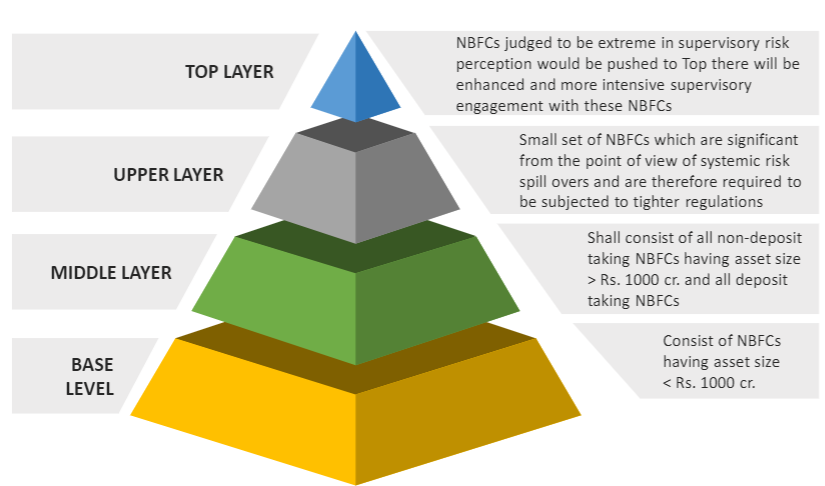

As a part of the overhaul for the NBFC Sector, the Reserve Bank of India (‘RBI’) had, on October 22, 2021, introduced the Scale Based Regulations (SBR): ‘A Revised Regulatory Framework for NBFCs’. Upon application of SBR, NBFCs will now be divided into four major categories starting from base layer, followed by middle and upper layers and a top layer. The categories can be briefly summarised through the below chart (visit https://vinodkothari.com/sbr/ to read our write-ups on SBR and related topics).

Overview of the Scalar Approach for Classifying NBFCs

Through SBR, various governance guidelines have been newly introduced while the existing guidelines have been modified to keep up with the current market practices. One of the requirements is the introduction of Core Financial Services Solution (CFSS) for NBFCs videRBI circular dated February 23, 2022 (‘CFSS Circular’).

In this article, we discuss the applicability of CFSS on NBFCs, explore the current core banking systems of banks, highlight the necessary modules which can be adopted by NBFCs along with the issues that may arise during implementation.

Recently, the Ministry of Corporate Affairs (MCA) has implemented a series of amendments which relates to investments in India by foreign nationals or entities incorporated in a country which shares a land border with India. These amendments are in tandem with the amendment made by the Department for Promotion of Industry and Internal Trade (DPIIT) in FDI Policy and by the Ministry of Finance, Department of Economic Affairs, in FEM (Non Debt Instruments) Rules, 2019 (NDI Rules).

DPIIT amended the FDI policy vide press note no. 3 dated 17 April, 2020 to curb the hostile takeovers of Indian Companies by nationals/entities of neighbouring countries. Erstwhile, only a citizen of Bangladesh & Pakistan or an entity incorporated in Bangladesh & Pakistan were required to take government approval for investing in India. Pursuant to amendment, any entity incorporated in a country, citizen or beneficial owner of a country, which shares land border with India, needs to obtain government approval for investing in the equity instrument of the Indian Company. Thus, nationals/entities from Pakistan, Afghanistan, China, Bhutan, Nepal, Myanmar and Bangladesh can invest in India only under approval route.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-06-16 17:30:142022-06-16 17:30:16Investments from neighbouring countries under stringent scan of GoI

Response: Regulation and control of “large exposures” is a part of financial sector regulations globally to control concentration of exposures (thus, risks) to a few individuals/entities/groups. The Basel Committee of Banking Standards has been having recommendatory pieces on this topic since 1991, if not earlier. The Basel standard subsequently became a part of the Basel capital adequacy framework.

There is a large exposures framework in case of banks as well.

The intent behind the large exposure framework, which essentially limits the exposures to a single entity or group or group of economically interdependent entities is to strengthen the capital regulations. Capital regulations prescribe minimum capital in case of financial entities. The adequacy of capital is obviously connected with the risks on the asset side – hence, if the assets represent exposure in a single borrower or economically connected group of borrowers, a credit event with respect to such borrower may deplete the adequacy of capital very quickly. Hence, regulators limit the exposure to a single entity or a group.

There might be other forms of credit concentrations – for example, sectoral or geographical concentrations – these are not captured by the Framework.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2022-06-14 13:36:372022-09-23 12:13:06FAQs on Large Exposures Framework (‘LEF’) for NBFCs under Scale Based Regulatory Framework

The function of NBFCs as a supplemental route of credit intermediation alongside banks and its contribution to supporting real economic activity are well known. Within the financial sector, the NBFCs have grown significantly in terms of scale, complexity, and interconnectedness over time. Many companies have expanded to the point where they are systemically significant, necessitating the alignment of the regulatory framework for NBFCs in light of their shifting risk profile.

To address the same, RBI vide its circular dated October 22, 2021[1] has introduced Scale Based Regulation (SBR) for all NBFCs and has classified NBFCs in four layers- Base, Middle, Upper and Top layer.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2022-06-07 18:46:262022-09-23 12:13:22Differential Standard Asset Provisioning for NBFC-UL

Everyone has probably had some form of interaction with the concept of embedded finance while possibly not knowing what it is. This budding concept has its eyes set on massively changing the way business is done.

Today, convenience in trade and commerce is probably the most sought after by customers. The idea of having everything in one place at high speeds is what drives trade in this modern world. This is where embedded finance would come into play.

Embedded Finance (‘EmFi’) is a concept that typically allows non-financial entities to integrate financial services/ products into its own platform through the use of APIs (‘Application Programming Interface’) which is a software intermediary that allows two applications to talk to each other.

Put simply in the form of an example, let’s say you want to purchase a flight ticket. You reach the payment stage and see an option to purchase insurance as well, without having to leave the app you are currently using. This integration of an insurance purchase on a non-financial entities platform is just one small part of the bigger picture of embedded finance.

This article will focus on explaining the concept of embedded finance with specific focus on embedded lending.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-06-03 17:50:522022-06-03 17:50:54Foreign nationals to comply with stringent MCA norms

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-06-02 12:26:522022-06-30 11:18:31Conference on Secondary Markets in Distressed Loans

The table below provides the rate of stamp duty applicable on assignment of receivables in major states across India:

State

Stamp Duty

Andhra Pradesh

0.1% of the loan securitized or debt assigned with underlying securities subject to maximum limit of Rs.1 Lakh. [1]

Assam

8.25 percent.

Bihar

0.1% of the loan securitized or debt assigned with underlying securities subject to maximum limit of Rs.1 Lakh[2].

Chhattisgarh

0.1% of the loan securitized or with underlying securities subject to maximum limit of Rs.1 Lakh[3].

Delhi

one rupee for every one thousand rupees or part thereof, of the loan securitized or the debt assigned with underlying securities, subject to a maximum of Rs 1 lakh.[4]

Goa

8 percent.

Gujarat

Bombay Stamps Act, 1958 (as applicable to the state of Gujarat) , No. GHM – 98-221H.STP/1096/2527/H.1. In exercise of the powers conferred by Clause (a) of Section 9 of the Bombay Stamp Act. 1958 (Bom LX of 1958), the Government of Gujarat hereby reduces the duty with which an instrument of securitisation of Loans or the Assignment of Debt with underlying securities is chargeable under Article 20(a) of Schedule 1 to the said Act, to ten paise for every rupees 100 or part thereof of the loan securitised or debt assigned with underlying securities’ subject to a maximum of rupees 1 lakh[5].

Haryana

Approx. 12.5% for conveyance amounting to sale for immovable property and 6.25% for other conveyances.

Karnataka

Karnataka Stamp Act, 1957.The Government of Karnataka, Department of Stamps & Registration have specified that that with effect from 1st April 1999, ‘Deeds relating to assignment of receivables in the process of securitisation will be charged to a reduced duty of 0.1% subject to a maximum of Rs. One Lakh.’[6] Two rupees for every thousand rupees or part thereof subject to a maximum of rupees five lakhs, effective from 3rd February 2024.

Madhya Pradesh

Stamp duty of 7.5% of amount of debt assigned.

Maharashtra

Bombay Stamp Act, 1958. ‘Order dated 11th May 1994, No. STP. 1094/CR-369/(C)-M-1 – In exercise of the powers conferred by Clause (a) of Section 9 of the Bombay Stamp Act, 1958 (Bom. LX of 1958), the Government of Maharashtra hereby reduces with effect from 1st April 1994 the duty with which an instrument of securitisation of Loans or Assignment of Debt with underlying securities is chargeable under Clause (a) of Article 25 of Schedule 1 to the said Act, to ‘Fifty Paise’ for every rupees 500 or part thereof of the loan securitised or debt assigned with underlying securities subject to a maximum of Rs 1 lakh and in case of instrument of Assignment of Receivables in respect of use of credit cards to ‘Two Rupees and Fifty Paise for every rupees 500 or part thereof.’ subject to a maximum of Rs 1 lakh.[7]

Manipur

7 percent.

Meghalaya

upto Rs 50,000 – 4.6%, more than Rs 50,000 and upto Rs 90,000 – 6%, more than Rs 90,000 and upto Rs 1,50,000 – 8% , More than Rs 1,50,000 – 9.9%.

Nagaland

7.5 percent.

Odisha

0.1% of the amount or value of the consideration set forth in the said instrument.[8]

Punjab

3 percent.

Rajasthan

In exercise of the powers conferred by sub-section (1) of section 9 of the Rajasthan Stamp Act, 1998 (Act No. 14 of 1999) and in supersession of this department’s Notification No. F.4(4) FD/Tax/2015-230 dated March 9, 2015, the State Government, stamp duty chargeable on the instrument of debt assignment executed in respect of performing assets (standard assets) is charged at the rate of 0.15 percent of the amount of debt subject to maximum of rupees five lacs.[9]

Tamil Nadu

In exercise of the powers conferred by clause (a) of sub-section (1) of], the governor of Tamil Nadu hereby reduces the duty chargeable under the said act to ten paise for every Rs 100or part thereof the market value of the property which is the subject matter of conveyance, subject to the maximum of Rs 1 lakh, in respect of the instruments providing for transfer of non-performing assets or assignment of debt with or without underlying securities whether movable or immovable or intangible. in favour of reconstruction companies under SARFAESI act ,2002. the notifications appended to this order will be published in an extraordinary issue of Tamil Nadu government gazette dated 4-3-2005.

The stamp duty was reduced to 5% vide notification no. 297/XXVII (9)/2011/Stamp-61/2009 dated May 31, 2011 issued by the Department of Finance, State of Uttarakhand and is currently applicable. However, the said exemption is applicable only upto the value of the property being 25 lakhs. In the event the value exceeds 25 lakhs, then upto 25 lakhs, the stamp payable will be reduced by 25% i.e. 3.75% of market value will be payable, and above 25 lakhs, the stamp duty will be paid at 5% of market value.

[1] Notification G.O.Ms. No.305 dated 29.03.2004 issued by Registration and stamps Department, Government of Andhra Pradesh. This shall apply to ARC’s.

[2] Notification S.O.No.-1/M1-126-2004/2904 dated 29.12.2004 issued by Department of Registration, Government of Bihar. This shall apply to ARC’s.

[3] Notification No./F10-9-2004-C.T.-(R) –V-(32) dated 28.02.2004 issued by Financial and Planning Department {Commercial Tax (Registration) Department}, Government of Chhattisgarh.

[8] 1. Notification No. Stamp-6/05/35723/R. dated 31.08.2005 issued by Revenue Department, Government of Orrisa. 2. Notification No. Stamp-6/05/35723/R. dated 31.08.2005 issued by Revenue Department, Government of Orrisa.

[10] Notification No.K.N.5-1023/11-2005-500(137)-2003 dated 15.03.2005 as amended by No.K.N.5-1389/11-2005-500(137)/2003 dated 29.03.2005 issued by Kar Evam Nibandhan Anubhag-5, Government of Uttar Pradesh.

[11]Notification No.2307-F.T. dated 02.07.2004 issued by Finance (Revenue) Department, Government of West Bengal.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-06-01 15:54:342024-05-07 18:22:09Stamp Duty on Assignment of Receivables