Unlocking Working Capital: An Overview of Supply Chain Finance

-Dayita Kanodia, Executive | finserv@vinodkothari.com

The best way to reduce your supply chain inventory is to sell it.” Dilbert.

Background

A supply chain is a complex network of organizations, people, activities, information, and resources involved in the creation and distribution of a product or service from its initial sourcing of raw materials to the delivery of the final product to the end customer. The supply chain of a business can vary significantly depending on the industry, size of the company, and the specific products or services it offers.

Financing the supply chain is a critical aspect of supply chain management and is essential for ensuring the smooth flow of goods and services.

This article discusses the model of supply chain finance and how it helps in improving the health of the supply chain.

Structure of Supply Chain Finance

Supply Chain Finance (SCF), also known as channel finance or reverse factoring, is a financial arrangement that helps companies optimize their working capital and improve the efficiency of their supply chain operations. It involves the use of financial instruments and techniques to facilitate the smooth flow of funds between buyers, suppliers, and financial institutions.

Here is how it typically works:

Buyer-Supplier Relationship: In a typical supply chain, a buyer purchases goods or services from a supplier. In vendor finance (as discussed below) it is generally a large company which is the buyer and multiple smaller suppliers. The buyer generally purchases raw materials for manufacturing purposes.

A business may also have a chain of dealers to whom it supplies goods for further distribution. The dealers may however not have the sufficient resources to pay for the goods upfront.

Invoice Approval: After receiving goods or services, the buyer approves the invoice, which specifies the amount owed and payment terms. Payment terms can vary but often range from 30 to 90 days.

Supplier’s Dilemma: Suppliers often face a cash flow challenge in waiting for payment from the buyer. They may need funds to cover their operational costs, such as materials, labor, and other expenses. This delay in payment can strain their finances.

Financial Institution’s Involvement: SCF involves a financial institution (like a bank or a specialized supply chain finance provider) that steps in to help suppliers access early payment for their invoices. The financial institution evaluates the creditworthiness of the buyer rather than the supplier, which allows suppliers to obtain financing at favorable rates.

Supplier Receives Early Payment: The financial institution may pay the supplier a significant portion (usually a high percentage) of the invoice amount, often within a few days of invoice approval. This helps the supplier cover its immediate financial needs.

Buyer’s Benefit: The buyer still pays the full invoice amount to the financial institution on the originally agreed-upon payment terms. However, this delayed payment benefits the buyer by allowing them to optimize their working capital and extend their payment terms.

Advantages

SCF offers several advantages for both buyers and suppliers:

Working Capital Optimization: Buyers can extend their payment terms, which can free up cash for other investments, while suppliers can access early payments to meet their financial obligations.

Improved Supplier Relationships: Early payment to suppliers can strengthen the relationship between buyers and suppliers, leading to better collaboration and potentially lower costs.

Risk Mitigation: Suppliers face less financial risk because they receive early payment, reducing their exposure to late or non-payment.

Increased chances of payment on the due date by the buyer: Due to the presence of the lending institution, there is an increased likelihood that the buyer will make the payment on the due date.

Access to Lower-Cost Financing: Suppliers can access financing at a lower cost compared to traditional forms of borrowing, such as loans or lines of credit.

Efficiency and Transparency: Supply chain finance platforms and technology can streamline the invoicing and payment processes, improving transparency and reducing errors.

Overall, supply chain finance is a financial strategy that benefits both sides of a transaction by optimizing cash flow, reducing risk, and enhancing collaboration within the supply chain.

Suppliers face less financial risk because they receive early payment, reducing their exposure to late or non-payment.

Overall, supply chain finance is a financial strategy that benefits both sides of a transaction by optimizing cash flow, reducing risk, and enhancing collaboration within the supply chain.

Forms of supply chain Finance

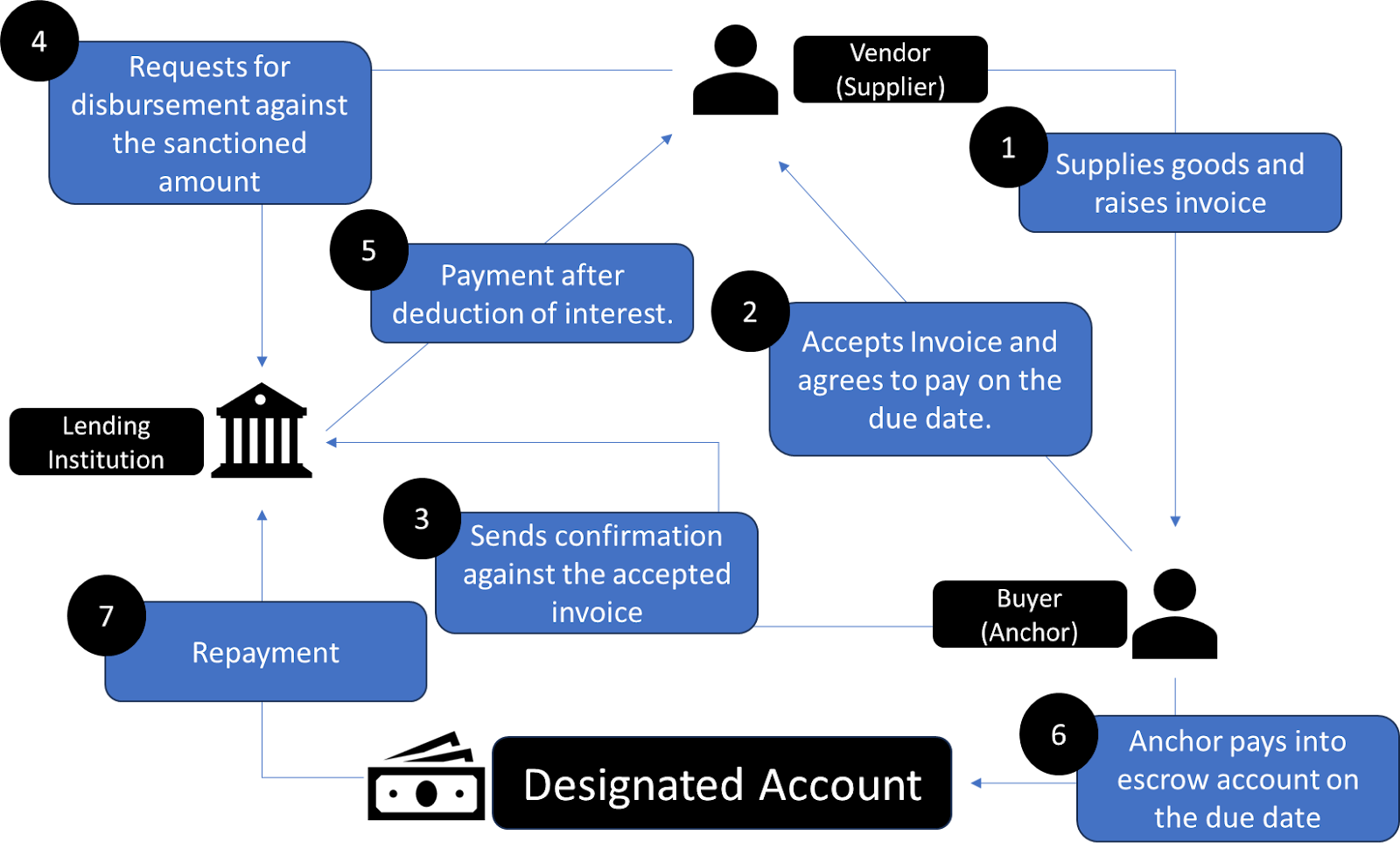

Vendor Financing

Vendor finance is an aspect of SCF where the buyer of goods (who are mostly large corporations) get extended payment terms for the goods purchased from their suppliers. This is because of the presence of a lending institution which advances money against the invoices duly accepted by the buyer ( generally referred to as the anchor) to the supplier (referred to as the borrower). This disbursement to the supplier generally happens after deduction of interest.

Subsequently on the due date the money is paid by the anchor into the designated account of the lender.

Let’s assume ABC ltd is engaged in the business of manufacturing jute bags. It has a network of suppliers who supply raw materials for the manufacturing process. Naturally these suppliers will raise invoices against the raw materials supplied. However, there is a time lag between the manufacturing of jute bags and subsequently selling it to get enough cash flow to pay to the suppliers. It therefore approaches a lending institution and provides it with a list of suppliers who are fulfilling such criterias as decided between ABC ltd and the lending institution.

Subsequently, a supplier raises an invoice of Rs.10000 on ABC ltd which is confirmed by it. The lending institution then advances Rs.8500 (interest of Rs.1500 is deducted) to the supplier. On the due date ABC deposits Rs. 10000 into the designated account of the lending institution.

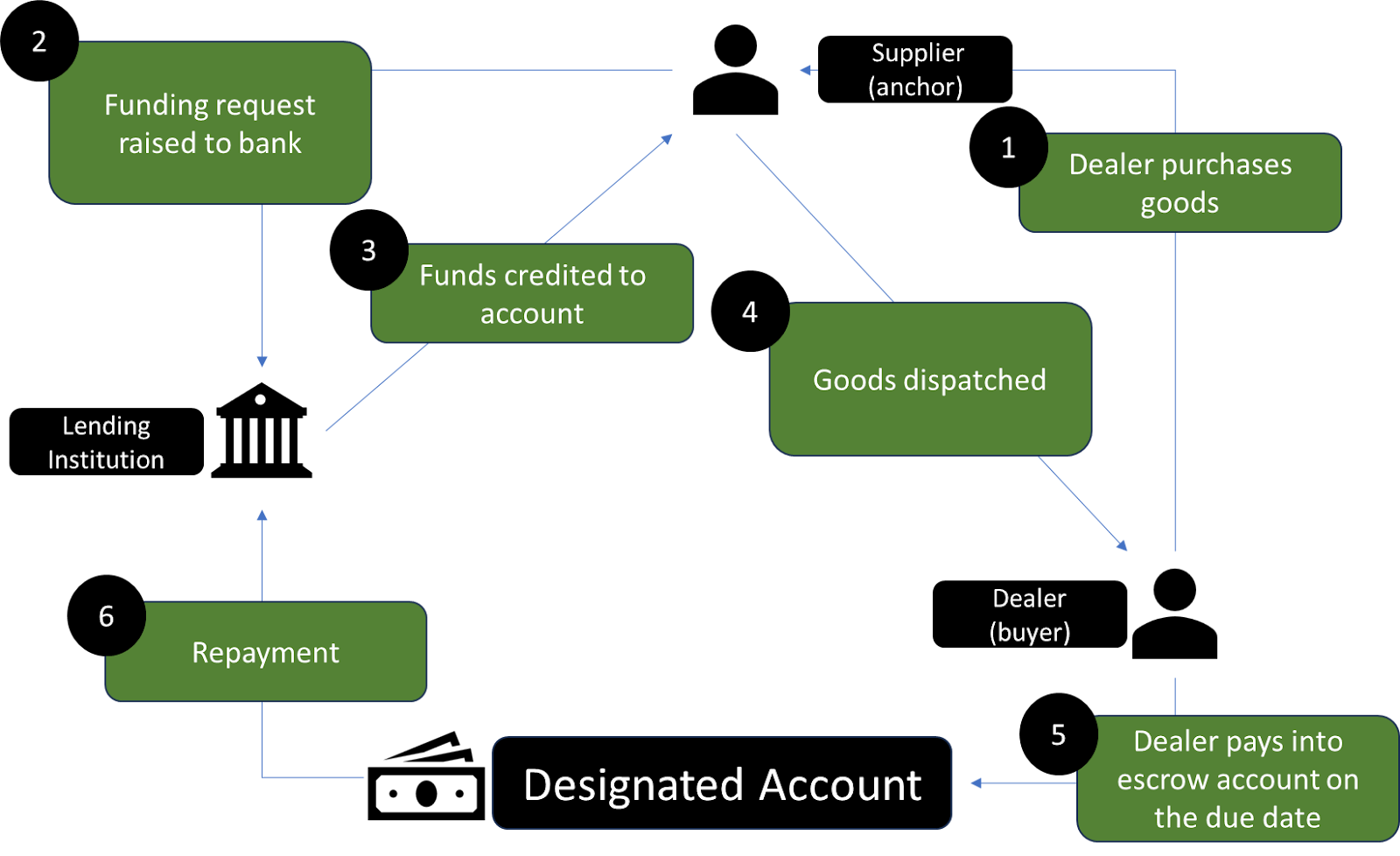

Dealer Financing

Another aspect of SCF is dealer finance which allows dealers to purchase goods from sellers (also referred to as anchor) at flexible payment terms. Here, a lending institution on the basis of an indent advances money to the seller for the goods purchased by the dealer. The dealer then on the due date makes payment to the lending institution.

A manufacturer of Television has a network of dealers who purchase the TV sets from it to sell it in the market. However, it is very difficult for these dealers to pay the upfront price for the TV sets before the same is sold in the market. The manufacturer who wants upfront payment approaches a lending institution and provides it with a list of dealers.

Lets say a TV set of Rs.60000 is sold to the dealer and an invoice is raised. The lending institution will then advance money against this invoice to the manufacturer and the dealer is therefore obligated to pay on the due date to the lending institution.

Anchor and the lending Institution

Anchor is the entity which initiates the program.

In vendor finance, the buyer has an arrangement with the lending institution wherein, it provides the institution with a list of suppliers fulfilling certain eligibility criteria. This list is generally updated from time to time. Here it is the buyer of goods who is referred to as the anchor.

Similarly, in case of dealer finance, the sellers which are generally large corporations provide a list of dealers to the lending institution. Therefore, the anchor over here is the seller of goods.

What happens if the buyer fails to pay on the due date ?

SCF puts an obligation on the buyer to make the payment on the due date. But what happens if the buyer fails to do the same ? – Will the lender then have a recourse against the seller ?

Typically yes. In case the buyer (dealer in case of dealer finance) fails to deposit the amount into the designated account of the lender, the lender then gives a notice to the seller and asks it to make the payment within 2-3 working days.

Maintenance of a security deposit by the anchor

It is a common practice for the anchor to maintain a security deposit in the form of cash or lien marked fixed deposit with the lender.

This security deposit is generally maintained from the very inception of the program, i.e before any disbursement is made by the lending institution.

The lender then has a right to use this security deposit in the event the buyer does not make the payment on the due date.Thus, the lender has dual recourse to recover its money – one against the seller (as discussed above) and second, by way of a set off against the security deposit maintained by the anchor. Sometimes, lenders prefer to first ask the supplier for payment before proceeding to set off the amount against the security deposit.

Other securities and credit supports

Apart from the maintenance of a security deposit, it is a common practice among lending institutions to obtain collateral from the supplier or the buyer. This includes obtaining personal guarantees from third parties for the supplier (dealer in case of dealer finance).

Factoring and Reverse Factoring

SCF is also referred to as reverse factoring. Therefore, it is important to understand the difference between factoring and reverse factoring.

Factoring and reverse factoring are both financial mechanisms used by businesses to manage cash flow and working capital, but they operate in different ways and serve distinct purposes.

Factoring, also known as accounts receivable factoring, involves a business selling its outstanding invoices (accounts receivable) to a third-party financial institution (the factor) at a discount. The factor provides an immediate cash advance to the business, typically around 70-90% of the invoice value, and assumes responsibility for collecting payment from the customers.

On the other hand, reverse factoring is a financial arrangement that facilitates early payments from a buyer to its suppliers with the assistance of a third-party financial institution. It is designed to optimize cash flow within the supply chain.

Unlike factoring, reverse factoring is typically initiated by the buyer, not the seller.

Further, factoring helps businesses access immediate cash flow by converting unpaid invoices into working capital. It is often used by businesses, especially small and medium-sized enterprises (SMEs), to address cash flow challenges caused by slow-paying customers.

However, reverse factoring aims to enhance the financial stability of both buyers and suppliers. It allows buyers to extend their payment terms while offering suppliers early payment options at a lower cost compared to traditional financing.

Thus we can say that factoring is akin to invoice discounting and reverse factoring is akin to supply chain finance.

Way forward

Overall, supply chain finance is a financial strategy that benefits both sides of a transaction by optimizing cash flow, reducing risk, and enhancing collaboration within the supply chain. For every participant in the supply chain ecosystem—access to quick, low-cost and efficient financing is crucial to optimize the cash flow.

In fact as per estimates the supply chain finance market size by 2031 will be around $13.4 billion as compared to $6 billion in 2021.

Thus, as the business landscape continues to evolve, supply chain finance is expected to play an increasingly prominent role in helping companies adapt and thrive.

| Our articles on the subject can be viewed below- 1. Basics of Factoring in India 2. India Factoring Report 2023 |

Do we need to perform KYC for Anchor/ dealer, in whose account we are disbursing the loan amount