The Great Consolidation: RBI’s subtle shifts; big impacts on NBFCs

Team Finserv | finserv@vinodkothari.com

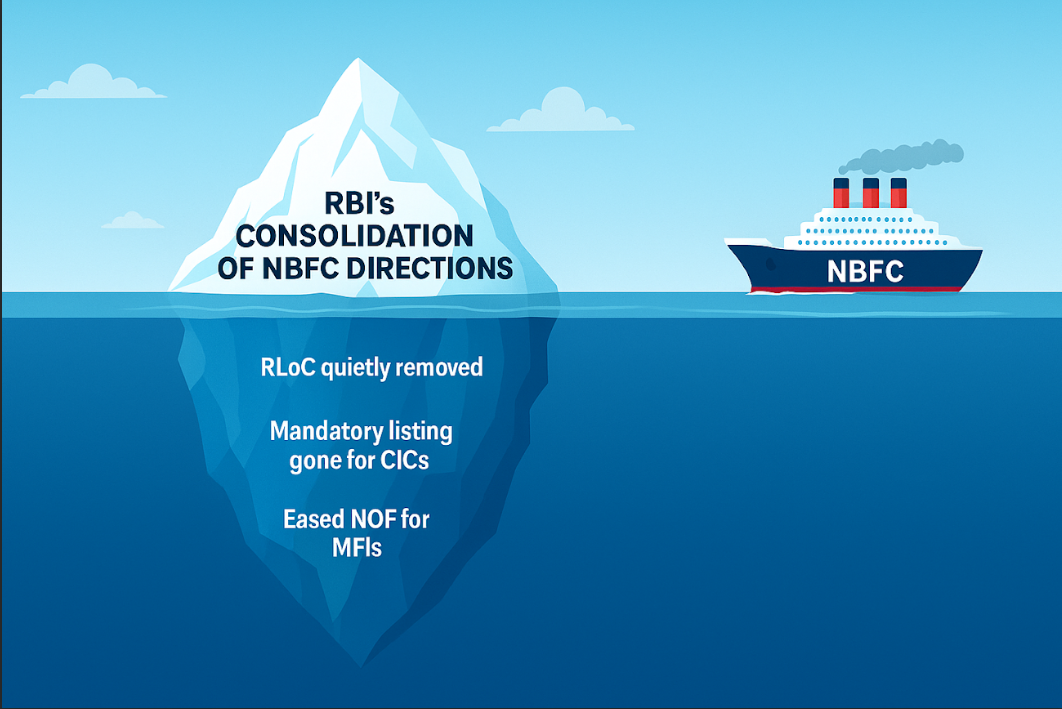

In its recent consolidation exercise of the Master Directions applicable to NBFCs, the RBI has done a lot of clause shifting, reshuffling, reorganisation, replication for different regulated entities, pruning of redundancies, etc. However, there are certain places where subtle changes or glimpses of mindset may have a lot of impact on NBFCs. Here are some:

1. RBI’s silent signal on revolving line of credit for NBFCs

Sometimes, silence says a lot! The RBI has removed all references to Revolving Line of Credit (RLoC) products from the proposed drafts, while these references exist in the draft directions for banks. This subtle change could indicate the regulator’s intent to restrict NBFCs from offering such facilities.

RLoC allows borrowers to withdraw, repay, and reborrow funds within a specified credit limit, thus functioning similarly to a credit card. Read our write-up explaining RLoC here. While this structure provides flexibility to borrowers, the RBI has, on multiple occasions, expressed concerns that such products may facilitate evergreening of loans, wherein borrowers use fresh disbursements to service existing obligations.

Further, the RBI has noted that these products resemble the features of credit cards, which can only be issued with the regulator’s prior approval and upon meeting the minimum eligibility requirements. NBFCs providing such RLoC facilities were seen to be bypassing this approval framework.

Accordingly, the omission of references to revolving line of credit from the proposed drafts may be viewed as a regulatory signal discouraging NBFCs from extending such facilities. Reference to RLoC, which was previously present, has been removed from the following directions:

- Digital Lending and default loss guarantee (Part of Reserve Bank of India (Non-Banking Financial Companies – Credit Facilities) Directions, 2025)

- Transfer of Loan Exposure (Part of Reserve Bank of India (Non-Banking Financial Companies – Transfer and Distribution of Credit Risk) Directions, 2025)

- Prudential Framework for the resolution of stressed assets (Part of Reserve Bank of India (Non-Banking Financial Companies – Resolution of Stressed Assets) Directions, 2025)

It may, however, be noted that the corresponding Directions issued for banks on the above aspects include reference to RLoC. This may be a strong indication by the RBI to explicitly state its prohibition on NBFCs offering such RLoC facilities.

2. Ta-Ta! To listing requirement for Upper-layer CICs

Under the extant norms, NBFCs on being notified as an Upper Layer NBFC, are required to opt for mandatory listing within three years of being identified as such. At present, 16 NBFCs are notified under the Upper Layer, which includes a Core Investment Company as well.

As a part of the consolidation exercise, RBI has proposed to replace the existing Master Directions for CICs with a consolidated Master Directions for CICs. Under the proposed Master Directions, the relevant provisions applicable on CICs, classified as Middle Layer and Upper Layer, have been consolidated making reference to the other proposed drafts, where required. While the extant provisions make a reference to the regulations applicable for CICs in Upper Layer, including the governance requirements, such as mandatory listing, the proposed draft have neither specified nor made reference to the governance norms.

It is arguable if the same is a drafting error or has been done intentionally. In case the RBI intends to relax the mandatory listing requirement, it would be a blessing in disguise for NBFC-CICs classified in Upper Layer. The draft amendment, which comes amid reports of a large conglomerate seeking exemption from this requirement, reflects the RBI’s reconsideration of a one-size-fits-all approach. Industry participants had raised concerns that mandatory listing could disrupt group structures or strategic control of such NBFCs. If finalised, the change will ease compliance pressure on large CICs, allowing them flexibility in determining their capital-expansion strategies.

3. RBI’s gentle adjustment: Easing NOF requirements for existing MFI

As per the extant RBI MFI Directions, existing MFIs were required to attain a minimum NOF of ₹7 crore (₹5 crore for MFIs registered in the North Eastern region) by March 31, 2025. However, the Draft MFI Directions seek to make a retrospective amendment, prescribing a uniform minimum NOF requirement of ₹5 crore for all MFIs by March 31, 2025. This proposed relaxation clearly indicates a regulatory intent to shelter the entities that were unable to meet the existing ₹7 crore gliding path threshold. Further, the NOF requirement of ₹10 crore by March 31, 2027 remains the same.

At a time when MFIs are finding it hard to find capital, this relaxation may have substantial value.

Read our other resources:

The draft prudential norms (page 26) explicitly mention capital adequacy requirements against lines of credit. Hence, I do not think that the RBI is planning to curb NBFCs from issuing la ine of credit.