Appraising post IPO governance requirements

Appraising post IPO governance requirements

Other ‘I am the best’ presentations can be viewed here

Our other relevant resources –

Other ‘I am the best’ presentations can be viewed here

Our other relevant resources –

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –

Other ‘I am the best’ presentations can be viewed here

Our other related articles –

Corplaw Team | corplaw@vinodkothari.com

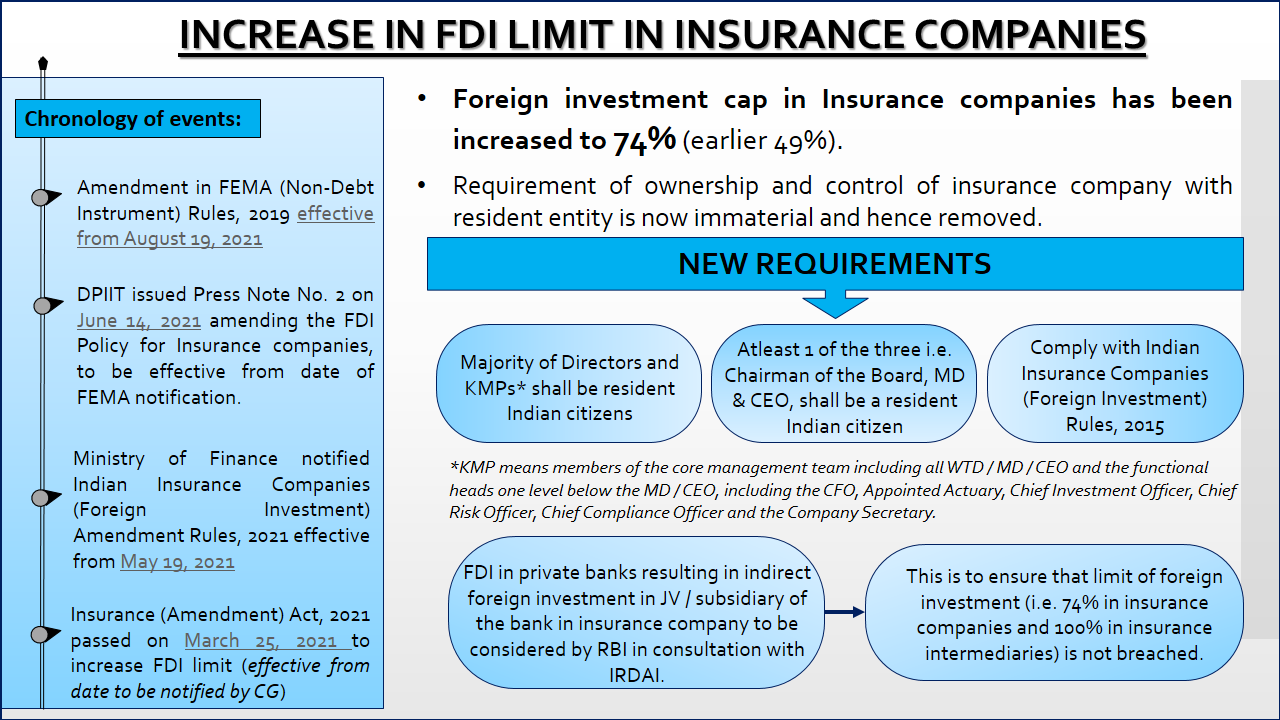

Amendment in Foreign Exchange Management (NDI) Rules, 2019 effective August 19, 2021- https://egazette.nic.in/WriteReadData/2021/229165.pdf

DPIIT Press Note on June 14, 2021 amending the FDI Policy for Insurance companies which shall be effective from date of FEMA notification – https://dpiit.gov.in/sites/default/files/pn2-2021.pdf

Consequential amendment in Indian Insurance Companies (Foreign Investment) Rules, 2015 are on May 19, 2021 – https://financialservices.gov.in/sites/default/files/Indian%20Insurance%20Companies%20(Foreign%20Investment%20)(amendment)%20Rules,%202021.pdf

Insurance (Amendment) Act, 2021 is passed on March 25, 2021 to increase FDI limit – https://financialservices.gov.in/sites/default/files/Insurance%20(Amendment)%20Act%202021%2025_3_2021.pdf

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –

– Ajay Kumar KV, Manager & Himanshu Dubey, Executive

From a little-known word and a preserve of a select few finance professionals, the term Special Purpose Acquisition Companies (SPACs) is today a buzzword. The regulators across the globe are taking necessary actions to enable SPACs to raise money from investors – jurisdictions like the US, UK and Malaysia lead from the front. Having a sound regulatory framework is important because if investors are keen towards SPACs, and the regulators do not enable it, it is quite likely that the country will not be a friendly destination for SPACs. Hence, India’s securities regulator SEBI has recently constituted an Expert Group for examining the feasibility of SPACs in India, and the International Financial Services Center Authority (IFSCA) has issued IFSCA (Issuance and Listing of Securities) Regulations, 2021[1] which provides a regulatory framework for listing of SPACs within its jurisdiction.

In this write up, the authors take a look at the global legislative measures, and also outline the various changes in the regulations that may be needed in India to enable to make India a SPAC-friendly jurisdiction.

Contents

Important regulatory concerns. 3

Regulatory framework in India. 6

Exploring some scenarios and the concomitant regulatory ramifications. 13

Proposes segregation of regulatory and the operational part in rules and regulations respectively

FCS Vinita Nair |Senior Partner, Vinod Kothari & Company

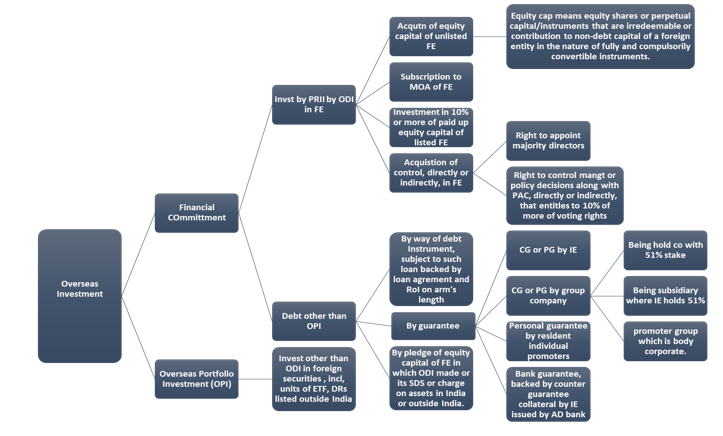

Investments by Indian entities outside India is a very common phenomenon and several companies have presence outside India by virtue of forming a Joint Venture (‘JV’) and Wholly Owned Subsidiaries (‘WOS’)

With the enforcement of amendment proposed in Finance Act, 2015 in October, 2019[1] powers vested with Central Government (CG) and Reserve Bank of India (RBI) with respect to permissible Capital Account Transaction were revisited. Power to frame rules relating to Non-Debt instruments (‘NDI’) were vested with CG and to frame regulations relating to debt instruments were vested with RBI. The scope of NDI inter alia covers all investment in equity instruments in incorporated entities: public, private, listed and unlisted; acquisition, sale or dealing directly in immoveable property.

RBI intends to combine erstwhile FEMA (Transfer or Issue of Foreign Security) Regulations, 2004[2] (‘erstwhile ODI regulations’) and FEMA (Acquisition and Transfer of immoveable property outside India) Regulations, 2015[3] into FEMA (Non-debt Instruments – Overseas Investment) Rules, 2021[4] (‘NDI Rules’) and FEMA (Overseas Investment) Regulations, 2021[5] (‘OI Regulations’) and has rolled out the draft regulations for public comments to be sent by August 23, 2021[6].

NDI Rules will provide the regulatory framework for making of overseas investment covering the permissions, conditions for making overseas investment, restrictions from making Overseas Direct Investment (‘ODI’), pricing guidelines, transfer, liquidation and restructuring of ODI. While the NDI Rules will be framed by CG, however, the same will be administered by the RBI.

OI Regulations, on the other hand, will provide only the operational part covering conditions for undertaking Financial Commitment (‘FC’), other than investment in equity capital, consideration in case of acquisition or transfer of equity capital of a Foreign Entity (‘FE’), mode of payment, obligations of Persons Resident in India (‘PRII’), reporting requirements, consequence of delay in reporting and restrictions on further FC/ transfer.

Under the erstwhile ODI regulations, currently in force, there is a concept of direct investment outside India in JV and WOS that excludes portfolio investment and FC. NDI Rules combine the two to define FC and separately defines the term Overseas Portfolio Investment (‘OPI’). Overseas Investment (‘OI’) is FC + OPI.

The classification as ODI depends on the nature of instruments in which investment is made, the nature of the entity in which investment is made and whether control has been acquired or not.

The diagram below provides a snapshot of the same.

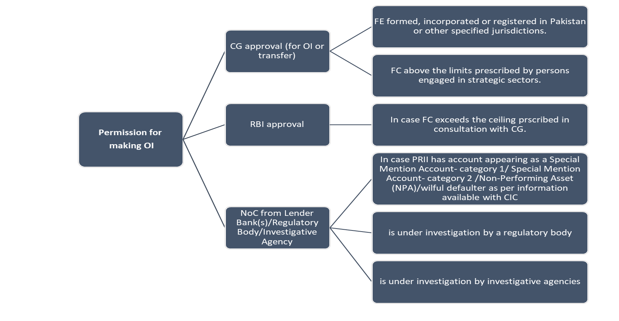

The NDI Rules provides investments that require prior approval of Central Government, RBI and NOC from lender banks/ regulatory body etc. The Erstwhile ODI Regulations only mandated prior approval of RBI in case eligibility conditions stipulated were not met by the Indian party or resident individual.

Our other videos and write-ups may be accessed below:

YouTube:

https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

Other write-up relating to corporate laws:

https://vinodkothari.com/category/corporate-laws/fema/

[1] https://egazette.nic.in/WriteReadData/2019/213265.pdf

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=2126&Mode=0

[3] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10257&Mode=0

[4] https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=4024

[5] https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=4023

[6] https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52026

– Megha Mittal

The concept of Special Purpose Acquisition Companies (‘SPACs’) has gained significant attention and importance in India in recent times – from a subject preserved to select classes, the surge in transactions over 2020, has made it pave its way to every investor’s dictionary. And with all the spotlight that SPACs have attracted, the numbers seem to only lend to the hype. To begin with, the global SPAC IPO proceeds in 2020 alone is estimated to be $83 billion USD[1] with a total of 251 listings. This figure is further projected to grow to a massive 711 listings in 2021 with an average IPO size of USD 294.5 Million as on 15th August, 2021[2].

Globally, SPACs have become the investment vehicle of choice, more-so by startups looking for funding; and the US has been the flag bearer of the SPAC industry, leading from the front. Following shortly behind are economies like UK, Malaysia and Canada; and while India is playing catch-up, it seems to be speeding up quick enough, at least on the regulatory front.

For the uninitiated, a SPAC, often referred to as a Blank-check Company or a Shell Company, is a non-operating company with the admitted intent (read: special purpose) of acquiring of a potential target within a stipulated timeline[3].

In this article, while dealing with the basic regulatory framework via-a-vis SPACs, the author seeks to analyse the motivation(s) behind such transactions from all perspectives – the acquirer’s, the acquiree’s and the investors’.

Non-convertible debentures issued on private placement basis are one of the most practiced ways of raising finance by the companies in India. Considering the notification of SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021, effective from 16th August, 2021, the companies may be under a perplexity of how to comply with the requirements of the newly notified regulations. We have summarised the procedure into a checklist below for reference.

| Checklist for issuance of listed and unsecured NCDs on Private Placement Basis | |||

| Serial No. | Particulars | Relevant provisions | Remarks |

| Eligibility conditions: A. Eligibility requirements under the Companies Act, 2013: 1. Offer can be made to a maximum of 200 persons 2. No advertisement can be made in the newspapers 3. The Company shall not make a fresh offer or invitation unless the allotment with respect to any offer or invitation made earlier have been completed, or withdrawn or abandoned by the Company. B. Eligibility requirements under SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 No issuer shall make an issue of non-convertible securities if as on the date of filing of draft offer document or offer document: (a) the issuer, any of its promoters, promoter group or directors are debarred from accessing the securities market or dealing in securities by the Board; (b) any of the promoters or directors of the issuer is a promoter or director of another company which is debarred from accessing the securities market or dealing in securities by the Board; (c) any of its promoters or directors is a fugitive economic offender; or (d) any fine or penalties levied by the Board /Stock Exchanges is pending to be paid by the issuer at the time of filing the offer document: |

|||

| 1 | Convening of a Board Meeting: i. To consider and approve issue of debentures including the terms and conditions of issue for the entire FY ; ii. To authorise the Board Borrowing Committee/ other relevant committee [Optional] for the following: a. Appointment of RTA and execute tripartite agreement [Reg 9] b. Appointment of Credit Rating Agency and obtain Credit Rating. [Reg 10] c. Opening of Separate Bank Account with Schedule Bank [Proviso to Section 42(6)]. d. To identify group of persons to whom Debentures are proposed to be issued [Section 42(2)] e. To approve Private Placement offer letter f.Appointment of Depository [Reg 7] g. For allotment of NCDs h. other matters relevant to the issue of NCDs i.To appoint a debenture trustee before the issue of letter of offer for subscription of the debentures [Reg 8] j. To obtain in-principle approval from stock exchanges [Reg 6] |

Section 179(3) of CA Section 42, 71 & SS-1 |

|

| 2 | Approval of shareholders | Sec. 71, 42, Rule 14(1) of Companies (PAS) Rules,2014, Rule 18 of SHA Rules | not required if blanket approval already taken and issue is within the limit as per second proviso to Rule 2 of Companies (Prospectus and Allotment of Securities) Rules, 2016 |

| 3 | Filing of MGT-14 | Rule 14(1) of Companies (PAS) Rules, 2014 | Within 30 days of passing of the Board Resolution/ Shareholders resolution |

| 4 | a. Preparation and finalisation of Disclosure Document; b. Preparation and finalisation of DTD, DTA/ Debenture Subscription Agreement. |

||

| 5 | Obtain consent from Trustee | Before issue of offer document | |

| 6 | To convene Board Borrowing Committee/ other relevant committee meeting for the following: a. Approval of draft offer document/ Disclosure Document/ Information Memorandum, Debenture Trust Deed, Debenture Trustee Agreement,Application Form b. Identification of RTA c. Approval of List of proposed Allotees d. Approval for opening of Escrow Account (if already opened then noting of the same) e. All other matter as delgated by the Board as mentioned in Point 1 above. |

Section 42(3) of CA with Rule 14 (3) of Companies (Prospectus and allotment of Securities) Rules, 2014 | In terms of Rule 18(1)(c) & (5) of the Companies (Share Capital and Debentures) Rules, 2014 [Section 71(5)], the debenture trustee shall be appointed and DTD shal be executed at any time within 60 days of allotment of debentures. Accordingly, this may be done after the allotment of NCDs also. |

| 7 | Creation of debenture redemption reserve | Section 71(4) read with Rule 18 (7)(b)(iv)(B) | The value of debenture redemption reserve shall be 10% of the value of outstanding debentures.

DRR shall not be required in case of NBFCs [Rule 18 (7) (iv)(A) of Deposit Rules |

| 8 | Creation of recovery expense fund | Reg 11 read with SEBI Circular https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/oct-2020/1603361431987.pdf#page=1&zoom=page-width,-16,792 | deposit an amount equal to 0.01% of the issue size with designated stock exchange upto a maximum of Rs. 25 lakhs. |

| 9 | Obtain credit rating | Reg 10 | |

| 10 | Agreement with depository for dematerialisation | Reg 7 | |

| 11 | Private placement offer-cum-application shall be sent to the identified investors | Sec. 42 of CA 13 | |

| 12 | Maintain a complete record of persons to whom the Private Placement offer letter is sent in form PAS-5. | Rule 14(4) of PAS Rules | |

| 13 | Receipt of application money | Section 42 of CA | |

| 14 | Filing of Master Creation form with NSDL/CDSL -for demat issuance | ||

| 15 | Filing of listing application with stock exchanges and debenture trustees – (a) Placement Memorandum; (b) Memorandum of Association and Articles of Association; (c) Copy of the requisite board/ committee resolutions authorizing the borrowing and list of authorised signatories for the allotment of securities; (d) Copy of last three years Annual Reports; (e) Statement containing particulars of, dates of, and parties to all material contracts and agreements; (f) An undertaking from the issuer stating that the necessary documents for creation of the charge, wherever applicable, including the Trust Deed has been executed within the time frame prescribed in the relevant regulations/Act/rules etc. and the same would be uploaded on the website of the designated stock exchange, where such securities have been proposed to be listed; (g) In case of debt securities, an undertaking that permission / consent from the prior creditor for a second or pari passu charge being created, wherever applicable, in favour of the debenture trustee to the proposed issue has been obtained; and (h) Any other particulars or documents that the recognized stock exchange may call for as it deems fit: |

Reg 44 | |

| 16 | Allotment of NCDs after holding a meeting of Borrowing Committee/ other relevant committee | Section 42 of CA | |

| 17 | Filing of PAS-3 with ROC | Section 42(8) read with Rule 14(6) of Companies Prospectus and allotment of securities) Rules, 2014 | |

| 18 | Payment of fees to stock exchanges | Reg 13(2) | at the time of listing |

This is a general checklist for companies desiring to list its debt securities. For NBFCs and HFCs, the requirements may differ depending upon their specifically applicable regulations.

Further, you may read our article on the NCS Regulations here.

A comparison of the NCS Regulations from erstwhile ILDS Regulations can be accessed here.

A presentation on the various structures of debt securities can be viewed here – https://vinodkothari.com/2021/09/structuring-of-debt-instruments/