Workshop on Covered Bonds

Registrations can be made here:

https://docs.google.com/forms/d/e/1FAIpQLScR1WNKaoKyQIQxRKgZShcoLHHM9VprFX4FYswqGgGMfTzQNA/viewform

Registrations can be made here:

https://docs.google.com/forms/d/e/1FAIpQLScR1WNKaoKyQIQxRKgZShcoLHHM9VprFX4FYswqGgGMfTzQNA/viewform

– Abhirup Ghosh (abhirup@vinodkothari.com)

The pandemic disrupted life economies across the globe, and so did it to securitization transactions. However, increase in vaccinations across the globe has had a positive impact on the most of the structured finance markets world-wide, but potential new variants continue to be a threat.

This write-up reviews the performance of securitization across the major jurisdictions.

By CS Aisha Begum Ansari (aisha@vinodkothari.com)

When you go silent, you may be doing a soul searching, as for example, in meditational techniques. However, in case of listed entities, silent period is a period just before declaration of financial results, to ensure that there is no accidental leakage of confidential information. Silent period is different from “trading window closure” that most corporate professionals in India are familiar with. However, this article discusses the relevance of silent period, as a subset of the trading window closure, and its relevance to listed entities in India. While exploring the topic, the author also makes a study of the global laws around silent period.

Insider trading is a ‘white collar’ crime that seeks to exploit the unpublished, non-democratic information (that is, what is not available in public domain) to the advantage of a select few, and to the disadvantage of the market in general. Since, it is a fraud upon the market in general, it has always been a significant topic for the securities market regulators around the globe. In India, Securities and Exchange Board of India (‘SEBI’) has framed the regulatory framework to curb the insider trading called as SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’).

The material inside information is generally accessed by the top executives and employees of the company. To avoid the exploitation of such information, the company prohibits them from trading in its securities while having access to such information. The preventive framework of insider trading does not just end by prohibiting the employees from trading; it also needs to ensure that such material inside information is not leaked outside the organization. There are many ways used by the insiders to leak such information such as sharing the same on social media, sharing of information during analyst or institutional investor meets, etc.

Silent period is different from trading window closure. Silent period is when the company’s top executives, say that CEO, CFO etc. will refrain from doing public communications altogether. The intent is to ensure that there is no interaction with investors or public at large, so as to avoid unintended slippage of information. Currently, SEBI regulations do not require companies to mandatorily observe a silent period; therefore, companies may choose to adopt this practice by way of their Code of Fair Disclosure.

A silent period (also known as quiet period) is a stipulated time during which a company’s senior management and investor relation officers do not interact with the institutional investors, analysts and the media. The purpose of the silent period is to preserve the objectivity and avoid the appearance of the company providing insider information to select investors. During the silent period, the company does not make any announcements that can cause a normal investor to change their position on the company’s securities.

Trading window closure period (also known as blackout period or closed period) refers to the period during which the employees of the company who have access to material inside information are prohibited from trading in the securities of the company. In some of the developed countries, the securities market regulators give a freehand to the companies to decide the period during which the trading window shall be closed. In India, the PIT Regulations provide that the companies shall close the trading window from the end of the closure of the financial period for which results are to be announced till 48 hours after the disclosure of financial results to the stock exchanges. For any other material inside information, SEBI has given the responsibility to the compliance officers of the companies to close the trading window when the employees can reasonably be expected to have possession of inside information.

Silent period differs from the trading window closure in such a way that trading window closure prohibits the employees to trade in the securities of the company while having access to material inside information and silent period prohibits or restricts the company’s spokespersons to interact with the institutional investors or analysts. The purpose of trading window closure is to prohibit trading on the basis of inside information and the purpose of silent period is to prohibit communication of inside information illegitimately.

The PIT Regulations or any other regulatory framework in India do not provide for the requirements of silent period. So, the duration of silent period differs from company to company. Some companies specify the silent period as 20-30 days before the declaration of financial results till the date of disclosure and some companies align the silent period with the trading window closure period. The following table gives the synopsis of the practice followed by the Indian listed entities regarding silent period:

| Name of the Company | Practice followed |

| Mahindra & Mahindra Limited | Silent period commences from 20 days before the declaration of financial results till the date of disclosure of results |

| Tata Consultancy Services Limited | Quiet period starts 20 days before the declaration of financial results till the date of disclosure of results |

| HCL Technologies Limited | Silent period is same as trading window closure period |

| Asian Paints Limited | Silent period is observed between the end of the period and the publishing of the stock exchange release for that period |

| Wipro Limited | Quiet period commences from 16th day of the last month of the quarter and ends with 48 hours after earnings release. |

| Infosys Limited | Silent period is observed between the 16th day prior to the last day of the financial period for which results are required to be announced till the earnings release day. |

Thus, it can be concluded that the silent period is smaller than the trading window closure period.

Analysts/ investors meets can be a medium of leak of material inside information, therefore, the companies avoid interaction with them during trading window closure period. So, does it mean that companies completely abstain from interacting with the analysts and investors? While the answer may differ from company to company and the policies adopted by them for communication with analysts and investors. Some companies completely refrain from the analysts/ investors meets while some companies interact with them and discuss the past and historical information which is already available in public domain and general future prospects of the company, dodging the specific questions relating to the material inside information.

While the regulations framed by SEBI are silent about the silent period, the Guidelines for Investor Relations for Listed Central Public Sector Enterprises issued by the Department of Disinvestment, Ministry of Finance, Government of India, provides for the duration of silent period and obligations of the public sector enterprises in this regard. The Guidelines advise that the silent period should commence 15 days prior to the date of Board meeting in which financial results are considered and end 24 hours after the financial results are made public. The Guidelines requires the companies to abstain from meeting the analysts and investors and not communicate with them unless such communication would relate to the factual clarifications of previously disclosed information.

| Country | Trading window closure period | Silent period | Analyst meet during silent period |

| United States of America (USA)[2] | USA laws do not provide any specific timeline for trading window closure period. Thus, the companies are free to determine it | There are two types of silent period prevalent in USA:

1. When the company makes an Initial Public Offering (‘IPO’) – the Securities Exchange Commission (‘SEC’) mandates such companies to maintain a silent period from the date of registration with SEC which lasts till 40 days after the securities begin to trade on the stock exchanges. Such silent period is heavily regulated by the SEC. 2. During finalization of quarterly results – the silent period is not clearly defined by SEC. |

During the silent period, the interaction with the analysts and investors is reduced. The companies either go completely silent or they speak about only past and historical information. |

| United Kingdom (UK)[3] | Unlike USA, the UK laws prescribe the trading window closure period. Article 19.11 of Market Abuse Regulations specifies the period of trading window closure starting from 30 calendar days before the announcement of an interim financial report or a year-end report till the second trading day after announcement of financial report. | UK laws do not comment anything about the silent period. Thus, the companies determine the silent period as per their own discretion.

|

Since UK laws do not provide for silent period, the companies, as per their discretion, avoid interactions with the analysts and investors during such period.

|

| Canada[4] | Para 6.10 of National Policy on Disclosure Standards (‘Policy’) discusses about blackout period. It states that the company’s insider trading policy should specify the period which may mirror the quiet period. | Para 6.9 of the Policy talks about quiet period. While the Policy does not prescribe the duration of quiet period, it states that the period should run between the end of the quarter and the release of a quarterly earnings announcement. | The Policy states that the company need not completely stop communicating with the analysts and investors during the quiet period, but the communication should be limited to responding to inquiries concerning publicly available or non-material information. |

After discussing the practices followed by the Indian listed companies and the regulatory framework of other developed countries, it can be concluded that the concept of silent period is not something new, though unregulated. Some companies align the silent period with the trading window closure period while some provide for lesser duration for silent period. Some companies completely abstain from interacting with the analysts and the institutional investors during the silent period whereas some prefer discussing the generally available information only.

[1]https://www.dipam.gov.in/dipam/downloadFile?fileUrl=resources/pdf/capital-market-regulation/IR_Guidelines_website.doc

[2] https://www.irmagazine.com/reporting/six-commonly-asked-questions-and-answers-about-quiet-periods

[3] https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0596&from=EN

[4] http://ccmr-ocrmc.ca/wp-content/uploads/51-201_np_en.pdf

Other relevant materials of interest can be read here –

https://vinodkothari.com/2021/07/step-by-step-guide-for-disclosure-for-analysts-investors-meet/

https://vinodkothari.com/2021/05/sebi_defines_investors_meet/

Ajay Kumar KV, Manager and Himanshu Dubey, Executive (corplaw@vinodkothari.com)

The role or failure of independent directors in preventing corporate scandals became one of the central themes in corporate governance in India, and when SEBI issued a Consultation paper proposing a dual approval process for the appointment of independent directors, there was a substantial concern among leading companies in the country. Following discussions, the SEBI board has eventually decided to drop the proposal for dual approval, and instead, go for approval by a special majority. The decision of SEBI to not implement dual approval has not been appreciated by several commentators including Mr. Umakanth Varottil. Therefore, there is a sizzling controversy on the mode of appointment of independent directors.

In this article, we have made a comparison of the legislative framework for independent directors, especially the process of appointment, across various jurisdictions. While we note that some countries have moved to a dual approval process, the concept such as a database of IDs and a proficiency test remains an Indian aberration.

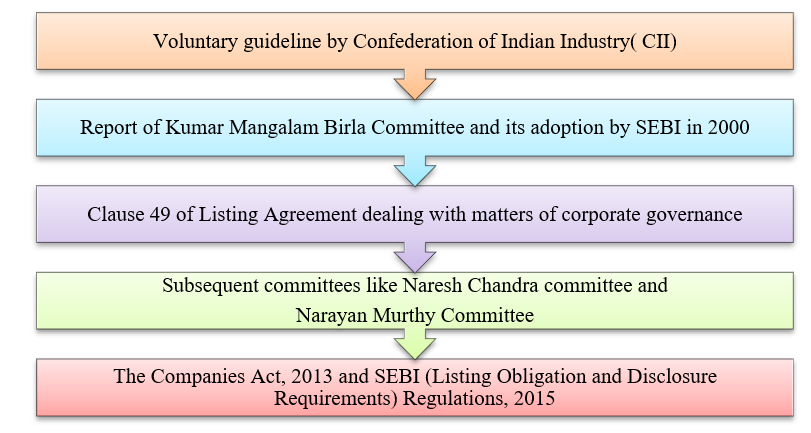

In India, the idea, or rather the need of having Independent Directors on the board of companies (especially those involving public interest) was acknowledged in the early 2000s through the SEBI Listing Agreement. Therefrom, the concept found a concrete legislative recognition in late 2013 as the Companies Act, 2013 took shape and character covering unlisted companies as well.

A snapshot of the concept’s evolution through guidelines and report to the Companies Act and SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 is given below –

As compared to India, the western world was way ahead in the race- the concept of Independent Directors traces its inception as long back as in the 1950s when the murmurs of representation of small shareholders surrounded the corporate world. However, like in India, it took a long time for countries in Europe and North America to bring the concept within the regulatory framework. In the USA, the concept of Independent Director received regulatory recognition under the Sarbanes-Oxley Act, 2002. Thereafter the regulations issued by various stock exchanges took the lead.

With all the hullabaloo about Independent Director, the natural question was ‘who is an independent director’; while the terminology was largely suggestive of the answer – “someone who is capable of putting forth an independent view about the business of the company”, it was crucial to define the term.

The definition of Independent Director from Section 149 of the Companies Act, 2013 (‘Act’) and Regulation 16 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘LODR’). While unlisted companies are required to adhere to the requirement under section 149 of the Act; listed companies or those intending to be listed are required to abide by LODR too.

On the same lines as discussed above, LODR identifies an independent director as someone who is not related to the company, either as a promoter or director of the company, its group companies, who do not have a material pecuniary relationship with the company or its group, as well as someone who does not or has not been related to the company in any manner in the recent position, such that s/he could influence the decisions/ business of the company.

The aforesaid is provided in Regulation 16 of LODR[1], which defines “Independent Director” as “a non-executive director, other than a nominee director of the listed entity, who:

[(A) is holding securities of or interest in the listed entity, its holding, subsidiary or associate company during the three immediately preceding financial years or during the current financial year of face value in excess of fifty lakh rupees or two percent of the paid-up capital of the listed entity, its holding, subsidiary or associate company, respectively, or such higher sum as may be specified;

(B) is indebted to the listed entity, its holding, subsidiary or associate company or their promoters or directors, in excess of such amount as may be specified during the three immediately preceding financial years or during the current financial year;

(C) has given a guarantee or provided any security in connection with the indebtedness of any third person to the listed entity, its holding, subsidiary or associate company or their promoters or directors, for such amount as may be specified during the three immediately preceding financial years or during the current financial year; or

(D) has any other pecuniary transaction or relationship with the listed entity, its holding, subsidiary or associate company amounting to two percent or more of its gross turnover or total income:

Provided that the pecuniary relationship or transaction with the listed entity, its holding, subsidiary or associate company or their promoters, or directors in relation to points (A) to (D) above shall not exceed two percent of its gross turnover or total income or fifty lakh rupees or such higher amount as may be specified from time to time, whichever is lower;]*

[Provided that in case of a relative, who is an employee other than key managerial personnel, the restriction under this clause shall not apply for his / her employment.]*

Evidently, the definition in India is very comprehensive compared to other major jurisdictions. Below we discuss and compare some major provisions in the definition of IDs in India, the USA and the UK –

| Basis | India | USA[2] | UK[3] |

| Material relationship | The director shall, apart from receiving director’s remuneration, has or had no material pecuniary relationship with the listed entity, its holding, subsidiary or associate company, or their promoters, or directors, during the three immediately preceding financial years or during the current financial year;

None of the director’s relatives [(A)is holding securities of or interest in the listed entity, its holding, subsidiary or associate company during the three immediately preceding financial years or during the current financial year of face value in excess of fifty lakh rupees or two percent of the paid-up capital of the listed entity, its holding, subsidiary or associate company, respectively, or such higher sum as may be specified;

(B) is indebted to the listed entity, its holding, subsidiary or associate company or their promoters or directors, in excess of such amount as may be specified during the three immediately preceding financial years or during the current financial year;

(C) has given a guarantee or provided any security in connection with the indebtedness of any third person to the listed entity, its holding, subsidiary or associate company or their promoters or directors, for such amount as may be specified during the three immediately preceding financial years or during the current financial year; or

(D) has any other pecuniary transaction or relationship with the listed entity, its holding, subsidiary or associate company amounting to two percent or more of its gross turnover or total income:

Provided that the pecuniary relationship or transaction with the listed entity, its holding, subsidiary or associate company or their promoters, or directors in relation to points (A) to (D) above shall not exceed two percent of its gross turnover or total income or fifty lakh rupees or such higher amount as may be specified from time to time, whichever is lower;]* |

The director qualifies as “independent” unless the board of directors affirmatively determines that the director has no material relationship with the listed company (either directly or as a partner, shareholder, or officer of an organization that has a relationship with the company).

The references to “listed company” would include any parent or subsidiary in a consolidated group with the listed company |

The director has, or had within the last three years, no material business relationship with the company, either directly or as a partner, shareholder, director or senior employee of a body that has such a relationship with the company;

The director has not received or receives additional remuneration from the company apart from a director’s fee, participates in the company’s share option or a performance-related pay scheme, or is a member of the company’s pension scheme |

| Employment | The director neither himself/herself nor his relatives hold or has held the position of a key managerial personnel or is or has been an employee of the listed entity or its holding, subsidiary or associate company, [or any company belonging to the promoter group of the listed entity]* in any of the three financial years immediately preceding the financial year in which he is proposed to be appointed.

[Provided that in case of a relative, who is an employee other than key managerial personnel, the restriction under this clause shall not apply for his / her employment]*

|

The director is not independent if the director is, or has been within the last three years, an employee of the listed company or an immediate family member is, or has been within the last three years, an executive officer, of the listed company.

The director has received or has an immediate family member who has received, during any twelve-month period within the last three years, more than $120,000 indirect compensation from the listed company, other than director and committee fees and pension or other forms of deferred compensation for prior service (provided such compensation is not contingent in any way on continued service). |

The director neither is or has been an employee of the company or group within the last five years |

| Promoter/director or related to them | The director is or was not a promoter of the listed entity or its holding, subsidiary or associate company or member of the promoter group of the listed entity;

Who is not related to promoters or directors in the listed entity, its holding, subsidiary, or associate company;

|

No director qualifies as “independent” unless the board of directors affirmatively determines that the director has no material relationship with the listed company either directly or as a partner, shareholder, or officer of an organization that has a relationship with the company. | The director has close family ties with any of the company’s advisers, directors, or senior employees. |

| Cross-directorship | The director is not a non-independent director of another company on the board of which any non-independent director of the listed entity is an independent director

|

The director or an immediate family member is or has been with the last three years, employed as an executive officer of another company where any of the listed company’s present executive officers at the same time serves or served on that company’s compensation committee. | The director holds cross-directorships or has significant links with other directors through involvement in other companies or bodies |

One may find many similarities in the definition of IDs in foreign jurisdictions with that in India but as already mentioned above, the definition in India is one of the most comprehensive and meticulous ones.

Appointment/reappointment process of IDs in different jurisdictions

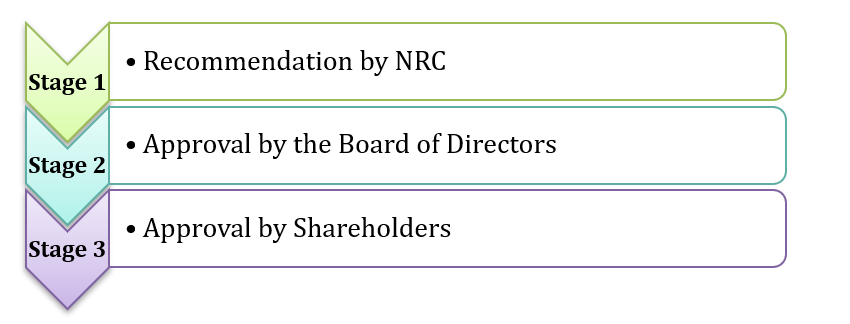

In India, the extant provisions require ordinary resolution to be passed by the shareholders for the appointment of IDs and a special resolution in case of re-appointment, based on the recommendation of the Nomination and Remuneration Committee (NRC) and the approval of the Board.

Earlier, SEBI had released a consultation paper w.r.t. regulatory provisions for Independent Directors which warranted a ‘dual approval’ for such appointment/ re-appointment as follows:

(Note: The Paper defined minority shareholders to mean shareholders other than the promoter and promoter group.)

However, owing to the response received thereafter, SEBI, in its Board Meeting held on June 29, 2021[4] (SEBI Board Meeting), disregarded the earlier proposal of a dual approval and instead decided that the approval of shareholders would be required by way of special resolution for both appointment and re-appointment

[SEBI, vide (Listing Obligations and Disclosure Requirements) (Third Amendment) Regulations, 2021 ( ‘Amendments’) notified on August 4, 2021, have amended the Regulation 25 providing that the appointment, re-appointment or removal of an independent director of a listed entity, shall be subject to the approval of shareholders by way of a special resolution. Thus, listed entities henceforth shall have to obtain the approval of members via a special resolution for the appointment as well.]*

In the USA, the NASDAQ Listing Rules provide that, where shareholders’ approval is required, the minimum vote that will constitute shareholder approval shall be a majority of the total votes cast on the proposal.

Akin to the NRC in India, the UK Corporate Governance Code of 2018 requires that the Board should establish a Nomination Committee, composed of majority independent non-executive directors, to lead the process for the appointment of all directors. Any appointment must be approved by the Board and shareholders of the company by way of an ordinary resolution.

However, as per the UK Listing Rules, the appointment of IDs is dependent on the existence of a controlling shareholding[5]. A snapshot of the manner of appointment is given below

Hence, approval is required from both the set of shareholders. If the company still proposes to appoint the same person as an independent director despite failing to receive the dual nod as discussed above, it can propose another resolution to elect the same person, but after 90 days from the date when the previous proposal was put to vote. This time the resolution will only require approval by the shareholders of the company[6].

Databank of Independent Directors & the Online Proficiency Test

One of the prerequisites to become an Independent Director in India is the inclusion of their name in the Databank of Independent Directors (‘Databank’) and passing an Online Proficiency Test (‘Test’) within a period of two years from the date of inclusion of name in the databank as per Section 150 of the Act, read with Rule 6 of the Companies (Appointment and Qualification of Directors) Rules, 2014. However, certain categories of persons have been exempted[7] from the requirement of passing the Test who possess requisite experience and expertise as prescribed;

The question, however, is whether such arduous and tedious criteria required for an appointment really ensure board independence and good governance practices. It is understood that the tenet behind such steps was quality control – it was to ensure that only persons with a certain minimum level of expertise & experience are appointed as Independent Directors.

Further, some previous instances of celebrity directorships were also to be discouraged since the role of IDs is to ensure good governance practices and upholding the interest of all the stakeholders as a whole including minority stakeholders. Therefore, it should not merely be used as a tool of publicity.

However, keeping in mind the seniority of the position of directors in companies as well as lack of precedent, the requirement of passing the test seems rather odd and brings anomalies in the IDs’ regulatory regime in India vis-à-vis the rest of the world.

Constituted Body for selection of candidates for the role of IDs

As per the extant laws in India, the NRC recommends the persons to be appointed as IDs on the board of the company. This committee oversees the functions of formulation and recommendation of remuneration of the directors and the senior management. It has been decided in the SEBI Board Meeting that the process to be followed by NRC while selecting candidates for appointment as IDs, shall be elaborated and be made more transparent including enhanced disclosures regarding the skills required for appointment as an ID and how the proposed candidate fits into that skillset.

[SEBI, via the Amendments, has added a new sub-clause after sub-clause (1) in Para A in Part D of Schedule II for implementing its decision on an elobaroted and transparent selection oricess of IDs.

The NRC of every listed entities shall, for every appointment of IDs,

For the purpose of identifying suitable candidates, the Committee may:

Thus, the NRCs of every listed company henceforth has to first formulate the description of the role of an ID after considering the skill sets and knowledge and experience required for acting as an ID of the company. This has also widened the scope of NRC as well as the responsibility for finding the right candidate for the position of an ID. The extant practice was to give disclosures in Corporate Governance Report and the Board report that forms part of the Annual Report of the Company.]*

Just like the NRC in India, companies in the USA have to constitute Compensation Committee as per the NASDAQ Stock Market LLC Rules [5605. Board of Directors and Committees] “Each Company must have, and certify that it has and will continue to have, a compensation committee of at least two members. Each committee member must be an Independent Director as defined under Rule 5605(a) (2).”

As per the NASDAQ Rules, director nominees must either be selected, or recommended for the Board’s selection, either by:

The New York Stock Exchange Listed Company Manual (‘NYSE Manual’) vests on the nominating/corporate governance committee, the sole authority to retain and/or terminate any search firm to be used to identify director candidates, including sole authority to approve the search firm’s fees and other retention terms.

The UK Corporate Governance Code, 2018 states that the board should establish a remuneration committee of independent non-executive directors, with a minimum membership of three, or in the case of smaller companies, two. In addition, the chair of the board can only be a member if they were independent on appointment and cannot chair the committee. Before appointment as chair of the remuneration committee, the appointee should have served on a remuneration committee for at least 12 months.

In India, one term of appointment of IDs is for a maximum of 5 years and can be re-appointed for another term. Such re-appointment has to be made by way of passing a special resolution. Further, the performance of Independent Directors is to be evaluated every year based on which the NRC recommends whether the said director shall be re-appointed or not. However, the question of such recommendation only comes when the tenure of the director comes to its end.

Furthermore, the UK Corporate Governance Code provides that all directors should be subject to annual re-election. The code also considers the presence of an ID for more than nine years on the Board of a company as a threat to his independence.

In Singapore, Rule 720(5) of the SGX Listing Rules (Mainboard) / Rule 720(4) of the SGX Listing Rules (Catalist)[8] requires all directors to submit themselves for re-nomination and re-election at least once every three years.

The rule requires a re-nomination & re-election of all directors of the company at least once in 3 years and it helps to ensure that the assessment of independence happens once in every 3 years by members.

In India, a cooling-off period of 2 years is required in case of any material pecuniary transactions between a person or his/her relative and the listed entity or its holding, subsidiary, or associate company. The LODR has prescribed a cooling-off period of three years for Key Managerial Personnel (and their relatives) or employees of the promoter group companies, for appointment as an ID in the listed entity. However, relatives of employees of the company, its holding, subsidiary, or associate company have been permitted to become IDs, without the requirement of a cooling-off period, in line with the Companies Act, 2013.

[SEBI via Amendments has provided that an ID who resigns from a listed entity, shall not be appointed as an executive / whole time director on the board of the listed entity, its holding, subsidiary or associate company or on the board of a company belonging to its promoter group, unless one year has elapsed from the date of resignation.]*

The NASDAQ Stock Market LLC Rules[9] (‘NASDAQ Rules’) have prescribed a cooling-off period of 3 years for the appointment of an independent director where such person has a relationship with the company as prescribed under the rule.

UK Corporate Governance Code, 2018[10] (‘UK Code’) provides that a person who has or had within the last three years, a material business relationship with the company, either directly or as a partner, shareholder, director, or senior employee of a body that has such a relationship with the company shall not be appointed as an Independent Director.

The Singapore Code of Corporate Governance, 2018[11] prescribes a cooling-off period of 3 years for the appointment of an independent director where such person has a relationship with the company.

Remuneration of Independent Directors

In India, offering stock options to Independent Directors is prohibited. On the contrary, as per the New York Stock Exchange Listed Company Manual (‘NYSE Manual’), Independent directors must not accept any consulting, advisory, or other compensatory fees from the Company other than for board service.

Further, the UK Corporate Governance Code 2018 provides that remuneration for all non-executive directors should not include share options or other performance-related elements. Independent directors shall not be a member of the company’s pension scheme.

The Singapore Code of Corporate Governance 2018 the Remuneration Committee should also consider implementing schemes to encourage non-executive directors (NEDs) to hold shares in the company so as to better align the interests of such NEDs with the interests of shareholders. However, NEDs should not be over-compensated to the extent that their independence may be compromised.

Fees payable to non-executive directors shall be by a fixed sum, and not by a commission on or a percentage of profits or turnover. (Appendix 2.2 Articles of Association)

Important determinants of Independence across jurisdictions

| Determinants of Independence | India | USA | UK | Singapore |

| Present or past employment relationship | Yes | Yes | Yes | Yes |

| Relationship of close family members | Yes | Yes | Yes | Yes |

| Pecuniary relationship with company* | Yes | Yes | Yes | Yes |

| Cooling-off period | Yes | Yes | Yes | Yes |

| Restriction on Stock options | Yes | Yes | Yes | No |

| ID databank & Proficiency test | Yes | No | No | No |

* Subject to specific monetary limits

The regulatory framework for Independent Directors in India has a lot of things in common with other jurisdictions around the world. However, the requirement of passing an online test for becoming eligible to be appointed as an Independent Director is something peculiar to India. The regulators across jurisdictions have been proactive in bringing changes to the Independent Director regime, to strengthen the corporate governance in listed companies. One may expect some of the above discussed benchmark practices in different foreign jurisdictions may soon be adopted in India as well.

Related presentation – https://vinodkothari.com/2021/08/ensuring-board-continuity-and-balance-of-capabilities/

[1] https://www.sebi.gov.in/legal/regulations/sep-2015/securities-and-exchange-board-of-india-listing-obligations-and-disclosure-requirement-regulations-2015-last-amended-on-may-5-2021-_37269.html

[2] https://nyse.wolterskluwer.cloud/listed-company-manual

[3]https://www.frc.org.uk/getattachment/88bd8c45-50ea-4841-95b0-d2f4f48069a2/2018-UK-Corporate-Governance-Code-FINAL.PDF

[4] https://www.sebi.gov.in/media/press-releases/jun-2021/sebi-board-meeting_50771.html

[5] A company is said to have controlling shareholder(s) if a shareholder/ an entity/ a group holds more than 30% voting power in the company

[6] https://www.mondaq.com/uk/acquisition-financelbosmbos/315598/new-dual-process-for-appointing-independent-directors-amendments-to-articles-of-association

[7] https://www.independentdirectorsdatabank.in/pdf/databank-rules/FifthAmdtRules_18122020.pdf

[8] https://rulebook.sgx.com/rulebook/board-matters-1

[9] https://listingcenter.nasdaq.com/rulebook/nasdaq/rules

[10] https://www.frc.org.uk/getattachment/88bd8c45-50ea-4841-95b0-d2f4f48069a2/2018-UK-Corporate-Governance-Code-FINAL.PD

[11] https://www.mas.gov.sg/-/media/MAS/Regulations-and-Financial-Stability/Regulatory-and-Supervisory-Framework/Corporate-Governance-of-Listed-Companies/Code-of-Corporate-Governance-6-Aug-2018.pdf

*[ The changes are applicable with effect from 1st January, 2022].

Payal Agarwal and Aanchal Kaur Nagpal ( corplaw@vinodkothari.com)

It will be ironic to the extent of being harsh to say that the Covid outbreak is a brutal reminder that mankind needs to ensure a balance between economic growth and environmental conservation. Environmental, Social and Governance (“ESG”) concerns have sharply risen globally, underscoring the financial relevance of various non-financial elements impacting business in several ways. In this scenario, one of the key areas of concern has been climate change. The United Kingdom (“UK”) recently proposed[1] significant changes in the regulatory framework in order to include mandatory climate-related financial disclosures in the regulatory regime. This article discusses the legislative measures proposed in the UK, and takes a look at what other countries are doing in this regard.

Task Force on Climate-related Financial Disclosures or (“TCFD”), as the name suggests, was established in 2015 with the main aim of providing recommendations as to how the climate-related disclosures can be brought to the mainstream financial reports. Established by the former Chairman of the Bank of England, UK, it is an internationally recognised body. It published its recommendations in the year 2017 highlighting what all should be included in the climate-related financial disclosures and how the companies and other corporate organisations can approach the climate related disclosures in its financial reports.

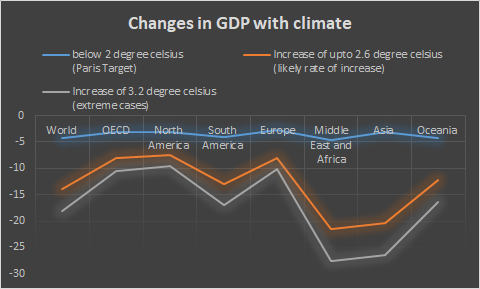

Studies have shown that global temperature rises will negatively impact GDP in all regions by 2050 whereas economies in southeast Asia (ASEAN) countries would be hit hardest. If climate risks are not properly managed, the Intergovernmental Panel on Climate Change estimates $69 trillion in global financial losses by 2100 from a 2-degree warming scenario. The Paris Agreement of 2016 was the first integrated approach towards recognizing the impact of climatic change and the need for taking an ambitious approach towards combating its ill effects. It is a legally binding international treaty on climate change adopted by 196 signatory countries around the world, India being one of them. Achieving targets set under the Agreement may prevent a significant global GDP loss while crossing these limits may drag the global economy to a doom. The below table shows the significant impact of global temperatures on global GDP.

Where countries around the world have a rather limited approach to climate disclosure, UK[2] has gone one step further, proposing mandatory reporting by companies on climate changes and becoming the first country to do so. It won’t be long before market regulators across the globe, including India, take steps to adopt the same in their homeland. In this background, let us understand the scope of reporting proposed by the UK, compared to the scope of climatic disclosures covered by India’s BRSR and the global reporting framework.

The Consultation Paper with respect to climatic disclosures are based on the recommendations of the Global Task Force on Climate-related Financial Disclosure (TCFD), which recommended economy-wide mandatory climate-related financial disclosure. These recommendations are based on four basic pillars, which have also been proposed under the UK Consultation Paper as well.  The financial impact of climatic changes may not be apparent but their implications on financial performance are far and wide. It is important that companies ensure to include the potential impact of climate change in its major decisions. It is essential that climate-induced behaviours are embedded into the company’s culture so that climate change is considered at all levels of an organisation, which these disclosures intend to capture.

The financial impact of climatic changes may not be apparent but their implications on financial performance are far and wide. It is important that companies ensure to include the potential impact of climate change in its major decisions. It is essential that climate-induced behaviours are embedded into the company’s culture so that climate change is considered at all levels of an organisation, which these disclosures intend to capture.

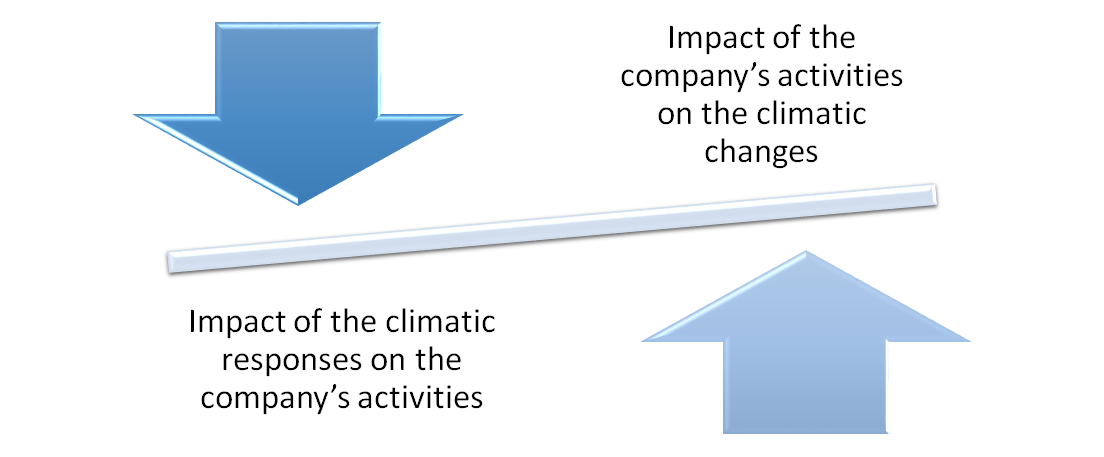

The most peculiar feature of the UK Consultation Paper is that apart from the obvious impact company operations have on the environment, it recognizes that climate change would also bring about various risks (and opportunities) on company operations too. For doing so, the Consultation Paper seeks impact of climatic responses on the company as well, thereby giving rise to dual disclosure format.

The UK Government released a roadmap aiming to mandate climate-related disclosures throughout the UK economy by 2025 in a gradual manner. The consultation paper was developed to bring the TCFD’s recommendations based climatic disclosures within the purview of the regulatory obligations by the end of 2021 to come into effect from the year 2022 onwards for large companies and LLPs such as –

Note – Large private companies and LLPs mean one having more than 500 employees and turnover being more than 500 million dollars. However, entities in the UK, like the Bank of England, have already started implementing such disclosures as per their Annual Report for 2021, thereby setting a benchmark for reporting by other companies. Large corporates have been targeted as it is likely that the larger the company or LLP, the greater their impact on the environment and subsequent climate risk. Further, larger corporates are also interconnected with various other companies and stakeholders. It becomes all the more important that climate risk is well understood and disclosed by them to avoid systemic risks due to climate changes.

The need for climatic disclosures has been motivated by the aim of transitioning to a net-zero emissions economy. Net-zero emissions refers to an overall balance between the green-house gases (GHG) emitted and absorbed so that the net effect of such emissions is ultimately zero or nil. This can be achieved by either reducing the GHG emissions or taking steps that help in absorption of such GHG emissions. Owing to the above, the UK Government intends to ensure that companies with a material economic or environmental impact or exposure assess, disclose and ultimately take actions against climate-related risks and opportunities. This will not only induce companies to take action but also provide investors with the needed information to adequately understand and manage climate-related financial risks. The disclosures aim to achieve the following –

The idea behind the mandatory disclosures was also put forth by the Chancellor[3], ‘this new chapter means putting the full weight of private sector innovation, expertise and capital behind the critical global effort to tackle climate change and protect the environment. We’re announcing the UK’s intention to mandate climate disclosures by large companies and financial institutions across our economy, by 2025. Going further than recommended by the Taskforce on Climate-related Financial Disclosures. And the first G20 country to do so.

The Bank of England has become the first entity in the world to publish climate disclosures in its Annual Report in June, 2020, continuing the legacy in this year as well. These disclosures may act as a guidance to other entities in the UK as well in other countries to report on TCFD’s recommendations.

The development of climate-related financial disclosures and contribution of the UK in same can be presented by the following timelines –

In India, SEBI has recently released the Business Responsibility and Sustainability Reporting (BRSR) framework, applicable on the selected listed companies[4] of the country, which includes of various environment related disclosures covering aspects such as resource usage (energy and water), air pollutant emissions, green-house (GHG) emissions, transitioning to circular economy, waste generated and waste management practices, bio-diversity etc. In India, the BRSR is currently the only sustainability report in force by means of regulatory provisions. The BRSR is required to be disclosed in the Annual Report of listed companies. A detailed analysis of the same can be referred to in our article.

The BRSR requires the companies to give the following disclosures with regards to climate-

The above disclosures are mainly quantitative providing merely metrics and only cover the impact of companies on climate changes.

| Pillars of disclosure | Under the UK Consultation Paper (TCFD recommendations) | Under BRSR |

| Governance | a. Broad oversight of climate related risks and opportunities b. management’s role in assessing and managing climate-related risks and opportunities. | a. Details of the highest authority responsible for implementation and oversight of the Business Responsibility policy. b. Statement by director responsible for the business responsibility report, highlighting ESG related challenges, targets and achievements c. Details of specified board committee,, if any responsible for decision making on sustainability related issues. |

| Strategy | a. climate-related risks and opportunities that the organization has identified over the short, medium, and long term. b. impact of climate related risks and opportunities on the organization’s businesses, strategy, and financial planning. c. resilience of the organization’s strategy, taking into consideration different climate-related scenarios, including a 2°C or lower scenario. | BRSR does not require any specific disclosure with respect to the strategy followed by the companies towards its environmental commitments. |

| Risk Management | a. processes for identifying and assessing climate-related risks b. processes for managing climate-related risks. c. Integration of the same into the overall risk management strategy of the organisation. | Overview of the entity’s material responsible business conduct issues. It requires the business to indicate material responsible business conduct and sustainability issues pertaining to environmental and social matters that present a risk or an opportunity to your business, rationale for identifying the same, approach to adapt or mitigate the risk along-with its financial implications. |

| Metrics and targets | a. Disclose the metrics used by the organization to assess climate related risks and opportunities in line with its strategy and risk management process b. Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks c. the targets used by the organization to manage climate-related risks and opportunities and performance against targets. | a. Details of GHG emissions – i. current year v/s past year classified into Scope 1 and Scope 2 ii. Emission intensity per rupee of turnover iii. Total emission intensity b. Details of independent assessment/valuation etc if any by an external agency c. Details of projects, if any, relating to reduction of GHG emissions |

It has to be noted here that while BRSR requires some mandatory disclosures in relation to GHG emissions, these are only quantitative metrics. The other pillars, being governance, risk management and strategy towards climate change have not been specifically catered to under climate change. Rather these fall under the general purview where a company may conveniently skip to address some environmental issues, such as climatic change.

Though India is one of the signatories to the Paris Agreement, proposing, amongst other things, net-zero emissions as a goal, India has not shown a supportive view towards achieving net zero emissions in the country. As per a press release, India is not ruling out the possibility of achieving the net zero emissions mission, however, it does not want to extend an international commitment at the present time. Unlike the UK, India is a developing country and GHG emissions, mainly carbon prints, are indispensable considering the continuing need for development. Moreover, the cost of countering its CHG emissions are also very high. In the given scenario, therefore, India is not in a position to commit to the cause of net-zero emissions. However, the same does not imply that India is not taking any action for reduction of emissions. The metrics required under the BRSR report serve as evidence to the same.

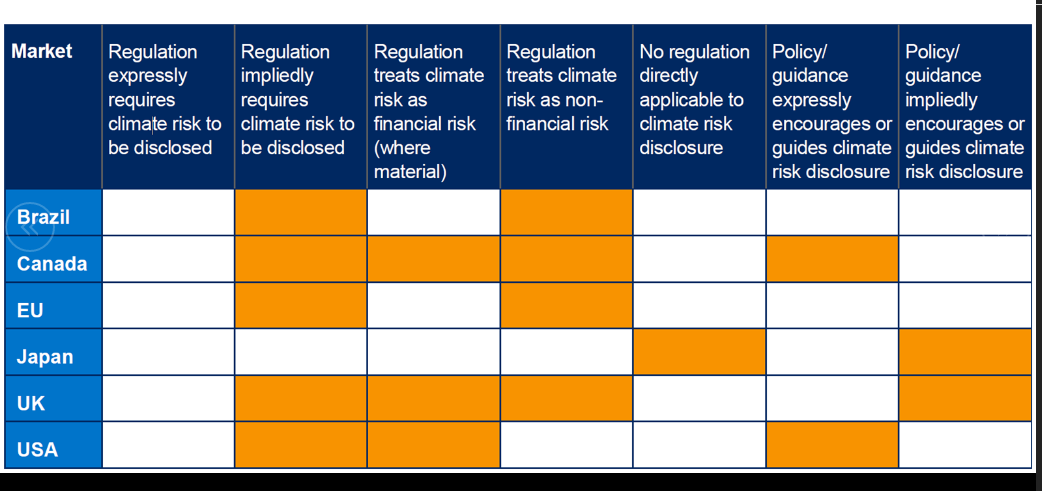

An overview[5] of the climatic change responses of various countries as on 2017 are presented below –  The above presentation clearly demonstrates that no major country in the world has made disclosures pertaining to climate risk mandatory and the situation is still the same. Most countries have, however, urged companies to disclose such information voluntarily. Below, we have discussed the current position of climatic change reporting in some countries.

The above presentation clearly demonstrates that no major country in the world has made disclosures pertaining to climate risk mandatory and the situation is still the same. Most countries have, however, urged companies to disclose such information voluntarily. Below, we have discussed the current position of climatic change reporting in some countries.

One of the signatories to the Paris Agreement, Brazil has at present no governmental emission trading schemes[6]. The Brazilian Stock Exchange (“B3”) maintains an index of shares of 100 companies (50 till 2020), called Carbon Efficient Index[7] (“ICO2”), that agree to adopt transparency practices regarding greenhouse gas (GHG) emissions. B3 follows a “report or explain” approach towards GHG emissions reporting[8] and compensates for its GHG emissions to make the effect neutral.

In Canada, the TSX (stock exchange) requires issuers to disclose certain environment information as per National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102), National Instrument 58-101 Disclosure of Corporate Governance Practices (NI 58-101) and National Instrument 52-110 Audit Committees (NI 52-110). A guidance note with respect to same was released in 2010[9] followed by another in furtherance to the same in 2019[10], which refers to the TCFD’s recommendations but does not mandate the same.

The Climate Disclosure Standards Board (CDSB) of European Union did a research[11] on the climatic change related reporting by the companies of the country and found that whilst 68% of company disclosures had made some reference to TCFD, the vast majority have still only partially adopted the recommended disclosures. Much lagging was found in adoption of practices such as scenario analysis and risk time horizons. The CDSB even made recommendations to the regulator to imbibe the climate related disclosures in line with the TCFD recommendations into the Directives[12] to ensure reporting in line with the same. The Directives mainly deal with GHG emissions and decarbonisation, although specific reference to TCFD has not been made part of such Directives till date.

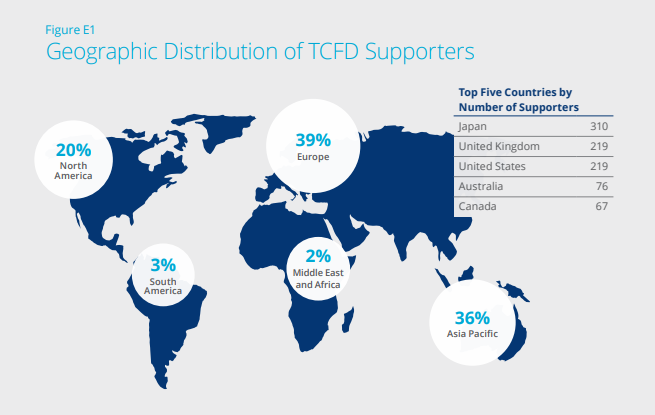

Recently, in October, 2020, the President of Japan committed[13] to the target of reaching net-zero emissions by 2020. The TCFD Status Report, 2020 also presents a picture of how Japan is devoted to the cause of climatic change and is supporting the TCFD Recommendations.  As of 2020, TCFD has the highest number of supporters from Japan. It has to be noted that while the Japanese Government has decided to put the commitment of net-zero emissions into law, till date there is no mandatory reporting requirement on the same. However, the companies take voluntary stands against climate change and give voluntary disclosures on the same.

As of 2020, TCFD has the highest number of supporters from Japan. It has to be noted that while the Japanese Government has decided to put the commitment of net-zero emissions into law, till date there is no mandatory reporting requirement on the same. However, the companies take voluntary stands against climate change and give voluntary disclosures on the same.

USA, once a signatory to the Paris Agreement, had pulled out of the same under the leadership of former President Mr. Donald Trump. However, with effect from 19th February, 2021, USA has re-entered into the Paris Agreement under Joe Biden, the current President of the United States. On May 20, 2021, he signed an executive order directing federal financial regulators to take a broad range of actions to assess and respond to climate-related financial risks, including enhancing the disclosure of climate-related financial risks. Consequently, a bill has been placed to pass the Climate Risk Disclosure Act, however the same has not been passed as on date.

A study of major countries in the world shows one considerable trend, gradually moving towards mandating climatic disclosures. While some companies have already taken a voluntary move towards such reporting, the reporting is mostly restricted to the present metrics and future targets, the qualitative parts remain untouched. With the regulators mandating such disclosures as part of a legal framework, the companies will be left with no alternative other than reporting. This will help in identifying the gaps, risks and opportunities, and stimulate working in a strategic way to reduce impact of climatic changes. While disclosure by companies is essential to ensure climate risk is appropriately measured, it is also important that companies move towards recognizing climate change as an important risk and opportunity to their organization.

Our resource center on Business Responsibility and Sustainable Reporting can be accessed here –

[1]https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/972422/Consultation_on_BEIS_mandatory_climate-related_disclosure_requirements.pdf [2] Consultation Paper – https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/972422/Consultation_on_BEIS_mandatory_climate-related_disclosure_requirements.pdf [3] https://www.gov.uk/government/speeches/chancellor-statement-to-the-house-financial-services [4] Reporting as per BRSR is currently made applicable to the top 1000 listed entities based on market capitalization [5] Source: https://www.unpri.org/climate-change/tcfd-recommendations-country-reviews/278.article [6] https://iclg.com/practice-areas/environment-and-climate-change-laws-and-regulations/brazil [7]http://www.b3.com.br/en_us/market-data-and-indices/indices/sustainability-indices/carbon-efficient-index-ico2.htm [8] http://www.b3.com.br/en_us/b3/sustainability/at-b3/transparency/ [9] https://www.osc.ca/sites/default/files/pdfs/irps/csa_20101027_51-333_environmental-reporting.pdf [10]https://www.osc.ca/sites/default/files/pdfs/irps/csa_20190801_51-358_reporting-of-climate-change-related-risks.pdf [11] https://www.cdsb.net/sites/default/files/nfrd2020_briefing_tcfd_climate.pdf [12] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32020R1818 [13] https://japan.kantei.go.jp/99_suga/statement/202010/_00006.html Read our other articles on related topics –

Loading…

Loading…

Abhirup Ghosh | abhirup@vinodkothari.com

It is not uncommon to have Indianised version of global dishes when introduced in India, and we are very good in creating fusion food. We have a paneer pizza, and we have a Chinese bhel. As covered bonds, the European financial instrument with over 250 years of history were introduced in India, its look and taste may be quite different from how it is in European market, but that is how we introduce things in India.

It is also interesting to note that regulatory attempts to introduce covered bonds in India did not quite succeed – the National Housing Bank constituted Working Group on Securitisation and Covered Bonds in the Indian Housing Finance Sector, suggested some structures that could work in the Indian market[1] and thereafter, the SEBI COBOSAC also had a separate agenda item on covered bonds. Several multilateral bodies have also put their reports on covered bonds[2].

However, the market did not wait for regulators’ intervention, and in the peak of the liquidity crisis of the NBFCs, covered bonds got uncovered – first slowly, and now, there seems to be a blizzard of covered bond issuances. Of course, there is no legislative bankruptcy remoteness for these covered bonds.

There are two types of covered bonds, first, the legislative covered bonds, and second, the contractual covered bonds. While the former enjoys a legislative support that makes the instrument bankruptcy remote, the latter achieves bankruptcy remoteness through contractual features.

To give a brief understanding of the instrument, a standard covered bond issuance would reflect the following:

Therefore, covered bond is a half-way house, and lies mid-way between a secured corporate bond and the securitized paper. The table below gives comparison of the three instruments:

| Covered bonds | Securitization | Corporate Bonds | |

| Purpose | Essentially, to raise liquidity | Liquidity, off balance sheet, risk management,

Monetization of excess profits, etc. |

To raise liquidity |

| Risk transfer | The borrower continues to absorb default risk as well as prepayment risk of the pool | The originator does not absorb default risk above the credit support agreed; prepayment risk is usually transferred entirely to investors. | The borrower continues to absorb default risk as well as prepayment risk of the pool |

| Legal structure | A direct and unconditional obligation of the issuer, backed by creation of security interest. Assets may or may not be parked with a distinct entity; bankruptcy remoteness is achieved either due to specific law or by common law principles | True sale of assets to a distinct entity; bankruptcy remoteness is achieved by isolation of assets | A direct and unconditional obligation of the issuer, backed by creation of security interest. No bankruptcy remoteness is achieved. |

| Type of pool of assets | Mostly dynamic. Borrower is allowed to manage the pool as long as the required “covers” are ensured. From a common pool of cover assets, there may be multiple issuances. | Mostly static. Except in case of master trusts, the investors make investment in an identifiable pool of assets. Generally, from a single pool of assets, there is only issuance. | Dynamic. |

| Maturity matching | From out of a dynamic pool, securities may be issued over a period of time | Typically, securities are matched with the cashflows from the pool. When the static pool is paid off, the securities are redeemed. | From out of a dynamic pool, securities may be issued over a period of time. |

| Payment of interest and principal to investors | Interest and principal are paid from the general cashflows of the issuer | Interest and principal are paid from the asset pool | Interest and principal are paid from the general cashflows of the issuer. |

| Prepayment risk | In view of the managed nature of the pool, prepayment of loans does not affect investors | Prepayment of underlying loans is passed on to investors; hence investors take prepayment risk | Prepayment risk of the pool does not affect the investors, as the same is absorbed by the issuer. |

| Nature of credit enhancement | The cover, that is, excess of the cover assets over the outstanding funding. | Different forms of credit enhancement are used, such as excess spread, subordination, over-collateralization, etc. | No credit enhancement. Usually, the cover is 100% of the pool principal and interest payable. |

| Classes of securities | Usually, a single class of bonds are issued | Most transactions come up with different classes of securities, with different risk and returns | Single class of bonds are issued. |

| Independence of the ratings from the rating of the issuer | Theoretically, the securities are those of the issuer, but in view of bankruptcy-proofing and the value of “cover assets”, usually AAA ratings are given | AAA ratings are given usually to senior-most classes, based on adequacy of credit enhancement from the lower classes. | There is no question of independent rating. |

| Off balance sheet treatment | Not off the balance sheet | Usually off the balance sheet | Not applicable. |

| Capital relief | Under standardized approaches, will be treated as on-balance sheet retail portfolio, appropriately risk weighted. Calls for regulatory capital | Calls for regulatory capital only upto the retained risks of the seller | Not applicable |

This article would briefly talk about the issuance of Covered bonds world-wide and in India, and what are the distinctive features of the issuances in India.

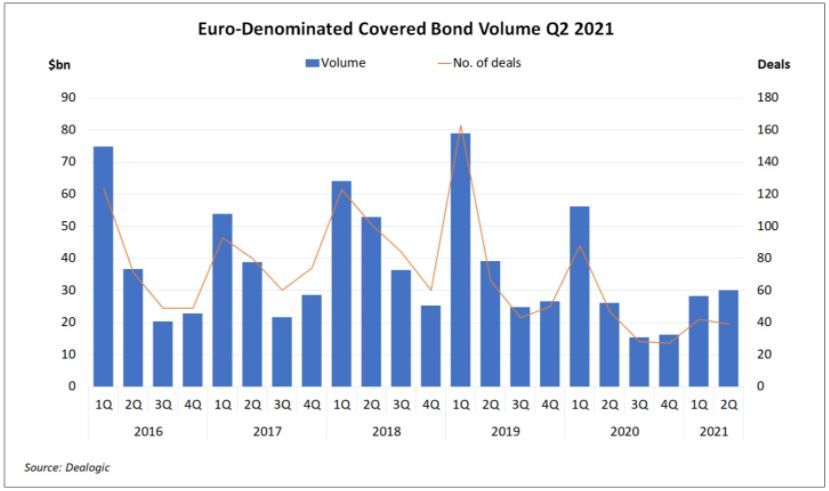

Since most volumes for covered bonds came from Europe, there has been a decline due to supply side issues. This is evident from the latest data on Euro-Denominated Covered bonds Volume. The performance in FY 2020 and FY 2021 has been subdued mainly due to COVID-19. Though, the volumes suffered significantly in the Q3 and Q4 of FY 20, but returned to moderate levels by the beginning of FY 2021.

The figure below shows Euro-Denominated Covered bond Issuances until Q2 2021.

Source: Dealogic[3]

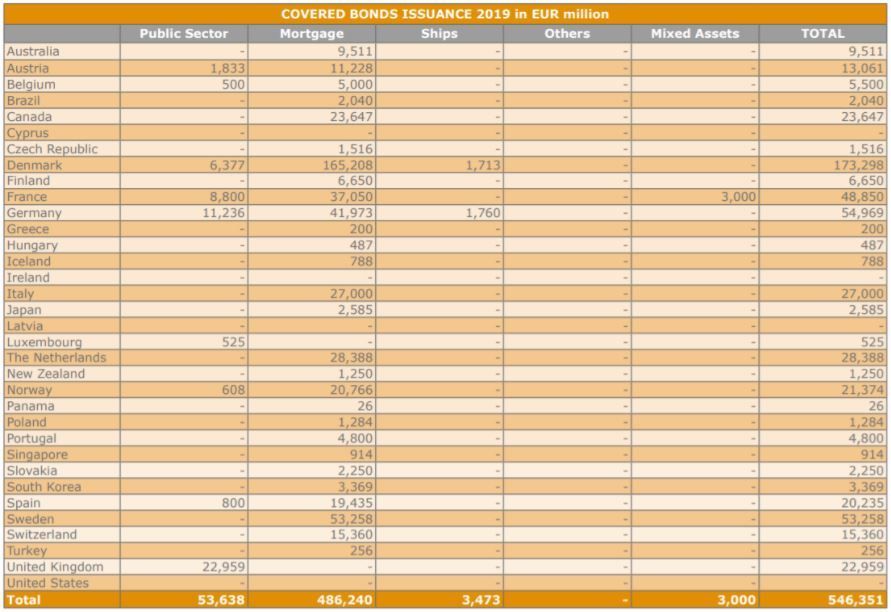

Countries like Denmark, Germany, Sweden continues to be dominant markets for covered bond issuances. The countries in the Asia-Pacific region like Japan, Singapore, and Australia continues to report moderate level of activities. In North America, Canada represents all the whole of the issuance, with no issuances in the USA.

The tables below would show the trend of issuances in different jurisdictions in 2019 (latest available data):

Source: ECBC Factbook 2020[4]

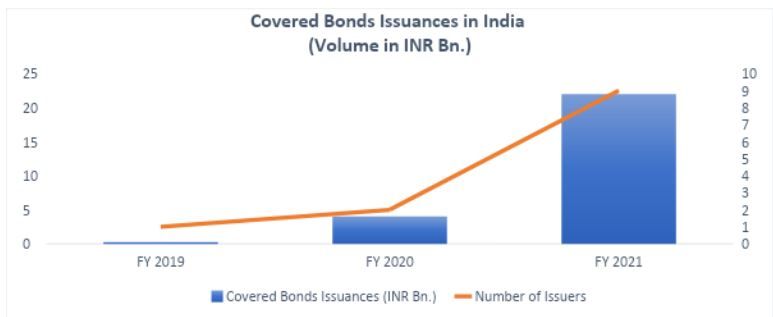

In India, the struggle to introduce covered bonds started way back in 2012, when the National Housing Bank formed a working group[5] to promote RMBS and covered bonds in the Indian housing finance market. Though the outcome of the working group resulted in some securitisation activity, however, nothing was seen on covered bonds.[6]

Some leading financial institutions attempted to issue covered bonds in the Indian market, but they failed. Lastly, FY 2019 witnessed the first instance of covered bonds, which was backed by vehicle loans.

In India, issuance of covered bonds witnessed a sharp growth in FY 2021, as the numbers increased to INR 22 Bn, as against INR 4 Bn in FY 2020. Even though the volume of issuances grew, the number of issuers failed to touch the two-digit mark. The issuances in FY 2021 came from 9 issuers, whereas, the issuances in FY 2020 were from only 2 issuers. Interestingly, all were non-banking financial companies, which is a stark contrast to the situation outside India.

The figure below shows the growth trajectory of covered bonds in India:

Source: ICRA, VKC Analysis

The growth in the FY 2021 was catapulted by the improved acceptance in Indian market in the second half of the year, given the uncertainty on the collections due to the pandemic, and the additional recourse on the issuer that the instrument offers, when compared to a traditional securitisation transaction.

Almost 75% of the issuances were done by issuers have ‘A’ rating, the following could be the reasons for such:

The Indian covered bonds market is however, significantly different from other jurisdictions. Traditionally, covered bonds are meant to be long term papers, however, in India, these are short to medium term papers. Traditionally covered bonds are backed by residential mortgage loans, however, in India the receivables mostly non-mortgages, gold loans and vehicle loans being the most popular asset classes.

In terms of investors too, the Indian market has shown differences. Globally, long term investors like pension funds and insurance companies are the most popular investor classes, however, in India, so far only Family Wealth Offices and High Net-worth Individuals have invested in covered bonds so far.

Another distinct feature of the Indian market is that a significant share of issuances carry market linked features, that is, the coupon rate varies with the market conditions and the issuers’ ability to meet the security cover requirements.

But the most important to note here is that unlike any other jurisdiction, covered bonds don’t have a legislative support in India. In Europe, the hotspot for covered bonds, most of the countries have legislations declaring covered bonds as a bankruptcy-remote instruments. In India, however, the bankruptcy-remoteness is achieved through product engineering by doing a legal sale of the cover pool to a separate trust, yet retaining the economic control in the hands of the issuer until happening of some pre-decided trigger events, and not with the help of any legislative support. In some cases, the legal sale is done upfront too.

Considering the importance and market acceptability of the instrument, rating agencies in India have laid down detailed rating methodologies for covered bonds[7].

Covered Bonds issued in India will not match most of the features of a traditional covered bond issued in Europe, however, the fact that finally the investors community in India has started recognizing it as an investment opportunity is very encouraging.

The real economics of covered bonds will come to the fore only when the market grows with different classes of investors, like the mutual funds, pension funds, insurance companies etc. in the demand side, which seems a bit far-fetched for now.

[1] A working group was constituted by the National Housing Bank to promote RMBS and Covered Bonds, the report of the working group can be viewed here: https://www.nhb.org.in/Whats_new/NHB%20Covered%20Bond%20Report.pdf

[2] In 2014-15, the Asian Development Bank appointed Vinod Kothari Consultants to conduct a Study on Covered Bonds and Alternate Financing Instruments for the Indian Housing Finance Segment

[3] https://www.icmagroup.org/resources/market-data/Market-Data-Dealogic/#14

[4] https://hypo.org/app/uploads/sites/3/2020/10/ECBC-Fact-Book-2020.pdf

[5] A working group was constituted by the National Housing Bank to promote RMBS and Covered Bonds, the report of the working group can be viewed here: https://www.nhb.org.in/Whats_new/NHB%20Covered%20Bond%20Report.pdf

[6] Vinod Kothari Consultants has been a strong advocate for a legal recognition of Covered Bonds in India. They were involved in the initiatives taken by the NHB to recognize Covered Bonds as a bankruptcy remote instrument in India.

[7] The rating methodology adopted by ICRA Ratings can be viewed here: https://www.icra.in/Rating/ShowMethodologyReport/?id=709

The rating methodology adopted by CRISIL can be viewed here: https://www.crisil.com/mnt/winshare/Ratings/SectorMethodology/MethodologyDocs/criteria/crisils%20criteria%20for%20rating%20covered%20bonds.pdf

—

Our Video on Covered Bonds can be viewed here <https://www.youtube.com/watch?v=XyoPcuzbys4>

Some resources on Covered Bonds can be accessed here –

Introduction to Covered Bonds by Vinod Kothari: https://vinodkothari.com/2015/01/introduction-to-covered-bonds-by-vinod-kothari/

The Name is Bond. Covered Bond. By Vinod Kothari: http://www.vinodkothari.com/wp-content/uploads/covered-bonds-article-by-vinod-kothari.pdf

NHB’s Working Paper on Covered Bonds: https://www.nhb.org.in/Whats_new/NHB%20Covered%20Bond%20Report.pdf

Do’s and don’ts to be ensured by listed companies

Updated as on September 28, 2023 , pursuant to the SEBI LODR (Second Amendment) Regulations, 2023

In order to disseminate information regarding performance of the company, its future prospects etc. listed companies usually conduct gatherings of analysts/investors after dissemination of quarterly results or atleast once in a year. Such meets generally include conference calls or meeting with group of investors or one-to-one meet or calls with investors or analysts, including those in the nature of walk-in. The idea behind conducting such meets is to provide transparency for the company’s performance figures, to address the queries of the analysts/investors and to ensure that the company’s information is available to the stakeholders. However, the risk of information asymmetry in such meets or gatherings is very inherent.

While the regulatory framework of SEBI i.e. SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘Listing Regulations’) provided for disclosure of adequate and timely information to enable investors to track the performance of a company including the information pertaining to occurrence of investors meet/conference call with analysts, however, several inconsistencies were observed in the disclosures made by the companies. For instance, some entities were not divulging the details of what transpired in such investors’ meetings and were merely disclosing the limited presentations w.r.t. the meetings. As such, minority shareholders, who did not attend these meetings, were not privy to the information shared with a select group of investors, thereby creating information asymmetry among different classes of shareholders.

Realizing this, SEBI, on November 20, 2020, came up with the Consultation Paper and recommended enhanced disclosure requirements w.r.t. post earning calls and one-to-one meets. Our write-up analyzing the said consultation paper can be viewed here.

Later, vide notification dated May 05, 2021, SEBI enhanced the disclosure requirements w.r.t. Investors’/ Analysts’ meet. In this article, the author has made an attempt to discuss the changes made in the disclosure requirements w.r.t. analyst meet step by step.

On May 05, 2021, SEBI amended the Listing Regulations which inter alia, covered analyst meet. Pursuant to the said amendment, the companies are required to include enhanced disclosure requirements with respect to analyst/ investors meets so as to avoid selective disclosure and information asymmetry and to ensure market integrity and to safeguard the interest of investors. The said amendments were voluntary for FY 2021-22, and became mandatory from FY 2022-23. The synopsis of the amendment is provided below:

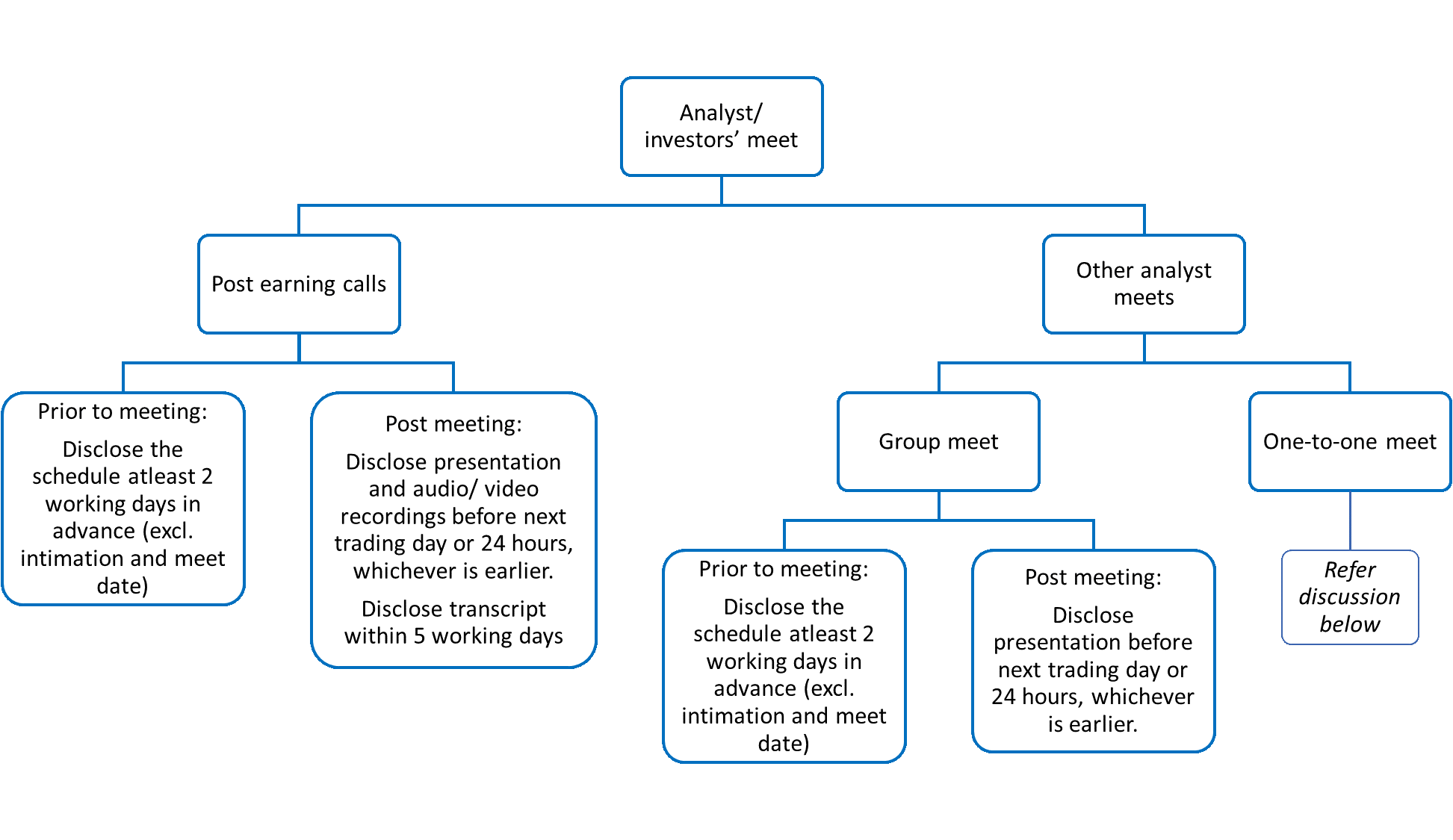

Figure 1: Disclosure requirement for analyst meet

In respect of one-to-one meet, there are no explicit disclosure requirements as such. However, considering the intent of the Listing Regulations and SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’), the following things are explicitly clear:

Regulation 8 of PIT Regulations mandates every listed company to frame a code of practices and procedures for fair disclosure of UPSI in line with the principles set out in Schedule A to PIT Regulations. Para 6 of Schedule A requires the company to ensure that information shared with analysts and research personnel is not UPSI. Para 7 provides for developing best practices to make transcripts or records of proceedings of meetings with analysts and other investor relations conferences on the official website to ensure official confirmation and documentation of disclosures made.

The PIT Regulations do not distinguish between group meets and one-to-one meets. It requires the company to record such meets and develop best practices to disclose the same on its website. The practice of recording the meet also safeguards the company officials participating in the meeting from any possible allegation of having divulged UPSI.

The PIT Regulations prohibit sharing of UPSI in any manner to any person including analysts/ investors and require the companies to take all required steps to ensure the same. Considering the same, the fact whether it is a group meet/ call or otherwise or whether such meet/ call was organized by the company itself or not, becomes irrelevant and the prohibition shall apply in all cases.

Therefore, there is a remote chance of sharing such UPSI until and unless the same is as per the provisions of code of fair disclosure framed by the company. Accordingly, if any UPSI is shared, legitimately in terms of the said code or otherwise, the entity will have to disclose the audio/ video recordings or the transcripts of such meeting to the stock exchange promptly.

The amendment in the Listing Regulations came up with various interpretations and ambiguities w.r.t. disclosure requirements. We have discussed such anomalies in our previous article which can be viewed here.

In order to clear the ambiguities w.r.t the disclosure requirements, BSE, vide circular dated 29th June, 2021 and July 29, 2022, provided further clarifications and recommendations. In this article, we have tried to provide step-by-step guide for disclosure on analyst meets and post earning calls. Further, we have also provided the do’s and don’ts to be ensured by the companies.

In order to comply with the provisions of Listing Regulations in letter and spirit, the companies are required to ensure that it makes timely disclosure to stock exchanges and on their own website. The compliance requirement as per the amended provisions w.r.t. analysts/ investors meet are jotted down below:

| Sr. No. | Cases | Disclose what? | By When? | Other Points to be ensured |

| 1. | Post earning calls/ Quarterly calls, by whatever name called (after disclosure of quarterly financial results) | Schedule of such meeting | Atleast 2 working days in advance (excluding the date of intimation and date of the meet). | Mandatory only for group meets. |

| Presentation and the audio/ video recordings of such meeting | Before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier. | Mandatory for both group meets and one to one meets.To be disclosed whether conducted by a company or any other entity.To be hosted on the website of the company for minimum 5 years and thereafter as per the archival policy of the company. To be disclosed simultaneously to the stock exchange. | ||

| Transcripts of such meeting | Within 5 working days of conclusion of the meet. | Mandatory for both group meets and one-to-one meets.To be disclosed whether conducted by a company or any other entity.To be hosted on the website of the company and preserved permanently.To be disclosed simultaneously to the stock exchange. | ||

| 2. | Other Analysts/ Investors meets | Schedule of such meeting | Atleast 2 working days in advance (excluding the date of intimation and date of the meet) | Mandatory only for group meets. |

| Presentation made in such meeting | Before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier.. | Mandatory only for group meets.To be disclosed on the website of the company, whether conducted by company or any other entity.To be disclosed simultaneously to the stock exchange. | ||

| In case any UPSI is shared | Audio/video recordings or transcripts of such meeting | Promptly | Applicable to both group as well as one-to-one meets.To be disclosed on the website of the company, whether conducted by a company or any other entity.To be disclosed simultaneously to the stock exchange. |

While making disclosure of schedules, the company may also provide the details pertaining to the meet/ call, mode of attending, details pertaining to registrations, disclaimers/ note to complete/ ease registration/ attending the call, details regarding specific platform requirements, if any, inclusions/ exclusions of audience/ participants if any, etc.

Further, a disclaimer or a confirmation may be added in the intimation stating that ‘Company will be referring to publicly available documents for discussions’ or ‘No UPSI is proposed to be shared during the meeting / call’. This will create confidence amongst the investors and will maintain sanctity of the meet / call.

While disclosing the transcripts of the meet/ call, the companies may also consider providing the list of attendees and record the dialogues, Q&As and assents and dissents of the analysts/ investors. Further, a confirmation may be added in the disclosure that no unpublished price sensitive information was shared/ discussed in the meeting / call.

The companies will be required to observe some crucial points while scheduling or attending analysts’/ investors’ meet, conference calls, post earning calls etc. Briefly, the following are the do’s and don’ts:

| Sr. No. | Do’s | Don’ts |

| 1. | Always conduct scheduled meets. | Avoid unscheduled meets. |

| 2. | Always schedule group meets. | Avoid scheduling one-to-one meet. |

| 3. | Upload the schedule of group meets/ calls on the website atleast 2 working days in advance (excluding the date of intimation and date of the meet) and also simultaneously submit the same with the stock exchange. | Do not forget to upload and send the schedule on the website and to the stock exchanges, respectively beyond the prescribed time. |

| 4. | Upload the presentation made to analysts/ investors in the scheduled group meet on the website promptly before the next trading day or within 24 hours from the conclusion of the meet, whichever is earlier and also simultaneously submit the same with the stock exchange. | Do not forget to upload and send the schedule on the website and to SE, respectively beyond the prescribed time. |

| 5. | Ensure to make audio and video recording of the post earnings/ quarterly calls, whether conducted physically or through digital means, either conducted by company or any other entity including one- to-one meets. | Do not avoid making audio/video recording of such calls irrespective the same was conducted by the company itself or by any other entity. |

| 6. | Ensure transcripts of the post earnings/quarterly calls, whether conducted physically or through digital means, either conducted by company or any other entity including one-to-one meets. | Do not avoid making transcripts of the proceedings of such calls irrespective the same was conducted by the company itself or by any other entity. |

| 7. | Ensure that the information shared with the investors is already available in the public domain. | Do not share UPSI with the investors. |