Moving towards sustainable finance through sustainable bonds

SLBs awe-inspiring issuers and investors ! Payal Agarwal, Executive (payal@vinodkothari.com) ESG or Environmental, Social and Governance concerns are been on a high focus in recent times. The issues are not only been addressed by the environmentalists, but the corporate world is also becoming more and more attentive towards the ESG concerns and devising various ways and means to collate them with their operational activities. One of the various such treads in this regard is the issuance of ESG focussed bonds, which is gradually becoming a popular trend in the global economy, India being no exception. These bonds give a boost to sustainable finance, helping issuers raise finance and investors ensuring their investments fulfil their sustainability goals.

Legal framework in India

In India, the green bonds[1] are one of the most popular and legally recognised means of raising sustainable finance. SEBI, vide its circular dated May 30, 2017 has issued “Disclosure Requirements for Issuance and Listing of Green Debt Securities” which are in addition to the general requirements under the SEBI (Issue and Listing of Debt Securities) Regulations, 2008. Amidst the constant push towards business sustainability and responsibility conduct through reporting for listed entities[2], India also recognised the need for such ESG debt securities in the Consultation Paper released on draft International Financial Service Centres Authority (Issuance and Listing of Securities) Regulations. The said consultation paper provides for a framework for issuance and listing of securities, including ESG debt securities in the stock exchanges under the IFSC region in India. Now, the International Financial Service Centres Authority (Issuance and Listing of Securities) Regulations, 2021 (“IFSC Regulations”) provide a framework for listing of “ESG debt securities”. In this article, we will discuss the internationally recognised means of raising sustainable finance and the present and potential capacities of India in raising such sustainable finance by means of ESG debt securities.

Meaning and types

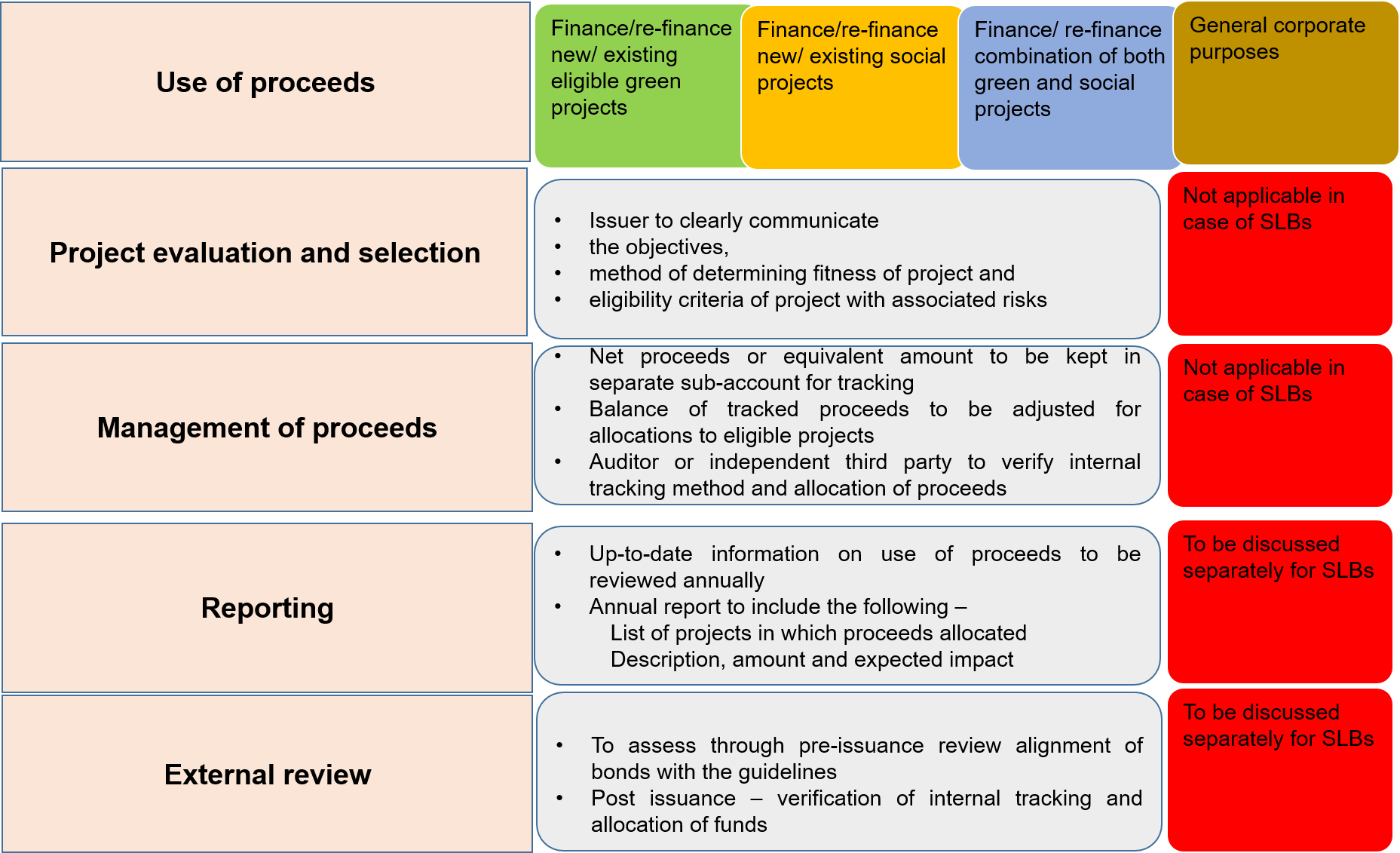

As the name suggests, ESG bonds or debt securities are debt instruments that are linked to or contribute to the development of ESG concepts in some way or the other. The International Capital Market Association (ICMA) recognises 4 types of bonds that are interested in sustainable financing –  Further separate guidelines[3] have been issued by ICMA in respect of each of these bonds. A snapshot showing comparative between these 4 types of bonds is as follows –

Further separate guidelines[3] have been issued by ICMA in respect of each of these bonds. A snapshot showing comparative between these 4 types of bonds is as follows –  A study of these guidelines show that the SLBs are quite different from other sources of sustainable finance, being “general corporate funds” instead of “use of proceeds” funds. Therefore, the same has been discussed separately in later parts of this article. Further, the categories of projects in which proceeds of green bonds, social bonds, and sustainable bonds can be used have been listed below (the list is illustrative) –

A study of these guidelines show that the SLBs are quite different from other sources of sustainable finance, being “general corporate funds” instead of “use of proceeds” funds. Therefore, the same has been discussed separately in later parts of this article. Further, the categories of projects in which proceeds of green bonds, social bonds, and sustainable bonds can be used have been listed below (the list is illustrative) –

Similar standards have been issued by the Climate Bonds Standard Board that recognises only green bonds, Association of South East Asian Nations (ASEAN) having set different standards for green bonds, social bonds and sustainable bonds. Similar standards have also been issued by the European Union for green bonds and social bonds. It is noteworthy that all these standards are voluntary in nature and aligned with the ICMA Guidelines with some modifications of their own. The IFSC Regulations also recognise all the 4 types of bonds as ESG debt securities, issued as under any of the aforesaid guidelines.

Similar standards have been issued by the Climate Bonds Standard Board that recognises only green bonds, Association of South East Asian Nations (ASEAN) having set different standards for green bonds, social bonds and sustainable bonds. Similar standards have also been issued by the European Union for green bonds and social bonds. It is noteworthy that all these standards are voluntary in nature and aligned with the ICMA Guidelines with some modifications of their own. The IFSC Regulations also recognise all the 4 types of bonds as ESG debt securities, issued as under any of the aforesaid guidelines.

Sustainability-linked bonds (SLBs) – where lies the uniqueness?

As discussed above, internationally there are four types of recognised ESG bonds, which are also proposed to be imbibed in the legal framework in India. While the first three being in the nature of “use-of-proceeds” bonds, the Sustainability-linked bonds or SLBs have distinguishing features. The SLBs rests on five key pillars, as follows –  The SLBs require companies to frame key performance indicators and Sustainability Performance Targets. To give an example, a company may frame its sustainability performance target to reduce its greenhouse gas (GHG) emissions by 20% compared to that of the year 2018 as baseline. In this case, the key performance indicators can be reduction of CO2 emissions, reduction of carbon footprint etc.

The SLBs require companies to frame key performance indicators and Sustainability Performance Targets. To give an example, a company may frame its sustainability performance target to reduce its greenhouse gas (GHG) emissions by 20% compared to that of the year 2018 as baseline. In this case, the key performance indicators can be reduction of CO2 emissions, reduction of carbon footprint etc.

Growth of ESG bonds

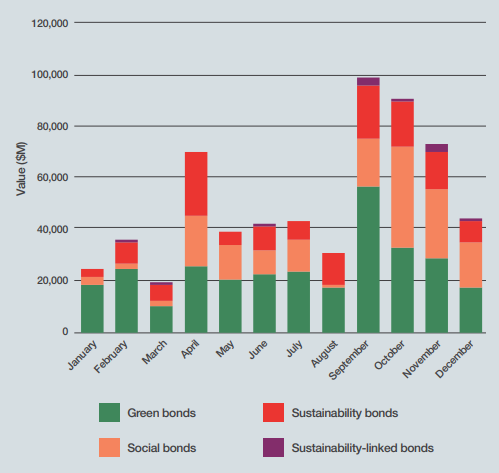

The Environmental Finance – Sustainable Bonds Insight, 2021 provides  data analytics in respect of the various types of sustainable bonds issued during the year 2020. The data shows high volume of green and social bonds issued during the year as compared to sustainable bonds and SLBs, which are relatively new and evolving concept. While the figures show a comparative between different types of ESG bonds issuance, it also provides an insight on the increasing volume of the ESG bonds being issued in the Covid era (an increase in the bonds issuance in the months of September, October and November).

data analytics in respect of the various types of sustainable bonds issued during the year 2020. The data shows high volume of green and social bonds issued during the year as compared to sustainable bonds and SLBs, which are relatively new and evolving concept. While the figures show a comparative between different types of ESG bonds issuance, it also provides an insight on the increasing volume of the ESG bonds being issued in the Covid era (an increase in the bonds issuance in the months of September, October and November).

Present position v/s potential growth

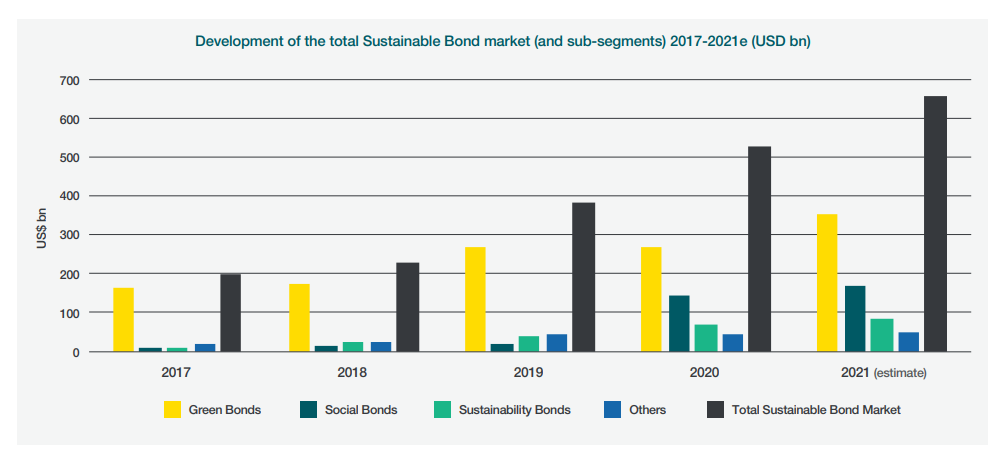

The Report shows a comparison of the development of sustainable bond market in the recent years and an estimate of what is expected in the current year 2021. It demonstrates clearly that the sustainable bond market is expected to rise further in the upcoming areas.

Growth of ESG bond market in India in recent times

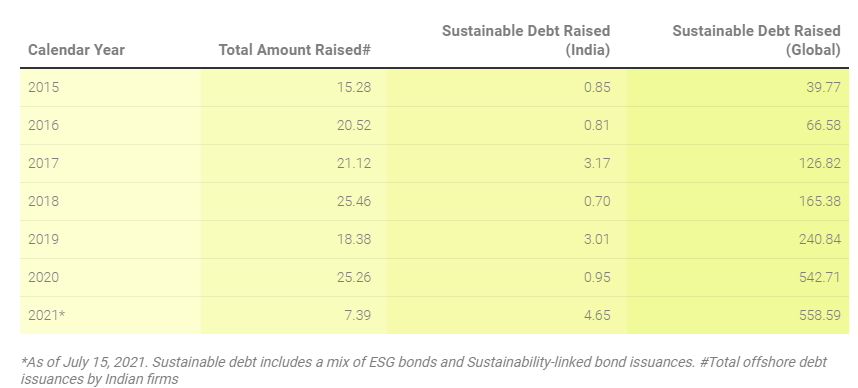

In India, the ESG bonds issuance is witnessing an evident upshot. However, the same has not found much investors’ interest in the country. Nevertheless, the Indian issuer companies have still been able to raise much funds from the issuance of ESG bonds from global investors. The below chart clearly demonstrates the increase in funds raised by way of issue of ESG bonds[4]. Some of the big Indian issuers of ESG focussed bonds include GreenCo, JSW Hydro Energy, Shriram Transport Finance Company, India Green Power Holdings, ReNew Power, Ultratech Cement Ltd etc. Sustainability linked bonds or SLBs, as discussed, is relatively new and innovative concept in the podium of ESG bonds in the world. India has made a remarkable entry in this field with Ultratech Cement Limited[5], issuing SLBs, thereby, being the first company in India and second in Asia to issue SLBs. The company has raised a total of 400 million USD equivalent to Rs. 2900 crores by way of issuance of such SLBs. The same has been listed in the Singapore Exchange Securities Trading Limited[6].

Some of the big Indian issuers of ESG focussed bonds include GreenCo, JSW Hydro Energy, Shriram Transport Finance Company, India Green Power Holdings, ReNew Power, Ultratech Cement Ltd etc. Sustainability linked bonds or SLBs, as discussed, is relatively new and innovative concept in the podium of ESG bonds in the world. India has made a remarkable entry in this field with Ultratech Cement Limited[5], issuing SLBs, thereby, being the first company in India and second in Asia to issue SLBs. The company has raised a total of 400 million USD equivalent to Rs. 2900 crores by way of issuance of such SLBs. The same has been listed in the Singapore Exchange Securities Trading Limited[6].

ESG Bonds – Motivations for the Issuer and Investor

Issuer’s perspective

- Cost advantage due to yield reduction – The yield payment in respect of ESG bonds are relatively lower than that of other conventional bonds[7]. A reason for such lower yields is increase in demand with limited supply of such bonds. An example may be the issuance of green bonds by Italian Government[8], which was oversubscribed by 10 times.

- Role as corporate citizens – The ESG bonds contribute to demonstrating the role of issuers as responsible corporate citizens, spending the proceeds generally on sourcing of renewable energy, pollution reduction, climate change initiatives.

- Attracts responsible investors – The ESG bonds align with social development goals (SDGs) and principles of responsible investing (PRI) thereby attracting socially responsible investors whose investment decisions are more of impact-oriented than yield-based.

- Seen as ethical companies – The companies issuing ESG bonds are looked upon as ethical companies by the stakeholders thereby helping in demonstrating a good corporate image.

Some additional advantages motivation lies for issuance of SLBs –

- Flexibility of designing structure – The main feature of SLB is that it gives a flexibility to the issuers to design their issued bonds in their own way.

- Flexibility with regard to use of proceeds – Another flexibility is with regard to the use of issue proceeds which need not necessarily be towards promoting green projects, social projects or the like. Therefore, the companies are free to use the proceeds for their operational activities without giving a second thought on whether the same qualifies as a green project or social project.

- Motivation for fulfilment of ESG targets – The SLBs put a “step-up” on the coupon rate of the bonds in case the issuer misses its ESG target. Therefore, it gives an additional economic interest for the issuers to fulfil their ESG targets.

Investor’s perspective

It is said that behind the investors’ growing interest in ESG bonds lies two reasons – (i) values-driven and (ii) value-driven. While the investors, as part of their responsibility towards the society and environment, consider ESG in their investment analysis, that is not the only reason investors are investing in ESG bonds. Another reason that drives the investors in supporting ESG concerns and investing in ESG bonds is the long term perspective and the expectation of deriving great value from their investment portfolio. The investors believe that a company that invests in the ESG concerns and addresses the ESG issues properly, are more likely to earn profits in the long term. Therefore, while the investors are demonstrating their values and responsible behaviour by choosing ESG focussed bonds, they are also booking adequate profits for themselves in the long run. Now, with the new SLBs coming into picture, the investors are likely to get more benefits out of their investment in the ESG bonds in the form of SLBs. The terms of SLBs are designed as such that the investors get a “step-up” or hike in the coupon rates as and when the issuer misses a pre-defined target (identified as SPTs).

Sustainability-linked bonds (SLBs) – investors always at the winning end

The concept of SLBs comes with a very interesting feature – where investor benefits on the issuer missing its ESG target. Since the investor is making profits on the cost of compromise in ESG responsibilities by issuer, therefore it is controversial that how can an investor show his ESG responsibility at a time when it is making profits on failure to reach ESG targets? However, that is not the case. Another viewpoint towards the case maybe that the investors are motivating their issuers in reaching their ESG targets, and where they fail to do, the investors cast a penalty on the issuer. Whatever the case may be, in both the scenarios, investors are the one who are at the winning side. A recent interesting case of issue of ESG bonds in the form of SLBs may be discussed here. A Japanese firm, Nomura Research Institute Ltd, has issued ESG bonds with the “variable bond characteristics” as below –

- Where the issuer reaches target – early redemption of debts

- Where the issuer misses target – extra yield to investors

In both the cases, the investors will be benefitted. In the first case, the investor will earn return on their investments early, so they will be in possession of their funds again at a shorter span of time. On the contrary, in the second case, though the funds of the investors will be locked for a longer time, the same will bring them higher yield. So, the investors, are very well in a win-win position in all probable cases.

Requirements for listing of ESG debt securities in India

The Ministry of Finance has notified the IFSCA (Issuance and Listing of Securities) Regulations, 2021 or the IFSC Regulations. It is a unified framework for various kinds of securities and is framed with the main intent of consolidating the regulatory requirements in order to access the global capital with more ease and less complexity. The concept of ESG bonds have been specifically recognized and captured under Chapter X of the said Regulations. However, it has to be noted that these IFSC regulations are applicable only for the IFSC-listed companies. No specific framework is provided for ESG bonds for other domestic companies in India outside the scope of IFSC Regulations. The same can still be taken as a guidance for other domestic issuances. While the requirements for issuance and listing of ESG bonds are given in Chapter X, the same is in addition to those under Chapter IX of the Regulations. Please note that, Chapter IX lays down the requirements for issuance and listing of debt securities. By “debt securities” is meant the non-convertible debt securities, as is clear from the definition of “debt securities” under Regulation 2(e) of the Regulations. The additional requirements for the ESG bonds are as follows –

- An independent external review is required to be obtained in order to satisfy that the issue of ESG bonds are in line with internationally recognised standards set for ESG bonds, the principles of ICMA being one of them.

- Review may be in the form of verification, certification, second party opinion, or scoring/rating.

- The most important requirement under ESG investing is disclosure and reporting The same is being discussed here under a separate head.

- Impact report is important in order to measure the actual impact of the projects in which the ESG funds have been spent.

Disclosure and reporting

As also envisaged by the Sustainability-linked bond principles of ICMA, disclosure is a main pillar of ESG investing. The IFSCA Regulations also focusses on the disclosure requirements. Under the IFSCA Regulations, the following disclosures are required to be made –

- The objectives of the issue of debt securities

- The process followed for selection and evaluation of projects

- The system employed for tracking deployment of issue proceeds

- Intended vs actual utilisation of issue proceeds

- Specific projects to which the issue proceeds have been disbursed/ allocated.

Further, in case of SLBs, the reporting guidance as under the ICMA Guidelines shall apply.

Applicability to other listed entities not covered under IFSC Regulations

The IFSC Regulations are not applicable to companies other than those listed under the jurisdiction of IFSC Authority. However, the IFSC Regulations are in alignment with other internationally-recognised principles in this regard. We have taken examples of some Indian companies like JSW Steel, Ultratech Cement, Adani Energy, Shriram Transport Finance Co. Ltd, Ultratech Cement etc which provides disclosures and follow the requirements of external review in line with the ICMA Guidelines and IFSC Regulations, which re-iterate requirements of ICMA and other internationally recognised guidelines.

Conclusion

As the world has approached the twentieth century, a shift has become apparent towards more grounded aspects of life – rather than just profit earning. Earlier, it was believed that the corporate world has only one motive – the profit earning motive. However, the focus has now been modified to include various other aspects as well. With instruments like ESG bonds, the efforts are being made to include sustainability in the economy, so that both can progress side-by-side. As the statistics above suggest, India is nowhere lagging behind in the ESG investing. This may be seen as one of the probable cause that IFSCA has included ESG bonds as a specified security in its Listing Regulations. The IFSCA Regulations do not introduce the ESG bonds in India for the first time, rather it just seeks to regulate issuance of the same by means of express regulations in this regard.

Our resource center on Business Responsibility and Sustainable Reporting can be accessed here –

[1] Our article on the same can be read here [2] Read our articles on the same here [3] Green Bond Principles Social Bond Principles Sustainability Bond Guidelines Sustainability-linked Bond Principles [4] https://www.refinitiv.com/ [5] See Page 4 of the Annual Report here [6] Listing confirmation can be accessed here [7] Asian Development Outlook – 2021 [8] Read this here Our other related resources –

- https://vinodkothari.com/2014/03/prospects-green-bonds-rise/

- https://vinodkothari.com/2017/05/guidelines-for-issuance-of-green-bonds/

- https://vinodkothari.com/wp-content/uploads/2017/03/India_plans_to_tap_Green_Bonds-1.pdf

- https://vinodkothari.com/2020/08/cartload-of-details-in-brsr-a-challenge-ahead-for-elaborate-reporting/

- https://vinodkothari.com/2020/08/brr-in-process-to-become-a-fully-loaded-electronic-form/

- https://vinodkothari.com/2021/03/esg-concerns-on-corporate-governance-in-india/

- https://vinodkothari.com/2021/07/corporate-responsibility-towards-climate-change-uk-leads-regulatory-measures/

An Insolvency Resolution Process sans Claims – A Defunct Process?

- Devika Agrawal, Executive (resolution@vinodkothari.com )

Introduction

Under the provisions of Insolvency and Bankruptcy Code, 2016 (IBC), the determining criteria for insolvency is a definite default, rather than financial sickness or ‘inability to pay’ . While the latter is certainly suggestive of a larger state of insolvency, where the company may be unable to pay its outstanding debts, the former does not necessitate the same. Hence, the likelihood of an application for initiation of CIRP on the basis of an isolated event of default/ non-payment, sans a financial stress in the company, cannot be ruled out.

Owing to such uncertainty, it may so happen that an application, initiated on the basis of such an isolated event of default, is admitted before the adjudicating authority without any other cases of defaults by the company. Naturally, there would be no claims to file except that of the applicant. If it were to happen, it forces one to ponder as to how CIRP will proceed, and if at all there is something to resolve.

CIRP without claims?

As per the Code, CIRP commences after an application has been admitted by the AA. Once an application is admitted by the AA, an Interim Resolution Professional is appointed, who is responsible for invitation and collation of claims, and subsequent constitution of the committee of creditors (‘CoC’). All decisions with respect to the corporate debtor’s business are thereafter taken with the approval of CoC, including approval of Resolution Plan or passing of a resolution for liquidation of the Corporate Debtor. Hence, it can be said that the CoC, constituted on the basis of the claims, drives the CD through the process till revival/ liquidation, as the case may be.

However, in a rather odd situation, when no claims are received after the initiation of CIRP, how will the IRP constitute CoC? In essence, when no claims are received by the Interim Resolution Professional (‘IRP’) after the initiation of CIRP, the questions that would arise are (aside, the broader question as to whether there was at all a need for resolution, will remain) – how is the CIRP likely to proceed, how will IRP constitute CoC, and most importantly, what is it for which the IRP should invite resolution plans? Does non-receipt of any claims by the creditors prove that the Corporate Debtor is, in fact, not a defaulter?

Books of the corporate debtor/public announcement

At the first instance, the books of the corporate debtor will assist in determining whether at all the CD has liabilities (financial/operational, otherwise). It may be the case that the CD does not have any liability at all (besides that pertaining to the creditor who filed the application). In such a case, attempts can be made by the CD and the Creditor to arrive at an agreement among themselves, instead of proceeding with CIRP and having the CD jammed in a situation of Moratorium.

However, there may be cases where the books acknowledge liabilities but there are no claimants. This might pose practical difficulties for the IRP because if no claims are received, the constitution of CoC would become impossible which in turn would lead to the CIRP coming to a complete halt. Occurrence of such a situation might necessitate the following actions to be taken by the IRP-

- sending of individual mails, requesting claims, to the Financial creditors so that, at least, a CoC can be constituted.

- ensure that the public announcement, inviting claims of creditors, are made in accordance with the manner laid down in the CIRP Regulations and in newspapers with wide reach.

- if, in case, no claims are received despite of efforts being made by the IRP, a final attempt should be made by the IRP by way of re-issuance of public announcement

Say, even after these efforts, no one shows up. There is a stage set, but there are no creditors to run the show. In such cases, what can the IRP do? We can explore the following alternatives.

Section 12A of Insolvency and Bankruptcy Code, 2016

Prior to section 12A of the Code, the withdrawal of an admitted insolvency resolution process was not expressly provided for. However, in view of reasons like a post-admission settlement or restructuring, the need to allow such withdrawal was realised – Section 12A of the Code enables withdrawal of the applications filed under Section 7, 9 or 10 of IBC, post its admission, if the committee of creditors (CoC) approves of such withdrawal by a voting share of at least ninety percent.

The very fact that section 12A mandates the approval of CoC as a precondition for withdrawal, there is no occasion to apply the said provisions before the constitution of CoC. A deeper reading of section 12A further indicates that the application for withdrawal must be filed by the very applicant who initiated the process. The reason is simple, the cause initiated by one cannot be withdrawn merely by virtue of a majority of others. Thus, the fact that withdrawal can be done only at the behest of the original applicant and with the consent of at least 90% CoC members maintains the much required trade off.

However, in the given state of affairs, the devil lies in the fact that no claims have been received so as to constitute the CoC. Further, to assume that the applicant who, at the first place, initiated the application, and thereafter chose to remain missing in action would initiate the withdrawal process, seems rather bizarre.

Even if one were to assume the possibility of withdrawal application by such a creditor, would the very filing be construed as a mere pressure tactic for recovery of claims? If yes, the same would attract penal provisions under the Code, and as such the Applicant would be liable for the consequences.

Knocking the Doors of NCLT

From the above discussion, we understand that a situation as such would indeed put the IRP/ RP in a pickle. Another probable way out could be an application being filed by the IRP/ RP under section 60 (5) of the Code thereby praying for annulling the process or directing the original applicant to file an application under section 12A.

Further, in Swiss Ribbons (P) Ltd. v. Union of India (Supra)[1], the Hon’ble Supreme Court made it clear that “at any stage where the committee of creditors is not yet constituted, a party can approach the NCLT directly, which Tribunal may, in exercise of its inherent powers under Rule 11 of the NCLT Rules, 2016, allow or disallow an application for withdrawal or settlement…….”

Thus, on the strength of the aforesaid order and the power and jurisdiction in section 60 (5), the IRP/ RP may take necessary steps before the Hon’ble Bench.

Such entanglement would leave the IPR/ RP in the middle of the sea, so to say that he can neither continue the CIRP in absence of the CoC, nor proceed for withdrawal as per section 12A.

Corporate Debtor – a Defaulter or no

Another line of thought that arises in the given facts could be whether the Corporate Debtor can be construed as a ‘defaulter’. In the given case, since no claims are received after the initiation of CIRP, can it be assumed that the Corporate Debtor has not defaulted in the payment of dues of any other creditor except for that of the applicant. Based on this assumption, can it be said that the CD is not a defaulter?

The above straight jacket assumption would not hold good as it is important to note that another probable situation that could arise is that the default of other creditors is apparent from the books of accounts of the Corporate Debtor. In such cases, if no claims are received by the IRP, the IRP may, in furtherance to the mandatory public announcement, send a mail to the banks/ financial creditors, inviting claims from them so that at least the CoC can be constituted and the CIRP can proceed.

While the above situation is a rather odd one, it would indeed be an interesting situation to understand the possible course of action that the IPs could resort to, and the role of the Adjudicating Authorities in such cases.

RBI eases norms on loans and advances to directors and its related entities

Payal Agarwal, Executive, Vinod Kothari & Company ( payal@vinodkothari.com )

RBI has recently, vide its notification dated 23rd July, 2021 (hereinafter called the “Amendment Notification”), revised the regulatory restrictions on loans and advances given by banks to directors of other banks and the related entities. The Amendment Notification has brought changes under the Master Circular – Loans and Advances – Statutory and Other Restrictions (hereinafter called “Master Circular”). The Amendment Notification provides for increased limits in the loans and advances permissible to be given by banks to certain parties, thereby allowing the banks to take more prudent decisions in lending.

Statutory restrictions

Section 20 of the Banking Regulation Act, 1949 (hereinafter called the “BR Act”) puts complete prohibition on banks from entering into any commitment for granting of loan to or on behalf of any of its directors and specified other parties in which the director is interested. The Master Circular is in furtherance of the same and specifies restrictions and prohibitions as below –

*since the same does not fall within the meaning of loans and advances for this Master Circular

Loans and advances without prior approval of Board

The Master Circular further specifies some persons/ entities that can be given loans and advances upto a specified limit without the approval of Board, subject to disclosures in the Board’s Report of the bank. The Amendment Notification has enhanced the limits for some classes of persons specified.

| Serial No. | Category of person | Existing limits specified under Master Circular | Enhanced limits under Amendment Notification |

| 1 | Directors of other banks | Upto Rs. 25 lacs | Upto Rs. 5 crores for personal loans

(Please note that the enhancement is only in respect of personal loans and not otherwise) |

| 2 | Firm in which directors of other banks interested as partner/ guarantor | Upto Rs. 25 lacs | No change |

| 3 | Companies in which directors of other banks hold substantial interest/ is a director/ guarantor | Upto Rs. 25 lacs | No change |

| 4 | Relative(other than spouse) and minor/ dependent children of Chairman/ MD or other directors | Upto Rs. 25 lacs | Upto Rs. 5 crores |

| 5 | Relative(other than spouse) and minor/ dependent children of Chairman/ MD or other directors of other banks | Upto Rs. 25 lacs | Upto Rs. 5 crores |

| 6 | Firm in which such relatives (as specified in 4 or 5 above) are partners/ guarantors | Upto Rs. 25 lacs | Upto Rs. 5 crores |

| 7 | Companies in which relatives (as specified in 4 or 5 above) are interested as director or guarantor or holds substantial interest if he/she is a major shareholder | Upto Rs. 25 lacs | Upto Rs. 5 crores |

Need for such changes

The Master Circular was released on 1st July, 2015, which is more than 5 years from now. Considering the inflation over time, the limits have become kind of vague and ambiguous and required to be revisited. Moreover, the population all over the world is facing hard times due to the Covid-19 outbreak. At this point of time, such relaxation can be looked upon as the need of the hour.

Impact of the phrase ‘Substantial interest’ vs ‘Major shareholder’

The Master Circular uses the term “substantial interest” to generally regulate in the context of lending to companies in which a director is substantially interested.

The relevant places where the term has been used are as below –

| Completely prohibited | Allowed with conditions | |

| Section 20(1) of the BR Act – for companies in which directors are substantially interested | Para 2.2.1.2. of Master Circular – for companies in which directors of other banks are substantially interested – upto a limit of Rs. 25 lacs without prior approval of Board

|

|

| Para 2.1.2.2. of Master Circular – for companies in which directors are substantially interested | Para 2.2.1.4. of Master Circular – for the companies in which the relatives of directors of any bank are substantially interested – upto Rs. 25 lacs without prior approval of Board | After amendment, the para stands modified as – for the companies in which the relatives of directors of any bank are major shareholders – upto Rs. 5 crores without prior approval of Board |

While the Amendment Notification itself provides for the meaning of “major shareholder”, the meaning of “substantial interest” for the purposes of the Master Circular has to be taken from Section 5(ne) of the BR Act which reads as follows –

- in relation to a company, means the holding of a beneficial interest by an individual or his spouse or minor child, whether singly or taken together, in the shares thereof, the amount paid up on which exceeds five lakhs of rupees or ten percent of the paid-up capital of the company, whichever is less;

- in relation to a firm, means the beneficial interest held therein by an individual or his spouse or minor child, whether singly or taken together, which represents more than ten per cent of the total capital subscribed by all the partners of the said firm;

The above definition provides for a maximum limit of shareholding as Rs. 5 lacs, exceeding which a company falls into the list of a company in which director is substantially interested. The net effect is that a lot of companies fall into the radar of this provision and therefore, ineligible to take loans or advances from banks.

However, the Amendment Notification provides an explanation to the meaning of “major shareholder” as –

“The term “major shareholder” shall mean a person holding 10% or more of the paid-up share capital or five crore rupees in paid-up shares, whichever is less.”

This eases the strict limits because of which several companies may fall outside the periphery of the aforesaid restriction. Having observed the meaning of both the terms it is clear that while ‘substantial interest’ lays down strict limits and therefore, covers several companies under the prohibition list, the term ‘major shareholder’ eases the limit and makes several companies eligible to receive loans and advances from the bank subject to requisite approvals thereby setting a more realistic criteria.

The BR Act was enacted about half a century ago when the amount of Rs. 5 lacs would have been substantial, but not at the present length of time. Keeping this in mind, while RBI has substituted the requirement of “substantial interest” to “major shareholder” in one of the clauses, the other clauses and the principal Act are still required to comply with the “substantial interest” criteria, thereby, keeping a lot of companies into the ambit of restricted/ prohibited class of companies in the matter of loans and advances from banks.

Other petty amendments

Deeming interest of relative –

The Amendment Notification has the effect of inserting a new proviso to the extant Master Circular which specifies as below –

“Provided that a relative of a director shall also be deemed to be interested in a company, being the subsidiary or holding company, if he/she is a major shareholder or is in control of the respective holding or subsidiary company.”

This has the effect of including both holding and subsidiary company as well within the meaning of company by providing that a major shareholder of holding company is deemed to be interested in subsidiary company and vice versa.

Explanations to new terms –

The Amendment Notification allows the banks to lend upto Rs. 5 crores to directors of other banks provided the same is taken as personal loans. The meaning of “personal loans” has to be taken from the RBI circular on harmonisation of banking statistics which provides the meaning of personal loans as below –

Personal loans refers to loans given to individuals and consist of (a) consumer credit, (b) education loan, (c) loans given for creation/ enhancement of immovable assets (e.g., housing, etc.), and (d) loans given for investment in financial assets (shares, debentures, etc.).

Other terms used in the Amendment Notification such as “major shareholder” and “control” has also been defined. The meaning of “major shareholder” has already been discussed in the earlier part of this article. The meaning of “control” has been aligned with that under the Companies Act, 2013.

Concluding remarks

Overall, the Amendment Circular is a welcoming move by the financial market regulator. However, as pointed out in this article, several monetary limits under the BR Act have become completely incohesive and therefore, needs revision in the light of the current situation.

Home Buyers under IBC & Case Studies

Ever since the Jaypee and Amrapali cases, home buyers have been under the scanner. From orders of the Hon’ble Supreme Court to multiple amendments in the Insolvency and Bankruptcy Code, measures have been taken to protect the interest of the home buyers. While earlier, the home buyers were treated as ‘other creditors’, that is, neither operational nor financial, with the landmark ruling in Chitra Sharma v. Union of India, there status as financial creditors was established – the same also found place in the Code by way of amendments in section 7 of the Code.

In this presentation, we discuss the provisions w.r.t. Home Buyers under the Code and a detailed case study of the Amrapali Case and Jaypee Infratech Case.

A Regulatory Affair: Fair Value Discovery in Preferential Share Issues

Payal Agarwal, Vinod Kothari and Company ( payal@vinodkothari.com )

The recent cases of intervention by the stock market regulator and stock exchanges in preferential allotment of listed companies have brought to fore an important but fundamental point. That is, with a price band fixed under the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘ICDR Regulations’), and considering th e liquidity in listed (and frequently traded) shares, whether there is a need for an independent valuation report, has become a question of great interest. Since the issue is currently under litigation will want to say that it will be interesting to see the evolution of jurisprudence on this important issue. While the issue is of relevance to minority shareholders, but it also touches a key issue in valuation as to whether there is a fair value beyond the quoted value of a company whose shares are not infrequently traded.

e liquidity in listed (and frequently traded) shares, whether there is a need for an independent valuation report, has become a question of great interest. Since the issue is currently under litigation will want to say that it will be interesting to see the evolution of jurisprudence on this important issue. While the issue is of relevance to minority shareholders, but it also touches a key issue in valuation as to whether there is a fair value beyond the quoted value of a company whose shares are not infrequently traded.

Further, there might be scenario, where a preferential allotment triggers an open offer under SEBI (Substantial Acquisition of Shares and Disclosure Requirements) Regulations, 2011 (“SAST Regulations”). The SAST Regulations provides formula for determining offer price, which establish a clear nexus between the price of shares offered under preferential allotment and price of shares under open offer as per SAST Regulations. Given that the pricing of open offer is influenced by the pricing under preferential allotment, should the price under the ICDR Regulations be accepted or fair valuation of shares should be sought in order to ensure fair compensation to shareholders?

At this stage of discussion, it becomes important to look into the relevant provisions and the meaning of “fair value” and understand how fair it is to have a preferential allotment without ascertainment of such fair value by an independent valuer.

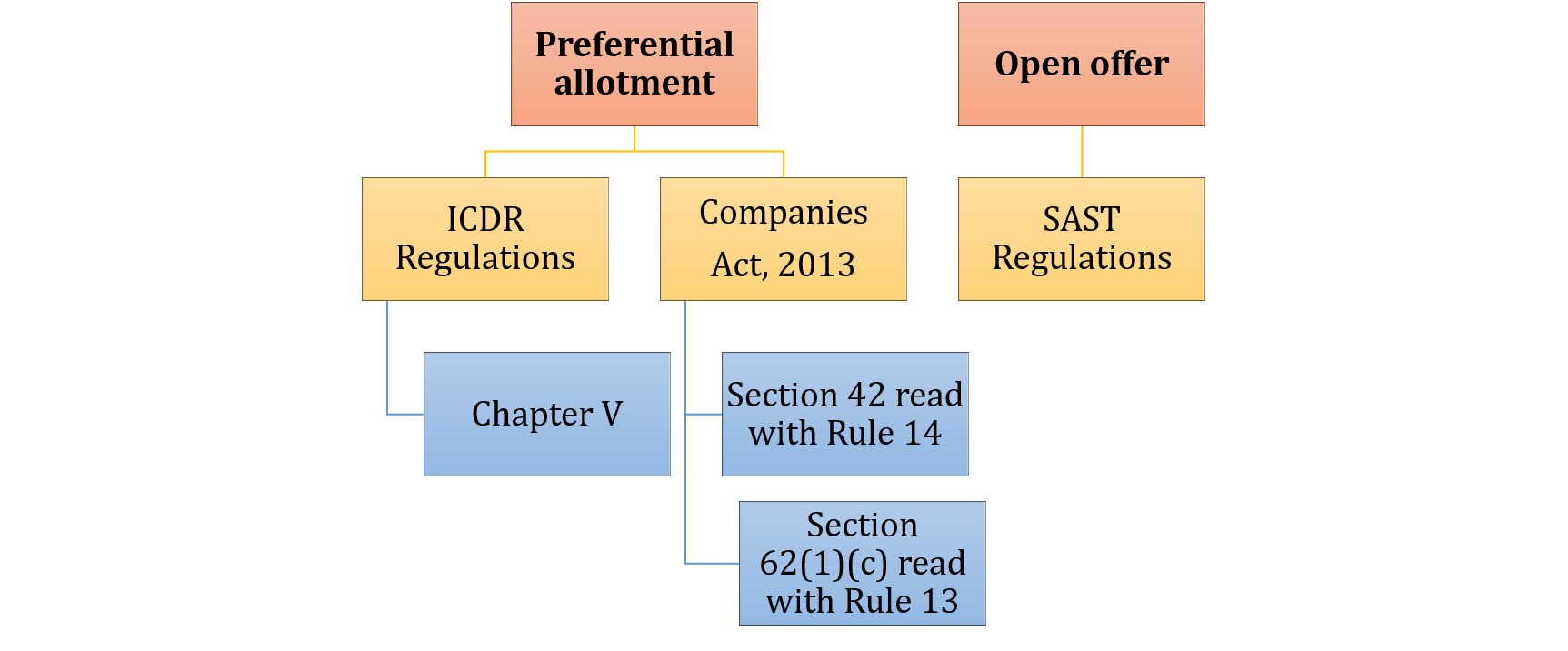

Regulatory provisions with respect to preferential allotment

Preferential allotment in listed companies are governed by the following provisions –

- Section 42 of the Companies Act, 2013 [“Companies Act”], read with Rule 14 of Companies (Prospectus and Allotment of Securities) Rules, 2014

- Section 62(1)(c) of the Companies Act. read with Rule 13 of Companies (Share Capital and Debentures) Rules, 2014

- Chapter V of ICDR (Regulation 164)

Preferential offers under section 62(1)(c) can be made to any person, if so authorised by a special resolution passed in general meeting if the price of such shares is determined by way of a valuation report of a registered valuer. However, if one goes through allied Rule 13 of SCD Rules, it becomes clear that the companies whose shares are listed on a stock exchange are not required to obtain a valuation report from a registered valuer. The said rules clearly bring out a distinction between preferential offers made by a listed company versus those made by unlisted companies. Sub-rule (2) specifically states that for companies whose shares are listed on a recognised stock exchange, the requirements under the relevant SEBI regulations (ICDR Regulations) will apply, while the unlisted companies will be governed by the provisions of the Companies Act; and sub-rule (3) states that the price under the preferential allotment shall not be less than the price determined on the basis of valuation report of registered valuer. Hence, it becomes clear that in case of a listed company, as per section 62 and rule 13, there is no requirement of a valuation report, per se. Instead, the legislature has left it to be regulated by SEBI regulations. Therefore, one will have to look for what ICDR says.

Reg. 164 of ICDR lays the floor limit of the price, which is to be calculated as the higher of average of weekly high and low of volume weighted average price of related equity shares quoted on a recognised stock exchange for –

- 26 weeks preceding the relevant date

- 2 weeks preceding the relevant date

The Regulation does not call for an independent valuation report. This must be read in contradistinction to regulation 165, which deals with pricing of infrequently traded shares. Reg. 165 rather specifically requires an independent valuation.

Requirement of independent valuation under regulatory provisions

The above clearly demonstrates that the regulations have consciously exempted listed entities from seeking an independent valuation where listed shares are frequently traded. The regulations, in fact, draw a timeframe to extract weighted averages of the market prices to ensure that the fluctuations in prices, if any, are ironed out and the resultant price is the even price at which the market has transacted during that period. This, admittedly and reasonably too, is based on the assumption that ‘market’ is the best reflection of a fair price which a willing seller and a willing investor are ready to deal in. This view can also be substantiated with similar stipulations in other laws and valuation standards.

Meaning of fair valuation under various applicable laws

Meaning of fair value under applicable accounting standards –

Meaning of fair value under applicable accounting standards –

Ind AS 113 deals with the fair valuation of equity shares. This Ind AS defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, and thus considers fair value to be “a market based measurement and not an entity specific measurement.”

Clause 18 of the Ind AS 113 provides, “If there is a principal market for the asset or liability, the fair value measurement shall represent the price in that market.”

Meaning of fair value under the Income Tax Rules

Rule 11UA (1)(c) of the Income Tax Rules provides for the fair value of shares listed in a stock exchange.

It renders the transaction value of such shares to be the fair value in case the transaction has been done through stock exchange. Otherwise, the fair market value of such shares are taken to be –

“(a)the lowest price of such shares and securities quoted on any recognized stock exchange on the valuation date, and

(b)the lowest price of such shares and securities on any recognized stock exchange on a date immediately preceding the valuation date when such shares and securities were traded on such stock exchange, in cases where on the valuation date there is no trading in such shares and securities on any recognized stock exchange”

Meaning of fair value under the Valuation Standards

Rule 18 of the Companies (Registered Valuers and Valuation) Rules, 2017 requires the registered valuer to follow such valuation standards as prescribed by the Central Government. For valuation with effect from 01st July, 2018, all registered valuers are mandatorily required to apply the ICAI Valuation Standards in their valuation assignments for the purposes of the Companies Act, 2013.

The definition of ‘fair value’ under ICAI Valuation Standard (101) is the same as that in IndAS 113, that is, fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the valuation date. IVS 101 further states that fair value assumes that the price is negotiated in a free market. The ICAI Valuation Standards recognises three approaches for valuation, being – market approach, income approach, and cost approach.

Where the assets to be valued are traded in active market, the market approach is followed for valuation purposes.

Paragraphs 18-20 gives guidance over the valuation as follows –

“18. A valuer shall consider the traded price observed over a reasonable period while valuing assets which are traded in the active market.

- A valuer shall also consider the market where the trading volume of asset is the highest when such asset is traded in more than one active market.

- A valuer shall use average price of the asset over a reasonable period. The valuer should consider using weighted average or volume weighted average to reduce the impact of volatility or any one time event in the asset.”

The stipulations as above clearly reflect that for quoted shares, fair valuation is based on quoted prices only. Given that IVS too refers to ‘traded prices’, a registered valuer would rely on such traded prices to arrive at a fair value. It may be reiterated that ICDR uses a ‘range’ of time so as to spread out the fluctuations in prices, which has been similarly captured in the IVS.

One may argue that the price of a company’s shares can be tampered with, by the company as per its whims and wishes. However, for a listed company, whose every information is readily available on public domain, does such an argument hold good? In view of the strict regulatory surveillance constantly placed by SEBI and stock exchanges on listed companies, this does not seem to be a possible scenario.

Valuation in respect of infrequently traded shares

The aforesaid logic and arguments may not hold good in case of shares that are infrequently traded or are unlisted. As indicated above, the applicable rules/regulations and standards prescribe a different methodology to arrive at fair values of such shares. For instance, regulation 165 of ICDR requires the minimum price in case of infrequently traded shares to be determined on the basis of valuation as per applicable parameters. Also, the SAST Regulations requires the offer price in case of infrequently traded shares to be determined by way of valuation taking into account various valuation parameters such as comparable trading multiples, book value and such others.

To reiterate, such distinction made out between frequently traded and infrequently traded shares clearly buttresses the views here.

Conclusion

The chances of a listed company acquiring a fair deal without falling into the formalities of fair valuation does not seem to be a scarce event. Listed companies are well governed under the provisions of ICDR Regulations as regards pricing of shares under preferential allotment. To ensure shareholder protection, ICDR already prescribes a minimum threshold based on average quoted prices. The prices depend on the market price of related equity shares quoted and traded on stock exchanges. Further, fair value of equity shares depend on market value of such shares and there does not seem to be chances of much disparity among the price under ICDR versus that as determined by way of fair valuation.

Proxy advisors and their role in corporate decision making on questions of law

Sharon Pinto, Manager, corplaw@vinodkothari.com

Concept of proxy advisors

Proxy advisors are research based entities that formulate recommendations on the decisions of companies which require shareholder approval. SEBI (Research Analysts) Regulations, 2014 (‘SEBI Regulations’), defines proxy advisors “as any person who provides advice, through any means, to institutional investor or shareholder of a company, in relation to exercise of their rights in the company including recommendations on public offer or voting recommendation on agenda items”. Thus, these advisory firms guide shareholders to make sound investment decisions and exercise their voting rights effectively. Matters that require shareholder approval under the Companies Act, 2013, are of significant importance and include decisions pertaining to appointment of directors (including managing director, whole-time directors, independent directors), manager, approval of their remuneration, alteration of Articles or Memorandum of Association of the company, etc. The clientele of the proxy advisory firms includes institutional investors, who are usually not privy to the affairs of the company. Thus, they may rely on the recommendations issued by the said entities. As in case of certain companies the shareholding/voting rights of such investors may be considerably large, the recommendations of a proxy advisory firm may substantially affect the decision-making by the investor, and in turn, the affairs of the company.

As per Regulation 2 (1) (m) of SEBI (Investment Advisors) Regulations, 2013, ‘investment advisor’ means a person who is engaged in the business of providing investment advice for a consideration. However, a proxy advisor is into recommending voting decisions to shareholders, and are not into recommending whether an investor or a potential investor should or should not make/keep an investment.

Investment advisors are entities that specifically provide financial advice. They undertake research in order to provide advice relating to investment decisions of their clients, separating them from proxy advisors, who provide voting recommendations on agenda items, which may also include approval of public offer by the shareholders. Thus, the role of proxy advisors does not entail provision of financial advice.

In this article, the author deliberates on the role of proxy advisors and the issues concerning their functioning, the enforceability of the recommendations, while perusing the position of applicable laws in India as well as in the global context.

Effect of proxy advisor recommendation on corporate decisions

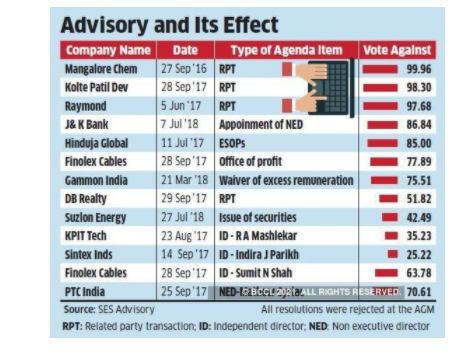

The role of proxy advisors is of a benign nature. They perform the function of educating investors of the right corporate governance practices on the basis of the research undertaken by them. Thus, they may act as catalysts in strengthening corporate governance. However, the downside to the process is the possibility of concentration of power with the proxy advisors and lack of regulatory overview or safeguards w.r.t. their opinions. Since the guidelines are based on best governance practices, they may go beyond the provisions of law. Further, the recommendations and guidelines thus issued are not subject to regulatory overview or approval. They are solely the views of the advisory entities and may thus differ on the grounds of interpretation or factual information. Thus, the said recommendations and guidelines must be used as a tool for further analysis by the investor and thereafter making independent decisions and not as views of the regulator, on account of the proxy advisors being licensed market intermediaries. The below figure shows an analysis of the effect of negative voting recommendations of the proxy advisor on the resolutions pertaining to related party transactions, appointment of non-executive directors, independent directors and other significant corporate decisions:

The current provisions applicable to proxy advisory entities in India do not prescribe for prior interaction of the firms with the company. While the same may act as a safeguard for the freedom of proxy advisory entities to express their opinions, the recommendations of the advisory entities may lack the consideration of necessary facts or information in order to give a comprehensive picture of the proposed decision of the company.

Concerns stemming from voting guidelines and recommendations of proxy advisors and existing regulatory framework

As the regulatory framework governing proxy advisors is still evolving, certain issues relating to the functioning of the proxy advisors and the guidelines and recommendations issued by them require further regulatory oversight. The existing regulatory framework and safeguards in place have been discussed below with respect to the said concerns.

India

Proxy advisory firms operating in India are required to obtain a license under the afore-mentioned SEBI Regulations. They are also required to mandatorily adopt a code of conduct as prescribed under the SEBI Regulations. The SEBI Regulations have set forth provisions relating to registration, eligibility criteria, management of conflict of interest, adoption of code of conduct among other matters.

- Conflict of interest

Conflict of interest is a major concern in case of proxy advisory firms providing other services like consultancy services to the company in addition to being advisors to its investors. Thus, it may give rise to biased opinions which are reflected in the recommendations of the advisory entity, resulting in negative impact on the shareholder interest. Chapter III of the SEBI Regulations deals with management of conflict of interest and disclosure requirements which mutatis mutandis applies to proxy advisors.

As per Regulation 15 (1) of SEBI Regulations, the entities are required to maintain internal policies and procedures governing the dealing and trading by any research analyst for addressing actual or potential conflict of interest arising from such dealings or trading of securities of the subject company. The said Regulations further prescribe restrictions on the dealings by employees of the advisory firms. Regulation 17 provides for the conditions on the compensation received by research analysts, wherein the compensation is required to be reviewed by the board of the research entity and is to be independent of the brokerage services division. Further, the SEBI Regulations prescribe for restriction on publication and distribution of reports of a subject company in which the research analyst has acted as a manager or co-manager.

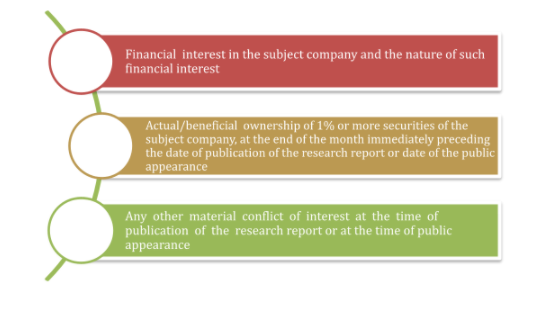

In addition to other disclosures, following w.r.t. whether the research analyst or research entity or his associate or his relative has any, will form part of the research report:

As per SEBI procedural guidelines for proxy advisors issued on August 3, 2020, proxy advisors are required to disclose conflict of interest on every specific document where they are giving their advice. Further, the disclosures should especially address possible areas of potential conflict and the safeguards that have been put in place to mitigate possible conflicts of interest. They are also required to establish clear procedures to disclose, manage and/or mitigate any potential conflicts of interest resulting from other business activities including consulting services, if any, undertaken by them and disclose the same to clients.

- Material misstatements and factual errors

Proxy advisors are required to additionally disclose in their reports the extent of research involved in a particular recommendation and the extent and/or effectiveness of its controls and procedures in ensuring the accuracy of issuer data in accordance with Regulation 23 of the SEBI Regulations. Further, the above-mentioned procedural guidelines issued by SEBI state that proxy advisors shall ensure that the recommendation policies are reviewed at least once annually. They shall further disclose the methodologies and processes followed in the development of their research and corresponding recommendations to their clients.

Regulation 20 of the SEBI Regulations, has prescribed the following with regard to contents of the Report:

- Research analyst or research entity shall take steps to ensure that facts in its research reports are based on reliable information and shall define the terms used in making recommendations, and these terms shall be consistently used.

- Research analyst or research entity that employs a rating system must clearly define the meaning of each such rating including the time horizon and benchmarks on which a rating is based.

- If a research report contains either a rating or price target for subject company’s securities and the research analyst or research entity has assigned a rating or price target to the securities for at least one year, such research report shall also provide the graph of daily closing price of such securities for the period assigned or for a three-year period, whichever is shorter.

- Interaction with the subject company

Regulation 23 of the SEBI Regulations, stipulates a proxy advisor to disclose the policies and procedures for interacting with issuers, informing issuers about the recommendation and review of recommendations. The afore-mentioned SEBI procedural guidelines for proxy advisors state that the proxy advisor shall have a stated process to communicate with its clients and the company. Further, proxy advisors shall share their report with their clients and the company at the same time. The said ‘sharing policy’ is required to be disclosed by proxy advisors on their website. Timeline to receive comments from company may be defined by proxy advisors and all comments/clarifications received from the company, within the said timeline, shall be included as an addendum to the report. If the company has a different viewpoint on the recommendations stated in the report of the proxy advisors, then proxy advisors, after taking into account the said viewpoint, may either revise the recommendation in the addendum report or issue an addendum to the report with its remarks, as considered appropriate.

- Difference of opinion

The views of proxy advisors as discussed herein are solely based on their research and interpretation not subject to the approval of any regulator. Further, the benchmarks set by the entities are based on highest corporate governance principles, hence they may surpass the requirement of law.

The procedural guidelines issued by SEBI state that they shall clearly disclose in their recommendations the legal requirement vis-a-vis higher standard they are suggesting if any, and the rationale behind the recommendation of higher standards.

The Report of the Working Group dated July 29, 2019, formulated by SEBI on issues concerning proxy advisors has proposed for proxy advisors to send an unedited response of the company to all its subscribers. In case a company is not satisfied with the response, it may write again to proxy advisors and in case the response is still not acceptable, the Company concerned may approach SEBI under the SEBI Regulations seeking SEBI’s intervention. However, mere differences based on opinion, which are backed with authentic public data and analysis, cannot be the basis of any complaint or litigation. Litigation should not be initiated merely because an opinion is not favourable to the management of a company, especially if opportunity had been given by proxy advisors to the company and the same has been duly addressed. Thus, an objection may only be raised by companies in case of abuse of power by the proxy advisors by violating the Code of Conduct as mandatorily prescribed under SEBI Regulations. A mere case of difference of opinion basis different interpretations, which is not on account of factual misstatement or lack of material facts, cannot be the basis of contention.

United States of America

Under the Securities Exchange Act of 1934 (‘Exchange Act’), Securities and Exchange Commission (‘SEC’) regulates the proxy solicitation process for publicly traded equity securities. SEC also regulates the activities of proxy advisory firms that are registered with SEC as investment advisers under the Investment Advisers Act of 1940 (Advisers Act). As per the SEC’s Interpretation and Guidance on Applicability of Proxy Rules on Proxy Voting Advice, it has stated that proxy voting advice should be considered a solicitation, subject to the federal proxy rules because it is “a communication to security holders under circumstances reasonably calculated to result in the procurement, withholding or revocation of a proxy.”

- Conflict of interest

SEC in its Guidance on Investment Advisor’s use of Proxy Advisors states that an investment adviser’s decision regarding whether to retain a proxy advisory firm should also include a reasonable review of the proxy advisory firm’s policies and procedures regarding how it identifies and addresses conflicts of interest. Since proxy voting advice has been considered as solicitation, relevant federal proxy rules shall apply. Solicitations that are exempt from the federal proxy rules’ information and filing requirements remain subject to Rule 14a-9 of General Rules and Regulations of Exchange Act. Accordingly, the provider of the proxy voting advice should consider whether, depending on the particular statement, it may need to disclose about material conflicts of interest that arise in connection with providing the proxy voting advice in reasonably sufficient detail so that the client can assess the relevance of those conflicts in order to avoid a potential violation of the aforesaid rule.

SEC has proposed amendments to regulate proxy advisors which shall be mandatory from December 1, 2021. As per the said amendments, any person providing proxy voting advice within the scope of proposed rules, who wishes to utilize the exemption in either Rule 14a–2(b)(1) or (b)(3) must include in their voting advice (or in any electronic medium used to deliver the advice) prominent disclosure of:

- Any information regarding an interest, transaction, or relationship of the proxy voting advice business (or its affiliates) that is material to assessing the objectivity of the proxy voting advice in light of the circumstances of the particular interest, transaction, or relationship; and

- Any policies and procedures used to identify, as well as the steps taken to address, any such material conflicts of interest arising from such interest, transaction, or relationship

- Material misstatements and factual errors

Rule 14a–9 prohibits any proxy solicitation from containing false or misleading statements with respect to any material fact at the time and in light of the circumstances under which the statements are made. In addition, such solicitation must not omit to state any material fact necessary in order to make the statements therein not false or misleading. As per the SEC amendments mentioned above, entities providing proxy voting advice, in case of failure to disclose material information regarding proxy voting advice, ‘‘such as the proxy voting advice business’s methodology, sources of information, or conflicts of interest’’ could, depending upon particular facts and circumstances, be misleading within the meaning of the rule. It has been further stated that, the amendment does not make mere differences of opinion actionable under Rule 14a–9.

- Interaction with the subject company

SEC amendments in Rule 14a of the Exchange Act, 1934, provide certain exemptions with respect to filing requirements of the proxy rules subject to the condition that registrants that are the subject of proxy voting advice have such advice made available to them at or prior to the time when such advice is disseminated to the proxy voting advice business’s clients.

The amendments also provide for safe harbour rules specifying policies and procedures of the proxy advisors may include conditions requiring registrants to –

- file their definitive proxy statement at least 40 calendar days before the security holder meeting

- expressly acknowledge that they will only use the proxy voting advice for their internal purposes and/or in connection with the solicitation and will not publish or otherwise share the proxy voting advice except with the registrant’s employees or advisers.

- Difference of opinion

While Rule 14a-9 of Exchange Act, 1934 states that no solicitation subject to this regulation shall be made by means of any proxy statement or other communication, written or oral, containing any statement which, at the time and in the light of the circumstances under which it is made, is false or misleading with respect to any material fact, the same is not applicable in case of difference of opinion. However, since as per the proposed SEC amendments, entities will be required to make their proxy voting advice available to the registrants at or prior to the time when such advice is disseminated to the proxy voting advice business’s clients, the same shall provide a fair opportunity for representation to the registrant companies.

United Kingdom

As per the Directive (EU) 2017/828, a proxy advisor is a legal person that analyses, on a professional and commercial basis, the corporate disclosure and, where relevant, other information of listed companies with a view to informing investors’ voting decisions by providing research, advice or voting recommendations that relate to the exercise of voting rights. The Proxy Advisors (Shareholders’ Rights) Regulations 2019, came into force on 10th June, 2019. The Proxy Advisors (Shareholders’ Rights) Regulations in part implement the revised Shareholders Rights Directive (Shareholder Rights Directive II).

- Conflict of interest

The Proxy Advisors (Shareholders’ Rights) Regulations, 2019, under Regulation 5, state that the proxy advisor must take all appropriate steps to ensure that it identifies any actual or potential conflict of interest or any business relationship that may influence the advisor in the preparation of research, advice or voting recommendations. Further, such a conflict of interest or business relationship is required to be identified without delay after the time at which it arises. In case of identification of an actual or potential conflict of interest, the proxy advisor must disclose the fact to its clients together with particulars of the conflict of interest or business relationship concerned, in addition to a statement of the action it has undertaken to eliminate, mitigate or manage the conflict of interest or business relationship concerned.

- Material misstatements and factual errors

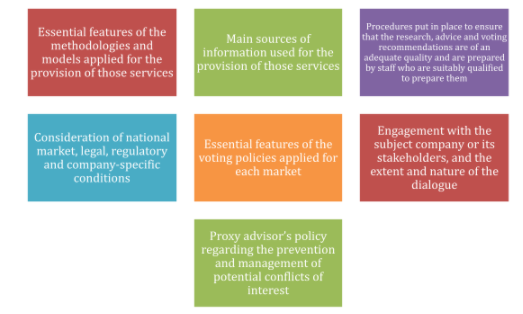

Regulation 4 of the Proxy Advisors (Shareholders’ Rights) Regulations, 2019, prescribes minimum information to be disclosed relating to preparation of research, advice and voting recommendations, as given below:

Similar to the legislation in India, the policies and procedures are required to be reviewed at intervals of no more than twelve months beginning with the date on which it was last updated.

- Difference of opinion

Adoption of Code of Conduct is not mandatory under the Proxy Advisors (Shareholders’ Rights), 2019, provided the proxy advisors provide a clear and reasoned explanation of reasons for not doing so. The provisions prescribe a person may submit a complaint to the Financial Conduct Authority (FCA), in case of contravention of any requirement. Further, the Code of Conduct is required to be updated at an interval of not more than twelve months.

Australia

Under the Australian regime, only the proxy advisors providing financial services are required to obtain a license referred to as Australian Financial Services (AFS) license, under the Australian Corporations Act, 2001. Thus, the obligations set forth under the said Act are not applicable to proxy advisors that undertake research and provide voting recommendations.

- Conflict of interest

In case of proxy advisory firms providing financial services pursuant to Australian financial services (AFS) license, one of the obligations under Section 912A of the Corporations Act stipulates that the proxy advisors are to have adequate arrangements in place for the management of conflicts of interest that may arise wholly, or partially, in relation to activities undertaken in the provision of financial services.

- Interaction with the subject company

On the same lines as the amendments proposed by SEC, in the consultation paper issued by the Treasury of Australian Government in April 2021, it is proposed that proxy advisers will be required to provide their report containing the research and voting recommendations for resolutions at a company’s meeting, to the relevant company before distributing the final report to subscribing investors. It has also been proposed that the advisory entities will be required to notify their clients on how to access the company’s response to the report, by providing a website link or instructions on how to access the response elsewhere. Thus, at present there is no requirement of prior engagement with the subject company.

- Difference of opinion

Section 912D of the Corporations Act of Australia states that a licensed financial advisor is obligated to lodge a written report with the ASIC in case of a breach of the obligation prescribed under the Act, as soon as practicable but not later than 10 business days after becoming aware of the breach. However, as proxy advisory entities are currently not required to obtain a license under the Corporations Act, the said provisions are not applicable to them.

ASIC in its review of proxy advisor engagement practices dated June 2018, recommended that if a subject company discovers a matter that is materially false or misleading in a proxy adviser report, the company should:

- notify the proxy adviser of the matter promptly and seek a correction

- consider whether it would be appropriate to respond to the matter by way of an ASX announcement or other communication to investors.

Closing thoughts with respect to tightening of norms relating to proxy advisors

Fair disclosure of information: Proxy advisory entities have garnered more attention in recent years. They have an increased influence over institutional investors and thus have the power to affect the functioning of companies on the basis of the voting recommendations they provide. It is thus necessary that fair and complete disclosure relating to the facts and interpretation of the proxy advisor entity be stated. While certain advisory firms state a disclaimer in their reports, mentioning the fact that the views of the report are not approved by the regulatory authorities, but based on their own benchmarks, the same is not a requirement specified under the regulations governing the entities.

Regulatory oversight of adherence of code of conduct: While it is mandatory for the proxy advisory entities to adopt a code of conduct under the SEBI Regulations, there should be a regulatory oversight on the adherence of the said Code. Further, there is a requirement of placing a fiduciary responsibility on the proxy advisory entities as the guidelines and recommendations published by them are available in the public domain and may affect the opinions of the shareholders of the company. Therefore, the same is required to be unbiased and must state a fair representation of the facts involved. Further, it may be stipulated that, in cases where the proxy advisor is taking a view based on an interpretation of law, which might differ across market participants, the proxy advisor shall specifically state so, and advise the client to take an independent view.

Representation of the subject company: Currently, SEBI procedural guidelines require that the proxy advisors share the report with their clients and the subject company at the same time. However, as per the amendments proposed in the US and Australian regulatory framework, proxy advisors would be required to provide their report to the subject company prior to the issue of the same to its clients. The same may fill the gap arising out of incomplete or obsolete information. Hence, it may be more relevant if the draft report is shared with the subject company before the same is shared with the client/investors; such that a consolidated report, including the views and interpretations of the subject company, may be issued to the shareholders/clients. This would ensure – (i) a fair opportunity to the subject company to rebut the views/interpretations taken by the proxy advisor, (ii) that the shareholder’s views are not pre-conditioned by the sole views of proxy-advisors, as they do not get the views of the subject company at the first instance. As a matter of reasonable checks, the shareholders may be given the right to seek for the draft report shared by the proxy-advisor with the subject company.

Responsibility of institutional investors – The institutional investors should appropriately weigh on the views of the proxy advisors and the subject company, and ultimately make their own independent analysis of the facts in hand to decide on the issue.

Other articles on proxy advisors:

- Dance of Corporate Democracy: The rise of proxy advisors

- SEBI prescribes stricter regimes for Proxy Advisors; Issues procedural guidelines to be followed in addition to Code of Conduct

- SEBI revisits regulatory framework for Proxy Advisors

- Scope of Proxy Advisors to issue general voting guidelines

https://vinodkothari.com/2021/06/scope-of-proxy-advisors-to-issue-general-voting-guidelines/