SEBI measure may ease out issuance of debt securities

Introduction –

By a 9th August, 2021 Notification, SEBI has consolidated the regulatory framework pertaining to issue of non-convertible debentures (‘NCDs’), non-convertible preference shares (‘NCPS’), perpetual debt securities (‘PDIs’), and listed commercial paper. Along with the consolidation exercise, SEBI has also tried to iron out some of the difficulties being faced in respect of debt issuance by companies. Accordingly, the new SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (‘NCS Regulations’), notified on 9th August, 2021, have the effect of merging (and consequently, repealing) the SEBI (Issue & Listing of Debt Securities) Regulations, 2008 (‘ILDS Regulations’) and SEBI (Issue & Listing of Non-Convertible Redeemable Preference Shares) Regulations, 2013 (‘NCRPS Regulations’)

The NCS regulations have been introduced in line with the Draft Consultation Paper[1] (‘Consultation Paper’) issued by SEBI on the subject on 19th May, 2021.

In this article, we discuss and highlight the important changes incorporated in the NCS Regulations as compared to the ILDS Regulations and NCRPS Regulations.

Effective date and prospective applicability

The regulations shall be effective on the 7th day from the date of their publication in the Official Gazette i.e. 16th August, 2021.

As to whether NCS Regulations are applicable on issuances done before the effective date, it is evident from a reading of regulation 4(2) that NCS Regulations are to be satisfied by the issuer as on the date of filing draft offer document/offer document with SEBI, stock exchanges and RoC. This indicates that securities which are already floating in the market pursuant to issuances done before 16th August, 2021, NCS Regulations should not make a difference. Hence, the new regulations shall be applicable only to new issuances or new listing applications made on or after August 16, 2021.

The view is further substantiated by the fact that –

- There is no grandfathering clause in the NCS Regulations, and

- The provisions pertaining to ‘repeal and savings’ provide for continuation of “right, privilege, obligation or liability acquired, accrued or incurred under the repealed regulations” as if the repealed regulations have never been repealed – see discussion later.

Rationale behind the fused regulations–

Debentures, specifically non-convertible debentures, are purely debt instruments. However, NCRPS are hybrid instruments combining characteristics of both debt and equity thereby being ‘quasi-debt instruments’. Due to this reason, the NCRPS regulations were mostly modelled based on the ILDS regulations providing similar provisions on eligibility conditions, disclosure requirements, etc. Therefore, merging the two regulations would only be reasonable. The move to merge both these regulations may not be a complete solution to the regulatory chaos, but is definitely in the direction to combat multiplicity of laws. Further, the NCS Regulations also aim to –

- Harmonise provisions of the Companies Act, Rules made thereunder and SEBI Regulations

- Align various circulars, guidelines issued by SEBI

- Identify policy changes in line with the present market practices for ease of doing business

- Merge all the existing circulars into a single operational circular

Repeal of existing regulations –

The NCS regulations shall repeal the existing ILDS Regulations and NCRPS Regulations from the effective date. Reference to any provision under these regulations shall be deemed to make reference to corresponding provisions in the NCS regulations.

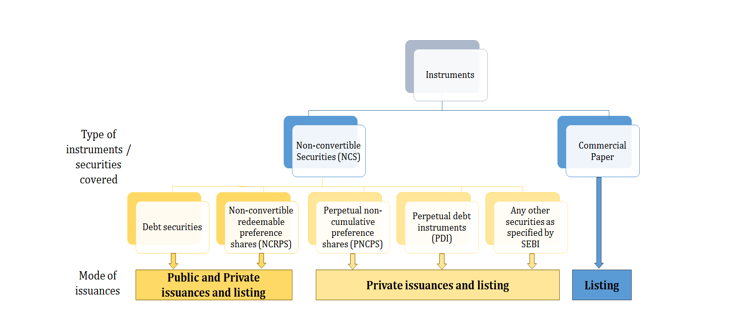

Applicability of the NCS Regulations-

The following have been covered by the NCS Regulations:

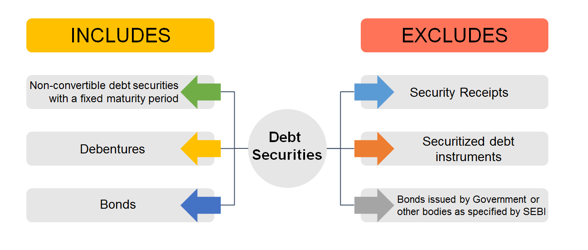

Definition of Debt securities –

Listing of Commercial Paper

Another important point to note is that the NCS Regulations only deal with listing of CP and issuance thereof shall not be covered. The NCS Regulations have adopted the earlier SEBI Circular on Listing of CPs with respect to provisions on the said subject. The caveats relating to eligibility, mode of issuance, etc. shall still be governed by the provisions of RBI read with FIMMDA operational guidelines.

Only additional caveats arising from the NCS regulation for the issuer is that they shall be required to register on SCORES Platform. In case the entity has its NCDs or NCRPs listed they are already required to register on SCORES Platform in terms of SEBI (Listing Obligation and Disclosure Requirements) Regulations, 201 (‘LODR Regulations’).

Issuers covered under the NCS regulations

Point at which conditions are to be satisfied

There are several conditions in the NCS Regulations which the issuer needs to fulfil as on the date of filing draft offer documents/offer documents – see, regulation 4(2). For instance, as on the date of filing of draft offer document or offer document, neither the issuer its promoters, promoter group or directors should be debarred from accessing the securities market or dealing in securities by SEBI, none of the promoters or whole-time directors of the issuer shall be promoter or whole-time director of another company which is a wilful defaulter. Therefore, if this condition is, say, breached after the securities are listed, the issuer shall not be seen as in breach of the regulations.

While most of the requirements have been retained from the erstwhile regulations, the NCS regulations also additionally prohibit any issuer from making an issue if as on the date of filing of the draft offer letter, if any of its promoters or whole-time directors are a promoter or whole-time director of another company which is a wilful defaulter.

Whether LLPs can issue debentures?

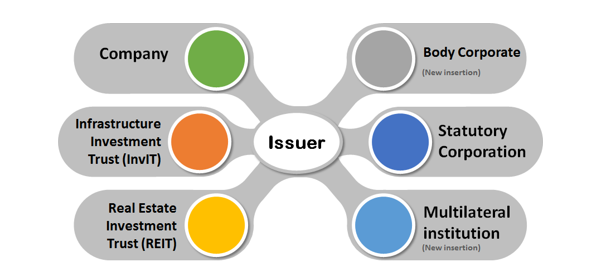

Key highlight of the definition of “issuer” under the NCS Regulations is inclusion of the term “body corporate”. The erstwhile definition of “issuer” under the ILDS Regulations did not include body corporates. Several rulings have established that an LLP is, in fact, a body corporate. Accordingly, this exclusion raised a question on the permissibility of listed debt issuances by an LLP. It was always, therefore, deemed that LLPs could only issue unlisted debt securities while listed debt securities by LLPs was not permitted by the ILDS Regulations. The said inclusion of “body corporate” in the definition of “issuer” will, therefore, enable LLPs to issue listed debt securities as well as NCRPS, thereby making way for further raising of funds.

However, the same shall be subject to any conditions in the LLP Act, 2008. The Company Law Committee Report[2] for decriminalization of LLP Act also discussed on raising of funds through issuance of secured non-convertible debentures to bodies corporate or trusts regulated by SEBI or RBI with certain fetters and suggested inclusion of new section in the LLP Act, 2008 for the same.

Highlights

1) Appointment of Debenture Trustee for all issues of debt security

The ILDS Regulations provided for appointment of a Debenture Trustee (’DT’) for public issuance of debt securities. While there was no explicit requirement for the appointment of debenture trustee for private placement of debt securities in the ILDS Regulations, in terms of Companies Act, 2013 (‘CA, 2013’) and SEBI Circular dated November 03, 2020, security was required to be created in the favour of a DT. Accordingly, there was no clarity as to the appointment of debenture trustee in case of issuance of unsecured NCDs through private placement. The NCS regulations now provide for mandatory appointment of DTs in case of all issuances of debt securities (Regulation 8 of the NCS Regulations).

Our Comments –

The same is a welcome change as it provides the required clarity on appointment of DTs. Considering the increasing relevance and importance of DTs in case of debt issuances, appointment of DTs in case of all debt securities becomes all the more important.

2) Widened applicability of EBP platform

The EBP platform is presently applicable to private placements of debentures amounting to Rs. 200 crores and above in a financial year. SEBI, in its Consultation Paper, proposed to reduce such limit to Rs.100 crores or above and making EBP mandatory for issues breaching the said limit. The same was proposed considering the benefits of the EBP platform and need for further increased participation from issuers and investors.

The said change did not reflect either in the draft or the final regulations. The revision in the limits may be made in the EBP Circular by SEBI.

Our Comments –

The concept of the EBP was introduced by SEBI with a view to make participation in the privately-placed bond market more inclusive. Electronic bidding platforms are there in several other markets – however, in most cases, these are private bidding engines, and are optional.

The private placement market in India is completely bespoke in nature, and issuances are almost completely OTC negotiations. In order to remove the veil of opacity, and allow a larger base of investors to participate, the EBP mechanism was introduced.

However, various market participants are averse to the EBP platform. Lengthy procedures delay the process for issuers which may not be suitable for a sensitive debt market. Different EBP platforms have different procedures thereby causing confusion. Most issuers still continue to negotiate on OTC basis and place the offer on EBP or make use of regulatory arbitrage methods such as market-linked debentures (‘MLDs’).

Therefore, increasing the scope of applicability of EBP may not be conducive to the Indian bond market. SEBI may consider making the EBP optional rather than mandatory. Where the issuer desires a wider audience for its proposed issue, the issuer may put the offer on the bidding platform. However, where an OTC deal is done, the issuer should be allowed to go ahead with the private placement straightaway. A potential investor wanting to invest therein will still have the chance to participate in the secondary market.

3) Private Placement Requirements

The NCS Regulations [regulation 44(2)] clarify the ambiguity regarding issuance of debt securities on private placement basis by a company in existence for less than three years. The requirement to provide annual reports for previous three years while making an application for listing presumed the requirement for a company to be in existence for at least three years to list its privately placed debentures. However, the proviso to regulation 44(2) resolves the above by specifying that ‘provided that issuers desirous of issuing debt securities on private placement basis who are in existence for less than three years may provide Annual Reports pertaining to the years of existence.

4) Exercise of Call or Put Option (Right to recall or redeem prior to maturity date)

The erstwhile provisions for issuance of non-convertible debt securities, provided framework for right to recall (i.e. Call Option) and right of redemption (i.e. Put Option) prior to maturity, in case of public issue of NCDs. In case of private placement of NCDs, the same was entirely guided by the terms of issue.

However, the NCS regulations have now stipulated that provisions relating to call and put option shall equally apply in case of public issuances as well as private placement.

This seems to take away the flexibility that issuers enjoyed in certain cases for issuers of privately placed debentures for example, where an interest rate in case of delay on part of the issuer could be avoided or kept at a minimal rate, the same will be charged at 15% interest rate.

It may be noted here that there is an apparent change in the language – while regulation 15 of NCS Regulations uses “shall”, regulation 17A of ILDS Regulations used “may”. However, this change in language does not change the law – it is still a ‘right’ in the hands of the issuer to “recall” the securities using a “call option” or “provide a right” to investors to “redeem” the securities using a “put option”. As it is a matter of right to the issuer, the right can still be exercised (or not exercised) by suitably providing for the same in the terms of issue.

Also, regulation 15 itself specifies that the issuer shall have a right to provide such right of redemption of debt securities prior to the maturity date (put option) to all the investors or only to retail investors.

The NCS Regulations do not state the time period for payment of interest, which was specified as 15 days from the day from which such right could be exercised under the erstwhile provisions.

Our Comments –

Since the Call and Put Option are exercised in accordance with the terms of issue and detailed disclosure made in this regard in the offer document, the issuers of privately placed debt securities issued prior to the NCS Regulations can provide these options after the expiry of one year from date of issue and only if it was disclosed in the offer document.

Further, it must be noted that the ‘call option’ feature would be relevant for debt securities as well as NCPS; however, ‘put’ option feature will only be relevant for debt securities. This is because a ‘put option’ enables the investor to exercise a ‘right’ to sell the securities to the issuer. Redemption of preference shares can either be done out of profits of the company or out of fresh issue of shares, as per Section 55 (2) (a) of Companies Act. In case the put option is exercised, the company will be under obligation to redeem and this may result in violation of section 55 in case the issuer is not able to redeem in the prescribed manner. Hence, while clause (a) of regulation 15(1) applies to all non-convertible securities (debt + NCPS), clause (b) applies only to debt securities.

5) Exemption from restriction of use of proceeds

Issuers of non-convertible securities are prohibited from using proceeds from issuances of such securities for providing loans to or acquisition of shares of entities under their promoter group or group companies. The erstwhile laws failed to distinguish between a financial entity and non-financial entity as regards to the nature of business. Therefore, the said restriction was applicable in case of all listed entities alike.

The NCS regulations provide the much needed relaxation from the said clenching restriction in case of a Non-Banking Finance Company (‘NBFC’), Housing Finance Company (‘HFC’) and a Public Financial Institution.

Our Comments –

The intent behind the restriction was to discourage using public money for funding group entities. However, providing loans or acquiring securities aren’t peculiar transactions in case of NBFCs and HFCs since they are ordinarily in such business.

6) Validity of shelf prospectus:

In case of Public Issue of debt securities:

The ILDS Regulations provide that not more than four issuances can be made under a single shelf prospectus while there is no such restriction under the Companies Act. To enable issuers to raise funds quickly without filing a separate prospectus each time, this restriction has been removed from NCS Regulations.

In case of private placement of debt securities:

The time validity of shelf prospectus in case of private placement of debt securities has been increased from 180 days to 1 year.

Our Comments –

This is a welcome move, as this will eliminate hassles for frequent issuers to file shelf prospectus multiple times.

7) Criteria of eligible issuer

Under the NCS Regulations, the condition that the issuer shall not be debarred from accessing the securities market or dealing in securities has been extended to promoter group entity as well. Further, certain additional conditions such as the promoter or WTD shall not be a promoter or WTD of a company which is a wilful defaulter, no promoters or directors shall be fugitive economic offenders or no fines or penalties are pending at the time of filing of offer document have been inserted.

Our Comments –

Associating payment of fines and penalties with listing might not be a feasible idea; as there might be situations where the issuer may have raised disputes/concerns on liability to pay such fines/penalties.

8) Additional Disclosures for NBFCs

In case the issuer is an NBFC/HFC additional disclosures on asset liability management are required to be provided pertaining to the latest audited financials. The same was not required under the ILDS Regulations. The disclosures also include details of contingent liabilities specifying the nature and amount of such liabilities.

9) Companies existing for less than 3 years – Annual report submission provision

As per the NCS Regulations in case an issuer who has been in existence for less than 3 years is desirous of issuing debt securities, annual reports pertaining to years of existence have been permitted to be provided.

10) Creation of Recovery Expense Fund – Whether applicable in case of NCPS?

Under the NCPs regulations requirement of maintenance is included under the general conditions applicable in case of public issuance of debt securities and NCPs and private placement of NCS. However, due regard must be given to SEBI circular dated October 22, 2020[3] which provides the manner and mode for creation and maintenance of recovery expense fund, specifically restricts the requirement only in case of issue of debt securities. Moreover, it may be noted that preference shares can be redeemed only out of profits and out of proceeds of new issuances (as provided for under section 55) and are thus, inherently different from debt securities. Hence, this requirement of recovery expense fund should not apply in case of NCPS.

11) Minimum subscription in case of public issue of Debt Securities

The ILDS Regulations gave the option to the issuer to identify the minimum subscription, however the NCS Regulations has straight away set a bar of 75% of the base issue size. This might take away the flexibility from the issuers.

The requirement of minimum subscription is however not applicable in the case of issuance of tax free bonds as specified by the Central Board of Direct Taxes.

12) Creation of Security

As per the ILDS Regulations, in case of secured debentures, the assets offered as collateral are required to be unencumbered provided that if the same are already charged to secure a debt, relevant permission to create a pari passu or a second charge will be taken from the existing chargeholders. This requirement was applicable to the total security cover in case of a debt issuance i.e. even in case of over-collaterisation.

However, the NCS regulations have eased out the said stipulation providing that the same shall apply on assets to the extent of 100% security cover. Thus, assets over and above the 100% security cover may be encumbered and the same may be provided as security without obtaining relevant permissions from the existing chargeholders.

For instance, if an issue of debentures is secured to the extent of 125% of the issue size – earlier the assets securing the entire 125% charge were required to be unencumbered, now only assets constituting 100% charge of the issue will be required to be unencumbered.

13) Due Diligence

The requirement of undertaking due diligence in case of public issue of NCDs was already there in the ILDS Regulations Additionally, SEBI vide its circular dated November 03, 2020, also required DTs to undertake due diligence w.r.t creation of security, irrespective of the debentures being issued publicly or on a private placement basis. The NCS Regulations now provide for due diligence in case of private placement as well, before filing of the offer document.

Overall, it seems that the Regulations are on a positive note. The discussion above is a quick compilation of the important points which come out of the NCS Regulations. We shall be continuously updating the list above on the basis of further observations.

You may also refer to our following articles on related subjects-

- Presentation on Corporate Bonds and Debentures

https://vinodkothari.com/2021/03/presentation-corporate-bonds-debentures/

- SEBI’s stringent norms for secured debentures

https://vinodkothari.com/2020/11/sebis-stringent-norms-for-secured-debentures/

- Market-Linked Debentures – Real or Illusory?

https://vinodkothari.com/2021/01/market-linked-debentures-real-or-illusory/

https://vinodkothari.com/2019/11/faqs-on-commercial-paper/

Our our Book on Law and Practice Relating to Corporate Bonds and Debentures, authored by Ms. Vinita Nair Dedhia, Senior Partner and Mr. Abhirup Ghosh, Partner can be ordered though the below link:

https://www.taxmann.com/bookstore/product/6330-law-and-practice-relating-to-debentures-and-corporate-bonds

Our presentation on the structuring of debt securities can be viewed here – https://vinodkothari.com/2021/09/structuring-of-debt-instruments/

[1] https://www.sebi.gov.in/reports-and-statistics/reports/may-2021/consultation-paper-review-and-merger-of-sebi-issue-and-listing-of-debt-securities-regulations-2008-and-sebi-issue-and-listing-of-non-convertible-redeemable-preference-shares-regulations-2013-i-_50192.html

[2] https://www.mca.gov.in/Ministry/pdf/Report%20of%20the%20Company%20Law%20Committee%20on%20Decriminalization%20of%20The%20Limited%20Liability%20Partnership%20Act,%202008.pdf

[3] https://www.sebi.gov.in/legal/circulars/oct-2020/contribution-by-issuers-of-listed-or-proposed-to-be-listed-debt-securities-towards-creation-of-recovery-expense-fund-_47939.html