etc. understand accessibility requirements

Phase 6 : Continuous Improvement and Compliance

Actionables for REs under phase 6 are listed below:

- Define the frequency of the accessibility audit and ensure that the audit is conducted on a regular basis (as per the decided frequency)

- Submit compliance status/plan of implementation to RBI as and when required

Closing Remarks

The Supreme Court’s judgment in the Pragya Prasun case elevates digital accessibility from a moral imperative to a constitutional mandate. Banks and NBFCs must view this not as a burden but as an opportunity to transform compliance into competitive advantage by becoming an accessibility leader.

[1] List of Empanelled Web Accessibility Auditors with Department of Empowerment of Persons with Disabilities, Ministry of Social Justice & Empowerment, Govt. of India.

Read More: Resources on KYC

Presentation on IBC Amendment Bill, 2025

YouTube Recording of Discussion on Bill: https://youtube.com/live/jAvKP7U5qKY

Read More:

IBC for a makeover: bold and beautiful! Quick highlights of the IBC Amendment Bill, 2025

RBI rationalises Guarantee regulations

Introduces principle-based regulatory approach and reporting requirements

– Vinita Nair & Harshita Malik | corplaw@vinodkothari.com

– Updated on January 13, 2026

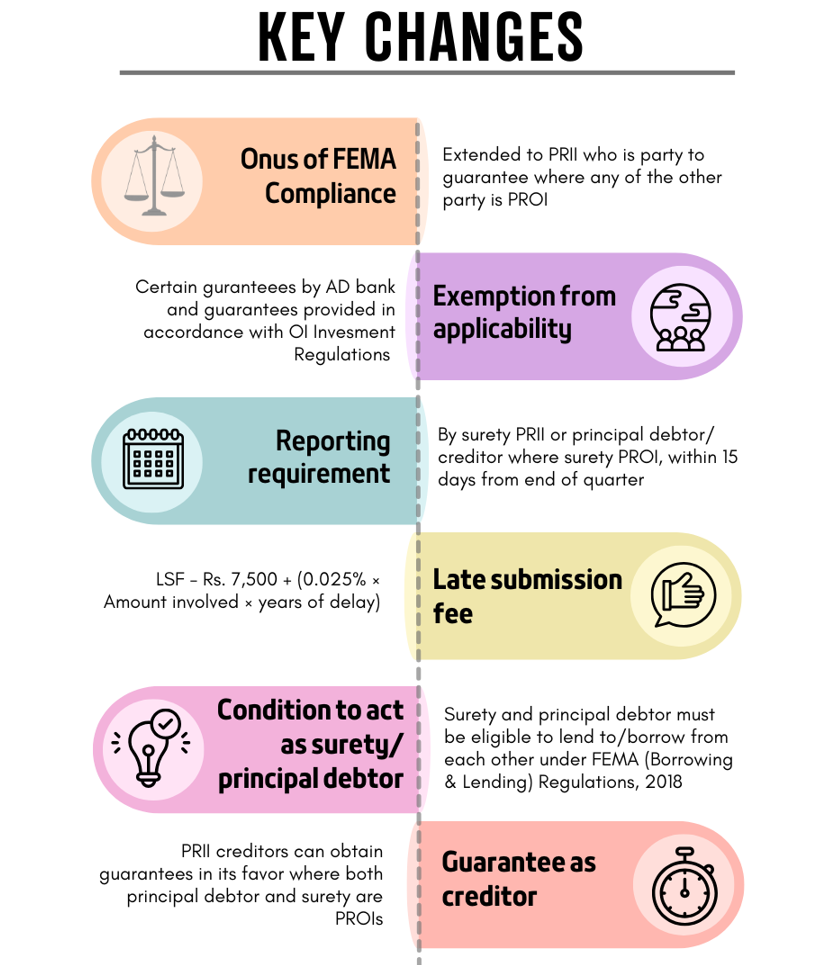

Effective January 10, 2026, FEMA (Guarantees) Regulations, 2026 (‘Regulations, 2026’) came into force repealing the 26-year-old FEMA (Guarantees) Regulations, 2000 (‘Erstwhile Regulations’), moving to principle based requirements and introducing comprehensive reporting of all requirements for all guarantees . Regulations, 2026 apply to guarantee arrangements involving a surety (person who gives the guarantee), a principal debtor (a person in respect of whose default the guarantee is given) and a creditor (means a person to whom the guarantee is given) where the Person Resident In India (‘PRII’) provides/ avails guarantee to/ from a Person Resident Outside India (‘PROI’). The meaning of guarantee1 includes counter guarantees and (based on stakeholders feedback) also a guarantee for securing a portfolio of debt, obligations or other liabilities.

Regulations, 2026 comprises of 8 regulations covering the general Prohibition (Reg 3), Exemptions for certain transactions by AD Bank and (based on stakeholders feedback) guarantees extended in terms of overseas investment regulations (Reg 4), Permission to act as a surety or a principal debtor (Reg 5), Permission to obtain a guarantee as a creditor (Reg 6), Reporting Requirements (Reg 7) and Late Submission fee for delayed reporting (Reg.8). These have been notified based on the feedback received on the Draft FEMA (Guarantees) Regulations, 2025 (‘Draft Regulations’) issued in August 2025.

Onus of compliance [Reg. 3]

The Erstwhile Regulations placed the onus on the PRII giving a guarantee or a surety in relation to a debt, obligation or other liability owed to or undertaken by PROI. Regulations, 2026 additionally extends the onus even to a PRII who is the party to a guarantee (surety or creditor or a principal debtor) where any of the other party is a PROI.

Exemptions under Regulations, 2026 [ Reg 4]

- Guarantees by AD Bank’s branch outside India or in IFSC (based on stakeholders feedback), unless any of the other parties to guarantee is a PRII;

- Guarantees by AD Bank in the nature of Irrevocable Payment Commitment (IPC) issued as a custodian bank for a registered FPI on behalf of an authorised central counterparty in India, considering the same is treated as a financial guarantee in terms of RBI prudential norms for commercial banks.

- Guarantees provided in accordance with FEMA (Overseas Investment) Regulations 2022 (based on stakeholders feedback) – considering those are governed and reported under a separate framework altogether.

Conditions to act as Surety/ Principal Debtor [Reg. 5]

A PRII can give a guarantee or be the principal debtor if the following two conditions are met:

- Condition 1: The underlying transaction for which the guarantee is being given or arranged is NOT prohibited under FEMA; and

- Condition 2: Surety and principal debtor must be eligible to lend to and borrow from each other under FEMA (Borrowing & Lending) Regulations, 2018 (clause earlier referred to ‘resultant transaction’ and has been modified based on stakeholders feedback). It is intended that at the time of issuance of guarantee itself, the surety and the principal debtor shall ensure that they are eligible to lend and borrow to each other as per Foreign Exchange Management (Borrowing and Lending) Regulations, 2018. Compliance with other attendant conditions, such as cost, maturity, etc. for borrowing and lending is not envisaged.

However, Condition 2 provides for three exceptions (listed below in the table):

| Nature of guarantee | Given by | In favor of | Condition for exemption |

|---|---|---|---|

| Guarantees by AD bank backed by counter guarantee or collateral (based on stakeholders feedback) | AD Bank | PROI | Covered by counter-guarantee OR 100% cash collateral in the form of deposit from PROI |

| Guarantee by agents of foreign Shipping/Airline company | Agent in India | Foreign Shipping/Airline Co. | In connection with its obligation/ liability owed to statutory/Government authority in India |

| Both Indian Parties | PRII | PRII | Both surety & principal debtor are PRIIs |

Further, the prohibition added in the Draft Regulations in line with RBI Circular of March 13, 2018 disallowing AD Bank from giving a Letter of Comfort or a Letter of Undertaking is not expressly covered in Regulations, 2026. However, the circular of March 2018 does not seem to have been repealed by RBI either. Accordingly, the prohibition seems to continue.

Permission to obtain guarantee as a creditor [Reg. 6]

Explicit permission given to PRII creditors to obtain guarantees in its favor where both principal debtor and surety are PROIs, where the underlying transaction is not prohibited under the FEMA.

Reporting requirements [Reg. 7 and 8]

The Erstwhile Regulations did not provide for any reporting requirements. Guarantees provided as part of ECB or in favor of overseas subsidiaries were covered under the reporting made under respective regulations. Regulations, 2026 provide for detailed reporting requirements, with RBI having the right to put the information in public domain.

Who is to report: Regulations, 2026 mandate reporting of guarantees through the AD Banks. Reporting is required to be made by the

a) Resident surety; or

b) Principal debtor who arranged the guarantee, where surety is PROI; or

c) Creditor – where both surety and principal debtor are PROI or where the creditor has arranged the guarantee.

In case of more than one surety/ principal debtor/ creditor to the same guarantee, any of them can be designated to report that guarantee (based on stakeholders feedback).

To whom: To the AD Bank

What is to be reported: Guarantees covered in Regulations, 2026 – (a) issuance of guarantee, (b) any subsequent change in guarantee terms, namely – guarantee amount, extension of period or pre-closure, and (c) invocation of guarantee, if any,

Format: Form GRN (format provided at Annex to the Regulations, 2026).

One of the instructions for filing form GRN states that change of guarantees issued prior to coming into effect of these regulations i.e. January 10, 2026 shall be reported as a fresh issuance of guarantee from the date of modification. This seems to indicate that guarantees outstanding as on January 10, 2026 need not be reported unless there is a modification. In that case, an invocation of an existing guarantee may also not be required to be reported unless there is any modification which has been reported to the AD Bank under Regulations, 2026.

Further, quarterly reporting on issuance of guarantee for Trade Credit is being discontinued from quarter ending March 2026.

Periodicity and timeline: On a quarterly basis, within 15 days from the end of the respective quarter (revised to periodic basis from ‘as and when basis’ based on stakeholders feedback). Draft regulations provided for reporting within7 days from the date of issuance/ aforementioned change/ invocation of such guarantee

Further, AD Bank to onward report to RBI within 30 days from end of quarter.

Late Submission fee: Rs. 7,500 + (0.025% × A × n) rounded up to nearest hundred, where:

- A = amount involved in the delayed reporting in INR; and

- n = years of delay rounded-upwards to the nearest month and expressed up to 2 decimal points.

Amendments to ECB Master Directions

Deletion of Para 17.2 of the Master Direction – External Commercial Borrowings, Trade Credits and Structured Obligations (ECB Master Directions) dealing with the quarterly reporting requirement on data on bank guarantees for trade credits furnished by AD Bank.

Deletion of guarantee related provisions in Part III dealing with Structured Obligations: Para 19 dealing with terms and conditions for Non-resident guarantee for domestic fund based and non-fund based facilities and Para 20 dealing with terms and conditions for Facility of Credit Enhancement by eligible non-resident entities to domestic debt raised through issue of capital market instruments.

Amendments to other Master Directions

Master Directions – Export of Goods and Services, Master Directions – Import of Goods and Services , Master Direction – Other Remittance Facilities – Deletion of provision relating to issue of various guarantee in relation to export, import transactions covered under Erstwhile Regulations as Regulations, 2026 move to a principal based regime.

Master Direction – Reporting under Foreign Exchange Management Act, 1999 inserting Form GRN in relation to reporting of guarantees .

Conclusion

The Regulations, 2026 is certainly a welcome change, introducing principle-driven framework, expanded scope (counter-guarantees, portfolio guarantees), and simplified quarterly reporting. Specific requirements provided under ECB norms, ODI rules, Borrowing and lending regulations etc. shall continue to be complied while undertaking the transaction and the existing arrangements should be reviewed for new quarterly reporting obligations in case of modifications.

You may read more at our Resource centre on FEMA

- including a ‘counter guarantee’ means a contract, by whatever name called, to perform the promise, or discharge a debt, obligation or other liability (including a portfolio of debts, obligations or other liabilities), in case of default by the principal debtor ↩︎

FAQs on profit computation under section 198 of the Companies Act, 2013

Setu-ing the Standard: NPCI’s New Path to Aadhaar e-KYC

Archisman Bhattacharjee | finserv@vinodkothari.com

Introduction

The National Payments Corporation of India (NPCI), vide its notification NPCI/2024-25/e-KYC/003 dated 10 March 2025, formally introduced the e-KYC Setu facility. As outlined on NPCI’s official platform, e-KYC Setu enables Aadhaar-based e-KYC authentication under the Aadhaar (Targeted Delivery of Financial and Other Subsidies, Benefits and Services) Act, 2016 (Aadhaar Act), without disclosing the individual’s Aadhaar number to the requesting (verification-seeking) entity.

Designed as a one-stop onboarding solution for regulated financial-sector entities, e-KYC Setu leverages Aadhaar-based e-KYC services while ensuring compliance with privacy safeguards under the Aadhaar Act. A key feature and a significant compliance advantage is that regulated entities using e-KYC Setu are not required to obtain a separate notification under Section 11A of the Prevention of Money-laundering Act, 2002 (PMLA). This allows financial sector regulator entities to conduct Aadhaar-based authentication without directly collecting Aadhaar numbers or integrating with UIDAI as a licensed AUA/KUA, thereby reducing both operational complexity and regulatory burden.

In this article, we examine the regulatory implications for RBI-regulated entities, the legal permissibility for non-AUA/KUA entities to conduct authentication through e-KYC Setu, process how e-KYC setu operatives and the operational and business benefits of adopting this framework.

Read more →