The new dispensation implemented from 5th December 2025 implies that lending business, obviously carried in the parent bank, needs to be allocated between the bank and the group entities so as to avoid overlaps. The bank will have to take its business allocation plan, at a group level, to its board, by 31st March 2026.

The RBI’s present move has certain global precedents. Singapore passed an anti-commingling rule applicable to banking groups way back in 2004, but has subsequently relaxed the rule by a provision referred to as section 23G of the Banking Regulations. However, the approach is not uniformly shared across jurisdictions.

We are of the view that as the decision works both at the bank as well as the NBFC/HFC level, the same has to be taken to the boards of the respective NBFCs/HFCs too.

Businesses which currently overlap include the following:

Loans against properties

Housing finance

Loans against shares

Trade finance

Personal loans

Digital lending

Small business loans

Gold loans

Loans against vehicles – passenger and commercial, or loans against construction equipment

In our view, banks will have serious concerns in meeting their priority sector lending targets, unless they decide to keep priority sector lending business in the bank’s books. Priority sector lending is quite often much less profitable, and the NBFCs in the group are able to create such loans at much higher rates of return due to their delivery strengths or customer franchise. As to how the banks will be able to originate such loans departmentally, will remain a big question.

There are other implications of the above restrictions too:

If a bank is engaged, for example, in MSME lending, but auto loans are done at the group entity, the bank cannot be a co-lender with its group entity, nor can it acquire auto loans originated by its group entity.

Extending the same argument, if the banking group is carrying auto loan activity in its group NBFC, it cannot buy auto loans either by way of a direct assignment or co-lending, originated by other banks or other independent NBFCs. The reason for this is obvious – if the bank has decided to carry auto lending activity in its group entity, it should stay away from that exposure, even if originated by other entities.

The decision to keep particular loan products with group entities – can it be stretched to the extent that bank will not have indirect exposure in such products, for example, by way of giving a loan to its group entity for on-lending for a product which the bank does not undertake departmentally? One of the reasons that may have prompted the Mohanty Group report in 2020 to segregate products between the bank and its group entities was contagion risk. If contagion is at the core of the present restriction, then that risk is still there even if the bank lends to a group entity for on-lending for a product. However, in our view, the present restriction is primarily aimed at avoiding regulatory arbitrages, and cannot be expected to require a completely independent financing of the loan products that a subsidiary finances, and not the bank.

Therefore, in our view, a bank may not only on-lend to its group entities (of course, on the basis of an arm’s length lending approach), but it may also buy the asset-backed securities arising from such loan portfolios as sit with its group entities.

Factors to decide loan product allocation

In case of several non-lending products such as securities trading, demat services, etc., the approach may be easier. However, lending services constitute the bulk of any bank’s financial business, and group NBFCs and HFCs are also evidently engaged in lending. Hence, there may be a delicate decisioning by each of the boards on who does what. Note that this choice is not spasmodic – it is a strategic decision that will bind the entities for several years.

The factors based on which banks will have to decide on their business allocation may include:

Delivery mechanisms – Mostly, branch and team strengths are sitting in group entities. Therefore, the loan products that entail last mile customer outreach, geographical access, etc are naturally housed in entities which possess those abilities.

Technology strength: Some of the products are based on fintech or similar technology strength, which may be sitting with respective entities.

Recovery mechanisms – Group entities are typically more nimble than banks. Hence, while banks may keep loans on their books, but they may engage group entities for recovery purposes.

Priority sector requirements-: This will be a very important factor in deciding business allocation. Banks are mandated to invest 40% of their ANBC in qualifying priority sector loans – not NBFCs. Hence, for such loans as qualify as priority sector, the option may be to house the portfolios with the bank, or to invest in pass through certificates.

Securitised notes: whether investment in group entities?

Talking about pass through certificates, there is a complicated question as to whether the investment limits imposed by the 5th Dec. 2025 amendment on aggregate investments in group entities will include investment in pass through certificates arising out of pools originated by group entities. In our view, the answer is in the negative, as the investment is not originator, but in the asset pools. However, if the bank makes investment in the equity tranche or credit enhancing unrated tranches, the view may be different.

Conclusion

Banks are heading shortly in the last quarter of a year which is laden with strong headwinds. In this scenario, facing business allocation decisions, rather than business expansion or risk management, may be more challenging than it may seem to the regulators.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-12-06 16:29:452025-12-06 16:46:40Banking group NBFCs: Need to map businesses to avoid overlaps with the parent banks

The RBI has long been stitching up the seams where AIF structures threatened to pull at the fabric of Banking regulation. The latest amendment to the Reserve Bank of India (Commercial Banks – Undertaking of Financial Services) Directions, 2025 is another careful thread in that ongoing work. The provisions apply not only to banks directly but also to exposures routed through their group entities (meaning subsidiary, JV or associate of the bank). Banks (and their group entities) may still participate in AIFs but only within closely drawn boundaries. The message is unambiguous: the AIF route cannot be used to skirt evergreen exposures or manufacture regulatory arbitrage.

Limits on investment in AIF schemes

For Category I and Category II AIFs, limits apply at both the individual bank level and at the group level.

At the bank level, no bank may contribute more than 10% of the corpus of any AIF scheme;

At the bank group level, investments are permitted within a corridor:

Less than 20% of the corpus of Cat I or Cat II AIFs may be invested without prior approval, provided the parent bank continues to meet minimum capital requirements and has reported net profit in each of the preceding two financial years. This means even the AMC along with the bank cannot hold more than 20%;

Between 20% and 30% of the corpus may be invested with prior RBI approval.

A systemic cap overlays this: contributions from all regulated entities – banks, NBFCs, co-operative banks and AIFIs etc. – cannot collectively exceed 20% of any AIF corpus. Similarly investment in the unit capital of REITs and InvITs is capped at 10%, within the overall ceiling of 20% of net worth for equity, convertible instruments and AIF exposures.

A question may arise on whether such limits, as applicable to investments in AIFs, would also be applicable to making investments in FMEs operating in IFSC? Practically, Indian banks are unlikely to invest in FMEs, because such investments would cause the FME to lose its tax benefits. For an FME to qualify as a “specified fund”, all its units must be held by non-residents, except those held by the sponsor. When this condition is met, the income of the fund is exempt under Section 10(4D) and the income received by non-resident investors is exempt under Section 10(23FBC) of the Income Tax Act.

No circumvention of regulations through investments in AIFs

Banks shall ensure that their exposure in an investee company through their investments in AIF schemes does not result in circumvention of any regulations applicable to banks. (see para 38D). This would mean that where a bank is restricted from having any exposure in an investee company (this may include restrictions on account of the end-use of funds, or restrictions in terms of limits to exposures etc), such exposures cannot be made indirectly through making investments in AIF schemes, which, in turn, leads to the bank’s exposures to such investee companies.

Prohibition on Category III AIFs

The clearest prohibition concerns Category III AIFs. Banks are not permitted to invest in their corpus at all. If a subsidiary is a sponsor, it may hold only the minimum contribution required under SEBI’s regulations (which currently is lower of 5% of the corpus or ₹10 Crore as per proviso to Regulation 10(d) of the SEBI AIF Regulations, 2012). Highly traded, leveraged or long-short strategies are thus kept outside the perimeter of bank funding in a deliberate effort to insulate bank balance sheets from hedge-fund-type risk.

Globally, regulators have taken a different, more permissive route. In the United States, banks are not barred from investing in hedge-fund-type vehicles. Instead, the Volcker Rule restricts ownership to de-minimis levels, generally up to 3% of a fund and 3% of Tier 1 capital in aggregate.1

Under Basel’s CRE 60 framework, investments in funds are permitted, however, discipline lies in capital treatment:

If the bank can look-through to underlying exposures, risk weights are based on the underlying assets2;

Where transparency is not available, risk weights can rise to punitive levels, up to 1,250% – making opaque fund exposures extremely capital-intensive.

Recently, IMF in its October 2025 Financial Stability Report has highlighted that banks’ exposures to non-banks, including private-credit and private-equity funds, have grown materially, raising concerns about concentration and potential spill-over risks.

India therefore stands apart. Where other jurisdictions rely on expensive capital and other constraints to manage hedge-fund-type exposures, the RBI has chosen to keep such structures outside the banking perimeter altogether.

Provisioning and Capital Treatment

Capital consequences have also been tightened. Where a bank holds more than 5% of the corpus of an AIF that subsequently invests – other than in equity instruments3 – into a debtor company of the bank, a 100% provision must be created for the bank’s proportionate exposure (See our write-up on the same here). This directly addresses the risk that AIFs could become conduits for evergreening or indirect refinancing of stressed loans.

Overall Perspective

The Amendment Directions extend the guardrails on AIF participation to the bank group, as against the previous approach of regulating only the bank’s exposures. Guardrails are numerical and backed by provisioning and capital consequences. Any breach in the limits require reporting to RBI, with clear reasons and plan for corrective actions. For existing investments, banks are required to provide an action plan by 31st March, 2026 – ensuring the compliances within a maximum of 2 years, viz., 31st March 2028.

RBI’s stance is more conservative than many international regimes, but the regulatory intent is unmistakable: prudential norms are not to be diluted simply because exposure is packaged through an AIF.

CRE 60 offers three routes for capital treatment – look-through, mandate-based and fall-back – chosen according to how much visibility the bank has into the fund’s underlying assets. ↩︎

Equity instruments means equity shares, compulsorily convertible preference shares (CCPS) and compulsorily convertible debentures (CCDs) ↩︎

Follow the regulations as applicable in case of NBFC-UL (except the listing requirement)

Adhere to certain stipulations as provided under RBI (Commercial Banks – Credit Risk Management) Directions, 2025 and RBI (Commercial Banks – Credit Facilities) Directions, 2025

The requirements become applicable from the date of notification itself that is December 5, 2025. Further, it may be noted that the applicability would be on fresh loans as well as renewals and not on existing loans. The following table gives an overview of the compliances that NBFCs/HFCs, which are a part of the banking group will be required to adhere to:

NBFCs/HFCs which are group entities of banks would have to adhere to the Large Exposures Framework issued by RBI.

Internal Exposure Limits

In addition to the limits on internal SSE exposures, the Board of such bank-group NBFCs/HFCs shall determine internal exposure limits on other important sectors to which credit is extended. Further, an internal Board approved limit for exposure to the NBFC sector is also required to be put in place.

NBFC in the banking group shall be required to undertake a review of its Board composition to ensure the same is competent to manage the affairs of the entity. The composition of the Board should ensure a mix of educational qualification and experience within the Board. Specific expertise of Board members will be a prerequisite depending on the type of business pursued by the NBFC.

Removal of Independent Director

The NBFCs belonging to a banking group shall be required to report to the supervisors in case any Independent Director is removed/ resigns before completion of his normal tenure.

Restriction on granting a loan against the parent Bank’s shares

Conditions w.r.t financing promoters’ contributions towards equity capital apply in terms of Para 166 of the Credit Facilities Directions. Such financing is permitted only to meet promoters’ contribution requirements in anticipation of raising resources, in accordance with the board-approved policy and treated as the bank’s investment in shares, thus, subject to the aggregate Capital Market Exposure (CME) of 40% of the bank’s net worth.

Prohibition on Loans for financing land acquisition

Group NBFCs shall not grant loans to private builders for acquisition and development of land. Further, in case of public agencies as borrowers, such loans can be sanctioned only by way of term loans, and the project shall be completed within a maximum of 3 years. Valuation of such land for collateral purpose shall be done at current market value only.

NBFCs/HFCs, which are group entities of Banks can only undertake agency business for financial products which a bank is permitted to undertake in terms of the Banking Regulations Act, 1949.

Undertaking of the same form of business by more than one entity in the bank group

UFS Directions

There should only be one entity in a bank group undertaking a certain form of business unless there is proper rationale and justification for undertaking of such business by more than one entities.

Investment Restrictions

Restrictions on investments made by the banking group entities (at a group level) must be adhered to.

Read our write-up on other amendments introduced for banks and their group entities here.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-12-06 11:24:572025-12-06 12:43:35Bank group NBFCs fall in Upper Layer without RBI identification

Similar amendments have been made for Commercial Banks, Local Area Banks, Small Finance Banks, Rural and Urban Co-operative Banks, RRBs, ARCs and AIFIs.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-12-05 17:11:002025-12-05 18:57:55NBFCs shift to 4-snapshots a month for quicker credit reporting

Private credit is becoming a new force in India’s lending ecosystem. As traditional banks and NBFCs operate under the strict regulations on capital, exposure and asset quality norms, they are often unable, or unwilling to cater to certain borrowers. In addition, for banks in particular, what kind of lending opportunities can be tapped is often a matter of having typecast lending products, policies and procedures. This leaves occasional, however, lucrative gaps in funding needs which are not serviced by regulated lenders. Into these gaps step in Private Credit AIFs (in India), Business Development Companies (BDCs) and Private Collateralized Loan Obligations (CLOs) (in the USA and Australia), these funds can structure deals creatively, customise financing to borrower needs and capture higher-yield opportunities that conventional lenders must pass over. What is emerging is a parallel channel of credit, one that is nimble, agile and focused.

Globally, this shift hasn’t gone unnoticed. Policymakers and institutions like the IMF have flagged the risks tied to private credit markets, especially around opacity, leverage and borrower quality (see below). Yet in India, the momentum continues to build. Tight constraints on banks, the rise of alternative asset managers and the unmet capital needs of businesses beyond the traditional credit universe are all fuelling rapid expansion.

This article examines what private credit is, why it is growing in India, the risks associated with this market and whether their growth creates regulatory arbitrage relative to banks and NBFCs.

What is Private Credit?

As per an IMF paper1, private credit is defined as “non-bank corporate credit provided through bilateral agreements or small “club deals” outside the realm of public securities or commercial banks. This definition excludes bank loans, broadly syndicated loans, and funding provided through publicly traded assets such as corporate bonds.

Simply, private credit is the lending by non-bank and non-NBFCs. The sector predominantly involves alternative asset managers2 who raise capital from institutional investors using closed-end funds and lend directly to predominantly middle-market firms3.

How is it Different From Normal Credit?

Unlike traditional credit, private credit is typically tailored to the specific needs of each borrower. Repayment terms can, for instance, be aligned with the timing of a funding round or disbursements can be structured to match capital expenditure plans. Interest rates may also be designed on a step-up basis, linked to the borrower’s turnover. Many elements that are otherwise rigid under RBI-regulated lending can be flexibly structured in private credit (see table 2 below). This flexibility is especially valuable for start-ups and small businesses, which often require customised financing solutions that traditional lenders may be unable to provide.

Parameter

Private Credit

Traditional Credit

Source of Capita

Private debt funds (Category II AIFs), investors like HNIs, family offices, institutional investors

Banks, NBFCs and mutual funds

Target Borrowers

Companies lacking access to banks; SMEs, mid-market firms, high-growth businesses

Higher-rated, established borrowers.

Deal Structure

Bespoke, customised, structured financing

Standardised loan products

Flexibility

High flexibility in terms, covenants, and structuring

Restricted by regulatory norms and rigid approval processes

Returns

Higher yields (approx. 10–25%)

Lower yields (traditional fixed-income)

Risk Level

Higher risk due to borrower profile and limited diversification

Lower risk due to stronger credit profiles and diversified portfolios

Regulation

Light SEBI AIF regulations; fewer lending restrictions

Heavily regulated by RBI and sector-specific norms

Liquidity

Closed-ended funds; limited exit options

More liquid; established repayment structures; some products have secondary markets

Diversification

Limited number of deals; concentrated portfolios

Broad, diversified loan books

Role in Market

Fills credit gaps not served by traditional lenders

Core credit providers in the financial system

Table 1: Differences between private credit and traditional credit

How Much of it is in India?

Global private credit assets under management have quadrupled over the past decade to US$2.1 trillion in 20234. Compared with the rest of the world, the private credit market in India is very small, with estimated assets under management of $25 billion to $30 billion as of March 31, 2025, representing about 0.6% of India’s GDP and 30-35% of the total investments made by AIFs in India.5

Figure 1: Private credit share (1%) as a part of overall corporate lending. Source: RBI, AMFI

Figure 2: Size of Private Credit Market. Source: RBI

Reasons for Rise in Private Credit?

Private credit is expanding rapidly because it steps in where traditional banks hesitate. It provides capital for last-mile project completion, cost overruns and promoter equity infusion; areas that fall outside the comfort zone of regulated lending. The asset class has also delivered consistently higher risk-adjusted returns, a compelling draw for global and domestic investors, especially through long phases of low interest rates.6

A key advantage lies in its flexibility. Private lenders can tailor covenants7, link returns to cash flows and restructure repayment terms during stress, offering a level of customisation that conventional bank credit cannot match. For investors, this translates into both diversification and access to high-growth segments that remain beyond the scope of mainstream credit markets.

Sector specific regulatory gaps: There is a concern that tighter bank regulation will continue to encourage the migration of credit from banks to private credit lenders8. Certain regulatory restrictions on banks directly push borrowers toward private credit:

Real estate: Banks cannot lend for land acquisition (Para 3.3.1, Master Circular – Housing Finance), leading to real estate becoming a major private-credit segment, accounting for about one-third of all private credit deals.9

Mergers & acquisitions: Banks are not expected to lend to promoters for acquiring shares of other companies (Para 2.3.1.6, Master Circular – Loans and Advances). Consequently, 35% of private credit deals involve M&A financing. However, RBI’s Draft Directions on Acquisition Finance proposes to somewhat ease this restriction.10

Apart from the above, The IBC significantly strengthened creditor rights and recovery prospects, boosting confidence among lenders and supporting the growth of private credit. At the same time, many borrowers, particularly smaller firms, those with weak earnings, high leverage or insufficient collateral, struggle to access bank loans making private credit a natural alternative11. This shift was further accelerated by an extended period of low global interest rates, which pushed investors to seek higher-yielding opportunities and increased capital flows into private credit strategies.

The most common structure for channelising private credit is an AIF – more specifically, a Category II AIF. A ‘Private Credit AIF’ is essentially an AIF whose primary investment strategy is direct debt financing (by investing in debt instruments) to borrowers outside the conventional banking/syndicated loan market. Since AIFs are not subject to the same regulatory framework as traditional lenders (for example, no deposit-taking, no CRR/SLR requirements etc.), they can offer tailor-made structures such as step‐up interest rates, bullet repayments, equity warrants, convertible features, etc.

A private credit fund requires long-term, stable capital, and frequent redemption demands can disrupt lending strategy. A closed-ended Category II AIF structure suits this model well, as it locks in investor capital for the fund’s life and prevents premature withdrawals. Private credit deals are idiosyncratic and difficult for outside parties to value or trade, lenders typically rely on long-term pools of locked-up capital for financing. One advantage AIFs have over mutual funds is that mutual funds are restricted to investing only up to 10% of their debt portfolio in unlisted plain vanilla NCDs.

Compared to private equity or venture capital, where performance depends heavily on market conditions and timing exits, private credit offers returns that are largely predetermined by contract. The trade-off, however, is that like most AIFs, these investments typically come with multi-year lock-ins and fewer exit opportunities, underscoring their inherently illiquid nature. Typically, investors which can commit long term capital are well-suited to invest in such AIFs – such as pension funds and sovereign wealth funds etc.

Rise of Business Development Companies

A Business Development Company (BDC) is a U.S. investment vehicle designed to channel capital to small and mid-sized businesses that lack easy access to traditional bank financing or public capital markets. BDCs were created by the U.S. in 1980, through amendments to the Investment Company Act of 1940(see sections 2(48), 54 and 55), with a clear policy objective: to allow retail investors to participate in private credit and growth capital, an area previously accessible only to institutional investors.

As per a Federal Reserve Paper: BDCs are a way for retail investors to invest money in small and medium-sized private companies and, to a lesser extent, other investments, including public companies. BDCs are structured in different ways. Public BDCs refer to those with shares traded on national securities exchanges, and those whose shares are not traded on national securities exchanges but placed through SEC-registered or private placement offerings are non-publicly traded BDCs. BDCs typically finance middle-market firms—companies with EBITDA between $5 to $100 million, which historically have had limited access to funding from commercial banks and public debt markets. They also provide finance to development-stage companies in sectors such as technology, life science, healthcare information and services and sustainability industries, and private-equity owned or sponsored companies. Structure and regulatory framework: Legally, a BDC is an unregistered closed-end investment company (fund). To qualify as BDC, a company must invest at least 70% of its assets in ‘eligible portfolio companies’ i.e. firms with market values below $250 million and provide ‘significant managerial assistance’ to its portfolio companies [see section 2(48) of the Investment Company Act, 1940]. These companies are often private, thinly traded public firms, or businesses undergoing financial stress. To avoid corporate-level taxation, they must distribute at least 90% of their taxable income to shareholders each year (like REITs and InvITs in India). BDCs are also permitted to use leverage (up to 2x the amount of assets).

BDCs raise capital through IPOs, follow-on equity issuance, corporate bonds or hybrid securities. While many BDCs are publicly traded on stock exchanges (50 in number), offering daily liquidity to investors, some exist as non-traded BDCs with limited liquidity (47 in number) and yet some as private BDCs (50 in number).12

Investment mix: Although BDCs are permitted to invest in both equity and debt, their portfolios are majorly debt-focused. In practice, 60–85% of a typical BDC portfolio is invested in debt instruments, such as senior secured loans, second-lien loans, or mezzanine debt. Equity investments usually comprise 15–30% of assets.13 Because of this allocation, interest income from loans is the primary driver of BDC earnings. This income tends to be steady and predictable, which aligns well with the BDC structure. For example, Ares Capital, one of the largest BDCs, allocates roughly 78–83% of its portfolio to debt (primarily first-lien loans) and about 17% to equity.

How BDCs generate returns: BDCs generate returns through multiple channels:

Interest income from loans to portfolio companies (the dominant source)

Dividends from preferred or common equity holdings

Capital gains from selling equity stakes or converting and exiting convertible securities

Many BDC loans are floating-rate, which provides partial protection in rising interest rate environments. However, most BDC investments are below investment-grade or unrated and equity positions are often in privately held or financially stressed companies, introducing credit and valuation risk.

Comparison with venture capital, private equity AIFs and Mutual Funds: BDCs are often compared with venture capital and private equity funds because all three invest in private, illiquid companies and may provide strategic or managerial support. The key distinction lies in investor access and structure. Venture capital and private equity funds are privately placed vehicles, restricted to institutions and wealthy investors, with long lock-ups and limited transparency. BDCs, by contrast, are designed to be accessible to retail investors and trade on public exchanges.

This distinction becomes especially relevant when comparing BDCs with AIFs in India, particularly private credit AIFs. Economically, BDCs resemble private credit AIFs; both lend to mid-market companies and rely heavily on interest income. The crucial difference lies in retail participation. In India, AIFs exclude retail participation by making the minimum investment amount of Rs. 1 Crore and prohibiting public issuances. In the U.S., BDCs were created to enable retail participation therefore there are no minimum investment norms and public issuances are allowed for BDCs. In this sense, BDCs can be thought of as private credit AIF-like strategies wrapped in a publicly traded structure, placing them between mutual funds (fully liquid public-market vehicles) and AIFs (illiquid private-market vehicles) on the investment spectrum.

From an Indian regulatory perspective, mutual funds offer the closest structural comparison to BDCs, albeit with important distinctions. Indian mutual funds are not permitted to employ leverage as part of their investment strategy and may borrow only to meet temporary liquidity requirements, capped at 20% of net assets (see Regulation 44 of the SEBI Mutual Fund Regulations). In addition, mutual funds face strict asset-side constraints, including a limit of 10% of the debt portfolio in unlisted plain-vanilla non-convertible debentures (see paragraph 12.1.1 of the SEBI Master Circular on Mutual Funds). These restrictions constrain exposure to illiquid private credit, making a BDC-like structure regulatorily infeasible in India under the mutual fund framework.

Global context: No other major market has created a true equivalent of the BDC. While regions such as Europe, Canada, and Australia have listed private credit funds, specialty finance vehicles, or credit income trusts, these structures typically limit or discourage retail participation. Risk considerations: While BDCs may have stable and regular income, they carry elevated risks. Their portfolios consist largely of non-investment-grade debt and equity in small or distressed companies, often with limited public information. Credit losses, economic downturns or excessive leverage can materially impact returns.

Regulatory Concerns with Growth of Private Credit?

IMF in its 2024 Global Financial Stability Report highlighted risks w.r.t rise in private credit since its growth comes with several structural weaknesses that make the market vulnerable, especially in a downturn. Its rapid expansion is happening largely outside traditional regulatory oversight and because the market has not been stress-tested, the true scale of risk remains unclear. Borrowers tend to be smaller and more leveraged and with most loans being floating-rate, repayment stress can escalate quickly when interest rates rise. Although private credit funds’ leverage appears low compared with other lenders, end borrowers tend to be more highly leveraged than those in public markets, increasing the risks to financial stability.14

The increased complexity and the interconnections with leveraged financial entities create more channels through which unexpected losses in private credit could spread to the broader financial system15

Instruments such as PIK interest16 only defer the problem, increasing loss severity if performance deteriorates. Liquidity is another pressure point since private credit funds are inherently illiquid. Risk is further amplified by layers of hidden leverage, at the borrower, SPV, investor and fund level making contagion hard to track. Layers of leverage are created by the AIF lending against equity to a holding entity, which infuses the equity into an operating company, and the operating company borrowing against such equity.

Because loans are private, unrated and rarely traded, valuation is opaque and losses may remain masked until too late. Growing competition also risks weakening underwriting standards and covenant discipline, particularly as larger banks participate in private deals.

Practical challenges add to this vulnerability. Collateral enforcement may not always hold up legally, say due to restrictions on transferability of collateral (say, shares of a private company). Equity-linked security is volatile as well, and during distress, equity tends to lose its value almost completely. In essence, private credit offers flexibility and returns, but its opacity, leverage, illiquidity and weaker borrower profiles create risks that could surface sharply in stress conditions. Private credit certainly warrants closer attention. Nonbank lenders, especially private credit funds, have grown rapidly in recent years, adding to financial stability risks because they are less transparent and not as firmly regulated.

Do private credit AIFs create any regulatory arbitrage?

What you cannot do directly, you cannot do indirectly – the age-old maxim might apply in case a RE which is otherwise barred by RBI for an object, uses the AIF route to achieve that object. Below we examine some of the distinctions in the regulatory oversight:

Function

Private Credit AIFs

RE

Credit & Investment rules

Credit underwriting standards

No regulatory prescription

No such specific rating-linked limits. However, improper underwriting will increase NPAs in the future.

Lending decision

Manager-led

Investment Committee under Reg. 20(7) may decide lending

Manager controls composition of IC;

IC may include internal/external members;

IC responsibilities may be waived if investor commitment ≥₹70 Cr w/ undertaking Primarily i.e. the main thrust should be in: – Unlisted securities; and/or – Listed debt rated ‘A’ or below

Lending decisions guided by Board-approved credit policy

Exposure norms

Max 25% of investible funds in one investee company.

Exposure is limited to 25% of Tier 1 Capital per borrower and 40% per borrower group for NBFC ML;

No such limit for NBFC BL.

Banks can lend maximum upto 15% of their Tier 1 + Tier 2 capital to a single borrower. Large exposure norms may apply in case of banks and Upper Layer NBFCs

End-use restrictions

None prescribed under AIF Regulations, results in high investment flexibility

Banks cannot lend for land acquisition or for funding a M&A deal [refer ‘sector-specific regulatory gaps’ above] NBFCs do not have any such restrictions. They do have internal limits on sensitive sector exposures which includes capital market and commercial real estate [See Para 92 of SBR]

Related party transactions

Need 75% investors consent [reg 15(1)(e)]

Board approval mandatory for loans ≥₹5 Cr to directors/relatives/interested entities;

Disclosure + abstention from decision-making;Loans to senior officers requires Board reporting [See para 93 of SBR]

Capital, Liquidity & Leverage Requirements

Capital requirements

No regulatory prescription as the entire capital of the fund is unit capital

Minimum net owned funds of ₹10 Cr, CRAR 15% for NBFC-ML and above [See para 133.1 of SBR]9% CRAR in case of banks,

Liquidity & ALM

Uninvested funds may be parked in liquid assets (MFs, T-Bills, CP/CDs, deposits etc.) [15(1)(f)]

NBFC asset size more than 100 Cr. have to do LRM [Para 26]

Leverage limits

No leverage permitted at AIF level for investment activities Only operational borrowing allowed

Leverage ratio of BL NBFC cannot be more than 7 No restriction on NBFC ML however, CRAR of 15% makes results into leverage limit of 5.6 times For Banks, in addition to CRAR, there is minimum leverage ratio is 4%

Monitoring, Restructuring and Settlements

Loan monitoring

No regulatory prescription

RBI-defined SMA classification, special monitoring, provisioning & reporting.

Compromise & settlements

No regulatory prescription

Governed by RBI’s Compromise & Settlement Framework

Governance, Oversight & Compliance

Governance & oversight

Operate in interest of investors Timely dissemination of info Effective risk management process and internal controls Have written policies for conflict of interest, AML. Prohibit any unethical means to sell/market/induce investors Annual audit of PPM termsAudit of accounts 15(1)(i) – investments shall be in demat form Valuation of investments every 6 months

A Risk Management Committee is required for all NBFCs. [See para 39 of SBR] AC [94.1], NRC [94], CRO [95] ID and internal guidelines on CG [100] required for NBFC-ML and above

Diversity of borrowers

Private credit AIFs usually have 15-20 borrowers.

Far more diversified as compared to AIFs

Pricing

Freely negotiated which allows for high structuring flexibility

Guided by internal risk model

Table 2: Differences in regulatory oversight between AIFs and Regulated Entities (REs)

The core difference between private credit AIFs and RBI-regulated lenders lies in regulatory intent. SEBI is a disclosure-driven market regulator, it relies on transparency, governance and informed investor choice. RBI is a prudential regulator tasked with protecting systemic stability, and therefore imposes capital buffers, exposure limits and stricter supervision. Private credit AIFs operate within SEBI’s lighter, disclosure-based approach, while banks and NBFCs function under RBI’s risk-averse framework. This does not always create arbitrage, but it does allow credit activity to grow outside the prudential perimeter. As private credit scales, a coordinated SEBI-RBI framework may be necessary to preserve flexibility without compromising financial stability.

It is important to recognise that Category I and Category II AIFs are prohibited from taking long-term leverage. As a result, any loss arising from their lending or investment exposures does not cascade into the wider financial system. Therefore, concerns around applying capital adequacy requirements to these AIF categories are largely unwarranted.

Conclusion

Though still a small fragment of India’s wider corporate lending landscape, private credit AIFs are steadily gaining ground reaching those nooks and crannies of credit demand that banks and NBFCs often cannot, or would not, serve. Their ability to operate beyond the traditional comfort zone of regulated lenders is what makes this segment structurally relevant and increasingly attractive to borrowers and investors alike.

At the same time, rapid expansion brings the potential for regulatory arbitrage. The RBI has already acknowledged this risk, most notably through its actions on evergreening via AIF structures, ultimately resulting in exposure caps of 10% for individual regulated entities and 20% collectively, along with mandatory full provisioning where exposure exceeds 5% in an AIF lending to the same borrower. These measures serve as guardrails to prevent private credit vehicles from functioning as an indirect tool for evergreening of loans.

A middle-market firm is a firm that is typically too small to issue public debt and requires financing amounts too large for a single bank because of its size and risk profile. The size of middle-market firms varies widely. In the United States, they are sometimes defined as businesses with between $100 million and $1 billion in annual revenue. ↩︎

Payment-in-kind (PIK) is noncash compensation, usually by treating accrued interest as an extension of the loan. ↩︎

See our other resources of Alternative Investment Funds here

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-12-02 11:01:512026-01-07 14:56:59Private Credit AIFs: Lenders of Last Resort?

Operational risk, as defined by the Basel framework, refers to the possibility that a financial institution’s routine operations may be disrupted due to failures in processes, systems, people, or external events. While historically treated as secondary to credit and market risk, it has increasingly become a central focus of risk management, particularly for institutions with complex operations, heavy technology dependence, extensive outsourcing, and stringent regulatory obligations. Reflecting this shift, the RBI’s 2024 Guidance Note on Operational Risk Management and Resilience expands its expectations for operational risk management to all NBFCs.

Having previously discussed the guidance note (refer here), this article now explains the fundamentals of operational risk assessment and outlines its process.

Operational Risk Management

Operational risk poses unique challenges because many of the events that cause losses arise from internal factors, making them difficult to generalise or predict. Large operational losses are often viewed as rare, which can make it difficult to get sustained management attention on the steady, routine work required to identify issues and track trends1. Operational risks typically stem from people, processes, systems and external events, ironically, the same resources essential for running the business. Unlike credit and market risk which are modelled and hedged, operational risks are often idiosyncratic, event-driven and subject to human, process and system failure.

Relevance For Financial Institutions

Financial institutions operate with complex processes, large transaction volumes, strict regulatory reporting requirements and often heavy dependence on technology, outsourcing arrangements and third-party service providers. Because of this, operational failures, such as system glitches, fraud, compliance breaches or breakdowns in business continuity, can result in substantial financial losses, regulatory sanctions, reputational harm and other disruptions to business operations.

Given these risks, regulators have placed growing emphasis on the measurement and management of operational risk. Based on our experience, RBI has frequently raised queries regarding the operational risk frameworks of NBFCs during its supervisory inspections. Under Basel II, for instance, banks using the Advanced Measurement Approach were required to maintain strong, demonstrable operational risk management systems. Recognising the importance of operational risk, the Bank of England’s FSA0732 report, which is applicable on banks and large investment firms, requires firms to record the top ten operational risk loss events for each reporting year. This provides a clear view of what went wrong, where it occurred and the scale of the financial impact.

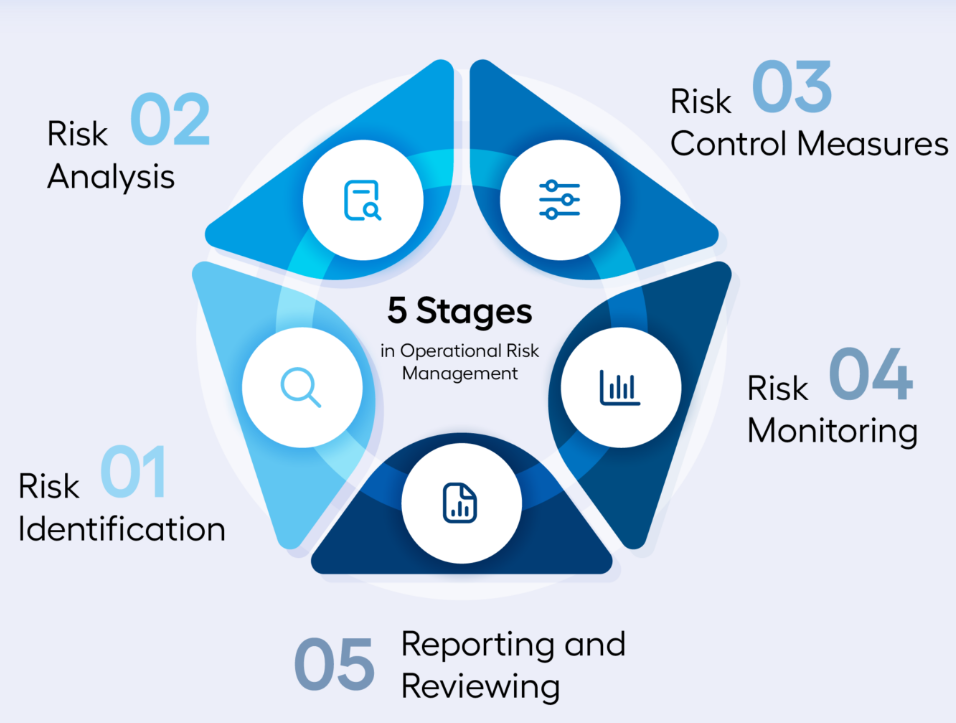

Operational Risk Assessment Process

In its guidance note for operational risk, RBI at many places underscored the importance for risk assessment. One such example is given below:

Principle 6: Senior Management should ensure the comprehensive identification and assessment of the Operational Risk inherent in all material products, activities, processes and systems to make sure the inherent risks and incentives are well understood. Both internal and external threats and potential failures in people, processes and systems should be assessed promptly and on an ongoing basis. Assessment of vulnerabilities in critical operations should be done in a proactive and prompt manner. All the resulting risks should be managed in accordance with operational resilience approach.

6.1 Risk identification and assessment are fundamental characteristics of an effective Operational Risk Management system, and directly contribute to operational resilience capabilities. Effective risk identification considers both internal and external factors. Sound risk assessment allows an RE to better understand its risk profile and allocate risk management resources and strategies most effectively.

Figure 1: Operational Risk Assessment Process

Risk identification

Risk identification means figuring out what exactly you need to assess. It involves recognising the different risk sources and risk events that may disrupt your business. A risk source is the underlying cause, something that has the potential to create a problem. A risk event is when that problem actually occurs. For example, a weak password is a risk source, while a data breach caused by that weak password is the risk event.

As per the RBI’s Guidance Note, REs are expected to take a comprehensive view of their entire “risk universe”. This means identifying all categories of risks, traditional or emerging, that could potentially affect their operations. These may include insurance risk, climate-related risk, fourth- and fifth-party risks, geopolitical risk, AML and corruption risk, legal and compliance risks, and many others. The underlying expectation is simple: an RE should systematically identify everything that can go wrong within its business model, processes, people, systems, and external dependencies, and ensure that no material source of risk is overlooked.

There are many ways to identify risks. You may use questionnaires, self-assessments by business or functional heads, workshops with staff involved in risk management, or you may review past failures within the company. Industry reports, experiences of peers, and linking organisational goals to potential obstacles can also reveal important risks. You can even look at upcoming strategic initiatives and think ahead about the risks that may arise when these changes are implemented.

Every organisation has its own risk profile. A lender may worry about borrowers not repaying, untrained staff, biases in an AI underwriting model, IT system failures, employee fraud, or suppliers not delivering on time. These risks should be recorded in a risk register, but it is important that this register reflects your business. A company offering only physical loans may not face digital lending risks, and should not simply copy any generic list. The goal is to identify risks that genuinely matter to your day-to-day operations.

Assessment

Once you know which risks matter, the next step is to assess each of them. For every risk, ask yourself two basic questions:

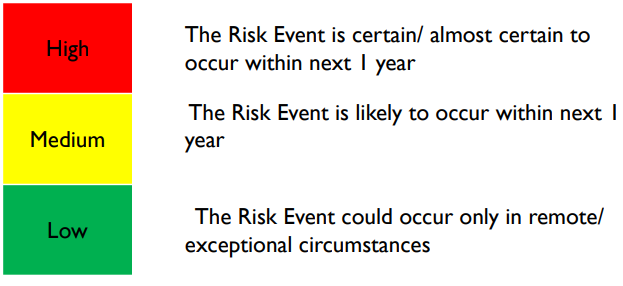

What is the likelihood of this risk actually happening? This is simply the chance that the event might occur; You may assign parameters to determine the likelihood – for eg if the risk event is almost certain to occur in the next 1 year or is it likely to occur or it will occur only in remote situations?

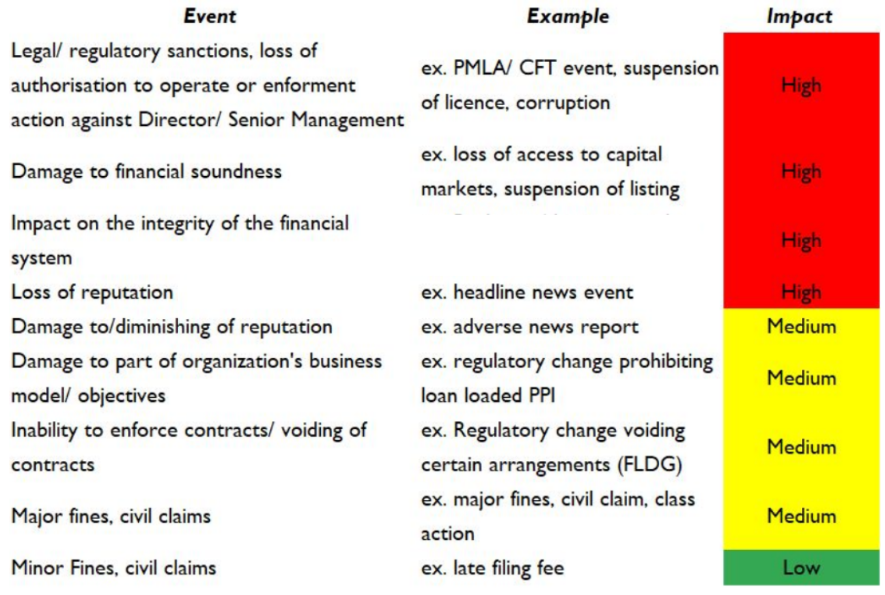

If it does happen, what impact will it have on my organisation? Will it hurt my reputation? Lead to financial loss? Negative feedback from customers? Cause a data leak? One can record the impact of the risk as High, medium or low based on its gravity

Figure 3: Illustrative impact assessment of risks

These two questions help you understand how serious the risk is inherently (inherent risk level) i.e, before considering whether you have any controls in place. Note that at this stage, you’re only interested in the natural level of risk that exists ignoring any controls you might already have.

Evaluating Controls

Once the inherent risks are understood, the next step is to look at how these risks are currently being managed. These risk-reducing efforts are your controls or mitigation measures. Controls are simply the actions, checks, or processes already in place to lower the likelihood or impact of a risk. For example: Is your underwriting model checked for bias? Are board committees meeting regularly? Do you have proper maker–checker checks in your V-CIP process? Controls can take many forms such as policies, procedures, tools, system checks, reviews, or even day-to-day practices followed by employees. In essence, a control is any measure that maintains or modifies risk and helps the organisation manage it more effectively.

Residual Risk

After evaluating the controls, you can determine the residual risk i.e. the level of risk that remains even after your mitigation measures have been applied. Residual risk shows whether the remaining exposure is acceptable or whether additional controls are needed. By definition, residual risk can never be higher than inherent risk. Generally, residual risk can be interpreted as follows:

Low Residual Risk: When the effectiveness of internal controls fully covers or even exceeds the inherent risk;

Medium Residual Risk: When controls reduce most of the risk, leaving only a small gap;

High Residual Risk: When controls address only part of the risk and a significant gap still remains;

Category

Risk Source

Risk event

Root cause

Likelihood

Consequence

Level of inherent risk

Control Effectiveness

Level of Residual Risk

People Risk

Employees / Staff

Employee fraud, misappropriation, or collusion

Weak internal controls, poor background checks

Highly Likely

Medium

High

Weak

HIGH

Information Technology & Cyber Risk

IT Infrastructure / Systems

System downtime or core platform failure

Server outage, inadequate IT resilience

Possible

Low

Low

Strong

LOW

Process & Internal Control Risk

Onboarding / KYC Processes

Non-compliance with KYC or onboarding procedures

Inadequate verification, manual errors

Possible

High

High

Adequate

MEDIUM

Legal & Compliance Risk

Outsourcing / LSP Arrangements

Non-compliance in outsourcing / LSP arrangements

Weak SLA oversight, inadequate due diligence

Unlikely

Low

Low

Adequate

LOW

External Fraud Risk

Borrowers / External Parties

Borrower fraud – identity theft, fake borrowers, or collusion

Forged documents, weak KYC

Possible

Low

Low

Strong

LOW

Model / Automation / Reporting Risk

Data Aggregation / Systems

Failure in data aggregation across systems for regulatory returns

System inconsistencies, poor data governance

Highly Likely

Medium

High

Strong

LOW

Reputation Risk / Customer Experience

Customer Communication / Sales Practices

Miscommunication of terms or conditions to customers

Poor training, unclear communication scripts

Possible

Medium

Medium

Weak

MEDIUM

Figure 5: An illustrative Snapshot of Operational Risk Assessment

Understanding residual risk helps decide where further action is required and where the organisation may still be vulnerable.

Conclusion

The goal, therefore, is to move away from a simple “tick-box” approach and make the operational risk assessment truly tailored to the organisation. For ML and above NBFCs, the ICAAP requirement to set aside capital for operational risk is useful, but it covers only a narrow part of what operational risk really involves. A comprehensive assessment goes much further by examining the strength of the entity’s internal controls and how effectively they manage real-world risks. If the residual risk exceeds the organisation’s tolerance level, it should trigger a closer look at those controls and prompt corrective action. Ultimately, the focus should be on building a risk framework that is meaningful, proactive, and aligned with how the organisation actually operates. The ultimate goal is therefore to develop ‘operational resilience’ which as per Bank of England3 is the ability of firms and the financial sector as a whole to prevent, adapt, respond to, recover from, and learn from operational disruptions.

Call it Trump relief! The RBI announced relief measures on the 14th Nov to help the exporters of certain specified items, who may have availed export credit facilities from a regulated lender, whereby all regulated entities (REs) “may” provide a moratorium, from 1st September 2025 to 31st December, 2025. The grant of such a relief shall be based on a policy, consisting of the criteria for grant of the subject relief, and such criteria shall be disclosed publicly. Not only this, REs shall also make a fortnightly disclosure of the reliefs granted to eligible borrowers on a RBI format on Daksh portal.

The Reserve Bank of India (Trade Relief Measures) Directions, 2025 (‘Directions’) are applicable to NBFCs and HFCs as well. This is accompanied with amendment to Foreign Exchange Management (Export of Goods and Services) (Second Amendment) Regulations, 2025 for extension of the period for both realization/repatriation of export value (from 9 to 15 months) and the shipment of goods against advance payment (from 1 to 3 years).

Highlights:

Whether your company grants an export credit or not, if your borrower is the one who has availed export credit for export of specified goods or services, the borrower may approach you for the moratorium.

Are you bound to grant the moratorium? Answer is, no. However, basis a policy which is publicly hosted, you will consider the eligibility of the borrower. The relevant factors on which the eligibility will be examined may also form a part of the policy, and ideally, should include the extent of dependence on exports of specified items to the USA, tariff-based disruption in the cashflows, alternative markets and transitioning possibilities, etc.

Effective: Immediately.

Actionables: (a) Framing of policy to consider the eligibility of affected borrowers; (b) Hosting the policy on public website; (c) Creating mechanism for receiving and transmission of borrower requests for the moratorium and giving timely responses to the same (d) RBI fortnightly reporting.

What is the intent?

To mitigate the disruptions caused by global headwinds, and to ensure the continuity of viable businesses.

Tariff impositions by the USA are likely to impact several exporters. There may be a ripple effect on penultimate sellers or other segments of the economy as well, but the intent of the Trade Relief Directions seems limited to the direct exporters only.

Which all regulated entities are covered?

The Directions are applicable to following entities:

Commercial Banks

Primary (Urban) Co-operative Banks, State Co-operative Banks and Central Co-operative Banks

NBFCs

HFCs

All-India Financial Institutions

Credit Information Companies (only with reference to paragraph 16 of these Directions).

Does it matter whether the RE in question is giving export credit facilities or not? In our view, it does not matter. The intent of the Directions is to mitigate the impact of trade disruptions. Of course, the borrower in question must be an exporter, must have an export credit facility outstanding as on 31st Aug 2025, and the same must be standard.

If these conditions are met, then the RE which holds the export credit, as also other REs (of course, the nexus between the trade disruption and the servicing of the credit facility will have to be seen) should consider the borrower for the purpose of grant of relief.

Relief may or may not be granted.

Policy on granting relief

The consideration of the grant of relief will be based on a policy.

Below are some of the brief pointers to be incorporated in the policy:

Purpose and Scope: define which loan products, sectors, or borrower categories are covered; effective period for granting relief

Eligibility Criteria for borrowers

Assessment criteria for relief requests received from the borrowers

Authority responsible for approving such request

Relief measures that can be offered to borrowers

Impact on asset classification and provisioning

Disclosure Requirements

Monitoring and Review: Authority which is responsible for monitoring such accounts; periodicity of review

How is the assessment of eligible borrowers to be done?

In our view, the relevant information to be obtained from the candidates should be:

Total export over a relevant period in the past, say 3 years

Break up of export of “impacted items” and other item

Of the above, exports to the USA

Gross profit margin

Impact on the cashflows

Information about cancellation of export orders from US importers

Any damages or other payments receivable from such importers

Any damages or other payments to be made to the penultimate suppliers

Alternative business strategies – repositioning of markets, alternative buyer base, etc

Cashflow forecasts, and how the borrower proposes to pay after the Moratorium Period.

What sort of lending facilities are covered?

Please note the following from the preamble: “mitigating the burden of debt servicing brought about by trade disruptions caused by global headwinds and to ensure the continuity of viable businesses”. Therefore, clearly, the relief intended here is one where “trade disruptions” create such a burden on debt servicing, which may impact the viability of the business.

From this, it implies that the entity in question must be a business entity, and the loan in question should be a business loan.

In our thinking, the following facilities seem covered:

Export credits of all forms, including packing credit, funded as well as unfunded, letters of credit, etc.

Buyer’s credit or facilities for inward acquisitions/purchases by an exporter

Cash credits, overdrafts or working capital related facilities, intended for export business of impacted items.

Term loans relating to an impacted business

Loans against property, where the end use is working capital

Eligible and ineligible borrowers:

Eligible borrowers:

Borrowers who have availed credit for export

Borrower had an outstanding export credit facility from a RE as of August 31, 2025 (However, in case the borrower has a sanctioned facility pending disbursement as on Aug 31, the same shall not be eligible)

Borrower with all REs was/were classified as ‘Standard’ as on August 31, 2025

In our view, the following borrowers/ credit facilities are not eligible for the relief:

Individuals or borrowers who have not borrowed for business purposes

Home loans or loans against specific assets or cashflows, where the debt servicing is unconnected with the cash flows from an export business

Loans against securities or against any other financial assets

Gold loans, other than those acquired for business purposes

Car loans, loans against commercial vehicles or construction equipment, unless the borrower is engaged in export business and the cashflows have a nexus with such business

Borrower is engaged in exports relating to any of the sectors specified

Borrower accounts which were restructured before August 31, 2025

Accounts which are classified as NPA as on August 31, 2025

Consider a borrower who is not an exporter himself, but an ancillary supplier, supplying to a trading house. Will such a penultimate exporter be covered by the Relief Directions? In our view, the answer is negative, as the “eligible borrowers” are defined to mean an exporter.

Impacted items and impacted markets

The list of impacted items broadly covers a wide spectrum of manufacturing and export-oriented sectors, including marine products, chemicals, plastics, rubber, leather goods, textiles and apparel, footwear, stone and mineral-based articles, jewellery and precious metals, metal products, machinery, electrical and electronic equipment, automobiles and auto components, medical and precision instruments, and furniture and furnishing items.

Is it mandatory that the borrower shall be exporting to USA? While the Directions do not specifically mandate that the borrower shall be exporting to the USA, the concerned REs should, as part of their assessment, evaluate whether the borrower genuinely requires such relief measures and, in our view, should consider the extent to which the borrower depends on exports of the specified items to the USA.

Why have HFCs been covered?

Generally speaking, the servicing of home loans is not supposed to be based on business cashflows, and therefore, the impact of trade disruptions on servicing of a home loan does not seem easy to establish.

However, HFCs grant other credit facilities too, including LAP or business loans. Therefore, there is no carve out for HFCs as such. HFCs are also expected to prepare the policy referred to above and be sensitive to requests from impacted borrowers.

Is the moratorium retrospective?

Yes, clearly, the moratorium is retrospective, as it covers the period from 1st September to 31st December. This is the range over which the moratorium may be granted; of course, the decision as to how much moratorium, within the above maximum range, is warranted in the particular case, is that of the lender. Let us call the agreed moratorium as the Moratorium Period.

If the moratorium is granted from 1st Sept., then any payments which were due for the period covered by the Moratorium Period will not be taken as having fallen due. This will have significant impact on the loan management systems:

Considering that we are already in the middle of November, the day count for any payments due during the part of the Moratorium Period will be set to zero. In other words, day count will stop during the Moratorium Period. Thus, if an account was showing a DPD status of 60 days as on Aug 31, 2025, the DPD count will remain at a standstill till the moratorium period is over.

However, in case a borrower has made payment during the moratorium period, will the DPD count decrease or will it remain the same?

The RBI Directions state that the days past due (DPD) count during the moratorium period will be excluded. However, this does not imply that a borrower who makes payments during this period should be denied the corresponding benefit. In our view, if a payment is received from the borrower, the DPD count should accordingly be reduced.

Any payments already made during the part of the Moratorium Period already elapsed may be taken towards principal, or may be held to be adjusted against the future dues of the borrower, after the Moratorium Period. This should also, appropriately, be captured in the policy.

Further, for accounts for which the CIC reporting has already been done on or after Aug 31, 2025, and the lender decides to extend the moratorium benefit, it must be ensured that the DPD count is revised so as to reflect the status as on Aug 31, 2025.

Do lenders have to necessarily grant moratorium, or grant partial interest/principal relief?

The RBI Directions do not mandate REs from granting such relief measures. Accordingly, the concerned RE will need to assess individual cases based on the sectors, the need for such relief and the extent to which such relief may be granted.

Lenders may grant full moratorium during the Moratorium Period, or may grant relief as may be considered appropriate.

Do lenders take positive actions, or simply respond to borrower requests?

The lenders must establish a policy for granting such relief measures prior to extending any relief, as the authority to do so will be derived from this policy. As discussed above, the discretion to grant relief rests with the concerned RE; therefore, each request submitted by a borrower must be evaluated on an individual basis.

For this purpose, the following information must be obtained from the borrowers seeking relief:

The concerned sector and how the same has been impacted necessitating such relief

Information relating to the current financial condition of the business of the borrower

Facilities taken and outstanding with other REs

Non-compounding of interest during the Moratorium Period:

Para 9 (iii) provides that while interest will accrue during the Moratorium Period, but the interest shall be simple, that is, shall not be compounded.

This may require REs to tweak their loan management systems to stop the compounding of interest during the Moratorium Period.

However, the actual population of affected borrowers for a particular RE may be quite limited. Hence, REs may do manual or spreadsheet-based adjustments for affected borrowers, instead of making adjustments to their LMS itself.

Recomputation of facility cashflows after Moratorium:

During the moratorium period, as per the RBI directive, the lender can only accrue simple interest. Accordingly, the IRR of the credit facility will have a negative impact unlike the covid moratorium where the compound interest loss was compensated by the central government.

Further, it has also been provided that the accrued interest may be converted into a new term loan which shall however be repayable in one or more installments after March 31, 2026, but not later than September 30, 2026. Accordingly, the accrued interest should anyhow be received by September 30, 2026.

Similar moratoriums in the past

Moratorium on loans due to COVID-19 disruption: Refer to our write-up here.

Moratorium 2.0 on term loans and working capital: Refer to our write-up here.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-11-15 11:57:082025-11-15 13:49:41RBI Trade Relief Directions: How is your company impacted?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-11-13 17:16:502025-11-27 11:52:53Virtual Certificate Course on Grooming of Chief Compliance Officers of NBFCs

Co-lending is an arrangement where two or more regulated entities (REs) jointly extend credit to a borrower under a pre-agreed Co-Lending Agreement (CLA). The CLA, signed before origination, defines borrower selection criteria, product lines, operational responsibilities, servicing terms and the proportion in which each lender will fund and share the loan. The aim is to combine the origination strength of a RE with the lower cost of funds of another RE, thereby expanding credit outreach.

Before the issuance of the RBI (Co-Lending Arrangements) Directions, 2025 (‘Directions’), there was no formal co-lending framework for non-PSL loans and for PSL loans, the CLM-2 ‘originate-and-transfer’ model was the most common structure. Under this model, the originating RE would book 100% of the loan in its books and, within a stipulated period, selectively transfer a portion to the funding partner. This post-origination discretion enabled ‘cherry-picking’ of loans. CLM-2 mirrored a loan sale under TLE framework but without any minimum holding period restrictions, making it a preferred route. It offered the economic and accounting benefits of transfer, including derecognition and upfront gain recognition without waiting for loan seasoning.

Upon transfer, the originating RE would derecognise the transferred portion and book ‘upfront gains’. The upfront gain arose from the excess spread between the interest rate charged to the borrower and the yield at which the loan pool was transferred to the funding partner. For example, if the originating RE extended loans at 24% and sold down 80% of the pool at 18%, the 6% differential represented the excess spread. This spread, which would otherwise have been earned over the life of the loan, was discounted to present value and recognised as gain on transfer upfront, at the time of derecognition. This led to the originating RE recognising profits immediately despite not receiving any actual cash on the co-lent loans. This practice allowed originating REs to show higher profits upfront, even though no cash had actually been received on the co-lent loans.

The Directions fundamentally alter this framework as well as the prevalent market practice. They move away from originate-and-transfer and institute a pure co-origination model. It has been expressly stated that The CLA must now be executed before origination, with borrower selection and product parameters agreed ex ante. The funding partner must give an irrevocable commitment to take its share on a back-to-back basis as loans are originated. Importantly, the 15-day window provided under the Directions is only for operational formalities such as fund transfers, data exchange and accounting. It is not for evaluating or selecting loans after origination. If the transfer does not occur within 15 days due to inability, not discretion, the originating RE must retain the loan or transfer it under the securitisation route or as per Transfer of Loan Exposure framework. In short, post-origination cherry-picking is no longer permitted.

This change has direct accounting consequences. Under Ind AS 109, a financial asset is recognised only when the entity becomes a party to the contractual provisions and has enforceable rights to the underlying cash flows (see para 3.1.1 and B3.1.1). In a co-lending transaction under the Directions where co-origination is a must, each lender should recognise only its respective share of the loan at origination. The originating partner should not recognise the funding partner’s share at any stage, except as a temporary receivable if it disburses on behalf of the funding partner. Since the originating partner never recognises the funding partner’s share (except as a servicer), there is no recognition and therefore, there is no question of any subsequent derecognition and booking of any gain on sale. Income, if any, is limited to servicing fees or mutually agreed charges, not upfront profit.

By eliminating post-origination discretion, RBI has closed the upfronting route. Co-lending is now truly co-origination, joint funding from day one, with proportionate recognition and no accounting arbitrage. The practice that once allowed REs to accelerate income has been uprooted.

Click here to see our other resources on co-lending

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-10-31 16:05:382025-11-01 14:41:15Upfronting Uprooted: RBI puts an end to early profit booking in Co-lending

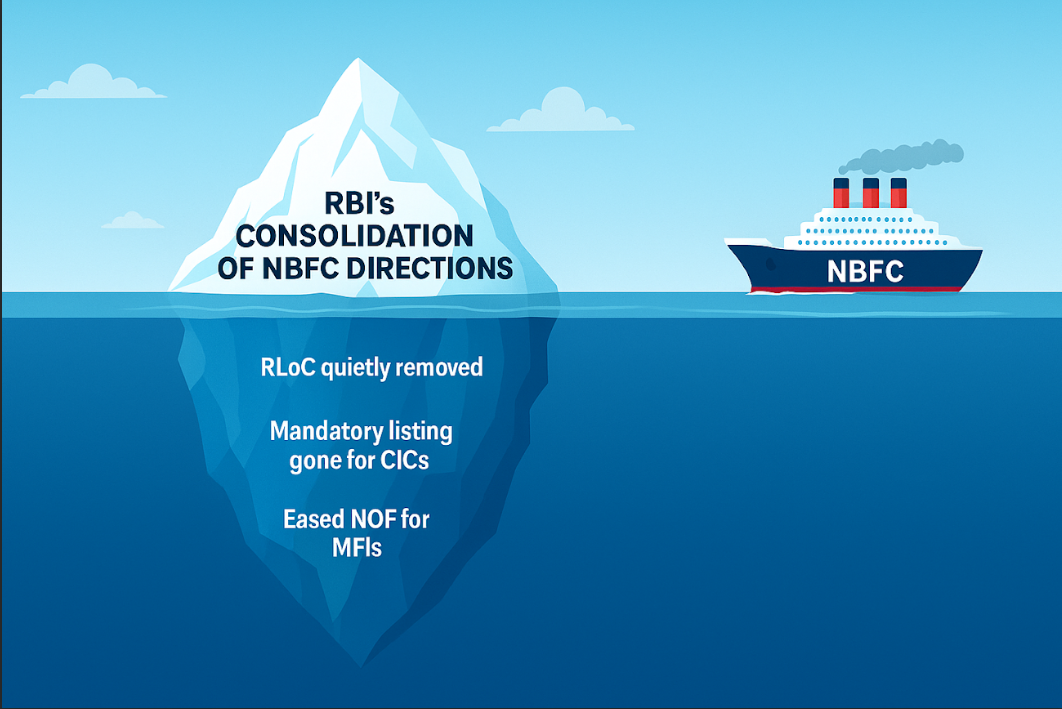

In its recent consolidation exercise of the Master Directions applicable to NBFCs, the RBI has done a lot of clause shifting, reshuffling, reorganisation, replication for different regulated entities, pruning of redundancies, etc. However, there are certain places where subtle changes or glimpses of mindset may have a lot of impact on NBFCs. Here are some:

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-15 15:11:142025-10-15 19:01:29The Great Consolidation: RBI’s subtle shifts; big impacts on NBFCs