Far reaching changes, several strategic initiatives, bold moves to overcome impact of jurisprudence that did not seem to serve the policy framework – these few words may just approximately describe the IBC Amendment Bill. The Bill has been put to a Select Committee of the Parliament, and may hopefully come back in the Winter Session. However, the mind of the Government is clear: if a bold legal reform has faced implementation challenges, the Government will clear the roadblocks. Some extremely crucial amendments might soon see the light of day, providing much-required clarity on priority of creditors, role of AA, group insolvency, among others.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-08-13 14:42:572025-08-15 17:40:54IBC for a makeover: bold and beautiful! Quick highlights of the IBC Amendment Bill, 2025

Since its introduction in 2021, the concept of Accredited Investors (AIs) has been through some changes. A Consultation Paper was published on 17th June, 2025 to provide for certain flexibilities in the accreditation framework. Another Consultation Paper dated 8th August 2025(‘AI CP’) proposed to bring light-touch regulations for AIF schemes seeking investments from only AIs, including extension of various exemptions to such schemes, that are currently available to Large Value Funds (LVFs).

Further, vide another Consultation Paper(‘LVF CP’), some relaxations were also proposed to be extended to Large Value Funds (LVFs) for AIs. Note that the LVFs are available only for AIs, and hence, the Amendment Regulations define the AIs-only schemes to include LVF.

The SEBI (Alternative Investment Funds) (Third Amendment) Regulations, 2025 has been notified on 18th November, 2025, thus introducing the concept of AI-only schemes in the regulatory framework. Note that, vide the 2nd Amendment Regulations, the angel funds have also been exclusively restricted to Accredited Investors only. See an article on the Angel Funds 2.0: Navigating the New Regulatory Landscape.

Accredited Investors – who are they?

An AI is considered as an investor having professional expertise and experience of making riskier investments. Reg 2(1)(ab) of AIF Regulations defines an accredited investor as any person who is granted a certificate of accreditation by an accreditation agency, and specifies eligibility criteria. The eligibility criteria is as follows:

Further, certain categories of investors are deemed to be AIs, that is, certificate of accreditation is not required, such as, Central and State Governments, developmental agencies set up under the aegis of the Central Government or the State Governments, sovereign wealth funds and multilateral agencies, funds set up by the Government, Category I foreign portfolio investors, qualified institutional buyers, etc.

‘Accreditation’ as a measure of risk sophistication

AIFs are investment vehicles pooling funds of sophisticated investors, and not for soliciting money from retail investors. The measure of sophistication, as specified in the AIF Regulations currently, is in the form of the ‘minimum commitment threshold’. Reg 10(c) of the Regulations require a minimum investment of Rs. 1 crore, except in case of investors who are employees or directors of the AIF or of the Manager.

There are certain shortcomings of considering the minimum commitment threshold as the metric of risk sophistication of an investor, such as:

May not necessarily lead to an actual draw-down, thus exposing to the risk of onboarding investors with inflated commitments. As per the data available on SEBI’s website, out of the total commitment of Rs. 13 lac crores for the quarter ended 31st March 2024, only about Rs. 5 lac crores worth of funds were actually drawn down. Similarly, for the quarter ended 31st March 2025, the value of commitment vis-a-vis funds raised

Does not consider the investor’s financial health (income, net worth etc), hence, a potential risk of the investor putting majority of its wealth in AIFs, a riskier investment class.

The concept of AIs, as proposed in February 2021, was to introduce a class of investors who have an understanding of various financial products and the risks and returns associated with them and therefore, are able to take informed decisions regarding their investments. Accreditation of investors is a way of ensuring that investors are capable of assessing risk responsibly.

The June 2025 CP indicated that it is being examined to move AIFs gradually in an exclusively for AIs approach, starting with investments in angel funds and in framework for co-investing in unlisted securities of investee companies of AIFs. Accordingly, the present CP has proposed a gradual and consultative transition from ‘minimum commitment threshold’ to ‘accreditation status’ as a metric of risk sophistication of an investor.

Flexibility for AIs-only schemes vis-a-vis other AIFs

The accreditation status is to be ensured at the time of onboarding of investors only. Therefore, if an investor subsequently loses the status of AI in interim, the same shall still be considered as an AI for the AI only scheme, once on-boarded. The following relaxations have been extended to AIs-only schemes, in order to provide for a light-touch regulatory framework, from investor protection viewpoint, considering that the AIs have the necessary knowledge and means to understand the features including risks involved in such investment products:

This facilitates differential rights to different classes of investors within a scheme.

Extension of tenure of close-ended funds [reg 13(5)]

up to two years subject to approval of two-thirds of the unit holders by value of their investment in AIF

This facilitates a longer tenure extension to an existing close-ended scheme, if suited to investors.

However, it is further clarified that the maximum extension permissible to such AI only schemes, inclusive of any tenure extension prior to such conversion, shall be 5 years.

Certification criteria for key investment team of Manager [reg 4(g)(i)]

Atleast one key personnel with relevant NISM certification

The investors, being accredited, the reliance on key investment team of the Manager is comparatively low.

Further, in case of AIs-only Funds, the responsibilities of Trustee as specified in Reg 20 r/w the Fourth Schedule shall be fulfilled by the Manager itself. This is based on the premise that, the investors, being accredited, the reliance on Trustee for investor protection is comparatively low.

Large Value Funds: a sub-category of AIs only scheme

The concept of LVF was also introduced in 2021, along with the concept of AIs. An LVF, in fact, is an AIs only fund, with a minimum investment threshold. Reg 2(1)(pa) of the AIF Regulations defines LVF as:

“large value fund for accredited investors” means an Alternative Investment Fund or scheme of an Alternative Investment Fund in which each investor (other than the Manager, Sponsor, employees or directors of the Alternative Investment Fund or employees or directors of the Manager) is an accredited investor and invests not less than seventy crore rupees.

Since an LVF is included within the meaning of an AIs-only scheme, all exemptions as available to an AIs only scheme, are naturally available with an LVF, although the converse is not true.

Additional Exemptions available to LVFs (other than as available to AIs only scheme)

In addition to the relaxations extended to an AIs only scheme, there are additional exemptions available to an LVF. These are:

Regulatory reference

Topic

Exemption for LVF

Reg 12(2)

Filing of placement memorandum through merchant banker

Not applicable

Reg 12(3)

Comments of SEBI on PPM through merchant banker

Not applicable, only filing with SEBI required

Reg 15(1)(c)

Investment concentration for Cat I and Cat II AIFs – cannot invest more than 25% of investable funds in an investee company, directly or through units of other AIFs

May invest upto 50% of investable funds in an investee company, directly or through units of other AIFs

Reg 15(1)(d)

Investment concentration for Cat III AIFs – cannot invest more than 10% of investable funds in an investee company, directly or through units of other AIFs

May invest upto 25% of investable funds in an investee company, directly or through units of other AIFs

Reduction in minimum investment size for LVFs

The minimum investment threshold for investors in LVF has been reduced from Rs. 70 crores to Rs. 25 crores, based on the recommendations of SEBI’s Alternative Investment Policy Advisory Committee (AIPAC). The rationale is to lower entry barriers to facilitate improved fund raising, without compromising on the level of investor sophistication. The reduction of investment thresholds would also facilitate investments by regulated entities having a strict exposure limit, such as insurance companies.

Exemptions from requiring specific waivers for certain provisions

The extant regulations permitted that the responsibilities of the Investment Committee may be waived by the investors (other than the Manager, Sponsor, and employees/ directors of Manager and AIF), if they have a commitment of at least Rs. 70 crores (USD 10 billion or other equivalent currency), by providing an undertaking to such effect, in the format as provided under Annexure 11 of the AIF Master Circular, including a confirmation that they have the independent ability and mechanism to carry out due diligence of the investments.

The requirement of specific waiver has been omitted for LVFs considering that AIs are already required to provide an undertaking for the purpose of availing benefits of ‘accreditation’. The undertaking, as per the format given in Annexure 8 of the AIF Master Circular states the following:

(i) The prospective investor ‘consents’ to avail benefits under the AI framework.

(ii) The prospective investor has the necessary knowledge and means to understand the features of the investment Product/service eligible for AIs, including the risks associated with the investment.

(iii) The prospective investor is aware that investments by AIs may not be subject to the same regulatory oversight as applicable to investment by other investors.

(iv) The prospective investor has the ability to bear the financial risks associated with the investment.

Similarly, LVFs have been exempt from following the standard PPM template without the requirement of obtaining specific waiver from investors.

Migration of existing eligible AIFs

One of the proposals of the LVF CP is to permit eligible AIFs, not formed as an LVF, to convert themselves into an LVF and avail the benefits available to LVF schemes. The conversion shall be subject to obtaining positive consent from all the investors. Following the same, the modalities for such migration has been specified by SEBI vide circular dated 8th December, 2025.

Pursuant to such migration, the AIF manager shall ensure that:

Name of the converted scheme contains ‘AI only fund’ or ‘LVF’ as the case may be

Such conversion and change in name to be reported to SEBI within 15 days through dedicated email ID

Such change in name to be reported to depositories within 15 days of conversion

Limit on maximum number of investors

Reg 10(f) puts a cap on the maximum number of investors in a scheme. Pursuant to the Amendment Regulations, the cap of 1000 investors shall not include the AIs.

In practice, the number of investors in an AIF is much lower than 1000, and hence, the amendment may not have much of a practical relevance.

Conclusion

The amendments are a step towards providing a lighter regulatory regime for AIFs, meant for sophisticated investors, capable of making well-informed decisions. The move is expected to witness more schemes focussed on AIs only, and thus, bring an AIs only regime for AIFs. In order to differentiate an AIs only scheme or an LVF from other AIF schemes, it is mandatory for the newly launched schemes henceforth to have the words ‘AI only fund’ or ‘LVF’ as the case maybe.

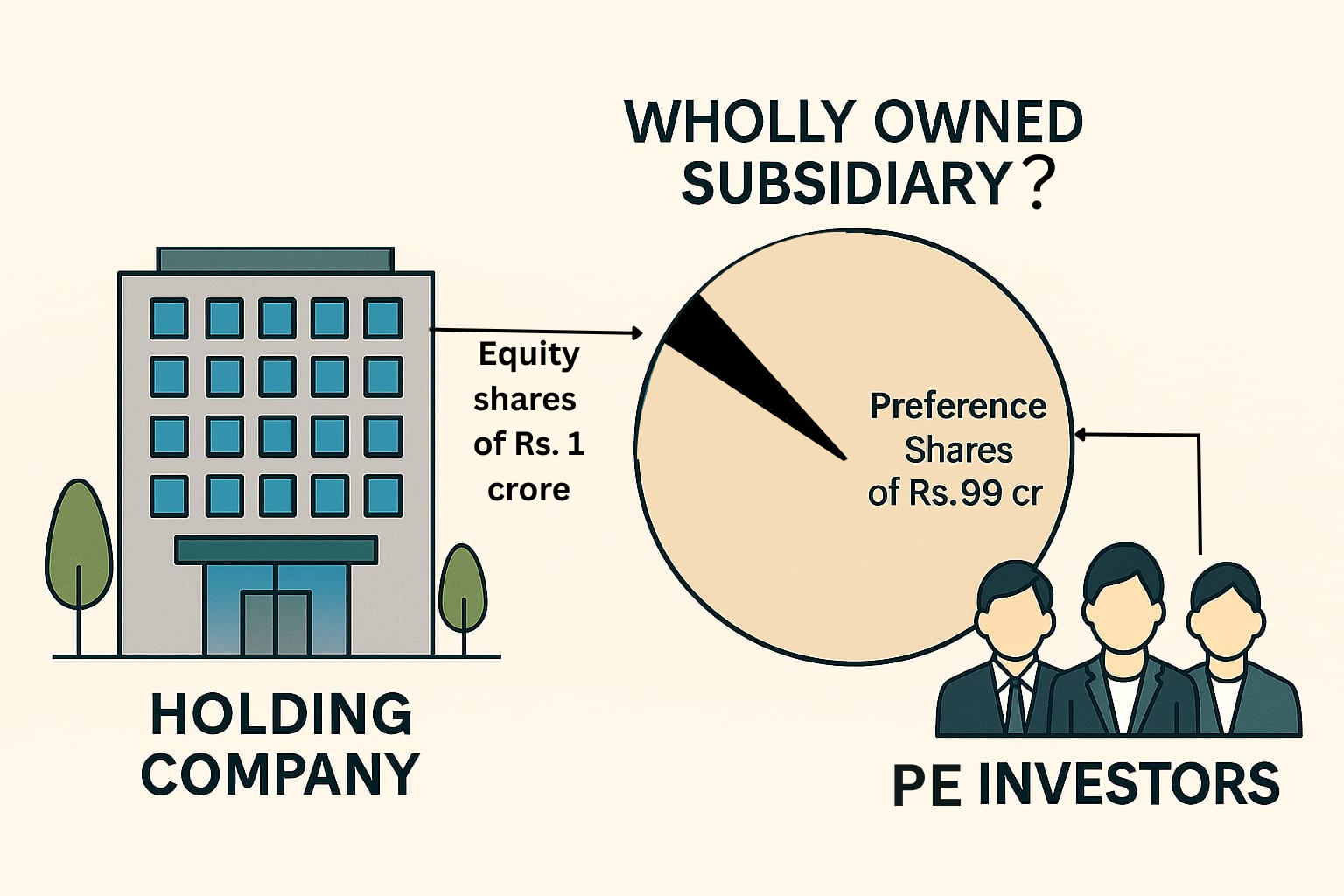

Do preference shares matter for wholly-owned subsidiary status?

Preference shares are a much preferred means of raising funds from third party investors by Indian startups. The reasons for such popularity may be accorded to the priority of payment over the equity shares, thus providing a layer of protection, flexibility in exit as compared to the permanent equity capital, ease of structuring and various other factors. Very often, this may lead to the total preference share capital holding a higher proportion as against the equity share capital of the company.

This brings a very interesting question to the fore – whether a company having preference share capital held by third parties, may still be considered to be a “Wholly Owned Subsidiary” (WOS), if such company has a sole equity shareholder, as its holding company. The question becomes particularly relevant in view of the exemptions provided to a company/ its group with respect to the WOS.

Compliance haven provided to a WOS

The Indian laws provide a myriad of relaxations in statutory requirements – a compliance haven to wholly owned subsidiaries.

Some of these have been tabulated below:

Sr. No

Law

Section / Rule/ Regulation

Exemption

1.

CA, 2013

Section 185

The prohibitions/ restrictions u/s 185 does not apply with respect to the loans given by the holding company to its WOS or security or guarantee provided in respect of loans to its WOS.

2.

CA, 2013

Section 186

The limits on loan, guarantee, security, investments etc by holding company is not applicable in case of WOS.

3.

CA, 2013

Section 177(4)(iv) and 188

Transactions between a holding company and its WOS are exempt from the approval of the Audit Committee, except in some cases. Further, RPTs specified under section 188 are exempt from shareholders’ approval. Our article on RPTs with WOS may be accessed here.

4.

SEBI Listing Regulations, 2015

Regulation 23

Exemption from AC and shareholders’ approval for RPTs with a WOS or between two WOS of the listed holding company.

5.

CA, 2013

Section 149(4), 177 and 178 read with Rule 4 of the Companies (Appointment and Qualification of Directors) Rules, 2014 and Rule 6 of Companies (Meetings of Board and its Powers) Rules, 2014

The following requirements do not apply: Appointment of independent directors Constitution of Audit Committee Constitution of Nomination and Remuneration Committee

6.

CA, 2013

Section 2(87) r/w Rule 2(1) of the Companies (Restriction on Number of Layers) Rules, 2017

A layer consisting entirely of 1 or more WOS is not considered as a layer for the prohibition on having only 2 layers of subsidiaries. Our article on the restrictions w.r.t. layers of subsidiaries may be read here.

7.

CA, 2013

Section 29 read with Rule 9A(11) of the Companies (Prospectus and Allotment of Securities) Rules, 2017

A public company that is a WOS is exempt from the requirement of mandatory dematerialisation of securities. Read our article on mandatory dematerialisation of shares here.

8.

CA, 2013

Section 233

Fast track Merger is permitted between a holding company and its WOS. See our article on the procedure of fast track merger here.

9.

SEBI Listing Regulations, 2015

Regulation 37

The requirement of obtaining a No-Objection Letter from the Stock exchange is dispensed for a scheme of arrangement between a listed holding company and its WOS.

10.

SEBI Listing Regulations, 2015

Regulation 37A

The requirement of shareholders’ approval for sale, lease or disposal of an undertaking, outside a scheme of arrangement, is exempt if made to the WOS.

11.

The Indian Stamp Act, 1899

Articles 23 and 62 of Schedule I, Circular issued in 1937

Stamp duty on mergers is remitted if the merger is between a parent company and subsidiary company (parent company holding beneficial ownership of at least 90% of its share capital) or2 subsidiary companies (Common parent company is holding the beneficial ownership of at least 90% of the share capital of both the companies). Our article on the same may be accessed here

The exemptions follow primarily an enterprise level approach, as against, entity level – thus, considering the WOS as nothing but an extended arm of the holding company. The Listing Regulations further uses the expression: whose accounts are consolidated with such listed entity, thus, signifying the relevance of ‘control’ while availing exemptions w.r.t. a WOS.

Thus, the position and rights of the preference shareholders need to be analysed in reference to whether the same provides any sort of ‘ownership’ or ‘control’ to such shareholders.

Preference shareholder as a member of the company

Section 2(55) of the CA, 2013 defines the term ‘member’ in the following manner:

(i) the subscriber to the memorandum of the company who shall be deemed to have agreed to become member of the company, and on its registration, shall be entered as member in its register of members;

(ii) every other person who agrees in writing to become a member of the company and whose name is entered in the register of membersof the company;

(iii) every person holding shares of the company and whose name is entered as a beneficial owner in the records of a depository;

The definition covers every person whose name is entered in the register of members, as well as every person holding ‘shares’ in the company having their name recorded with the depository. The term ‘shares’ covers both equity and preference shares [Section 2(84) read with Section 43]. Further, in terms of section 88, the details of preference shareholders shall also be entered in the register of members. Thus, it is beyond doubt that the preference shareholders, too, are members of the company.

Preference shares: equivalent to ‘debt’ or considered as ‘capital’

In accounting parlance, preference shares are more likely to be classified as ‘debt’ than ‘equity’, depending on the terms of redemption or conversion. However, legally, the position of preference shareholder is not considered equivalent to a ‘creditor’, as has been a matter of jurisprudence in various cases.

“The shareholders of redeemable preference shares of the company do not become creditors of the company in case their shares are not redeemed by the company at the appropriate time. They continue to be shareholders, no doubt subject to certain preferential rights mentioned in Section 85 of the Companies Act, 1956.”

“ . . . we cannot persuade ourselves to accept the contentions of the assessee and hold that when a company issues redeemable preference shares it is in fact obtaining a loan as it could by issuing debentures. There is a fundamental difference between the capital made available to a company by issue of a share and money obtained by a company under a loan or a debenture. Respective incidences and consequences of issuing a share and borrowing money on loan or on a debenture are different and distinctive. A debenture-holder as a creditor has a right to sue the company, whereas a shareholder has no such right. Apart from that the scheme of the Companies Act and in particular the forms and contents of its balance-sheets are extremely rigid and, in our view, by reason of the specific compartments in such accounts it is not possible to convert an item of capital into an item of loan as has been suggested on behalf of the assesse.”

In the context of assigning a vote to the preference shareholders in a meeting of creditors, the Hon’ble Bombay High Court held the following in the case of State Bank Of India vs Alstom Power Boilers Ltd :

“A preference share is not a debt instrument. Preference share amount is a capital and not a debt. Thus, in the meeting of the creditors, it would not be possible to assign a value to the vote of a holder of preference share. If we were to hold that the preference shareholders who are not paid dividend for more than two years are also entitled to attend the meeting of the creditors under Section 391 of the Act and to vote thereat, then it would be impossible to determine what would be the value to their votes vis-a-vis the value of votes of creditors. It would be wrong to contend that preference shareholders have a right to vote but, valuation of their vote is unascertainable. We are therefore of the view that preference shareholders are not entitled to attend and vote at the meeting of the creditors convened under Section 391 of the Act even though dividend on the preference shares have remained unpaid for more than 2 years.

In Globe United Engineering & Foundry Co. Ltd, the Hon’ble Delhi High Court, while dealing with the question pertaining to the rights of the preference shareholders over arrears of dividend, observed the following:

“(15) The outside investor may be induced to subscribe for preference rather than ordinary shares by reason of the bargain offered; such investor has usually little knowledge of the company’s business, has no wish to participate in the company’s management and is keen only on his promised return. It may also happen that if the companies want to raise new capital when their existing shares are worth less than the nominal value the only direct way of raising new capital. apart from borrowings and debentures, will be to issue new class of shares with preferential rights over the existing ones. The preference shares are really part of the company share capital: they are not loans.”

The question of whether a failed redemption of preference shares constitute a contractual debt, has been a matter of jurisprudence, primarily in the context of maintainability of an application under IBC. See an article on the same here. The Hon’ble NCLAT, in a very recent judgement in the matter of EPC Constructions India Limited v. M/S Matix Fertiliser and Chemicals Limited, pertaining to the maintainability of an application by the preference shareholders under section 7 of IBC, held the following:

“…the Appellant who is holder CRPS is holder of shares which is in the nature of equity in capital, which is part of preferential share capital as defined in Section 43. Preferential shares being part of the preferential share capital of the Company shall not transfer any debt so as to initiate any Section 7 proceeding. Further, the Company having not earned any profit nor any dividend having been declared, no redemption was permissible by the statutory provision, hence, no debt was due on basis of which Section 7 application could be filed by the Appellant. There is also no material that any proceeds of a fresh issue of shares made for the Company Appeal (AT) (Insolvency) No. 1424 of 2023 purpose of such redemption was available. We, thus, fully endorse the finding of the Adjudicating Authority that there did not exist any default.”

Rights of the Preference Shareholders

Based on the various rulings discussed above, it is amply clear that preference shareholders are not creditors of the company, rather, shareholders. However, these are not equity shares, and cannot be treated at par with the equity shareholders. Murray A Pickering, in a scholarly analysis [The Problem of the Preference Share, Vol. 26 (1963) Modem Law Review], regards three principles as basically established and quotes from three decisions :

(1) The rights inter se of preference and ordinary shareholders must depend on the terms of the instrument which contains the bargain that they have made with the company and each other (a question of construction, vide Lord Simonds in Scottish Insurance Corporation, Limited v. Wilsons & Clyde Coal Company Limited, 1949 A.C. 462);

(2) where the articles set out the rights attached to a class of shares to participate in profits while the company is a going concern or to share in the property of the company in liquidation; prima facie, the rights so set out are in each case exhaustive (vide Wynn Parry, J. in re The Isle of Thenet Electricity Supply Co. Ltd., (1950) Ch. 161) and

(3) In the absence of specific provisions the rights of all shareholders are deemed to be the same (vide Lord Macnaghten in Birch v. Cooper and others, (1889) 14 A.C. 525)- case not referred (page 500 of Pickcring’s Article).

Thus, the rights of preference shareholders are based on the terms of the instrument and the Articles of the company. In the absence of any specific provisions, the rights of all shareholders are deemed to be the same.

Under the Companies Act, 2013, the rights of the preference shareholders are briefly contained in section 43 and section 47. Further, where a right is available to equity shareholders only, the same is stated expressly under the relevant provision. For instance, section 62 of the Act explicitly recognises only equity shareholders to be eligible for participating in a rights issue.

Economic rights of preference shareholders

Certain rights are available to preference shareholders, by definition. This includes preferential rights with respect to:

Payment of dividend, either as a fixed amount or a fixed rate

Repayment of capital, at the time of winding up or otherwise

Depending on the terms of issue, this may further include the participating rights with respect to surplus dividend or capital repayment.

Voting rights of preference shareholders

Section 47(2) of CA, 2013 limits the preference shareholders’ right to vote in a company on the following resolutions only in the same proportion as the paid-up capital in respect of the preference shares bears to the paid-up capital in respect of the equity capital:

Resolutions which directly affect the rights attached to their preference shares.

Resolution for winding up of the company.

Resolution for the repayment or reduction of its equity or preference share capital.

However, pursuant to the second proviso to the said section, the preference shareholders acquire a right to vote on all the resolutions of the company where the dividend in respect of that particular class of preference shares has not been paid for a period of 2 years or more. Thus, the preference shareholders are not completely devoid of voting rights, they too have the right to vote on some matters or in specified conditions.

Preference shareholders, thus, may be compared with a sleeping monster. As long as the dividend is paid, the monster remains sleeping. But if the company defaults in the payment of their dividend for a period of 2 years, the monster awakens and is entitled to equal voting rights in the company as the equity shareholders. Once the default is made good by the company, that is to say, dividend is paid to the preference shareholders, whether the additional voting rights of such preference shareholders are revoked and they assume their erstwhile status or the voting rights assume permanence is not clearly laid down under the current provisions of CA, 2013. The question has been discussed in our article titled Voting Rights on Preference Shares: An Unclear Provision?. Companies putting off the payment of dividend on preference shares risk waking up the monster who might never go back to sleep again.

Further, pursuant to MCA notification no. GSR 464 (E) dated 5th June, 2015, certain exemptions were given to private companies. The notification, amongst others, provides exemption from the applicability of section 43 and section 47 to a private company where memorandum or articles of association of the private company so provides.

Hence, flexibility is provided to a private company to structure its share capital, including the voting rights therein, in the manner as may be required by such company, by providing for the same in the MoA or AoA of the company.

Thus, the voting rights on preference shares are not only in accordance with section 47 of the Act, but are also dependent on the terms of issue. In fact, companies which have issued compulsorily convertible preference shares (CCPS) often determine their total voting power on ‘as if converted’ basis.

Rights as a member of the company

In addition to the rights specific to preference shares, other rights that are available to any member of a company are also available to a preference shareholder. These rights inter alia include:

Right to receive annual reports and financial statements of the company [section 136]

Right to receive notice and attend general meetings of the company [section 101]

Right to inspect the registers and records of the company [section 94]

Right to give special notice for removing directors [section 115]

Right to give consent to or object to any proposed variation of shareholders’ rights [section 48]

Right to apply to the Tribunal for relief in case of oppression & mismanagement [section 244]

Meaning of ‘subsidiary’: based on shares or voting rights?

Wholly owned subsidiary is basically a ‘subsidiary’ that is ‘wholly owned’ by a shareholder. The term ‘Wholly Owned Subsidiary’ has not been defined under the CA, 2013 or the SEBI Listing Regulations, 2015. However, reference may be drawn from the definition of ‘subsidiary company’ as defined in section 2(87) of the CA, 2013. The definition reads as:

‘A company in which the holding company controls the composition of the Board of Directors or exercises or controls more than one-half of the total voting power either at its own or together with one or more of its subsidiary companies.’

Note that a subsidiary is defined with reference to ‘voting powers’ and not ‘shareholding’. Therefore, the non-voting share capital of a company is not required to be considered in the determination of a company as a ‘subsidiary’.

The shift from ‘total share capital’ to ‘total voting power’ was based on the recommendations of the Company Law Committee, which considered the alignment of the meaning of subsidiary with consolidation principles in accounting. The CLC deliberated as follows:

During the deliberations, it was noted that by virtue of the present definition, a company in which the preference share capital was greater than its equity share capital, could become a subsidiary of an entity that holds the preference shares, even though it might not have control, or any voting rights in such a company. Further, inclusion of the preference share capital in the total share capital could create confusion about ownership of the company. Further, such companies could be shown as subsidiaries, but would not be considered for consolidation purposes, as per the applicable Accounting Standards.

Thus, preference shareholding would generally not be considered for the purpose of determining a holding-subsidiary relationship, unless such preference shares carry voting rights. Further, in view of the rationale provided by the CLC, it is clear that the voting rights need to be in the nature of ‘decision-making’ rights, and not merely affirmative or protective rights.

Wholly-owned subsidiary: is control the only factor?

While the determination of a subsidiary is based on voting powers, can it be said that it is only the equity shareholders that ‘own’ a company? In other words, whether the preference shareholders do not have any ‘ownership’ rights over the company?

In the context of incorporating a WoS outside India, the erstwhile Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2000, further amended in 2004defined the term Wholly Owned Subsidiary as “A foreign entity formed, registered or incorporated in accordance with the laws and regulations of the host country, whose entire capital is held by the Indian party.” In the absence of any specific exclusions from the meaning of ‘capital’, the same would cover both equity and preference share capital.

Though this definition is no longer in force, the same hints on the intent of the regulator in considering the entire share capital holding as a criteria for considering a company as WoS.

WOS in the Global Context

That the determination of ‘subsidiary’ is a control-based approach, whereas a WoS is based on the entire shareholding and not merely voting rights is very clearly laid down in section 1159 of the Companies Act, 2006 of the United Kingdom. The section defines both ‘subsidiary’ and ‘wholly owned subsidiary’, in the following manner:

Subsidiary

Wholly owned subsidiary

A company is a “subsidiary” of another company, its “holding company”, if that other company— (a)holds a majority of the voting rights in it, or (b)is a member of it and has the right to appoint or remove a majority of its board of directors, or (c)is a member of it and controls alone, pursuant to an agreement with other members, a majority of the voting rights in it, or if it is a subsidiary of a company that is itself a subsidiary of that other company.

A company is a “wholly-owned subsidiary” of another company if it has no members except that other and that other’s wholly-owned subsidiaries or persons acting on behalf of that other or its wholly-owned subsidiaries.

Thus, while a ‘subsidiary’ is based on majority voting rights or such other rights that leads to ‘control’, the test of ‘wholly owned subsidiary’ is dependent on the sole membership, and is not restricted to just voting rights.

5.—(1) For the purposes of this Act, a corporation shall, subject to subsection (3), be deemed to be a subsidiary of another corporation, if — that other corporation — (i) controls the composition of the board of directors of the first-mentioned corporation; (ii) controls more than half of the voting power of the first-mentioned corporation; or (iii) holds more than half of the issued share capital of the first-mentioned corporation (excluding any part thereof which consists of preference shares and treasury shares); or the first-mentioned corporation is a subsidiary of any corporation which is that other corporation’s subsidiary.

5B. For the purposes of this Act, a corporation is a wholly owned subsidiary of another corporation if none of the members of the first-mentioned corporation is a person other than — that other corporation;a nominee of that other corporation;a subsidiary of that other corporation being a subsidiary none of the members of which is a person other than that other corporation or a nominee of that other corporation; ora nominee of such subsidiary.

Thus, while preference shares are explicitly excluded from the definition of ‘subsidiary’, no similar approach is followed in defining a wholly owned subsidiary.

15 U.S. Code § 80a-2 defines the term WoS in reference to ‘voting securities’. Thus, WoS is defined as: “acompany 95 per centum or more of the outstanding voting securities of which are owned by such person, or by acompany which, within the meaning of this paragraph, is a Wholly Owned Subsidiary of suchperson”. ‘Voting securities’, as defined in the said Code means “any security presently entitling the owner or holder thereof to vote for the election of directors of a company”. This may also include the preference shares, given the 12 U.S. Code § 51b entitles preference shareholders to such voting rights as may be provided for in the Articles of Association of the company.

Conclusion

Preference shareholders, though having certain rights distinct from equity shareholders, are still members of the company. Voting rights may be assigned to them either as a part of the terms of issue or upon non-payment of dividend. These preference shares may either be redeemable or convertible, and in case of the latter, becomes a part of equity share capital upon conversion. Wholly owned subsidiary should indicate complete ownership, in the form of 100% shareholding, and hence, even non-voting shares should be considered for the purpose of identification of an entity as such.

Where the preference shares are held by a person other than the holding company, the company should not be entitled to the benefits of being a wholly owned subsidiary.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-08-12 12:51:012025-08-12 16:38:38Wholly controlled, but not wholly owned

What was ushered in as a new era of legal reforms in the country, with keen interest from all over the world, is now a bruised, battered structure, even before it cuts its cake for the 10th time.

The BLRC Vision

When the Bankruptcy Law Reforms Committee first put the Insolvency and Bankruptcy Code, 2016 (“IBC”) into its mould, they envisaged it as a tool in the hands of creditors who should decide on the fate of a defaulting firm. As they put it, “The appropriate disposition of a defaulting firm is a business decision, and only the creditors should make it.” Needless to say, they also recognised that decision-making has to be quick – as delays lead to value destruction. Indeed, the design and structure of IBC was promising enough – a unique categorisation of creditors as financial and operational creditors (found no-where in the world) with financial creditors, a creditor-driven resolution process, strict hardbound timelines, an irreversible liquidation outcome, a well-thought of priority waterfall, and a court-appointed liquidator taking the corporate debtor to the death pyre.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-08-11 19:13:362025-08-15 17:41:29Done, dented, damaged: The IBC edifice, even before it’s 10

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-08-09 15:09:402025-08-12 10:17:37Lending Together Rewinded

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-08-08 13:01:122025-09-03 15:45:3512 hours Certificate Course on Nuts and Bolts of Related Party Transactions

The Directions definitively eliminate discretionary co-lending arrangements (CLM-2 model), mandating that any cherry-picking or selective loan purchase arrangements must comply with Transfer of Loan Exposures (TLE) Directions rather than co-lending provisions. The Directions are uniformly applicable to priority sector lending as well as any other lending, thereby having a harmonised regulatory framework.

In each case, a minimum funding share of fundamental restructuring requires each co-lending partner to maintain a minimum 10% (lowered from the previous requirement of 20% in case of the PSL co-lending arrangement) risk retention, ensuring genuine skin-in-the-game for all participants. In addition to the minimum 10% funding share, the Originating RE (even in non-digital lending cases) may also provide a Default Loss Guarantee (DLG) up to 5% of the “outstanding loans” (see discussion below – this expression has to be read in consonance with DLG framework). The Directions, however, explicitly prohibit subordination, waiver, or deferral of servicing fees thereby limiting credit enhancements in any other manner, but the flavour of the regulations seems to restrict credit support to DLG, for promoting transparent DLG structures only.

Unpacking the Highlights

As is always the case, some operational complexities have been addressed, while some have been created. There are also enhanced disclosure requirements, mandating clear segregation of roles and responsibilities in loan agreements, identification of single customer interface points and comprehensive Key Facts Statement (KFS) disclosures.

The Directions introduce borrower-level asset classification synchronization, requiring real-time information sharing (latest by next working day) when either lender classifies an exposure as SMA/NPA, creating significant operational challenges for lenders’ systems and processes. While KYC requirements have been streamlined to allow partner REs to rely on originating REs for customer identification as per the provisions of the KYC Master Directions, 2016, Credit Information Company (CIC) reporting is explicitly stipulated for each lender, which, in our view, is both unnecessary and undesirable. This results in continuing operational complexities for multiple reporting mechanisms.

Website disclosure requirements now mandate listing all active CLA partners (removing previous blended rate disclosure obligations), while financial statement disclosures shift to quarterly/annual basis aligned with applicable RE reporting cycles. The framework retains provisions for unrealized profit recognition “if applicable,” though, in our view, being pre-agreed and non-discretionary, the transfer of the Partner RE’s share is merely a consummation of what was anyways concluded, and therefore, there is no case of “transfer” in case of co-lending. If there is no sale, there is no case for booking of a gain on sale. And in our view, Co-lending structures typically wouldn’t trigger gain-on-sale accounting.

Customer protection is enhanced through mandatory prior intimation requirements for any changes in customer interface, ensuring continuity and transparency throughout the loan lifecycle. These comprehensive changes reflect RBI’s intent to create a more transparent, operationally robust, and prudentially sound co-lending ecosystem while addressing past regulatory ambiguities and market practices.

Please find below our highlights for an easy read.

The RBI’s framework for partial credit enhancement for bonds has significant improvements over the last 2015 version

The RBI has released a new comprehensive framework for non-fund based support, including guarantees, co-acceptances, as well as partial credit enhancement (PCE) for bonds. The guidelines with respect to non-fund based facilities other than PCE are not applicable on NBFCs. The PCE framework has been significantly revamped, over its earlier 2015 version.

Note that PCE for corporate bonds was mentioned in the FM’s Budget 20251, specifically indicating the setting up of a PCE facility under the National Bank for Financing of Infrastructural Development (NaBFID).nd

The highlights of the new PCE framework are:

What is PCE?

Partial Credit Enhancement (PCE) is a risk-mitigating financial tool where a third party provides limited financial backing to improve the creditworthiness of a debt instrument. Provision of wrap or credit support for bonds is quite a common practice globally.

PCE is a contingent liquidity facility – it allows the bond issuer to draw upon the PCE provider to service the bond. For example, if a coupon payment of a bond is due and the issuer has difficulty in servicing the same, the issuer may tap the PCE facility and do the servicing. The amount so tapped becomes the liability of the issuer to the PCE provider, of course, subordinated to the bondholders. In this sense, the PCE facility is a contingent line of credit.

A situation of inability may arise at the time of eventual redemption of the bonds too – at that stage as well, the issuer may draw upon the PCE facility.

Since the credit support is partial and not total, the maximum claim of the bond issuer against the PCE provider is limited to the extent of guarantee – if there is a 20% guarantee, only 20% of the bond size may be drawn by the issuer. If the facility is revolving in nature, this 20% may refer to the maximum amount tapped at any point of time.

Given that bond defaults are quite often triggered by timing and not the eventual failure of the bond issuer, a PCE facility provides a great avenue for avoiding default and consequential downgrade. PCE provides a liquidity window, allowing the issuer to arrange liquidity in the meantime.

Who can be the guarantee provider?

PCE under the earlier framework could have been given by banks. The ambit of guarantee providers has been expanded to include SCBs, AIFIs, NBFCs in Top, Upper and Middle Layers and HFCs.

As may be known, entities such as NABFID have been tasked with promoting bond markets by giving credit support.

Who may be the bond issuers?

The PCE can be extended against bonds issued by corporates /special purpose vehicles (SPVs) for funding all types of projects and to bonds issued by Non-deposit taking NBFCs with asset size of ₹1,000 crore and above registered with RBI (including HFCs).

What are the key features of the bonds?

REs may offer PCE only in respect of bonds whose pre-enhanced rating is “BBB minus” or better.

REs shall not invest in corporate bonds which are credit enhanced by other REs. They may, however, provide other need based credit facilities (funded and/ or non-funded) to the corporate/ SPV.

To be eligible for PCE, corporate bonds shall be rated by a minimum of two external credit rating agencies at all times.

Further, additional conditions for providing PCE to bonds issued by NBFCs and HFCs:

The tenor of the bond issued by NBFCs/ HFCs for which PCE is provided shall not be less than three years.

The proceeds from the bonds backed by PCE from REs shall only be utilized for refinancing the existing debt of the NBFCs/ HFCs. Further, REs shall introduce appropriate mechanisms to monitor and ensure that the end-use condition is met.

What will be the form of PCE?

PCE shall be provided in the form of an irrevocable contingent line of credit (LOC) which will be drawn in case of shortfall in cash flows for servicing the bonds and thereby may improve the credit rating of the bond issue. The contingent facility may, at the discretion of the PCE providing RE, be made available as a revolving facility. Further, PCE cannot be provided by way of guarantee.

What is the difference between a guarantee and an LOC? If a guarantor is called upon to make payments for a beneficiary, the guarantor steps into the shoes of the creditor, and has the same claim against the beneficiary as the original creditor. For example, if a guarantor makes a payment for a bond issuer’s obligations, the guarantor will have the same rights as the bondholders (security, priority, etc). On the contrary, the LOC is simply a line of liquidity, and explicitly, the claims of the LOC provider are subordinated to the claims of the bondholders.

If the bond partly amortises, is the amount of the PCE proportionately reduced? This should not be so. In fact, the PCE facility continues till the amortisation of the bonds in full. It is quite natural to expect that the defaults by a bond issuer may be back-heavy. For example, if there is a 20% PCE, it may have to be used for making the last tranche of redemption of the bonds. Therefore, the liability of the PCE provider will come down only when the outstanding obligation of the bond issuer comes to less than the size of the PCE.

Any limits or restrictions on the quantum of PCE by a single RE?

The previous PCE framework restricted a single entity to providing only 20% of the total 50% PCE limit for a bond issuance. The sub-limit of 20% has now been removed, enabling single entity to provide upto 50% PCE support.

Further, the exposure of an RE by way of PCEs to bonds issued by an NBFC/ HFC shall be restricted to one percent of capital funds of the RE, within the extant single/ group borrower exposure limits.

Who can invest in credit-enhanced bonds?

Under the earlier framework, only the entities providing PCE were restricted from investing in the bonds they had credit-enhanced. However, the new Directions expand this restriction by prohibiting all REs from investing in bonds that have been credit-enhanced through a PCE, regardless of whether they are the PCE provider. The new regulations state that the same is with an intent to promote REs enabling wider investor participation.

This is, in fact, a major point that may need the attention of the regulator. A universal bar on all REs from investing in bonds which are wrapped by a PCE is neither desirable, nor optimal. Most bond placements are done by REs, and REs may have to warehouse the bonds. In addition, the treasuries of many REs make opportunistic investments in bonds.

Take, for instance, bonds credit enhanced by NABFID. The whole purpose of NABFID is to permit bonds to be issued by infrastructure sector entities, by which banks who may have extended funding will get an exit. But the treasuries of the very same banks may want to invest in the bonds, once the bonds have the backing of NABFID support. There is no reason why, for the sake of wider participation, investment by regulated entities should be barred. This is particularly at the present stage of India’s bond markets, where the markets are not liquid and mature enough to attract retail participation.

What is the impact on capital computation?

Under the new Directions the capital is required to be maintained by the REs providing PCE based on the PCE amount based on applicable risk weight to the pre-enhanced rating of the bond. Under the earlier framework, the capital was computed so as to be equal to the difference between the capital required on bond before credit enhancement and the capital required on bond after credit enhancement. That is, the earlier framework ensured that the PCE does not result into a capital release on a system-wide basis. This was not a logical provision, and we at VKC have made this point on various occasions2.

Securitisation Transactions in India are primarily governed by:

The RBI Securitisation of Standard Assets Directions, 2021 (in case the originator is regulated by RBI)

SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, which become applicable if the securitisation notes are listed.

Consequently, an RBI regulated originator will be required to adhere to both the SSA Directions as well as the SDI Framework in case it intends to go for listing of the securisation notes.

Here, we have discussed the additional prohinitions and compliance requirements for RBI regulated originators which becomes applicable in case of listing of securitisation notes.

Additional Prohibitions under the SEBI SDI Framework for RBI Regulated Originators

Para Ref

Relevant Regulatory Provision

Our Comments

Single Asset Securitisation not permitted

19A(a)

“No obligor shall have more than twenty-five percent in asset pool at the time of issuance.”

An RBI regulated originator will not be able to undertake single asset securitisation if it intends to list the securitisation notes, though the same is permitted under the RBI regulations (proviso to para 5(s) of the SSA Directions). Comments: Single asset securitisation is not a very common practice, but this is explicitly permitted under RBI regulations

All assets to be homogenous

19A(b)

“Assets comprising the securitisation pool shall be homogeneous.”

The RBI SSA Directions only require the assets to be homogeneous in case of simple, transparent, and comparable securitisation transactions (STC Transactions). STC transactions are currently not very common, and in any case, is an investor classification, not that of issuer.For non-STC cases, there is no such requirement. Therefore, originators will be required to ensure that the assets comprising the pool are homogeneous in case they intend to go for listing of the securitisation notes. Comment: Homogeneity may be subjective

SPV can only be constituted in the form of a trust

9(1)

“The special purpose distinct entity shall be constituted in the form of a trust the constitutional document whereof entitles the trustees to issue securitised debt instruments.”

The RBI SSA Directions (para 5(w)) allow SPVs to be constituted in the form of a company, trust or other entity. Comment: Not a very big pain, as SPVs in India are almost always in the trust form.

Originator and Trustee not be under the same group or control.

10(3)

“No special purpose distinct entity shall acquire any debt or receivables from any originator which is part of the same group or which is under the same control as the trustee.”

This requirement, although essential to maintain independence, is not a part of the RBI SSA Directions. Accordingly, the same will be required to be ensured.

Additional Compliances applicable to RBI regulated Originators under the SEBI SDI Framework

Para Ref

Relevant Regulatory Provision

Our Comments

Registration of Trustees under the Securities and Exchange Board of India(Debenture Trustees) Regulations, 1993

4(b)

“(1) On and from the commencement of these regulations, no person shall make a public offer of securitised debt instruments or seek listing for such securitised debt instruments unless –XX(b)all its trustees are registered with the Board under 26[the Securities and Exchange Board of India(Debenture Trustees) Regulations, 1993];XX”

Accordingly, the trustees will be required to comply with the SEBI Debenture Trustee regulations. Comment: This is a useful provision, and mostly, the SPV trustees are registered debenture trustees. Hence, it is a useful regulatory requirement.

Contents of the Instrument of Trust

Schedule IV

Schedule IV of the SEBI SDI Framework prescribes the minimum contents of the instrument of trust.

The contents prescribed under the SDI Framework are more detailed as compared to the RBI SSA Directions, which only indicate the contents of the trust deed. Comment: Useful regulation, serving the purpose of proper disclosures. Notably, disclosures are the domain of the securities regulator.

Quarterly reports to the trustee about the performance of the underlying pool and auditor certificate

10A(1) and (2)

“(1) The originator shall provide the periodic reports to the trustee regarding the performance of the underlying asset pool, at least on a quarterly basis. (2) The originator shall provide a certificate from its auditor (s) regarding the disclosures of underlying asset pool assigned to the securitization trust, as made by the originator, on quarterly basis.”

The RBI SSA Directions (para 114 and 115) require semi-annual disclosures to be made. Further, there is no requirement to provide an auditor’s certificate under the RBI Directions. Comment: Useful regulation, serving the purpose of investor information. These disclosures are typically part of the securities regulators’ domain.

Minimum Ticket Size for subsequent transfers

30A(2)(i)

“The minimum ticket size for subsequent transfers of a securitised debt instrument shall be as follows:(i)for originators which are not regulated by the Reserve Bank of India, the minimum ticket size shall be rupees one crore.”

In case of public offer of SDIs, the minimum ticket size is Rs. 1 Crore even for subsequent transfers of SDIs. This requirement is more stringent as compared to the RBI SSA Directions (para 28), which only requires the minimum ticket size of Rs. 1 Crore to be seen at the time of issuance. Comments: The requirement has only been introduced for the public offer of SDIs. Public issue of SDIs is howe,ver not a common practice currently. Accordingly, this may not seem to be a major concern for RBI regulated originators.

Other miscellaneous provisions – offer period, allotment period, dematerialisation

29, 31(1)

Offer Period: No public offer of securitised debt instruments shall remain open for less than two working days and more than ten working days. Allotment Period:The securitised debt instruments shall be allotted to the investors within five days of closure of the offer. Further, the securitises will need to be issued mandatorily in demat form.

Comments: These requirements are applicable only in case of public offers.

Facility to avail electronic bidding platform

Master Circular dated May 16, 2025

On issue and listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper and on Review of provisions pertaining to Electronic Book Provider (EBP) platform to increase its efficacy and utility

The facility of using EBP has been extended to SDIs too. Comment: This is an optional facility, and as of now, very limited issuers have made use of this.

LODR Requirements – Chapter III

Disclosure by KMPs, directors, etc

Reg 5

5. The listed entity shall ensure that key managerial personnel, directors, promoters or any other person dealing with the listed entity, complies with responsibilities or obligations, if any, assigned to them under these regulations 51[:]52[Provided that the key managerial personnel, directors, promoter, promoter group or any other person dealing with the listed entity shall disclose to the listed entity all information that is relevant and necessary for the listed entity to ensure compliance with the applicable laws.]

This requires the concerned officers of the Listed Entity (in this case, the SPV] to make requisite disclosures for the purpose of complying with the law. Comment: Does not seem to be practically relevant, as Originators’ KMPs mostly do not have interest in the SPV. However, where needed, it is a useful disclosure.

Compliance officer to be appointed.

Reg 6, Chap III

6. (1) A listed entity shall appoint a qualified company secretary as the compliance officer Other provisions of the regulation

An issuer of SDIs is required to appoint a Compliance Officer. Comments: The requirement may be complied with at SPV level.

Share Transfer Agent

Reg 7

(1)The listed entity shall appoint a share transfer agent or manage the share transfer facility in-house:Other requirements of the regulation

The requirement to appoint a share transfer agent is typically part of the securities regulators’ domain. Comment: Mostly not relevant as the securities are offered in demat form.

Information to intermediaries

Reg 8

The listed entity, wherever applicable, shall co-operate with and submit correct and adequate information to the intermediaries registered with the Board such as credit rating agencies, registrar to an issue and share transfer agents, debenture trustees etc, within timelines and procedures specified under the Act, regulations and circulars issued there under:Provided that requirements of this regulation shall not be applicable to the units issued by mutual funds listed on a recognised stock exchange(s) for which the provisions of the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996 shall be applicable.

Requirement to share information with the information agencies. Comment: In case of listed SDIs, this is a part of the information eco system.

Policy for preservation of documents

Reg 9

The listed entity shall have a policy for preservation of documents, etc.

Useful for preservation of documents.

Filing of reports, statements and other documents

Reg 10

(1) The listed entity shall file the reports, statements, documents, filings and any other information with the recognised stock exchange(s) on the electronic platform as specified by the Board or the recognised stock exchange(s).Other provisions of the regulation

This is a general filing requirement for filing of information on the stock exchanges.

Scheme of arrangement to not violate, affect or override the provisions of securities law

Reg 11

The listed entity shall ensure that any scheme of arrangement /amalgamation /merger /reconstruction /reduction of capital etc. to be presented to any Court or Tribunal does not in any way violate, override or limit the provisions of securities laws or requirements of the stock exchange(s):.

Mostly not relevant for SDIs

Use of electronic mode of payments

Reg 12

The listed entity shall use any of the electronic mode of payment facility approved by the Reserve Bank of India, in the manner specified in Schedule I, for the payment of the following:(a) dividends;(b) interest;(c) redemption or repayment amounts:

Provides for mode of payments to investors. Not a cumbersome requirement as it refers to RBI-permitted payment systems to be used.

SCORES

Reg 13

(1) 61[The listed entity shall redress investor grievances promptly but not later than twenty-one calendar days from the date of receipt of the grievance and in such manner as may be specified by the Board.]Other provisions of the Regulation

This relates to use of the SCORES mechanism for settling investor issues

Payment of Fees and charges

Reg 14

The listed entity shall pay all such fees or charges, as applicable, to the recognised stock exchange(s), in the manner specified by the Board or the recognised stock exchange(s).

This mandates payment of listing fees. Usual provision for all listed securities

LODR Regulations – Chapter VIII

The entire Chapter is dedicated to listed SDI issuance.

Reg 81

Applicability(1) The provisions of this chapter shall apply to Special Purpose Distinct Entity issuing securitised debt instruments and trustees of Special Purpose Distinct Entity shall ensure compliance with each of the provisions of these regulations.(2) The expressions “asset pool”, “clean up call option”, “credit enhancement”, “debt or receivables”, “investor”, “liquidity provider”, “obligor”, “originator”, “regulated activity”, “scheme”, “securitization”, “securitized debt instrument”, “servicer”, “special purpose distinct entity”, “sponsor” and “trustee” shall have the same meaning as assigned to them under [Securities and Exchange Board of India (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008]555;

Specifies applicability of the Chapter and refers to meaning of relevant expressions

Intimation and filings with stock exchange(s)

Reg 82

(1) The listed entity shall intimate the Stock exchange, of its intention to issue new securitized debt instruments either through a public issue or on private placement basis (if it proposes to list such privately placed debt securities on the Stock exchange) prior to issuing such securities.(2) The listed entity shall intimate to the stock exchange(s), at least two working days in advance, excluding the date of the intimation and date of the meeting, regarding the meeting of its board of trustees, at which the recommendation or declaration of issue of securitized debt instruments or any other matter affecting the rights or interests of holders of securitized debt instruments is proposed to be considered.(3) The listed entity shall submit such statements, reports or information including financial information pertaining to Schemes to stock exchange within seven days from the end of the month/ actual payment date, either by itself or through the servicer, on a monthly basis in the format as specified by the Board from time to time:Provided that where periodicity of the receivables is not monthly, reporting shall be made for the relevant periods.(4) The listed entity shall provide the stock exchange, either by itself or through the servicer, loan level information, without disclosing particulars of individual borrowers, in manner specified by stock exchange.

This regulation is equivalent of reg 29 in case of listed equities, and provides for prior intimation to investors for certain critical actions on the part of issuers.

Disclosure of information having bearing on performance/operation of listed entity and/or price sensitive information

83 read with Part D of Schedule III

(1) The listed entity shall promptly inform the stock exchange(s) of all information having bearing on the on performance/operation of the listed entity and price sensitive information.(2) Without prejudice to the generality of sub-regulation(1), the listed entity shall make the disclosures specified in Part D of Schedule III.Explanation.- The expression ‘promptly inform’, shall imply that the stock exchange must be informed must as soon as practically possible and without any delay and that the information shall be given first to the stock exchange(s) before providing the same to any third party.

This regulation is to ensure the regular flow of information from issuers to investors, to maintain information symmetry. This is typical for all listed securities – for example, Reg 30 in case of listed equities, and reg 51 in case of listed non convertible debt securities.

Credit Rating to be periodically reviewed and any revision to be notified

Reg 84

(1) Every rating obtained by the listed entity with respect to securitised debt instruments shall be periodically reviewed, preferably once a year, by a credit rating agency registered by the Board.(2) Any revision in rating(s) shall be disseminated by the stock exchange(s).

This Regulation requires a mandatory annual review of credit ratings on the SDIs by a SEBI-registered CRA, and intimation of any revision to the stock exchanges.

Information to Investors

Reg 85

(1) The listed entity shall provide either by itself or through the servicer, loan level information without disclosing particulars of individual borrower to its investors.(2) The listed entity shall provide information regarding revision in rating as a result of credit rating done periodically in terms of regulation 84 above to its investors.(3) The information at sub-regulation (1) and (2) may be sent to investors in electronic form/fax if so consented by the investors.(4) The listed entity shall display the email address of the grievance redressal division and other relevant details prominently on its website and in the various materials / pamphlets/ advertisement campaigns initiated by it for creating investor awareness.

This clause requires certain pool level information; useful information for the poolComment: As in case of other jurisdictions, the disclosure requirements are typically laid by the securities regulations

Terms of Securitized Debt Instruments

Reg 86

(1) The listed entity shall ensure that no material modification shall be made to the structure of the securitized debt instruments in terms of coupon, conversion, redemption, or otherwise without prior approval of the recognised stock exchange(s) where the securitized debt instruments are listed and the listed entity shall make an application to the recognised stock exchange(s) only after the approval by Trustees.(2) The listed entity shall ensure timely interest/ redemption payment.(3) The listed entity shall ensure that where credit enhancement has been provided for, it shall make credit enhancement available for listed securitized debt instruments at all times.(4) The listed entity shall not forfeit unclaimed interest and principal and such unclaimed interest and principal shall be, after a period of seven years, transferred to the Investor Protection and Education Fund established under the Securities and Exchange Board of India (Investor Protection and Education Fund) Regulations, 2009.(5) Unless the terms of issue provide otherwise, the listed entity shall not select any of its listed securitized debt instruments for redemption otherwise than on pro rata basis or by lot and shall promptly submit to the recognised stock exchange(s) the details thereof.(6) The listed entity shall remain listed till the maturity or redemption of securitised debt instruments or till the same are delisted as per the procedure laid down by the BoardProvided that the provisions of this sub-regulation shall not restrict the right of the recognised stock exchange(s) to delist, suspend or remove the securities at any time and for any reason which the recognised stock exchange(s) considers proper in accordance with the applicable legal provisions.

This requires prior approval of the stock exchange to be obtained for making any material modification to the structure of SDIs. It also requires the originator to ensure timely payments of interest and for the credit enhancement to be available at all times.

Record Date

Reg 87

(1) The listed entity shall fix a record date for payment of interest and payment of redemption or repayment amount or for such other purposes as specified by the recognised stock exchange(s).(2) The listed entity shall give notice in advance of atleast seven working days (excluding the date of intimation and the record date) to the recognised stock exchange(s) of the record date or of as many days as the Stock Exchange may agree to or require specifying the purpose of the record date.

This is for fixation of record date for payouts; useful for investor decisions for entry or exit.

Disclosure of Information having bearing on performance/ operation of listed entity and/ or price sensitive information

Part D of Schedule III

Several disclosure requirements for significant events and developments

See comments under reg 83

Other Resources: Buy our book on Securitised Debt Instruments here.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-08-06 12:10:422025-08-06 12:17:05Listed and Restricted? Additional Compliances and Prohibitions for listing of SDIs by RBI regulated Originators