https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2026-02-11 23:16:422026-02-20 19:25:48From Consent to Compensation: RBI’s Draft Directions for REs on Sales Practices

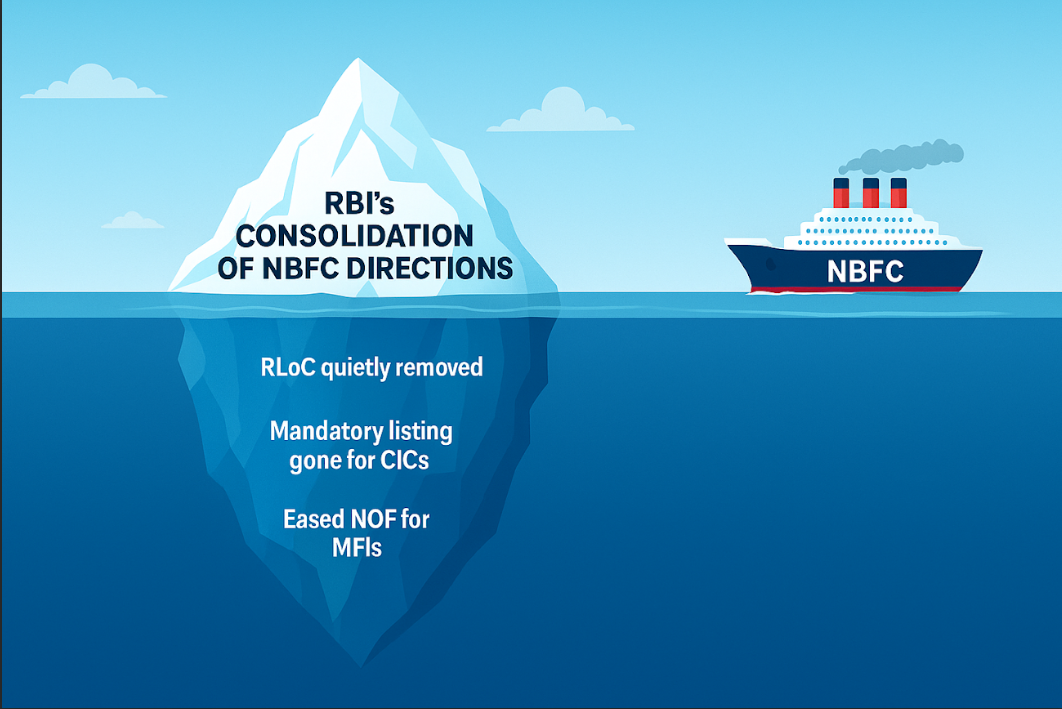

In its recent consolidation exercise of the Master Directions applicable to NBFCs, the RBI has done a lot of clause shifting, reshuffling, reorganisation, replication for different regulated entities, pruning of redundancies, etc. However, there are certain places where subtle changes or glimpses of mindset may have a lot of impact on NBFCs. Here are some:

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-15 15:11:142025-10-15 19:01:29The Great Consolidation: RBI’s subtle shifts; big impacts on NBFCs

In 2021, RBI had set up an expert committee with the ideal objective of consolidating the multitude of separate notifications, Directions, circulars, and regulations applicable to various regulated entities. The aim was to create a comprehensive repository that such REs could easily refer to, streamlining compliance and reducing ambiguity.

This consolidation exercise builds upon the groundwork laid by the Regulations Review Authority, which was tasked with reviewing regulations, circulars, and reporting requirements based on feedback from the public, banks and financial institutions, as highlighted in the press release dated April 15, 2021.

Ever since RBI was entrusted with the powers to regulate the financial sector entities, the RBI’s regulatory framework has steadily expanded, issuing numerous Directions under its statutory powers. While such evolution is natural, overlapping jurisdictions and a lack of clear supersession of older instructions have added complexity to the regulatory landscape.

In line with the above, the RBI has carried out a thorough consolidation of the regulatory instructions currently overseen by the Department of Regulation. On a prima facie review, it seems that this exercise has been carried out on an ‘as-is’ basis, with only minor editorial updates to clarify language or update terminology. There has been no substantive review of the instructions as such for any revisions or new additions.

Under the consolidation exercise, more than 9000 circulars and Directions issued up to October 9, 2025, have been streamlined into 238 Master Directions, covering 11 specific categories of regulated entities across up to 30 functional areas. As a result, all these existing circulars, including various Master Circulars and Master Directions, administered by the Department of Regulation are proposed to be repealed.

Previously, a single circular often applied to multiple entities, with provisions scattered across different sections. This sometimes led to some confusion- for example, under the KYC Directions, 2016, reference to “opening a small account” applied to banks, however, it created ambiguity about whether this shall be applicable to a borrower taking a loan in the case of NBFCs.

It has been proposed that the regulatory framework shall be divided amongst regulated entities like commercial banks, payments banks, All India financial institutions, NBFCs, etc. Additionally, within each entity the provisions shall be separated into key areas such as, prudential requirements, interest on advances, asset liability management, valuation of investments, concentration risks, credit reporting, outsourcing, disclosures, etc. The aim is to ease out the compliance process by simplifying and arranging the regulations into identified key operational areas applicable to a particular RE

While the intent of the consolidation exercise was refinement of the regulatory provisions and clarify any existing ambiguities, however, the segregation exercise requires a thorough review before being notified. Various provisions that were once uniformly applicable across all regulated entities have now been segregated based on the construct of respective REs, however, in ironing out one ambiguity, other creases may have surfaced! This underscores the need for a critical analysis of the implications of these provisions on individual regulated entities.

Drafts of these Master Directions have been circulated for comments to enable stakeholders to provide their views on this step taken towards ease of compliance. There could be uncertainties that would still persist post the streamlining process, and hence, warrants thorough review.

For reference, RBI has made available on its website the following draft documents for public comments, with a focus on their completeness and accuracy:

Major changes have been proposed by the RBI in the regime on what has become a major part of the business model of NBFCs and MFIs in the country – direct assignments (DAs). We have separately dealt with the Draft Directions on Securitisation of Standard Assets in a write up titled “New regime for securitisation and sale of financial assets”

The term DA is so very typical of the Indian scene – globally, the practice of loan trading, loan sales or so-called whole-loan transfers has largely been out of the regulatory domain. However, in India, the motivation to shift from securitisation to DAs were partly the RBI Guidelines of 2006 which regulated securitisation but did not regulate DAs, and partly, the tax issues on securitisation that began prominent around 2011-12 or so. However, the DA model has, over the years, been a sizeable part of securitisation volumes in India, and is the mainstay of transfer of priority-sector loans from NBFCs to banks. Now that NBFCs have been permitted a major push for MSE lending by several GoI schemes, NBFCs are eagerly looking for another round of DA drive, and therefore, it is important to see whether the proposed regulatory regime for loan sales will facilitate NBFC-originated loans to end up on the books of banks and other investors.