https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-03-21 23:19:472024-03-22 11:42:41Fractional property shares: Come either as Small REIT, or wind up

Navigating the world of fundraising for startups is no easy feat. This becomes all the more challenging for a pre-revenue start-up which cannot have a valuation. Amongst the several fundraising options available to a start-up, one of the budding and lesser-known sources happens to be iSAFE.

Origin

iSAFE, short for, India Simple Agreement for Future Equity, was first introduced in India by 100X.VC, an early-stage investment firm. This move was inspired by US’s ‘Simple Agreement for Future Equity (‘SAFE’)’, an alternative to convertible debt and the brainchild of an American start-up incubator. SAFE is a financing contract between a startup and an investor that grants the investor the right to acquire equity in the firm subject to specific activating events, such as a future equity fundraising.[1]

So far as the success of SAFE in India is concerned, being neither debt (since they do not accrue interest), nor equity (since they do not carry any dividend or shareholders’ rights) or any other instrument, it could not carve its place in India and was cornered as a mere contingent contract with low reliability and security. On the contrary, iSAFE happened to be the game changer in the Indian context, being a significantly modified version of SAFE.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00mahakagarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngmahakagarwal2024-03-21 11:10:152025-05-06 14:55:43The iSAFE option to start up funding: Legality and taxation

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-03-17 22:55:342024-03-17 23:17:18SEBI approves uniform approach for market rumour verification, eases on-going compliance requirement for listed companies, eases norms for IPO/ fund raising, AIFs, relaxes requirement for FPI & extends timeline for HVDLE on March 15, 2024

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-03-15 11:54:232024-05-02 19:09:40Mandatory bond issuance by Large Corporates: FAQs on revised framework

In a recent Supreme Court ruling in the matter of Association for Democratic Reforms & Anr. v/s Union of India, Electoral Bond Scheme (EBS/ Scheme) was declared as unconstitutional, including certain amendments to section 182 of the Companies Act, 2013 (“CA”), amended vide the Finance Act, 2017 as arbitrary and violative of the Constitution of India (COI).

Naturally, a question arises: What is wrong? Contributions to political parties? No. It is only the opacity of the recipient which has been hit. Hence, if companies have contributed, they couldn’t have kept a shroud of secrecy over the same.

Two, if companies had to disclose, and the amendments on 2017 are now junked, does it mean companies have to go back and disclose? It doesn’t seem so. In fact, the apex court itself has taken care of the actionables and put the burden of disclosure on the Election Commission of India (ECI).

Corporate houses, apparently, the largest contributors to electoral bonds, have expressed concerns on what will be the implications of the ruling on donor companies. Several questions arise – What has been declared unconstitutional and what is still valid? What would be the fate of the political donations already made? What actionables arise on a company having made donations to political parties through electoral bonds or otherwise? In this write-up, the author has attempted to analyze the same in light of the 232-pager ruling.

Section 182 of CA – Pre and Post Finance Act 2017

In order to understand what has been rendered unconstitutional and why, let us analyse the provisions of section 182 of CA as it stood prior to the amendment pursuant to Finance Act 2017 v/s how it stands today.

Particulars

Position prior to Finance Act, 2017

Position post Finance Act, 2017

Whether unconstitutional as per SC ruling?

Limits on political contribution – Proviso to Sec 182(1)

Aggregate value of contribution to political parties cannot exceed 7.5% of 3-years’ average net profits

No maximum limit on political contributions

Yes. The SC concluded removal of limits to be “manifest arbitrariness” for removing a classification without recognising the harms thereof.

Disclosure in financial statements – Section 182(3)

Contributor company to disclose names of each parties against the total amount contributed to such parties

Only total amount contributed to be disclosed, without disclosing names

Yes. The SC concluded this to be an “essential” information for effective exercise of voting, and hence, non-disclosure as an infringement to the right of information of voter under Article 19(1)(a) of COI

Mode of contribution – Section 182(3A)

New insertion pursuant to Finance Act

Political contributions to be made only through banking channels (account paying cheque/ bank draft/ ECS) and through instruments issued under a scheme for political contributions (electoral bonds)

No impact. However, the Electoral Bond Scheme has been declared to be unconstitutional.

Consequences for donor companies

The SC ruling does not declare “political donations” per se as unconstitutional or invalid, what is rendered violative of constitutional rights is the Electoral Bond Scheme and the amendments to section 182 of CA vide Finance Act, 2017 permitting unlimited and anonymous contributions to political parties.

The legal implications of declaring a statute unconstitutional has been discussed in various rulings in the past, such as, reBehram Khurshid Pesikaka v. State of Bombay, and others. These say the consequences are dealt with by the court only. In the present matter of Electoral Bond Scheme, the SC has directed SBI and the Election Commission of India to disclose the details of contributions received through electoral bonds, and refund the non-encashed amounts to the donor.

In essence it does not seem apt that any burden will be cast upon companies for going by a law which was valid till it was scrapped. Hence, no adverse implications should follow for the donor companies. However, for the sake of its corporate duty, a company which has contributed in the past may now do a disclosure in the forthcoming annual report. Thus, The omission of disclosure of particulars of political donations made along with names of the parties, between FY 2017-18 to FY 2022-23, may be made good by companies in the financial statement for the FY 2023-24 giving details of contribution made along with names of the political parties for each of the previous financial years, along with the current FY 23-24.

Principle of “manifest arbitrariness”

Having reference to various rulings and judicial precedents, the SC has summarized that the doctrine of “manifest arbitrariness” can be imposed to strike down a provision. Such a proposition can be applied where:

the legislature fails to make a classification by recognizing the degrees of harm, and

the purpose is not in consonance with constitutional values.

In the context of permitting unlimited contribution to political parties, on the grounds of removing classification between donations by “individuals” v/s “companies”, or between “loss making companies” and “profit making companies”, the degree of potential harm has been ignored. Section 182 was enacted to curb corruption in electoral financing, however, the amendment allowed companies, incorporated for a specific purpose as per their MoA, to contribute unlimited amounts to political parties without any accountability and scrutiny. This may also facilitate incorporation of “shell companies” solely for the purpose of making such political contributions and permit undue influence of companies in the electoral process, thus violating the principle of free and fair elections and political equality.

The hon’ble SC has ruled the deletion of maximum limit as “violative” of COI and “manifestly arbitrary” for not recognising the degrees of harm in removing the classification between –

Political donations by “companies” and “individuals” where the ability to influence electoral process is much higher with the former, since “Contributions made by individuals have a degree of support or affiliation to a political association. However, contributions made by companies are purely business transactions, made with the intent of securing benefits in return.”

“Profit-making” and “loss-making companies” for the purposes of political contributions, since “it is more plausible that loss-making companies will contribute to political parties with a quid pro quo and not for the purpose of income tax benefits.”

The present SC ruling quashes the anonymous political donations and the amendments in CA permitting unlimited corporate donations to political parties. Political donations are not unconstitutional, however a company, making such donations, shall ensure the same does not result into emptying the resources of the company while also ensuring transparency in disclosure of such political donations in its financial statements for the right of information of the concerned shareholders as well as larger stakeholder and voter base.

Streamlining internal compliance monitoring function

The recent RBI directive on streamlining the internal compliance monitoring function by leveraging technology has raised concerns regarding actionable on the part of regulated entities covered thereunder. The notification on Streamlining of Internal Compliance monitoring function – leveraging use of technology dated January 31, 2024 is based on RBI’s review of of the prevailing system in place for internal monitoring of compliance with regulatory instructions and the extent of usage of technological solutions to support this function.

The Micro, Small and Medium Enterprises Development Act, 2006 (‘MSME Act’) has been around for close to 2 decades now, providing for penal interest for delayed payments to MSMEs; yet, it is only of late that there has been buzz around this. Why?

This attributes to clause (h) of Section 43B of the Income Tax Act, 1961 (IT Act, 1961), inserted by the Finance Act, 2023, effective FY 23-24. That is to say, its impact will be faced for outstanding payments as on 31st March, 2024. Now, with the year end fast approaching, there’s a sense of confusion amongst taxpayers who buy goods or services from MSMEs.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00mahakagarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngmahakagarwal2024-02-08 16:27:542024-02-27 11:41:30The big buzz on small business payment delays

The Ministry of Finance, Government of India, through its Department of Revenue, has issued a draft Indian Stamp Bill, 2023[1] on 17th January, 2024 inviting public comments and suggestions within 30 days, with an intent to align it with the modern stamp duty regime. Once enacted, the Bill seeks to replace the Indian Stamp Act, 1899[2].

The Indian Stamp Act, 1899 is a fiscal legislation enacted for the purpose of generating revenue to the Government. Being enacted during the British era, the Act has undergone several amendments from time to time, however, most of the provisions still stand redundant, for instance, proviso under section 8(2) of the Act provides for the treatment of stamp duty on bonds, debentures or other securities issued by the local authority prior to 26th March, 1897, the Act at several places uses denomination of money in ‘anna’ which has no role in the present. Such transitional provisions hold no stand anymore, thus may be removed. Therefore, it has been proposed to modernise the legislation to enable it to deal with the present realities and objectives.

In this article, we have made an attempt to analyse the changes proposed.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00executivehttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngexecutive2024-02-07 17:55:042024-02-07 18:14:46Finance Ministry to modernize the Indian Stamp Act

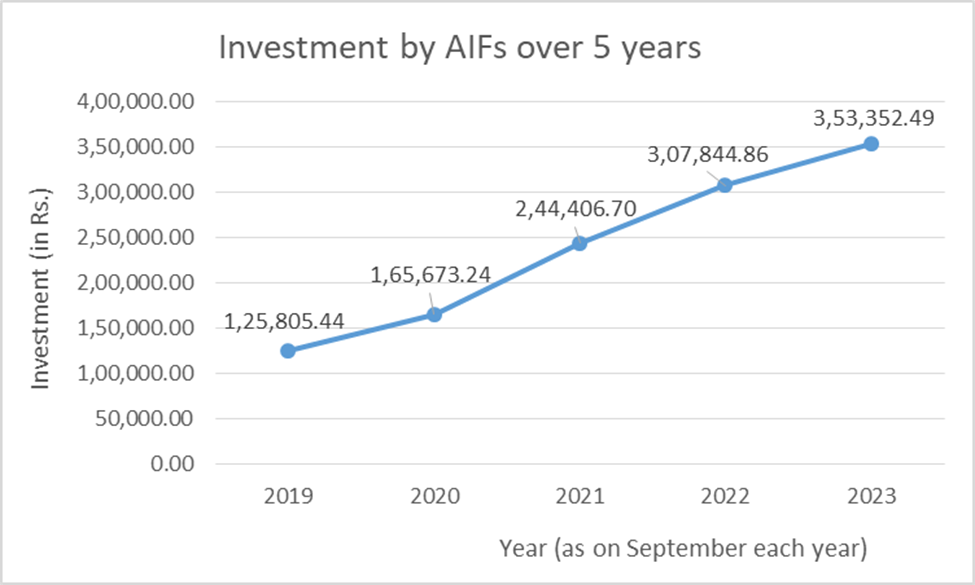

The alternative investment management industry in India works in the form alternative investment funds (AIFs), a SEBI-regulated vehicle. Most of the PE, VC funds, and hedge funds in India work in this mode.

Now, SEBI, vide a Consultation Paper dated 19th January heaped a bunch of similar concerns, and required AIFs to affirm that the AIF or investments therein are not being used for regulatory breaches. These concerns, SEBI says, are a result of an ongoing thematic check on the AIF industry, and SEBI says it has already detected at least 40 cases, involving AUM over Rs 30000 crores, where the structure was used to create dents in existing financial regulations.

The AIF industry has demonstrated steady growth in recent years. As of September 2023, the assets under management (AUM) of AIFs have surged to 3.88 lakh crores, a substantial increase from the 13,000 crores recorded in September 2015. [See Graph above].

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kotharihttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari2024-01-31 16:48:142024-10-22 15:48:31AIFs ail SEBI: Cannot be used for regulatory breach

Loading…

Loading…