https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-05-20 16:54:482024-05-23 15:36:54Online workshop on Verification of Market Rumour by listed entities and other related amendments

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2024-05-18 19:34:542025-01-28 15:25:02SEBI notifies rumour verification requirements, application of market cap based provisions etc

Given the significance of the amendments, we are organizing an online workshop on Verification of Market Rumours by listed entities and other related amendments on Monday, 27th May, 2024. Details of workshop can be accessed here Register here

Regulatory instruments and standards on rumour response:

Reg 30 (11) & (11A) of Listing Regulations dealing with rumour verification. There was a work in progress at SEBI on making the regulation more certain and easier-to-implement. Changes were made in Re. 30 (11) requiring top 100/top 250 companies to mandatorily respond to market rumours, but there were several issues in implementation. SEBI Consultation Paper w.r.t. Verification of Market Rumours (‘CP’) based on the recommendations of the Industry Standards Forum (ISF) and subsequently, SEBI Board decision taken in the meeting held on March 15, 2024 resulted into these changes.

Original implementation dates were October 1, 2023 and thereafter, extended twice to February 1, 2024/ August 1, 2024 and thereafter to June 1, 2024/ December 1, 2024 for top 100/ top 250 companies1. It is now confirmed that the implementation dates remain the same.

Further, SEBI vide Circular dated May 21, 2024 has given recognition to the Industry Standards Forum (‘ISF’)2 that released the Industry Standards Note (ISN) on rumour verification in order to facilitate uniform approach and set out an SOP for compliance with rumour verification requirement. The compliance with Industry Standards are mandatory for the listed entities [SEBI Circular dated 21 May, 2024]. The ISN inter alia covers following aspects:

Delineation of “mainstream media” (as requirement to respond will only be applicable to rumours reported in specific media sources (see below) ;

Guidance on rumour responses through illustrative scenarios pertaining to potential M&A transactions, ;

Guiding principles through some illustrative non M&A transaction scenarios, such as whistleblower complaints, internal investigations, potential change in KMPs, ill health of MD/ CEO etc.

Top 100/top 250 companies based on market capitalisation.

Presently as per March 31, 2024

Effective from December 31, 2024 based on the average market capitalisation from July 1 to December 31 of that calendar year

Top 100 companies – 1st June 2024

Top 250 companies – 1st Dec 2024

For the rest of the companies, the framework is still voluntary, but logically, the reference point being “material price movement” may be extended to these companies too.

What will affected companies be required to do?

If:

There is a material price movement (MPM)

There is a rumour in mainstream media

About some definitive event or information

Which is “impending”, that is, about to happen or waiting to be disclosed by the Company.

The company shall respond:

Either confirm that rumour

Or deny it

Or make a statement that the rumoured event has not become disclosable at the present time

Or remain silent, if the rumour does not qualify for a response in terms of the ISN

And for either confirmation or denial, if the company needs further information from a promoter, director, KMP, or SMP (that is, the rumoured information pertains to them), the company shall promptly seek the same, and the counterparty shall promptly, accurately and adequately respond to the same.

The company shall do the confirmation or denial or provide a clarification within 24 hours from the trigger of the MPM

The company need not respond:

If the rumoured event or information is not “specific”, or does not otherwise qualify for a response

If the rumoured event/information pertains to the pre-intimated items in a notice of Board meeting u/r 29 (1) of Listing Regulations .

Appropriate disclosure to be made after conclusion of the Board meeting.

However, if the rumour goes beyond the information in the pre-intimation, and otherwise qualifies for response, the company will respond.

Basic attributes of a rumour requiring response:

Should be relating to the Company and not generally about sector, industry, geography, etc

Should be specific, that is, should give some facts/information likely to influence the decision of investors, or should have quoted a source which can be relied for the information in question

Should be relating to an event/development which is impending, that is, imminent, at a stage of development

Should not be an elaboration of something that has already been disclosed by the Company, unless new material facts or information not disclosed by the company are contained

Should be contained in “mainstream media”

Should have caused an MPM

There should be a reasonable nexus between the rumour and the MPM, so as to lead to a conclusion that the MPM has been triggered by the rumour

What is the trigger point of the MPM (MPM Trigger)?

Since MPM (see discussion below) is based on price movements during a day, the trigger point may happen at any time during trading hours.

Cut off percentages [that is, 5, 4 or 3%, +/- relevant index variation in the same direction as the MPM – see below] for price variation, or the price band being hit ;

Relevant index changes: Nifty 50 in case of NSE listed entity/ Sensex in case of BSE listed entity/ both in case listed on both, to be seen at the start of the trading day i.e. at 9.30 a.m. That is, change in the index is frozen at the start of the trading day.

ISN intends to classify rumoured news into “positive news” or “negative news”, and correlate the price change with the same (that is, require response only where prices have gone up with a positive news and gone down with a negative news). However, for many news pieces, the ascertainment of whether the news is positive or negative will not be possible. Therefore, the only basis for determination of the direction of the news is the direction of the prices. For instance, disposal of a division may be negative news, if the sustainable income from the same will be lost, but may be taken as positive if the rate of return from the outgoing division was suboptimal.

However, the reflection of the movement in the Index (provided is equal to or more than 1%) needs to be done on the MPM cut off percentages only if the Index movement is in the same direction as the MPM.

As for the stock, the price movements are taken at any time during the trading day..

Percentage variation in share price and the benchmark index movement will be calculated wrt the closing price of the immediately preceding trading day.

Price range of the listed equity shares

Percentage variation in share price which shall be treated as material price

Benchmark index movement (+/-) is less than 1% at 9.30 am

Benchmark index movement (+/-) is greater than 1% at 9.30 am, and MPM is in the same direction as the Index change

In cases not covered by column on LHS

Rs. 0 to 99.99

≥ 5%

≥ 5% + % change in Benchmark index at 9:30 am) or Band hit

≥ 5%

Rs. 100 to 199.99

≥ 4%

≥4% + % change in Benchmark index at 9:30 am) or Band hit

≥ 4%

Rs. 200 and above

≥ 3%

≥3% + % change in Benchmark index at 9:30 am) or Band hit

≥ 3%

Assuming there is an MPM in my scrip at 12.30, which subsides later in the day, shall we still say the MPM has occurred? Answer seems to be yes. In case of intraday price movement (i.e. after 9:30 am), only the price range-based price variation in the scrip to be considered, irrespective of the Index movement.

While there may be price movement due to a combination of various factors such as rumour, announcements or other events (other than the rumoured event), then MPM is deemed attributed \to the rumour.

Where should one look for rumour?

ISN has restricted the scope of “mainstream media” to the following:

English national dailies satisfying the following conditions:

Top English dailies with a circulation of 1 lakh or more copies as per RNI data; currently 14 newspapers along with the editions have been listed by ISN.

Business/ Financial News Dailies: Economic Times, Business Standard, Live Mint, Financial Express and Hindu Business Line.

Regional Dailies: the top 2 (two) regional dailies having the highest circulation, for each of the 22 (twenty two) official languages of India, subject to meeting the RNI Circulation Threshold, as per the list of regional dailies given in ISN.

Digital versions of the newspapers covered above

Digital/ online news sources: specified news sources meeting the following Business News Parameters:

Specified sources are – Bloomberg, BQ Prime, Money Control, Business Today, Business World, Reuters, Reuters India, and Press Trust India.

International media :

Top business/ finance dailies (from top 5 jurisdictions from where foreign portfolio investments are concentrated) comprise –

Wall Street Journal and Financial Times for USA;

Business Times and Financial Times for Singapore; and

Financial Times for UK;

For other jurisdictions where the Company has “material operations” (in our view, the Policy may define what is “material” operation), the Board is required to identify list of English business/ financial news sources from such jurisdictions. List to be published in the materiality policy.

Business News Channels: satisfying the following conditions:

English news channels – CNBC TV-18, ET Now and NDTV Profit

Other Business news channels – CNBC Awaaz, ET Swadesh, Zee Business and CNBC Bazaar

Exclusions: News aggregators (for e.g. google news, inshorts, daily hunt etc.) and social media platforms (for e.g. whatsapp, twitter, facebook, instagram etc.) will not get covered under mainstream media.

Inclusions: Social media handles of news sources identified above, will be included. However, quotes/ re-tweets/ re-posts made from such social media handles will not be included.

What are the actionable for companies w.r.t. Mainstream media?

Companies to put in place appropriate technology solutions, engage external media agencies;

For identifying and tracking the digital news sources set out above.

Implement internal systems for prompt reporting, coordination and communication between investor relations, corporate communications and compliance teams.

Companies are required to respond only once and not when the same or similar rumour is published in another news source.

Question – are companies expected to track all that is written about the company, in all the “mainstream media”, at all times? Answer should be No. However, the company may have to keep sources/media agencies on the standby, that is, to trigger them into action when there is MPM.

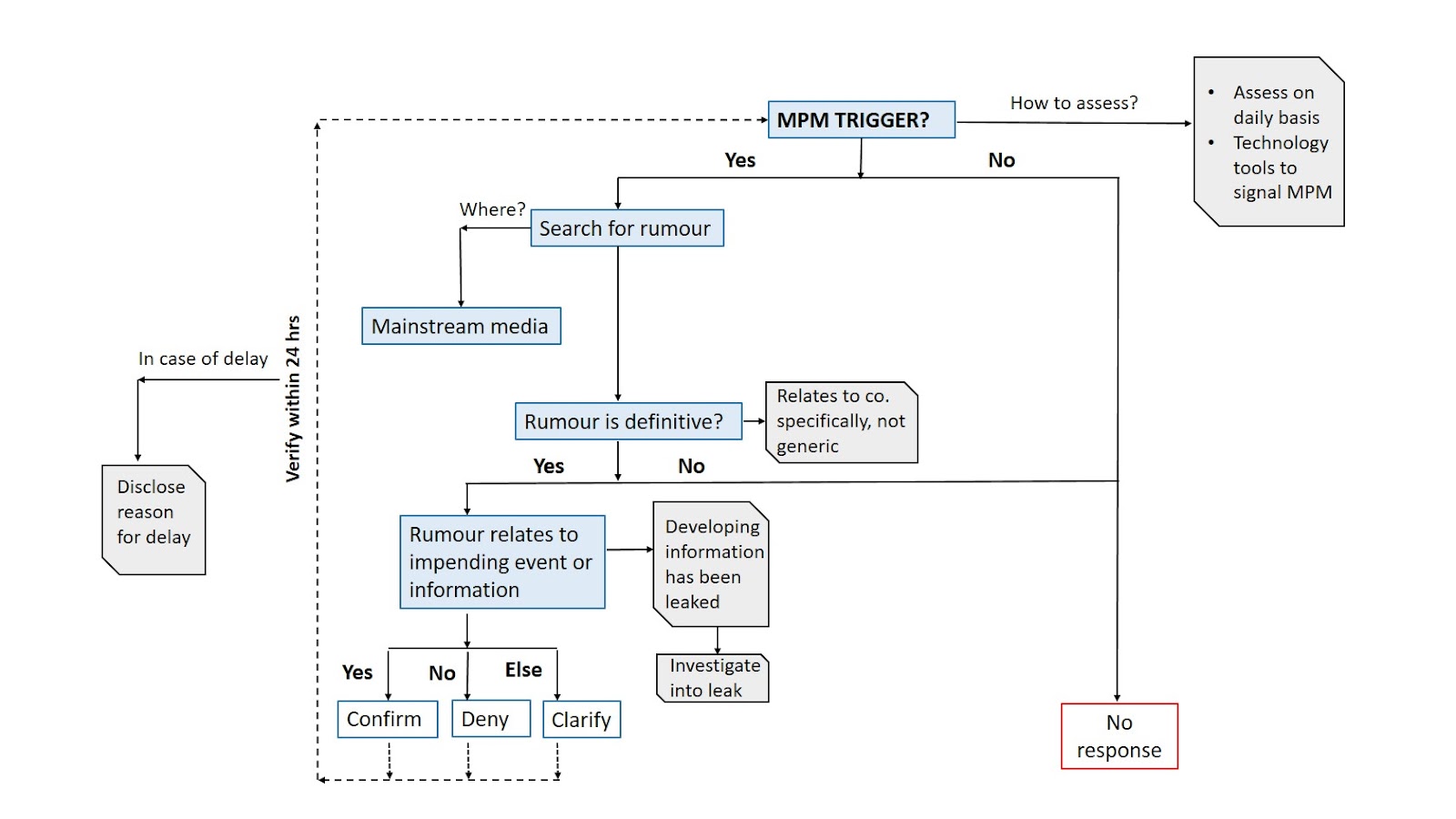

What is the guidance for action?

Companies have to be alert on MPM. MPM is assessed on a daily basis – therefore, companies may have appropriate technology tools to give a signal if there is an MPM.

If there is an MPM, the company will have to search for “rumour” in “mainstream media”.

Here, while companies may be required to keep appropriate technology/ arrangements with external media agencies in place, the same should not be taken to mean that the company is required to track rumour on a daily basis, irrespective of the MPM trigger.

The tracking has to be done for a reasonable period of time backwards. Ideally speaking, the impact of a rumour on price will be reflected within 24-48 hours itself, however, companies may consider keeping a window of 5-10 trading days or any other specific period as part of their internal SOP for the tracking back of rumour in case of an MPM trigger.

What does the rumour relate to? Is it about some “definitive” event or information, or generic in nature (say performance, prospects, etc)? Is it about the company or relates to the company specifically, and not generic (for example, sector, country, economy, etc)? If the answer to these questions are yes, see below.

If the answer is yes, does the rumour relate to an “impending” event or information? That is, there is some event or information within the company which is developing, but the rumour has leaked the same. If yes, confirm it. If no, then deny.

Do all of this within 24 hours of the MPM Trigger.

[Note – Where a prior intimation of Board meeting of the company has been given under Reg 29 of LODR for such “impending” event or information, the company need not respond to the rumour till the conclusion of the Board meeting.]

In the Table below, we take few situations to understand the applicability of verification of market rumour:

MPM

Impending specific event under reg. 30

Rumour in mainstream media

Verification of rumour by company required?

Yes

Yes

Yes

Yes

Yes

No

Yes

Yes, as the existence of MPM by itself satisfies the condition for rumour verification

Yes

Yes

No

No, there is no rumour to be verified. The company may disclose based on the information/event reaching the appropriate stage.

Yes

No

No

There is no rumour to be verified.

No

Yes

Yes

Rumour verification is not required, but the general principles of disclosure of events or information at an appropriate stage will be followed.

What happens if the rumour is confirmed?

Any reported event or information on which below mentioned pricing norms apply, the effect on the price of the equity shares of the listed entity due to MPM and confirmation of the reported event or information to be excluded for calculation of the unaffected price for that transaction.

Chapter V (preferential issue) of the ICDR Regulations (refer amendment including as part of a scheme of arrangement; or

Chapter VI (QIP) of the ICDR Regulations (refer amendment);

Regulation 8 (17) (offer price) or Regulation 9 (6) (listed securities offered as consideration) of the SAST Regulations (refer amendment);

Regulation 19 (price in case of open market buy-back) or Regulation 22B (vi) (computation of lower end of price range in case of buy-back through book building) of the Buy-back regulations (refer amendment).

scheme of arrangement involving a listed company (irrespective of whether the scheme involves a preferential issue or not), undertaken in compliance with the requirements of the SEBI Master Circular on Schemes of Arrangement, dated June 20, 2023; or

any other transaction where the pricing is regulatorily required to be linked to the traded price of the scrip, including but not limited to cross border transactions involving the equity instruments (as defined in FEMA NDI Rules) of a listed company (i.e. purchase, sale, issuance of such equity instruments).

What happens if the rumor is not verified?

Unverified event or information cannot be considered as generally available information for the purpose of PIT Regulations. The definition has been amended to exclude unverified event or information reported in print or electronic media (refer amendment). That is to say, merely because the event/information is rumoured, but not confirmed by the company, it cannot be said to be generally available information.

No “unaffected price” computation; that is, all price movements will be taken into consideration for the purpose of corporate actions

Are any changes in materiality policy required?

Amendments in law will override. The timeline for responding may be aligned from 24 hours from the reporting of the event or information to 24 hours from the trigger of MPM. The obligation cast on the promoter, director, KMP or SMP may also be inserted in the policy.

Specific amendments to be made in line with the ISN as indicated below:

In addition to the specified international news sources for top 100 listed entities, all listed entities covered by mandatory rumour verification requirement are required to identify the foreign jurisdictions where the company has material business operations, along with a list of English business/ financial news sources from such foreign jurisdictions to be tracked. List of such news sources and parameters applied for determining what would constitute ‘material business operation’ to be published in the materiality policy.

SOP may be framed additionally to add the responsibility centers, timelines and other operational aspects.

This may also cover the time frame upto which rumours will be tracked in mainstream media, in the event of an MPM trigger.

Who will be responsible to ensure compliance?

Companies will have to define responsibility. Generally speaking, the compliance officer remains responsible to ensure compliance with LODR Regulations [Reg. 6(2)(a)], but internally, for rumours and responses, companies may define the ownership/responsibility centre.

The Industry Standards refer to “officers” u/s 2(59) of Companies Act. The definition therein is a very broad and inclusive definition. For the purpose of compliance with these regulations, the company may specify the meaning of “officers” to refer to the KMPs and SMPs of the company.

If the information has been sought by the company from the promoter, director, KMP, SMP, then the respective promoter, director, KMP, SMP is responsible to give adequate, accurate and timely response to queries raised or explanation sought.

The stock exchanges shall independently continue to seek clarification from the listed entities on news/rumours pertaining to the listed entity as part of their existing surveillance measures.

What are the Industry Standards w.r.t. M&A Transaction Specific Aspects?

Scope of M&A Transactions

transactions concerning purchase, sale, buyback, delisting of securities of listed company;

Preferential issue or any other fund-raising;

Scheme of arrangement involving listed entity or any of its subsidiaries

Acquisition / sale of undertaking or shareholding of another company;

Proposed joint venture between listed entity and another entity.

Exclusions – transactions undertaken in the ordinary course of business

An on-market bulk/ block deal transaction, in respect of listed entity’s securities.

An on-market treasury transaction or non-strategic transaction (pursuant to treasury management policies/ objectives – for e.g. investing surplus funds to acquire 0.5% equity stake undertaken by a listed entity in respect of another listed company)

Treasury transaction/ non-strategic transaction would generally have the following features –

pertains to the treasury function, i.e., investment of surplus funds of the company,

indicates the regular investments made by the company in the stock market,

is not intended to fulfil any strategic expectations of the company,

the size of such investments are similar to other frequent investments,

the company has not raised funds specifically for making such investments, and

decisions with respect to such investments are generally taken by a delegated authority under section 179 of the Companies Act, 2013.

Transaction stages –

Preparatory stage (where the name of the target/ counterparty is not disclosable); and

Signing of NDA, non-binding term sheet, letter of intent, commencement of DD, engagement of professionals for DD, evaluating overall viability of the deal (including for internal management) or engaging registered valuers;

Constitution of sub-committee of Board to evaluate material terms/ assess viability, Committee granting an in-principle approval subject to further evaluation.

Illustrative language of disclosure provided for each of the two sub-stages discussed above.

Advanced stages (where the name of the target/ counterparty is disclosable)

Multi-party bid process is ongoing and sole/ exclusive bidder is pending to be identified/ confirmed or has been confirmed,

parties have entered into binding term-sheet w.r.t. listed target,

where all material commercial terms have been agreed and final approval of Board or delegated board committee is being sought,

Illustrative language of disclosure provided for listed bidder(s) and for listed target.

Unaffected price to be considered only in case of advanced stages.

Where company is not a party to the deal/ does not have ‘knowledge of the deal’3

no specific confirmation/ denial would be required.

What are the Industry Standards w.r.t. Non M&A Transaction Specific Aspects?

Illustration of Non-M&A Transactions

Whistle-blower complaint received by the Company;

Internal Review or Investigation i.r.o. operational / financial aspects of the Company;

Potential change in KMPs4 (including resignation and/ or removal of KMPs);

Situation where MD/CEO is indisposed or unavailable to carry out the role in a regular manner for more than 45 days in any rolling period of 90 days on account of ill health.

Guiding Principles for rumour verification of non-M&A Transactions

The market rumour should provide specific identifiable details:

details of the matter/ event; or

Should provide quotes or be attributed to sources who are reasonably expected to be knowledgeable about the matter,

Excludes market rumours that are vague or general in nature.

The market rumour should be i.r.o impending event i.e imminent event, close at hand or about to happen,

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-05-18 19:16:252024-05-23 18:04:29Top companies forced to respond to rumours on big price spikes: Changes in Listing Regulations relate rumour responses to “material price movement”

The broad spectrum of the definition of Related Party Transactions (RPTs) under the Listing Regulation, continues to be an error prone area in terms of compliance. A recent SEBI ruling1 has further strengthens this aspect where the phrase ‘transfer of resources, services or obligations’ has been explained in an extremely new dimension with a commendable insight from the authorities which again shows that the regulators can no more be restricted by the imaginary boundaries placed by the corporates when it comes tightening the loose ends of corporate governance.

This article delves into the basis which the Regulators considered for concluding a mutual understanding and agreement between related parties to be an RPT notwithstanding the contention of the company. The essential question of law involved in this case was whether the allocation of certain products and geographic areas between RPs constitutes an RPT. The article contains our analysis of SEBI’s order and highlights the recent order passed by the SAT upon appeal in the matter, reaffirming the said stand.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00mahakagarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngmahakagarwal2024-05-06 13:53:272025-12-13 13:00:52Relinquishment of source of profit in favour of an RP: also an RPT

SEBI had raised concerns relating to evergreening of loans, circumvention of FEMA norms, QIB regulations and other concerns on regulatory arbitrage by Alternative Investment Funds (‘AIFs’) in its Consultation Paper issued in January, 2024. SEBI also recorded 40+ cases wherein the structure of AIF had been abused and used to circumvent extant financial sector regulations. Read our analysis in the article ‘AIFs ail SEBI: Cannot be used for regulatory breach’ dated January 31, 2024. Further, RBI had also barred all regulated entities (REs) with respect to their investments in AIFs, discussed in our article.

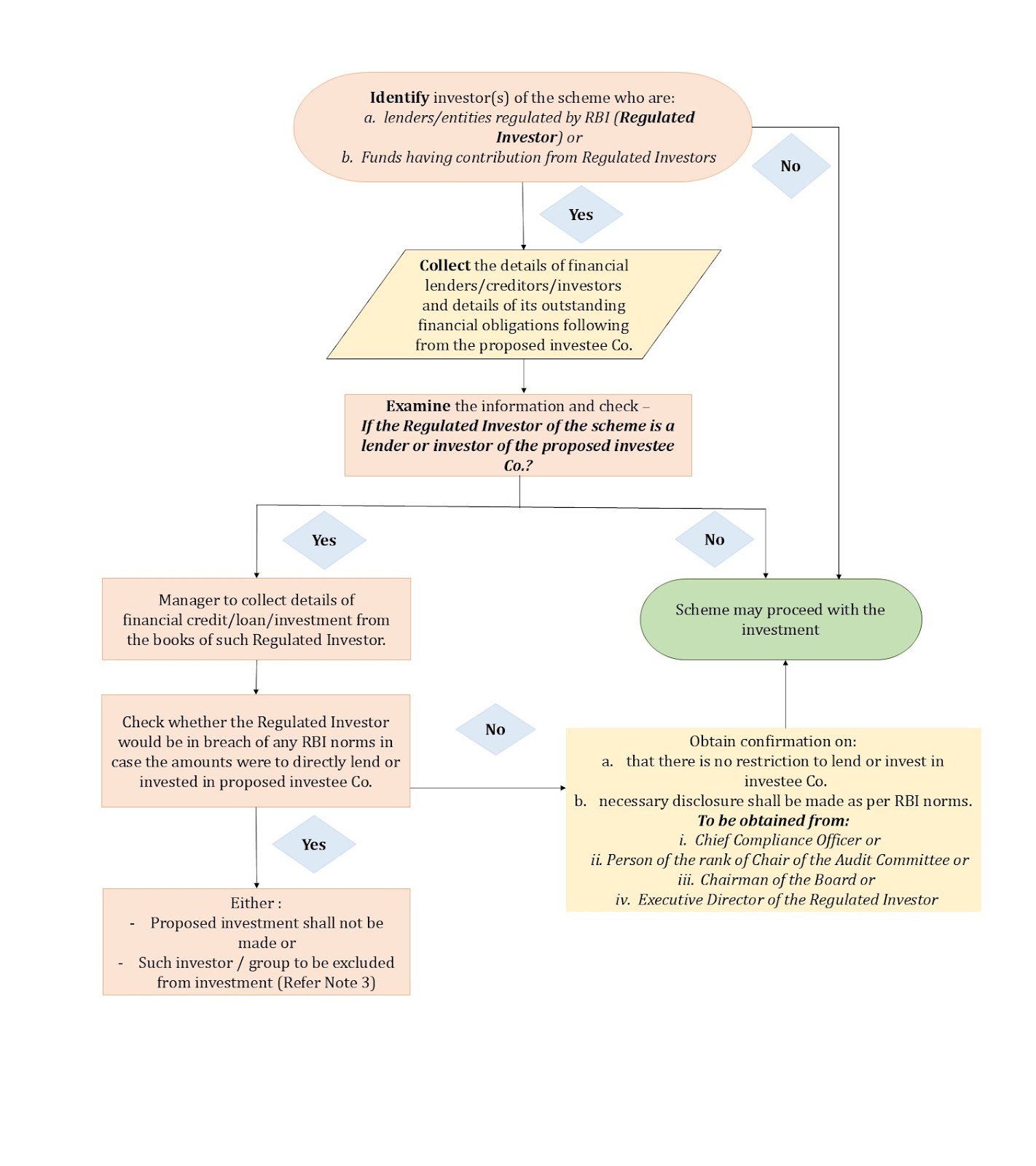

Subsequent to receipt of public comments, the proposal to mandate due-diligence (‘DD’) of investors and each of the investments made by the AIF was approved in the SEBI Board meeting held on March 15, 2024. SEBI notifiedSEBI(Alternative Investment Funds) (Second Amendment) Regulations, 2024 effective from April 25, 2024 amending Reg. 20 of the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’) dealing with general obligations thereby requiring every a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager, to exercise specific DD with respect to their investors and investments in order to prevent facilitation of circumvention of such laws as may be specified by SEBI from time to time.

The list of laws, thresholds and conditions for DD, reporting requirements etc. has been provided in SEBI circular dated Oct 8, 2024 (‘SEBI Circular’). DD is required to be carried out prior to making of investments as per implementation standards formulated by Standard Setting Forum for AIFs (‘SFA’) and published on websites of the industry associations which are part of the SFA, i.e., Indian Venture and Alternate Capital Association (‘IVCA’), PE VC CFO Association and Trustee Association of India.

Scope of laws covered under the ambit of due diligence

The list of laws provided in the SEBI Circular comprises of the following:

Provisions of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘ICDR Regulations’), and other regulations of SEBI wherein benefits or relaxations have been provided to entities designated as Qualified Institutional Buyers (‘QIBs’).

Provisions of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (‘SARFAESI Act’) wherein benefits are provided to entities designated as Qualified Buyers (‘QBs’).

Prudential norms specified by RBI for regulated lenders with respect to Income Recognition, Asset Classification, Provisioning and restructuring of stressed assets;

Rule 6 of FEMA (Non-Debt Instruments) Rules, 2019 (NDI Rules) for investment from countries sharing land border with India ( read with Press Note 3 dated April 17, 2020 of FDI Policy 2020)

Timing, thresholds for DD, reporting requirements

Pursuant to the SEBI Circular, the due diligence for various investors and investments is required to be carried out by a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager in accordance with the Implementation Standards. The table below indicates in brief the criteria, checkpoints and timelines for conducting due diligence along with the consequences of the outcome.

Sr. No

Objective intended to be achieved by investors through investments in AIF scheme

Regulations/ Directions/ Norms applicable

Applicability of requirement of DD for every scheme of AIF (refer Note 1)

Checkpoints for manager for specific DD

Timing of DD

Consequence of outcome of DD & reporting requirements, if any

1

Benefits designated for QIBs

ICDR and other SEBI Regulations

If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme.

Manager to check if such if investor/ investors of the same group is/are:(i) QIBs themselves or,(ii) Entities established, owned or controlled by the Central Government or a State Government or the Government of a foreign country, including central banks and sovereign wealth funds.Note: Where such investor is an AIF or fund set up in IFSC or outside India, above check to be carried out on a look through basis.

Prior to availing benefits available to QIBs

Refer Note 2 below for existing investments & Note 3 for proposed investments.Manager to provide confirmation to SE or lead manager or merchant banker on this.

2

Benefits designated for QBs

Under SARFAESI Act

If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme.

Same as above

Prior to making any investments or availing benefits

Refer Note 2 below for existing investments & Note 3 for proposed investments.

RBI norms on Income Recognition, Asset Classification, Provisioning and Restructuring of stressed loans/ assets

(a)whose manager or sponsor is an entity regulated by RBI; or,(b)that has investor(s)regulated by RBI who:(i)individually or along with investors of the same group contribute(s) 25% or more to the corpus of the scheme; or(ii) is an associate of the manager/ sponsor of the AIF;(iii) has majority or veto power [by itself, or through its representatives/ nominees] in voting over decisions of the investment committee set up by the manager to approve investment decisions of the scheme.Note: where investor is an AIF or fund set up in IFSC or outside India, criteria check to be carried out on a look through basis.

Refer Note 4.

Prior to making any investments, to avoid indirect investment by RBI regulated lender/ entity.

Refer Note 2 below for existing investments & Note 3 for proposed investments.

4

Investment from countries sharing land border with India

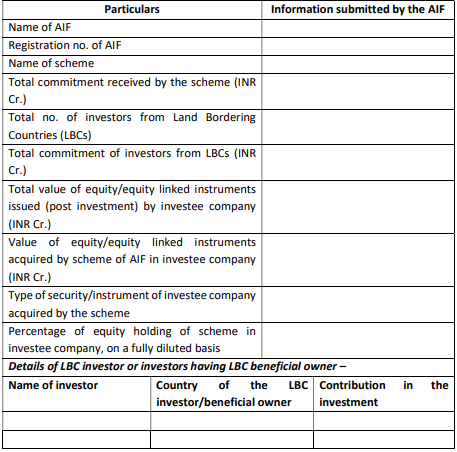

FEMA (NDI) Rules, 2019

Where 50% or more of the corpus of the scheme is contributed by investors (a)who are citizens of/are from/are situated in a country which shares land border with India; or(b)whose beneficial owners, as determined in terms of Rule 9 (3) of the PMLA (Maintenance of Records) Rules, 2005, are citizens of/are from/are situated in a country which shares a land border with India.

If the proposed investment would result in the scheme holding 10 % or more of equity/equity-linked securities issued by the company (on a fully-diluted basis), the manager to check details stated in the previous column, by collecting information on the country of investors and their beneficial owners.

Prior to making any investment

Refer Note 2 below for existing investments & Note 5 for proposed investments.

Note 1: same group’ shall mean ‘related parties’ and ‘relatives’ as defined in SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Note 2:

For Sr nos 1 to 3: DD requirement is applicable for existing investments too, held by AIF schemes as on October 8, 2024:

If DD check not satisfactory – details of investment to be reported to AIF’s custodian on or before April 07, 2025, in the format as per Annexure 1 of the circular;

If DD check satisfactory – AIF manager to submit an undertaking to AIF’s custodian on or before April 07, 2025.

For Sr no. 4: Reporting is required to be made for existing investments held by AIF schemes as on October 8, 2024 if the scheme holds 10% or more of equity/ equity-linked securities on a fully-diluted basis, to AIF’s custodian on or before April 07, 2025 in the format prescribed by SFA.

Note 3:

Consequence of not satisfying requirements of DD checks specified by SFA for proposed investments in case of Sr nos 1 to 3:

Such investor or investor group to be excluded along with necessary disclosure in the private placement memorandum (PPM); or

Investment cannot be made.

Note 4:

Note 5: Details of investment, which would result in the scheme holding 10% or more of equity/ equity-linked securities on a fully-diluted basis, to be reported to the custodian within 30 days of investment, in the below format specified by SFA.

DD requirement – one-time or ongoing?

As discussed in the SEBI BM Agenda, the purpose of the due-diligence check is to prevent facilitation of any circumvention of provisions of financial sector regulators, which cannot be a time specific check. An entity who intends to circumvent can design the structure in such a way that, at a later date post investment, it acquires the units of AIFs post investment, such as buying the units of an existing investor or by acquiring control over the existing investor entity, as per prior arrangement. Accordingly, it has been indicated that due diligence around investors and investments will be an ongoing one.

Applicability of DD – prospective or retrospective?

As per the SEBI circular this is applicable for existing and prospective investments. Refer Note 2 above.

Obligations of Custodian to the AIF

Information received from AIFs under Note 2 to be furnished to SEBI on or before May 7, 2025.

Information received from AIFs in terms of Note 4 above on a monthly basis to be compiled and reported to SEBI within 10 working days from month end.

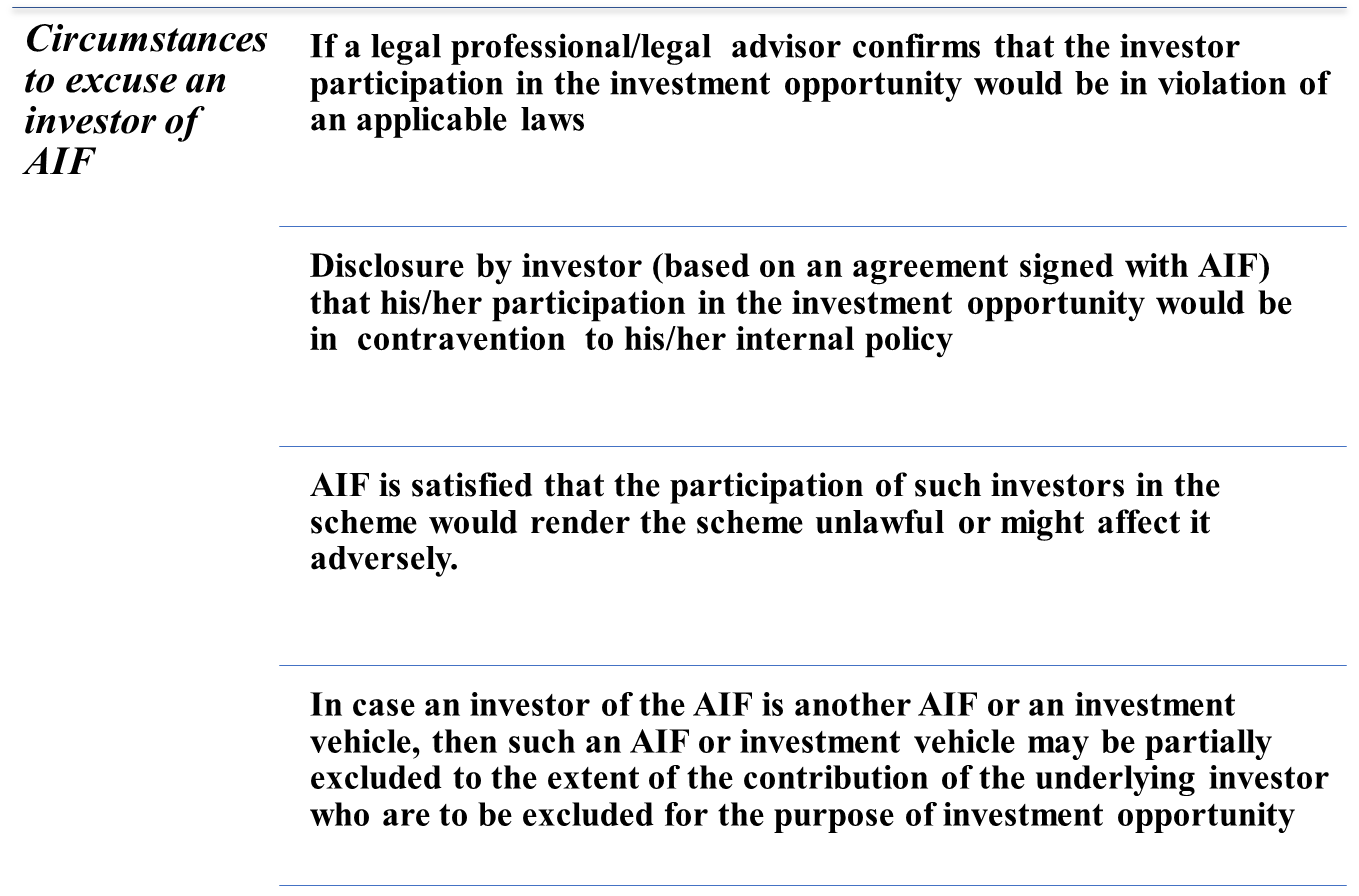

Power of AIF to exclude an investor

As per SEBI Circular, in cases where the outcome of DD is not satisfactory, in that case the AIF will either have to exclude the investor or investor group or abstain from making the proposed investment.

Figure 1: Circumstances to excuse an investor of AIF

Conclusion

The present amendment and SEBI Circular lays an onerous burden on the AIF, manager and KMP of the AIF and the manager. The DD requirement has become effective from October 8, 2024 and applies to existing investments as well. The AIFs have an actionable of evaluating the existing investments in the scheme in the light of the present amendment and ensure reporting in next 6 months. The obligation of on-going due diligence will result in a compliance burden, but is justified given the intent of law as “quando aliquid prohibetur ex directo, prohibetur et per obliquum” i.e. things that cannot be done directly should not be done indirectly either. AIFs will continue ‘trust, but verify’ using the DD standards for due diligence. The trustee/ sponsor of the AIF is required to ensure that compliance status of this amendment is reported to SEBI in the ‘Compliance Test Report’ prepared by the manager in terms of Chapter 15 of Master Circular for AIFs.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-05-03 20:07:492024-10-22 15:43:43Trust, but verify: AIFs cannot be used as regulatory arbitrage

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-05-03 13:40:552025-02-10 21:34:23Proposals approved in SEBI Board Meeting held on April 30, 2024

Use of digital platforms for tapping the early stage or ongoing funding is being seen more often than before, and quite obviously so, in a networked world where crowdsourcing and crowd placing of almost everything is the norm[1]. Several well-known platforms have been showcasing the immense potential to raise funds for startups from either private equity investors, reaching very often to retail investors too. Popular TV shows spotlighting investments in start-ups have turned fundraising entrepreneurs into celebrities, further fueling this trend. In such an environment, it is notable to find that crowdsourcing funds by a startups is said to breach the law and is attracting huge penalties.

It is essential to consider several provisions of the Companies Act, 2013 (‘CA 2013’ or ‘Act’) dealing with public issuances and private placement, along with recent orders by the RoC and SEBI. These authorities, through detailed reasoning, have imposed significant penalties for violation, highlighting that offering privately placed securities to the public—especially through online platforms—is being done in striking contravention to Act, SEBI Act as well the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (‘NCS Regulations’).

This article delves into the regulatory framework for private placements, instances of non-compliance, and the legal challenges highlighted by the RoC Delhi’s order as well as a recent ex-parte interim order passed by SEBI. It also explores how start-ups with innovative ideas but limited financial history can navigate these rules to raise funds without affecting enterprise and innovation.

The Guidelines for Corporate Governance (‘2016 Guidelines’) for insurers in India have been around for close to a decade now. These Guidelines were initially brought as an update to the then 2009 Guidelines for the purpose of aligning the same with the extensive changes to the governance of companies brought about by the Companies Act, 2013. As such, the new Guidelines were framed to be mostly in line with the Act of 2013 except certain provisions such as requiring the CEO to be a WTD of the Board (where the chairman is NED), prescribing fit and proper criteria for directors, requiring certain additional committees, having only profit criteria for CSR applicability, etc.

Through the years, these Guidelines have served as a valuable source of direction in ensuring corporate governance for insurers; laying down guidance for the composition, roles and responsibilities of the Board, functions of various Board Committees, appointment and remuneration of KMPs, disclosures in financial statements, etc.

There has been a growing emphasis on sustainability across various sectors including finance, especially, with a growing mandatory requirement of disclosure of sustainability practices by companies around the world. Various sustainability-linked finance products are designed to promote the ESG objectives of the borrower while providing financial solutions.

Traditionally, loans have remained the most common way of raising finance, and sustainable finance is no exception to the same. These loans may be labelled as green loans, social loans, sustainable loans etc. Various organisations have issued voluntary guiding principles around the same[1]. A commonality in these loans is the restriction on the “use of proceeds” – that are directed towards the green, social or sustainable objectives of the borrower. Another form of sustainable finance through loans is Sustainability-linked Loans (SLLs), where the loan contains certain sustainability-linked terms. Contrary to typical green finance products, which allocate funds for designated green projects or assets, SLLs align the loan conditions with the sustainability performance of the borrower.

Other instruments of raising sustainable finance can be through the issuance of labelled bonds or GSS+ bonds. Read more about the same in our article – Sustainable finance and GSS+ bonds. One of the more recent innovative ways of financing sustainability objects of the borrower can be through Sustainability-linked derivatives.

August 2, 2024 (original article dated October 31, 2023)

SEBI Circular, effective 1st November 2023, required FPIs to provide the details of their beneficial owners without applying any threshold in the shareholding or on layers of intermediate entities until all the natural persons are identified. An enabling provision to this effect had also been inserted as Reg. 22(6) in SEBI (Foreign Portfolio Investors) Regulations, 2019 effective from 10th August 2023. SEBI vide circular dated 27th July, 2023, had also mandated all non-individual FPIs to obtain Legal Entity Identifier (LEI) number by 23rd January 2024[1]. However, LEI could not address the requirement of additional disclosures as the LEI data stops at the parent entity level and does not provide the details of natural persons in control of the entity.

As to what could be the trigger for these regulatory changes may be anybody’s guess, but tacitly, the SEBI circular dated 24th August, 2023[2] (Circular) introducing some significant changes in beneficial ownership details by FPIs, made several admissions. It seemingly admitted that the disclosure of beneficial ownership by FPIs took advantage of technicalities by structuring the holding of natural persons to less than 10%. It also admitted that several FPIs had concentric investments in a single corporate group, making it apparent that these FPIs were used as conduits for investing in a single entity, and therefore, there may be affiliation between the FPIs and the controlling shareholders.

Briefly stated, the changed norms required FPIs, which have either (a) 50% or more of their Indian equity AUM in a single corporate group; or (b) hold along with investor group more than INR 25,000 Crore of equity AUM in Indian markets, to disclose their beneficial ownership, drilled down to the natural person level, irrespective of the percentage of holding, unless eligible for exemption.

These requirements, though effective from 1st November 2023, gave a time frame of 90 calendar days for existing FPIs to re-adjust their holdings. Meaning, FPIs had time till 29th January 2024 to realign their investment within the threshold prescribed in order to avoid providing the details of the beneficial owner as required under the Circular. Post 29th January 2024, FPIs whose investment continued to exceed the threshold as mentioned above were required to disclose the details of beneficial owners within 30 trading days ending on 12th March 2024, which if not provided led to cancellation of the FPI registration license and in the interim, blocking of account for further purchase of equity securities and restricted voting rights in investee companies.

Mandatory Beneficial Ownership (‘BO’) disclosure

The new norms differed from the erstwhile norms, where BO disclosure was required if a natural person’s beneficial holding exceeded the threshold as prescribed under PML (Maintenance of Records) Rules 2005, as indicated below:

Figure I – Threshold under PML (Maintenance of Records) Rules, 2005

The new norms required mandatory disclosure of BO, irrespective of the percentage of holding by the BO. No matter how many layers of entities covered the identity of the BO, FPIs had to identify the natural persons holding any ownership, economic interest, or exercising control, if the FPIs fall in either of the 2 categories discussed below, unless exempted.

FPIs covered under the Circular

Single Corporate Group focused FPIs:

If, instead of investing in a diverse pool of assets, an FPI has concentrated into a single corporate group, there are apparent concerns that the FPI is being used as a facade for making investments into a single entity. Thus, if on an AUM basis, more than 50% of the AUM of an FPI is in a “single corporate group”, the FPI has to provide the BO disclosure unless exempted (refer discussion below).

Intent: As per SEBI BM Agenda, the intent is to ensure there is no circumvention of minimum public shareholding norms or disclosures under SAST Regulations or investing funds routed through land border sharing countries and therefore, the need to obtain granular information around the ownership of, economic interest in, and control of FPIs with concentrated equity holdings in single companies or corporate groups.

Meaning of single corporate group: SEBI did not provide any clarity on single corporate group and left it to the stock exchanges/depositories. Rather than limiting to the existing law, BSE/NSE[3] identified a single corporate group more practically. Apart from entities having common control i.e. holding, subsidiary, associate, joint venture, and entities where promoters have major shareholding, entities which are mentioned on the website or in the annual report of the entity as a group company, have also been considered as a part of the group.

Basis this definition, BSE on its own identified the companies forming part of a single corporate group and asked the listed entities to confirm the name of the group as identified by BSE by sending communication in terms of Para 16 of the SEBI Circular that requires Stock exchanges/ Depositories to maintain a repository containing names of companies forming a part of each single corporate group and disseminate the same publicly on their websites[4].

Large sized FPIs:

FPIs with an AUM of more than INR 25,000 crore, either individually or along with their investor group[5], may pose a systematic risk in the Indian markets. It will be more concerning if such FPIs are tacitly controlled by unfriendly nations, and therefore, SEBI mandated BO disclosure from such FPIs too.

Intent: As per SEBI BM Agenda, the intent was to examine from the perspective of DPIIT Press Note 3 of April 17, 2020 (although not applicable to FPI investments), if the FPI route could potentially be misused to circumvent the stipulations of the same and disrupt the orderly functioning of Indian securities markets by their actions by having a substantial number of investors from countries that share land borders with India. It is likely that the FPI with a large Indian equity portfolio may itself be situated out of a non–land bordering country, the first level/ intermediate investors in such FPIs may be based out of land–bordering countries. This reiterated the need to obtain granular information around the ownership of, economic interest in, and control of such FPIs.

Exemption from BO disclosure

Single Corporate Group (‘SCG’) focused FPIs

Investment in SCG is insignificant compared to global investment

There might be cases where the FPI has taken exposure over an SCG only, however, may have investments globally as well and the percentage of Indian investments might be quite less when compared with its overall global investment. In such a scenario, there are fewer chances of FPIs being used as a conduit for avoiding compliance or hiding the identity of the BO. Therefore, the FPIs which are holding more than 50% of their Indian AUM in an SCG and such investments are less than 25% of their global AUM, are exempt from providing the BO disclosure.

No identified promoter in SCG

SEBI vide circular[6] dated 20th March, 2024, further exempted SCG focused FPIs meeting the following conditions:

The apex company does not have identified promoter;

Such FPI holds not more than 50% of its India equity AUM in the corporate group, after excluding its holding in the apex company with no identified promoter.

The composite holdings of all such FPIs (having SCG exposure) in the apex company with no identified promoter, is less than 3% of its total equity share capital,

Intent: As per the Consultation Paper the intent is that if FPI has exposure in SCG with no identified promoter in the apex company, there is no risk of circumvention of minimum public shareholding provision and may be exempted from the disclosure requirement. Further, there is a possibility that even though the apex company itself has no identified promoter, the FPI might still hold a significant part of its portfolio in group companies that have an identified promoter and therefore if their holding in the group is not significant exemption can be granted.

Fig. II Exemption from disclosure requirement in case there is no promoter in SCG.

Large sized FPIs,

FPIs whose Indian AUM is more than INR 25,000 crore and their investments in India are less than 50% of their overall global investments are exempt from providing such disclosure since the probability of such FPIs being used as a facade to obtain control over Indian markets is quite less.

General Exemption

FPIs that have a wide investor base or are backed by the government or government related investors do not pose any risk to Indian markets or the probability is quite low, and therefore the following categories of FPIs are exempt from providing BO disclosure. Also, if the investors in FPI fall under the below mentioned categories, then identification of BO for such investors will not be required. In case the constituents of Large sized FPIs fall under below mentioned category, their holding will also not be aggregated with their investor group to calculate the limit of Rs. 25,000 Crore.

The below figures provide a gist of the scenarios where FPIs are required to provide the disclosure

Figure IV – Flowchart depicting the scenarios that would warrant additional disclosures

Responsibility of DDPs/Depository

The FPIs are put under the obligation to ensure compliance with the SEBI Circular, i.e. providing the BO disclosure and monitoring the concentration limit in a single corporate group and the equity investments in India. Additionally, DDPs are also required to monitor the same and intimate the FPIs wherever they breach the criteria and once the registration of FPI is invalidated as a result of non-disclosure, the Depository will intimate the investee listed company to freeze the voting rights of such FPIs to the extent of actual shareholding or shareholding corresponding to 50% of its equity AUM on the date its FPI registration is rendered invalid, whichever is lower (refer the example below).

To ensure that there is no regulatory arbitrage amongst DDPs, a standard operating procedure (SOP)[8] has been framed & followed by all the DDPs to independently validate the conformance of FPIs with the conditions and exemptions prescribed. The SOP is based on the application of the core principles of minimising Type II errors i.e. where legitimate FPIs and their investors face challenges of onerous regulatory requirements) without adding to Type I errors i.e., where FPIs that may be breaching regulations, circumvent the need to make disclosures that would bring such breaches to light, through the ‘trust – but verify’ route.

Responsibility of a Listed Entity

The FPIs whose registration is rendered invalid as a result of non-disclosure are restricted from casting their vote and it is the responsibility of investee listed company to ensure that the voting rights of such FPIs are freezed to the extent of actual shareholding or shareholding corresponding to 50% of equity AUM on the date its FPI registration is rendered invalid, whichever is lower. The said information will be provided by the depository to the investee listed entity/its RTA. The following example clarifies calculation of extent of shareholding to be freezed.

Eg. FPI XYZ has 60 shares of Company A and 40 shares of Company B as on May 13, 2024, and the FPI fails to make the additional disclosures, thereby rendering its FPI registration invalid from May 13, 2024. Thereafter, FPI’s voting rights shall be restricted to shareholding corresponding to 30 shares of Company A and 20 shares of Company B.

Suppose as on July 01, 2024, the FPI has liquidated some shares and holds 15 shares of Company A and 30 shares of Company B. As on this date, the FPI will be able to exercise voting rights corresponding to 15 shares of Company A but only 20 shares of Company B (maximum permissible voting rights in Company A).[9]

The listed entities were required to intimate the details of their corporate group to the stock exchanges and any change is to be intimated within 2 working days of the effective date of such change[10].

The non-compliant FPIs are also restricted from purchasing further equity shares, however, the responsibility is not upon the listed entity to not issue equity shares to such FPIs. The DDPs/Custodian will block the account of FPIs for further purchases and they cannot participate in any corporate action which increases the equity shareholding such as rights issue, FPOs, etc. However, credit as a result of any involuntary corporate actions such as bonus issue, scheme of arrangement, etc will be allowed.

Conclusion

SEBI had stated that there cannot be sustained capital formation without transparency and trust. The Circular is a move to foster trust and increase transparency in the Indian Capital markets. The Circular does not seem to be a hindrance to genuine FPIs, though operational challenges might be faced by the FPIs in identifying the BOs.

[1] 180 days from the date of issue of the SEBI Circular.

[2] The said circular was approved in the SEBI Board meeting dated 28th June, 2023

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Prapti Kanakiahttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPrapti Kanakia2024-03-22 13:33:522024-08-02 13:15:24Single Corporate Group focused FPIs & Large value FPIs to disclose granular details of beneficial ownership

Loading…

Loading…