Representation on the draft Amendment Directions for exemption from registration to eligible NBFCs

Loading…

Loading…

Loading…

Loading…

Vinod Kothari & Chirag Agarwal | finserv@vinodkothari.com

RBI had earlier directed NBFCs to compute expected credit loss (ECL) without considering the impact of any default loss guarantees (DLGs) obtained from its lending service provider (LSP). We had published a short note explaining why this position was debatable (See our article on the topic here) and had also made a formal representation to RBI on the issue.

Back to the present, RBI has issued an amendment to the IRACP Directions, 2025 (dated February 13, 2026), permitting lenders to factor in DLG while determining provisions under the ECL framework across all stages.

Further, RBI has also specified that upon every event of invocation of DLG, the DLG cover reduces to the extent of invocation. Accordingly, REs shall recompute their ECL provisioning requirements across stages, after duly adjusting for the reduced DLG cover.

With these clarifications now in place, the next question that arises is: How should Regulated Entities (REs) appropriately factor DLG into their ECL computations? The article below discusses the above question at length.

Let us understand this in simple terms. Suppose a lender estimates that the expected loss on a loan pool is 3.8%. If the lender has received a guarantee of 5%, backed by fixed deposits that are lien-marked in its favour. The guarantee is sufficient to cover the expected loss. In such a case, effectively, the lender does not expect to bear any loss. On the other hand, if the expected loss is 6.8% and the guarantee covers only 5%, then the lender’s net expected loss would be the balance 1.8%.

However, this adjustment assumes that the guarantee will actually be honoured when required. A guarantee does not, however, eliminate risk completely; it merely shifts the risk of default or loss from the borrower to the guarantor, up to the guaranteed amount.

The DLG guidelines specify the forms in which a DLG can be obtained. DLG can be accepted in any one of the following forms:

Accordingly, DLG can only be obtained in fully funded forms, thus eliminating any question of incurring credit loss on such a guarantee. Does that mean that even in case of insolvency of the DLG provider the lender will have the right to invoke the guarantee? The answer to this is negative. Because unlike in the case of bankruptcy-remote SPV, the guarantor is an operating entity, and is prone to the risk of insolvency.

In case of initiation of insolvency proceedings, all the assets of an insolvent entity form part of the insolvency administration/liquidation estate and are beyond the reach of the creditors. The proceeds from the realisation of assets are paid to the creditors in accordance with the waterfall mechanism as specified under section 53 of the IBC, 2016 .

Accordingly, it becomes important to determine how each permitted form of DLG would be treated in the event of insolvency of the DLG provider.

So, even if the DLG is structured as a funded guarantee, the actual invocation can become complicated if the DLG provider goes into insolvency before such invocation. In such a situation, the lender may not be able to simply invoke the guarantee and take the money. Instead, it may have to submit its claim and wait for distribution under the insolvency process, where payments are made in the statutory priority order.

Under the waterfall mechanism, secured creditors rank alongside workmen’s dues. Now, in most DLG structures, the guarantor is a fintech entity or a co-lender. These entities typically do not have significant workmen-related liabilities. This may mean that the lender’s priority position is relatively stronger.

Further, the actual invocation process of the DLG should also be considered. For instance, cash held with the lender can be easily invoked and adjusted as compared to a lien-marked FD or bank guarantee, where there could be procedural delays.

Illustration: Consider a loan pool of ₹100 crore where the gross ECL rate is estimated at 6.8% (for the static pool covered by the guarantee), resulting in a gross ECL of ₹6.8 crore. The lender has a DLG cover of 5% of the pool (₹5 crore), structured as a lien-marked fixed deposit provided by a fintech sourcing partner. While the DLG is funded, there remains a risk that the guarantor may become insolvent. The first relevant question here is whether we will take a probability of default (PD) as per Stage 1 (12 months PD), or Stage 2/3 (lifelong PD). While the guarantor in question is not in default at all, however, given that the 6.8% ECL is a combination of Stage 1 as well as Stage 2/3 loans, in our view, the PD for the guarantor, to remain conservative, should be the lifelong PD over the tenure of the loans. Let us assume a 20% Probability of Default (PD) for the guarantor. Next question is assessment of Loss Given Default (LGD). As discussed above, the lender has the benefit of full security in form of lien on the fixed deposit, however, there may be depletion of the same on account of first priority in the waterfall, that is, costs of insolvency and bankruptcy process. On a conservative basis, we may, therefore, assume a 10% LGD. Thus, the expected loss on the DLG cover would therefore be 20% × 10% = 2%.

As a result, the ECL computation may now be:

= 5%*2% + 1.8% = 1.9%

Based on the aforesaid discussion, in our view, while the guarantee is funded the lender may have to adjust the probability of default to factor in the risk of insolvency, particularly where the guarantee is funded in the form of a cash deposit or a lien marked FD.

Which funded form of DLG is most suited?

As per the analysis, the various options of funded DLG can be ranked basis the maximum consideration allowable for ECL computation:

However, given that there will not be a sizable or material difference in the quantum of counter guarantee risk, the selection of the options for ECL computation may not be significant.

One of the ways to mitigate the risk of insolvency is by structuring the guarantee in such a way that the guarantee may be invoked upon the occurrence of an adverse material change in the financial condition of the guarantor. In other words, other than the occurrence of losses in the pool, if there are events of default such as adverse material change, insolvency of the guarantor etc., the lender may invoke the guarantee.

Early invocation upon identifiable stress on the part of the guarantor could help the lender realise the guarantee amount before the commencement of insolvency proceedings.

However, such clauses must be appropriately incorporated and drafted in the DLG agreement to ensure the following:

RBI has also provided a clarification that upon every event of invocation of DLG, the DLG cover reduces to the extent of invocation. Accordingly, REs would be required to recompute their ECL provisioning requirements across stages, after duly adjusting for the reduced DLG cover.

Pool-based guarantees presuppose that the pool is static. This is purely intuitive because if the pool is dynamic, new loans will continue to enter the pool, and therefore, the guarantor’s exposure will keep spreading over a continuing flow of new loans.

Where the pool is static, the loans gradually get repaid (amortised) over time. As borrowers repay their instalments, the outstanding amount of the loan pool keeps reducing. Since the exposure is shrinking, the ECL on that pool will also typically reduce over time, assuming normal performance. Therefore, whether the utilisation of the DLG on account of pool defaults may cause the ECL computation to increase? This may be so for 2 reasons: one, usual terms of DLG invocation will be the full amount of the defaulted loan will be recovered (due to escalation of the entire principal outstanding). Thus, while the performing loans amortise over time, the non-performing loans are fully recovered once they reach “default”, causing the utilisation of the DLG to run faster than the amortization of the performing loans. Second reason is that once the pool actually starts defaulting, there may be a reason to provide higher estimates of probability of default as well.

Para 36A of the IRAC Directions read with the principles under Ind AS 109 provides that credit enhancements may be considered while computing ECL only where such enhancements are “integral to the contractual terms.” The expression “integral to the contractual terms” is taken from the definition of “credit loss” in Ind AS 109. Credit losses are measured after considering the expected cashflows from an asset. Those cashflows will factor in the recovery of any collateral, or credit enhancements, as long as the said credit enhancement is integral to the contractual terms.

What exactly is the meaning of “integral to the contractual terms”? Are we expecting the guarantee (DLG in the present case) to be a part of the terms of the loan contract? That would never be the case, as the so-called guarantee (which may legally be regarded as an indemnity contract) is a bilateral contract between the lender and the DLG provider. Neither is the borrower aware of the guarantee, nor is it desirable to have the borrower know of the guarantee, for obvious reasons.

IFRS 9 uses the same language. US ASC has more elaborate discussion on this. Para 326-20-30-12 says:

The estimate of expected credit losses shall reflect how credit enhancements (other than those that are freestanding contracts) mitigate expected credit losses on financial assets, including consideration of the financial condition of the guarantor, the willingness of the guarantor to pay, and/or whether any subordinated interests are expected to be capable of absorbing credit losses on any underlying financial assets. However, when estimating expected credit losses, an entity shall not combine a financial asset with a separate freestanding contract that serves to mitigate credit loss. As a result, the estimate of expected credit losses on a financial asset (or group of financial assets) shall not be offset by a freestanding contract (for example, a purchased credit-default swap) that may mitigate expected credit losses on the financial asset (or group of financial assets)

There has been a significant discussion on whether the benefit of a guarantee or credit enhancement which is not a part of the contractual terms of the loan can be factored in ECL computation. From discussions before the IASB, as back as in 2018, two conditions for recognising the benefit of credit enhancements were discussed:

The second condition is easy to understand. For example, if the risk of default is hedged by a credit default swap, the value of the same, amounting to a derivative, is separately recognised. Hence, the question of factoring the same while computing ECL does not arise. However, the first condition, relating to contractual terms of the asset, still remains vague.

One may try to get some clues in the US FASB discussions, where para 326-20-30-12 has been interpreted in technical interpretations. In addition, there is a definition of “freestanding contracts” under the Glossary of ASC 326:

A freestanding contract is entered into either:

a. Separate and apart from any of the entity’s other financial instruments or equity transactions

b. In conjunction with some other transaction and is legally detachable and separately exercisable.

The “forming integral part of the contractual terms” does not warrant the principal contract to provide for the guarantee or the credit enhancements. Insisting on the same will be counter-intuitive, except in case of trilateral contracts. However, the conditions indicate that the guarantee or credit enhancement integrates and becomes an inseparable part of the underlying loan or group of loans. For example, if the group of loans was to be transferred, is it such that the benefit of the guarantee may stay iwth the originator and loans may be transferred, or the guarantee travels along with the loans? If the latter is the case, there is no doubt that in reality, the guarantee has become an embedded part of the loan transaction.

Another factor may be the contractual association between the loan cashflows and the payout from the credit enhancements. Some relevant considerations:

The presence of these factors will suggest the integration or embedding of the guarantee into the contractual cashflows from the loans.

While the recent amendment by the RBI brings welcome clarity by allowing DLG to be factored into ECL computation, lenders must approach this carefully and realistically. A DLG can reduce the expected loss, but it does not make the risk disappear, as the DLG provider itself faces the risk of insolvency. The form of the guarantee, its enforceability, and the possibility of invocation- all of these matter in assessing the true level of protection. REs should not treat DLG as a mechanical deduction from ECL, but as a risk mitigant that requires thoughtful evaluation, continuous monitoring, and recalibration as the pool amortises and the cover reduces.

See our other resources:

Tejasvi Thakkar and Simrat Singh | Finserv@vinodkothari.com

Pursuant to the RBI’s stated intent in the Statement on Developmental and Regulatory Policies to harmonise the conduct of Regulated Entities in relation to loan recovery, comprehensive draft instructions have been proposed, to be effective from July 1, 2026, consolidating and rationalising the existing scattered provisions. The instructions are applicable to all NBFCs, excluding Mortgage Guarantee Companies, Core Investment Companies, NBFC-Account Aggregators, Standalone Primary Dealers, Non-Operating Financial Housing Companies, and NBFCs not having any customer interface. The key requirements of the proposed framework are summarised below:

REs shall formulate a separate policy on recovery of loan dues, engagement of recovery agents and taking possession of security. The policy shall, inter-alia, cover:

Issue: Whether this can be combined with the policy on Code of Conduct for DSAs/DMAs?

Our view: Since the present requirement specifically deals with recovery conduct, possession and enforcement of security interest, and engagement of recovery agents, the same should ideally be maintained as a separate policy. The DSA/DMA CoC policy deals largely with sourcing-stage conduct such as mis-selling and consequent compensation-related aspects. However, where there are overlapping requirements, NBFCs may structure the same within a broader conduct framework, divided into separate sections. However, it should remain distinct from the outsourcing policy.

Issue: Whether the CoC prescribed earlier under HFC Directions stands subsumed?

Our view: Yes. The earlier HFC provisions largely stand harmonised and subsumed within the present draft framework, except for certain differences which have been captured in the Annexure below.

Recovery agents shall be required to carry recovery notice, identity card and authorisation letter, and shall adhere to the following conduct requirements:

REs shall:

Loan agreements shall contain a legally enforceable possession clause, clearly disclosed at the time of execution. The agreement shall, inter alia, specify:

REs shall put in place a management structure to monitor and control the activities of recovery agents and ensure that such agents refrain from actions that could harm the RE’s integrity and reputation. Accordingly, the RE should ensure:

Most of the proposed requirements are not entirely new in substance for HFCs, as they were already reflected in the Guidelines for Engaging Recovery Agents under paragraph 170 of the RBI HFC Directions, 2025. The proposal now is to delete those HFC-specific guidelines and require HFCs to comply with the proposed Directions.

However, while the underlying principles remain largely consistent, the proposed Directions significantly strengthen and formalise the recovery framework. The approach shifts from principle-based guidance to a more structured, prescriptive, and compliance-oriented regime. The key changes are as follows:

Recovery is as vital to lending as disbursement, if not more. Credit often begins with a courteous engagement by the lender, but too often, the standards of professionalism seen at the time of sanction weaken at the stage of enforcement. The right to recover is unquestionable; harassment is not. The proposed Directions seek to correct this imbalance by requiring lenders to uphold the same standards of fairness, transparency and discipline during recovery as at the time of origination.

See our other resources:

Vinod Kothari and Dayita Kanodia | Finserv@vinodkothari.com

Known by various alternative names as “synthetic risk transfers”, “credit risk transfers”, “on balance sheet securitisation” or “synthetic securitisation”, Significant Risk Transfers (SRT) have a history of over 25 years but have recently grown faster than other components of either traditional securitisation or credit derivatives. The pool value of banks’ synthetic securitizations has surpassed $670 billion, and the global sales of SRTs are expected to expand 11% annually on average over the next two years.

This article discusses SRT Transactions, the state of the market, different structures used, risks, capital benefits, and the regulatory permissibility of such transactions in different countries. Finally and quite significantly, this article makes a case as to why India, which is one of the very countries in the world presently prohibiting such structures, should rethink.

As per a report published by the International Association of Portfolio Managers, by the end of 2024, over € 700 bn of securitized loans were protected by $ 75 bn (9%) of SRT tranches, some 70% being issued by European banks. Further, the International Association of Credit Portfolio Managers reported that between 2016 and 2023, nearly 500 SRT transactions protected underlying portfolios adding to $ 1 trillion in loans, ranging from corporate loans to auto loans.

Period 2016- 2024 portfolio under SRTs totaled Euro 1311 billion (or roughly USD 1500 billions). In 2024, Europe, excluding the UK, took Euro 152 billion out of the Euro 260 billion protected portfolio.

Thus, nearly half of the SRT deals have originated from EU countries. The proportion was even larger historically, but US banks started aggressively getting into SRT Transactions in 2025.

SRT transactions have existed even before the Global Financial Crisis. In 2021, EU regulators extended the benefit of lower regulatory capital consuming “simple transparent and standard” (STS) securitisation treatment to synthetic transactions too. This has proved to be the game changer.

While corporate loans still represent almost two-third of the underlying pool assets (63%) in 2024, composition of other asset classes were: SMEs (13%), auto loans (7%), residential mortgages (3%), and specialized lending (3%). As in the past, in 2024 some 80% of issued synthetic securitizations support commercial lending to Corporates and SMEs.

Specialised credit funds, aka private credit funds, and debt fund managers are the largest investors. The following graph shows the composition of SRT investors:

The following are examples of some of the recent SRT transactions:

Banco Santander IFC transaction (2024)

The International Finance Corporation (IFC), a member of the World Bank Group, announced that it will provide a credit guarantee of $93 million to Banco Santander Mexico so that it can allocate more resources to financing small and medium-sized businesses (SMEs) in the country.

Aareal Bank (2025)

Aareal Bank, a German Bank completed its first SRT transaction, synthetically referencing a portfolio of performing European commercial real estate loans. With this transaction, Aareal Bank offered investors an opportunity to take exposure to a €2 billion CRE portfolio, which is equivalent to approximately 6 per cent of Aareal Bank’s overall CRE portfolio.

Synthetic securitisation uses credit derivatives or similar devices to transfer the risk of a mezzanine tranche(s) of the credit risk of a pool of assets to capital markets by embedding such risk into credit-linked securities. The word “synthetic” is used in distinction to a traditional securitisation, which may be called “cash securitisation” or “true sale securitisation”. In every traditional or cash securitisation, there is a pooling of credit assets to constitute a reasonably diversified pool. The pool is then tranched into multiple tranches, such that, usually, the first loss tranche is retained by the originator, and mezzanine and senior tranches are moved to capital markets through a special purpose vehicle. The result is funding as well as risk transfer. The first loss piece, retained by the originator, neither leads to funding, nor risk transfer. However, for the mezzanine and senior tranches, there is a movement of money from the investors to the originator through the SPV, and risk transfer in the opposite direction. In synthetic securitisation, the purpose is not funding: the purpose is risk transfer. Therefore, the first loss piece still typically stays with the originator, but the risk in the mezzanine is moved to capital markets through the issue of credit-linked securities. The transfer of risk, without funding, may happen using credit default swaps, or guarantees

Over three-quarters of the reported trades in 2024 are issued without SPV. The percentage of protected tranche notional issued directly by banks increased from some 25% in 2016 to 73% in 2024.

In the case of an SPV structure, an SPV is brought in as an intermediary between the investors and the originator. In case of cash or traditional securitisation arrangements, an SPV is brought in to hold the assets as a repository for the investors. In synthetic structures, there is no transfer of assets at all, an SPV is commonly used for the following reasons:

The structure of SRT transactions has not changed from what it was before the GFC. For example, n December 2001, DBS Bank Singapore introduced its first synthetic securitisation transaction involving a reference portfolio of approximately S$2.8 billion of corporate loans. The transaction used credit default swaps to transfer credit risk to an SPV, ALCO 1 Limited, without a true sale of assets. The SPV issued around S$224 million of multi-currency, multi-tranche notes (rated from AAA to BBB), while DBS retained the first-loss and super-senior exposures. The deal enabled regulatory capital relief and risk-weighted asset optimisation, and is widely regarded as one of Asia’s earliest synthetic CLO-style transactions outside Japan, marking a milestone in regional structured finance markets. Although this transaction was undertaken more than two decades ago, the structure used primarily remains the same. The following diagram illustrates a common SRT SPV structure:

As explained above, typically an SPV is required in cash or traditional structures for holding the asset, isolating it from the originator, protecting the assets from bankruptcy risks of the originator. A rating arbitrage, that is, any of the securities of the SPV being rated higher than the originator, is not theoretically possible if any of the securities represent a claim against the originator. In synthetic structures, there are no actual assets, only synthetic; therefore there is no need to protect the assets (meaning assets of the investors). However, synthetic CDOs do have assets to the extent of funding contributed by the investors. If this funding were to be prepaid or invested in the originator the claims of the investors are backed up by the claim against the originator, and hence, are subject to the rating cap of the originator.

It is understandable that the cash assets of a synthetic structure is only a fraction of the synthetic assets and hence the need for originator bankruptcy isolation is less prominent. A number of synthetic transactions have found it less necessary to involve a facade between the originator and the investors and have gone ahead with non- SPV structures. In this structure, the securities are issued by the originator himself and therefore represent a claim against the originator.

There are various Non-SPV structures observed in the market, Unfunded bilateral guarantee/CDS with no SPV, Funded bilateral guarantee/CDS with no SPV, Funded Credit Linked Note issued by originator with no collateral.

The table below shows the difference between SPV and Non-SPV structures:

| SPV Structure | Non-SPV Structure | |

| Counterparty risk | In the case of an SPV structure, the entire money paid by the investors will be held by the SPV. This ensures that the investors are protected from the counterparty risk w.r.t the originator since any amount paid by them is held by a bankruptcy remote vehicle. | In this case, the investor will be exposed to both the risk of default in the assets as well as counterparty risk of the originator, as opposed to the SPV structure, where the counterparty risk is eliminated. |

| Rating Cap | The SPV is a separate bankruptcy remote entity, and hence no cap on rating because of the counterparty risk of the originator. | The rating of the securities will be capped at the rating of the originator due to counterparty risk. |

In a blind reference pool SRT, the bank does not reveal borrower details to the investor or protection provider, and the investor only has access to high-level characteristics of the reference loan portfolio (such as industry distribution, credit ratings, or geographic exposure). Under this type of structure, investors face higher uncertainty as they must rely on the bank’s understanding of standards and risk management practices instead of conducting their own loan-level risk analysis.

In case of funded structures, the originator and the investor enter into a bilateral credit protection contract which may be drafted as a guarantee or a credit derivative. The investor then places a collateral equivalent to the maximum payment obligation under the contract. The money from this collateral amount deposited is only paid to the originator when losses hit the protected tranche. The collateral amount remaining after absorbing the losses is returned to the investor.

Unfunded SRTs are transactions not secured by financial collateral. The investor (protection provider) does not make any upfront payments to cover potential losses and is only required to compensate the bank if a credit event occurs. The protection provider is considered to have a high enough credit quality to mitigate the counterparty risk and is subject to eligibility criteria in Europe. The protection providers are typically, in Europe, insurance companies, pension funds, or multilateral development banks. The bank originating the SRT is exposed to counterparty credit risk.

SRTs with a replenishment period allow a bank to add new loans to the loan portfolio as old loans mature, subject to eligibility criteria. Typically, the loans will come from the same portfolio and share the original loan’s credit characteristics. The risk for the investor is potential asset quality deterioration of the reference pool, as the likelihood of credit losses could increase from lower asset quality loans being added, or from changes in the risk profile of the reference pool.

Consider a room with bombs placed in 5 different regions, as opposed to all the bombs placed in one place. The probability of a person stepping on the bomb will be far less in the first case than in the second one. The same is the case with assets.

The economics of risk transfer in securitisation are rooted in the principles of integration and differentiation that underpin structured finance. A diversified set of underlying assets is first aggregated into a single pool, enabling risk to be spread across a broader portfolio rather than remaining concentrated at the individual loan level. This pooled risk is then differentiated through tranching, whereby cash flows and credit risk are allocated among distinct tranches with varying risk-return profiles. Such structuring facilitates more efficient risk allocation and diversification, making the protection buyer better off as compared to obtaining guarantees or credit protection on each loan on a standalone basis, where risk remains fragmented and less efficiently distributed.

Thus, integration and differentiation ensure that correlation risk, or the risk that other assets also default on a default by one asset, is minimal.

The following are some of the risks associated with SRT Transactions:

In an SRT transaction, a bank buys protection for the mezzanine tranche by issuing CLNs to investors. Under securitization treatment, the senior tranche carries 20 percent RWA, and the first-loss tranche carries 1,250 percent RWA. The RWA for the mezzanine tranche becomes zero because the bank is no longer exposed to the losses from this tranche.

The following examples illustrates maintenance of capital in case of SRT vs non-SRT transactions:

| Non-SRT (in USD million) | SRT (in USD million) | ||

| Asset Pool | 100 | Asset Pool | 100 |

| RWA ratio | 50% | First Loss Tranche % | 0.50% |

| RWA | 50 | RWA ratio | 1250% |

| Tier 1 Capital | 10.50% | RWA | 6.25 |

| Tier 1 Capital Required | 5.3 | Mezzanine Tranche % | 4.50% |

| RWA ratio (as risk transferred, backed by cash) | 0% | ||

| RWA | 0 | ||

| Senior Tranche | 95% | ||

| RWA ratio | 20% | ||

| RWA | 19 | ||

| Total Capital Required | 2.7 | ||

Thus, the capital required to be maintained in case of SRT structures is significantly lower as compared to non-SRT structures thus allowing originators capital relief. This, however, is a function of the size of the junior tranche. In the same example as above, if the thickness of the junior tranche was 3%, the required capital would have gone up.

In India, synthetic securitisation, which is defined as a structure where the credit risk of an underlying pool of exposures is transferred, in whole or in part, through the use of credit derivatives or credit guarantees that serve to hedge the credit risk of the portfolio, which remains on the balance sheet of the NBFC, is prohibited. [para 5(3) of the Reserve Bank of India (Non-Banking Financial Companies – Securitisation Transactions) Directions, 2025]. Accordingly, SRT transactions where there is only a transfer of the risk and rewards without the transfer of the asset are prohibited in India.

The below table shows the regulatory permissibility of SRT in various jurisdictions:

| Countries | Regulatory Permissibility of SRT |

| India | Prohibited |

| Australia | Not eligible for capital relief |

| UK | Permissible |

| Hong Kong | Permissible |

| Canada | Permissible |

| Indonesia | Prohibited |

| China | Prohibited |

| Japan | Permissible within regulatory limits |

| EU | Permissible |

| Korea | Prohibited |

| Singapore | Permissible |

Over the years, SRTs have become a very potent tool for regulatory capital and risk management. SRTs have also permitted private credit funds to acquire exposure on loan portfolios without organically creating them. The regulatory antipathy for synthetic securitisation was the multiple layers of risk transfers as seen during the GFC. This was, however, more in case of structured finance CDOs and arbitrage transactions. SRTs are currently mostly related to on-balance sheet assets – hence, the question of any unwarranted risk transfers or risk build up do not arise. Of course, any securitisation transaction creates an interconnection between the banking system and capital markets, but that is also a cushion against risk as it has a potential for risk of contagion.

The RBI’s proposed relief to exempt pure investment companies from exemption from regulation is not a cakewalk but a hurdle race. It is not an exemption that comes in auto mode; you need to earn the right to be exempt. Some of the important pre-conditions that the RBI has proposed are:

| Type of NBFC | Options Available |

| NBFCs holding Type I Registration as on April 1, 2026 | Option 1: Apply for deregistration Option 2: Continue to remain as Type I NBFC |

| Entities that fulfil the conditions for Unregistered Type I NBFC, after April 1, 2026 | Option 1: Satisfy the conditions under 66A and remain unregistered [see box on Conditions Subsequent] Option 2: Apply for registration as Type I NBFC |

| NBFCs not having a customer interface and public funds and having an asset size below ₹1000 crores, but not registered as Type I | Option 1: Apply for deregistration Option 2: Apply for registration as Type I NBFC to avail regulatory exemptionOption 3: Maintain status quo |

| NBFCs not having a customer interface and public funds and having asset size above ₹1000 crores, but not registered as Type I | Option 1: Apply for registration as NBFC Type I Option 2: Apply for registration as NBFC Type II, in case of changes in business model |

Several NBFCs that have been registered with the RBI before the concept of Type 1 was introduced in 2016 may not have the CoR as a Type 1 NBFC in spite of the fact that as on date they don’t have access to public funds nor any customer interface. Such an NBFC with an asset size less than ₹1000 crores will still have an option to apply for deregistration, subject to the satisfaction of the conditions prescribed. However, such NBFCs in case they decide to maintain the status quo will not be eligible for the regulatory exemption available to Type 1 NBFCs.

If an entity carries investment activity with owned funds, within a limit of ₹1000 crores, does it need RBI registration? The answer seems to be – no. Such a company obviously does not have to go through the rigour of seeking registration first, and then qualifying for an exemption.

The company in question still has to satisfy the exemption conditions; and the auditor will need to give an exception report. The meaning of exception report is that if there is a breach of any of the conditions of exemption, or there is any breach of any other provisions of the law, the auditor shall be required to make an exception report.

Notably, CARO Order also requires auditors to comment on adherence to RBI regulations, which, in future, will include these conditions too.

Is the requirement of asset size being within ₹1000 crores based on stand-alone financial statements, or will the assets of companies within the group be aggregated, as is done for the purpose of determination of the middle layer status of companies?

It seems that the aggregation requirement is not there for the Type 1 exemption.

The basis for this is FAQ 13, which states as follows:

Q13. As per regulations of the Reserve Bank, total assets of all the NBFCs in a Group are consolidated to determine the classification of NBFCs in the Middle 11 Layer. What shall be the treatment given to ‘Type I NBFCs’ and ‘Unregistered Type I companies’ in this regard?

Ans: For aggregation purposes, the asset size of ‘Type I NBFCs’ shall be considered but asset size of ‘Unregistered Type I NBFCs’ shall not be considered. It is emphasized that ‘Type I NBFCs’ shall always be classified in Base Layer regardless of such aggregation.

Are the exemption conditions, that there is no access to public funds and no customer interface, merely a statement of intent, or must also be borne out by the conduct in any of the past 3 financial years? Looking at the definition in para 6 (14A), which reads “Not accepting public funds and not intending to accept public funds”, and likewise, “Not having customer interface and not intending to have customer interface”, it appears that the exemption conditions are both a statement of fact as well as intent. If one is negated by the fact, a mere statement of intent may not help.

However, assume there are isolated instances of intra-group loans taken or intra-group loans given. The transactions are not indicating a “business model”, at least the ones on the asset side. Are we saying that the breach of the conditions of “no public funds” and “no customer interface”, at any time during the last 3 years, will disentitle the exemption?

We do NOT think so. There are two reasons to say this:

In our view, since the deregistration application has to be made within September 30, 2026, the audited financials for FY 25-26 must have been prepared. Hence, the last three financial years that would be considered are FY 23-24, 24-25 and 25-26.

It is usually hard to get a relief from a regulator, as relief is seen as a prize that you earn. If the idea was based on the premise that what does not matter for the financial system, and is still being regulated, is a burden both for the regulator and for the regulated, there would have been a more welcoming approach to exemption. Specifically:

– Dayita Kanodia, Assistant Manager | finserv@vinodkothari.com

Holding Companies whose primary intent is to invest in their group companies have lately faced a paradox with respect to the requirement of registration as a Core Investment Company (CIC).

CICs are entities whose principal activity is the acquisition and holding of investments in group companies, rather than engaging in external investments or lending exposure outside the group. Para 3 of the Reserve Bank of India (Core Investment Companies) Directions, 2025 (‘CIC Directions’) prescribes the quantitative thresholds for classification of an NBFC as a CIC. In terms thereof, an NBFC that holds not less than 90% of its net assets in the form of investments in group companies, of which at least 60% is in equity instruments, is classified as a CIC and is required to obtain registration from the RBI, unless exempted.

Conceptually, a CIC is a sub-category of a Non-Banking Financial Company (NBFC) (para 3 of the CIC Directions), just like Housing Finance Companies, Micro Finance Institutions, etc. The threshold criteria that NBFCs are required to satisfy is the principal business criteria (PBC), pursuant to which at least 50% of the total assets of the entity must consist of financial assets and at least 50% of its total income must be derived from such financial assets.

The PBC has historically served as the foundational threshold for determining whether an entity is an NBFC. Once the entity satisfies this principal requirement of carrying out financial activity, the sub-category is to be determined based on its line of business, which, lately, has seen quite a varietty – fron tradtional variants such as investment and lending activities (ICC), to housing finance (HFC), to financing of receivables (Factoring companies), the more recent inclusions are account aggregators (AA), mortgage guarantee companies (MGCs), infrastructure finance compaies (IFC), etc. Each of these NBFCs first, and then they fall in their respective class. For instance, HFCs are a type of NBFCs that primarily focus on extending housing loans and hence, must have a minimum housing loan portfolio of 60% and an individual housing loan of 50%.

Accordingly, all categories of NBFCs must first be ascertained to be carrying out financial activities as their primary business, and thereafter, the specific product helps to determine the category. Consequently, holding companies or CICs should ideally also adhere to the 50-50 criteria first and thereafter meet the 90-60 criteria for CIC classification.

However, there is a common perception among the market participants that CICs, irrespective of meeting such PBC, in case they reach the 90-60 criteria, will be required to obtain registration as a CIC. Several news reports also note this perception.

This perception among the market participants that CICs are not required to adhere to the PBC criteria stems from para 17(3) of the CIC Directions, which explicitly provides that:

“CICs need not meet the principal business criteria for NBFCs as specified under paragraph 38 of the Reserve Bank of India (Non-Banking Financial Companies – Registration, Exemptions and Framework for Scale Based Regulation) Directions.”

It may be noted that the above-quoted provision, which has recently been made a part of the CIC Directions pursuant to the November 28 consolidation exercise, was earlier included in the FAQs released by RBI on CICs. FAQs are RBI staff views; whereas Directions or Regulations are a part of subordinate law; however, in the consolidation exercise, a whole lot of FAQs and circulars became a part of the Directions.

Going by the intent of the NBFC classification and categorisation, the above-quoted provisions seem more relevant for registered CICs, implying that CICs once registered need not meet the PBC on an ongoing basis. CICs predominantly hold investments in group companies and therefore satisfy the 90–60 thresholds, but often do not derive any financial income from such investments. Group investments, being strategic in nature, are rarely disposed of, and the dividend income from such investments depends on the dividend/payout ratio, which may be quite low. In several cases, such entities continue to earn income, say, by way of royalty for a group brand name. Even the slightest of non-financial income will seem to breach the PBC criteria, which may challenge the continuation of registration of the CIC as an NBFC. In order to redress this, the provision under para 17(3) of the CIC Directions provides that CICs need not meet the PBC criteria on an ongoing basis.

What is the basis of this argument? The definition of a CIC comes from para 3, which says as follows: “These directions shall be applicable to every Core Investment Company (hereinafter collectively referred to as ‘CICs’ and individually as a ‘CIC’), that is to say, a non-banking financial company carrying on the business of acquisition of shares and securities, and which satisfies the following conditions.” Para 17 (3) is a note to Para 17, which apparently deals with conditions of continued registration.

Given that CIC is a category of NBFC, it would be counter-intuitive to say that the regulatory requirement requires holding companies to go for registration as a CIC even if they do not meet the PBC for an NBFC. In fact, if an entity is not an NBFC because it fails the principality of its business, it would not even come under the statutory ambit of the RBI by virtue of section 45-IC.

Accordingly, without going by just the text of the regulations, in our view, considering the regulatory intent, the following could be inferred:

Other Resources:

By Archisman Bhattacharjee & Avikal Kothari | Finserv@vinodkothari.com

On November 28, 2025, the Reserve Bank of India (“RBI”) issued the Reserve Bank of India (Non-Banking Financial Companies – Managing Risks in Outsourcing) Directions, 2025 (“Outsourcing Directions”), thereby repealing the erstwhile directions governing IT outsourcing and financial services outsourcing. For the purposes of this article, our discussion is confined to Chapter IV of the Outsourcing Directions, which specifically deals with outsourcing of information technology (“IT”) services. While the Outsourcing Directions largely represent a consolidation of the existing regulatory framework as also clarified by the RBI in its Consolidation of Regulations – Withdrawal of Circulars dated November 28, 2025, they also provide enhanced clarity and structure to the regulatory expectations applicable to IT outsourcing arrangements of NBFCs. This article seeks to examine whether, and to what extent, any additional or expanded obligations have been introduced by the RBI under the consolidated framework.

Chapter IV of the Outsourcing Directions, dealing with IT services outsourcing is applicable on NBFC-ML and above, which was also the case for the Erstwhile IT Outsourcing Directions

The erstwhile IT Outsourcing Directions had become applicable with effect from October 1, 2023. Under the Outsourcing Directions, the RBI has now prescribed a specific transition mechanism for existing IT outsourcing arrangements. In this regard, para 2 of the Outsourcing Directions provides that:

“These Directions shall come into force with immediate effect

Provided that for Non-Banking Financial Companies covered under the scope of these Directions, as mentioned in paragraph 3, their existing Information Technology (IT) outsourcing agreements, regardless of whether they are due for renewal on or after the effective date of these Directions, shall comply with the provisions of these Directions either at the time of renewal or by April 10, 2026, whichever is earlier.”

Given that the Outsourcing Directions are primarily in the nature of a consolidation exercise and do not introduce materially new obligations, the timeline up to April 10, 2026 appears to be intended to provide NBFCs with a reasonable window to align their existing IT outsourcing agreements with the consolidated framework. Accordingly, NBFCs should utilise this transition period to review, amend, and, where necessary, renegotiate their existing IT outsourcing contracts to ensure full compliance with the Outsourcing Directions within the prescribed timeline.

Against this backdrop, it becomes important to examine the substantive requirements laid down under Chapter IV of the Outsourcing Directions in relation to outsourcing of IT services to third-party vendors. The following section discusses the key regulatory expectations and compliance obligations applicable to NBFCs when engaging third-party service providers for IT outsourcing.

The definition of “service provider” as defined under paragraph 58(3) of the Outsourcing Directions is expansive and extends beyond the primary contracting entity to include sub-contractors, third-party vendors, and entities forming part of the service delivery chain. Further the Outsourcing Directions under paragraph 58(4)have also now defined the term “sub-contractor” to mean:

“… those providing material / significant IT services to the service provider and is specific to the material / significant IT services arrangement that the NBFC has entered into with the service provider”

Accordingly, a sub-contractor that provides material or significant IT services to a service provider, where such services are critical to the delivery of the outsourced arrangement to the NBFC, would also fall within the ambit of the Outsourcing Directions. For instance, where an NBFC avails a SaaS solution from a third-party service provider, any entity that supplies core software or technology to such SaaS provider, without which the service cannot be effectively rendered, may be regarded as a material service provider for the purposes of the Outsourcing Directions.

While the erstwhile IT Outsourcing Directions did prescribe certain obligations in respect of sub-contractors (and the obligations of NBFCs vis-à-vis their primary service providers largely remain unchanged under the Outsourcing Directions), the current framework introduces greater clarity on who qualifies as a “sub-contractor.”

Actionables for NBFCs:

NBFCs should reassess their existing IT outsourcing landscape to identify all arrangements that fall within the expanded scope, including indirect or layered service delivery models. Vendor inventories should be updated to capture not only primary service providers but also material sub-contractors and supply-chain entities involved in the provision of IT services. Furthermore, NBFCs are advised suitably amend its existing policies to clearly specify the framework and criteria for identification of sub-contractors. This may, inter alia, include requiring service providers to furnish a list of their appointed sub-contractors along with details of the functions performed by each, and undertaking an assessment, in consultation with the relevant service provider, to determine whether such sub-contractors are material or non-material.

The Outsourcing Directions require NBFCs to conduct risk-based due diligence of IT service providers, this includes tracking system performance, uptime, service availability, Service Level Agreement, compliance and incident response on an ongoing basis. Regular risk-based audits of service providers, including sub-contractors, have been formalised, with an option to rely on pooled audits or recognised third-party certifications, though this does not dilute the NBFC’s responsibility for data security and system availability. NBFCs must also periodically review the financial and operational strength of service providers to identify any deterioration in performance, security or resilience. Access rights have been strengthened, requiring service providers to provide unrestricted access to relevant data and premises for NBFCs, auditors and regulators.

Actionables for NBFCs:

NBFCs should strengthen vendor due diligence processes and establish mechanisms for periodic review of service providers. Oversight frameworks should extend to subcontractors and material supply-chain entities, with clear accountability resting on the primary service provider. Overall, the changes make due diligence an ongoing obligation rather than a one-time exercise, requiring NBFCs to strengthen internal monitoring structures, audit planning and vendor risk management practices.

Further, considering that the RBI has mandated compliance of the agreements with the Outsourcing Directions by April 10, 2026, it is advisable for NBFCs to undertake a comprehensive review of the service level agreements and other contractual arrangements executed with all its material IT vendors to ensure alignment with the requirements set out under paragraphs 33, 34, 73 and 74 of the Outsourcing Directions.

Additionally, prior to April 10, 2026, NBFCs are suggested to conduct audits of its material service providers to verify:

Alternatively, the Company may also rely on globally recognised third-party certifications made available by the service provider in lieu of conducting independent audits.

Where, based on such review or audit, the NBFC forms the view that a vendor is not in compliance with the contractual terms or applicable regulatory requirements, the NBFC should require the vendor to implement corrective action within defined timelines and, where necessary, amend or renegotiate the existing agreements to ensure alignment with the Outsourcing Directions.

Further, the NBFC should appropriately document such reviews, audits, and remediation measures and place the same before the senior management, in accordance with the requirements of paragraph 78 of the Outsourcing Directions, and/or before such a committee as may be identified under the NBFC’s IT Outsourcing Policy. Any material or adverse developments should also be escalated to the Board in alignment with the requirements of paragraph 78 of the Outsourcing Directions.

In cases where remediation or contractual modification is not feasible, the Company should maintain an exit plan/exit strategy, including identification of alternate service providers and/or arrangements for bringing the outsourced services in-house, so as to ensure continuity of critical operations and minimal disruption to customers.

The Outsourcing Directions mark a significant step by the RBI towards consolidating and strengthening the regulatory framework governing IT outsourcing by NBFCs. While the underlying obligations remain broadly consistent with the erstwhile regime, the transition period up to April 10, 2026 provides NBFCs with a critical opportunity to holistically reassess their IT outsourcing arrangements, rationalise vendor ecosystems, and embed robust contractual, operational, and governance safeguards. NBFCs that proactively undertake structured reviews, strengthen vendor risk management, and institutionalise ongoing monitoring mechanisms will be better positioned not only to achieve regulatory compliance but also to enhance operational resilience and customer trust.

Ultimately, IT outsourcing under the Outsourcing Directions is no longer a purely contractual or procurement function—it is a core governance and risk management responsibility. Treating it as such will be essential for NBFCs navigating an increasingly digital and interconnected financial services ecosystem.

See our other resources:

Simrat Singh | finserv@vinodkothari.com

When nature unsettles the ordinary course of life, the regulatory hand should neither be withdrawn nor clenched; it should extend a humane touch, easing distress and guiding the return of order. In this spirit, the RBI has released draft directions on Relief Measures in Areas Affected by Natural Calamities, setting out a framework under which banks, NBFCs and other Regulated Entities (REs) may provide relief to borrowers impacted by natural calamities or similar external events. The framework enables REs to extend resolution plans to eligible borrowers, while permitting retention of standard asset classification and lower provisioning, benefits that would otherwise not be available if such restructuring were undertaken under the normal IRACP framework.

It may be noted that earlier RBI had issued guidelines for banks in connection with matters relating to relief measures to be provided in areas affected by natural calamities consolidated under ‘Master Direction – Reserve Bank of India (Relief Measures by Banks in Areas affected by Natural Calamities) Directions 2018 – SCBs’ dated October 17, 2018. In 2016, these guidelines were made applicable, mutatis mutandis, to all NBFCs as well, in areas affected by natural calamities as identified for implementation of suitable relief measures by the institutional framework viz., District Consultative Committee (DCCs)/ State Level Bankers’ Committee (SLBCs). However, given that the provisions were drafted considering the banking operations, the implementation by NBFCs was ambiguous and the provisions were often overlooked.

While the proposed framework applies to both banks (Commercial, RRB, Local area banks etc) and NBFCs, there are separate draft Directions issued for each RE. In case of banks the provisions carry additional system-level and public service responsibilities, reflecting their role within SLBCs and DCCs.

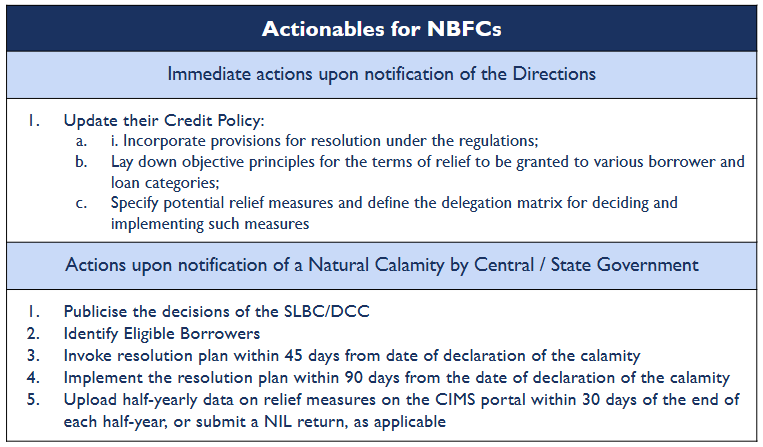

Fig 1: Actionables for NBFCs under the draft directions

The draft directions are proposed to come into effect from 1 April 2026, after the final directions are notified. The framework is triggered upon formal notification of a natural calamity by the Central Government or the concerned State Government.

Where a calamity affects a substantial part of a State, it is proposed that a special meeting of the SLBC shall be convened within 15 days of such declaration. If the impact is confined to one or more districts, the corresponding DCC(s) are required to meet within the same timeframe. These committees assess the severity of the impact on economic activity, determine objective criteria for identifying impacted borrowers and indicate the nature and extent of relief such as moratoriums that may be extended by regulated entities operating in the affected areas. The decisions taken in these meetings are communicated to regulated entities and are required to be given adequate publicity, primarily by banks, through field outreach and public communication. The relief framework becomes operational in line with such Government notifications and the decisions of the SLBC or DCC, as applicable.

The draft directions propose that the REs update their credit policies to incorporate a structured and pre-defined framework for dealing with borrower stress arising from natural calamities. The credit policy is expected to provide for resolution in line with the provisions and to set out objective principles governing the terms of relief across different borrower segments and loan categories.

While the precise parameters may vary depending on the nature and severity of the calamity, the decisions of the SLBC/DCC/Governments, the credit policy is expected to lay down a consistent framework to be applied by the REs when extending relief. This includes identifying potential relief measures, specifying verifiable parameters for determining eligibility of borrowers and extent of relief and defining the delegation matrix for approval and implementation. The emphasis is on ensuring timely decision-making, particularly in relation to restructuring of existing exposures and sanction of additional finance.

Relief under the draft Directions is proposed to be available only to borrowers who meet the prescribed eligibility conditions as on the date of occurrence of the natural calamity. To qualify, the borrower’s account must be classified as ‘Standard’ and must not be in default for more than 30 days with the concerned RE in respect of any facility. Other additional conditions may be laid down in the credit policy.

Borrowers who do not meet these conditions fall outside the scope of the calamity relief framework and may instead be considered for resolution under the applicable Resolution of Stressed Assets Directions. In such cases, however, the RE does not receive the benefit of standard asset classification or lower provisioning (see discussion below). The framework extends its shelter only to those borrowers who, till the moment the calamity struck, had kept their financial obligations substantially intact. The protection is not meant to rescue infirm credit, but to steady sound accounts momentarily shaken by forces beyond human control.

Where a RE decides to extend relief, the resolution plan is to be structured based on an assessment of the borrower’s post-calamity viability. The draft Directions propose a range of relief measures, including rescheduling of repayments, grant of moratorium, and conversion of accrued or future interest into another credit facility. Regulated entities may also consider sanctioning additional or fresh finance to address temporary financial stress, subject to appropriate assessment of viability and credit risk.

Notably, the framework is enabling rather than mandatory. It does not require automatic restructuring of all eligible accounts, thereby allowing REs to exercise credit judgement while operating within the prescribed regulatory parameters.

It is proposed that resolution under the framework must be invoked within 45 days from the date of declaration of the natural calamity, unless an extension is granted by the Regional Director or Officer-in-Charge of the Reserve Bank. This would mean that the aggrieved borrower must approach the lender and the terms of restructuring must be agreed between both of them within the said timeframe. Once invoked, the resolution plan must be implemented within 90 days from the date of invocation.

In practice, this means that following the Government notification and the SLBC or DCC meeting, typically held within the first 15 days from the notification, REs have a limited 30-day window to complete borrower identification, viability assessment, documentation and approval. Failure to adhere to these timelines results in loss of the regulatory benefits available under the framework.

The most significant regulatory benefit under the proposed framework relates to asset classification. Where a resolution plan is implemented in compliance with the Directions, borrower accounts classified as ‘Standard’ may be retained as such upon implementation instead of facing any downgrade. Further, accounts that may have slipped into NPA status between the date of occurrence of the calamity and the implementation of the resolution plan are permitted to be upgraded to ‘Standard’ upon implementation. However, as per the ECL Policy of the RE, generally any restructuring would automatically be treated as a SICR and therefore, the staging may change and a higher ECL would be required to be provided on such restructuring which may nullify the benefit.

After implementation, subsequent asset classification is governed by the applicable IRACP norms. The proposed framework also addresses cases of repeated restructuring. Where a borrower account is restructured again under these Directions before the reversal of additional provisions (see below), it may continue to be classified as ‘Standard’, subject to recognition of interest on a cash basis from the second restructuring onwards and maintenance of an additional specific provision of five per cent of the outstanding debt for each restructuring, subject to an overall ceiling of 100 per cent.

For restructured accounts, it is proposed that interest income may be recognised on an accrual basis. At the same time, REs are required to maintain an additional specific provision of 5% of the outstanding debt, over and above the applicable provisioning under IRACP norms. Reversal of this additional provision can happen only where the borrower repays at least 20% of the outstanding debt, the account does not slip into NPA status after implementation of the restructuring and no further restructuring is undertaken during the relevant period. Specifically for banks, if the outstanding debt post-restructuring is only in the form of non-fund-based facilities or facilities in the nature of cash credit / overdraft, the additional provisions can be reversed after one year, post implementation of the restructuring, provided the borrower was not in default at any point of time during the period concerned.

It is proposed that the REs be required to extend interest subvention or prompt repayment incentive benefits notified by the Government to all eligible borrowers. They must also ensure that any relief already provided, or being provided, by the Central or State Governments is duly factored into the resolution process.

For agricultural loans secured by land, the draft Directions propose acceptance of certificates issued by Revenue Department officials where original title documents have been lost due to the calamity. In areas governed by community ownership arrangements, certificates issued by competent community authorities may also be accepted. REs may also, at their discretion, provide additional relief such as waiver or reduction of fees and charges for borrowers in affected areas, for a period not exceeding one year. Expected proceeds from insurance policies may also be kept while deciding the relief. Additionally for banks it is proposed that they shall open small accounts for displaced borrowers and take immediate action to restore ATM services in the impacted areas. They may operate their natural calamity affected branches from temporary premises under advice to the RBI. For continuing the temporary premise beyond 30 days, banks may obtain specific approval from the concerned Regional Office of RBI. A bank shall also make arrangements to render banking services in the affected areas by setting up satellite offices, extension counters or mobile banking facilities etc. under intimation to the RBI.

It is proposed that the REs shall upload data on relief measures extended under the framework in the prescribed format on a half-yearly basis. The data points include ‘Outstanding eligible for restructuring as on the date of notification of natural calamity’, ‘Credit facilities restructured/rescheduled during the half year’, ‘Additional/fresh loans provided to affected borrowers during the half year’ etc. The data must be submitted within 30 days from the end of each half-year, i.e., as of 30 September and 31 March, through the CIMS portal. Where no relief measures are extended during a reporting period, a NIL statement is required to be submitted.

See our other resources: